Macroeconomic Analysis: Volkswagen Company in Germany and China

VerifiedAdded on 2023/06/04

|20

|4816

|212

Report

AI Summary

This report provides a comprehensive analysis of Volkswagen's operations in Germany and China, examining the company's business overview, market structures (oligopoly in both countries), and macroeconomic environments. The report compares key macroeconomic indicators such as GDP growth, inflation, unemployment rates, and government balances, and assesses their impact on Volkswagen's economic activities. It delves into the monetary and fiscal policies of both countries, analyzing how these policies influence the company's performance. The report also briefly touches on foreign trade policy instruments and their implications. The findings highlight the contrasting economic landscapes of Germany and China, and their respective influences on Volkswagen's global strategy and profitability. The report concludes by offering insights into the challenges and opportunities that Volkswagen faces in these key markets.

Running Head: REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 1

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA

Student Name

Institution Affiliation

Facilitator

Course

Date

Table of Contents

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA

Student Name

Institution Affiliation

Facilitator

Course

Date

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 2

1.0 BUSINESS OVERVIEW..........................................................................................................4

2.0 PURPOSE OF THE REPORT...................................................................................................5

3.0 ANALYSIS OF THE MARKET STRUCTURE- GERMANY & CHINA..............................5

3.1 GERMANY...........................................................................................................................5

3.2 CHINA...................................................................................................................................7

4.0 MACROECONOMIC INDICATORS- GERMANY & CHINA..............................................8

5.0 ANALYSIS OF THE MONETARY AND FISCAL POLICY...............................................16

6.0 ANALYSIS OF FOREIGN TRADE POLICY INSTRUMENTS..........................................17

7.0 REFERENCES........................................................................................................................18

LIST OF FIGURES

1.0 BUSINESS OVERVIEW..........................................................................................................4

2.0 PURPOSE OF THE REPORT...................................................................................................5

3.0 ANALYSIS OF THE MARKET STRUCTURE- GERMANY & CHINA..............................5

3.1 GERMANY...........................................................................................................................5

3.2 CHINA...................................................................................................................................7

4.0 MACROECONOMIC INDICATORS- GERMANY & CHINA..............................................8

5.0 ANALYSIS OF THE MONETARY AND FISCAL POLICY...............................................16

6.0 ANALYSIS OF FOREIGN TRADE POLICY INSTRUMENTS..........................................17

7.0 REFERENCES........................................................................................................................18

LIST OF FIGURES

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 3

FIGURE 1.1: GDP GROWTH RATE, CHINA & GERMANY

FIGURE 1.2: GDP CONSTANT-PRICE, CHINA & GERMANY

FIGURE 1.3: INFLATION RATES, CHINA & GERMANY

FIGURE 1.4: UNEMPLOYMENT RATES, CHINA & GERMANY

FIGURE 1.5: GENERAL GOVERNMENT BALANCES, CHINA &GERMANY

FIGURE1.6: BALANCE OF PAYMENTS, CHINA & GERMANY

FIGURE 1.1: GDP GROWTH RATE, CHINA & GERMANY

FIGURE 1.2: GDP CONSTANT-PRICE, CHINA & GERMANY

FIGURE 1.3: INFLATION RATES, CHINA & GERMANY

FIGURE 1.4: UNEMPLOYMENT RATES, CHINA & GERMANY

FIGURE 1.5: GENERAL GOVERNMENT BALANCES, CHINA &GERMANY

FIGURE1.6: BALANCE OF PAYMENTS, CHINA & GERMANY

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 4

1.0 BUSINESS OVERVIEW

Volkswagen is a major automobile manufacturer in Germany which was founded by the

government of Germany in the year 1937 to facilitate massive production of low priced people’s

vehicles. The headquarters of this company is in Wolfsburg in Germany. Originally, the

company was operated by German Labour Front (Deutsche Arbeitsfront). Ferdinand Porsche, the

original designer of the Volkswagen cars had been hired in the year 1934 from Australia by the

German Labour Front and left in the year 1938 to a new factory in Lower Saxony state. The

1939 outbreak of World War II occurred before the company picking up fully and that saw it

repurposed for production of military equipment and vehicles. Its military involvement, however,

acted as a disadvantage to it by making it a target for Allied bombers and by the time war ended,

it had been left in a devastated condition (Wei, Zhao,Wang, Cheng & Zhao, 2016). Later, it was

rebuilt by the British and mass production began in 1946. In 1949, the company control was then

transferred to West German government and Lower Saxony state. By that time, it had picked

because most of the passenger cars which were being produced within the country were

Volkswagens. Since the 1950s to today, the company production has been expanding rapidly

than any other automotive company in the country. This can be affirmed from its brands like

Audi and others like Porsche which have currently hit the market creating a lot of interest. Its

expansion has seen it establish branches in different countries like China as it will be seen

beneath (BoydUniversity, 2015).

History has recorded Volkswagen as the first German automobile company that entered

the Chinese market after opening policy and reforms were established. The company is recorded

to have entered the Chinese market through the joint venture of the two Chinese owned

enterprises, Changchun and Shanghai. The company has been considering doing well in China

1.0 BUSINESS OVERVIEW

Volkswagen is a major automobile manufacturer in Germany which was founded by the

government of Germany in the year 1937 to facilitate massive production of low priced people’s

vehicles. The headquarters of this company is in Wolfsburg in Germany. Originally, the

company was operated by German Labour Front (Deutsche Arbeitsfront). Ferdinand Porsche, the

original designer of the Volkswagen cars had been hired in the year 1934 from Australia by the

German Labour Front and left in the year 1938 to a new factory in Lower Saxony state. The

1939 outbreak of World War II occurred before the company picking up fully and that saw it

repurposed for production of military equipment and vehicles. Its military involvement, however,

acted as a disadvantage to it by making it a target for Allied bombers and by the time war ended,

it had been left in a devastated condition (Wei, Zhao,Wang, Cheng & Zhao, 2016). Later, it was

rebuilt by the British and mass production began in 1946. In 1949, the company control was then

transferred to West German government and Lower Saxony state. By that time, it had picked

because most of the passenger cars which were being produced within the country were

Volkswagens. Since the 1950s to today, the company production has been expanding rapidly

than any other automotive company in the country. This can be affirmed from its brands like

Audi and others like Porsche which have currently hit the market creating a lot of interest. Its

expansion has seen it establish branches in different countries like China as it will be seen

beneath (BoydUniversity, 2015).

History has recorded Volkswagen as the first German automobile company that entered

the Chinese market after opening policy and reforms were established. The company is recorded

to have entered the Chinese market through the joint venture of the two Chinese owned

enterprises, Changchun and Shanghai. The company has been considering doing well in China

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 5

since it entered the market. For instance, the sales volume of Volkswagen in China for the first

time exceeded those in Germany in 2011 (Li, 2018). During this year, its profit in China

accounted for 20% of its total profits worldwide. However, despite such an increase in sales

volume, the market share of Volkswagen Chinese car industry has declined from 40 percent to

17.7 percent between 2002 and 2018. The reason behind this decline in market share is the

entrance of other big international players like Toyota and Hyundai into the Chinese car market.

2.0 PURPOSE OF THE REPORT

This report will scrutinize the operations of Volkswagen Company in both its

headquarters at Germany and one of its main branches in China. The report will also make an

extra mile to examine the macroeconomic environments in the two countries, Germany & China

and determine how they might affect the company’s progress in the near future. Lastly, it will

also evaluate the current economic policies enacted within the context of the industrialization in

the two countries to back up the prediction of the company’s economic activities.

3.0 ANALYSIS OF THE MARKET STRUCTURE- GERMANY & CHINA

3.1 GERMANY

Germany automotive industry was inspired by British automotive industry in the 1860s

and following the development of four-stroke internal combustion engines by motor-car

pioneers Karl Benz and his colleague Nikolaus in 1870s, the modern cars have emerged. By the

year 1901, Germany automotive sector which comprised of two companies was producing

almost 900 cars per year. The existing automotive companies which belonged to Karl Benz and

Gottlieb Daimler merged in 1926 merged to and adopted the brand name Daimler-Benz and

since it entered the market. For instance, the sales volume of Volkswagen in China for the first

time exceeded those in Germany in 2011 (Li, 2018). During this year, its profit in China

accounted for 20% of its total profits worldwide. However, despite such an increase in sales

volume, the market share of Volkswagen Chinese car industry has declined from 40 percent to

17.7 percent between 2002 and 2018. The reason behind this decline in market share is the

entrance of other big international players like Toyota and Hyundai into the Chinese car market.

2.0 PURPOSE OF THE REPORT

This report will scrutinize the operations of Volkswagen Company in both its

headquarters at Germany and one of its main branches in China. The report will also make an

extra mile to examine the macroeconomic environments in the two countries, Germany & China

and determine how they might affect the company’s progress in the near future. Lastly, it will

also evaluate the current economic policies enacted within the context of the industrialization in

the two countries to back up the prediction of the company’s economic activities.

3.0 ANALYSIS OF THE MARKET STRUCTURE- GERMANY & CHINA

3.1 GERMANY

Germany automotive industry was inspired by British automotive industry in the 1860s

and following the development of four-stroke internal combustion engines by motor-car

pioneers Karl Benz and his colleague Nikolaus in 1870s, the modern cars have emerged. By the

year 1901, Germany automotive sector which comprised of two companies was producing

almost 900 cars per year. The existing automotive companies which belonged to Karl Benz and

Gottlieb Daimler merged in 1926 merged to and adopted the brand name Daimler-Benz and

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 6

started producing cars under the marque of Mercedes-Benz. BMW had also been founded in

1916 but had not started its auto production until 1928 (Hertrich & Mayrhofer, 2016). The

American economist Robert Brady has documented the process of industrial revolution in

Germany, and although his model applies to the automotive industry as well, the sector indicates

to be under poor conditions in later years under Weimar republic. The slow development of auto

industry in Germany exposed the market to major auto manufacturers of America like General

Motors who ended up taking over one of the German company, Opel in 1929, and Ford Motor

Company which has kept the successful German subordinate Ford-Werke since 1925.

The Germany Automotive sector has been making progress from one year to another and

is also expected to even witness a stronger growth rate in the near term future according to

economic predictions. The current trends, as well as the future predictions, are being driven by

the surging market conditions as well as the technological advancements. In regard to investment

opportunities and product sales, this sector is posing strong growth prospects for both domestic

companies as well as the international ones (Kundnani, 2015). Also, new market trends keep on

emerging in the country’s automotive sector and which is mainly driven by improving economic

conditions. The technological advancements coupled with the foray of new firms continue to

shape the new market dynamics.

Despite the milestones which have been made in this industry as well as the anticipated

changes, the automotive industry in Germany has remained under the domination of just a few

companies. Currently, the industry is dominated by five major companies and other seven

marques. These are Volkswagen AG (with its subsidiaries, Porsche & Audi), Adam Opel AG,

Ford-Werke GmbH, BMW AG and Daimler AG (Whittall, Martinez, Sánchez, Telljohann &

Mustchin, 2015). Considering the small number of companies operating in this industry, it comes

started producing cars under the marque of Mercedes-Benz. BMW had also been founded in

1916 but had not started its auto production until 1928 (Hertrich & Mayrhofer, 2016). The

American economist Robert Brady has documented the process of industrial revolution in

Germany, and although his model applies to the automotive industry as well, the sector indicates

to be under poor conditions in later years under Weimar republic. The slow development of auto

industry in Germany exposed the market to major auto manufacturers of America like General

Motors who ended up taking over one of the German company, Opel in 1929, and Ford Motor

Company which has kept the successful German subordinate Ford-Werke since 1925.

The Germany Automotive sector has been making progress from one year to another and

is also expected to even witness a stronger growth rate in the near term future according to

economic predictions. The current trends, as well as the future predictions, are being driven by

the surging market conditions as well as the technological advancements. In regard to investment

opportunities and product sales, this sector is posing strong growth prospects for both domestic

companies as well as the international ones (Kundnani, 2015). Also, new market trends keep on

emerging in the country’s automotive sector and which is mainly driven by improving economic

conditions. The technological advancements coupled with the foray of new firms continue to

shape the new market dynamics.

Despite the milestones which have been made in this industry as well as the anticipated

changes, the automotive industry in Germany has remained under the domination of just a few

companies. Currently, the industry is dominated by five major companies and other seven

marques. These are Volkswagen AG (with its subsidiaries, Porsche & Audi), Adam Opel AG,

Ford-Werke GmbH, BMW AG and Daimler AG (Whittall, Martinez, Sánchez, Telljohann &

Mustchin, 2015). Considering the small number of companies operating in this industry, it comes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 7

out without any reasonable doubt that this sector is under the Oligopoly type of market structure.

This is in consideration of the characteristics of this market structure: a large number of potential

buyers and few sellers, differentiated products and the presence of barriers to entry. A further

breakdown of this industry lands it to an impure oligopoly because the firms lack competition

and use product differentiation as the main source of market power (Goodwin, Harris, Nelson,

Roach & Torras, 2015).

3.2 CHINA

The history of China automobile industry has been traced back from the Soviet people;

the licensed auto designs which were founded in the 1950s by the USSR and which had small

volumes of between 100 and 200 thousand per year. The start of 1990 has seen this sector

develop very to exceed the production capacity of one million by the year 1992. By 2000, the

country was producing over two million vehicles per year. After its entry into the World Trade

Organization in 2001, the automobile sector of China’s economy has continued to accelerate

further (Feuerriegel & Gordon, 2018). Between the year 2002 and 2007, the sector grew by 21%,

or one million vehicles a year after the other. In 2009, the country produced 13.79 million

vehicles, of which 3.41 million were commercial vehicles and 8 million passenger cars, taking

the position which had been occupied States as the largest vehicle producer globally. In the

preceding year, both production and sells topped 18 million vehicles; 13.76 million being

passenger vehicles. In 2014, the total production hit a mark of 23.720 million, which was

approximately 26% of the world’s automotive production

The automobile industry in China has since then maintained its position as a ringleader,

exceeding the European Union or that of both Japan and US combined. Despite these interesting

out without any reasonable doubt that this sector is under the Oligopoly type of market structure.

This is in consideration of the characteristics of this market structure: a large number of potential

buyers and few sellers, differentiated products and the presence of barriers to entry. A further

breakdown of this industry lands it to an impure oligopoly because the firms lack competition

and use product differentiation as the main source of market power (Goodwin, Harris, Nelson,

Roach & Torras, 2015).

3.2 CHINA

The history of China automobile industry has been traced back from the Soviet people;

the licensed auto designs which were founded in the 1950s by the USSR and which had small

volumes of between 100 and 200 thousand per year. The start of 1990 has seen this sector

develop very to exceed the production capacity of one million by the year 1992. By 2000, the

country was producing over two million vehicles per year. After its entry into the World Trade

Organization in 2001, the automobile sector of China’s economy has continued to accelerate

further (Feuerriegel & Gordon, 2018). Between the year 2002 and 2007, the sector grew by 21%,

or one million vehicles a year after the other. In 2009, the country produced 13.79 million

vehicles, of which 3.41 million were commercial vehicles and 8 million passenger cars, taking

the position which had been occupied States as the largest vehicle producer globally. In the

preceding year, both production and sells topped 18 million vehicles; 13.76 million being

passenger vehicles. In 2014, the total production hit a mark of 23.720 million, which was

approximately 26% of the world’s automotive production

The automobile industry in China has since then maintained its position as a ringleader,

exceeding the European Union or that of both Japan and US combined. Despite these interesting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 8

facts about the sector in China, the industry is still controlled and dominated by just a few

companies. The traditional “Big four” manufactures still control the market. These are

Dongfeng, SAIC Motors, Chang’an and FAW. There are also other small manufacturers who are

in their initial steps of the establishment. Those include Brilliance, Beijing Automotive Group,

Geely, Jianghuai, Chery, BYD and Great Wall. In addition, there are several other multinational

manufacturers which have partnered with domestic manufacturers (Hadaś, 2015).

Based on the evidence from the number of manufactures in this industry, it is without any

reasonable doubt that the industry fits under the category of Oligopoly market structure. This is

in consideration of the characteristics of this market structure: a large number of potential buyers

and few sellers, differentiated products and the presence of barriers to entry. A further

breakdown of this industry lands it to an impure oligopoly because the firms lack competition

and use product differentiation as the main source of market power.

4.0 MACROECONOMIC INDICATORS- GERMANY & CHINA

facts about the sector in China, the industry is still controlled and dominated by just a few

companies. The traditional “Big four” manufactures still control the market. These are

Dongfeng, SAIC Motors, Chang’an and FAW. There are also other small manufacturers who are

in their initial steps of the establishment. Those include Brilliance, Beijing Automotive Group,

Geely, Jianghuai, Chery, BYD and Great Wall. In addition, there are several other multinational

manufacturers which have partnered with domestic manufacturers (Hadaś, 2015).

Based on the evidence from the number of manufactures in this industry, it is without any

reasonable doubt that the industry fits under the category of Oligopoly market structure. This is

in consideration of the characteristics of this market structure: a large number of potential buyers

and few sellers, differentiated products and the presence of barriers to entry. A further

breakdown of this industry lands it to an impure oligopoly because the firms lack competition

and use product differentiation as the main source of market power.

4.0 MACROECONOMIC INDICATORS- GERMANY & CHINA

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 9

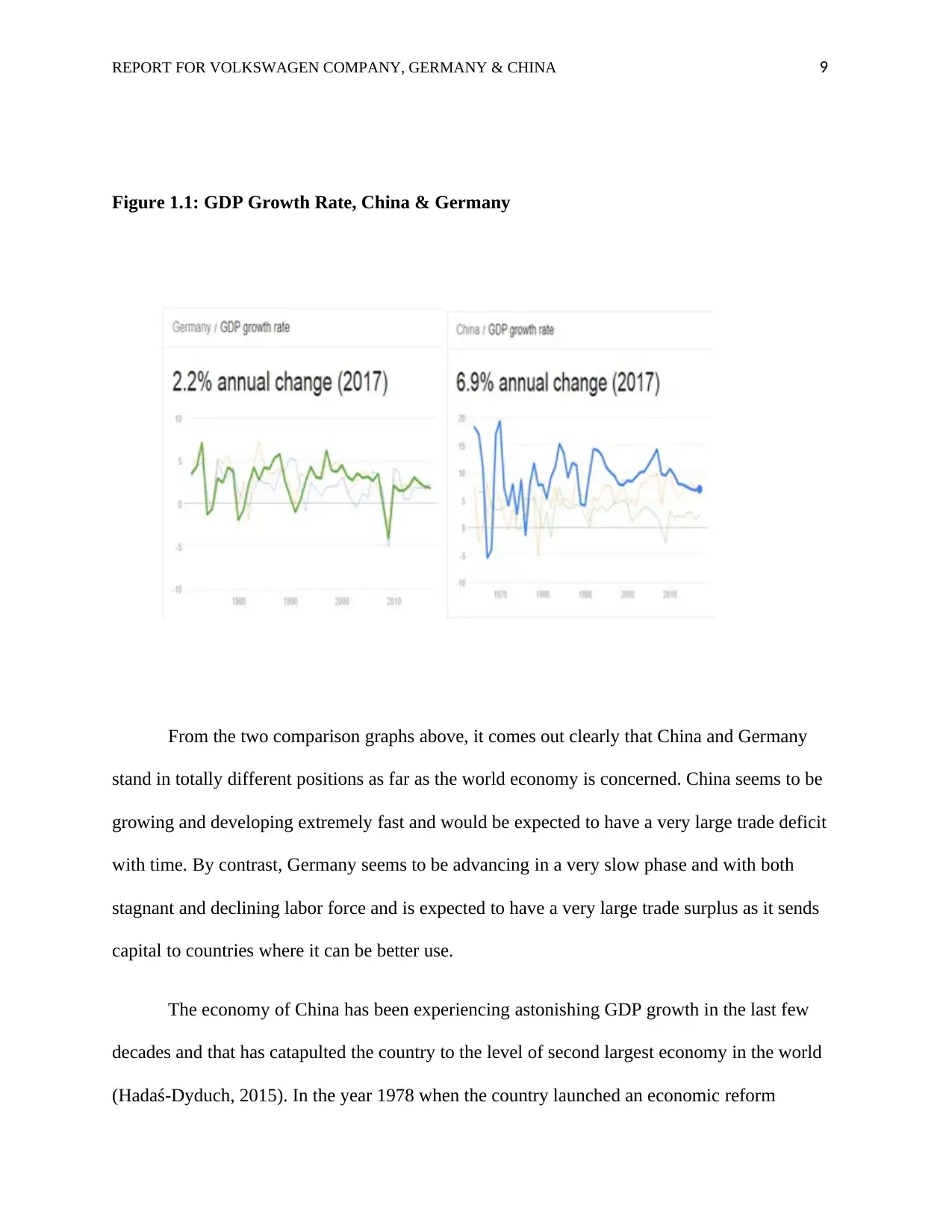

Figure 1.1: GDP Growth Rate, China & Germany

From the two comparison graphs above, it comes out clearly that China and Germany

stand in totally different positions as far as the world economy is concerned. China seems to be

growing and developing extremely fast and would be expected to have a very large trade deficit

with time. By contrast, Germany seems to be advancing in a very slow phase and with both

stagnant and declining labor force and is expected to have a very large trade surplus as it sends

capital to countries where it can be better use.

The economy of China has been experiencing astonishing GDP growth in the last few

decades and that has catapulted the country to the level of second largest economy in the world

(Hadaś-Dyduch, 2015). In the year 1978 when the country launched an economic reform

Figure 1.1: GDP Growth Rate, China & Germany

From the two comparison graphs above, it comes out clearly that China and Germany

stand in totally different positions as far as the world economy is concerned. China seems to be

growing and developing extremely fast and would be expected to have a very large trade deficit

with time. By contrast, Germany seems to be advancing in a very slow phase and with both

stagnant and declining labor force and is expected to have a very large trade surplus as it sends

capital to countries where it can be better use.

The economy of China has been experiencing astonishing GDP growth in the last few

decades and that has catapulted the country to the level of second largest economy in the world

(Hadaś-Dyduch, 2015). In the year 1978 when the country launched an economic reform

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 10

program, it was ranked ninth in the nominal gross domestic product (GDP) globally. 35 years

later it moved up to be the second after the US with a GDP of $9.2 trillion. It’s also due to the

reforms of 1978 that China has become the largest manufacturing hub globally, where the

secondary sector (which comprises construction and industry) made the largest GDP

contribution. China’s modernization has however propelled the tertiary sector to bypass the

secondary sector in terms of GDP contribution and with a share of 46.1% (Maier, Mönnig &

Zika, 2015). Meanwhile, the primary sector has shrunk dramatically in terms of GDP weight

following the exposure of the country into globalization trends. In average, the GDP growth rate

of China as per the 2017 statistics was 6.9%. These trends in the GDP growth of China has

enabled Volkswagen Company to continue expanding because the citizens can afford to purchase

the vehicles enabling the company to explore more opportunities in the world market (Bekaert &

Hoerova, 2016).

On the other hand, the German economy has been also advancing seasonally although at

a very low phase. Mainly, positive GDP growth rates have come from domestic demand, in

particular, household consumption, government spending, and gross fixed capital. Exports have

however contributed negatively to this trend and that sheds light on the fate of Volkswagen

Company within the country. This is in consideration to the fact that the company is operating

mainly on the domestic market which cannot be considered enough to facilitate the growth of an

established manufacturing company like Volkswagen (Mügge, 2016).

program, it was ranked ninth in the nominal gross domestic product (GDP) globally. 35 years

later it moved up to be the second after the US with a GDP of $9.2 trillion. It’s also due to the

reforms of 1978 that China has become the largest manufacturing hub globally, where the

secondary sector (which comprises construction and industry) made the largest GDP

contribution. China’s modernization has however propelled the tertiary sector to bypass the

secondary sector in terms of GDP contribution and with a share of 46.1% (Maier, Mönnig &

Zika, 2015). Meanwhile, the primary sector has shrunk dramatically in terms of GDP weight

following the exposure of the country into globalization trends. In average, the GDP growth rate

of China as per the 2017 statistics was 6.9%. These trends in the GDP growth of China has

enabled Volkswagen Company to continue expanding because the citizens can afford to purchase

the vehicles enabling the company to explore more opportunities in the world market (Bekaert &

Hoerova, 2016).

On the other hand, the German economy has been also advancing seasonally although at

a very low phase. Mainly, positive GDP growth rates have come from domestic demand, in

particular, household consumption, government spending, and gross fixed capital. Exports have

however contributed negatively to this trend and that sheds light on the fate of Volkswagen

Company within the country. This is in consideration to the fact that the company is operating

mainly on the domestic market which cannot be considered enough to facilitate the growth of an

established manufacturing company like Volkswagen (Mügge, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 11

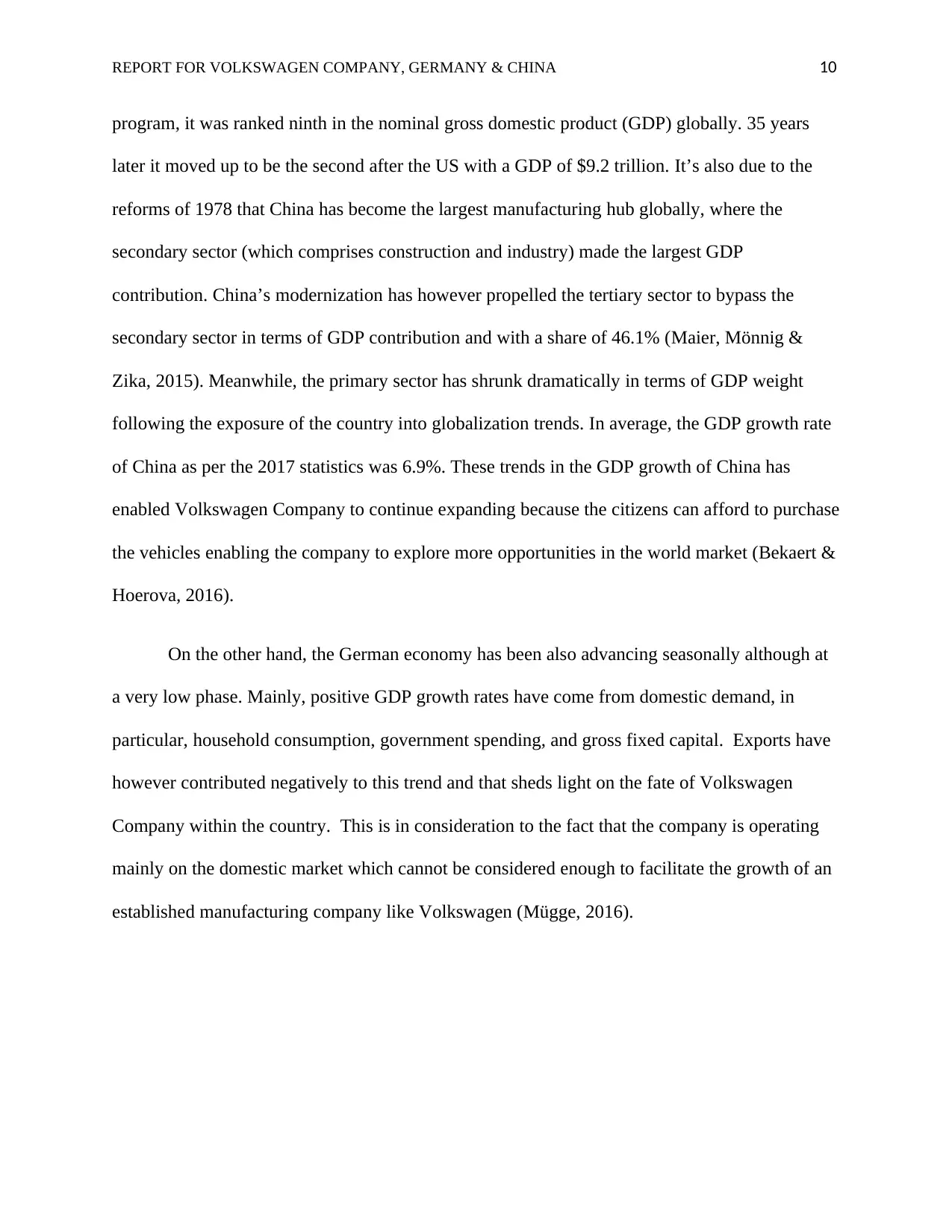

Figure 1.2: GDP Constant-Price, China & Germany

Constant-price GDP entails the calculation of the country’s economic activities in

current-day dollars. By comparison, it factors out the impacts of inflation and allows easy

comparisons by altering the dollar value in other time periods to current-day dollars. When the

GDP decreases for two successive quarters or more, then the economy is said to be in crisis,

meanwhile, when GDP expands too quickly also the chances of inflation increases (Pang &

Siklos, 2016). From the above chart, the GDP Constant Prices of both China and Germany have

been increasing although that of Germany has been doing so in a slower pace compared to the

one for China. I.e. 650899 CNY HML for China and 746.09 for Germany according to the

statistics of 2015-2018. This is an indication that Volkswagen Company expansion pace has been

facilitated by the Constant-price GDP in both countries.

Figure 1.2: GDP Constant-Price, China & Germany

Constant-price GDP entails the calculation of the country’s economic activities in

current-day dollars. By comparison, it factors out the impacts of inflation and allows easy

comparisons by altering the dollar value in other time periods to current-day dollars. When the

GDP decreases for two successive quarters or more, then the economy is said to be in crisis,

meanwhile, when GDP expands too quickly also the chances of inflation increases (Pang &

Siklos, 2016). From the above chart, the GDP Constant Prices of both China and Germany have

been increasing although that of Germany has been doing so in a slower pace compared to the

one for China. I.e. 650899 CNY HML for China and 746.09 for Germany according to the

statistics of 2015-2018. This is an indication that Volkswagen Company expansion pace has been

facilitated by the Constant-price GDP in both countries.

REPORT FOR VOLKSWAGEN COMPANY, GERMANY & CHINA 12

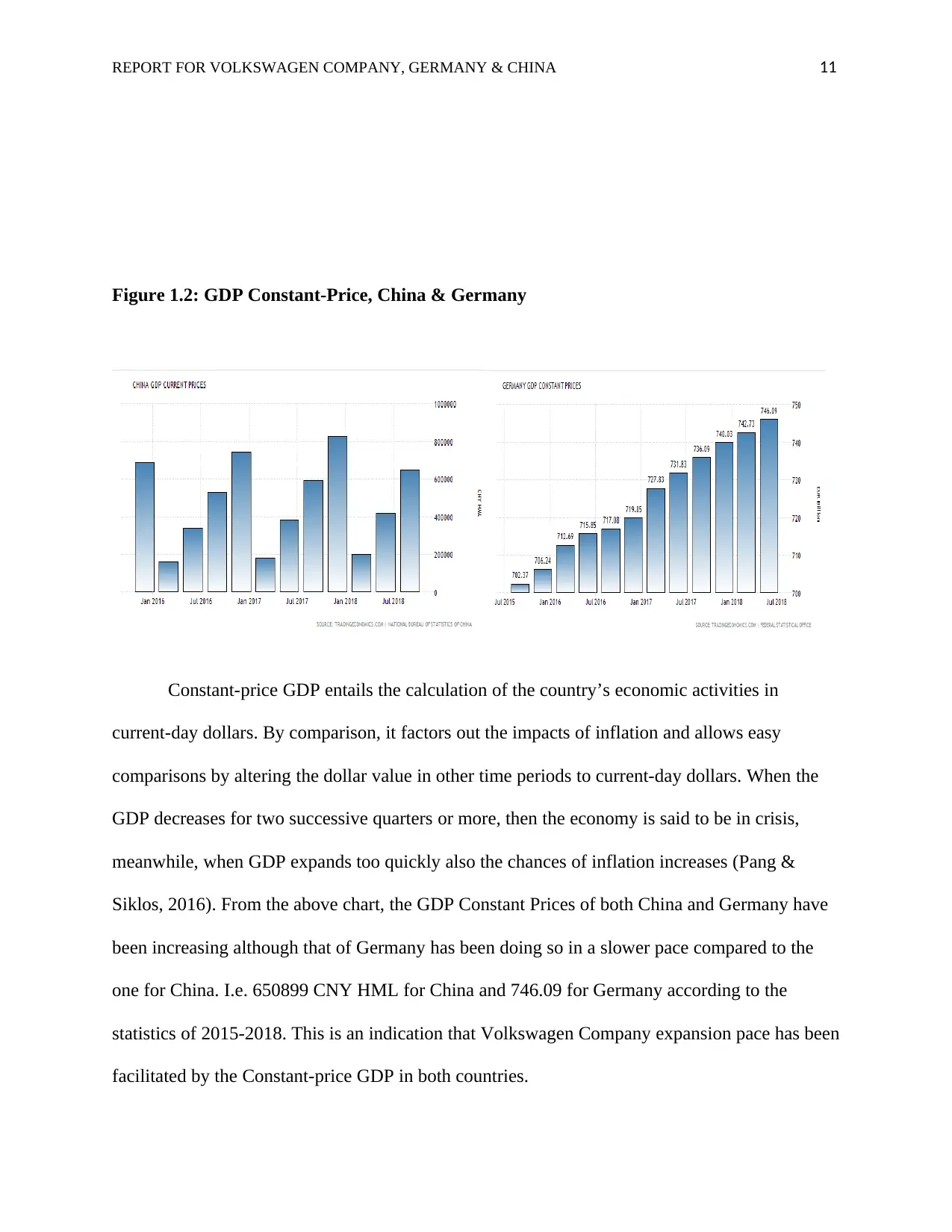

Figure 1.3: Inflation Rates, China & Germany

In both countries, the consumer price inflation has indicated a rising trend as indicated in

the chart above. For instance, the inflation rate in China has recorded an upsurge of 2.5% rose as

per the statistics of September 2018 from 2.3% where it stood in the month of August. The

Chinas Inflation Rate has, therefore, averaged 5.22% from the year 2017 to this year. On the

other hand, although at a slower phase compared to that of China, Germans inflation rate has

been confirmed at the rate of 2.3% as per the same September statistics from 2% where it stood

in August (Li, 2018). In Germany, this is the highest inflation rate which has been encountered

since 2017 as prices of energy; services and food have increased at faster rates. Inflation Rates in

Figure 1.3: Inflation Rates, China & Germany

In both countries, the consumer price inflation has indicated a rising trend as indicated in

the chart above. For instance, the inflation rate in China has recorded an upsurge of 2.5% rose as

per the statistics of September 2018 from 2.3% where it stood in the month of August. The

Chinas Inflation Rate has, therefore, averaged 5.22% from the year 2017 to this year. On the

other hand, although at a slower phase compared to that of China, Germans inflation rate has

been confirmed at the rate of 2.3% as per the same September statistics from 2% where it stood

in August (Li, 2018). In Germany, this is the highest inflation rate which has been encountered

since 2017 as prices of energy; services and food have increased at faster rates. Inflation Rates in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.