Detailed Financial Analysis: WACC, NPV, and Project Evaluation

VerifiedAdded on 2023/06/11

|7

|974

|130

Report

AI Summary

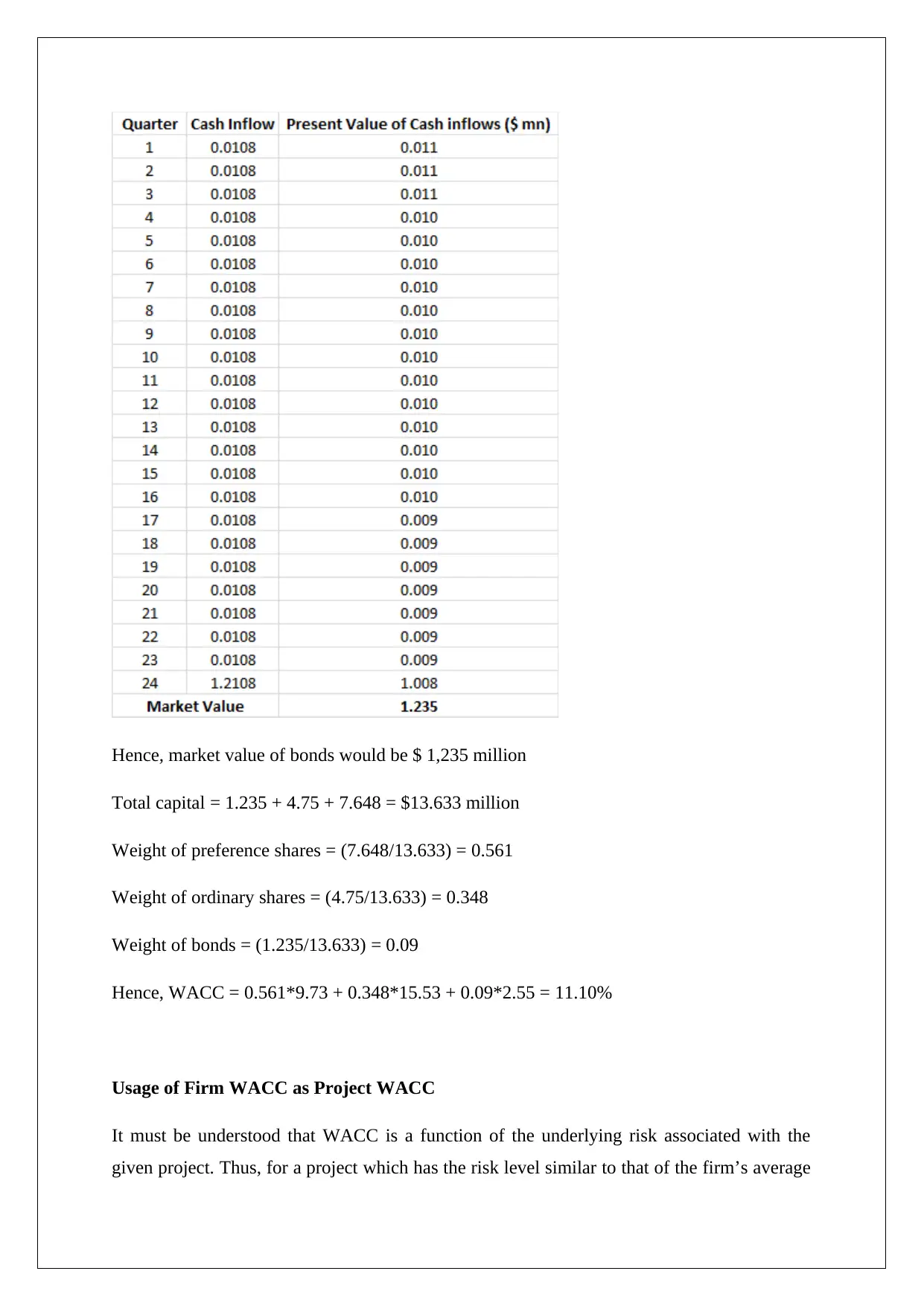

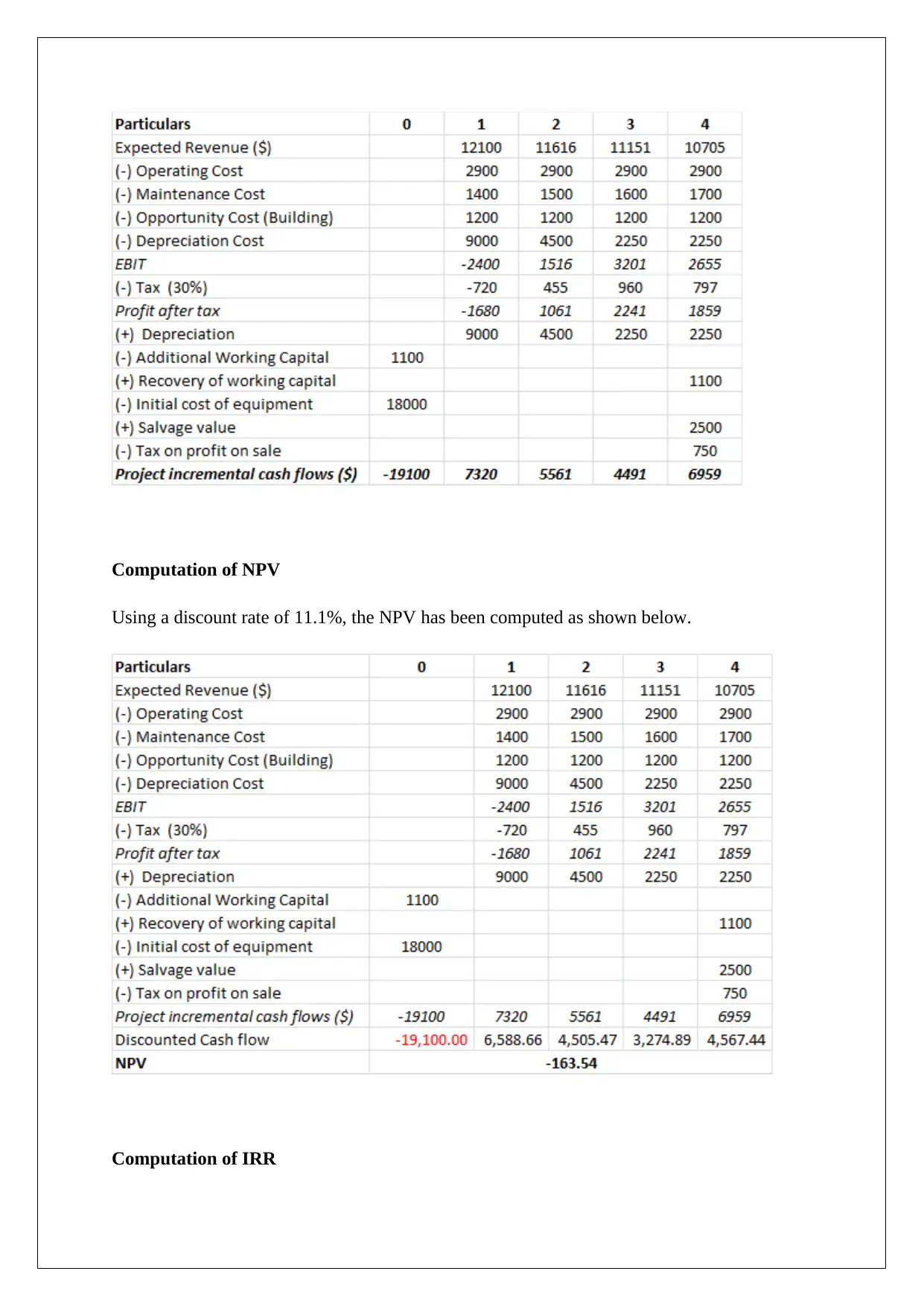

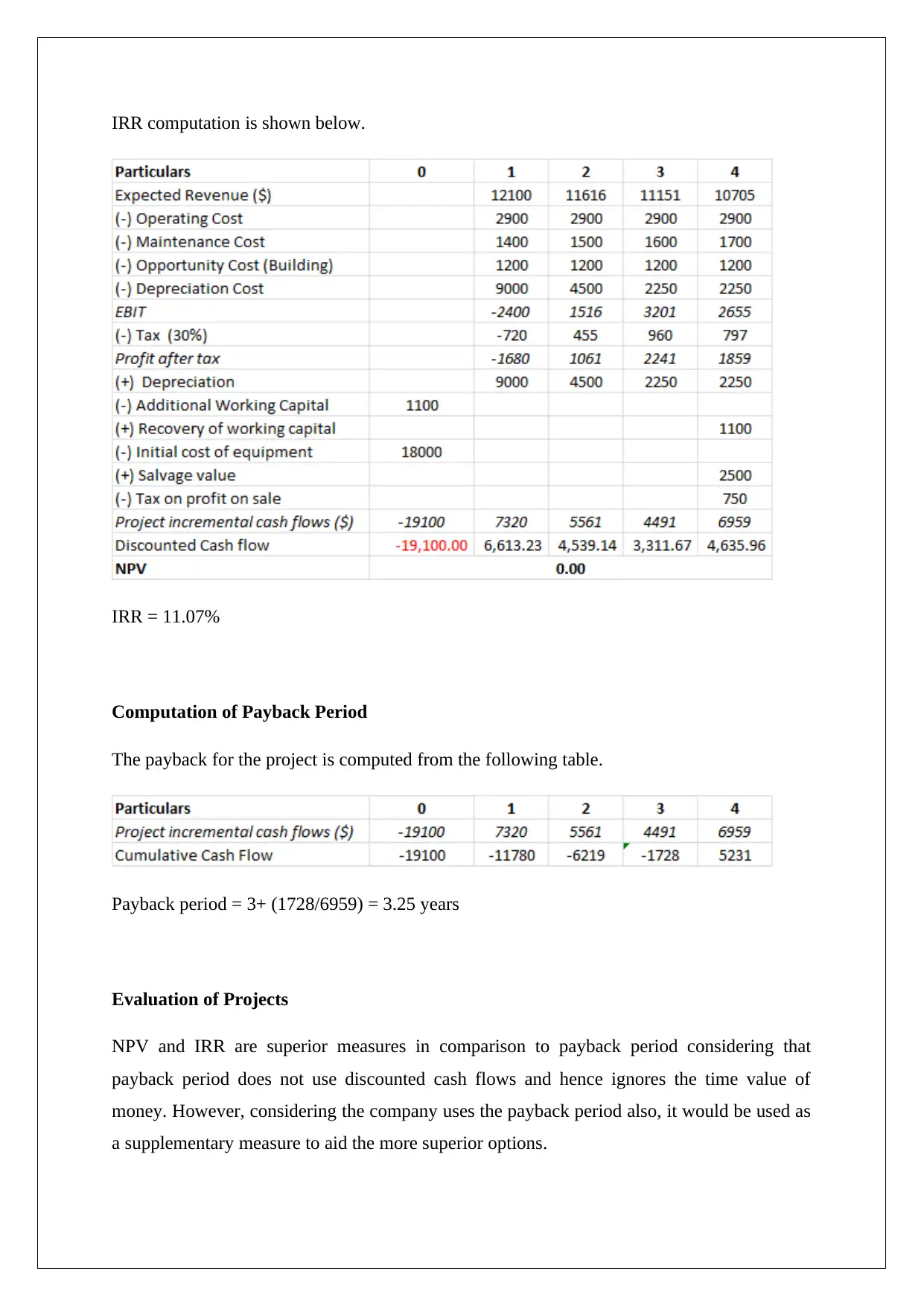

This report provides a detailed analysis of a company's Weighted Average Cost of Capital (WACC) and its application in evaluating a specific project. The WACC is calculated considering the cost of preference shares, equity shares (using the CAPM model), and bonds. Market values of these components are determined using methods like the Gordon dividend model and bond valuation techniques. The report then evaluates a project, taking into account relevant details like sunk costs, depreciation, opportunity costs, and terminal value taxation. Key metrics such as Net Present Value (NPV), Internal Rate of Return (IRR), and payback period are computed. Based on these calculations, the report recommends rejecting the project due to its negative NPV, IRR lower than the discount rate, and a payback period exceeding the company's threshold. Desklib offers this and many other solved assignments for students.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.