Nufarm Limited: Weighted Average Cost of Capital and Gearing Analysis

VerifiedAdded on 2022/11/14

|15

|3358

|124

Report

AI Summary

This report presents a comprehensive financial analysis of Nufarm Limited, focusing on its capital structure for the financial year 2018. It begins with the calculation of the Weighted Average Cost of Capital (WACC) using the Capital Asset Pricing Model (CAPM) to estimate the cost of equity and incorporating the cost of debt. The report details the estimation of key components, including the risk-free rate, market risk premium, and beta, drawing data from the Reserve Bank of Australia, ASX200 index, and Morningstar. Following the WACC calculation, the report calculates and analyzes Nufarm Limited's gearing ratios, including the debt-to-equity and interest coverage ratios, providing insights into the company's financial leverage. The analysis then applies capital structure theory to interpret the findings and concludes with recommendations to the board for optimizing the capital structure. The report also includes a reflection on the overall work performed and is supported by relevant references.

1

Capital Structure of Nufarm Limited

Capital Structure of Nufarm Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

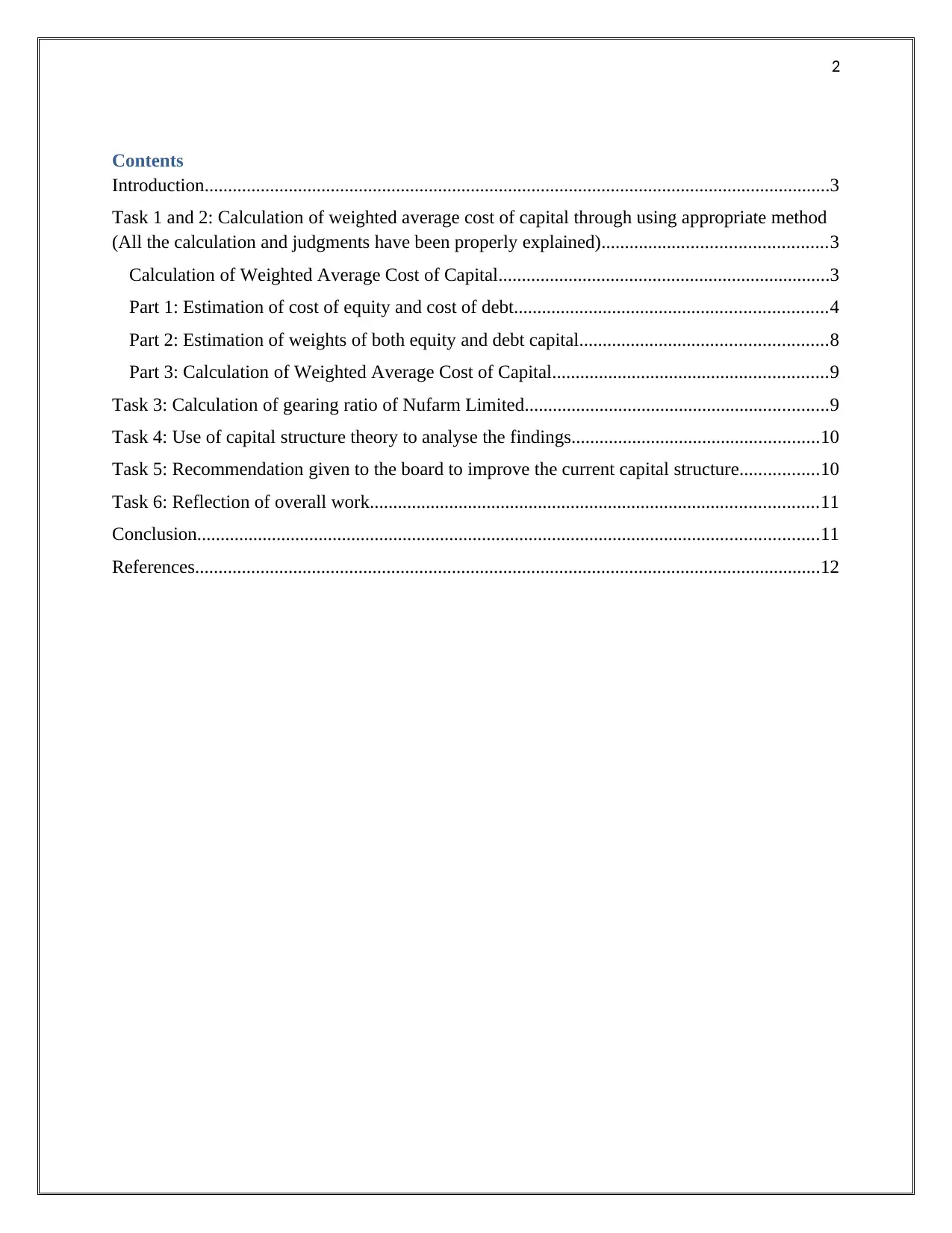

Contents

Introduction......................................................................................................................................3

Task 1 and 2: Calculation of weighted average cost of capital through using appropriate method

(All the calculation and judgments have been properly explained)................................................3

Calculation of Weighted Average Cost of Capital.......................................................................3

Part 1: Estimation of cost of equity and cost of debt...................................................................4

Part 2: Estimation of weights of both equity and debt capital.....................................................8

Part 3: Calculation of Weighted Average Cost of Capital...........................................................9

Task 3: Calculation of gearing ratio of Nufarm Limited.................................................................9

Task 4: Use of capital structure theory to analyse the findings.....................................................10

Task 5: Recommendation given to the board to improve the current capital structure.................10

Task 6: Reflection of overall work................................................................................................11

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Contents

Introduction......................................................................................................................................3

Task 1 and 2: Calculation of weighted average cost of capital through using appropriate method

(All the calculation and judgments have been properly explained)................................................3

Calculation of Weighted Average Cost of Capital.......................................................................3

Part 1: Estimation of cost of equity and cost of debt...................................................................4

Part 2: Estimation of weights of both equity and debt capital.....................................................8

Part 3: Calculation of Weighted Average Cost of Capital...........................................................9

Task 3: Calculation of gearing ratio of Nufarm Limited.................................................................9

Task 4: Use of capital structure theory to analyse the findings.....................................................10

Task 5: Recommendation given to the board to improve the current capital structure.................10

Task 6: Reflection of overall work................................................................................................11

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

Introduction

The calculation of appropriate weighted average cost of capital of any company is the

complex task and it requires appropriate use of technique or method to estimate correct WACC.

In this regard, this report is developed for calculating the WACC of Nufarm Limited through use

of capital asset pricing model as it is best model to estimate the required WACC of the selected

company. Capital asset pricing is used estimate the cost of equity and it requires calculating of

three important components that are beta factor, risk free rate of return and market premium. In

addition to this, the report also depicts the calculation of gearing ratios for Nufarm Limited and

analyzes the findings with the use of capital structure theory. This is followed by providing

recommendations to the Board on the current capital structure of the firm and presents reflection

on overall work performed to process this report.

The company selected for analysis purpose is Nufarm Limited; an agricultural company

headquartered within Australia and traded on ASX. It is involved in manufacturing of

agrochemical products such as weeds and herbicides and various types of other diverse range of

crop protection products.

Task 1 and 2: Calculation of weighted average cost of capital through using appropriate

method (All the calculation and judgments have been properly explained)

Calculation of Weighted Average Cost of Capital

This section of the report has been developed for calculating the weighted average cost of

capital for Nufarm Limited for the financial year 2018. The weighted average cost of capital is

regarded as the overall cost that is incurred by a company on its total capital. It is calculated by

weighing proportionally all the capitals employed by a company and the cost of each capital is

multiplied by weight for arriving at the weighted average cost of capital. The major type of

capital that is used by a company includes equity, debt, bonds, debentures, preferences and other

type of long-term debt. The weighted average cost of capital is dependent on the factors such as

risk free rate, beta, and rate of interest and market return. The cost of capital rise with the

increase in beta and the rate of return on equity. Thus, if there is increase in the WACC then it

reflects the rise in overall risk and decline in the valuation of capital. The formula for calculating

the weighted average cost of capital is stated as follows:

In the above formula:

‘E’ represents the equity value

Introduction

The calculation of appropriate weighted average cost of capital of any company is the

complex task and it requires appropriate use of technique or method to estimate correct WACC.

In this regard, this report is developed for calculating the WACC of Nufarm Limited through use

of capital asset pricing model as it is best model to estimate the required WACC of the selected

company. Capital asset pricing is used estimate the cost of equity and it requires calculating of

three important components that are beta factor, risk free rate of return and market premium. In

addition to this, the report also depicts the calculation of gearing ratios for Nufarm Limited and

analyzes the findings with the use of capital structure theory. This is followed by providing

recommendations to the Board on the current capital structure of the firm and presents reflection

on overall work performed to process this report.

The company selected for analysis purpose is Nufarm Limited; an agricultural company

headquartered within Australia and traded on ASX. It is involved in manufacturing of

agrochemical products such as weeds and herbicides and various types of other diverse range of

crop protection products.

Task 1 and 2: Calculation of weighted average cost of capital through using appropriate

method (All the calculation and judgments have been properly explained)

Calculation of Weighted Average Cost of Capital

This section of the report has been developed for calculating the weighted average cost of

capital for Nufarm Limited for the financial year 2018. The weighted average cost of capital is

regarded as the overall cost that is incurred by a company on its total capital. It is calculated by

weighing proportionally all the capitals employed by a company and the cost of each capital is

multiplied by weight for arriving at the weighted average cost of capital. The major type of

capital that is used by a company includes equity, debt, bonds, debentures, preferences and other

type of long-term debt. The weighted average cost of capital is dependent on the factors such as

risk free rate, beta, and rate of interest and market return. The cost of capital rise with the

increase in beta and the rate of return on equity. Thus, if there is increase in the WACC then it

reflects the rise in overall risk and decline in the valuation of capital. The formula for calculating

the weighted average cost of capital is stated as follows:

In the above formula:

‘E’ represents the equity value

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

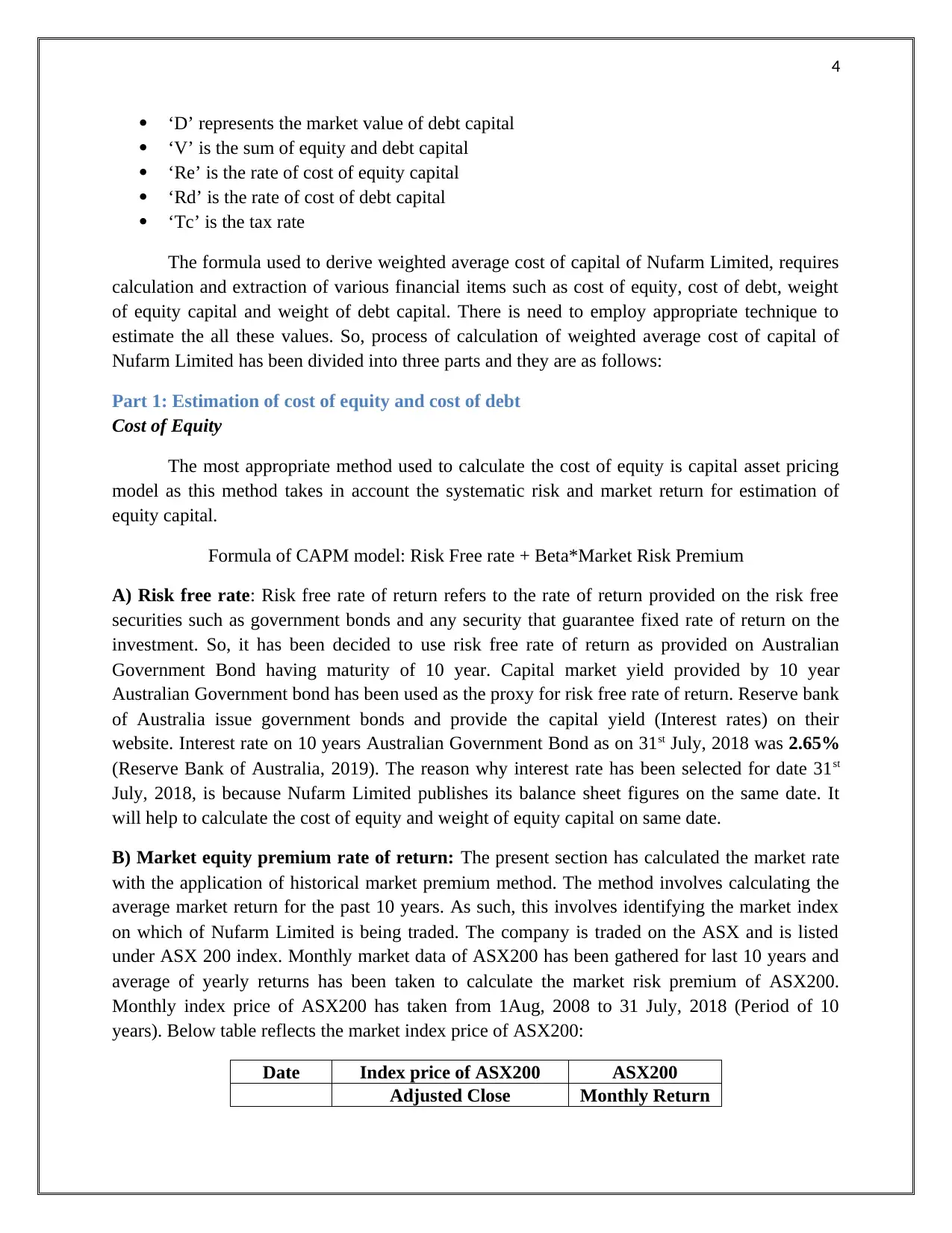

‘D’ represents the market value of debt capital

‘V’ is the sum of equity and debt capital

‘Re’ is the rate of cost of equity capital

‘Rd’ is the rate of cost of debt capital

‘Tc’ is the tax rate

The formula used to derive weighted average cost of capital of Nufarm Limited, requires

calculation and extraction of various financial items such as cost of equity, cost of debt, weight

of equity capital and weight of debt capital. There is need to employ appropriate technique to

estimate the all these values. So, process of calculation of weighted average cost of capital of

Nufarm Limited has been divided into three parts and they are as follows:

Part 1: Estimation of cost of equity and cost of debt

Cost of Equity

The most appropriate method used to calculate the cost of equity is capital asset pricing

model as this method takes in account the systematic risk and market return for estimation of

equity capital.

Formula of CAPM model: Risk Free rate + Beta*Market Risk Premium

A) Risk free rate: Risk free rate of return refers to the rate of return provided on the risk free

securities such as government bonds and any security that guarantee fixed rate of return on the

investment. So, it has been decided to use risk free rate of return as provided on Australian

Government Bond having maturity of 10 year. Capital market yield provided by 10 year

Australian Government bond has been used as the proxy for risk free rate of return. Reserve bank

of Australia issue government bonds and provide the capital yield (Interest rates) on their

website. Interest rate on 10 years Australian Government Bond as on 31st July, 2018 was 2.65%

(Reserve Bank of Australia, 2019). The reason why interest rate has been selected for date 31st

July, 2018, is because Nufarm Limited publishes its balance sheet figures on the same date. It

will help to calculate the cost of equity and weight of equity capital on same date.

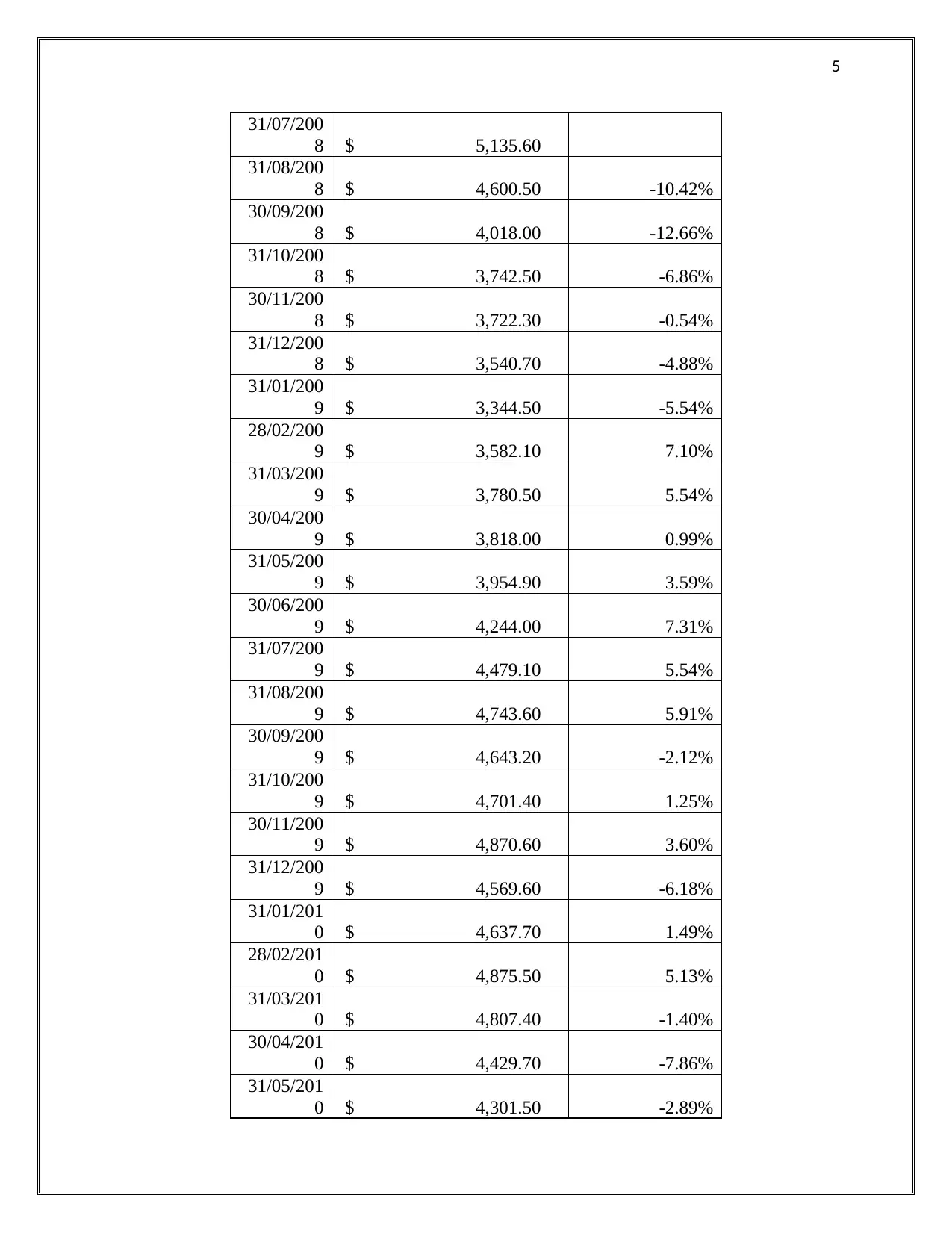

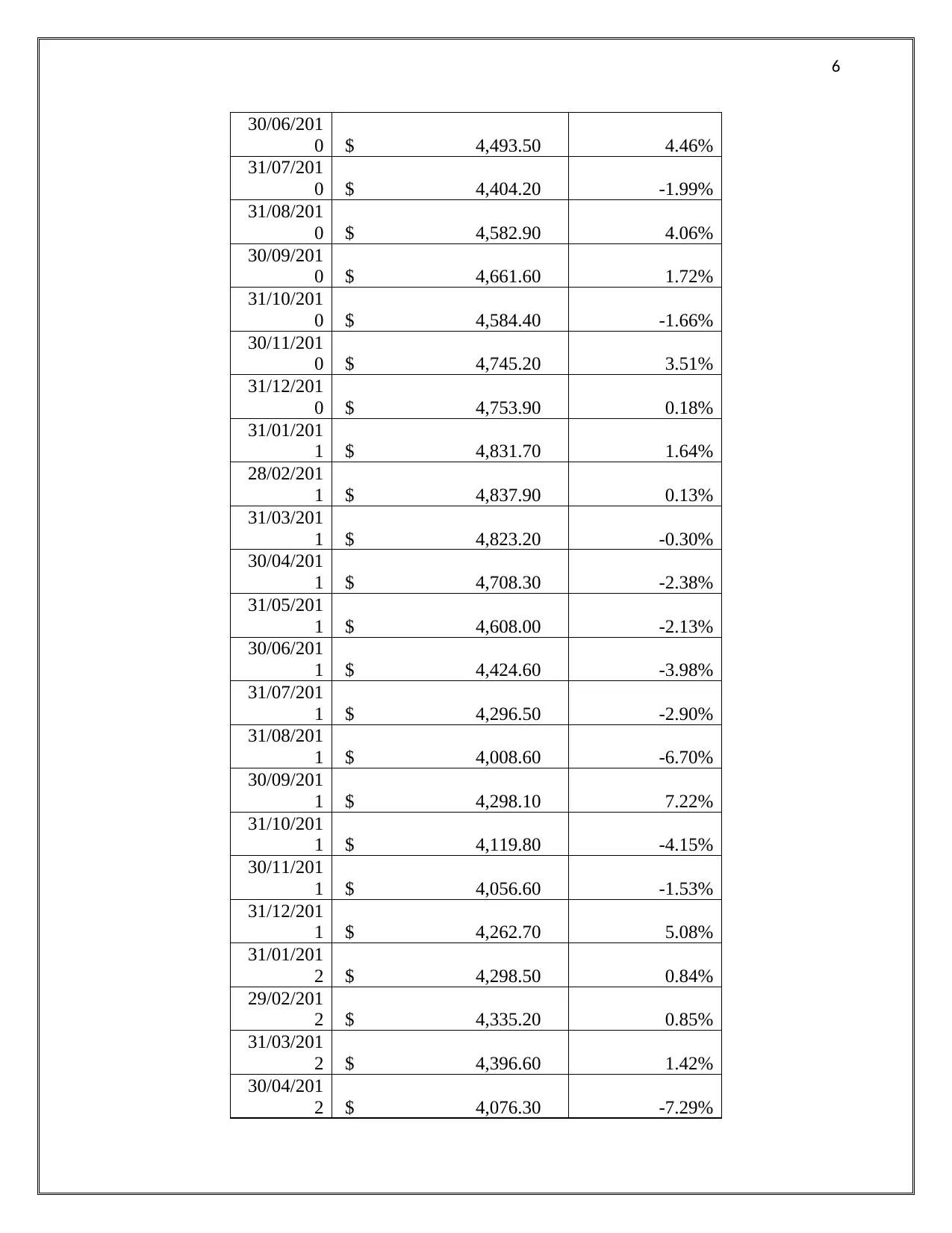

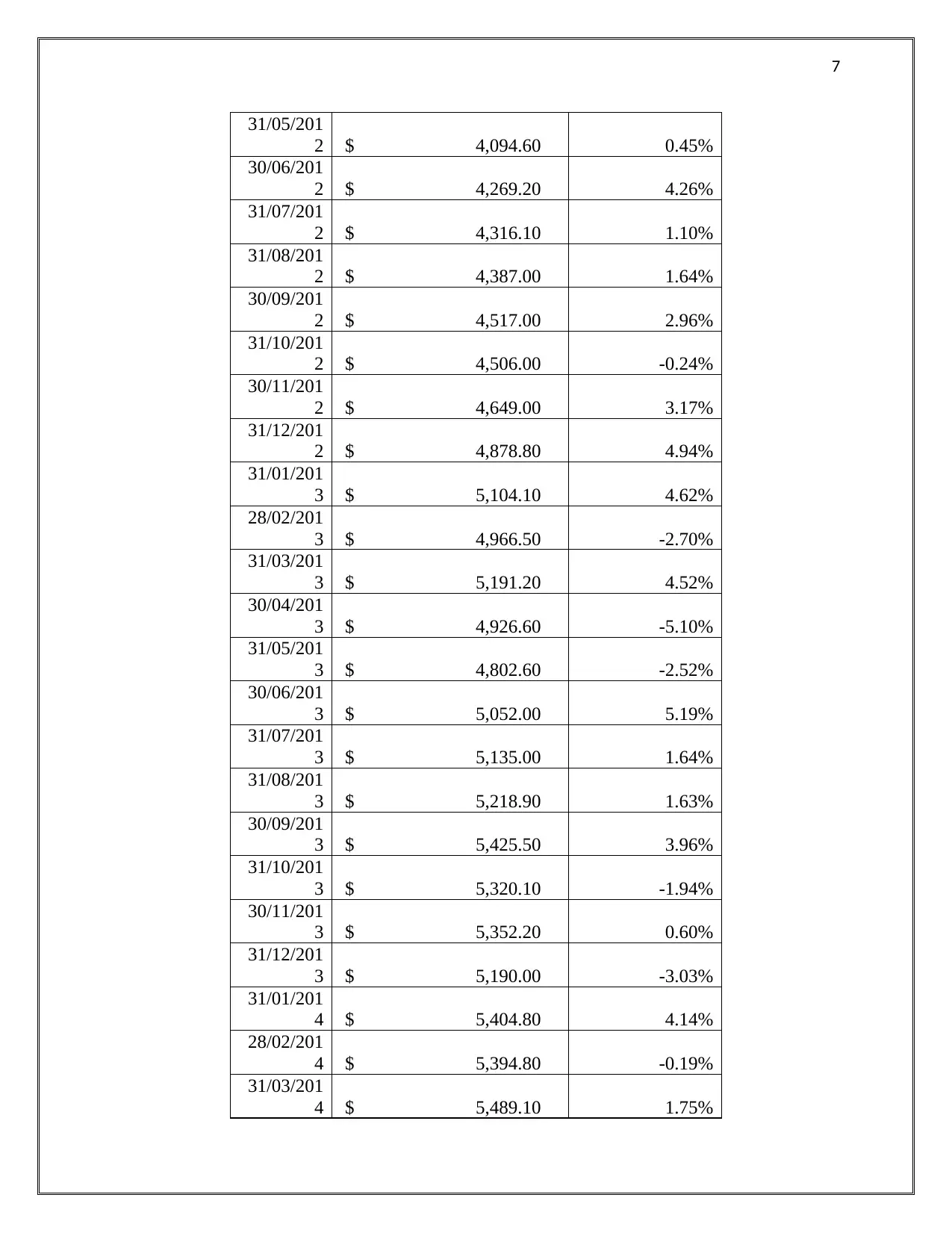

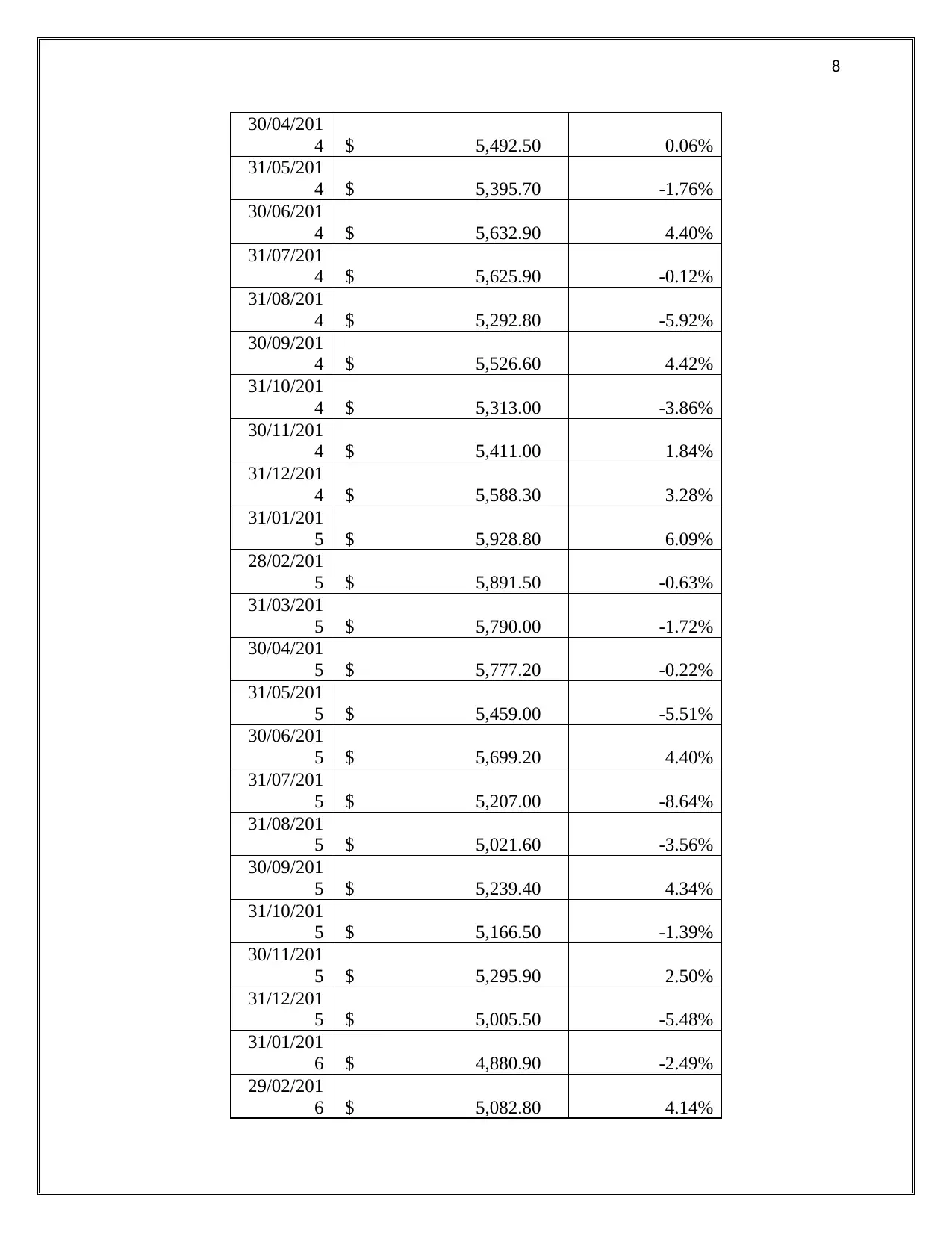

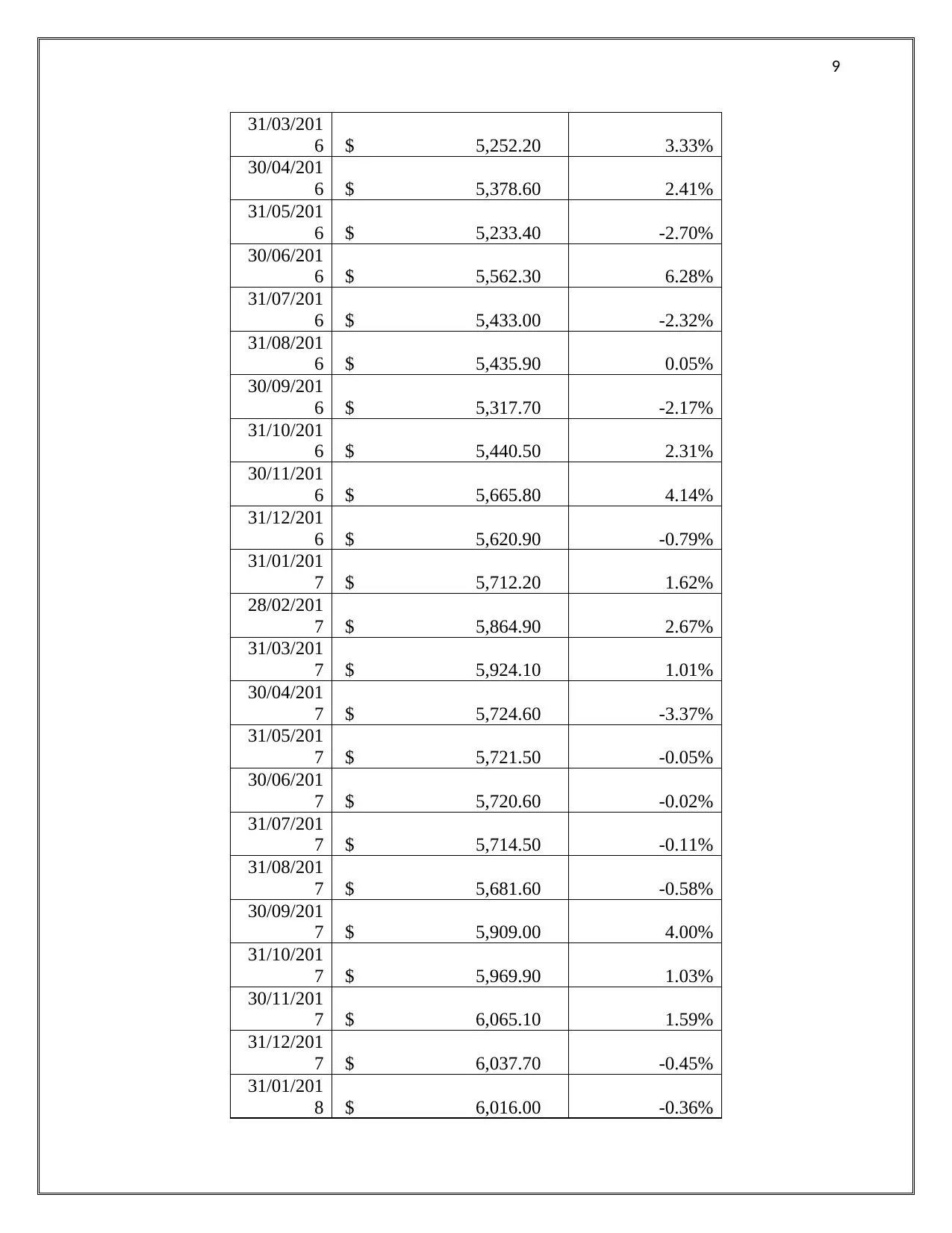

B) Market equity premium rate of return: The present section has calculated the market rate

with the application of historical market premium method. The method involves calculating the

average market return for the past 10 years. As such, this involves identifying the market index

on which of Nufarm Limited is being traded. The company is traded on the ASX and is listed

under ASX 200 index. Monthly market data of ASX200 has been gathered for last 10 years and

average of yearly returns has been taken to calculate the market risk premium of ASX200.

Monthly index price of ASX200 has taken from 1Aug, 2008 to 31 July, 2018 (Period of 10

years). Below table reflects the market index price of ASX200:

Date Index price of ASX200 ASX200

Adjusted Close Monthly Return

‘D’ represents the market value of debt capital

‘V’ is the sum of equity and debt capital

‘Re’ is the rate of cost of equity capital

‘Rd’ is the rate of cost of debt capital

‘Tc’ is the tax rate

The formula used to derive weighted average cost of capital of Nufarm Limited, requires

calculation and extraction of various financial items such as cost of equity, cost of debt, weight

of equity capital and weight of debt capital. There is need to employ appropriate technique to

estimate the all these values. So, process of calculation of weighted average cost of capital of

Nufarm Limited has been divided into three parts and they are as follows:

Part 1: Estimation of cost of equity and cost of debt

Cost of Equity

The most appropriate method used to calculate the cost of equity is capital asset pricing

model as this method takes in account the systematic risk and market return for estimation of

equity capital.

Formula of CAPM model: Risk Free rate + Beta*Market Risk Premium

A) Risk free rate: Risk free rate of return refers to the rate of return provided on the risk free

securities such as government bonds and any security that guarantee fixed rate of return on the

investment. So, it has been decided to use risk free rate of return as provided on Australian

Government Bond having maturity of 10 year. Capital market yield provided by 10 year

Australian Government bond has been used as the proxy for risk free rate of return. Reserve bank

of Australia issue government bonds and provide the capital yield (Interest rates) on their

website. Interest rate on 10 years Australian Government Bond as on 31st July, 2018 was 2.65%

(Reserve Bank of Australia, 2019). The reason why interest rate has been selected for date 31st

July, 2018, is because Nufarm Limited publishes its balance sheet figures on the same date. It

will help to calculate the cost of equity and weight of equity capital on same date.

B) Market equity premium rate of return: The present section has calculated the market rate

with the application of historical market premium method. The method involves calculating the

average market return for the past 10 years. As such, this involves identifying the market index

on which of Nufarm Limited is being traded. The company is traded on the ASX and is listed

under ASX 200 index. Monthly market data of ASX200 has been gathered for last 10 years and

average of yearly returns has been taken to calculate the market risk premium of ASX200.

Monthly index price of ASX200 has taken from 1Aug, 2008 to 31 July, 2018 (Period of 10

years). Below table reflects the market index price of ASX200:

Date Index price of ASX200 ASX200

Adjusted Close Monthly Return

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

31/07/200

8 $ 5,135.60

31/08/200

8 $ 4,600.50 -10.42%

30/09/200

8 $ 4,018.00 -12.66%

31/10/200

8 $ 3,742.50 -6.86%

30/11/200

8 $ 3,722.30 -0.54%

31/12/200

8 $ 3,540.70 -4.88%

31/01/200

9 $ 3,344.50 -5.54%

28/02/200

9 $ 3,582.10 7.10%

31/03/200

9 $ 3,780.50 5.54%

30/04/200

9 $ 3,818.00 0.99%

31/05/200

9 $ 3,954.90 3.59%

30/06/200

9 $ 4,244.00 7.31%

31/07/200

9 $ 4,479.10 5.54%

31/08/200

9 $ 4,743.60 5.91%

30/09/200

9 $ 4,643.20 -2.12%

31/10/200

9 $ 4,701.40 1.25%

30/11/200

9 $ 4,870.60 3.60%

31/12/200

9 $ 4,569.60 -6.18%

31/01/201

0 $ 4,637.70 1.49%

28/02/201

0 $ 4,875.50 5.13%

31/03/201

0 $ 4,807.40 -1.40%

30/04/201

0 $ 4,429.70 -7.86%

31/05/201

0 $ 4,301.50 -2.89%

31/07/200

8 $ 5,135.60

31/08/200

8 $ 4,600.50 -10.42%

30/09/200

8 $ 4,018.00 -12.66%

31/10/200

8 $ 3,742.50 -6.86%

30/11/200

8 $ 3,722.30 -0.54%

31/12/200

8 $ 3,540.70 -4.88%

31/01/200

9 $ 3,344.50 -5.54%

28/02/200

9 $ 3,582.10 7.10%

31/03/200

9 $ 3,780.50 5.54%

30/04/200

9 $ 3,818.00 0.99%

31/05/200

9 $ 3,954.90 3.59%

30/06/200

9 $ 4,244.00 7.31%

31/07/200

9 $ 4,479.10 5.54%

31/08/200

9 $ 4,743.60 5.91%

30/09/200

9 $ 4,643.20 -2.12%

31/10/200

9 $ 4,701.40 1.25%

30/11/200

9 $ 4,870.60 3.60%

31/12/200

9 $ 4,569.60 -6.18%

31/01/201

0 $ 4,637.70 1.49%

28/02/201

0 $ 4,875.50 5.13%

31/03/201

0 $ 4,807.40 -1.40%

30/04/201

0 $ 4,429.70 -7.86%

31/05/201

0 $ 4,301.50 -2.89%

6

30/06/201

0 $ 4,493.50 4.46%

31/07/201

0 $ 4,404.20 -1.99%

31/08/201

0 $ 4,582.90 4.06%

30/09/201

0 $ 4,661.60 1.72%

31/10/201

0 $ 4,584.40 -1.66%

30/11/201

0 $ 4,745.20 3.51%

31/12/201

0 $ 4,753.90 0.18%

31/01/201

1 $ 4,831.70 1.64%

28/02/201

1 $ 4,837.90 0.13%

31/03/201

1 $ 4,823.20 -0.30%

30/04/201

1 $ 4,708.30 -2.38%

31/05/201

1 $ 4,608.00 -2.13%

30/06/201

1 $ 4,424.60 -3.98%

31/07/201

1 $ 4,296.50 -2.90%

31/08/201

1 $ 4,008.60 -6.70%

30/09/201

1 $ 4,298.10 7.22%

31/10/201

1 $ 4,119.80 -4.15%

30/11/201

1 $ 4,056.60 -1.53%

31/12/201

1 $ 4,262.70 5.08%

31/01/201

2 $ 4,298.50 0.84%

29/02/201

2 $ 4,335.20 0.85%

31/03/201

2 $ 4,396.60 1.42%

30/04/201

2 $ 4,076.30 -7.29%

30/06/201

0 $ 4,493.50 4.46%

31/07/201

0 $ 4,404.20 -1.99%

31/08/201

0 $ 4,582.90 4.06%

30/09/201

0 $ 4,661.60 1.72%

31/10/201

0 $ 4,584.40 -1.66%

30/11/201

0 $ 4,745.20 3.51%

31/12/201

0 $ 4,753.90 0.18%

31/01/201

1 $ 4,831.70 1.64%

28/02/201

1 $ 4,837.90 0.13%

31/03/201

1 $ 4,823.20 -0.30%

30/04/201

1 $ 4,708.30 -2.38%

31/05/201

1 $ 4,608.00 -2.13%

30/06/201

1 $ 4,424.60 -3.98%

31/07/201

1 $ 4,296.50 -2.90%

31/08/201

1 $ 4,008.60 -6.70%

30/09/201

1 $ 4,298.10 7.22%

31/10/201

1 $ 4,119.80 -4.15%

30/11/201

1 $ 4,056.60 -1.53%

31/12/201

1 $ 4,262.70 5.08%

31/01/201

2 $ 4,298.50 0.84%

29/02/201

2 $ 4,335.20 0.85%

31/03/201

2 $ 4,396.60 1.42%

30/04/201

2 $ 4,076.30 -7.29%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

31/05/201

2 $ 4,094.60 0.45%

30/06/201

2 $ 4,269.20 4.26%

31/07/201

2 $ 4,316.10 1.10%

31/08/201

2 $ 4,387.00 1.64%

30/09/201

2 $ 4,517.00 2.96%

31/10/201

2 $ 4,506.00 -0.24%

30/11/201

2 $ 4,649.00 3.17%

31/12/201

2 $ 4,878.80 4.94%

31/01/201

3 $ 5,104.10 4.62%

28/02/201

3 $ 4,966.50 -2.70%

31/03/201

3 $ 5,191.20 4.52%

30/04/201

3 $ 4,926.60 -5.10%

31/05/201

3 $ 4,802.60 -2.52%

30/06/201

3 $ 5,052.00 5.19%

31/07/201

3 $ 5,135.00 1.64%

31/08/201

3 $ 5,218.90 1.63%

30/09/201

3 $ 5,425.50 3.96%

31/10/201

3 $ 5,320.10 -1.94%

30/11/201

3 $ 5,352.20 0.60%

31/12/201

3 $ 5,190.00 -3.03%

31/01/201

4 $ 5,404.80 4.14%

28/02/201

4 $ 5,394.80 -0.19%

31/03/201

4 $ 5,489.10 1.75%

31/05/201

2 $ 4,094.60 0.45%

30/06/201

2 $ 4,269.20 4.26%

31/07/201

2 $ 4,316.10 1.10%

31/08/201

2 $ 4,387.00 1.64%

30/09/201

2 $ 4,517.00 2.96%

31/10/201

2 $ 4,506.00 -0.24%

30/11/201

2 $ 4,649.00 3.17%

31/12/201

2 $ 4,878.80 4.94%

31/01/201

3 $ 5,104.10 4.62%

28/02/201

3 $ 4,966.50 -2.70%

31/03/201

3 $ 5,191.20 4.52%

30/04/201

3 $ 4,926.60 -5.10%

31/05/201

3 $ 4,802.60 -2.52%

30/06/201

3 $ 5,052.00 5.19%

31/07/201

3 $ 5,135.00 1.64%

31/08/201

3 $ 5,218.90 1.63%

30/09/201

3 $ 5,425.50 3.96%

31/10/201

3 $ 5,320.10 -1.94%

30/11/201

3 $ 5,352.20 0.60%

31/12/201

3 $ 5,190.00 -3.03%

31/01/201

4 $ 5,404.80 4.14%

28/02/201

4 $ 5,394.80 -0.19%

31/03/201

4 $ 5,489.10 1.75%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

30/04/201

4 $ 5,492.50 0.06%

31/05/201

4 $ 5,395.70 -1.76%

30/06/201

4 $ 5,632.90 4.40%

31/07/201

4 $ 5,625.90 -0.12%

31/08/201

4 $ 5,292.80 -5.92%

30/09/201

4 $ 5,526.60 4.42%

31/10/201

4 $ 5,313.00 -3.86%

30/11/201

4 $ 5,411.00 1.84%

31/12/201

4 $ 5,588.30 3.28%

31/01/201

5 $ 5,928.80 6.09%

28/02/201

5 $ 5,891.50 -0.63%

31/03/201

5 $ 5,790.00 -1.72%

30/04/201

5 $ 5,777.20 -0.22%

31/05/201

5 $ 5,459.00 -5.51%

30/06/201

5 $ 5,699.20 4.40%

31/07/201

5 $ 5,207.00 -8.64%

31/08/201

5 $ 5,021.60 -3.56%

30/09/201

5 $ 5,239.40 4.34%

31/10/201

5 $ 5,166.50 -1.39%

30/11/201

5 $ 5,295.90 2.50%

31/12/201

5 $ 5,005.50 -5.48%

31/01/201

6 $ 4,880.90 -2.49%

29/02/201

6 $ 5,082.80 4.14%

30/04/201

4 $ 5,492.50 0.06%

31/05/201

4 $ 5,395.70 -1.76%

30/06/201

4 $ 5,632.90 4.40%

31/07/201

4 $ 5,625.90 -0.12%

31/08/201

4 $ 5,292.80 -5.92%

30/09/201

4 $ 5,526.60 4.42%

31/10/201

4 $ 5,313.00 -3.86%

30/11/201

4 $ 5,411.00 1.84%

31/12/201

4 $ 5,588.30 3.28%

31/01/201

5 $ 5,928.80 6.09%

28/02/201

5 $ 5,891.50 -0.63%

31/03/201

5 $ 5,790.00 -1.72%

30/04/201

5 $ 5,777.20 -0.22%

31/05/201

5 $ 5,459.00 -5.51%

30/06/201

5 $ 5,699.20 4.40%

31/07/201

5 $ 5,207.00 -8.64%

31/08/201

5 $ 5,021.60 -3.56%

30/09/201

5 $ 5,239.40 4.34%

31/10/201

5 $ 5,166.50 -1.39%

30/11/201

5 $ 5,295.90 2.50%

31/12/201

5 $ 5,005.50 -5.48%

31/01/201

6 $ 4,880.90 -2.49%

29/02/201

6 $ 5,082.80 4.14%

9

31/03/201

6 $ 5,252.20 3.33%

30/04/201

6 $ 5,378.60 2.41%

31/05/201

6 $ 5,233.40 -2.70%

30/06/201

6 $ 5,562.30 6.28%

31/07/201

6 $ 5,433.00 -2.32%

31/08/201

6 $ 5,435.90 0.05%

30/09/201

6 $ 5,317.70 -2.17%

31/10/201

6 $ 5,440.50 2.31%

30/11/201

6 $ 5,665.80 4.14%

31/12/201

6 $ 5,620.90 -0.79%

31/01/201

7 $ 5,712.20 1.62%

28/02/201

7 $ 5,864.90 2.67%

31/03/201

7 $ 5,924.10 1.01%

30/04/201

7 $ 5,724.60 -3.37%

31/05/201

7 $ 5,721.50 -0.05%

30/06/201

7 $ 5,720.60 -0.02%

31/07/201

7 $ 5,714.50 -0.11%

31/08/201

7 $ 5,681.60 -0.58%

30/09/201

7 $ 5,909.00 4.00%

31/10/201

7 $ 5,969.90 1.03%

30/11/201

7 $ 6,065.10 1.59%

31/12/201

7 $ 6,037.70 -0.45%

31/01/201

8 $ 6,016.00 -0.36%

31/03/201

6 $ 5,252.20 3.33%

30/04/201

6 $ 5,378.60 2.41%

31/05/201

6 $ 5,233.40 -2.70%

30/06/201

6 $ 5,562.30 6.28%

31/07/201

6 $ 5,433.00 -2.32%

31/08/201

6 $ 5,435.90 0.05%

30/09/201

6 $ 5,317.70 -2.17%

31/10/201

6 $ 5,440.50 2.31%

30/11/201

6 $ 5,665.80 4.14%

31/12/201

6 $ 5,620.90 -0.79%

31/01/201

7 $ 5,712.20 1.62%

28/02/201

7 $ 5,864.90 2.67%

31/03/201

7 $ 5,924.10 1.01%

30/04/201

7 $ 5,724.60 -3.37%

31/05/201

7 $ 5,721.50 -0.05%

30/06/201

7 $ 5,720.60 -0.02%

31/07/201

7 $ 5,714.50 -0.11%

31/08/201

7 $ 5,681.60 -0.58%

30/09/201

7 $ 5,909.00 4.00%

31/10/201

7 $ 5,969.90 1.03%

30/11/201

7 $ 6,065.10 1.59%

31/12/201

7 $ 6,037.70 -0.45%

31/01/201

8 $ 6,016.00 -0.36%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

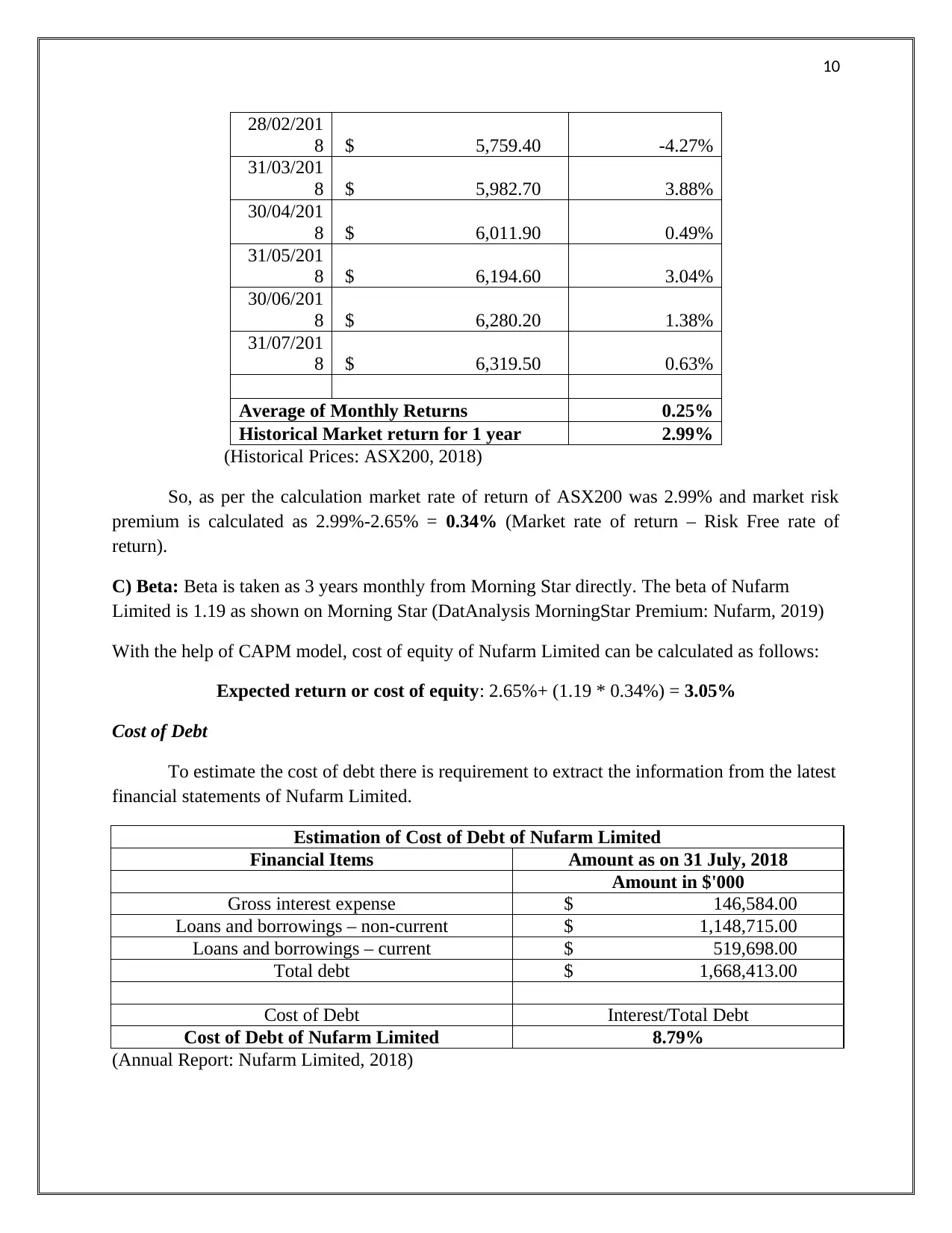

28/02/201

8 $ 5,759.40 -4.27%

31/03/201

8 $ 5,982.70 3.88%

30/04/201

8 $ 6,011.90 0.49%

31/05/201

8 $ 6,194.60 3.04%

30/06/201

8 $ 6,280.20 1.38%

31/07/201

8 $ 6,319.50 0.63%

Average of Monthly Returns 0.25%

Historical Market return for 1 year 2.99%

(Historical Prices: ASX200, 2018)

So, as per the calculation market rate of return of ASX200 was 2.99% and market risk

premium is calculated as 2.99%-2.65% = 0.34% (Market rate of return – Risk Free rate of

return).

C) Beta: Beta is taken as 3 years monthly from Morning Star directly. The beta of Nufarm

Limited is 1.19 as shown on Morning Star (DatAnalysis MorningStar Premium: Nufarm, 2019)

With the help of CAPM model, cost of equity of Nufarm Limited can be calculated as follows:

Expected return or cost of equity: 2.65%+ (1.19 * 0.34%) = 3.05%

Cost of Debt

To estimate the cost of debt there is requirement to extract the information from the latest

financial statements of Nufarm Limited.

Estimation of Cost of Debt of Nufarm Limited

Financial Items Amount as on 31 July, 2018

Amount in $'000

Gross interest expense $ 146,584.00

Loans and borrowings – non-current $ 1,148,715.00

Loans and borrowings – current $ 519,698.00

Total debt $ 1,668,413.00

Cost of Debt Interest/Total Debt

Cost of Debt of Nufarm Limited 8.79%

(Annual Report: Nufarm Limited, 2018)

28/02/201

8 $ 5,759.40 -4.27%

31/03/201

8 $ 5,982.70 3.88%

30/04/201

8 $ 6,011.90 0.49%

31/05/201

8 $ 6,194.60 3.04%

30/06/201

8 $ 6,280.20 1.38%

31/07/201

8 $ 6,319.50 0.63%

Average of Monthly Returns 0.25%

Historical Market return for 1 year 2.99%

(Historical Prices: ASX200, 2018)

So, as per the calculation market rate of return of ASX200 was 2.99% and market risk

premium is calculated as 2.99%-2.65% = 0.34% (Market rate of return – Risk Free rate of

return).

C) Beta: Beta is taken as 3 years monthly from Morning Star directly. The beta of Nufarm

Limited is 1.19 as shown on Morning Star (DatAnalysis MorningStar Premium: Nufarm, 2019)

With the help of CAPM model, cost of equity of Nufarm Limited can be calculated as follows:

Expected return or cost of equity: 2.65%+ (1.19 * 0.34%) = 3.05%

Cost of Debt

To estimate the cost of debt there is requirement to extract the information from the latest

financial statements of Nufarm Limited.

Estimation of Cost of Debt of Nufarm Limited

Financial Items Amount as on 31 July, 2018

Amount in $'000

Gross interest expense $ 146,584.00

Loans and borrowings – non-current $ 1,148,715.00

Loans and borrowings – current $ 519,698.00

Total debt $ 1,668,413.00

Cost of Debt Interest/Total Debt

Cost of Debt of Nufarm Limited 8.79%

(Annual Report: Nufarm Limited, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

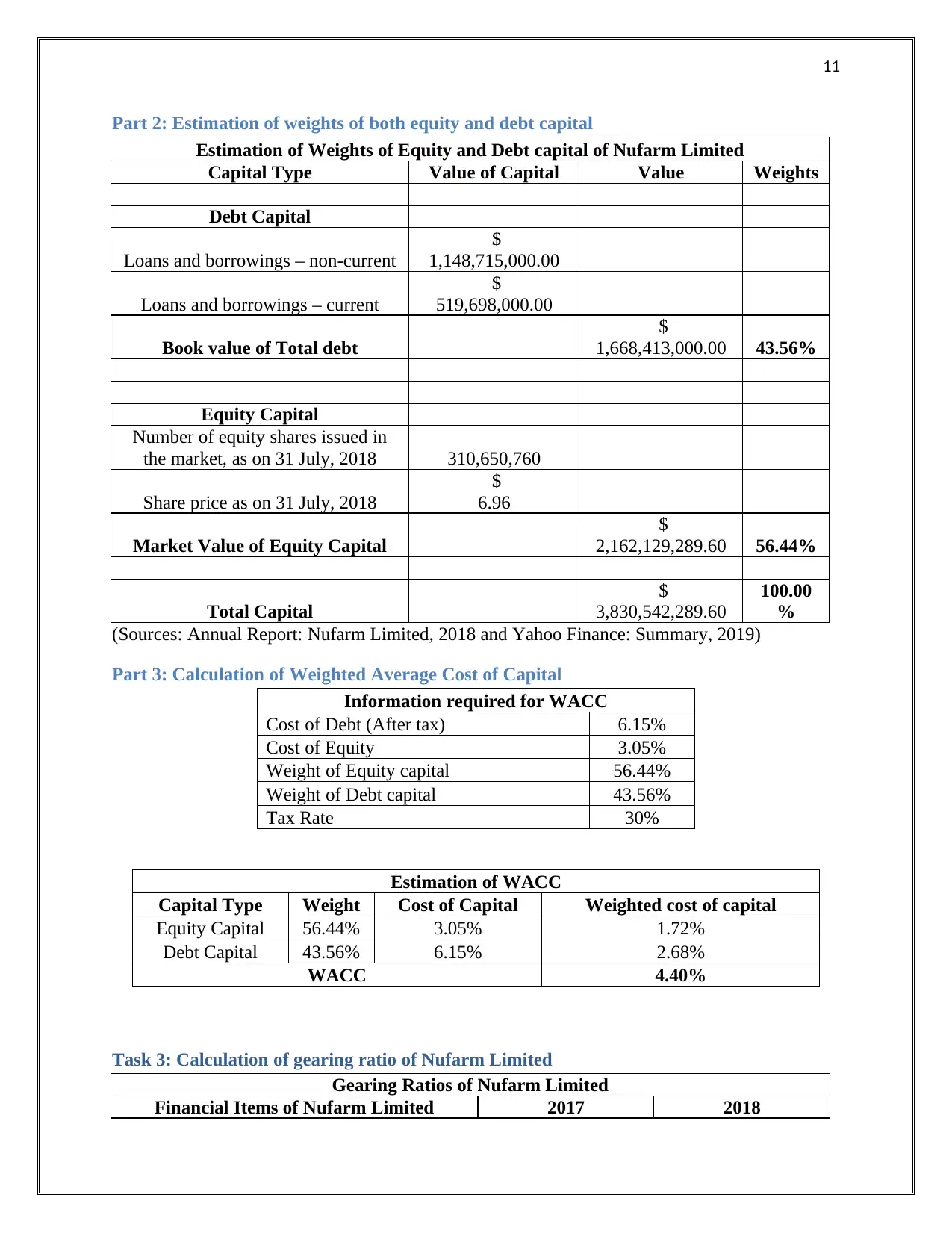

Part 2: Estimation of weights of both equity and debt capital

Estimation of Weights of Equity and Debt capital of Nufarm Limited

Capital Type Value of Capital Value Weights

Debt Capital

Loans and borrowings – non-current

$

1,148,715,000.00

Loans and borrowings – current

$

519,698,000.00

Book value of Total debt

$

1,668,413,000.00 43.56%

Equity Capital

Number of equity shares issued in

the market, as on 31 July, 2018 310,650,760

Share price as on 31 July, 2018

$

6.96

Market Value of Equity Capital

$

2,162,129,289.60 56.44%

Total Capital

$

3,830,542,289.60

100.00

%

(Sources: Annual Report: Nufarm Limited, 2018 and Yahoo Finance: Summary, 2019)

Part 3: Calculation of Weighted Average Cost of Capital

Information required for WACC

Cost of Debt (After tax) 6.15%

Cost of Equity 3.05%

Weight of Equity capital 56.44%

Weight of Debt capital 43.56%

Tax Rate 30%

Estimation of WACC

Capital Type Weight Cost of Capital Weighted cost of capital

Equity Capital 56.44% 3.05% 1.72%

Debt Capital 43.56% 6.15% 2.68%

WACC 4.40%

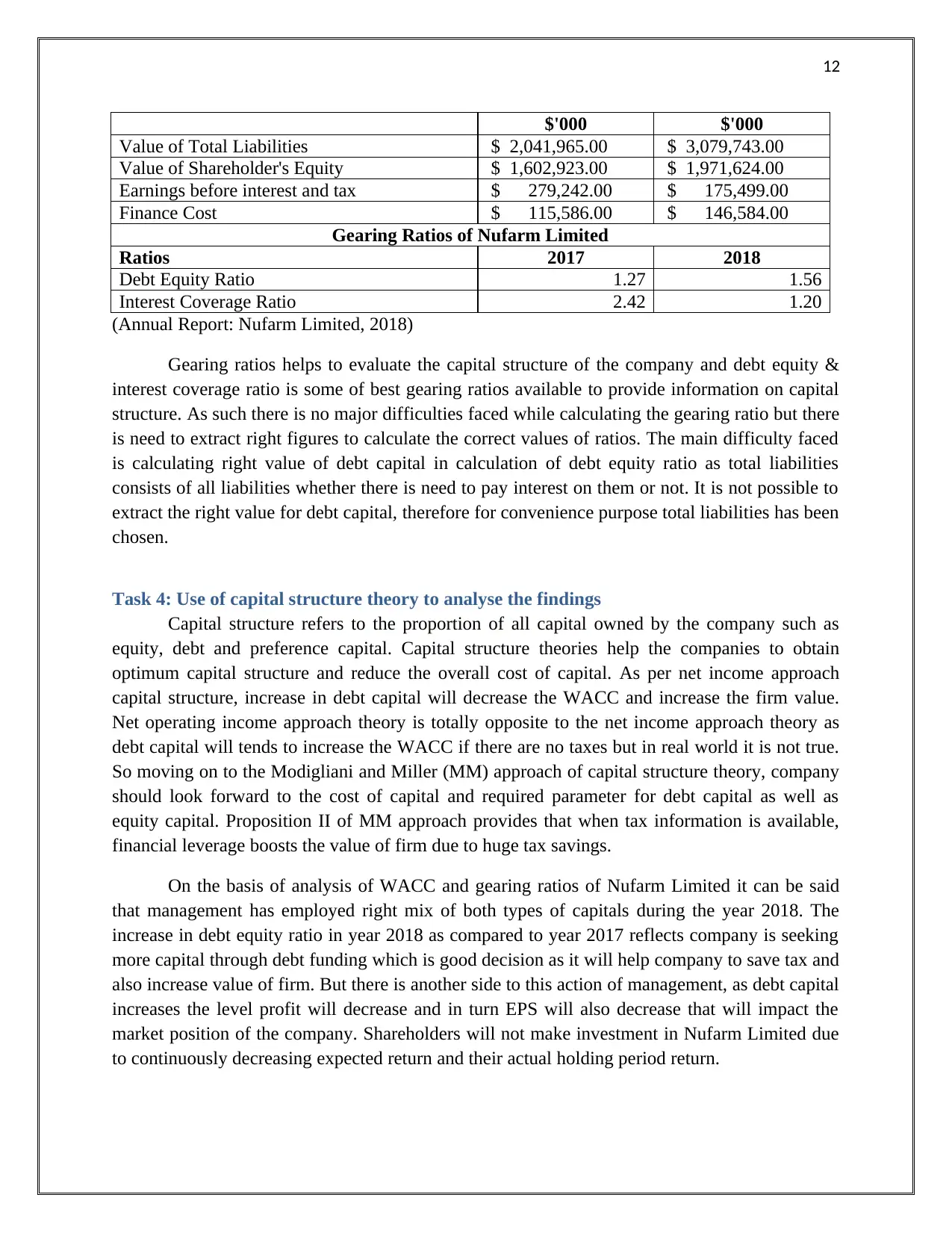

Task 3: Calculation of gearing ratio of Nufarm Limited

Gearing Ratios of Nufarm Limited

Financial Items of Nufarm Limited 2017 2018

Part 2: Estimation of weights of both equity and debt capital

Estimation of Weights of Equity and Debt capital of Nufarm Limited

Capital Type Value of Capital Value Weights

Debt Capital

Loans and borrowings – non-current

$

1,148,715,000.00

Loans and borrowings – current

$

519,698,000.00

Book value of Total debt

$

1,668,413,000.00 43.56%

Equity Capital

Number of equity shares issued in

the market, as on 31 July, 2018 310,650,760

Share price as on 31 July, 2018

$

6.96

Market Value of Equity Capital

$

2,162,129,289.60 56.44%

Total Capital

$

3,830,542,289.60

100.00

%

(Sources: Annual Report: Nufarm Limited, 2018 and Yahoo Finance: Summary, 2019)

Part 3: Calculation of Weighted Average Cost of Capital

Information required for WACC

Cost of Debt (After tax) 6.15%

Cost of Equity 3.05%

Weight of Equity capital 56.44%

Weight of Debt capital 43.56%

Tax Rate 30%

Estimation of WACC

Capital Type Weight Cost of Capital Weighted cost of capital

Equity Capital 56.44% 3.05% 1.72%

Debt Capital 43.56% 6.15% 2.68%

WACC 4.40%

Task 3: Calculation of gearing ratio of Nufarm Limited

Gearing Ratios of Nufarm Limited

Financial Items of Nufarm Limited 2017 2018

12

$'000 $'000

Value of Total Liabilities $ 2,041,965.00 $ 3,079,743.00

Value of Shareholder's Equity $ 1,602,923.00 $ 1,971,624.00

Earnings before interest and tax $ 279,242.00 $ 175,499.00

Finance Cost $ 115,586.00 $ 146,584.00

Gearing Ratios of Nufarm Limited

Ratios 2017 2018

Debt Equity Ratio 1.27 1.56

Interest Coverage Ratio 2.42 1.20

(Annual Report: Nufarm Limited, 2018)

Gearing ratios helps to evaluate the capital structure of the company and debt equity &

interest coverage ratio is some of best gearing ratios available to provide information on capital

structure. As such there is no major difficulties faced while calculating the gearing ratio but there

is need to extract right figures to calculate the correct values of ratios. The main difficulty faced

is calculating right value of debt capital in calculation of debt equity ratio as total liabilities

consists of all liabilities whether there is need to pay interest on them or not. It is not possible to

extract the right value for debt capital, therefore for convenience purpose total liabilities has been

chosen.

Task 4: Use of capital structure theory to analyse the findings

Capital structure refers to the proportion of all capital owned by the company such as

equity, debt and preference capital. Capital structure theories help the companies to obtain

optimum capital structure and reduce the overall cost of capital. As per net income approach

capital structure, increase in debt capital will decrease the WACC and increase the firm value.

Net operating income approach theory is totally opposite to the net income approach theory as

debt capital will tends to increase the WACC if there are no taxes but in real world it is not true.

So moving on to the Modigliani and Miller (MM) approach of capital structure theory, company

should look forward to the cost of capital and required parameter for debt capital as well as

equity capital. Proposition II of MM approach provides that when tax information is available,

financial leverage boosts the value of firm due to huge tax savings.

On the basis of analysis of WACC and gearing ratios of Nufarm Limited it can be said

that management has employed right mix of both types of capitals during the year 2018. The

increase in debt equity ratio in year 2018 as compared to year 2017 reflects company is seeking

more capital through debt funding which is good decision as it will help company to save tax and

also increase value of firm. But there is another side to this action of management, as debt capital

increases the level profit will decrease and in turn EPS will also decrease that will impact the

market position of the company. Shareholders will not make investment in Nufarm Limited due

to continuously decreasing expected return and their actual holding period return.

$'000 $'000

Value of Total Liabilities $ 2,041,965.00 $ 3,079,743.00

Value of Shareholder's Equity $ 1,602,923.00 $ 1,971,624.00

Earnings before interest and tax $ 279,242.00 $ 175,499.00

Finance Cost $ 115,586.00 $ 146,584.00

Gearing Ratios of Nufarm Limited

Ratios 2017 2018

Debt Equity Ratio 1.27 1.56

Interest Coverage Ratio 2.42 1.20

(Annual Report: Nufarm Limited, 2018)

Gearing ratios helps to evaluate the capital structure of the company and debt equity &

interest coverage ratio is some of best gearing ratios available to provide information on capital

structure. As such there is no major difficulties faced while calculating the gearing ratio but there

is need to extract right figures to calculate the correct values of ratios. The main difficulty faced

is calculating right value of debt capital in calculation of debt equity ratio as total liabilities

consists of all liabilities whether there is need to pay interest on them or not. It is not possible to

extract the right value for debt capital, therefore for convenience purpose total liabilities has been

chosen.

Task 4: Use of capital structure theory to analyse the findings

Capital structure refers to the proportion of all capital owned by the company such as

equity, debt and preference capital. Capital structure theories help the companies to obtain

optimum capital structure and reduce the overall cost of capital. As per net income approach

capital structure, increase in debt capital will decrease the WACC and increase the firm value.

Net operating income approach theory is totally opposite to the net income approach theory as

debt capital will tends to increase the WACC if there are no taxes but in real world it is not true.

So moving on to the Modigliani and Miller (MM) approach of capital structure theory, company

should look forward to the cost of capital and required parameter for debt capital as well as

equity capital. Proposition II of MM approach provides that when tax information is available,

financial leverage boosts the value of firm due to huge tax savings.

On the basis of analysis of WACC and gearing ratios of Nufarm Limited it can be said

that management has employed right mix of both types of capitals during the year 2018. The

increase in debt equity ratio in year 2018 as compared to year 2017 reflects company is seeking

more capital through debt funding which is good decision as it will help company to save tax and

also increase value of firm. But there is another side to this action of management, as debt capital

increases the level profit will decrease and in turn EPS will also decrease that will impact the

market position of the company. Shareholders will not make investment in Nufarm Limited due

to continuously decreasing expected return and their actual holding period return.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.