Accounting Fundamentals Report: Ratio Analysis and Financial Reporting

VerifiedAdded on 2023/01/07

|14

|4254

|79

Report

AI Summary

This report provides a comprehensive analysis of accounting fundamentals, focusing on the financial statements of Wales plc and Jerry plc. It includes an income statement and a statement of financial position for Wales plc, followed by a detailed ratio analysis for Jerry plc, covering areas like return on equity, earnings per share, and asset turnover. The report also explores the perspectives of various users of company accounts, including internal and external stakeholders, and discusses the advantages, disadvantages, and limitations of financial reporting. Furthermore, it examines the importance of accounting information for decision-making, covering topics such as investment strategies, performance evaluation, and risk assessment. Overall, the report offers a thorough understanding of accounting principles and their practical application in financial analysis.

ACCOUNTING

FUNDAMENTALS

FUNDAMENTALS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

Income Statement of the Wales plc for the year ended 31st December 2019..............................3

Statement of the financial position of Wales plc for the year ended 31st December 2019..........4

QUESTION 2..................................................................................................................................5

a) Calculation of Ratios for Jerry plc for year 2019 and 2018....................................................5

b) Situation being revealed by the ratios.....................................................................................6

Question 3........................................................................................................................................8

A) Three different group of user of company accounts and reason behind user interested in

information provided by financial statements.............................................................................8

B) Advantages and disadvantages of financial reporting regime for perspective from both user

and prepare of financial statements...........................................................................................10

C) Limitation of Financial statement.........................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

Income Statement of the Wales plc for the year ended 31st December 2019..............................3

Statement of the financial position of Wales plc for the year ended 31st December 2019..........4

QUESTION 2..................................................................................................................................5

a) Calculation of Ratios for Jerry plc for year 2019 and 2018....................................................5

b) Situation being revealed by the ratios.....................................................................................6

Question 3........................................................................................................................................8

A) Three different group of user of company accounts and reason behind user interested in

information provided by financial statements.............................................................................8

B) Advantages and disadvantages of financial reporting regime for perspective from both user

and prepare of financial statements...........................................................................................10

C) Limitation of Financial statement.........................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Business management is important process which involves arrangement of sufficient

resources such financial and human to complete particular task and delivered qualitative services

to customers. Accounting fundamental majorly includes five main parts like recording,

classifying, interpretation, analysis and formulation of financial reports to know about actual

amount of amount and operating expense within specific period of time. Therefore it is complex

process that includes crucial information of business that are need by all internal and external

stakeholders for their respective decision making. The report has prepared income and financial

statements of Wales Plc’s on 31 December 2019. Various ratio of Jerry Plc has been calculated

in the report on basis of income and financial statements of company to get important

information about company. At last it has explained about use, limitation of financial statements

or income statements of company.

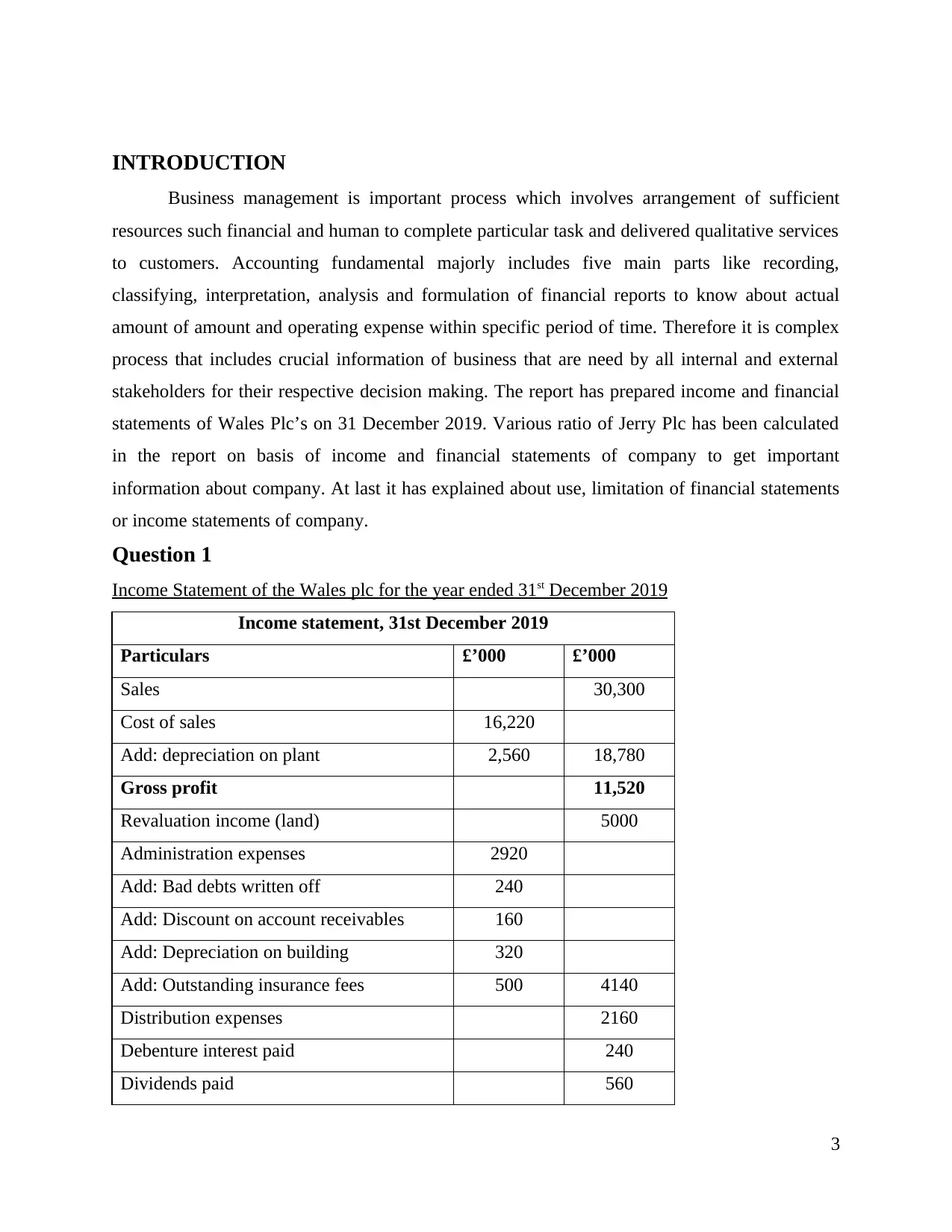

Question 1

Income Statement of the Wales plc for the year ended 31st December 2019

Income statement, 31st December 2019

Particulars £’000 £’000

Sales 30,300

Cost of sales 16,220

Add: depreciation on plant 2,560 18,780

Gross profit 11,520

Revaluation income (land) 5000

Administration expenses 2920

Add: Bad debts written off 240

Add: Discount on account receivables 160

Add: Depreciation on building 320

Add: Outstanding insurance fees 500 4140

Distribution expenses 2160

Debenture interest paid 240

Dividends paid 560

3

Business management is important process which involves arrangement of sufficient

resources such financial and human to complete particular task and delivered qualitative services

to customers. Accounting fundamental majorly includes five main parts like recording,

classifying, interpretation, analysis and formulation of financial reports to know about actual

amount of amount and operating expense within specific period of time. Therefore it is complex

process that includes crucial information of business that are need by all internal and external

stakeholders for their respective decision making. The report has prepared income and financial

statements of Wales Plc’s on 31 December 2019. Various ratio of Jerry Plc has been calculated

in the report on basis of income and financial statements of company to get important

information about company. At last it has explained about use, limitation of financial statements

or income statements of company.

Question 1

Income Statement of the Wales plc for the year ended 31st December 2019

Income statement, 31st December 2019

Particulars £’000 £’000

Sales 30,300

Cost of sales 16,220

Add: depreciation on plant 2,560 18,780

Gross profit 11,520

Revaluation income (land) 5000

Administration expenses 2920

Add: Bad debts written off 240

Add: Discount on account receivables 160

Add: Depreciation on building 320

Add: Outstanding insurance fees 500 4140

Distribution expenses 2160

Debenture interest paid 240

Dividends paid 560

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax paid 1600

Net profit 7,820

With the above statement it can be seen that that the net profit of the year was 7820 and the

income of the company was 30300 and the direct expenses were 18780. After deducting the

direct expenses from the income the gross profit of 11520. Further after deducting all the indirect

expenses from the gross profit the net profit was 7820.

Statement of the financial position of Wales plc for the year ended 31st December 2019

Statement of position as at 31st December 2019

Liabilities £’000 Assets £’000

Share capital 29000 Bank 320

Retained profit 8380 Land at cost 20000

Share premium 5000 Buildings at cost 16000

Net profit 7,820

Less: Accumulated

depreciation (4260 +

320) 4580 11420

12% debentures 2024 4000 Plant at cost 25600

Outstanding insurance fees 500

Less: Accumulated

depreciation (4960 +

2560) 7520 18080

Trade payables 4480

Trade receivables

(8240-240- 160) 7840

Income tax liability 1600 Inventory 3120

Total liabilities 60780 Total assets 60780

Workings

Working note

Building cost 16000

Depreciation (2% * 16000) 320

4

Net profit 7,820

With the above statement it can be seen that that the net profit of the year was 7820 and the

income of the company was 30300 and the direct expenses were 18780. After deducting the

direct expenses from the income the gross profit of 11520. Further after deducting all the indirect

expenses from the gross profit the net profit was 7820.

Statement of the financial position of Wales plc for the year ended 31st December 2019

Statement of position as at 31st December 2019

Liabilities £’000 Assets £’000

Share capital 29000 Bank 320

Retained profit 8380 Land at cost 20000

Share premium 5000 Buildings at cost 16000

Net profit 7,820

Less: Accumulated

depreciation (4260 +

320) 4580 11420

12% debentures 2024 4000 Plant at cost 25600

Outstanding insurance fees 500

Less: Accumulated

depreciation (4960 +

2560) 7520 18080

Trade payables 4480

Trade receivables

(8240-240- 160) 7840

Income tax liability 1600 Inventory 3120

Total liabilities 60780 Total assets 60780

Workings

Working note

Building cost 16000

Depreciation (2% * 16000) 320

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

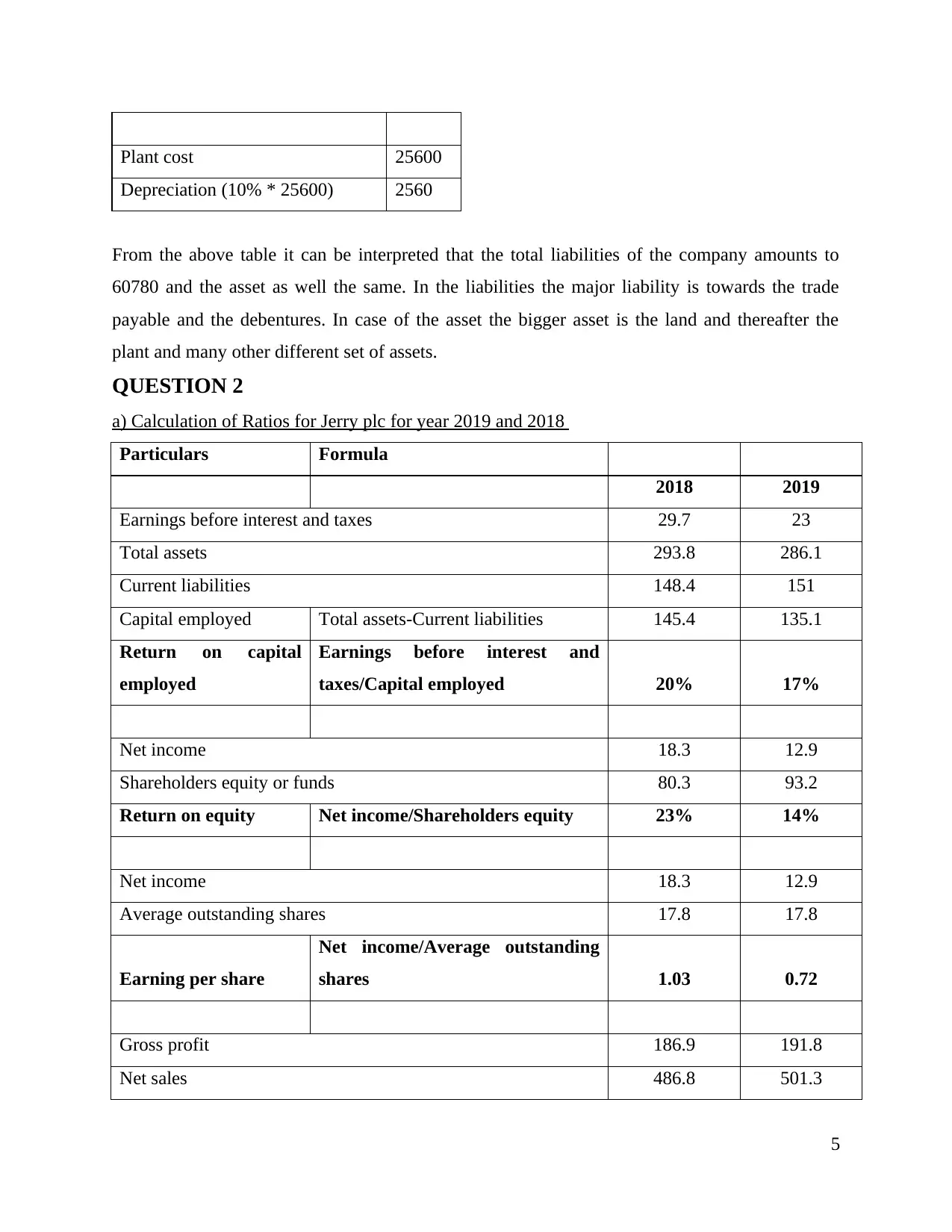

Plant cost 25600

Depreciation (10% * 25600) 2560

From the above table it can be interpreted that the total liabilities of the company amounts to

60780 and the asset as well the same. In the liabilities the major liability is towards the trade

payable and the debentures. In case of the asset the bigger asset is the land and thereafter the

plant and many other different set of assets.

QUESTION 2

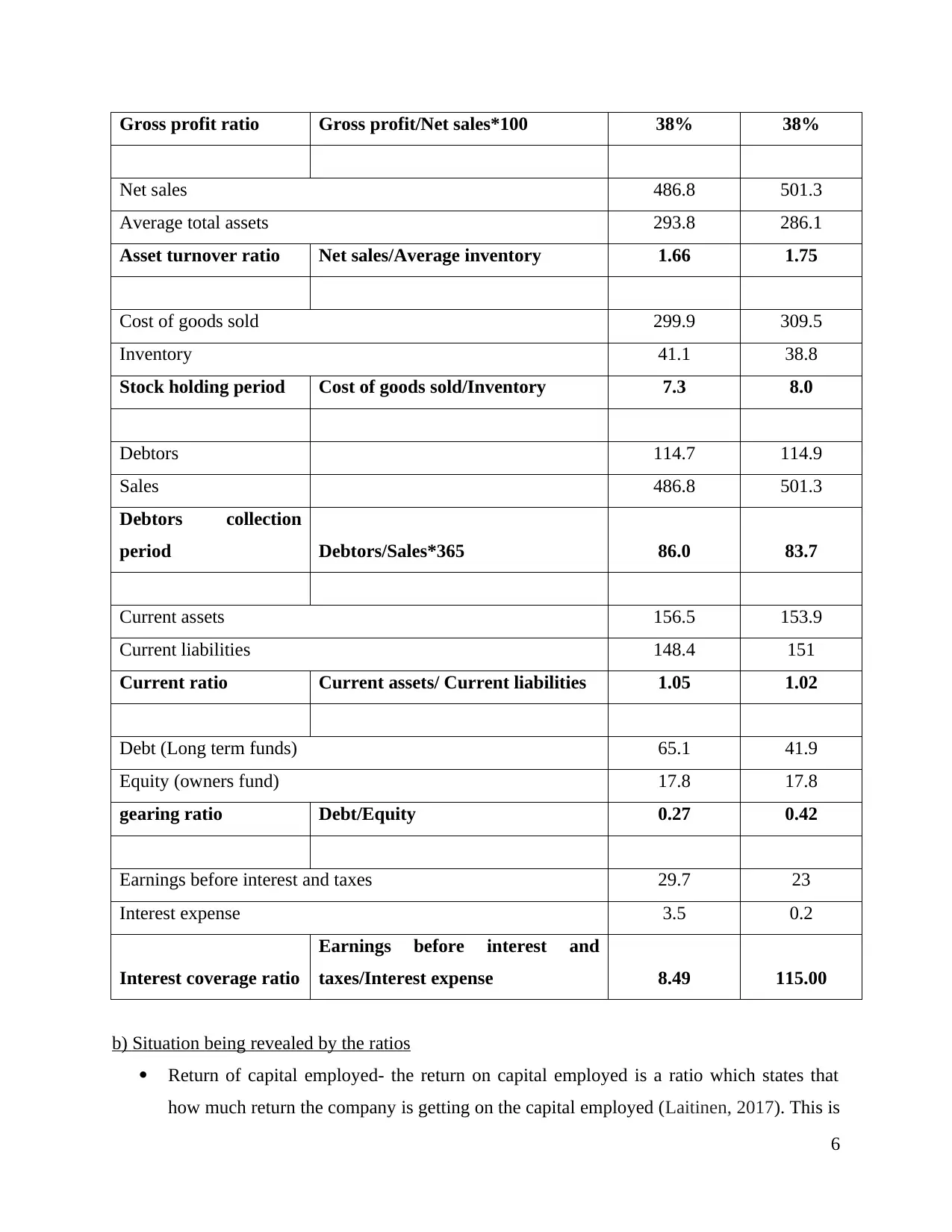

a) Calculation of Ratios for Jerry plc for year 2019 and 2018

Particulars Formula

2018 2019

Earnings before interest and taxes 29.7 23

Total assets 293.8 286.1

Current liabilities 148.4 151

Capital employed Total assets-Current liabilities 145.4 135.1

Return on capital

employed

Earnings before interest and

taxes/Capital employed 20% 17%

Net income 18.3 12.9

Shareholders equity or funds 80.3 93.2

Return on equity Net income/Shareholders equity 23% 14%

Net income 18.3 12.9

Average outstanding shares 17.8 17.8

Earning per share

Net income/Average outstanding

shares 1.03 0.72

Gross profit 186.9 191.8

Net sales 486.8 501.3

5

Depreciation (10% * 25600) 2560

From the above table it can be interpreted that the total liabilities of the company amounts to

60780 and the asset as well the same. In the liabilities the major liability is towards the trade

payable and the debentures. In case of the asset the bigger asset is the land and thereafter the

plant and many other different set of assets.

QUESTION 2

a) Calculation of Ratios for Jerry plc for year 2019 and 2018

Particulars Formula

2018 2019

Earnings before interest and taxes 29.7 23

Total assets 293.8 286.1

Current liabilities 148.4 151

Capital employed Total assets-Current liabilities 145.4 135.1

Return on capital

employed

Earnings before interest and

taxes/Capital employed 20% 17%

Net income 18.3 12.9

Shareholders equity or funds 80.3 93.2

Return on equity Net income/Shareholders equity 23% 14%

Net income 18.3 12.9

Average outstanding shares 17.8 17.8

Earning per share

Net income/Average outstanding

shares 1.03 0.72

Gross profit 186.9 191.8

Net sales 486.8 501.3

5

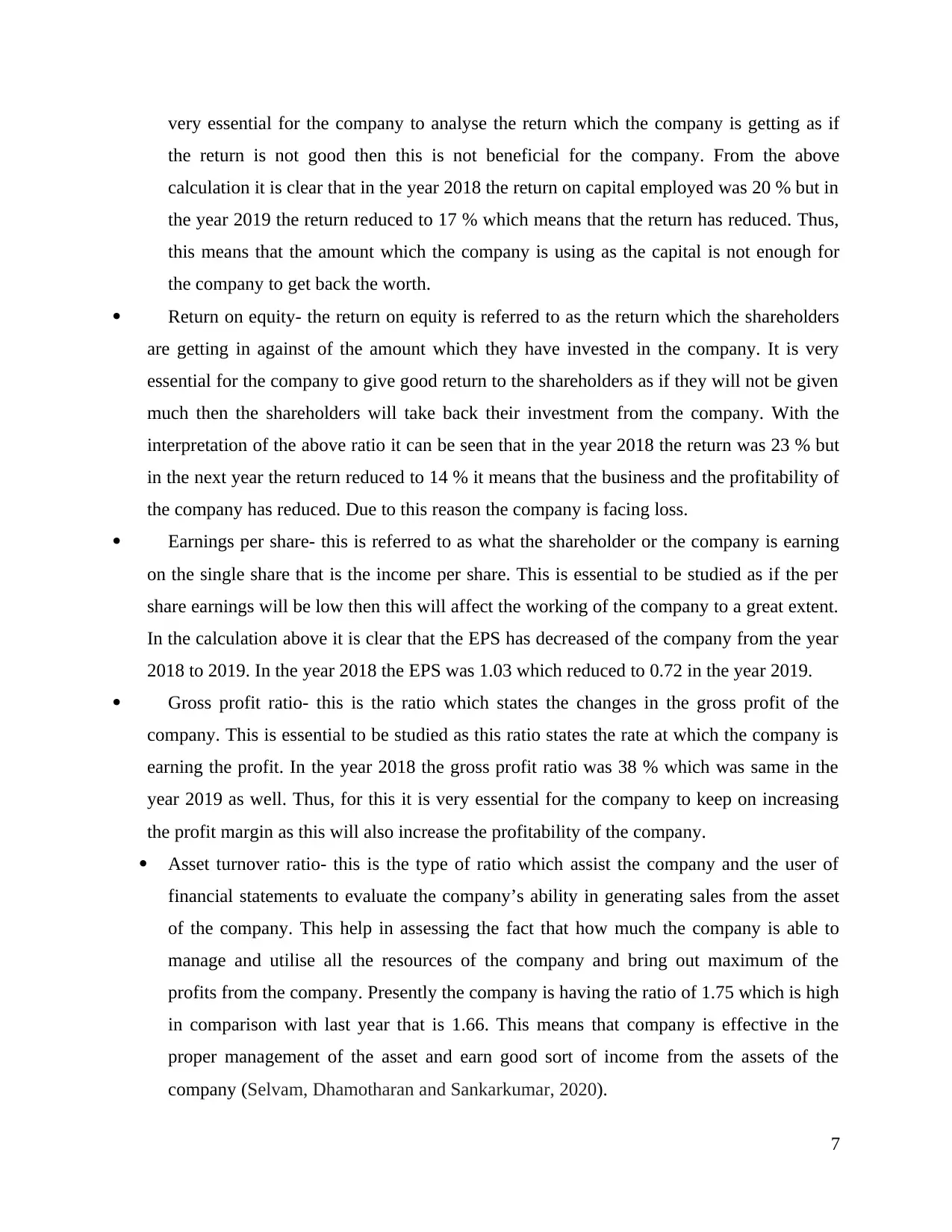

Gross profit ratio Gross profit/Net sales*100 38% 38%

Net sales 486.8 501.3

Average total assets 293.8 286.1

Asset turnover ratio Net sales/Average inventory 1.66 1.75

Cost of goods sold 299.9 309.5

Inventory 41.1 38.8

Stock holding period Cost of goods sold/Inventory 7.3 8.0

Debtors 114.7 114.9

Sales 486.8 501.3

Debtors collection

period Debtors/Sales*365 86.0 83.7

Current assets 156.5 153.9

Current liabilities 148.4 151

Current ratio Current assets/ Current liabilities 1.05 1.02

Debt (Long term funds) 65.1 41.9

Equity (owners fund) 17.8 17.8

gearing ratio Debt/Equity 0.27 0.42

Earnings before interest and taxes 29.7 23

Interest expense 3.5 0.2

Interest coverage ratio

Earnings before interest and

taxes/Interest expense 8.49 115.00

b) Situation being revealed by the ratios

Return of capital employed- the return on capital employed is a ratio which states that

how much return the company is getting on the capital employed (Laitinen, 2017). This is

6

Net sales 486.8 501.3

Average total assets 293.8 286.1

Asset turnover ratio Net sales/Average inventory 1.66 1.75

Cost of goods sold 299.9 309.5

Inventory 41.1 38.8

Stock holding period Cost of goods sold/Inventory 7.3 8.0

Debtors 114.7 114.9

Sales 486.8 501.3

Debtors collection

period Debtors/Sales*365 86.0 83.7

Current assets 156.5 153.9

Current liabilities 148.4 151

Current ratio Current assets/ Current liabilities 1.05 1.02

Debt (Long term funds) 65.1 41.9

Equity (owners fund) 17.8 17.8

gearing ratio Debt/Equity 0.27 0.42

Earnings before interest and taxes 29.7 23

Interest expense 3.5 0.2

Interest coverage ratio

Earnings before interest and

taxes/Interest expense 8.49 115.00

b) Situation being revealed by the ratios

Return of capital employed- the return on capital employed is a ratio which states that

how much return the company is getting on the capital employed (Laitinen, 2017). This is

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

very essential for the company to analyse the return which the company is getting as if

the return is not good then this is not beneficial for the company. From the above

calculation it is clear that in the year 2018 the return on capital employed was 20 % but in

the year 2019 the return reduced to 17 % which means that the return has reduced. Thus,

this means that the amount which the company is using as the capital is not enough for

the company to get back the worth.

Return on equity- the return on equity is referred to as the return which the shareholders

are getting in against of the amount which they have invested in the company. It is very

essential for the company to give good return to the shareholders as if they will not be given

much then the shareholders will take back their investment from the company. With the

interpretation of the above ratio it can be seen that in the year 2018 the return was 23 % but

in the next year the return reduced to 14 % it means that the business and the profitability of

the company has reduced. Due to this reason the company is facing loss.

Earnings per share- this is referred to as what the shareholder or the company is earning

on the single share that is the income per share. This is essential to be studied as if the per

share earnings will be low then this will affect the working of the company to a great extent.

In the calculation above it is clear that the EPS has decreased of the company from the year

2018 to 2019. In the year 2018 the EPS was 1.03 which reduced to 0.72 in the year 2019.

Gross profit ratio- this is the ratio which states the changes in the gross profit of the

company. This is essential to be studied as this ratio states the rate at which the company is

earning the profit. In the year 2018 the gross profit ratio was 38 % which was same in the

year 2019 as well. Thus, for this it is very essential for the company to keep on increasing

the profit margin as this will also increase the profitability of the company.

Asset turnover ratio- this is the type of ratio which assist the company and the user of

financial statements to evaluate the company’s ability in generating sales from the asset

of the company. This help in assessing the fact that how much the company is able to

manage and utilise all the resources of the company and bring out maximum of the

profits from the company. Presently the company is having the ratio of 1.75 which is high

in comparison with last year that is 1.66. This means that company is effective in the

proper management of the asset and earn good sort of income from the assets of the

company (Selvam, Dhamotharan and Sankarkumar, 2020).

7

the return is not good then this is not beneficial for the company. From the above

calculation it is clear that in the year 2018 the return on capital employed was 20 % but in

the year 2019 the return reduced to 17 % which means that the return has reduced. Thus,

this means that the amount which the company is using as the capital is not enough for

the company to get back the worth.

Return on equity- the return on equity is referred to as the return which the shareholders

are getting in against of the amount which they have invested in the company. It is very

essential for the company to give good return to the shareholders as if they will not be given

much then the shareholders will take back their investment from the company. With the

interpretation of the above ratio it can be seen that in the year 2018 the return was 23 % but

in the next year the return reduced to 14 % it means that the business and the profitability of

the company has reduced. Due to this reason the company is facing loss.

Earnings per share- this is referred to as what the shareholder or the company is earning

on the single share that is the income per share. This is essential to be studied as if the per

share earnings will be low then this will affect the working of the company to a great extent.

In the calculation above it is clear that the EPS has decreased of the company from the year

2018 to 2019. In the year 2018 the EPS was 1.03 which reduced to 0.72 in the year 2019.

Gross profit ratio- this is the ratio which states the changes in the gross profit of the

company. This is essential to be studied as this ratio states the rate at which the company is

earning the profit. In the year 2018 the gross profit ratio was 38 % which was same in the

year 2019 as well. Thus, for this it is very essential for the company to keep on increasing

the profit margin as this will also increase the profitability of the company.

Asset turnover ratio- this is the type of ratio which assist the company and the user of

financial statements to evaluate the company’s ability in generating sales from the asset

of the company. This help in assessing the fact that how much the company is able to

manage and utilise all the resources of the company and bring out maximum of the

profits from the company. Presently the company is having the ratio of 1.75 which is high

in comparison with last year that is 1.66. This means that company is effective in the

proper management of the asset and earn good sort of income from the assets of the

company (Selvam, Dhamotharan and Sankarkumar, 2020).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stock holding period- this is the ratio which is also known as inventory turnover ratio and

this ratio illustrates the average time which is taken by the company in converting the

inventory into sales. In the year 2018 the ratio was 7.3 and in 2018 this increased to 8.

Thus, it can be stated that the company need to work in the direction of minimising the

ratio so that in shorter time the inventory will be converted in cash (Martins, 2017).

Debtor’s collection period- this is the ratio which states that in how much time the

company will collect all the dues and credit from the customers and other people. In the year

2018, this period was 86 days and in 2019 it was 84 days and this states that the time has

reduced which is good for the company but it has to reduce it more.

Current ratio- this is the ratio which states that how much liquid is the company. In the

year 2018 the current ratio was 0.27 and in present year it was 0.42. This means that there

has been increasing move in the trend of current ratio which suggests that the company has

increased more towards the debt which is not good for the company and they need to reduce

it.

Gearing ratio- this is the ratio which is essential for the company as this assist the

company in evaluating the ratio of debt and equity in comparison with the overall capital of

the business. In the present year that is 2019 the ratio was 0.42 and in 2018 it was 0.27. This

has increased as compared to the last year and this states that the debt has increased and this

will result in the financial risk of the company.

Interest coverage ratio- this is the ratio which measures the company’s ability in making

and clearing all the payments relating to the interest of loans. In the present year the ratio

was 115 which was 8.49 in the last year. This suggest that the ability of the company has

increased with respect to the payment of the interest (Coulon, 2020).

Question 3

A) Three different group of user of company accounts and reason behind user interested in

information provided by financial statements

There are various group of people that are interested in financial statements of company

can be termed as external, internal and government or IRS. It can be stated that each group

analysis and make use of accounting information for different purpose thus present it in different

or unique way (Cheong and SHI, 2018). Therefore, three identified group of people that are

interested in financial statements of company are explained in detail below:

8

this ratio illustrates the average time which is taken by the company in converting the

inventory into sales. In the year 2018 the ratio was 7.3 and in 2018 this increased to 8.

Thus, it can be stated that the company need to work in the direction of minimising the

ratio so that in shorter time the inventory will be converted in cash (Martins, 2017).

Debtor’s collection period- this is the ratio which states that in how much time the

company will collect all the dues and credit from the customers and other people. In the year

2018, this period was 86 days and in 2019 it was 84 days and this states that the time has

reduced which is good for the company but it has to reduce it more.

Current ratio- this is the ratio which states that how much liquid is the company. In the

year 2018 the current ratio was 0.27 and in present year it was 0.42. This means that there

has been increasing move in the trend of current ratio which suggests that the company has

increased more towards the debt which is not good for the company and they need to reduce

it.

Gearing ratio- this is the ratio which is essential for the company as this assist the

company in evaluating the ratio of debt and equity in comparison with the overall capital of

the business. In the present year that is 2019 the ratio was 0.42 and in 2018 it was 0.27. This

has increased as compared to the last year and this states that the debt has increased and this

will result in the financial risk of the company.

Interest coverage ratio- this is the ratio which measures the company’s ability in making

and clearing all the payments relating to the interest of loans. In the present year the ratio

was 115 which was 8.49 in the last year. This suggest that the ability of the company has

increased with respect to the payment of the interest (Coulon, 2020).

Question 3

A) Three different group of user of company accounts and reason behind user interested in

information provided by financial statements

There are various group of people that are interested in financial statements of company

can be termed as external, internal and government or IRS. It can be stated that each group

analysis and make use of accounting information for different purpose thus present it in different

or unique way (Cheong and SHI, 2018). Therefore, three identified group of people that are

interested in financial statements of company are explained in detail below:

8

Internal users

These are primary user of accounting information so includes management, owners and

employees of firm. Such as:

Owners: It can be illustrated that owner of business required financial information or

company accounts in order to know overall profitability in particular year. At the same

time they are able to know about associated risk and total expenditure in financial year so

that various strategies can be planned to cope with future circumstances. Therefore it

helps owners to know or assess level of stability of business during various periods so

that it can make accurate decision to further invest in specific area to get better outcome.

Managers: Company manager require information related to company accounts for

planning, monitoring and evaluating of performance of business during specific financial

year. Accounting information contributed manager to take decision to prepare budget of

company by monitoring and analysing information of past performance of company and

key indicators which may lead to growth and success of enterprise (Lin, 2020). So, it can

be illustrated that manager requires accounting information to take business decision

likes setting prices and investments or finance for smooth operation of business.

Employees: These are other internal parties of company that are interested in company

accounts to know how well company is performing in market so that they can feel secure

and safe. On the other hand employees that are working in financial department of firm

used company account as part of their respective duties to prepare financial statement at

the end of year.

External user of company accounts

There are different types of external user of account information such as Investors,

suppliers, customers, tax authorities, auditors and general public. Like:

Investors: These are people that have invested their money or capital in business so by

evaluating and analysis financial statements they are able to know how well their

investment is performing. Thus, they are able to know amount of risk, profitability and

current value of investment that are useful in taking accurate decision to further invest in

business or not for better return on capital.

Suppliers/ lender/ creditors: Company needs various raw material or goods in order to

manufactured finished products that can be renders to end customers. Therefore,

9

These are primary user of accounting information so includes management, owners and

employees of firm. Such as:

Owners: It can be illustrated that owner of business required financial information or

company accounts in order to know overall profitability in particular year. At the same

time they are able to know about associated risk and total expenditure in financial year so

that various strategies can be planned to cope with future circumstances. Therefore it

helps owners to know or assess level of stability of business during various periods so

that it can make accurate decision to further invest in specific area to get better outcome.

Managers: Company manager require information related to company accounts for

planning, monitoring and evaluating of performance of business during specific financial

year. Accounting information contributed manager to take decision to prepare budget of

company by monitoring and analysing information of past performance of company and

key indicators which may lead to growth and success of enterprise (Lin, 2020). So, it can

be illustrated that manager requires accounting information to take business decision

likes setting prices and investments or finance for smooth operation of business.

Employees: These are other internal parties of company that are interested in company

accounts to know how well company is performing in market so that they can feel secure

and safe. On the other hand employees that are working in financial department of firm

used company account as part of their respective duties to prepare financial statement at

the end of year.

External user of company accounts

There are different types of external user of account information such as Investors,

suppliers, customers, tax authorities, auditors and general public. Like:

Investors: These are people that have invested their money or capital in business so by

evaluating and analysis financial statements they are able to know how well their

investment is performing. Thus, they are able to know amount of risk, profitability and

current value of investment that are useful in taking accurate decision to further invest in

business or not for better return on capital.

Suppliers/ lender/ creditors: Company needs various raw material or goods in order to

manufactured finished products that can be renders to end customers. Therefore,

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

suppliers before lending credit need to analysis financial position that is total profit, sales

volume and market position in order to know credit worthiness of its customers (Faccia

and Mosco, 2019). So, it helps them to take decision regarding whether credit need to be

given or not and amount to which it should be allocated.

Customers/ public: They are people or industrial customers which required financial

information to know about that it will have steady supply of goods in future circumstance

or not. People that are activist, academics, analysts or interest in knowing financial

statements of company to know the way these firm have contributed in economic growth

and development.

Auditors: It can be stated that auditors are responsible for creating audit report of

company based on its financial accounts so that external parties such as investors and

customers or interest stakeholder can trust the report and make decision accordingly.

Government/ IRS

It is third group of user of company accounts as government agencies in order to

evaluate or track tax record of company make use of business accounts. This helps government

to know that whether companies have pay tax as per current tax law or not (Maisuradze, 2018).

Tax auditors also review amount of money that needs to be paid by firm as tax which can

contribute economic growth and sustainability.

B) Advantages and disadvantages of financial reporting regime for perspective from both

user and prepare of financial statements

Financial statements are used by investor or market research to know about healthy

financial position of firm in competitive market condition. Regime financial report has both

advantages and disadvantages as per view of user and prepare of financial statements that can be

illustrated as follows:

Advantages of Financial report

Monitor and evaluation of operation procedure: It can be stated that regime or

standard financial report helps in effectively evaluating whether business in running

better or not (Mistary, 2020). It helps in identifying key performance indicators of

business thus contributed in building strong brand image of firm.

Manager can easily control operation of business: Accurate financial report helps

management of business to take corrective action to improve performance of business.

10

volume and market position in order to know credit worthiness of its customers (Faccia

and Mosco, 2019). So, it helps them to take decision regarding whether credit need to be

given or not and amount to which it should be allocated.

Customers/ public: They are people or industrial customers which required financial

information to know about that it will have steady supply of goods in future circumstance

or not. People that are activist, academics, analysts or interest in knowing financial

statements of company to know the way these firm have contributed in economic growth

and development.

Auditors: It can be stated that auditors are responsible for creating audit report of

company based on its financial accounts so that external parties such as investors and

customers or interest stakeholder can trust the report and make decision accordingly.

Government/ IRS

It is third group of user of company accounts as government agencies in order to

evaluate or track tax record of company make use of business accounts. This helps government

to know that whether companies have pay tax as per current tax law or not (Maisuradze, 2018).

Tax auditors also review amount of money that needs to be paid by firm as tax which can

contribute economic growth and sustainability.

B) Advantages and disadvantages of financial reporting regime for perspective from both

user and prepare of financial statements

Financial statements are used by investor or market research to know about healthy

financial position of firm in competitive market condition. Regime financial report has both

advantages and disadvantages as per view of user and prepare of financial statements that can be

illustrated as follows:

Advantages of Financial report

Monitor and evaluation of operation procedure: It can be stated that regime or

standard financial report helps in effectively evaluating whether business in running

better or not (Mistary, 2020). It helps in identifying key performance indicators of

business thus contributed in building strong brand image of firm.

Manager can easily control operation of business: Accurate financial report helps

management of business to take corrective action to improve performance of business.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Manager by analysing financial statements is able to find areas in which company lack

thus able to find better strategies for growth and success of enterprise.

Helps in improving performance of employees: It can be stated that maintenance of

financial as per standard helps in raising morale and motivation level of individual to

work hard so that company can gain competitive advantages. Employees by knowing

good financial position of firm are motivated to put their best so that it can easily expand

its business operation across worldwide.

Customers or user are more satisfied: People while selecting particular company

products and services rely on brand image, financial position of firm so that they can get

best qualitative products at reasonable rates (Faccia and Mosco, 2019). Therefore

accurate financial statement helps in building trust and motivating people to select

specific products and services of firm for satisfaction of their basic requirements.

Evaluation of investment: Regime financial statement provides ease and comfort to

investors to easily evaluates various alternative options of investment that company have

used in past. So, by evaluating investment alternative investors is able to take decision to

invest in particular field to get maximum outcome.

Thus, company can easily find strategies that it can use in future circumstances to gain

competitive advantages or expand overall profitability, market share of firm.

Disadvantages of Financial report

Despite of various advantages of regime financial report that are certain disadvantages of

financial report of company that are illustrated as follows:

Record only monetary transaction: Financial statements mainly includes transaction

that can be measured or enumerated in terms of money so there is no record of non-

financial transaction that have contributed in effective growth and success of enterprise

(Pelekh, Khocha and Holovchak, 2020). Therefore it hides qualitative information of

business such as hard working employees that are more important than quantitative data.

Time consuming: Another disadvantage of regime financial record is that it involves lot

of time, money and efforts to be invested to present correct statement to interested

parties. At the same time it is too expensive or lead to addition of cost as company in

order to prepared accurate financial statement have to hired people that have highly

skilled, knowledge and experienced.

11

thus able to find better strategies for growth and success of enterprise.

Helps in improving performance of employees: It can be stated that maintenance of

financial as per standard helps in raising morale and motivation level of individual to

work hard so that company can gain competitive advantages. Employees by knowing

good financial position of firm are motivated to put their best so that it can easily expand

its business operation across worldwide.

Customers or user are more satisfied: People while selecting particular company

products and services rely on brand image, financial position of firm so that they can get

best qualitative products at reasonable rates (Faccia and Mosco, 2019). Therefore

accurate financial statement helps in building trust and motivating people to select

specific products and services of firm for satisfaction of their basic requirements.

Evaluation of investment: Regime financial statement provides ease and comfort to

investors to easily evaluates various alternative options of investment that company have

used in past. So, by evaluating investment alternative investors is able to take decision to

invest in particular field to get maximum outcome.

Thus, company can easily find strategies that it can use in future circumstances to gain

competitive advantages or expand overall profitability, market share of firm.

Disadvantages of Financial report

Despite of various advantages of regime financial report that are certain disadvantages of

financial report of company that are illustrated as follows:

Record only monetary transaction: Financial statements mainly includes transaction

that can be measured or enumerated in terms of money so there is no record of non-

financial transaction that have contributed in effective growth and success of enterprise

(Pelekh, Khocha and Holovchak, 2020). Therefore it hides qualitative information of

business such as hard working employees that are more important than quantitative data.

Time consuming: Another disadvantage of regime financial record is that it involves lot

of time, money and efforts to be invested to present correct statement to interested

parties. At the same time it is too expensive or lead to addition of cost as company in

order to prepared accurate financial statement have to hired people that have highly

skilled, knowledge and experienced.

11

Difficult to understand: Sometimes technical financial reports of business are difficult

to understand by individual or stakeholders that are interested in operation of company.

Therefore it may act as disadvantages for user of financial records of firm for respective

purposes.

C) Limitation of Financial statement

Manager or any individual need to be aware of limitation of financial statement before

making use of its for different purposes such as based on historical cost, personal judgements and

inflation effects. Therefore various limitation of financial statement are discussed as follows:

Historical cost: It can be illustrated that financial statements are mostly based on

original or historical cost which contributed in decreasing value of asset over passage of

time because it have not considered actual or current prices of assets (Chen and et.al.,

2018). Sometimes income statement shows increase in profitability of company which

may be due to increased in prices or abnormal cause. Therefore it might state that

financial statements are unable to state accurate or fair pictures of total profit earned

during particular financial year.

Only interim report: Most of the data given in financial report are approximately so

accurate position of business can only find in case of liquidation or dissolution of

business. Individual on basis of its personal judgement may allocate cost and incomes to

different period with objectives to determine or represent more profit margins. Therefore

they are just interim report as they hide actual or final picture of firm in competitive

market.

Inflation: Another limitation of financial statement is that it does not consider effects or

impact of inflation on liabilities and assets of firm that are showed in balance sheet

(Malau and Murwaningsari, 2018). Thus, in case of high inflation balance show

sustainable low value thus mislead user of financial statements.

Specific time period: There are various or several changes in environment that needs to

be adapted by business in order to retain its market share and profitability. These

statements are prepared by enterprise for specific time period that is one month or year so

considering such period only may mislead as there are different changes in environment.

Not comparable: Companies in order to know their position in market make use of

financial statements so it is just an indication which means it does not depict true picture

12

to understand by individual or stakeholders that are interested in operation of company.

Therefore it may act as disadvantages for user of financial records of firm for respective

purposes.

C) Limitation of Financial statement

Manager or any individual need to be aware of limitation of financial statement before

making use of its for different purposes such as based on historical cost, personal judgements and

inflation effects. Therefore various limitation of financial statement are discussed as follows:

Historical cost: It can be illustrated that financial statements are mostly based on

original or historical cost which contributed in decreasing value of asset over passage of

time because it have not considered actual or current prices of assets (Chen and et.al.,

2018). Sometimes income statement shows increase in profitability of company which

may be due to increased in prices or abnormal cause. Therefore it might state that

financial statements are unable to state accurate or fair pictures of total profit earned

during particular financial year.

Only interim report: Most of the data given in financial report are approximately so

accurate position of business can only find in case of liquidation or dissolution of

business. Individual on basis of its personal judgement may allocate cost and incomes to

different period with objectives to determine or represent more profit margins. Therefore

they are just interim report as they hide actual or final picture of firm in competitive

market.

Inflation: Another limitation of financial statement is that it does not consider effects or

impact of inflation on liabilities and assets of firm that are showed in balance sheet

(Malau and Murwaningsari, 2018). Thus, in case of high inflation balance show

sustainable low value thus mislead user of financial statements.

Specific time period: There are various or several changes in environment that needs to

be adapted by business in order to retain its market share and profitability. These

statements are prepared by enterprise for specific time period that is one month or year so

considering such period only may mislead as there are different changes in environment.

Not comparable: Companies in order to know their position in market make use of

financial statements so it is just an indication which means it does not depict true picture

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.