Financial Analysis of Voltas Communication: Costing Assignment 2019

VerifiedAdded on 2022/11/10

|14

|2666

|426

Report

AI Summary

This report analyzes the costing methods used by Voltas Communication, focusing on job costing and activity-based costing. The assignment calculates manufacturing overhead, material consumption, and overhead recovery rates. It addresses the treatment of under and over-applied overheads, comparing methods like charging to cost of goods sold, apportionment, and allocation to specific jobs, recommending the latter. The report also evaluates the suitability of activity-based costing for Voltas Communication, discussing its advantages in allocating indirect costs and providing detailed calculations for closing stock valuation. The analysis covers various aspects of costing, including direct materials, labor, and overheads, providing a comprehensive overview of the company's financial data and cost allocation strategies.

Costing

Assignment

2019

Assignment

2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

Date: 28th May, 2018.

1 | P a g e

By student name

Professor

Date: 28th May, 2018.

1 | P a g e

2

Executive Summary

The purpose of this assignment is to demonstrate the ability to analyze the given financial

information in relation management Accounting problem through the help of the given case

study, based on which the finding of the study is to be presented. Our case study broadly covers

the scenario of the Voltas communication which is applying the Job costing method for

allocation of its indirect manufacturing overhead. It further discusses about the over and under

recovery of overheads along with the treatment of such under or over recovery of overheads. It

also throws light on the mostly used method for allocation of indirect overheads known as

activity-based costing and the suitability of its application in the given case of Voltas

Communication.

2 | P a g e

Executive Summary

The purpose of this assignment is to demonstrate the ability to analyze the given financial

information in relation management Accounting problem through the help of the given case

study, based on which the finding of the study is to be presented. Our case study broadly covers

the scenario of the Voltas communication which is applying the Job costing method for

allocation of its indirect manufacturing overhead. It further discusses about the over and under

recovery of overheads along with the treatment of such under or over recovery of overheads. It

also throws light on the mostly used method for allocation of indirect overheads known as

activity-based costing and the suitability of its application in the given case of Voltas

Communication.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................9

Conclusion.................................................................................................................................................11

References.................................................................................................................................................12

Question 1

Job costing method

As per job costing method the major motive of the manufacturer is to determine the cost of a

specific job rather than the cost of a process. In this way the revenue and expenses associated

with the job is matched to determine the profitability of a specific job.

As per the Job costing there are basically three major components of a specific job and they are

Material, labor and overheads. In case multiple jobs are being carried out by an entity it becomes

quite difficult to trac the costs associated with the job for which this method may be applied. It is

also a source of financial information to the cost accountant who can compare the actual costs

incurred for a job with the budgeted cost of the job to provide warning to the management in

case it exceeds the budgeted cost of the job (Abdullah & Said, 2017).

3 | P a g e

Contents

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................9

Conclusion.................................................................................................................................................11

References.................................................................................................................................................12

Question 1

Job costing method

As per job costing method the major motive of the manufacturer is to determine the cost of a

specific job rather than the cost of a process. In this way the revenue and expenses associated

with the job is matched to determine the profitability of a specific job.

As per the Job costing there are basically three major components of a specific job and they are

Material, labor and overheads. In case multiple jobs are being carried out by an entity it becomes

quite difficult to trac the costs associated with the job for which this method may be applied. It is

also a source of financial information to the cost accountant who can compare the actual costs

incurred for a job with the budgeted cost of the job to provide warning to the management in

case it exceeds the budgeted cost of the job (Abdullah & Said, 2017).

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

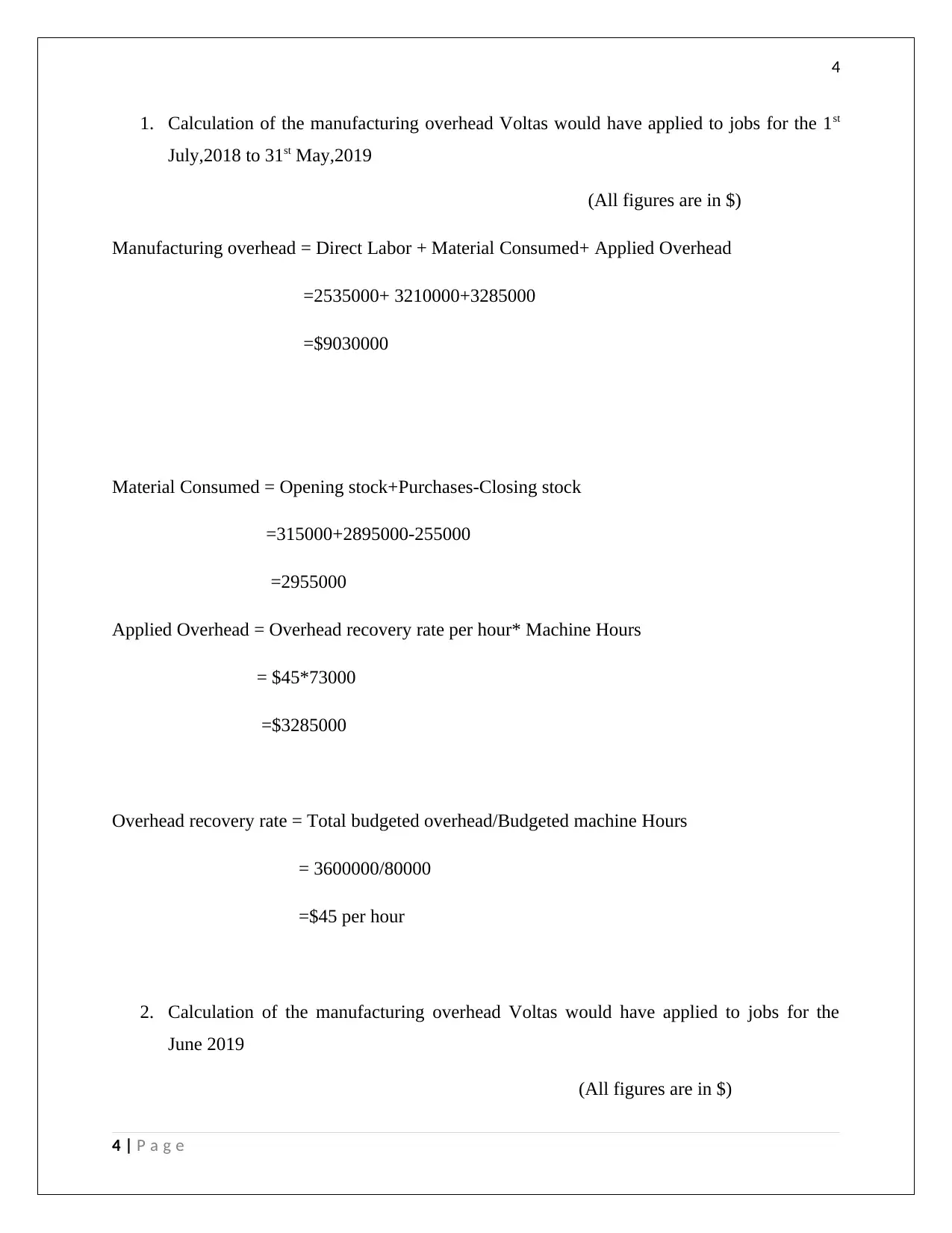

1. Calculation of the manufacturing overhead Voltas would have applied to jobs for the 1st

July,2018 to 31st May,2019

(All figures are in $)

Manufacturing overhead = Direct Labor + Material Consumed+ Applied Overhead

=2535000+ 3210000+3285000

=$9030000

Material Consumed = Opening stock+Purchases-Closing stock

=315000+2895000-255000

=2955000

Applied Overhead = Overhead recovery rate per hour* Machine Hours

= $45*73000

=$3285000

Overhead recovery rate = Total budgeted overhead/Budgeted machine Hours

= 3600000/80000

=$45 per hour

2. Calculation of the manufacturing overhead Voltas would have applied to jobs for the

June 2019

(All figures are in $)

4 | P a g e

1. Calculation of the manufacturing overhead Voltas would have applied to jobs for the 1st

July,2018 to 31st May,2019

(All figures are in $)

Manufacturing overhead = Direct Labor + Material Consumed+ Applied Overhead

=2535000+ 3210000+3285000

=$9030000

Material Consumed = Opening stock+Purchases-Closing stock

=315000+2895000-255000

=2955000

Applied Overhead = Overhead recovery rate per hour* Machine Hours

= $45*73000

=$3285000

Overhead recovery rate = Total budgeted overhead/Budgeted machine Hours

= 3600000/80000

=$45 per hour

2. Calculation of the manufacturing overhead Voltas would have applied to jobs for the

June 2019

(All figures are in $)

4 | P a g e

5

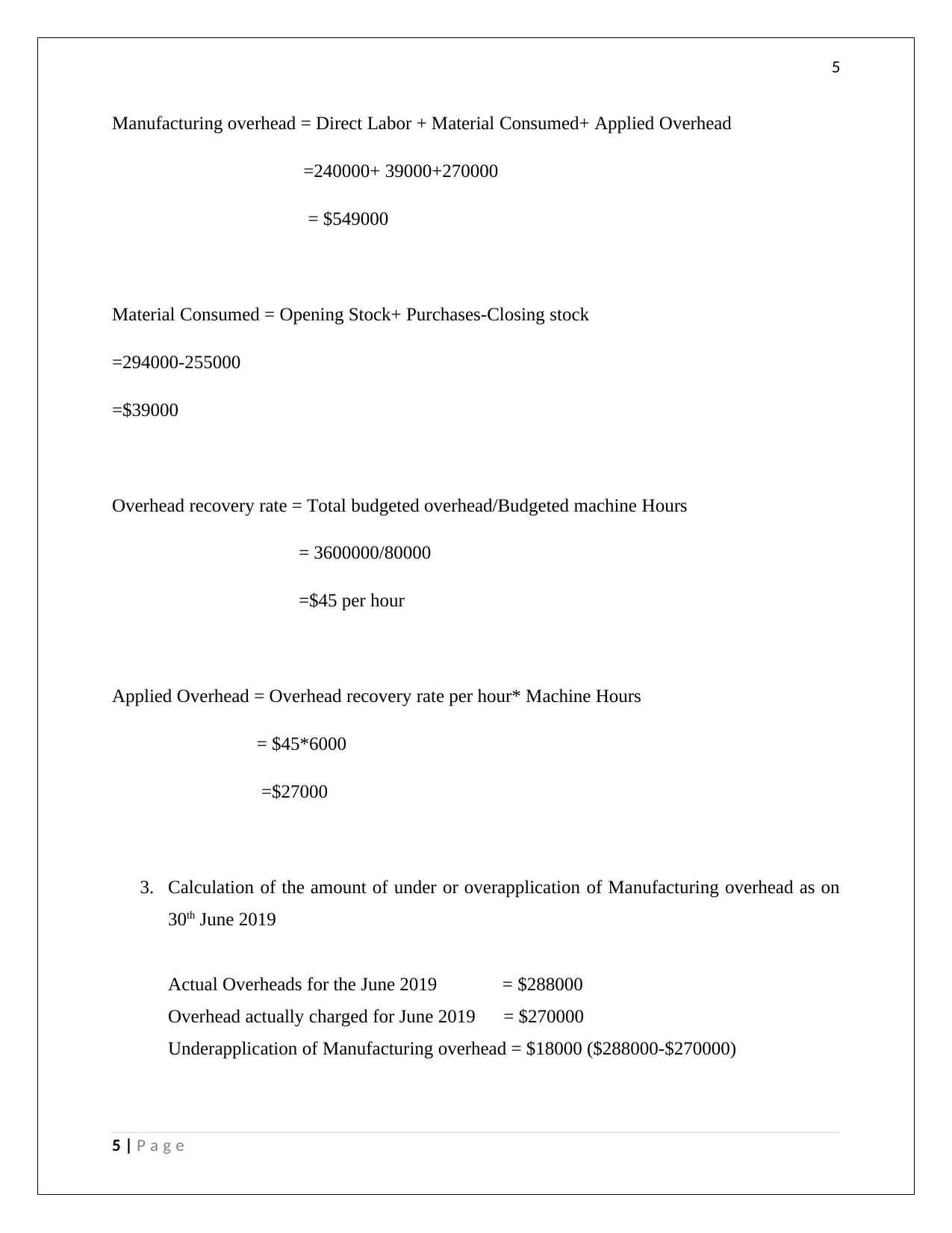

Manufacturing overhead = Direct Labor + Material Consumed+ Applied Overhead

=240000+ 39000+270000

= $549000

Material Consumed = Opening Stock+ Purchases-Closing stock

=294000-255000

=$39000

Overhead recovery rate = Total budgeted overhead/Budgeted machine Hours

= 3600000/80000

=$45 per hour

Applied Overhead = Overhead recovery rate per hour* Machine Hours

= $45*6000

=$27000

3. Calculation of the amount of under or overapplication of Manufacturing overhead as on

30th June 2019

Actual Overheads for the June 2019 = $288000

Overhead actually charged for June 2019 = $270000

Underapplication of Manufacturing overhead = $18000 ($288000-$270000)

5 | P a g e

Manufacturing overhead = Direct Labor + Material Consumed+ Applied Overhead

=240000+ 39000+270000

= $549000

Material Consumed = Opening Stock+ Purchases-Closing stock

=294000-255000

=$39000

Overhead recovery rate = Total budgeted overhead/Budgeted machine Hours

= 3600000/80000

=$45 per hour

Applied Overhead = Overhead recovery rate per hour* Machine Hours

= $45*6000

=$27000

3. Calculation of the amount of under or overapplication of Manufacturing overhead as on

30th June 2019

Actual Overheads for the June 2019 = $288000

Overhead actually charged for June 2019 = $270000

Underapplication of Manufacturing overhead = $18000 ($288000-$270000)

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

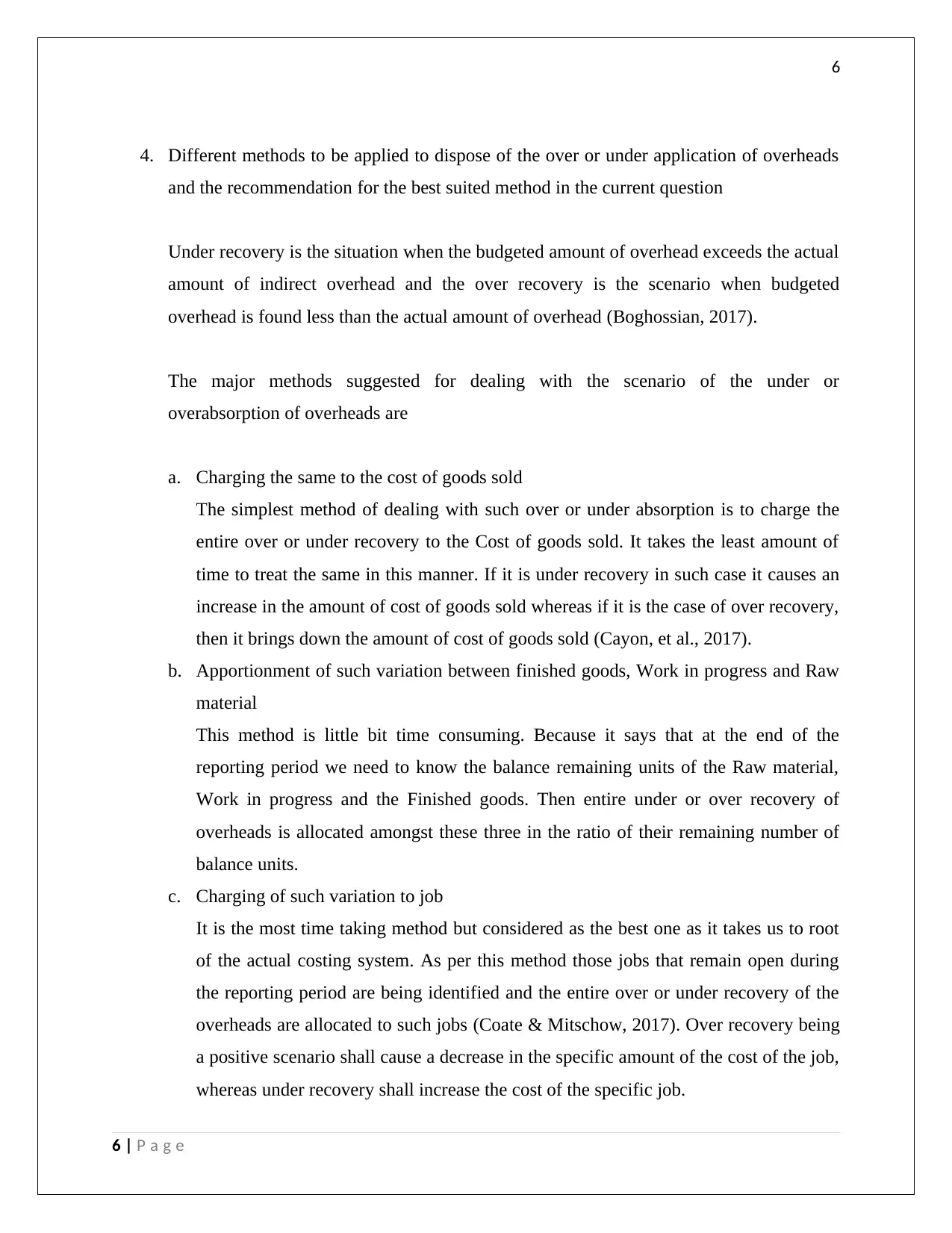

4. Different methods to be applied to dispose of the over or under application of overheads

and the recommendation for the best suited method in the current question

Under recovery is the situation when the budgeted amount of overhead exceeds the actual

amount of indirect overhead and the over recovery is the scenario when budgeted

overhead is found less than the actual amount of overhead (Boghossian, 2017).

The major methods suggested for dealing with the scenario of the under or

overabsorption of overheads are

a. Charging the same to the cost of goods sold

The simplest method of dealing with such over or under absorption is to charge the

entire over or under recovery to the Cost of goods sold. It takes the least amount of

time to treat the same in this manner. If it is under recovery in such case it causes an

increase in the amount of cost of goods sold whereas if it is the case of over recovery,

then it brings down the amount of cost of goods sold (Cayon, et al., 2017).

b. Apportionment of such variation between finished goods, Work in progress and Raw

material

This method is little bit time consuming. Because it says that at the end of the

reporting period we need to know the balance remaining units of the Raw material,

Work in progress and the Finished goods. Then entire under or over recovery of

overheads is allocated amongst these three in the ratio of their remaining number of

balance units.

c. Charging of such variation to job

It is the most time taking method but considered as the best one as it takes us to root

of the actual costing system. As per this method those jobs that remain open during

the reporting period are being identified and the entire over or under recovery of the

overheads are allocated to such jobs (Coate & Mitschow, 2017). Over recovery being

a positive scenario shall cause a decrease in the specific amount of the cost of the job,

whereas under recovery shall increase the cost of the specific job.

6 | P a g e

4. Different methods to be applied to dispose of the over or under application of overheads

and the recommendation for the best suited method in the current question

Under recovery is the situation when the budgeted amount of overhead exceeds the actual

amount of indirect overhead and the over recovery is the scenario when budgeted

overhead is found less than the actual amount of overhead (Boghossian, 2017).

The major methods suggested for dealing with the scenario of the under or

overabsorption of overheads are

a. Charging the same to the cost of goods sold

The simplest method of dealing with such over or under absorption is to charge the

entire over or under recovery to the Cost of goods sold. It takes the least amount of

time to treat the same in this manner. If it is under recovery in such case it causes an

increase in the amount of cost of goods sold whereas if it is the case of over recovery,

then it brings down the amount of cost of goods sold (Cayon, et al., 2017).

b. Apportionment of such variation between finished goods, Work in progress and Raw

material

This method is little bit time consuming. Because it says that at the end of the

reporting period we need to know the balance remaining units of the Raw material,

Work in progress and the Finished goods. Then entire under or over recovery of

overheads is allocated amongst these three in the ratio of their remaining number of

balance units.

c. Charging of such variation to job

It is the most time taking method but considered as the best one as it takes us to root

of the actual costing system. As per this method those jobs that remain open during

the reporting period are being identified and the entire over or under recovery of the

overheads are allocated to such jobs (Coate & Mitschow, 2017). Over recovery being

a positive scenario shall cause a decrease in the specific amount of the cost of the job,

whereas under recovery shall increase the cost of the specific job.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

In the given case the best suited method to be suggested is the application of the third

method that is dividing the over or under recovered overheads on the specific jobs

that were remain open at the end of the reporting period.

5. Activity based allocation of manufacturing overhead and its suitability in the given case

Activity based costing is the substitute for the traditional method of the allocation of the

indirect manufacturing overhead that basically suggests the prevention of arbitrary

allocation of indirect overheads, but such allocation is to be made on a reasonable basis.

Under this method of cost allocation at first the activities of the organizations are

identified and then the next step to identify the cost of the products or the services

produced or rendered by the organization (Delone & Mclean, 2004). Finally, the

consumption of resources by these activities are identified. It recognizes the relationship

between the manufactured products or rendered services, their costs and the activities of

the organization. Here the activity is termed as cost driver such machine set up or the

purchase orders. The cost driver rate is calculated by dividing the total cost pool by the

cost driver. It is because the cost should first be assigned to the various activities due to

which these costs have been incurred. The next step is to assign the cost of these

activities only to those products or services which demand such activity. If an activity is

not demanded by any specific product or service, then o cost of such activity is to be

allocated to such product or service. This is the principle on which the activity-based

costing works (Hellmann, et al., 2019).

There are numerous reasons why activity-based costing has gained significant importance

now a days few of them are discussed hereunder:

1. There has been a significant increase in manufacturing overhead.

When we are talking about particularly the manufacture of a product in such case it is

the manufacturing overhead that consists of almost 60 to 70 percent of the total cost

of the product. Hence the most accurate estimation is demanded.

7 | P a g e

In the given case the best suited method to be suggested is the application of the third

method that is dividing the over or under recovered overheads on the specific jobs

that were remain open at the end of the reporting period.

5. Activity based allocation of manufacturing overhead and its suitability in the given case

Activity based costing is the substitute for the traditional method of the allocation of the

indirect manufacturing overhead that basically suggests the prevention of arbitrary

allocation of indirect overheads, but such allocation is to be made on a reasonable basis.

Under this method of cost allocation at first the activities of the organizations are

identified and then the next step to identify the cost of the products or the services

produced or rendered by the organization (Delone & Mclean, 2004). Finally, the

consumption of resources by these activities are identified. It recognizes the relationship

between the manufactured products or rendered services, their costs and the activities of

the organization. Here the activity is termed as cost driver such machine set up or the

purchase orders. The cost driver rate is calculated by dividing the total cost pool by the

cost driver. It is because the cost should first be assigned to the various activities due to

which these costs have been incurred. The next step is to assign the cost of these

activities only to those products or services which demand such activity. If an activity is

not demanded by any specific product or service, then o cost of such activity is to be

allocated to such product or service. This is the principle on which the activity-based

costing works (Hellmann, et al., 2019).

There are numerous reasons why activity-based costing has gained significant importance

now a days few of them are discussed hereunder:

1. There has been a significant increase in manufacturing overhead.

When we are talking about particularly the manufacture of a product in such case it is

the manufacturing overhead that consists of almost 60 to 70 percent of the total cost

of the product. Hence the most accurate estimation is demanded.

7 | P a g e

8

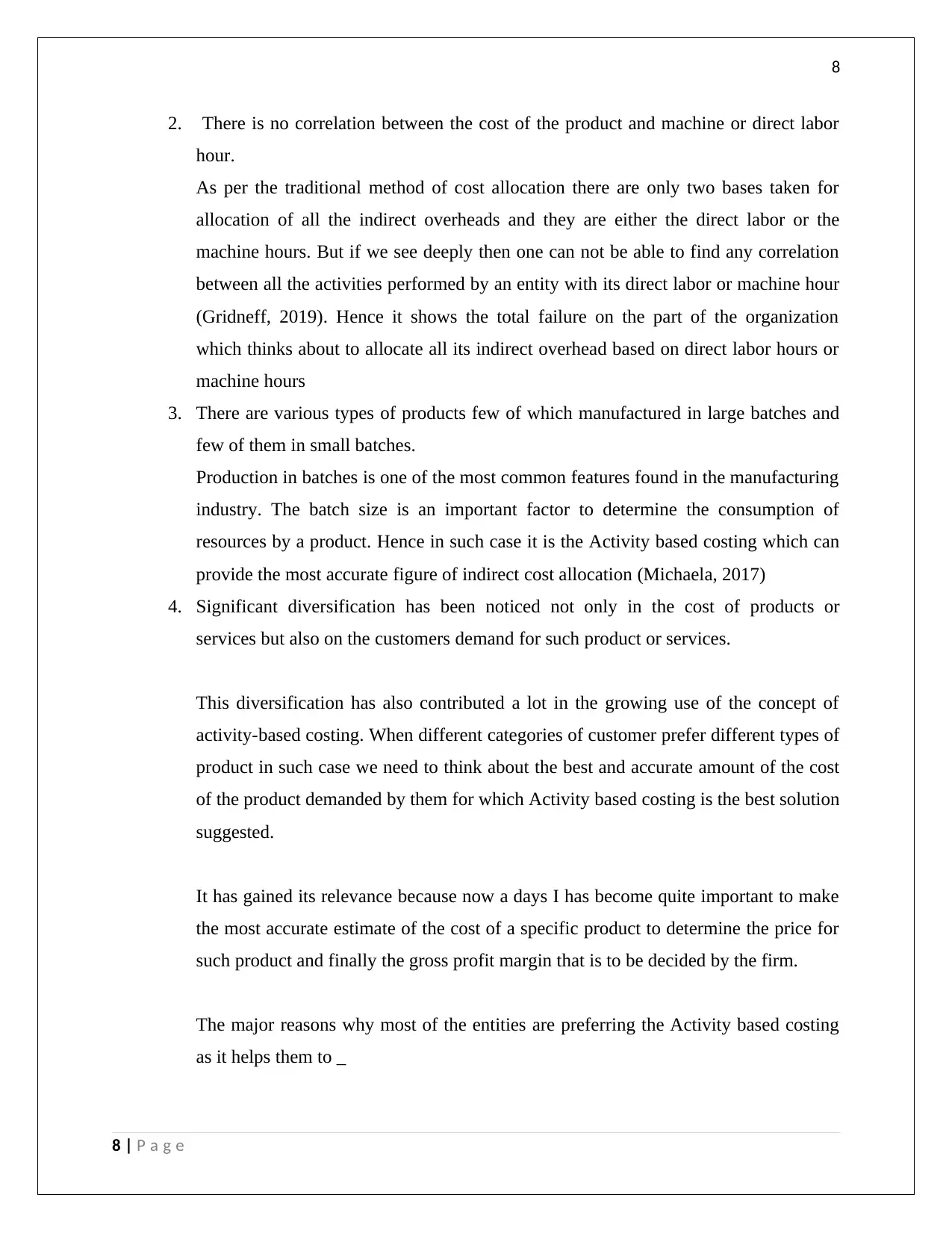

2. There is no correlation between the cost of the product and machine or direct labor

hour.

As per the traditional method of cost allocation there are only two bases taken for

allocation of all the indirect overheads and they are either the direct labor or the

machine hours. But if we see deeply then one can not be able to find any correlation

between all the activities performed by an entity with its direct labor or machine hour

(Gridneff, 2019). Hence it shows the total failure on the part of the organization

which thinks about to allocate all its indirect overhead based on direct labor hours or

machine hours

3. There are various types of products few of which manufactured in large batches and

few of them in small batches.

Production in batches is one of the most common features found in the manufacturing

industry. The batch size is an important factor to determine the consumption of

resources by a product. Hence in such case it is the Activity based costing which can

provide the most accurate figure of indirect cost allocation (Michaela, 2017)

4. Significant diversification has been noticed not only in the cost of products or

services but also on the customers demand for such product or services.

This diversification has also contributed a lot in the growing use of the concept of

activity-based costing. When different categories of customer prefer different types of

product in such case we need to think about the best and accurate amount of the cost

of the product demanded by them for which Activity based costing is the best solution

suggested.

It has gained its relevance because now a days I has become quite important to make

the most accurate estimate of the cost of a specific product to determine the price for

such product and finally the gross profit margin that is to be decided by the firm.

The major reasons why most of the entities are preferring the Activity based costing

as it helps them to _

8 | P a g e

2. There is no correlation between the cost of the product and machine or direct labor

hour.

As per the traditional method of cost allocation there are only two bases taken for

allocation of all the indirect overheads and they are either the direct labor or the

machine hours. But if we see deeply then one can not be able to find any correlation

between all the activities performed by an entity with its direct labor or machine hour

(Gridneff, 2019). Hence it shows the total failure on the part of the organization

which thinks about to allocate all its indirect overhead based on direct labor hours or

machine hours

3. There are various types of products few of which manufactured in large batches and

few of them in small batches.

Production in batches is one of the most common features found in the manufacturing

industry. The batch size is an important factor to determine the consumption of

resources by a product. Hence in such case it is the Activity based costing which can

provide the most accurate figure of indirect cost allocation (Michaela, 2017)

4. Significant diversification has been noticed not only in the cost of products or

services but also on the customers demand for such product or services.

This diversification has also contributed a lot in the growing use of the concept of

activity-based costing. When different categories of customer prefer different types of

product in such case we need to think about the best and accurate amount of the cost

of the product demanded by them for which Activity based costing is the best solution

suggested.

It has gained its relevance because now a days I has become quite important to make

the most accurate estimate of the cost of a specific product to determine the price for

such product and finally the gross profit margin that is to be decided by the firm.

The major reasons why most of the entities are preferring the Activity based costing

as it helps them to _

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

1. Eliminate the unnecessary costs from the production process

The meaning of unnecessary cost is those costs which are though incurred but

they don’t perceive any value in the minds of the customer or these are such costs

which can not be assumed to make any value addition to the product.

2. Eliminate the inefficient production process

Inefficient production process causes an increase in the cost incurred by the

enterprise because they cannot ensure the best utilization of the resources of

production. These are the inefficient way of doing or performing the job

3. Introducing most efficient method of cost allocation (Gridneff, 2019)

Once we need to introduce the most efficient way of performing activity then we

need to eliminate the inefficient way of doing the same. The is again a continuous

process in which ABC contributes in a most efficient way.

It aims to provide the valuable information to the management in relation to its

planning and decision-making activity. It is because activity-based costing does

not bring any major or drastic change in the structure of reporting of the financial

information, as it does the same thing as it is done by the traditional method for

allocation of the indirect method. What it simply does is to deal in a different way

of applying mathematics while determining the amount of indirect overheads.

Question 2

Whether Activity based costing can be applied in the case of Voltas Communication

In the case of volutes communication, we can see that there are basically four types of

indirect overheads exist and they are indirect material, indirect labor, utility and depreciation.

9 | P a g e

1. Eliminate the unnecessary costs from the production process

The meaning of unnecessary cost is those costs which are though incurred but

they don’t perceive any value in the minds of the customer or these are such costs

which can not be assumed to make any value addition to the product.

2. Eliminate the inefficient production process

Inefficient production process causes an increase in the cost incurred by the

enterprise because they cannot ensure the best utilization of the resources of

production. These are the inefficient way of doing or performing the job

3. Introducing most efficient method of cost allocation (Gridneff, 2019)

Once we need to introduce the most efficient way of performing activity then we

need to eliminate the inefficient way of doing the same. The is again a continuous

process in which ABC contributes in a most efficient way.

It aims to provide the valuable information to the management in relation to its

planning and decision-making activity. It is because activity-based costing does

not bring any major or drastic change in the structure of reporting of the financial

information, as it does the same thing as it is done by the traditional method for

allocation of the indirect method. What it simply does is to deal in a different way

of applying mathematics while determining the amount of indirect overheads.

Question 2

Whether Activity based costing can be applied in the case of Voltas Communication

In the case of volutes communication, we can see that there are basically four types of

indirect overheads exist and they are indirect material, indirect labor, utility and depreciation.

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

But for the application of the activity-based costing we need to have the cost drivers too. Cost

drivers are nothing but the identification of the activities due to which these costs have been

incurred. Depreciation can be allocated based on machine hours, indirect labor can be allocated

based on direct labor, similarly indirect material can be allocated based on the ratio of direct

labor amount and similarly utility too can be allocated on the same basis as the indirect labor was

allocated.

Hence in the given case it an be suggested that the Activity based costing shall be well suited for

the given case of Voltas Communication.

6.Calculation of the Value of Closing stock of Finished goods as on 30th June,2019

As in the given question it was clearly written that all the completed jobs except K12-009 have

been sold by the 30th June,2019, then it means it is only the cost of the K12-009 that was lying in

the stock. The cost of K12-009 has been calculated hereunder:

(All Figures are in $)

Direct Material 14000

Direct Labour 36000

Overheads 45000

Total value of Closing stock of Finished goods 95000

Overhead recovery rate = Total budgeted overhead/Budgeted machine Hours

10 | P a g e

But for the application of the activity-based costing we need to have the cost drivers too. Cost

drivers are nothing but the identification of the activities due to which these costs have been

incurred. Depreciation can be allocated based on machine hours, indirect labor can be allocated

based on direct labor, similarly indirect material can be allocated based on the ratio of direct

labor amount and similarly utility too can be allocated on the same basis as the indirect labor was

allocated.

Hence in the given case it an be suggested that the Activity based costing shall be well suited for

the given case of Voltas Communication.

6.Calculation of the Value of Closing stock of Finished goods as on 30th June,2019

As in the given question it was clearly written that all the completed jobs except K12-009 have

been sold by the 30th June,2019, then it means it is only the cost of the K12-009 that was lying in

the stock. The cost of K12-009 has been calculated hereunder:

(All Figures are in $)

Direct Material 14000

Direct Labour 36000

Overheads 45000

Total value of Closing stock of Finished goods 95000

Overhead recovery rate = Total budgeted overhead/Budgeted machine Hours

10 | P a g e

11

= 3600000/80000

=$45 per hour

Overheads = Machine hours* Overhead recovery rate

=1000*45

=$45000

Conclusion

From the above discussion and detailed calculation, it is quite evident that Job costing is

undoubtedly a major technique to ascertain the most accurate estimation of the cost associated

with a job. Though it has the drawback associated with it in the form of over or under recovery

of indirect manufacturing overhead but still it has suggested the three different ways of dealing

with such drawback. Again, if we are thinking about to make the best estimate of the indirect

cost of a manufactured product then in such a case Activity based costing is the best solution we

can opt for. It has proved itself by pinpointing the various loopholes found in the traditional

system of allocation of the indirect overhead. But at the same time, it is true too that every

manufacturing entity ma not be able to implement the activity-based costing due to significant

effort associated with its successful implementation. Hence one need to make a careful analysis

of the scenario present in one’s manufacturing entity before going to implement the same.

Further though the job costing method talks about the three different strategies of dealing the

situation of the under and over recovery of the indirect manufacturing cost, but each method so

not suitable for every type of industry. Some of these methods are easy to apply but other

methods are not only difficult but time consuming too. Hence it is often found that organizations

hesitate to use the concept of job costing.

11 | P a g e

= 3600000/80000

=$45 per hour

Overheads = Machine hours* Overhead recovery rate

=1000*45

=$45000

Conclusion

From the above discussion and detailed calculation, it is quite evident that Job costing is

undoubtedly a major technique to ascertain the most accurate estimation of the cost associated

with a job. Though it has the drawback associated with it in the form of over or under recovery

of indirect manufacturing overhead but still it has suggested the three different ways of dealing

with such drawback. Again, if we are thinking about to make the best estimate of the indirect

cost of a manufactured product then in such a case Activity based costing is the best solution we

can opt for. It has proved itself by pinpointing the various loopholes found in the traditional

system of allocation of the indirect overhead. But at the same time, it is true too that every

manufacturing entity ma not be able to implement the activity-based costing due to significant

effort associated with its successful implementation. Hence one need to make a careful analysis

of the scenario present in one’s manufacturing entity before going to implement the same.

Further though the job costing method talks about the three different strategies of dealing the

situation of the under and over recovery of the indirect manufacturing cost, but each method so

not suitable for every type of industry. Some of these methods are easy to apply but other

methods are not only difficult but time consuming too. Hence it is often found that organizations

hesitate to use the concept of job costing.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.