Financial Analysis Report: Watley's Manufacturing Company Performance

VerifiedAdded on 2022/02/15

|8

|2535

|13

Report

AI Summary

This report presents a financial analysis of Watley's Manufacturing Company, focusing on its performance in 2014 and 2015. The analysis employs four key financial ratios: liquidity, gearing, activity, and profitability. Liquidity ratios, including the current and quick ratios, indicate Watley's strong ability to meet short-term obligations. Gearing ratios demonstrate a low level of financial risk, suggesting a financially secure position. Activity ratios reveal an increase in inventory, implying slower sales than anticipated. Finally, the profitability ratios, specifically the ROCE, highlight a slight decline in profit margins, suggesting areas for improvement. The report concludes with recommendations for Watley's to enhance its financial performance by improving its revenue and decreasing expenses.

Financial Analysis for Watley’s Manufacturing Company

Intro:

Financial statements are reports that include statistics and information about the company and aid

management in evaluating the financial activities of the organization. by implementing the use of

financial ratio analysis, these statements help forecast the company's future growth. Financial ratios can

be used to evaluate a company's financial health.

Financial ratios can also measure the performance of a company for a certain accounting period and can

anticipate what the financial performance of the firm will be in the future. However, using ratio analysis

as a performance evaluation tool has a few drawbacks, since the figure that they provide are absolute

and not relative thus sometimes offering misleading information.

To begin with, the data derived from the previous accounting year's financial statements is underlined

as historical data, which implies that organizations cannot be certain that the same figures from

previous performance analysis would be maintained in the future. As a result, a ratio study for a single

period cannot always predict the company's performance would have the same corresponding future as

it had before. Furthermore, because financial statements are produced on a regular basis, another

limitation could be inflation within the market which they play a part in.

If there is inflation within the periods of accounting, the real prices will not be represented in the

financial accounts, making comparisons between periods impossible.The four basic categories of

financial ratios are as stated liquidity ratios, gearing ratios, activity ratios, and profitability ratios. The

goal of this article is to use these four financial ratios to analyze Watley's financial performance. In a

nutshell, Watley's is a tiny furniture manufacturing firm established in England that has 52 people and

specializes employed they specialize in putting together high-end furniture.

Overall, a financial analysis for Watley's will be undertaken in this report, with financial ratios being used

to calculate and then assess data for the years 2014 and 2015. This study evaluates the topic using both

primary and secondary data. Academic literature and financial information from Watley's Manufacturing

Company were used to compile the statistical results. Finally, a conclusion will be reached regarding the

company's financial health and what Watley's should change for the better of the companies financial

future.

Ratio Analysis:

Liquidity Ratios:

Liquidity ratios are used by businesses to assess their cash situation and ability to pay off

all of their short-term commitments. Thus a company's liquidity is defined by how fast it

can liquidate assets, or how it's assets can be converted into cash quickly(Atrill and

McLaney, 2019). The Current and Quick Ratios, are the two most critical liquidity ratios.

The current ratio, on the one hand, assesses a company's capacity to pay current

liabilities with current assets. To put it differently, the current ratio examines the

Intro:

Financial statements are reports that include statistics and information about the company and aid

management in evaluating the financial activities of the organization. by implementing the use of

financial ratio analysis, these statements help forecast the company's future growth. Financial ratios can

be used to evaluate a company's financial health.

Financial ratios can also measure the performance of a company for a certain accounting period and can

anticipate what the financial performance of the firm will be in the future. However, using ratio analysis

as a performance evaluation tool has a few drawbacks, since the figure that they provide are absolute

and not relative thus sometimes offering misleading information.

To begin with, the data derived from the previous accounting year's financial statements is underlined

as historical data, which implies that organizations cannot be certain that the same figures from

previous performance analysis would be maintained in the future. As a result, a ratio study for a single

period cannot always predict the company's performance would have the same corresponding future as

it had before. Furthermore, because financial statements are produced on a regular basis, another

limitation could be inflation within the market which they play a part in.

If there is inflation within the periods of accounting, the real prices will not be represented in the

financial accounts, making comparisons between periods impossible.The four basic categories of

financial ratios are as stated liquidity ratios, gearing ratios, activity ratios, and profitability ratios. The

goal of this article is to use these four financial ratios to analyze Watley's financial performance. In a

nutshell, Watley's is a tiny furniture manufacturing firm established in England that has 52 people and

specializes employed they specialize in putting together high-end furniture.

Overall, a financial analysis for Watley's will be undertaken in this report, with financial ratios being used

to calculate and then assess data for the years 2014 and 2015. This study evaluates the topic using both

primary and secondary data. Academic literature and financial information from Watley's Manufacturing

Company were used to compile the statistical results. Finally, a conclusion will be reached regarding the

company's financial health and what Watley's should change for the better of the companies financial

future.

Ratio Analysis:

Liquidity Ratios:

Liquidity ratios are used by businesses to assess their cash situation and ability to pay off

all of their short-term commitments. Thus a company's liquidity is defined by how fast it

can liquidate assets, or how it's assets can be converted into cash quickly(Atrill and

McLaney, 2019). The Current and Quick Ratios, are the two most critical liquidity ratios.

The current ratio, on the one hand, assesses a company's capacity to pay current

liabilities with current assets. To put it differently, the current ratio examines the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Analysis for Watley’s Manufacturing Company

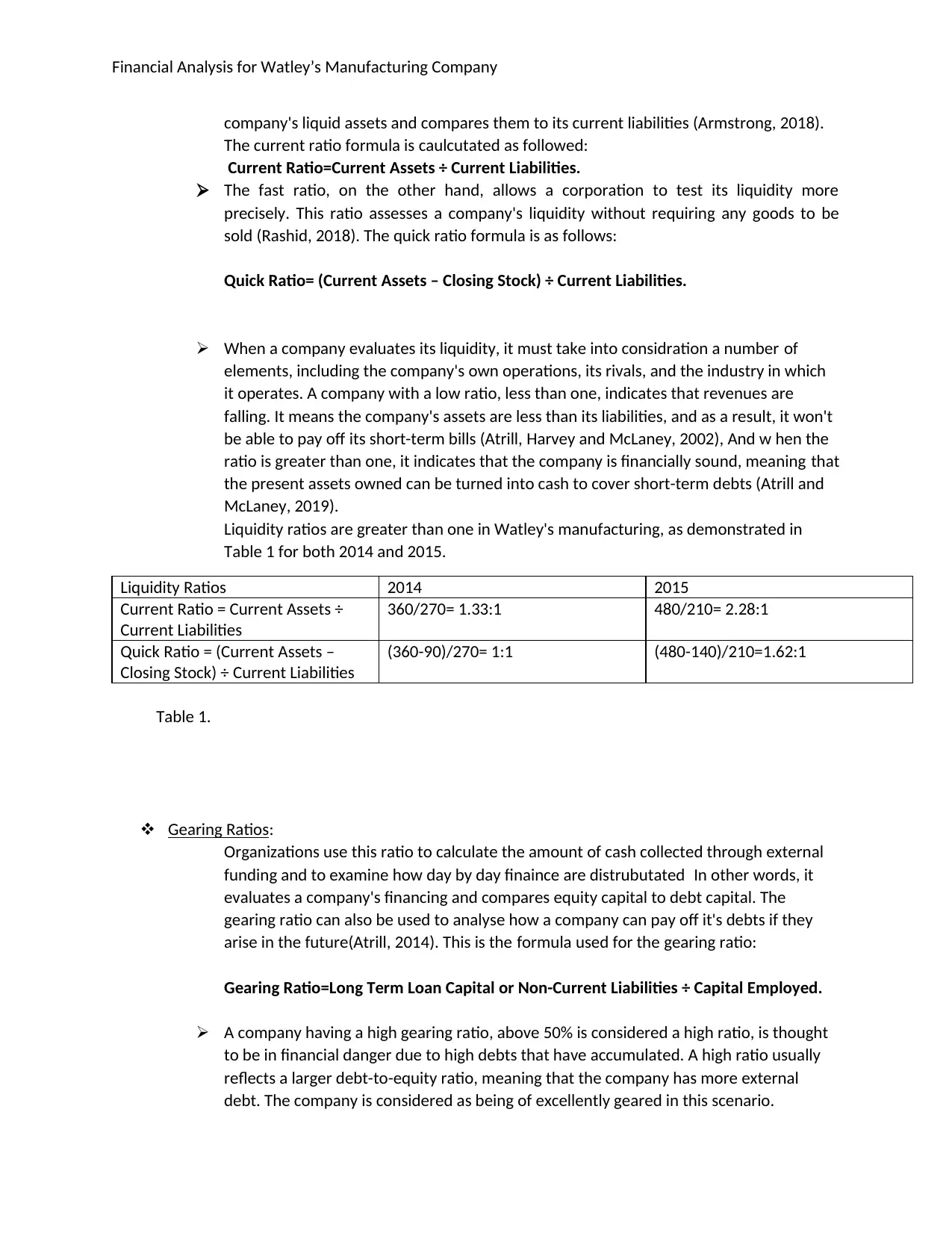

company's liquid assets and compares them to its current liabilities (Armstrong, 2018).

The current ratio formula is caulcutated as followed:

Current Ratio=Current Assets ÷ Current Liabilities.

The fast ratio, on the other hand, allows a corporation to test its liquidity more

precisely. This ratio assesses a company's liquidity without requiring any goods to be

sold (Rashid, 2018). The quick ratio formula is as follows:

Quick Ratio= (Current Assets – Closing Stock) ÷ Current Liabilities.

When a company evaluates its liquidity, it must take into considration a number of

elements, including the company's own operations, its rivals, and the industry in which

it operates. A company with a low ratio, less than one, indicates that revenues are

falling. It means the company's assets are less than its liabilities, and as a result, it won't

be able to pay off its short-term bills (Atrill, Harvey and McLaney, 2002), And w hen the

ratio is greater than one, it indicates that the company is financially sound, meaning that

the present assets owned can be turned into cash to cover short-term debts (Atrill and

McLaney, 2019).

Liquidity ratios are greater than one in Watley's manufacturing, as demonstrated in

Table 1 for both 2014 and 2015.

Liquidity Ratios 2014 2015

Current Ratio = Current Assets ÷

Current Liabilities

360/270= 1.33:1 480/210= 2.28:1

Quick Ratio = (Current Assets –

Closing Stock) ÷ Current Liabilities

(360-90)/270= 1:1 (480-140)/210=1.62:1

Table 1.

Gearing Ratios:

Organizations use this ratio to calculate the amount of cash collected through external

funding and to examine how day by day finaince are distrubutated In other words, it

evaluates a company's financing and compares equity capital to debt capital. The

gearing ratio can also be used to analyse how a company can pay off it's debts if they

arise in the future(Atrill, 2014). This is the formula used for the gearing ratio:

Gearing Ratio=Long Term Loan Capital or Non-Current Liabilities ÷ Capital Employed.

A company having a high gearing ratio, above 50% is considered a high ratio, is thought

to be in financial danger due to high debts that have accumulated. A high ratio usually

reflects a larger debt-to-equity ratio, meaning that the company has more external

debt. The company is considered as being of excellently geared in this scenario.

company's liquid assets and compares them to its current liabilities (Armstrong, 2018).

The current ratio formula is caulcutated as followed:

Current Ratio=Current Assets ÷ Current Liabilities.

The fast ratio, on the other hand, allows a corporation to test its liquidity more

precisely. This ratio assesses a company's liquidity without requiring any goods to be

sold (Rashid, 2018). The quick ratio formula is as follows:

Quick Ratio= (Current Assets – Closing Stock) ÷ Current Liabilities.

When a company evaluates its liquidity, it must take into considration a number of

elements, including the company's own operations, its rivals, and the industry in which

it operates. A company with a low ratio, less than one, indicates that revenues are

falling. It means the company's assets are less than its liabilities, and as a result, it won't

be able to pay off its short-term bills (Atrill, Harvey and McLaney, 2002), And w hen the

ratio is greater than one, it indicates that the company is financially sound, meaning that

the present assets owned can be turned into cash to cover short-term debts (Atrill and

McLaney, 2019).

Liquidity ratios are greater than one in Watley's manufacturing, as demonstrated in

Table 1 for both 2014 and 2015.

Liquidity Ratios 2014 2015

Current Ratio = Current Assets ÷

Current Liabilities

360/270= 1.33:1 480/210= 2.28:1

Quick Ratio = (Current Assets –

Closing Stock) ÷ Current Liabilities

(360-90)/270= 1:1 (480-140)/210=1.62:1

Table 1.

Gearing Ratios:

Organizations use this ratio to calculate the amount of cash collected through external

funding and to examine how day by day finaince are distrubutated In other words, it

evaluates a company's financing and compares equity capital to debt capital. The

gearing ratio can also be used to analyse how a company can pay off it's debts if they

arise in the future(Atrill, 2014). This is the formula used for the gearing ratio:

Gearing Ratio=Long Term Loan Capital or Non-Current Liabilities ÷ Capital Employed.

A company having a high gearing ratio, above 50% is considered a high ratio, is thought

to be in financial danger due to high debts that have accumulated. A high ratio usually

reflects a larger debt-to-equity ratio, meaning that the company has more external

debt. The company is considered as being of excellently geared in this scenario.

Financial Analysis for Watley’s Manufacturing Company

Furthermore, a company with a low ratio, less than 25%, is thought to be more

financially sound because it has raised a large portion of its capital through equity. As a

result, it looks to pose fewer financial risks to outside investors and is classified as low

geared. Additionally, a gearing ratio of 25 to 50 percent is regarded standard and

indicates a solid, well-established business. Without a doubt, if the company's gearing

ratio is excessive, there are various options for lowering it and paying off the debt,

including selling stock, converting loans, or increasing profits (Atrill, Harvey and

McLaney, 2002).

Gearing Ratios 2014 2015

GR= non-current liabilities/Capital

Employed

200/ (1080+200) =0.16=16% 200/ (1220+200) = 0.14 = 14%

Table 2.

As indicated in Table 2, the gearing ratio for Watley's manufacturing in 2014 and 2015 was

less than 25, indicating that the company is financially secure and less hazardous for its

investors. The gearing ratio decreased from 2014 to 2015 as equity increased and non-

current liabilities stayed unchanged.

Activity Ratios:

This ratio is used to shows how a company us well equipped to convert it’s inventory

into cash, these ratios are kind of significant since they show how a company operates.

The Inventory turn over shows how well a company maintain their inventory through

holding and distribution. This ratio changes with the cost of products sold, how many

times the inventory is stocked and sold and all of this is over a period of time to

determine the Activity ratio (Atrill and McLaney, 2019).

When companies have bad inventory turnovers, this demonstrates that the company

has/will fail to sale in a period which it’s supposed to. Low sales might end up costing

the company looses and this is called overstocking, when the current inventory exceeds

the time, it’s needed to sell it. When the turnover ratio is high this helps us determine

that the company has high sale ratios, the corporation that can quickly change their

inventory into cash from sales are consider and highly regarded as investment havens.

Below is the Formula for calculating Activity ratio and Turnover:

Activity ratio=Sales or Costs of Goods Sold ÷ Inventory.

Furthermore, a company with a low ratio, less than 25%, is thought to be more

financially sound because it has raised a large portion of its capital through equity. As a

result, it looks to pose fewer financial risks to outside investors and is classified as low

geared. Additionally, a gearing ratio of 25 to 50 percent is regarded standard and

indicates a solid, well-established business. Without a doubt, if the company's gearing

ratio is excessive, there are various options for lowering it and paying off the debt,

including selling stock, converting loans, or increasing profits (Atrill, Harvey and

McLaney, 2002).

Gearing Ratios 2014 2015

GR= non-current liabilities/Capital

Employed

200/ (1080+200) =0.16=16% 200/ (1220+200) = 0.14 = 14%

Table 2.

As indicated in Table 2, the gearing ratio for Watley's manufacturing in 2014 and 2015 was

less than 25, indicating that the company is financially secure and less hazardous for its

investors. The gearing ratio decreased from 2014 to 2015 as equity increased and non-

current liabilities stayed unchanged.

Activity Ratios:

This ratio is used to shows how a company us well equipped to convert it’s inventory

into cash, these ratios are kind of significant since they show how a company operates.

The Inventory turn over shows how well a company maintain their inventory through

holding and distribution. This ratio changes with the cost of products sold, how many

times the inventory is stocked and sold and all of this is over a period of time to

determine the Activity ratio (Atrill and McLaney, 2019).

When companies have bad inventory turnovers, this demonstrates that the company

has/will fail to sale in a period which it’s supposed to. Low sales might end up costing

the company looses and this is called overstocking, when the current inventory exceeds

the time, it’s needed to sell it. When the turnover ratio is high this helps us determine

that the company has high sale ratios, the corporation that can quickly change their

inventory into cash from sales are consider and highly regarded as investment havens.

Below is the Formula for calculating Activity ratio and Turnover:

Activity ratio=Sales or Costs of Goods Sold ÷ Inventory.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Analysis for Watley’s Manufacturing Company

In the financial statement we can see that Watly’s manufacturing had an incress in

inventory from the years 2014 t 2015. To be more precises the number of inventory

increased from 90 to 140 in a year which means sales were not as anticipated

Table 3.

Activity Ratios 2014 2015

Inventory Turnover=

Sales/Inventory

1290/90= 14.33 1500/140= 10.71

Profitability Ratios:

This ratio helps identify the profitability of a company over a certain amount of time.

ROCE is how a company efficiently evaluates how they earn their profits from capital

invested and is one of the most basic measures of business success. The Company’s

long-term capital and equity is referred to as capital employed (Boute, 2007). The

(ROCE) is used to calculate the money made and compering it to the operational profit

to capital employed (Atrill and McLaney, 2019). For the record, when the profitability

ratios are higher than the competitors that are compared, show how well and better the

company is performing.

Down below is the formula for calculating the ROCE ratio:

ROCE= Operating Profit ÷ Capital employed.

In 2014,Watley's manufacturing ROCE ratio, as shown in Table 4, reveals that Watley's

For every pound makes 0.33 pence, in the financial statement of 2015 the company has

earned 0.23 pence per pound invested which show a small decline in profits with in the

two-year comparisons. So for the upcoming year they should focus on inserting their

revenue for the fiscal year.

Table 4.

Profitability Ratios 2014 2015 2014 2015

ROCE= Operating Profit/ Capital

Employed

420/1280= 0.33 = 33% 320/ 1420= 0.23= 23%

The ROCE can be further better in many ways, Firstly by lowering costs on goods sold,

second, on increasing pricing of the luxury items sold, or increasing the company’s

operational profits and net profit by decreasing expenses

(Rutkowska-Ziarko, 2015; Atrill and McLaney, 2019). Another strategy to increase profits

is to refund the company's non-current liabilities and obligations. In that situation, the

amount of capital used will be lower, and the financial risks will be lower (Alexander and

Nobes 2013).

In the financial statement we can see that Watly’s manufacturing had an incress in

inventory from the years 2014 t 2015. To be more precises the number of inventory

increased from 90 to 140 in a year which means sales were not as anticipated

Table 3.

Activity Ratios 2014 2015

Inventory Turnover=

Sales/Inventory

1290/90= 14.33 1500/140= 10.71

Profitability Ratios:

This ratio helps identify the profitability of a company over a certain amount of time.

ROCE is how a company efficiently evaluates how they earn their profits from capital

invested and is one of the most basic measures of business success. The Company’s

long-term capital and equity is referred to as capital employed (Boute, 2007). The

(ROCE) is used to calculate the money made and compering it to the operational profit

to capital employed (Atrill and McLaney, 2019). For the record, when the profitability

ratios are higher than the competitors that are compared, show how well and better the

company is performing.

Down below is the formula for calculating the ROCE ratio:

ROCE= Operating Profit ÷ Capital employed.

In 2014,Watley's manufacturing ROCE ratio, as shown in Table 4, reveals that Watley's

For every pound makes 0.33 pence, in the financial statement of 2015 the company has

earned 0.23 pence per pound invested which show a small decline in profits with in the

two-year comparisons. So for the upcoming year they should focus on inserting their

revenue for the fiscal year.

Table 4.

Profitability Ratios 2014 2015 2014 2015

ROCE= Operating Profit/ Capital

Employed

420/1280= 0.33 = 33% 320/ 1420= 0.23= 23%

The ROCE can be further better in many ways, Firstly by lowering costs on goods sold,

second, on increasing pricing of the luxury items sold, or increasing the company’s

operational profits and net profit by decreasing expenses

(Rutkowska-Ziarko, 2015; Atrill and McLaney, 2019). Another strategy to increase profits

is to refund the company's non-current liabilities and obligations. In that situation, the

amount of capital used will be lower, and the financial risks will be lower (Alexander and

Nobes 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Analysis for Watley’s Manufacturing Company

Conclusion:

In this report we examined Watley’s Manufacturing's financial performance within the

given two year periods of 2014 and 2015 while using the four key ratios every business

uses to calculate it’s financial interests and risks. These ratios being liquidity, Gearing,

Activity, and profitability ratios. Each ratio has its own formula of determining certain

aspects about a company through it financial statement

The liquidity ratios and gearing ratios for Watley's manufacturing company in the

years 2014 and 2015 shows that the company and it's business are at less financial risks,

and are financially stable, and is fully capable of fulfilling its short-term obligations to

pay any debt to external lenders when needed. While looking at the company’s activity

ratio for both the years of 2014 and 2015, there was a surplus of inventory meaning the

company had more inventory than intend and failed to sale it with in the time while the

next ship f inventory was received, implies that the inventory retained has increased.

Similarly, the evidence for the ROCE ratio indicates that the corporation must commit to

boosting its return on capital employed in the coming year.

Reference:

Alexander, D. and Nobes, C. (2013) Financial accounting: an international introduction.

Pearson. Online via the Essex eLibrary.

Armstrong, L. (2018). How Liquidity Ratios Help You Understand Your Cash Position. [online]

Slcbookkeeping.com. Available at: https://www.slcbookkeeping.com/blog/how-liquidity-

ratios-help-you-understand-your-cash-position.

Atrill, P., Financial Management for Decision Makers, 7th edn, Pearson, 2014, Chapter 1.

Atrill, P. and McLaney, E. (2019) Accounting and Finance for Non-Specialists (11th Ed).

Harlow: Pearson Education

Atrill, P., Harvey, D. and McLaney, E. (2002). Accounting. 2nd ed. London: Prentice Hall.

Boute, R., Lambrecht, M., Lambrechts, O. and Sterckx, P. (2007). An Analysis of Inventory

Turnover in the Belgian Manufacturing Industry, Wholesale and Retail and the Financial

Impact on Inventory Reduction. SSRN Electronic Journal.

Ratios Analysis for Evaluating Companies’ Liquidity. International Journal of Social Sciences

& educational Studies, 4(4), pp.110-123. Rutkowska-Ziarko, A. (2015).

Conclusion:

In this report we examined Watley’s Manufacturing's financial performance within the

given two year periods of 2014 and 2015 while using the four key ratios every business

uses to calculate it’s financial interests and risks. These ratios being liquidity, Gearing,

Activity, and profitability ratios. Each ratio has its own formula of determining certain

aspects about a company through it financial statement

The liquidity ratios and gearing ratios for Watley's manufacturing company in the

years 2014 and 2015 shows that the company and it's business are at less financial risks,

and are financially stable, and is fully capable of fulfilling its short-term obligations to

pay any debt to external lenders when needed. While looking at the company’s activity

ratio for both the years of 2014 and 2015, there was a surplus of inventory meaning the

company had more inventory than intend and failed to sale it with in the time while the

next ship f inventory was received, implies that the inventory retained has increased.

Similarly, the evidence for the ROCE ratio indicates that the corporation must commit to

boosting its return on capital employed in the coming year.

Reference:

Alexander, D. and Nobes, C. (2013) Financial accounting: an international introduction.

Pearson. Online via the Essex eLibrary.

Armstrong, L. (2018). How Liquidity Ratios Help You Understand Your Cash Position. [online]

Slcbookkeeping.com. Available at: https://www.slcbookkeeping.com/blog/how-liquidity-

ratios-help-you-understand-your-cash-position.

Atrill, P., Financial Management for Decision Makers, 7th edn, Pearson, 2014, Chapter 1.

Atrill, P. and McLaney, E. (2019) Accounting and Finance for Non-Specialists (11th Ed).

Harlow: Pearson Education

Atrill, P., Harvey, D. and McLaney, E. (2002). Accounting. 2nd ed. London: Prentice Hall.

Boute, R., Lambrecht, M., Lambrechts, O. and Sterckx, P. (2007). An Analysis of Inventory

Turnover in the Belgian Manufacturing Industry, Wholesale and Retail and the Financial

Impact on Inventory Reduction. SSRN Electronic Journal.

Ratios Analysis for Evaluating Companies’ Liquidity. International Journal of Social Sciences

& educational Studies, 4(4), pp.110-123. Rutkowska-Ziarko, A. (2015).

Financial Analysis for Watley’s Manufacturing Company

The Influence of Profitability Ratios and Company Size on Profitability and Investment Risk in

the Capital Market. Folia Oeconomica Stetinensia, 15(1), pp.151-161.

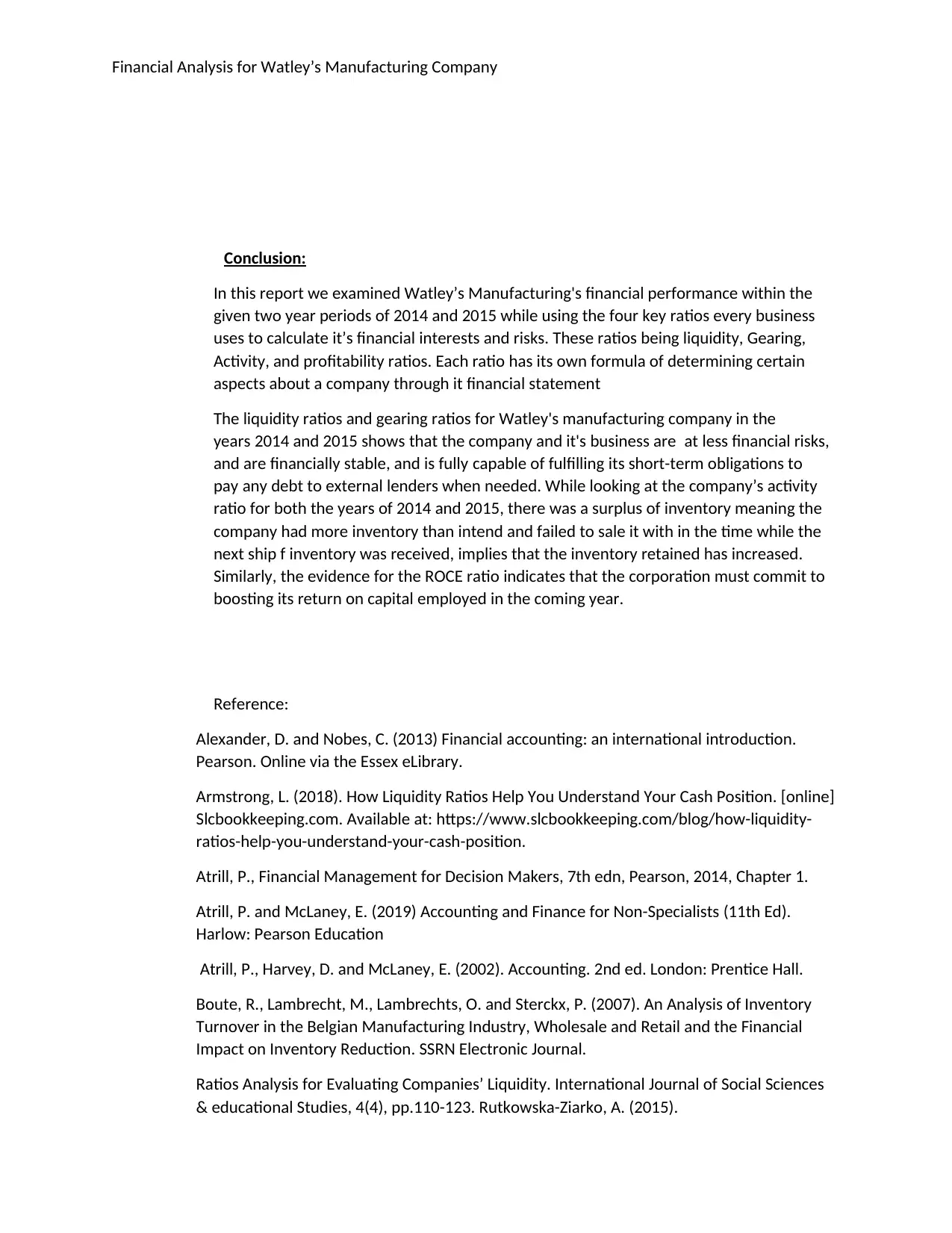

Ratio analysis:

Liquidity ratio

1) Current Ratio

Current ratio=Current assets ÷ Current Liabilities

2) Quick Ratio

Quick Ratio= (Current Assets – Closing Stock) ÷ Current Liabilities

Appendix B: Calculations Gearing Ratio

Year 2014 2015

Current Assets 360 480

Current Liabilities 270 210

2014 2015

360/270= 1.33 480/210=2.28

Year 2014 2015

Current Assets 360 480

Current Liabilities 270 210

Closing Stock (inventory) 90 140

2014 2015

(360-90)/270=1 (480-140)/210= 1.62

The Influence of Profitability Ratios and Company Size on Profitability and Investment Risk in

the Capital Market. Folia Oeconomica Stetinensia, 15(1), pp.151-161.

Ratio analysis:

Liquidity ratio

1) Current Ratio

Current ratio=Current assets ÷ Current Liabilities

2) Quick Ratio

Quick Ratio= (Current Assets – Closing Stock) ÷ Current Liabilities

Appendix B: Calculations Gearing Ratio

Year 2014 2015

Current Assets 360 480

Current Liabilities 270 210

2014 2015

360/270= 1.33 480/210=2.28

Year 2014 2015

Current Assets 360 480

Current Liabilities 270 210

Closing Stock (inventory) 90 140

2014 2015

(360-90)/270=1 (480-140)/210= 1.62

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Analysis for Watley’s Manufacturing Company

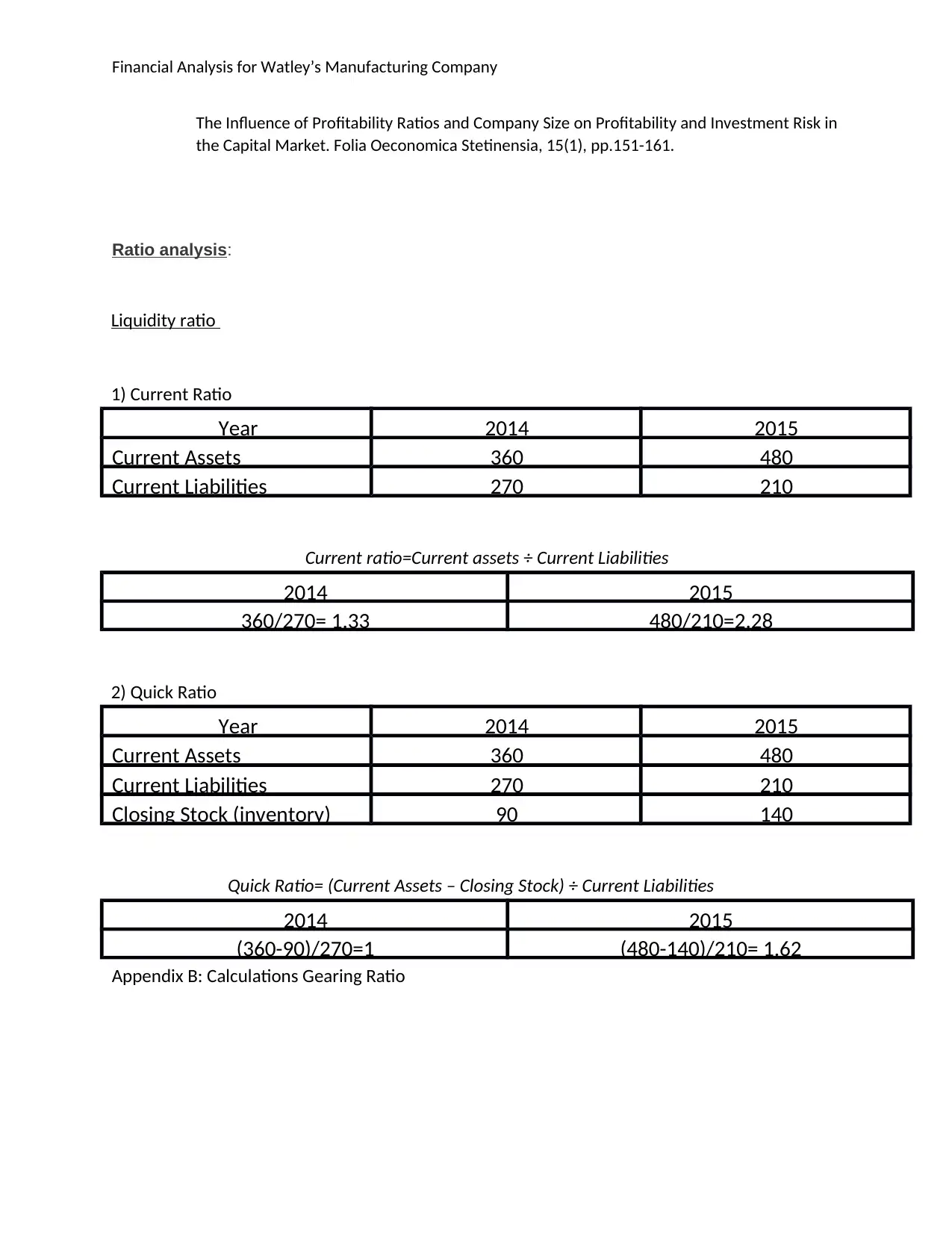

Gearing Ratio

Gearing Ratio=Long Term Loan Capital or Non-Current Liabilities ÷ Capital Employed

Appendix B: Calculations Activity

Ratio Activity Ratio

1) Inventory Turnover Ratio

Inventory turnover ratio=Sales or Costs of Goods Sold ÷ Inventory

Year 2014 2015

Non-Current Liabilities 200 200

Equity 1080 1220

2014 2015

200/(1080+200)=0.16=16% 200/(1220+200)=0.14-14%

Year 2014 2015

Cost Of Sales 1290 1500

Inventory 90 140

2014 2015

1290/90=14.33 1500/140=10.71

Gearing Ratio

Gearing Ratio=Long Term Loan Capital or Non-Current Liabilities ÷ Capital Employed

Appendix B: Calculations Activity

Ratio Activity Ratio

1) Inventory Turnover Ratio

Inventory turnover ratio=Sales or Costs of Goods Sold ÷ Inventory

Year 2014 2015

Non-Current Liabilities 200 200

Equity 1080 1220

2014 2015

200/(1080+200)=0.16=16% 200/(1220+200)=0.14-14%

Year 2014 2015

Cost Of Sales 1290 1500

Inventory 90 140

2014 2015

1290/90=14.33 1500/140=10.71

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Analysis for Watley’s Manufacturing Company

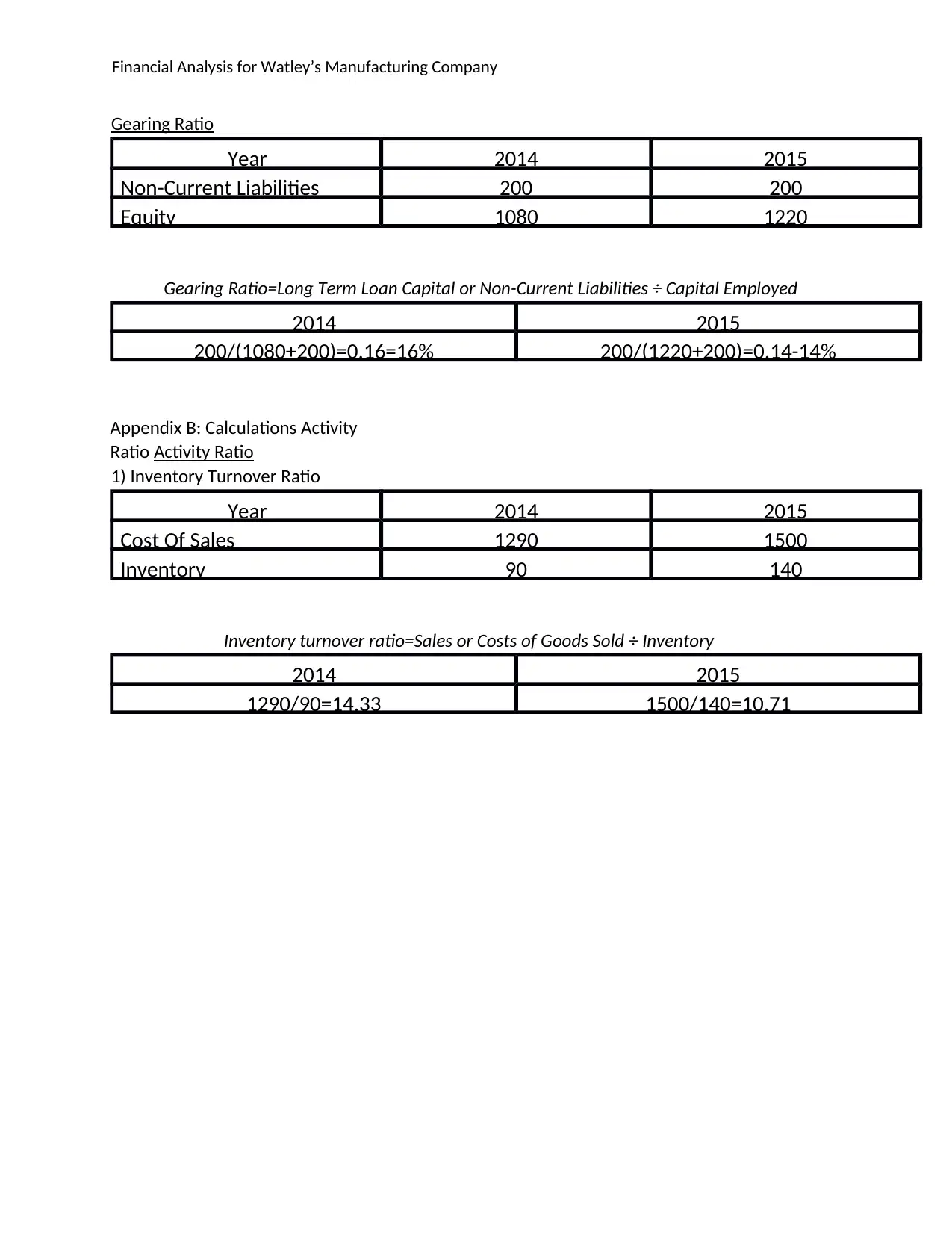

Appendix B: Calculations Profitability Ratio

Profitability Ratio

ROCE=Operating Profit ÷ Capital Employed

Return on Capital Employed Ratio1)

Year 2014 2015

Operating Profit 420 320

Equity 1080 1220

Non-Current Liabilities 200 200

2014 2015

420/1280=0.33=33% 320/1420=0.23-23%

Appendix B: Calculations Profitability Ratio

Profitability Ratio

ROCE=Operating Profit ÷ Capital Employed

Return on Capital Employed Ratio1)

Year 2014 2015

Operating Profit 420 320

Equity 1080 1220

Non-Current Liabilities 200 200

2014 2015

420/1280=0.33=33% 320/1420=0.23-23%

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.