Financial Planning and Personal Wealth Management Analysis Report

VerifiedAdded on 2022/11/11

|23

|4051

|133

Report

AI Summary

This report provides a comprehensive analysis of personal wealth management, focusing on a couple's (Dean and Hamish) financial situation. It includes a detailed examination of their life objectives (short, medium, and long term), personal details, balance sheet, income statement, and current financial position, which is assessed using various financial ratios (net worth, liquidity, savings, and debt service). The report further analyzes their asset allocation, projects their cash flow, and offers recommendations to improve their financial position, including refinancing their home loan and selling their car. It then provides an executive summary and dives into insurance product recommendations, specifically life, total and permanent disability, and income protection insurance for both individuals. The report also covers superannuation contribution strategies and provides justifications for the advice, discussing potential consequences, commissions, authority to proceed, and cooling-off periods. The assignment concludes with a bibliography.

Running head: PERSONAL WEALTH MANAGEMENT

Personal Wealth Management

Name of the Student:

Name of the University:

Author’s Note:

Personal Wealth Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

PERSONAL WEALTH MANAGEMENT

Table of Contents

Part A...............................................................................................................................................3

Life Objectives.............................................................................................................................3

Information about Dean and Hamish...........................................................................................3

Personal Details.......................................................................................................................3

Balance Sheet...........................................................................................................................4

Income Statement....................................................................................................................4

Current Financial Position...........................................................................................................5

Financial Ratios.......................................................................................................................5

Asset Allocation.......................................................................................................................5

Projected Cash Flow................................................................................................................7

Recommendation about your financial position..........................................................................7

Part B...............................................................................................................................................9

Executive Summary.....................................................................................................................9

Part C.............................................................................................................................................11

Insurance Product Recommendation.........................................................................................13

Insurance Needs for Dean..........................................................................................................13

Life Insurance........................................................................................................................13

Total and Permanent Disability Insurance.............................................................................14

Income Protection Insurance.................................................................................................14

PERSONAL WEALTH MANAGEMENT

Table of Contents

Part A...............................................................................................................................................3

Life Objectives.............................................................................................................................3

Information about Dean and Hamish...........................................................................................3

Personal Details.......................................................................................................................3

Balance Sheet...........................................................................................................................4

Income Statement....................................................................................................................4

Current Financial Position...........................................................................................................5

Financial Ratios.......................................................................................................................5

Asset Allocation.......................................................................................................................5

Projected Cash Flow................................................................................................................7

Recommendation about your financial position..........................................................................7

Part B...............................................................................................................................................9

Executive Summary.....................................................................................................................9

Part C.............................................................................................................................................11

Insurance Product Recommendation.........................................................................................13

Insurance Needs for Dean..........................................................................................................13

Life Insurance........................................................................................................................13

Total and Permanent Disability Insurance.............................................................................14

Income Protection Insurance.................................................................................................14

2

PERSONAL WEALTH MANAGEMENT

Insurance Need for Hamish.......................................................................................................15

Life Insurance........................................................................................................................15

Total Permanent Disability Insurance...................................................................................16

Income Protection Insurance.................................................................................................17

Superannuation Contribution Strategy for Dean and Hamish...................................................18

Reasons for Recommendation...................................................................................................18

How is my Advice Appropriate?...............................................................................................18

Consequences of advice.............................................................................................................19

Commissions..............................................................................................................................19

Authority to Proceed..................................................................................................................19

Cooling Off Period....................................................................................................................20

Bibliography..................................................................................................................................21

PERSONAL WEALTH MANAGEMENT

Insurance Need for Hamish.......................................................................................................15

Life Insurance........................................................................................................................15

Total Permanent Disability Insurance...................................................................................16

Income Protection Insurance.................................................................................................17

Superannuation Contribution Strategy for Dean and Hamish...................................................18

Reasons for Recommendation...................................................................................................18

How is my Advice Appropriate?...............................................................................................18

Consequences of advice.............................................................................................................19

Commissions..............................................................................................................................19

Authority to Proceed..................................................................................................................19

Cooling Off Period....................................................................................................................20

Bibliography..................................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

PERSONAL WEALTH MANAGEMENT

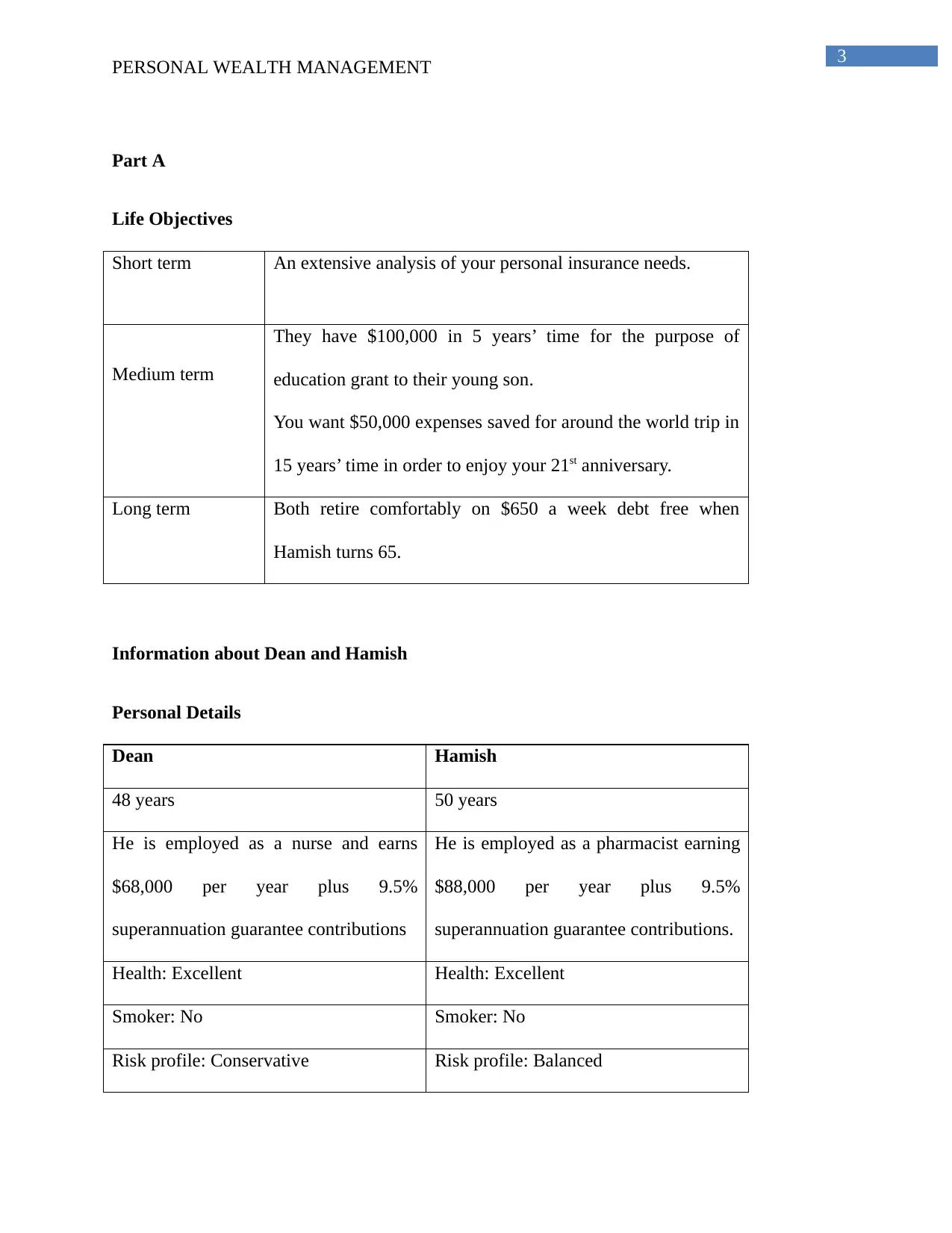

Part A

Life Objectives

Short term An extensive analysis of your personal insurance needs.

Medium term

They have $100,000 in 5 years’ time for the purpose of

education grant to their young son.

You want $50,000 expenses saved for around the world trip in

15 years’ time in order to enjoy your 21st anniversary.

Long term Both retire comfortably on $650 a week debt free when

Hamish turns 65.

Information about Dean and Hamish

Personal Details

Dean Hamish

48 years 50 years

He is employed as a nurse and earns

$68,000 per year plus 9.5%

superannuation guarantee contributions

He is employed as a pharmacist earning

$88,000 per year plus 9.5%

superannuation guarantee contributions.

Health: Excellent Health: Excellent

Smoker: No Smoker: No

Risk profile: Conservative Risk profile: Balanced

PERSONAL WEALTH MANAGEMENT

Part A

Life Objectives

Short term An extensive analysis of your personal insurance needs.

Medium term

They have $100,000 in 5 years’ time for the purpose of

education grant to their young son.

You want $50,000 expenses saved for around the world trip in

15 years’ time in order to enjoy your 21st anniversary.

Long term Both retire comfortably on $650 a week debt free when

Hamish turns 65.

Information about Dean and Hamish

Personal Details

Dean Hamish

48 years 50 years

He is employed as a nurse and earns

$68,000 per year plus 9.5%

superannuation guarantee contributions

He is employed as a pharmacist earning

$88,000 per year plus 9.5%

superannuation guarantee contributions.

Health: Excellent Health: Excellent

Smoker: No Smoker: No

Risk profile: Conservative Risk profile: Balanced

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

PERSONAL WEALTH MANAGEMENT

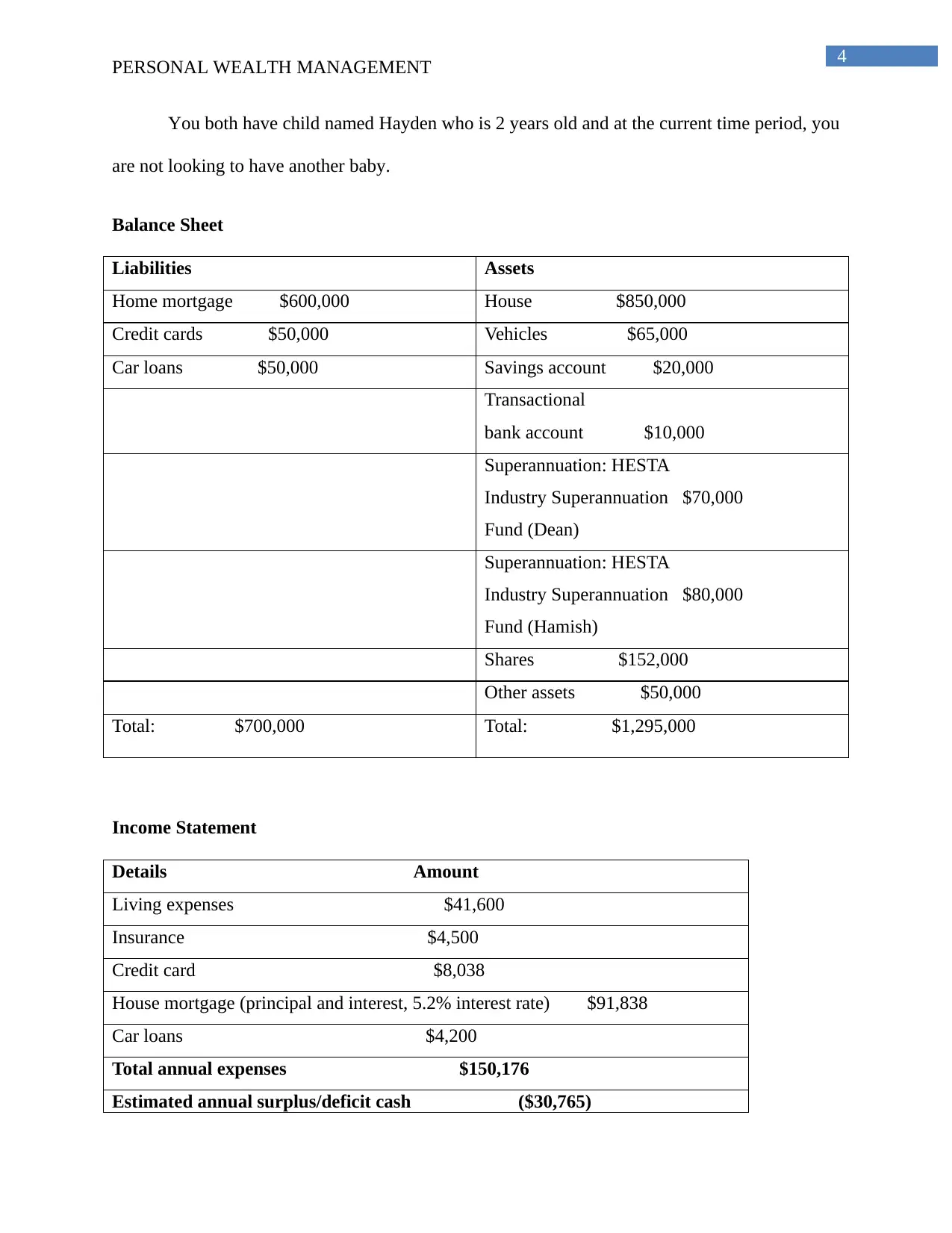

You both have child named Hayden who is 2 years old and at the current time period, you

are not looking to have another baby.

Balance Sheet

Liabilities Assets

Home mortgage $600,000 House $850,000

Credit cards $50,000 Vehicles $65,000

Car loans $50,000 Savings account $20,000

Transactional

bank account $10,000

Superannuation: HESTA

Industry Superannuation $70,000

Fund (Dean)

Superannuation: HESTA

Industry Superannuation $80,000

Fund (Hamish)

Shares $152,000

Other assets $50,000

Total: $700,000 Total: $1,295,000

Income Statement

Details Amount

Living expenses $41,600

Insurance $4,500

Credit card $8,038

House mortgage (principal and interest, 5.2% interest rate) $91,838

Car loans $4,200

Total annual expenses $150,176

Estimated annual surplus/deficit cash ($30,765)

PERSONAL WEALTH MANAGEMENT

You both have child named Hayden who is 2 years old and at the current time period, you

are not looking to have another baby.

Balance Sheet

Liabilities Assets

Home mortgage $600,000 House $850,000

Credit cards $50,000 Vehicles $65,000

Car loans $50,000 Savings account $20,000

Transactional

bank account $10,000

Superannuation: HESTA

Industry Superannuation $70,000

Fund (Dean)

Superannuation: HESTA

Industry Superannuation $80,000

Fund (Hamish)

Shares $152,000

Other assets $50,000

Total: $700,000 Total: $1,295,000

Income Statement

Details Amount

Living expenses $41,600

Insurance $4,500

Credit card $8,038

House mortgage (principal and interest, 5.2% interest rate) $91,838

Car loans $4,200

Total annual expenses $150,176

Estimated annual surplus/deficit cash ($30,765)

5

PERSONAL WEALTH MANAGEMENT

Current Financial Position

Financial Ratios

Net worth ratio

The net worth ratio calculated is 45.95%. Both of you own

45.95% of your assets while on the other hand your creditors

own 54.05%. This is not a favorable position to be in owning

lower than the amount that you to owe.

Liquidity ratio

Your liquidity ratio computed is 9.61%. This is seen to be a

bad scenario as you may not have sufficient cash to pay your

short-term debts.

Savings ratio As both of you pay an increased amount of mortgage the

savings ratio is negative and the value comes to -25.76%.

Monthly debt

service ratio

The monthly debt service ratio is 87.16% and this suggests

that 87.16% of the net income is going towards servicing

debt.

Asset Allocation

Dean

Asset class Asset allocation (%)

Cash 4.3

Fixed interest 11.1

Total defensive assets 15.4

Australian equities 54.9

International equities 5.3

Property 22.5

Alternative strategies (growth) 1.9

PERSONAL WEALTH MANAGEMENT

Current Financial Position

Financial Ratios

Net worth ratio

The net worth ratio calculated is 45.95%. Both of you own

45.95% of your assets while on the other hand your creditors

own 54.05%. This is not a favorable position to be in owning

lower than the amount that you to owe.

Liquidity ratio

Your liquidity ratio computed is 9.61%. This is seen to be a

bad scenario as you may not have sufficient cash to pay your

short-term debts.

Savings ratio As both of you pay an increased amount of mortgage the

savings ratio is negative and the value comes to -25.76%.

Monthly debt

service ratio

The monthly debt service ratio is 87.16% and this suggests

that 87.16% of the net income is going towards servicing

debt.

Asset Allocation

Dean

Asset class Asset allocation (%)

Cash 4.3

Fixed interest 11.1

Total defensive assets 15.4

Australian equities 54.9

International equities 5.3

Property 22.5

Alternative strategies (growth) 1.9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

PERSONAL WEALTH MANAGEMENT

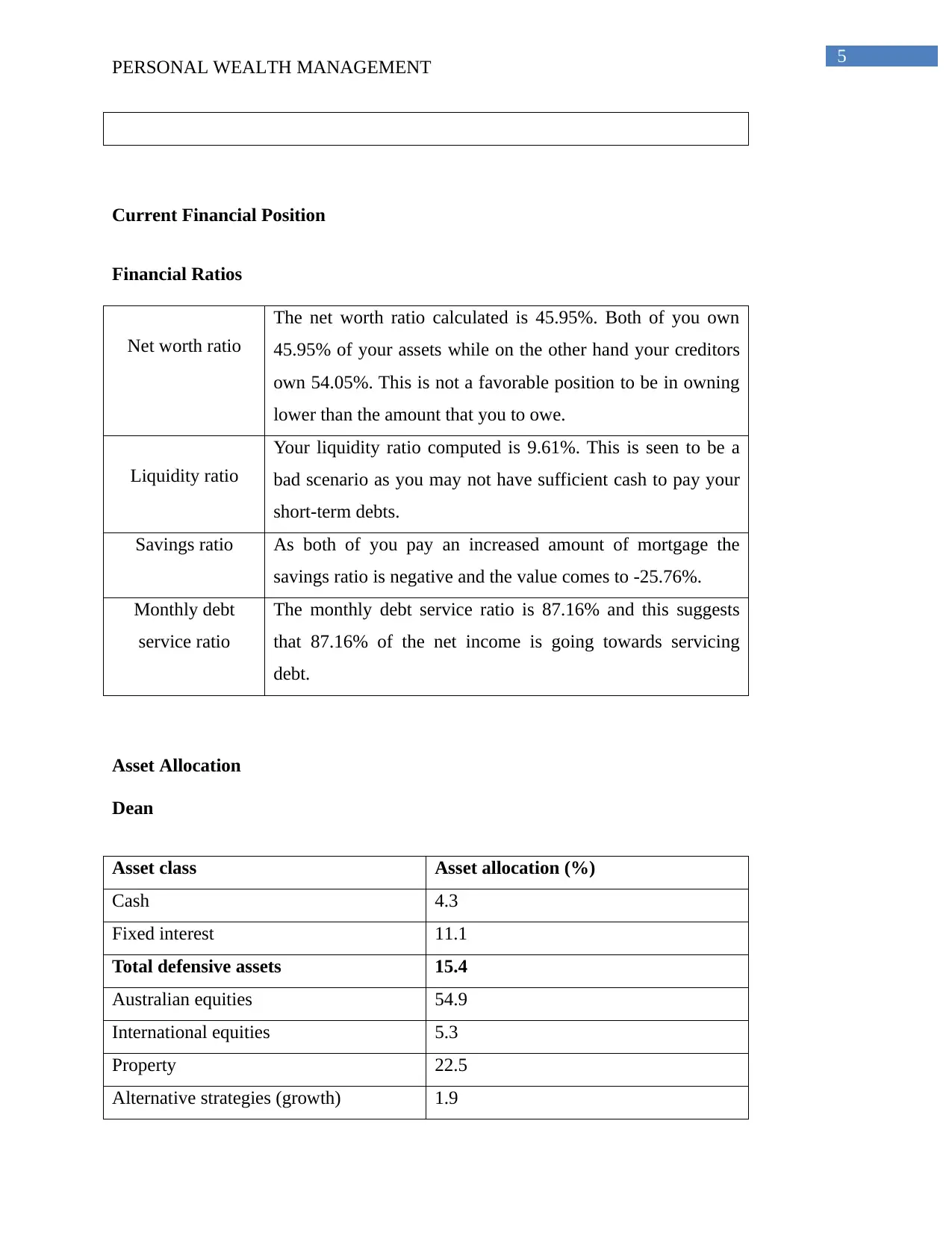

Total growth assets 84.6

Total 100

23%

2%

55%

5%

11%

4%

Asset allocation of Dean's assets

Property

Alternative assets

Australian equities

International equities

Fixed interest

Cash

It is seen that Dean your current asset allocation is found to be a risk profile that is

aggressive and therefore I can recommend that you sell off the growth assets in order to enhance

cash weight due to your conservative risk profile. An ideal allocation of your assets will be to

maintain defensive assets and the assets that are less growing.

Hamish

Asset class Asset allocation(%)

Cash 4.3

Fixed interest 11.5

Total defensive assets 15.8

Australian equities 54.1

International equities 5.9

Property 22.1

Alternative strategies (growth) 2.1

Total growth assets 84.2

Total 100

PERSONAL WEALTH MANAGEMENT

Total growth assets 84.6

Total 100

23%

2%

55%

5%

11%

4%

Asset allocation of Dean's assets

Property

Alternative assets

Australian equities

International equities

Fixed interest

Cash

It is seen that Dean your current asset allocation is found to be a risk profile that is

aggressive and therefore I can recommend that you sell off the growth assets in order to enhance

cash weight due to your conservative risk profile. An ideal allocation of your assets will be to

maintain defensive assets and the assets that are less growing.

Hamish

Asset class Asset allocation(%)

Cash 4.3

Fixed interest 11.5

Total defensive assets 15.8

Australian equities 54.1

International equities 5.9

Property 22.1

Alternative strategies (growth) 2.1

Total growth assets 84.2

Total 100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

PERSONAL WEALTH MANAGEMENT

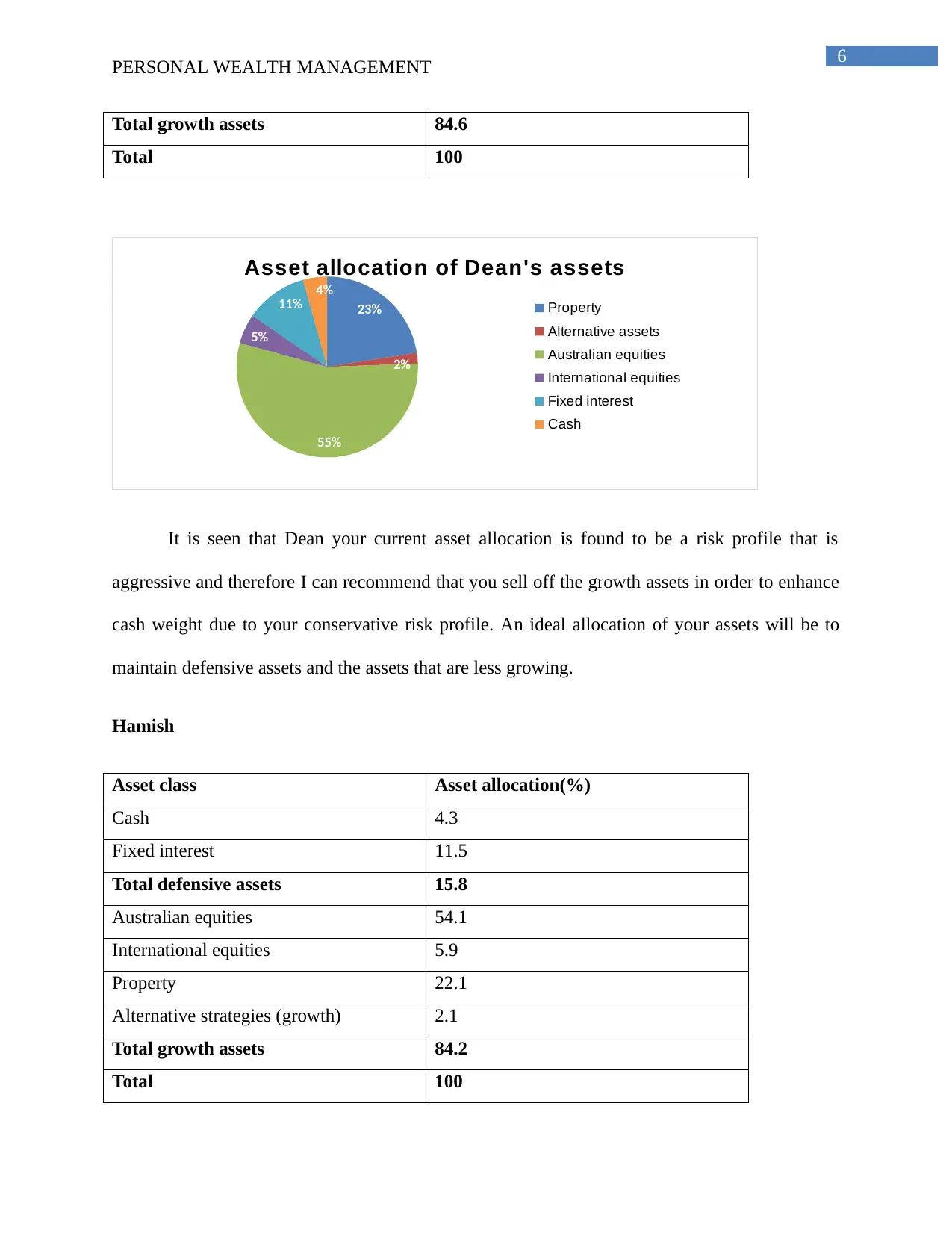

22%

2%

54%

6%

11%

4%

Asset allocation of Hamish's assets

Property

Alternative assets

Australian equities

International equities

Fixed interest

Cash

I can suggest you to sell off your Australian shares and withheld more of cash. The

current asset allocation is an Aggressive one and therefore this should be done in order to

maintain a Balanced Risk Profile. This can be done by maintaining defensive assets and half

growing assets that would be ideal for the purpose of asset allocation.

Projected Cash Flow

Dean and Hamish

2020 2021 2022 2023 2024

Income 119411 119411 119411 119411 119411

Expense 151424 152709 209815 151197 152602

Net cash

flow

$(32013) $(33298) $(90404) $(31786) $(33190)

Recommendation about your financial position

Hamish and Dean, the current issue for the objectives that is medium term has been

paying for your car and home loan. It is possible that you both may incur increased income with

the help of the growth assets you have over the defensive asset and still one cannot save money

PERSONAL WEALTH MANAGEMENT

22%

2%

54%

6%

11%

4%

Asset allocation of Hamish's assets

Property

Alternative assets

Australian equities

International equities

Fixed interest

Cash

I can suggest you to sell off your Australian shares and withheld more of cash. The

current asset allocation is an Aggressive one and therefore this should be done in order to

maintain a Balanced Risk Profile. This can be done by maintaining defensive assets and half

growing assets that would be ideal for the purpose of asset allocation.

Projected Cash Flow

Dean and Hamish

2020 2021 2022 2023 2024

Income 119411 119411 119411 119411 119411

Expense 151424 152709 209815 151197 152602

Net cash

flow

$(32013) $(33298) $(90404) $(31786) $(33190)

Recommendation about your financial position

Hamish and Dean, the current issue for the objectives that is medium term has been

paying for your car and home loan. It is possible that you both may incur increased income with

the help of the growth assets you have over the defensive asset and still one cannot save money

8

PERSONAL WEALTH MANAGEMENT

as the savings ratio is negative. I can therefore suggest you to undertake refinancing of your

house loan and sell off your car mainly due to your increased monthly debt service ratio.

It is seen that mainly due to the increased market value of your house, both of you can

borrow $680,000 from ANZ bank for 30 years. The interest that is aid is undertaken at a variable

rate of 5.36% p.a, which includes the payment of the interest as well as the principal. The

estimated monthly repayment as per the bank is $3,802.

After you receive a new loan from the bank, ANZ bank will pay off for the old loan and

you will receive a new mortgage within an additional $80,000 credit line for refinance.

You both can even sale your car as the present value of the car is more than the mortgage value

of the car.

The new five year projected cash flow after the incorporation of the recommendation is;

Dean and Hamish

2020 2021 2022 2023 2024

Income 119411 119411 119411 119411 119411

Expense 101010 102295 103619 104983 106387

Net cash

flow

$18401 $17116 $15792 $14428 $13024

It is seen that for the next five years both of you can save around $78,761 from the net

cash flow. With the help of the available cash, you will have sufficient money to attain you

medium term goal, which is attaining $100,000 in the next 5 years in order to meet the education

grant for your son.

PERSONAL WEALTH MANAGEMENT

as the savings ratio is negative. I can therefore suggest you to undertake refinancing of your

house loan and sell off your car mainly due to your increased monthly debt service ratio.

It is seen that mainly due to the increased market value of your house, both of you can

borrow $680,000 from ANZ bank for 30 years. The interest that is aid is undertaken at a variable

rate of 5.36% p.a, which includes the payment of the interest as well as the principal. The

estimated monthly repayment as per the bank is $3,802.

After you receive a new loan from the bank, ANZ bank will pay off for the old loan and

you will receive a new mortgage within an additional $80,000 credit line for refinance.

You both can even sale your car as the present value of the car is more than the mortgage value

of the car.

The new five year projected cash flow after the incorporation of the recommendation is;

Dean and Hamish

2020 2021 2022 2023 2024

Income 119411 119411 119411 119411 119411

Expense 101010 102295 103619 104983 106387

Net cash

flow

$18401 $17116 $15792 $14428 $13024

It is seen that for the next five years both of you can save around $78,761 from the net

cash flow. With the help of the available cash, you will have sufficient money to attain you

medium term goal, which is attaining $100,000 in the next 5 years in order to meet the education

grant for your son.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

PERSONAL WEALTH MANAGEMENT

Part B

Executive Summary

The current statement of advice that has been prepared for both of you gives out a clear

idea about the sort of products and money that you will require in order to attain your future

goals and objectives. The advice is solely based on the information that has been providing from

your end. The objectives have been segregated on the basis of the time within which the

objectives need to be attained. It is therefore seen that the short term goal has been to gain

various kinds of insurances with the help of which both of you can have a happy and satisfied

life. The medium term objective has been to maintain a cash balance with the help of which you

two will be able to pay off your home mortgage and car loan. The other medium objectives has

been to create a lump sum amount with the help of which the educational grant of their child can

be attained and even create a certain amount of money with the help of which they can fulfill

their dream of going on a worldwide trip.

On the basis of this, I have put forth a recommendation and this has been selling of your

car and undertakes refinance with the help of which the loan mortgage can be paid off and an

additional amount can be attained with the help of which the other expenses can be met. On the

basis of this I have even prepared a proper better recommendation regarding the insurance

products that is needed for you in order to safeguard your future and thereafter in case of any sort

of unprecedented events, financial remuneration can be given to you.

There have been several sorts of insurances that have been provided to you and one of the

key insurance that is required is life insurance for both of you so that in case of death of any one

of you financial benefits can be attained with the help of which your child can have a safe future.

PERSONAL WEALTH MANAGEMENT

Part B

Executive Summary

The current statement of advice that has been prepared for both of you gives out a clear

idea about the sort of products and money that you will require in order to attain your future

goals and objectives. The advice is solely based on the information that has been providing from

your end. The objectives have been segregated on the basis of the time within which the

objectives need to be attained. It is therefore seen that the short term goal has been to gain

various kinds of insurances with the help of which both of you can have a happy and satisfied

life. The medium term objective has been to maintain a cash balance with the help of which you

two will be able to pay off your home mortgage and car loan. The other medium objectives has

been to create a lump sum amount with the help of which the educational grant of their child can

be attained and even create a certain amount of money with the help of which they can fulfill

their dream of going on a worldwide trip.

On the basis of this, I have put forth a recommendation and this has been selling of your

car and undertakes refinance with the help of which the loan mortgage can be paid off and an

additional amount can be attained with the help of which the other expenses can be met. On the

basis of this I have even prepared a proper better recommendation regarding the insurance

products that is needed for you in order to safeguard your future and thereafter in case of any sort

of unprecedented events, financial remuneration can be given to you.

There have been several sorts of insurances that have been provided to you and one of the

key insurance that is required is life insurance for both of you so that in case of death of any one

of you financial benefits can be attained with the help of which your child can have a safe future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

PERSONAL WEALTH MANAGEMENT

Income protection insurance coverage is even beneficial and therefore has been recommended as

with the help of this insurance the income can be protected as well. Trauma insurance as well as

the Permanent and Temporary Disablement Insurance Coverage is even required with the help of

which both of you can have a safe and secured life. The recommended amount that will be

required for the purpose of retirement will be based on the total income and the objectives that

have been highlighted.

PERSONAL WEALTH MANAGEMENT

Income protection insurance coverage is even beneficial and therefore has been recommended as

with the help of this insurance the income can be protected as well. Trauma insurance as well as

the Permanent and Temporary Disablement Insurance Coverage is even required with the help of

which both of you can have a safe and secured life. The recommended amount that will be

required for the purpose of retirement will be based on the total income and the objectives that

have been highlighted.

11

PERSONAL WEALTH MANAGEMENT

Part C

It is seen that both of you are working and your total income sums to $156,000 p.a. The

personal items are valued at $50,000 your car is work $65,000.You both have various sorts of

investments along with the certain amount of money in superannuation. The amount of liability

that you two have are extensively high and it is seen that due to these factors you need to have a

lump sum amount so that even after paying off the debts enough money is there so that the

retired life can be secured. It is therefore recommended that both of you should have a life time

sum amount of $1,060,800 based on the fact that your life expectancy is 99 years and you are

looking to attain $650 per week after retirement debt free. With the help of this amount I can

recommend that even after paying off all the debts and meeting your expenses, you can have a

life as per your dream.

The projection of the superannuation is another key factor that will be considered and it is

seen that you both receive superannuation on the basis of 9.50% on the salary. Both of you are

looking to retire when Hamish attains the age of 65 years. The projection of superannuation for

Dean till the time you retire is $109,820 and on the other hand the projected superannuation

amount for Hamish is $125,400 and the total sum is found to be $235,220. There is a deficit of

$825,580 for you I would provide recommendations on the basis of which this amount ca be

adjusted.

I can recommend in accordance to the deficit that has been attained is that both of you

have to increase your income either through increasing your salary from the company were you

are working or need to initiate any sort of other source of income with the help of which you can

increase your income as well.

PERSONAL WEALTH MANAGEMENT

Part C

It is seen that both of you are working and your total income sums to $156,000 p.a. The

personal items are valued at $50,000 your car is work $65,000.You both have various sorts of

investments along with the certain amount of money in superannuation. The amount of liability

that you two have are extensively high and it is seen that due to these factors you need to have a

lump sum amount so that even after paying off the debts enough money is there so that the

retired life can be secured. It is therefore recommended that both of you should have a life time

sum amount of $1,060,800 based on the fact that your life expectancy is 99 years and you are

looking to attain $650 per week after retirement debt free. With the help of this amount I can

recommend that even after paying off all the debts and meeting your expenses, you can have a

life as per your dream.

The projection of the superannuation is another key factor that will be considered and it is

seen that you both receive superannuation on the basis of 9.50% on the salary. Both of you are

looking to retire when Hamish attains the age of 65 years. The projection of superannuation for

Dean till the time you retire is $109,820 and on the other hand the projected superannuation

amount for Hamish is $125,400 and the total sum is found to be $235,220. There is a deficit of

$825,580 for you I would provide recommendations on the basis of which this amount ca be

adjusted.

I can recommend in accordance to the deficit that has been attained is that both of you

have to increase your income either through increasing your salary from the company were you

are working or need to initiate any sort of other source of income with the help of which you can

increase your income as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.