Comprehensive Report: Analyzing Watley's Financial Performance

VerifiedAdded on 2023/06/08

|8

|2065

|250

Report

AI Summary

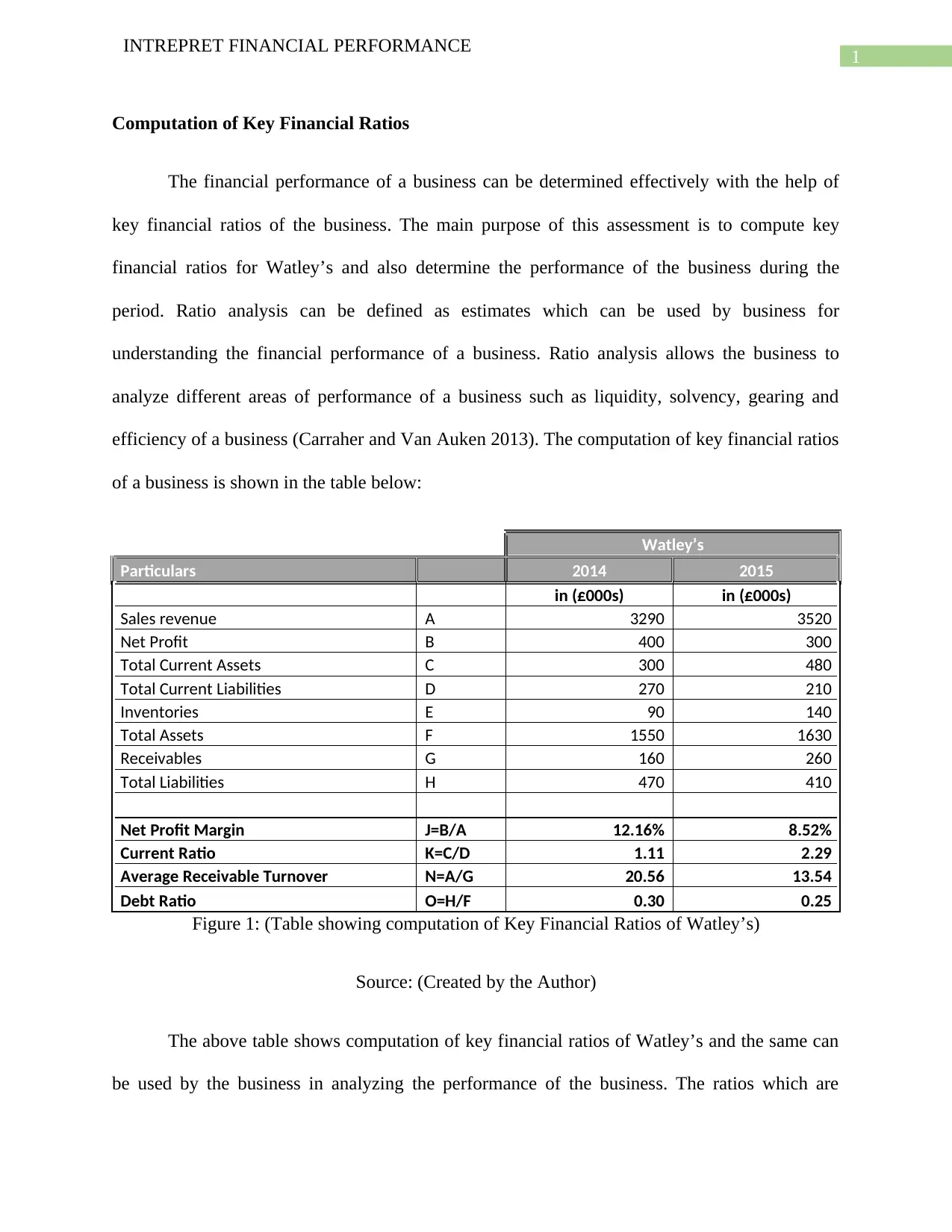

This report provides a comprehensive analysis of Watley's financial performance using key financial ratios for the years 2014 and 2015. It computes and analyzes ratios such as net profit margin, current ratio, average receivable turnover, and debt ratio to assess the company's profitability, liquidity, efficiency, and solvency. The analysis reveals a decrease in net profit margin from 12.16% in 2014 to 8.52% in 2015, indicating a potential issue with sales or cost management. The current ratio improved significantly, suggesting better liquidity. However, the average receivable turnover decreased, pointing to reduced efficiency in debt collection. The debt ratio also slightly decreased, indicating a reduction in debt. The report concludes with management recommendations to improve profitability and efficiency.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.