Analysis of WACC for Australian Companies and Decision Making

VerifiedAdded on 2023/06/07

|5

|1428

|421

Report

AI Summary

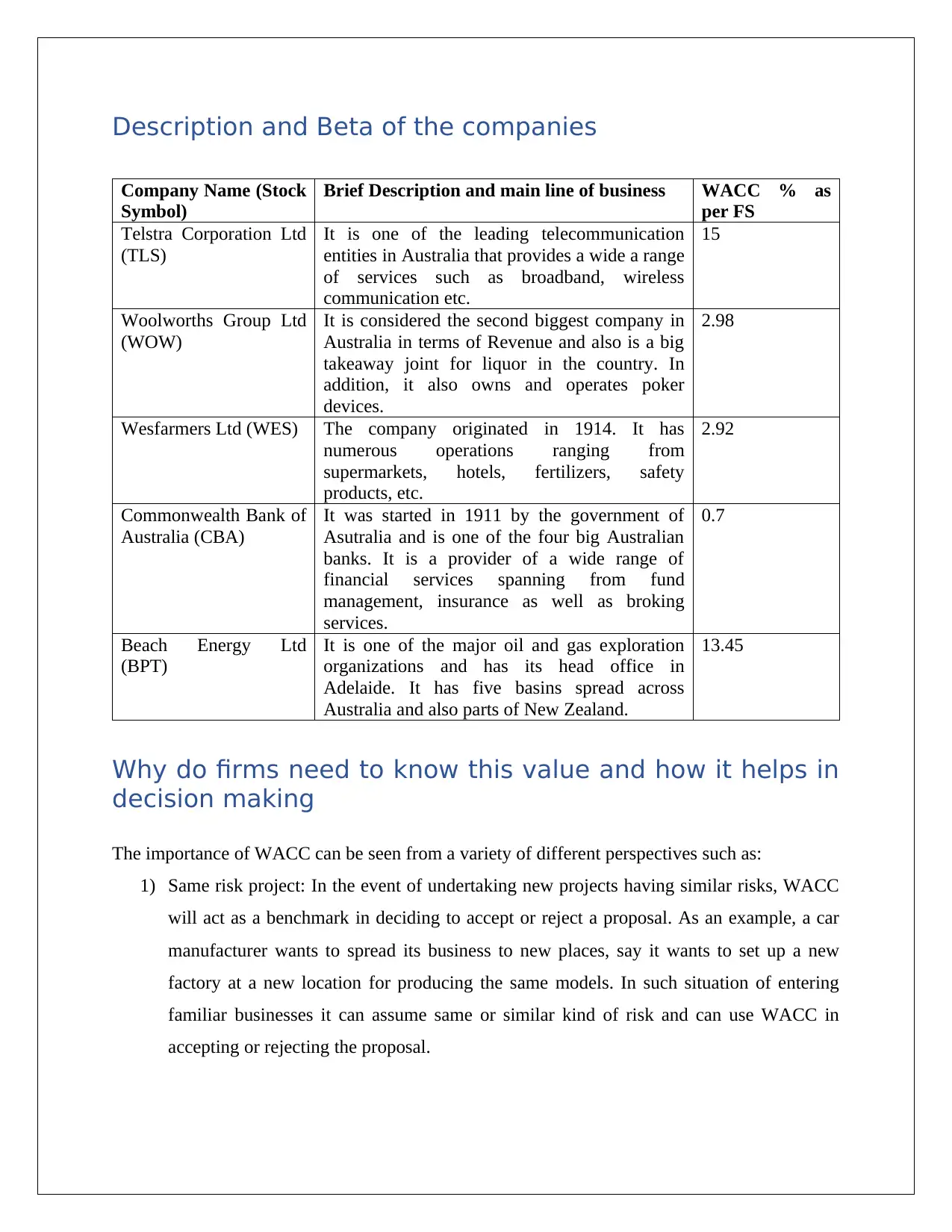

This report provides a detailed analysis of the Weighted Average Cost of Capital (WACC) and its application in financial decision-making. It begins with a table of contents and descriptions of several Australian companies, including Telstra, Woolworths, Wesfarmers, Commonwealth Bank, and Beach Energy, along with their stock symbols and brief business descriptions. The report explains the WACC computation process, outlining the three key steps: calculating the cost of capital components (debt and equity), determining the proportion of debt and equity in the company's capital structure, and weighing the cost of each capital form. It also explains why firms need to know the WACC and how it aids in decision-making, such as evaluating new projects with similar or different risks and computing Net Present Value (NPV). Furthermore, the report delves into the determination of WACC components, including risk-free return, market return, and beta. The report also discusses why WACC differs among companies, primarily due to variations in debt-to-equity ratios, beta, and other risk factors. Finally, the report includes a list of references used in its preparation.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.