MGMT20143 - Business Model Deconstruction: Volt Bank Analysis Report

VerifiedAdded on 2022/09/15

|12

|2252

|23

Report

AI Summary

This report provides an executive summary and detailed analysis of Volt Bank's business model. It begins with an introduction to Volt Bank, a neobank operating in Australia, and its use of a cloud-based platform. The report then breaks down the business model using the Business Model Canvas, examining customer segments, key partners, value propositions, key activities, channels, revenue streams, cost structures, key resources, and customer relationships. It explores the interrelationships between these building blocks, identifies critical success factors, and discusses downside risks. The report also suggests potential business model changes and concludes with recommendations, such as the use of cryptocurrency and potential mergers. The analysis highlights Volt Bank's strengths in digital banking and its competitive advantages, while also acknowledging challenges related to security, capital, and competition with traditional banks. The report is well-structured and uses references to support the analysis.

Running head: THINK BIG

Think Big

Name of the student

Name of the University

Author note

Think Big

Name of the student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1THINK BIG

Executive Summary

This report provides brief description on Volt bank which is the first to operate fully as a

digital bank with deposit and transaction features. The company uses a cloud based

platform based on Temenos T24 core banking along with Salesforce, Microsoft Azure

and Financial Crime Mitigation and Analytics. The analysis of the business canvas

model had shown that the company has a promising future if they are able to manage

the security issues and product portfolio when compared to the traditional banking

organisations.

Executive Summary

This report provides brief description on Volt bank which is the first to operate fully as a

digital bank with deposit and transaction features. The company uses a cloud based

platform based on Temenos T24 core banking along with Salesforce, Microsoft Azure

and Financial Crime Mitigation and Analytics. The analysis of the business canvas

model had shown that the company has a promising future if they are able to manage

the security issues and product portfolio when compared to the traditional banking

organisations.

2THINK BIG

Table of Contents

I. Introduction.....................................................................................................................4

II. Business model.............................................................................................................4

A. Building blocks...........................................................................................................4

1. Customer segments...............................................................................................4

2. Key partners...........................................................................................................4

3. Value proposition....................................................................................................4

4. Key activities...........................................................................................................4

5. Channels................................................................................................................5

6. Revenue Streams...................................................................................................5

7. Cost structure.........................................................................................................5

8. Key Resources.......................................................................................................5

9. Customer Relationships.........................................................................................5

B. Interrelationships.......................................................................................................5

C. Critical Success factors.............................................................................................6

D. Downside risks..........................................................................................................6

E. Business model changes...........................................................................................6

III. Conclusion....................................................................................................................6

IV. Recommendations.......................................................................................................7

References.........................................................................................................................8

Appendix 1 (Business Canvas Model)..............................................................................9

Table of Contents

I. Introduction.....................................................................................................................4

II. Business model.............................................................................................................4

A. Building blocks...........................................................................................................4

1. Customer segments...............................................................................................4

2. Key partners...........................................................................................................4

3. Value proposition....................................................................................................4

4. Key activities...........................................................................................................4

5. Channels................................................................................................................5

6. Revenue Streams...................................................................................................5

7. Cost structure.........................................................................................................5

8. Key Resources.......................................................................................................5

9. Customer Relationships.........................................................................................5

B. Interrelationships.......................................................................................................5

C. Critical Success factors.............................................................................................6

D. Downside risks..........................................................................................................6

E. Business model changes...........................................................................................6

III. Conclusion....................................................................................................................6

IV. Recommendations.......................................................................................................7

References.........................................................................................................................8

Appendix 1 (Business Canvas Model)..............................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3THINK BIG

I. Introduction

Volt bank is one of the neobanks in Australia and are the first bank to have

gained the full banking license among all the challengers. The company has its

headquarters in Sydney and have been found in the year of 2018. The authorization to

operate as a full banking and deposit taking institutions was issues in January, 2019

(voltbank.com.au, 2020). The company uses a cloud based platform based on Temenos

T24 core banking along with Salesforce, Microsoft Azure and Financial Crime Mitigation

and Analytics. The company has also published Volt Lab applications and mobile

applications for gathering feedback from the consumers through feedback on the

services and products offered by the bank. The main aim of the company has been to

change the way people operated in the banking industry (voltbank.com.au, 2020).

Therefore, the company aimed for complete transparency and experience for the

consumers.

II. Business model

A. Building blocks

1. Customer segments

The Volt bank has been targeting mainly the millennial generation in Australia

consisting of young corporate officials, budding entrepreneurs, freelancers and self-

employed people (voltbank.com.au, 2020). Online banking is quite convenient for these

consumers and prefer using digital banking than traditional banking. A research

conducted by Mozo shows that 75% of the Australians use computer or a smartphone

for banking services (Watson, 2020). When dividing the demography in different age

groups, it was seen that 43% of the consumers in the age group of 18-24 years used

online banking, 40% of the consumers in the age group 25-34 years used online

banking, 46% in age group of 35-44 years, 49% in the age group of 45-54 years, 64% in

the age group of 55-64 years and 67% in the age group of 65 and above (Watson,

2020).

2. Key partners

The key partners of Volt Bank includes Fintech, Frollo, Verrency, PayPal,

Collection House and Temenos (australianfintech.com.au, 2020; thepower50.com,

2020; PALMER-DERRIEN, 2019). These partners includes the software and platform

management companies along with investors. Some of these companies are

transaction partners such as PayPal and Verrency as payment service providers.

3. Value proposition

The Value proposition of the company is to offer banking experience and

convenience for the younger generation, low banking fee, highly secured banking and

full transparency (voltbank.com.au, 2020).

I. Introduction

Volt bank is one of the neobanks in Australia and are the first bank to have

gained the full banking license among all the challengers. The company has its

headquarters in Sydney and have been found in the year of 2018. The authorization to

operate as a full banking and deposit taking institutions was issues in January, 2019

(voltbank.com.au, 2020). The company uses a cloud based platform based on Temenos

T24 core banking along with Salesforce, Microsoft Azure and Financial Crime Mitigation

and Analytics. The company has also published Volt Lab applications and mobile

applications for gathering feedback from the consumers through feedback on the

services and products offered by the bank. The main aim of the company has been to

change the way people operated in the banking industry (voltbank.com.au, 2020).

Therefore, the company aimed for complete transparency and experience for the

consumers.

II. Business model

A. Building blocks

1. Customer segments

The Volt bank has been targeting mainly the millennial generation in Australia

consisting of young corporate officials, budding entrepreneurs, freelancers and self-

employed people (voltbank.com.au, 2020). Online banking is quite convenient for these

consumers and prefer using digital banking than traditional banking. A research

conducted by Mozo shows that 75% of the Australians use computer or a smartphone

for banking services (Watson, 2020). When dividing the demography in different age

groups, it was seen that 43% of the consumers in the age group of 18-24 years used

online banking, 40% of the consumers in the age group 25-34 years used online

banking, 46% in age group of 35-44 years, 49% in the age group of 45-54 years, 64% in

the age group of 55-64 years and 67% in the age group of 65 and above (Watson,

2020).

2. Key partners

The key partners of Volt Bank includes Fintech, Frollo, Verrency, PayPal,

Collection House and Temenos (australianfintech.com.au, 2020; thepower50.com,

2020; PALMER-DERRIEN, 2019). These partners includes the software and platform

management companies along with investors. Some of these companies are

transaction partners such as PayPal and Verrency as payment service providers.

3. Value proposition

The Value proposition of the company is to offer banking experience and

convenience for the younger generation, low banking fee, highly secured banking and

full transparency (voltbank.com.au, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4THINK BIG

4. Key activities

The company wishes to offer full-fledged banking services, product services and

24 hours customer support (voltbank.com.au, 2020). The company offers high speed

digital services by offering the latest technological platform.

5. Channels

The company is a fully digital banking organisation offering banking service

where complete digital networks are being used. The partner channels offer platform

support on the cloud along with transaction software (temenos.com, 2018). Social

media is another channel used by the company to gather new consumers and perform

banking services.

6. Revenue Streams

The revenue streams of the company is generated from online banking services

and product sales which is similar to the revenue streams of any traditional banking

structure (voltbank.com.au, 2020).

7. Cost structure

The cost structure includes factors such as technology and platform

development, marketing, customer service, administration, licensing, compliance and

regulations. The overall service of the organisation is totally dependent on technology

and platform development (finextra.com, 2019). The company has started up and have

turned into a full-fledged business so licensing, compliance and regulations also add up

to the cost incurred by the organisation.

8. Key Resources

The key resources include platform, brand and partnership, strong and unique brand

catering to youth, scalability of products in many verticals, partnership with companies

providing opportunity to expand at a faster rate and API platform. The brand has good

image in the market along with the partners providing funding and software support. The

new technological product improves the scalability of the products and transactions

resulting in agility and security of the banking model (temenos.com, 2018). Moreover,

the model has a pre country specific function which facilitated in fully operate as an

online banking organisation (temenos.com, 2018).

9. Customer Relationships

The customer relationships include digital banking, online service to the

consumers, mobile services, social media channels and cloud environment. The

company is a digital bank uses online platform along with mobile banking applications

and other applications for engaging with the consumers (voltbank.com.au, 2020).

B. Interrelationships

There is significant interrelationship between all the building blocks as all these

blocks are necessary for successfully operating the business. The key investors are

responsible for providing funding and generating new funds from partners to improve

the scale of operation (Berry, 2019). On the other hand, other partners such as the

technology and software operating companies are supporting volt to develop a digital

4. Key activities

The company wishes to offer full-fledged banking services, product services and

24 hours customer support (voltbank.com.au, 2020). The company offers high speed

digital services by offering the latest technological platform.

5. Channels

The company is a fully digital banking organisation offering banking service

where complete digital networks are being used. The partner channels offer platform

support on the cloud along with transaction software (temenos.com, 2018). Social

media is another channel used by the company to gather new consumers and perform

banking services.

6. Revenue Streams

The revenue streams of the company is generated from online banking services

and product sales which is similar to the revenue streams of any traditional banking

structure (voltbank.com.au, 2020).

7. Cost structure

The cost structure includes factors such as technology and platform

development, marketing, customer service, administration, licensing, compliance and

regulations. The overall service of the organisation is totally dependent on technology

and platform development (finextra.com, 2019). The company has started up and have

turned into a full-fledged business so licensing, compliance and regulations also add up

to the cost incurred by the organisation.

8. Key Resources

The key resources include platform, brand and partnership, strong and unique brand

catering to youth, scalability of products in many verticals, partnership with companies

providing opportunity to expand at a faster rate and API platform. The brand has good

image in the market along with the partners providing funding and software support. The

new technological product improves the scalability of the products and transactions

resulting in agility and security of the banking model (temenos.com, 2018). Moreover,

the model has a pre country specific function which facilitated in fully operate as an

online banking organisation (temenos.com, 2018).

9. Customer Relationships

The customer relationships include digital banking, online service to the

consumers, mobile services, social media channels and cloud environment. The

company is a digital bank uses online platform along with mobile banking applications

and other applications for engaging with the consumers (voltbank.com.au, 2020).

B. Interrelationships

There is significant interrelationship between all the building blocks as all these

blocks are necessary for successfully operating the business. The key investors are

responsible for providing funding and generating new funds from partners to improve

the scale of operation (Berry, 2019). On the other hand, other partners such as the

technology and software operating companies are supporting volt to develop a digital

5THINK BIG

banking website with high quality security along with the development of new

applications on the smartphone devices for improving the quality of engagement. It

defines the value proposition of the company that has been trying to develop a highly

transparent operation focused on providing convenience to the consumers.

The key resources of the company depict the use of resources to develop better

service and product opportunities for modern consumers allowing utmost convenience.

In order to maintain effective customer relationship, the key partners and cloud handling

organisations has developed effective platforms.

C. Critical Success factors

The key success factor for Volt bank includes innovation and transformation of

banking operations. It is essential to make sure that Volt is not only offering digital first

but mobile first to their consumers. The quality of experience on mobile banking has to

be totally exclusive and differentiated to traditional banking applications.

The second critical success factor is flexibility of the banking devices and

systems which should focus on continuous evolution of the system using agile

technology including autonomy to the third party providers. The third success factor is

offering low and zero fees for services which provides competitive to the company in

respect to other companies in the market. The final success factor is use of crypto

currency to attract new consumers and democratized the process of crypto trading.

D. Downside risks

Even though Neo banks have been revolutionary in changing the banking

industry, there are various drawbacks of Volt which affects their business and are risk

factors. Volt offers minimum services when compared to the traditional banking

organisations which is not due to the regulatory problems but due to the lack of capital.

Consumers does not trust online banking and even though traditional services does not

offer optimal experiences to the users but service portfolio is safer. The problem of

cyber security in digital banking along with protection of personal data is a great risk for

the consumers. Volt is just starting out and they need to expand by providing security

and quality services to the consumers to increase their market share but it is quite for

them to match up to the infrastructure of traditional banks.

E. Business model changes

There are significant changes to the business model which can be made to

improve it further such as the use of security based services and encrypted data to

improve the chance of cybercrimes. Volt bank should merge with major neo banks

already established in Europe to expand and learn from the first movers in the industry.

The company should launch new products and services at regular intervals to match up

to the services offered by the traditional organisations. The company should also target

consumers in emerging economies due to the penetration of technology and internet

banking to various parts of the world. The use of crypto currency to attract new

consumers and democratized the process of crypto trading is another change which

would provide upper hand to the company.

banking website with high quality security along with the development of new

applications on the smartphone devices for improving the quality of engagement. It

defines the value proposition of the company that has been trying to develop a highly

transparent operation focused on providing convenience to the consumers.

The key resources of the company depict the use of resources to develop better

service and product opportunities for modern consumers allowing utmost convenience.

In order to maintain effective customer relationship, the key partners and cloud handling

organisations has developed effective platforms.

C. Critical Success factors

The key success factor for Volt bank includes innovation and transformation of

banking operations. It is essential to make sure that Volt is not only offering digital first

but mobile first to their consumers. The quality of experience on mobile banking has to

be totally exclusive and differentiated to traditional banking applications.

The second critical success factor is flexibility of the banking devices and

systems which should focus on continuous evolution of the system using agile

technology including autonomy to the third party providers. The third success factor is

offering low and zero fees for services which provides competitive to the company in

respect to other companies in the market. The final success factor is use of crypto

currency to attract new consumers and democratized the process of crypto trading.

D. Downside risks

Even though Neo banks have been revolutionary in changing the banking

industry, there are various drawbacks of Volt which affects their business and are risk

factors. Volt offers minimum services when compared to the traditional banking

organisations which is not due to the regulatory problems but due to the lack of capital.

Consumers does not trust online banking and even though traditional services does not

offer optimal experiences to the users but service portfolio is safer. The problem of

cyber security in digital banking along with protection of personal data is a great risk for

the consumers. Volt is just starting out and they need to expand by providing security

and quality services to the consumers to increase their market share but it is quite for

them to match up to the infrastructure of traditional banks.

E. Business model changes

There are significant changes to the business model which can be made to

improve it further such as the use of security based services and encrypted data to

improve the chance of cybercrimes. Volt bank should merge with major neo banks

already established in Europe to expand and learn from the first movers in the industry.

The company should launch new products and services at regular intervals to match up

to the services offered by the traditional organisations. The company should also target

consumers in emerging economies due to the penetration of technology and internet

banking to various parts of the world. The use of crypto currency to attract new

consumers and democratized the process of crypto trading is another change which

would provide upper hand to the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6THINK BIG

III. Conclusion

The analysis of the business canvas model shows that the prospect of Volt

succeeding in the current banking industry is high as the majority of the consumers in

Australia are used to mobile and net banking facilities. Moreover, the business model

also shows that the key partners have been able to raise funds to expand the business

at large scale to match up to the traditional big four in Australia. Moreover, the

scalability and agility of the banking services in digital platform is far superior to any

normal banking applications which provides significant competitive advantage to the

company.

IV. Recommendations

Therefore, based on the analysis of the business model following recommendations

have been proposed:

The use of crypto currency to attract new consumers and democratized the

process of crypto trading is necessary to gain competitive advantage. The

consumers are interested in crypto currency but none of the traditional banks

consider it as legit trading currency.

Volt should merge with other Neo banks such as Xinja so that they can use both

their capital funding to match up to the scale of operation of any big four

traditional bank in Australia.

III. Conclusion

The analysis of the business canvas model shows that the prospect of Volt

succeeding in the current banking industry is high as the majority of the consumers in

Australia are used to mobile and net banking facilities. Moreover, the business model

also shows that the key partners have been able to raise funds to expand the business

at large scale to match up to the traditional big four in Australia. Moreover, the

scalability and agility of the banking services in digital platform is far superior to any

normal banking applications which provides significant competitive advantage to the

company.

IV. Recommendations

Therefore, based on the analysis of the business model following recommendations

have been proposed:

The use of crypto currency to attract new consumers and democratized the

process of crypto trading is necessary to gain competitive advantage. The

consumers are interested in crypto currency but none of the traditional banks

consider it as legit trading currency.

Volt should merge with other Neo banks such as Xinja so that they can use both

their capital funding to match up to the scale of operation of any big four

traditional bank in Australia.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7THINK BIG

References

australianfintech.com.au. (2020). Volt partners with Frollo to create Volt Labs and put

customers first. Australian FinTech. Retrieved 10 April 2020, from

https://australianfintech.com.au/volt-partners-with-frollo-to-create-volt-labs-and-

put-customers-first/.

Berry, P. (2019). Neobanks: How Do Volt & Xinja Plan To Change Banking? | Canstar.

Canstar.com.au. Retrieved 10 April 2020, from

https://www.canstar.com.au/online-banking/neobanks-how-do-volt-xinja-plan-to-

change-banking/.

finextra.com. (2019). Volt Bank contracts with FIS. Finextra Research. Retrieved 10

April 2020, from https://www.finextra.com/newsarticle/34155/volt-bank-contracts-

with-fis.

PALMER-DERRIEN, S. (2019). Volt becomes first neobank to secure full banking

licence — and celebrates a $8.4 million raise - SmartCompany. SmartCompany.

Retrieved 10 April 2020, from

https://www.smartcompany.com.au/startupsmart/news/volt-bank-neobank-full-

banking-licence/.

Rogers, I. (2019). Volt Bank counts on fintech sparkle. Banking Day. Retrieved 10 April

2020, from https://www.bankingday.com/nl06_news_selected.php?

selkey=25744.

temenos.com. (2018). Neobank Volt Bank Record Time Go Live With Temenos Digital

Banking. Temenos. Retrieved 10 April 2020, from

https://www.temenos.com/news/2018/12/19/neobank-volt-bank-record-time-go-

live-with-temenos-digital-banking/.

thepower50.com. (2020). volt bank inks deal with Verrency | The Fintech Power 50. The

Fintech Power 50. Retrieved 10 April 2020, from

https://www.thepower50.com/volt-bank-inks-deal-with-verrency/.

voltbank.com.au. (2020). About Us | Volt Bank. Voltbank.com.au. Retrieved 10 April

2020, from https://www.voltbank.com.au/about/.

Watson, T. (2020). Neobank Report 2020: Digital banking in a new decade.

Mozo.com.au. Retrieved 10 April 2020, from

https://mozo.com.au/neobanks/articles/neobank-2020-report-digital-banking-in-a-

new-decade.

References

australianfintech.com.au. (2020). Volt partners with Frollo to create Volt Labs and put

customers first. Australian FinTech. Retrieved 10 April 2020, from

https://australianfintech.com.au/volt-partners-with-frollo-to-create-volt-labs-and-

put-customers-first/.

Berry, P. (2019). Neobanks: How Do Volt & Xinja Plan To Change Banking? | Canstar.

Canstar.com.au. Retrieved 10 April 2020, from

https://www.canstar.com.au/online-banking/neobanks-how-do-volt-xinja-plan-to-

change-banking/.

finextra.com. (2019). Volt Bank contracts with FIS. Finextra Research. Retrieved 10

April 2020, from https://www.finextra.com/newsarticle/34155/volt-bank-contracts-

with-fis.

PALMER-DERRIEN, S. (2019). Volt becomes first neobank to secure full banking

licence — and celebrates a $8.4 million raise - SmartCompany. SmartCompany.

Retrieved 10 April 2020, from

https://www.smartcompany.com.au/startupsmart/news/volt-bank-neobank-full-

banking-licence/.

Rogers, I. (2019). Volt Bank counts on fintech sparkle. Banking Day. Retrieved 10 April

2020, from https://www.bankingday.com/nl06_news_selected.php?

selkey=25744.

temenos.com. (2018). Neobank Volt Bank Record Time Go Live With Temenos Digital

Banking. Temenos. Retrieved 10 April 2020, from

https://www.temenos.com/news/2018/12/19/neobank-volt-bank-record-time-go-

live-with-temenos-digital-banking/.

thepower50.com. (2020). volt bank inks deal with Verrency | The Fintech Power 50. The

Fintech Power 50. Retrieved 10 April 2020, from

https://www.thepower50.com/volt-bank-inks-deal-with-verrency/.

voltbank.com.au. (2020). About Us | Volt Bank. Voltbank.com.au. Retrieved 10 April

2020, from https://www.voltbank.com.au/about/.

Watson, T. (2020). Neobank Report 2020: Digital banking in a new decade.

Mozo.com.au. Retrieved 10 April 2020, from

https://mozo.com.au/neobanks/articles/neobank-2020-report-digital-banking-in-a-

new-decade.

8THINK BIG

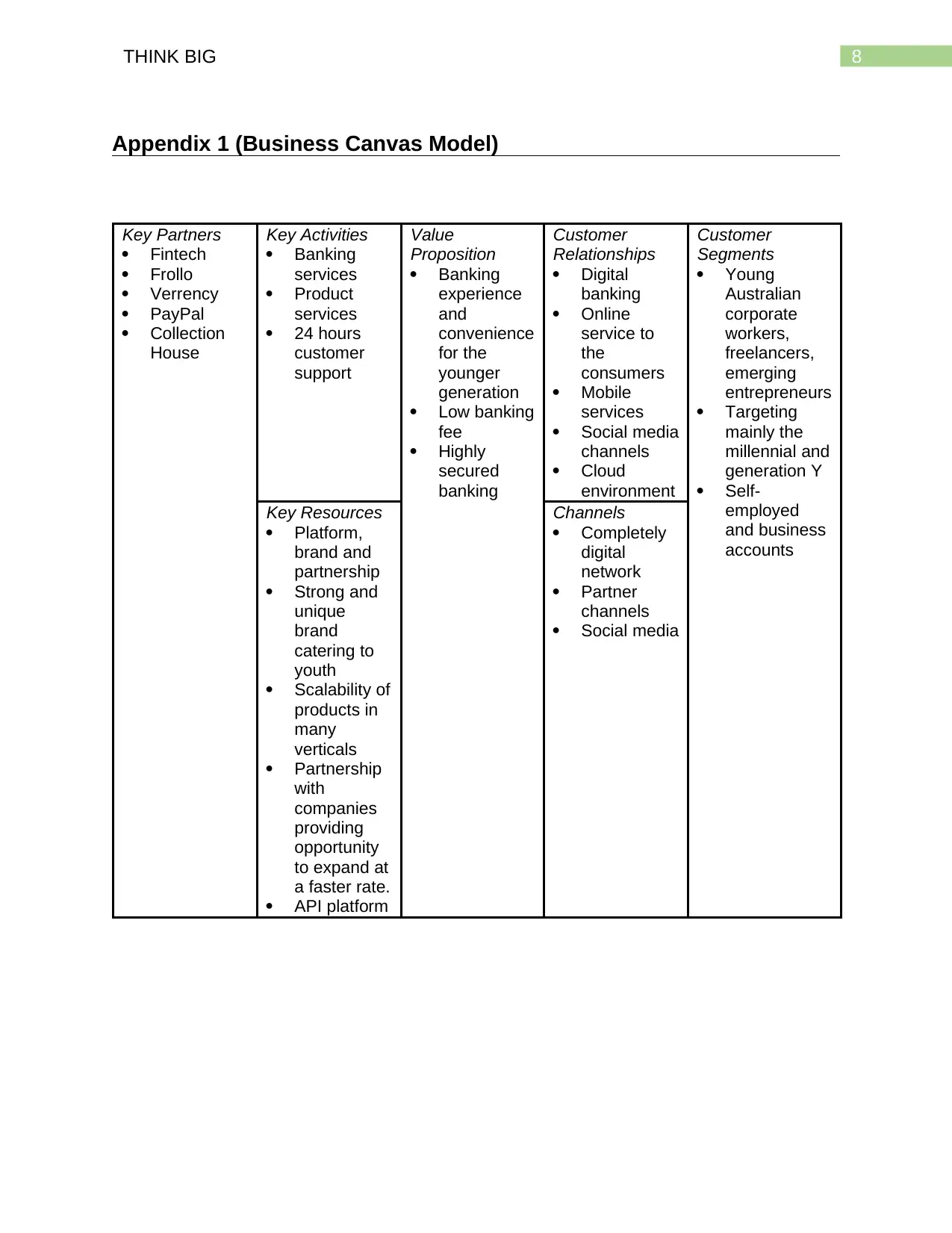

Appendix 1 (Business Canvas Model)

Key Partners

Fintech

Frollo

Verrency

PayPal

Collection

House

Key Activities

Banking

services

Product

services

24 hours

customer

support

Value

Proposition

Banking

experience

and

convenience

for the

younger

generation

Low banking

fee

Highly

secured

banking

Customer

Relationships

Digital

banking

Online

service to

the

consumers

Mobile

services

Social media

channels

Cloud

environment

Customer

Segments

Young

Australian

corporate

workers,

freelancers,

emerging

entrepreneurs

Targeting

mainly the

millennial and

generation Y

Self-

employed

and business

accounts

Key Resources

Platform,

brand and

partnership

Strong and

unique

brand

catering to

youth

Scalability of

products in

many

verticals

Partnership

with

companies

providing

opportunity

to expand at

a faster rate.

API platform

Channels

Completely

digital

network

Partner

channels

Social media

Appendix 1 (Business Canvas Model)

Key Partners

Fintech

Frollo

Verrency

PayPal

Collection

House

Key Activities

Banking

services

Product

services

24 hours

customer

support

Value

Proposition

Banking

experience

and

convenience

for the

younger

generation

Low banking

fee

Highly

secured

banking

Customer

Relationships

Digital

banking

Online

service to

the

consumers

Mobile

services

Social media

channels

Cloud

environment

Customer

Segments

Young

Australian

corporate

workers,

freelancers,

emerging

entrepreneurs

Targeting

mainly the

millennial and

generation Y

Self-

employed

and business

accounts

Key Resources

Platform,

brand and

partnership

Strong and

unique

brand

catering to

youth

Scalability of

products in

many

verticals

Partnership

with

companies

providing

opportunity

to expand at

a faster rate.

API platform

Channels

Completely

digital

network

Partner

channels

Social media

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9THINK BIG

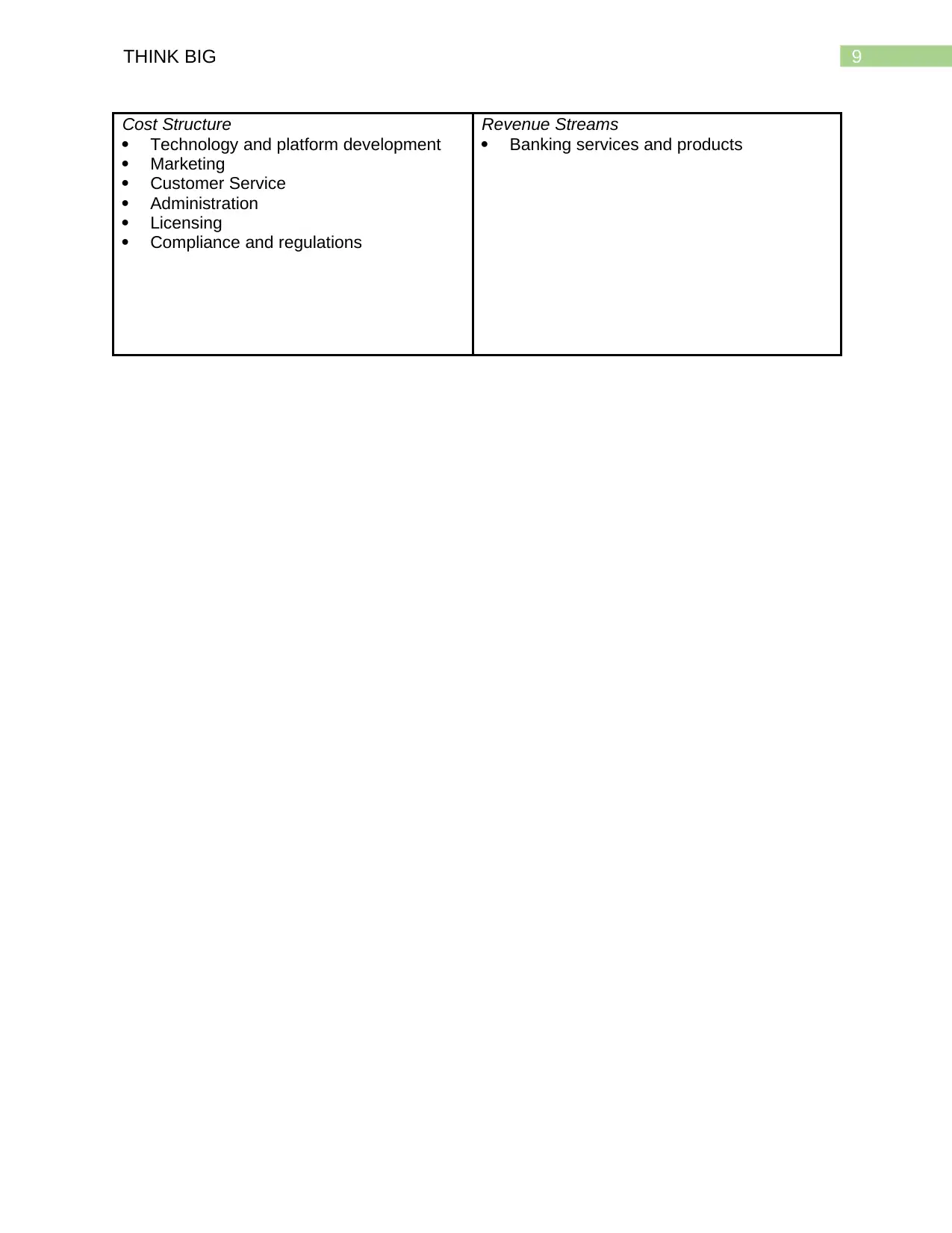

Cost Structure

Technology and platform development

Marketing

Customer Service

Administration

Licensing

Compliance and regulations

Revenue Streams

Banking services and products

Cost Structure

Technology and platform development

Marketing

Customer Service

Administration

Licensing

Compliance and regulations

Revenue Streams

Banking services and products

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10THINK BIG

Appendix 2

Appendix 2

11THINK BIG

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.