Financial Performance Evaluation: A Comparative Study of VS & SKP

VerifiedAdded on 2023/06/09

|26

|4450

|468

Report

AI Summary

This report provides a detailed financial analysis comparing V.S. Industry Berhad (VS) and SKP Resources Berhad over five years (2013-2017). It utilizes various financial ratios, including profitability, liquidity, efficiency, solvency, and investor ratios, to assess and compare their financial performance. The analysis identifies strategic and operational issues for both companies, offering recommendations for improvement. Key findings include fluctuating profitability trends, varying liquidity positions, and efficiency differences in inventory management. The report also addresses the limitations of ratio analysis and provides suggestions for a more comprehensive evaluation. Desklib offers this report as a resource for students, alongside a wide array of study tools, solved assignments, and past papers.

Running head: FINANCIAL ANALYSIS

Financial analysis

Name of the student

Name of the university

Student ID

Author note

Financial analysis

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ANALYSIS

Table of Contents

1.0 Introduction..........................................................................................................................4

2.0 Background of v.s. industry Berhad (vs).............................................................................5

2.1 Nature of core business....................................................................................................5

2.2 Future Outlook.................................................................................................................5

2.3 Key Challenges................................................................................................................5

3.0 Relative position in the industry..........................................................................................6

4.0 Ratios analysis of financial performance of VS vs SKP......................................................6

4.1 Background to ratio analysis............................................................................................6

4.2 Rationale for selecting VS and SKP for comparison.......................................................7

4.3 Profitability Analysis.......................................................................................................7

4.3.1 Background...................................................................................................................7

4.3.2 Table of Profitability ratios...........................................................................................8

4.3.3 Line Graph....................................................................................................................8

4.3.4 Interpretation...............................................................................................................10

4.4 Liquidity Analysis..........................................................................................................11

4.4.1 Background.................................................................................................................11

4.4.2 Table of Liquidity Analysis....................................................................................11

4.4.3 Line Graph..................................................................................................................12

4.4.4 Interpretations.............................................................................................................12

Table of Contents

1.0 Introduction..........................................................................................................................4

2.0 Background of v.s. industry Berhad (vs).............................................................................5

2.1 Nature of core business....................................................................................................5

2.2 Future Outlook.................................................................................................................5

2.3 Key Challenges................................................................................................................5

3.0 Relative position in the industry..........................................................................................6

4.0 Ratios analysis of financial performance of VS vs SKP......................................................6

4.1 Background to ratio analysis............................................................................................6

4.2 Rationale for selecting VS and SKP for comparison.......................................................7

4.3 Profitability Analysis.......................................................................................................7

4.3.1 Background...................................................................................................................7

4.3.2 Table of Profitability ratios...........................................................................................8

4.3.3 Line Graph....................................................................................................................8

4.3.4 Interpretation...............................................................................................................10

4.4 Liquidity Analysis..........................................................................................................11

4.4.1 Background.................................................................................................................11

4.4.2 Table of Liquidity Analysis....................................................................................11

4.4.3 Line Graph..................................................................................................................12

4.4.4 Interpretations.............................................................................................................12

2FINANCIAL ANALYSIS

4.5 Efficiency Analysis........................................................................................................13

4.5.1 Background.................................................................................................................13

4.5.2 Table of Efficiency Ratio............................................................................................13

4.5.3 Line Graph..................................................................................................................14

4.5.4 Interpretation...............................................................................................................15

4.6 Solvency Analysis..........................................................................................................16

4.6.1 Background.................................................................................................................16

4.6.2 Table of Solvency ratios...........................................................................................16

4.6.3 Line Graph..................................................................................................................17

4.6.4 Interpretation...............................................................................................................17

4.7 Investors Analysis..........................................................................................................18

4.7.1 Background.................................................................................................................18

4.7.2 Table of Investors Ratios............................................................................................19

4.7.3 Line Graph..................................................................................................................19

4.7.4 Interpretation...............................................................................................................21

5.0 Identification of strategic and operational issues and recommendations...........................22

5.1 Profitability....................................................................................................................22

5.1.1 Strategic issue..............................................................................................................22

5.1.2 Recommendation.........................................................................................................22

5.2 Gearing strategy.............................................................................................................22

5.2.1 Problem.......................................................................................................................22

4.5 Efficiency Analysis........................................................................................................13

4.5.1 Background.................................................................................................................13

4.5.2 Table of Efficiency Ratio............................................................................................13

4.5.3 Line Graph..................................................................................................................14

4.5.4 Interpretation...............................................................................................................15

4.6 Solvency Analysis..........................................................................................................16

4.6.1 Background.................................................................................................................16

4.6.2 Table of Solvency ratios...........................................................................................16

4.6.3 Line Graph..................................................................................................................17

4.6.4 Interpretation...............................................................................................................17

4.7 Investors Analysis..........................................................................................................18

4.7.1 Background.................................................................................................................18

4.7.2 Table of Investors Ratios............................................................................................19

4.7.3 Line Graph..................................................................................................................19

4.7.4 Interpretation...............................................................................................................21

5.0 Identification of strategic and operational issues and recommendations...........................22

5.1 Profitability....................................................................................................................22

5.1.1 Strategic issue..............................................................................................................22

5.1.2 Recommendation.........................................................................................................22

5.2 Gearing strategy.............................................................................................................22

5.2.1 Problem.......................................................................................................................22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ANALYSIS

5.2.3 Recommendation.........................................................................................................22

6.0 Limitation analysis.............................................................................................................23

6.1 Limitation of ratio analysis............................................................................................23

6.2 Recommendation............................................................................................................23

Reference..................................................................................................................................24

5.2.3 Recommendation.........................................................................................................22

6.0 Limitation analysis.............................................................................................................23

6.1 Limitation of ratio analysis............................................................................................23

6.2 Recommendation............................................................................................................23

Reference..................................................................................................................................24

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ANALYSIS

1.0 Introduction

Main objective of the report is to focus on the financial performance and position of

V.S. Industry Berhad (VS) agisnt SKP Resources Berhad (SKP) for the last 5 years that is

from 2013 to 2017. For the purpose of analysis various ratios like profitability ratios, liquidity

ratios, efficiency ratios, solvency ratios and investor’s ratios. Further, the report will identify

the operational and strategic issues of both the companies and will provide recommendations

based on the findings. Finally, the report will provide the limitations of ratio analysis.

V.S. Industry Berhad is the Malaysian company that operates under electronic

components sector. It is an investment holding company that assembles, manufactures and

sells the electrical and electronic products, plastic molded parts and components in Malaysia,

Europe, Indonesia and various other countries. Various manufacturing solutions provided by

the company includes mold design, fabrication services, product design, electronics, final

assembly, testing and services related to supply chain management (Vs-i.com 2018).

On the other hand, SKP Resources Berhad is the investment holding company and is

engaged in delivering management services to the subsidiaries. Further, the company is

engaged in sub-assembly of electrical and electronic equipments and various other secondary

processes. It offers wide range of products that includes video accessories, computer

accessories, audio accessories and various other miscellaneous accessories (Skpres.com

2018).

1.0 Introduction

Main objective of the report is to focus on the financial performance and position of

V.S. Industry Berhad (VS) agisnt SKP Resources Berhad (SKP) for the last 5 years that is

from 2013 to 2017. For the purpose of analysis various ratios like profitability ratios, liquidity

ratios, efficiency ratios, solvency ratios and investor’s ratios. Further, the report will identify

the operational and strategic issues of both the companies and will provide recommendations

based on the findings. Finally, the report will provide the limitations of ratio analysis.

V.S. Industry Berhad is the Malaysian company that operates under electronic

components sector. It is an investment holding company that assembles, manufactures and

sells the electrical and electronic products, plastic molded parts and components in Malaysia,

Europe, Indonesia and various other countries. Various manufacturing solutions provided by

the company includes mold design, fabrication services, product design, electronics, final

assembly, testing and services related to supply chain management (Vs-i.com 2018).

On the other hand, SKP Resources Berhad is the investment holding company and is

engaged in delivering management services to the subsidiaries. Further, the company is

engaged in sub-assembly of electrical and electronic equipments and various other secondary

processes. It offers wide range of products that includes video accessories, computer

accessories, audio accessories and various other miscellaneous accessories (Skpres.com

2018).

5FINANCIAL ANALYSIS

2.0 Background of v.s. industry Berhad (vs)

V.S. Industry Berhad (VS) was founded in 1982 and listed on the Main Market of

Stock Exchange Malaysia in 1998. VS has been classified in the Industrial Products sector.

2.1 Nature of core business

The company’s principal activities are manufacturing, assembling and sale of

electronic and electrical products and plastic moulded components and parts such as speakers

and remote controls. It also markets, distributes, and sells plastic household products. VS also

operates a palm oil plantation. Geographically the company is spread across Malaysia, United

States of America, Europe, Indonesia and Taiwan.

2.2 Future Outlook

VS is a global leader in integrated Electronics Manufacturing Services (EMS) for

office and household electrical and electronic products. In the EMS sector, the rapid pace of

globalization and technological adoptions, as well as innovation-led product replacements,

are expected to fuel growth in manufacturing activity. Increasing collaboration between brand

owners and manufacturing partners in crucial phases of product development and delivery

will be ongoing. Therefore, EMS players with in-house R&D as well as integrated global

supply chain expertise, are well-positioned to gain an upper hand.

2.3 Key Challenges

Operating environment remains challenging such as rising cost of materials,

escalating wages and utility costs, fluctuation in currency exchange, juggling human

resources especially on the production floors and talent engineer. Also, balancing between

costs down pressures from customers and managing upward cost increase remain as key

challenge.

2.0 Background of v.s. industry Berhad (vs)

V.S. Industry Berhad (VS) was founded in 1982 and listed on the Main Market of

Stock Exchange Malaysia in 1998. VS has been classified in the Industrial Products sector.

2.1 Nature of core business

The company’s principal activities are manufacturing, assembling and sale of

electronic and electrical products and plastic moulded components and parts such as speakers

and remote controls. It also markets, distributes, and sells plastic household products. VS also

operates a palm oil plantation. Geographically the company is spread across Malaysia, United

States of America, Europe, Indonesia and Taiwan.

2.2 Future Outlook

VS is a global leader in integrated Electronics Manufacturing Services (EMS) for

office and household electrical and electronic products. In the EMS sector, the rapid pace of

globalization and technological adoptions, as well as innovation-led product replacements,

are expected to fuel growth in manufacturing activity. Increasing collaboration between brand

owners and manufacturing partners in crucial phases of product development and delivery

will be ongoing. Therefore, EMS players with in-house R&D as well as integrated global

supply chain expertise, are well-positioned to gain an upper hand.

2.3 Key Challenges

Operating environment remains challenging such as rising cost of materials,

escalating wages and utility costs, fluctuation in currency exchange, juggling human

resources especially on the production floors and talent engineer. Also, balancing between

costs down pressures from customers and managing upward cost increase remain as key

challenge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ANALYSIS

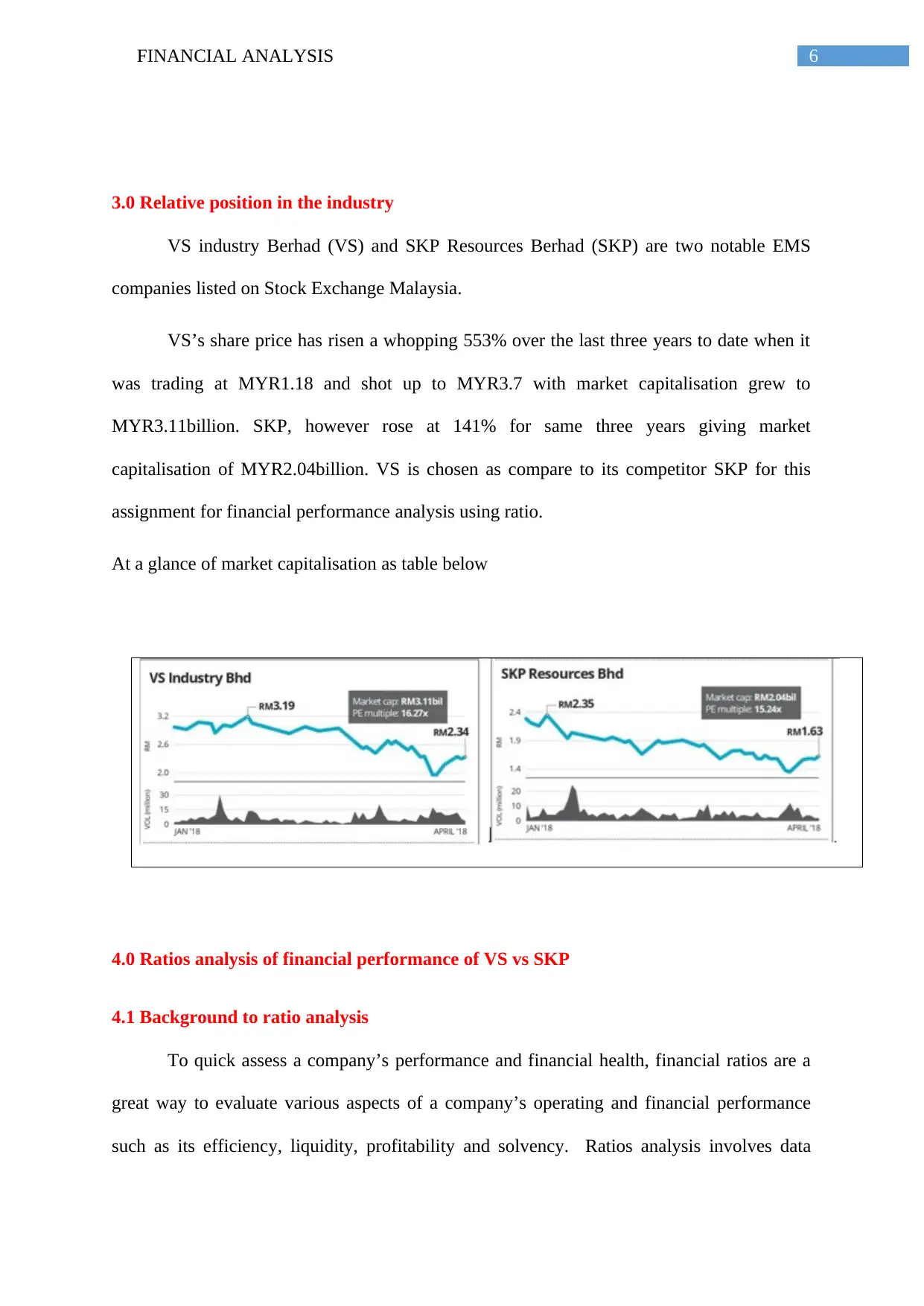

3.0 Relative position in the industry

VS industry Berhad (VS) and SKP Resources Berhad (SKP) are two notable EMS

companies listed on Stock Exchange Malaysia.

VS’s share price has risen a whopping 553% over the last three years to date when it

was trading at MYR1.18 and shot up to MYR3.7 with market capitalisation grew to

MYR3.11billion. SKP, however rose at 141% for same three years giving market

capitalisation of MYR2.04billion. VS is chosen as compare to its competitor SKP for this

assignment for financial performance analysis using ratio.

At a glance of market capitalisation as table below

4.0 Ratios analysis of financial performance of VS vs SKP

4.1 Background to ratio analysis

To quick assess a company’s performance and financial health, financial ratios are a

great way to evaluate various aspects of a company’s operating and financial performance

such as its efficiency, liquidity, profitability and solvency. Ratios analysis involves data

3.0 Relative position in the industry

VS industry Berhad (VS) and SKP Resources Berhad (SKP) are two notable EMS

companies listed on Stock Exchange Malaysia.

VS’s share price has risen a whopping 553% over the last three years to date when it

was trading at MYR1.18 and shot up to MYR3.7 with market capitalisation grew to

MYR3.11billion. SKP, however rose at 141% for same three years giving market

capitalisation of MYR2.04billion. VS is chosen as compare to its competitor SKP for this

assignment for financial performance analysis using ratio.

At a glance of market capitalisation as table below

4.0 Ratios analysis of financial performance of VS vs SKP

4.1 Background to ratio analysis

To quick assess a company’s performance and financial health, financial ratios are a

great way to evaluate various aspects of a company’s operating and financial performance

such as its efficiency, liquidity, profitability and solvency. Ratios analysis involves data

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ANALYSIS

retrieved from current and historical financial statements to access whether the company is

improving or deteriorating; or can be used to judge a company’s performance against other at

similarly-situated companies.

4.2 Rationale for selecting VS and SKP for comparison

VS is one of the top 50 EMS corporation in the world, with in-house printed circuit

board (PCB) and battery-pack assembly capabilities to provide one-stop manufacturing

solution to its clients. SKP is one of the fastest-growing integrated contract manufacturers,

catering for the electrical and electronics, industrials, automotive and food & beverage

industries. It also has better manufacturing capabilities. SKP’s in-house assembly capability

is coming in place, rivalling that of VS. Both companies delivered strong financial

performance in the past 3-5 financial years. Simply put, they are friendly competitors.

4.3 Profitability Analysis

4.3.1 Background

All the entities are concerned regarding their profitability and the profitability of the

company are analysed through various profitability ratios like net profit margin, gross profit

margin, return on assets and return on equity. These ratios state the ability of the company to

transform its sales into profit at different measurement stages. Further the return ratios

indicate the ability of the company to measure its overall efficiencies with regard to

generation of returns for the shareholders (Vogel 2014).

retrieved from current and historical financial statements to access whether the company is

improving or deteriorating; or can be used to judge a company’s performance against other at

similarly-situated companies.

4.2 Rationale for selecting VS and SKP for comparison

VS is one of the top 50 EMS corporation in the world, with in-house printed circuit

board (PCB) and battery-pack assembly capabilities to provide one-stop manufacturing

solution to its clients. SKP is one of the fastest-growing integrated contract manufacturers,

catering for the electrical and electronics, industrials, automotive and food & beverage

industries. It also has better manufacturing capabilities. SKP’s in-house assembly capability

is coming in place, rivalling that of VS. Both companies delivered strong financial

performance in the past 3-5 financial years. Simply put, they are friendly competitors.

4.3 Profitability Analysis

4.3.1 Background

All the entities are concerned regarding their profitability and the profitability of the

company are analysed through various profitability ratios like net profit margin, gross profit

margin, return on assets and return on equity. These ratios state the ability of the company to

transform its sales into profit at different measurement stages. Further the return ratios

indicate the ability of the company to measure its overall efficiencies with regard to

generation of returns for the shareholders (Vogel 2014).

8FINANCIAL ANALYSIS

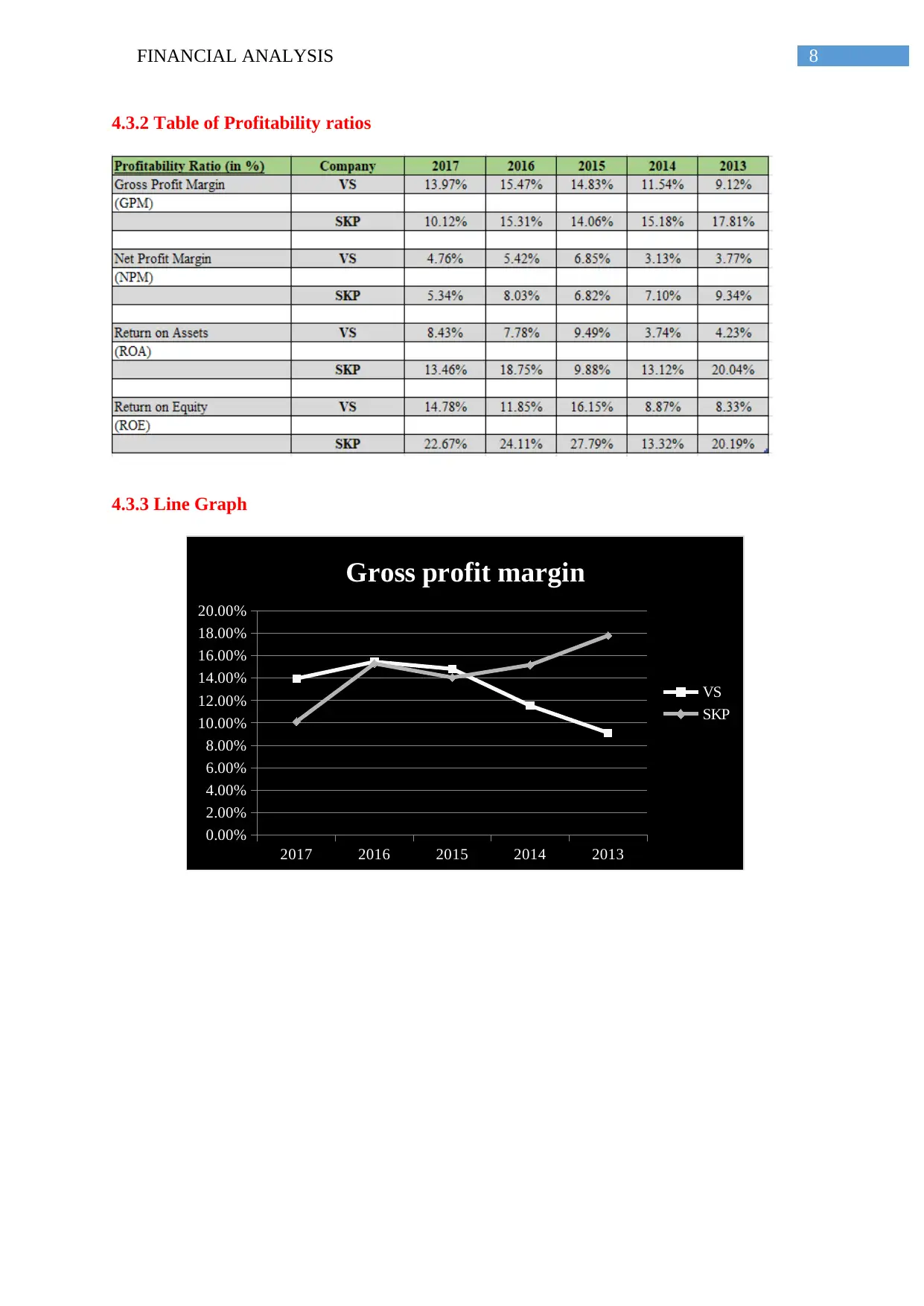

4.3.2 Table of Profitability ratios

4.3.3 Line Graph

2017 2016 2015 2014 2013

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

Gross profit margin

VS

SKP

4.3.2 Table of Profitability ratios

4.3.3 Line Graph

2017 2016 2015 2014 2013

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

Gross profit margin

VS

SKP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ANALYSIS

2017 2016 2015 2014 2013

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

Net profit margin

VS

SKP

2017 2016 2015 2014 2013

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Return on Asset

VS

SKP

2017 2016 2015 2014 2013

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Return on equity

VS

SKP

2017 2016 2015 2014 2013

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

Net profit margin

VS

SKP

2017 2016 2015 2014 2013

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Return on Asset

VS

SKP

2017 2016 2015 2014 2013

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Return on equity

VS

SKP

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ANALYSIS

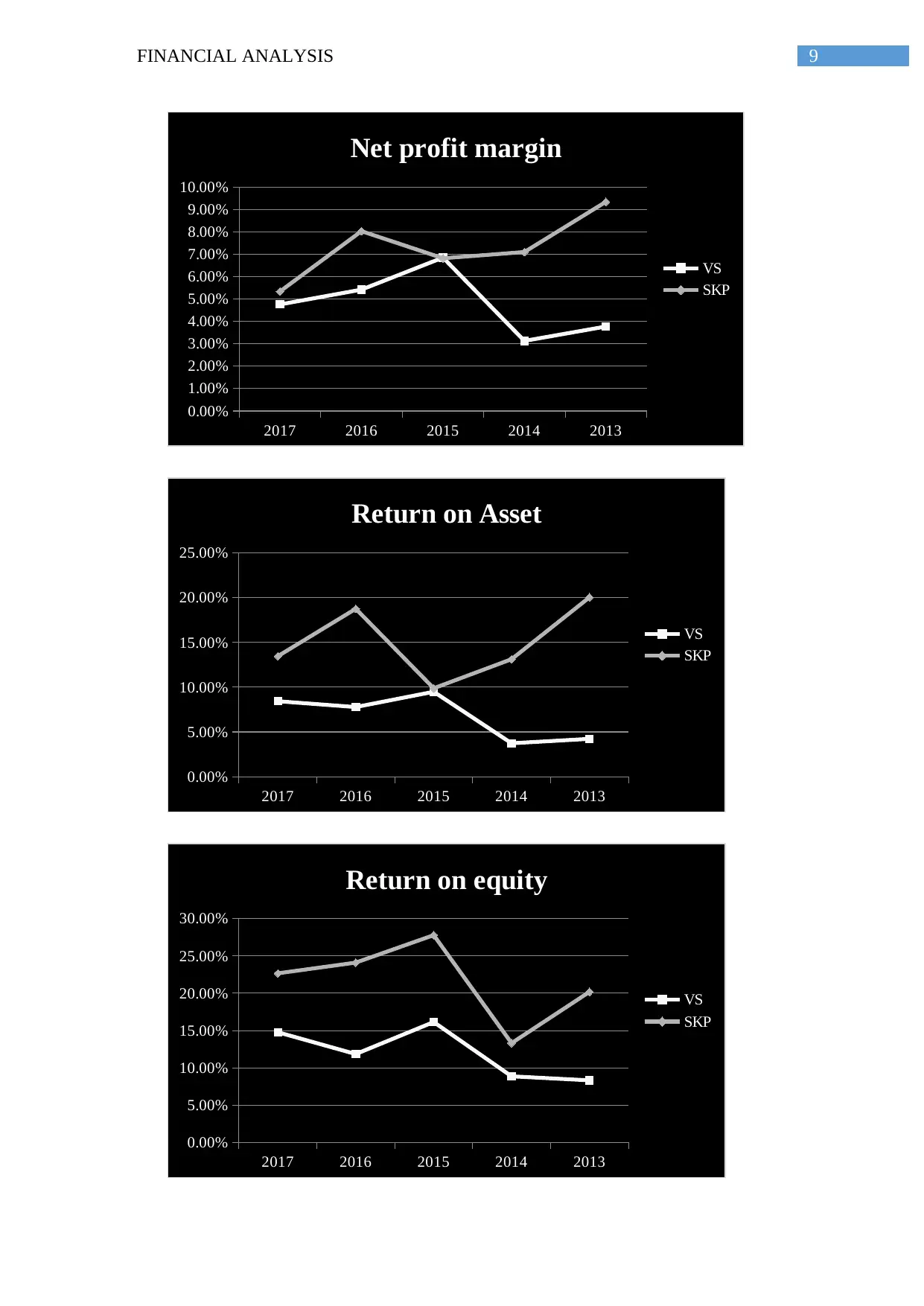

4.3.4 Interpretation

Gross profit margin of the company is the profitability metrics that is used for

assessing the financial health of the company through measuring the percentage of revenue

left with the company after paying off the cost for goods sold. If the company does not

possess sufficient gross margin it will not be able to meet its operational expenses efficiently.

Looking into the gross profit margin of VS as well as SKP it can be identified that the till

2016 the ratio for VS is in increasing trend and in 2017 it reduced to 13.97% from 15.47%.

On the other hand, the gross margin of SKP till 2015 was in reducing trend. However, it 2016

it increased from 14.06% to 15.31% and again reduced to 10.12% in 2017 (Sarlin 2015).

The net profit margin of the company is the profitability metrics that is used for

assessing the financial health of the company through measuring the percentage of revenue

left with the company after paying off all the operating expenses including the financial

expenses and tax expenses. Looking into the net profit margin of both the companies it can be

stated that the net profit of both the companies are fluctuating and have no particular trend.

Whereas the net profit of VS has increased from 3.77% to 4.76%, the net profit margin of

SKP has been reduced from 9.34% to 5.34% over the last 5 year period. However, the net

profitability position of SKP is better as compared to that of VS.

Return on assets indicates the profitability of the company as against its total assets. It

measures the ability of the company to generate income through deploying its assets. It can

be identified that the return on assets of VS is in increasing trend and it increased from 4.23%

to 8.43% over the last 5 years. On the other hand, the return on assets for SKP is in reducing

trend and it reduced to 13.46% from 20.04%. However, if both the companies are compared

4.3.4 Interpretation

Gross profit margin of the company is the profitability metrics that is used for

assessing the financial health of the company through measuring the percentage of revenue

left with the company after paying off the cost for goods sold. If the company does not

possess sufficient gross margin it will not be able to meet its operational expenses efficiently.

Looking into the gross profit margin of VS as well as SKP it can be identified that the till

2016 the ratio for VS is in increasing trend and in 2017 it reduced to 13.97% from 15.47%.

On the other hand, the gross margin of SKP till 2015 was in reducing trend. However, it 2016

it increased from 14.06% to 15.31% and again reduced to 10.12% in 2017 (Sarlin 2015).

The net profit margin of the company is the profitability metrics that is used for

assessing the financial health of the company through measuring the percentage of revenue

left with the company after paying off all the operating expenses including the financial

expenses and tax expenses. Looking into the net profit margin of both the companies it can be

stated that the net profit of both the companies are fluctuating and have no particular trend.

Whereas the net profit of VS has increased from 3.77% to 4.76%, the net profit margin of

SKP has been reduced from 9.34% to 5.34% over the last 5 year period. However, the net

profitability position of SKP is better as compared to that of VS.

Return on assets indicates the profitability of the company as against its total assets. It

measures the ability of the company to generate income through deploying its assets. It can

be identified that the return on assets of VS is in increasing trend and it increased from 4.23%

to 8.43% over the last 5 years. On the other hand, the return on assets for SKP is in reducing

trend and it reduced to 13.46% from 20.04%. However, if both the companies are compared

11FINANCIAL ANALYSIS

it can be stated that the performance of SKP is better as compared to VS (Heikal, Khaddafi

and Ummah 2014).

Return on equity measures the ability of the company to generate income through

deploying its shareholder’s equity. It can be recognized that both the company’s return on

equity are in increasing trend. Whereas the ROE of VS has increased from 8.33% to 14.78%,

the return on equity of SKP has been increased from 20.19% to 22.67% over the last 5 year

period. However, if both the companies are compared it can be stated that the performance of

SKP is better as compared to VS.

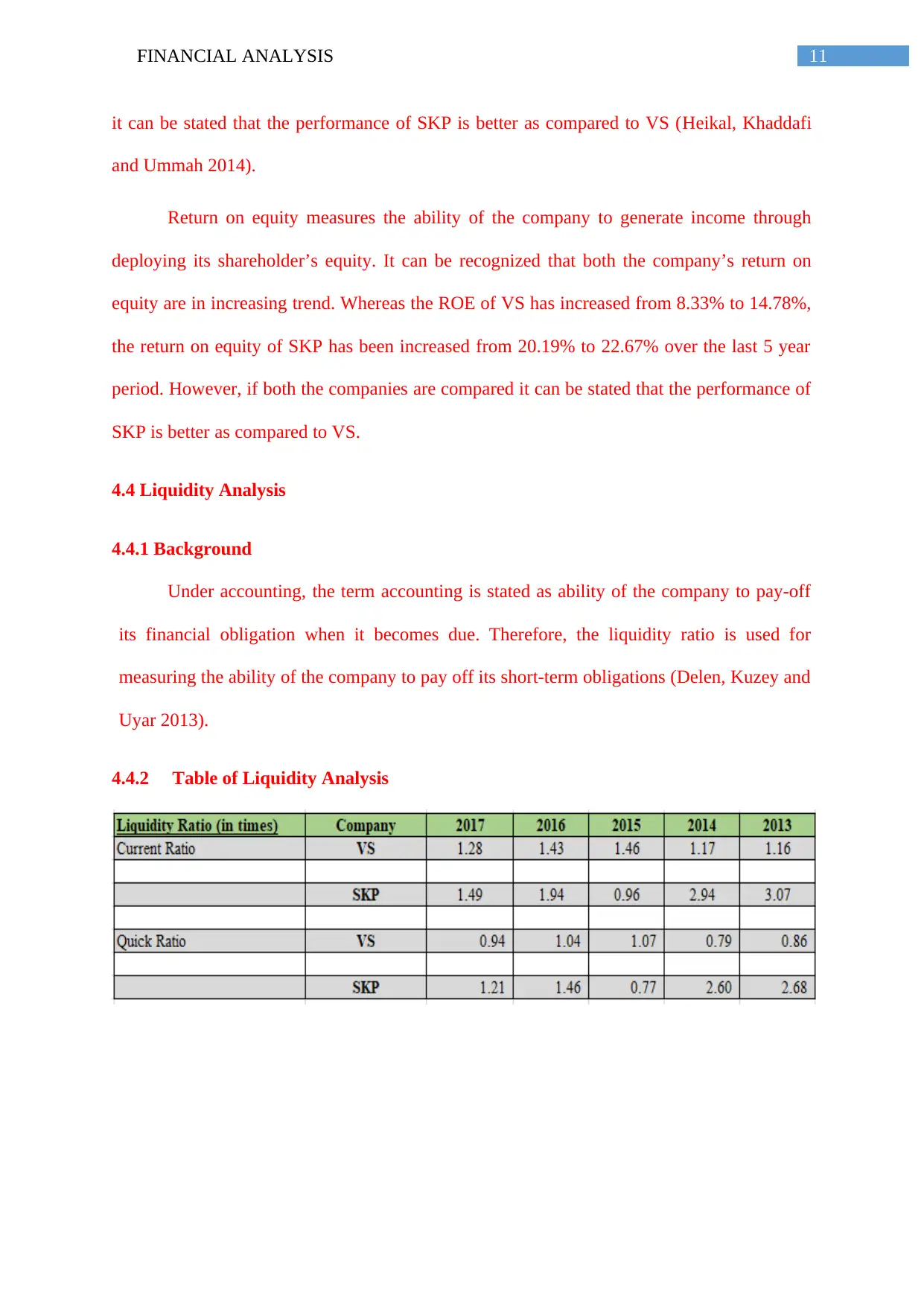

4.4 Liquidity Analysis

4.4.1 Background

Under accounting, the term accounting is stated as ability of the company to pay-off

its financial obligation when it becomes due. Therefore, the liquidity ratio is used for

measuring the ability of the company to pay off its short-term obligations (Delen, Kuzey and

Uyar 2013).

4.4.2 Table of Liquidity Analysis

it can be stated that the performance of SKP is better as compared to VS (Heikal, Khaddafi

and Ummah 2014).

Return on equity measures the ability of the company to generate income through

deploying its shareholder’s equity. It can be recognized that both the company’s return on

equity are in increasing trend. Whereas the ROE of VS has increased from 8.33% to 14.78%,

the return on equity of SKP has been increased from 20.19% to 22.67% over the last 5 year

period. However, if both the companies are compared it can be stated that the performance of

SKP is better as compared to VS.

4.4 Liquidity Analysis

4.4.1 Background

Under accounting, the term accounting is stated as ability of the company to pay-off

its financial obligation when it becomes due. Therefore, the liquidity ratio is used for

measuring the ability of the company to pay off its short-term obligations (Delen, Kuzey and

Uyar 2013).

4.4.2 Table of Liquidity Analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.