Webjet Ltd: In-depth Financial Accounting Report and Ratio Analysis

VerifiedAdded on 2023/06/07

|23

|6053

|384

Report

AI Summary

This report provides a comprehensive financial analysis of Webjet Ltd, a digital travel services provider, focusing on profitability, liquidity, and solvency ratios over a five-year period. It includes a comparative analysis with Flight Centre Travel Group Ltd to benchmark Webjet's performance against a key competitor. The analysis incorporates key financial ratios, growth rates, and visual aids such as tables and graphs to illustrate the financial health and trends of both companies. The report assesses net profit margins, return on equity, return on assets, and return on invested capital to evaluate the companies' financial performance and identify areas for improvement. The findings offer insights into the financial standing of Webjet Ltd and its competitive positioning within the travel industry.

Running head: ACCOUNTING REPORT ANALYSIS

Accounting Report Analysis

Name of the Student:

Name of the University:

Author’s Note

Accounting Report Analysis

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING REPORT ANALYSIS

Executive Summary

The main purpose of this assessment is to analyze the financial performance of Webjet ltd which

is engaged in providing digital travel services to the customers. The assessment considers the

profitability, liquidity and solvency ratios of the business for the purpose of analyzing the growth

and development of the business on the basis of the above mention criteria. The report also

includes comparative analysis of the performance of the business in relation to one of the close

competitors of Webjet ltd. The company which is taken is Flight Center Travel ltd. The analysis

will be comparative in nature in order to understand the performance of the Webjet in terms of

industry and competitors. The assessment also includes graphs and tables which are

appropriately shown and analyzed in the assessment.

ACCOUNTING REPORT ANALYSIS

Executive Summary

The main purpose of this assessment is to analyze the financial performance of Webjet ltd which

is engaged in providing digital travel services to the customers. The assessment considers the

profitability, liquidity and solvency ratios of the business for the purpose of analyzing the growth

and development of the business on the basis of the above mention criteria. The report also

includes comparative analysis of the performance of the business in relation to one of the close

competitors of Webjet ltd. The company which is taken is Flight Center Travel ltd. The analysis

will be comparative in nature in order to understand the performance of the Webjet in terms of

industry and competitors. The assessment also includes graphs and tables which are

appropriately shown and analyzed in the assessment.

2

ACCOUNTING REPORT ANALYSIS

Table of Contents

Introduction......................................................................................................................................3

Profitability Analysis.......................................................................................................................4

Liquidity Ratio...............................................................................................................................10

Solvency Analysis.........................................................................................................................15

Conclusion.....................................................................................................................................19

Reference.......................................................................................................................................20

ACCOUNTING REPORT ANALYSIS

Table of Contents

Introduction......................................................................................................................................3

Profitability Analysis.......................................................................................................................4

Liquidity Ratio...............................................................................................................................10

Solvency Analysis.........................................................................................................................15

Conclusion.....................................................................................................................................19

Reference.......................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING REPORT ANALYSIS

Introduction

The main purpose of this assessment is to analyze the financial statements of Webjet

limited in order understand the performance of the business in the industry. The report will be

considering the financial report of the company for a period of five years in order to estimate the

growth in the business of Webjet ltd. The assessment shows computation of key financial ratios

and the same are to be analyzed in order to identify growth in areas which are related to

profitability, solvency and liquidity of the business. The report also considers a close competitor

of Webjet ltd on the basis of which comparative analysis is to be conducted in order to compare

performance of both businesses. The company which is selected for the assessment is Flight

Center Travel Group Ltd.

Webjet ltd is engaged in the business of digital business which provides travel services to

the customers. The company is known to be a leading company which provides online travel

services, both domestic and foreign travel services for the customers of the business. In addition

to this, the company also provide hotel accommodation bookings. Deals, cruise car (Annual

Reports - Webjet Limited., 2018). The company has its headquarters in Australia and also has

operations in other countries like New Zealand, North America and other countries.

On the other hand, Flight Center Travel Group Ltd is considered to be one of the largest

retail travel service outlets which has operations predominately in Australia. The specialty of the

company is the swift and smooth services which it provides to the customers. The company was

founded in 1982 and the company has its headquarters in Australia (Annual Reports - Flight

Centre Travel Group., 2018). The company has a turnover of 20 billion and also employs a

significant force in employee all around the area of operations of the business.

The report shows comparative analysis between the two companies which includes

computation of key financial ratios and the report will also be containing graphs and tables

showing the computation of ratios which can be used for the identifying how well the company

has performed over the last five years.

ACCOUNTING REPORT ANALYSIS

Introduction

The main purpose of this assessment is to analyze the financial statements of Webjet

limited in order understand the performance of the business in the industry. The report will be

considering the financial report of the company for a period of five years in order to estimate the

growth in the business of Webjet ltd. The assessment shows computation of key financial ratios

and the same are to be analyzed in order to identify growth in areas which are related to

profitability, solvency and liquidity of the business. The report also considers a close competitor

of Webjet ltd on the basis of which comparative analysis is to be conducted in order to compare

performance of both businesses. The company which is selected for the assessment is Flight

Center Travel Group Ltd.

Webjet ltd is engaged in the business of digital business which provides travel services to

the customers. The company is known to be a leading company which provides online travel

services, both domestic and foreign travel services for the customers of the business. In addition

to this, the company also provide hotel accommodation bookings. Deals, cruise car (Annual

Reports - Webjet Limited., 2018). The company has its headquarters in Australia and also has

operations in other countries like New Zealand, North America and other countries.

On the other hand, Flight Center Travel Group Ltd is considered to be one of the largest

retail travel service outlets which has operations predominately in Australia. The specialty of the

company is the swift and smooth services which it provides to the customers. The company was

founded in 1982 and the company has its headquarters in Australia (Annual Reports - Flight

Centre Travel Group., 2018). The company has a turnover of 20 billion and also employs a

significant force in employee all around the area of operations of the business.

The report shows comparative analysis between the two companies which includes

computation of key financial ratios and the report will also be containing graphs and tables

showing the computation of ratios which can be used for the identifying how well the company

has performed over the last five years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING REPORT ANALYSIS

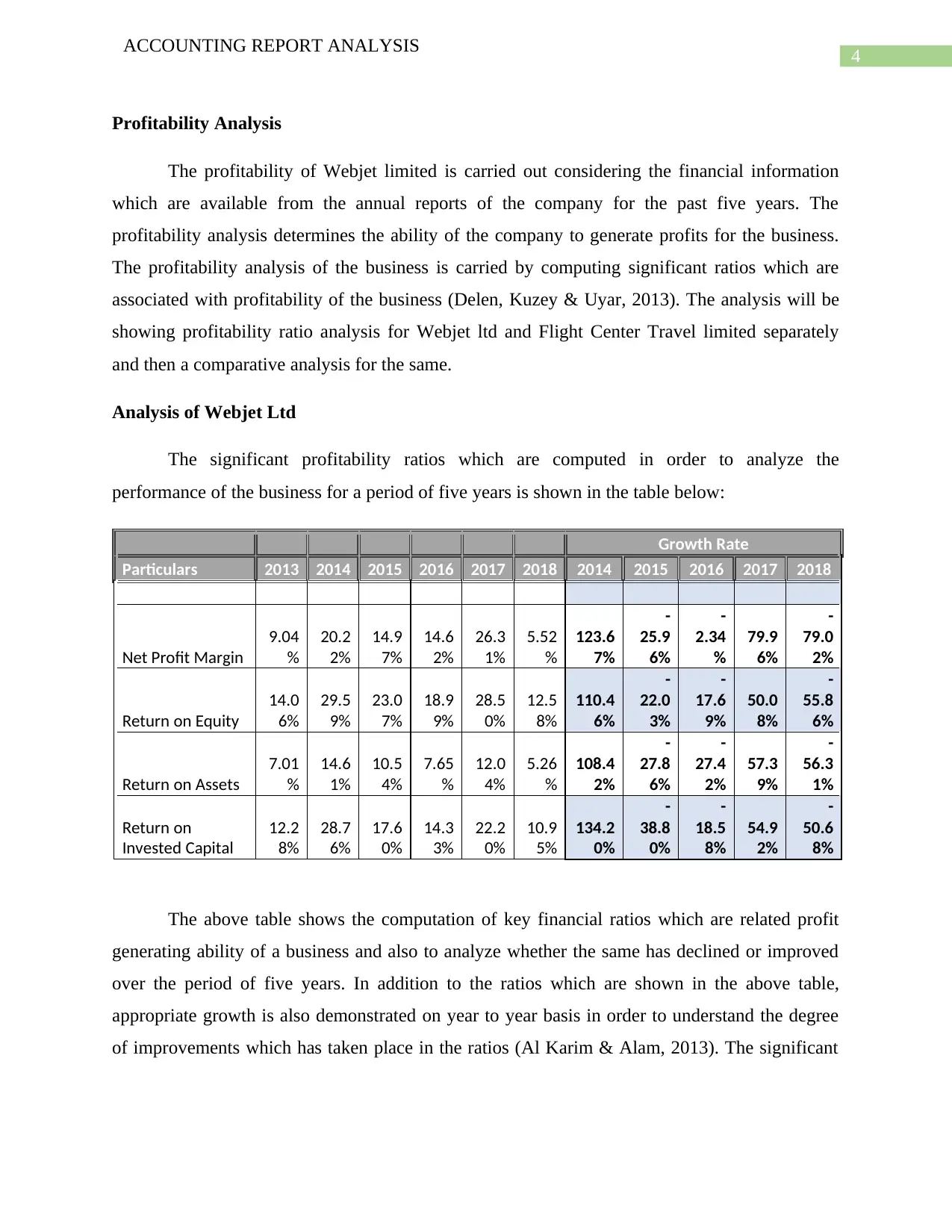

Profitability Analysis

The profitability of Webjet limited is carried out considering the financial information

which are available from the annual reports of the company for the past five years. The

profitability analysis determines the ability of the company to generate profits for the business.

The profitability analysis of the business is carried by computing significant ratios which are

associated with profitability of the business (Delen, Kuzey & Uyar, 2013). The analysis will be

showing profitability ratio analysis for Webjet ltd and Flight Center Travel limited separately

and then a comparative analysis for the same.

Analysis of Webjet Ltd

The significant profitability ratios which are computed in order to analyze the

performance of the business for a period of five years is shown in the table below:

Growth Rate

Particulars 2013 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Net Profit Margin

9.04

%

20.2

2%

14.9

7%

14.6

2%

26.3

1%

5.52

%

123.6

7%

-

25.9

6%

-

2.34

%

79.9

6%

-

79.0

2%

Return on Equity

14.0

6%

29.5

9%

23.0

7%

18.9

9%

28.5

0%

12.5

8%

110.4

6%

-

22.0

3%

-

17.6

9%

50.0

8%

-

55.8

6%

Return on Assets

7.01

%

14.6

1%

10.5

4%

7.65

%

12.0

4%

5.26

%

108.4

2%

-

27.8

6%

-

27.4

2%

57.3

9%

-

56.3

1%

Return on

Invested Capital

12.2

8%

28.7

6%

17.6

0%

14.3

3%

22.2

0%

10.9

5%

134.2

0%

-

38.8

0%

-

18.5

8%

54.9

2%

-

50.6

8%

The above table shows the computation of key financial ratios which are related profit

generating ability of a business and also to analyze whether the same has declined or improved

over the period of five years. In addition to the ratios which are shown in the above table,

appropriate growth is also demonstrated on year to year basis in order to understand the degree

of improvements which has taken place in the ratios (Al Karim & Alam, 2013). The significant

ACCOUNTING REPORT ANALYSIS

Profitability Analysis

The profitability of Webjet limited is carried out considering the financial information

which are available from the annual reports of the company for the past five years. The

profitability analysis determines the ability of the company to generate profits for the business.

The profitability analysis of the business is carried by computing significant ratios which are

associated with profitability of the business (Delen, Kuzey & Uyar, 2013). The analysis will be

showing profitability ratio analysis for Webjet ltd and Flight Center Travel limited separately

and then a comparative analysis for the same.

Analysis of Webjet Ltd

The significant profitability ratios which are computed in order to analyze the

performance of the business for a period of five years is shown in the table below:

Growth Rate

Particulars 2013 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Net Profit Margin

9.04

%

20.2

2%

14.9

7%

14.6

2%

26.3

1%

5.52

%

123.6

7%

-

25.9

6%

-

2.34

%

79.9

6%

-

79.0

2%

Return on Equity

14.0

6%

29.5

9%

23.0

7%

18.9

9%

28.5

0%

12.5

8%

110.4

6%

-

22.0

3%

-

17.6

9%

50.0

8%

-

55.8

6%

Return on Assets

7.01

%

14.6

1%

10.5

4%

7.65

%

12.0

4%

5.26

%

108.4

2%

-

27.8

6%

-

27.4

2%

57.3

9%

-

56.3

1%

Return on

Invested Capital

12.2

8%

28.7

6%

17.6

0%

14.3

3%

22.2

0%

10.9

5%

134.2

0%

-

38.8

0%

-

18.5

8%

54.9

2%

-

50.6

8%

The above table shows the computation of key financial ratios which are related profit

generating ability of a business and also to analyze whether the same has declined or improved

over the period of five years. In addition to the ratios which are shown in the above table,

appropriate growth is also demonstrated on year to year basis in order to understand the degree

of improvements which has taken place in the ratios (Al Karim & Alam, 2013). The significant

5

ACCOUNTING REPORT ANALYSIS

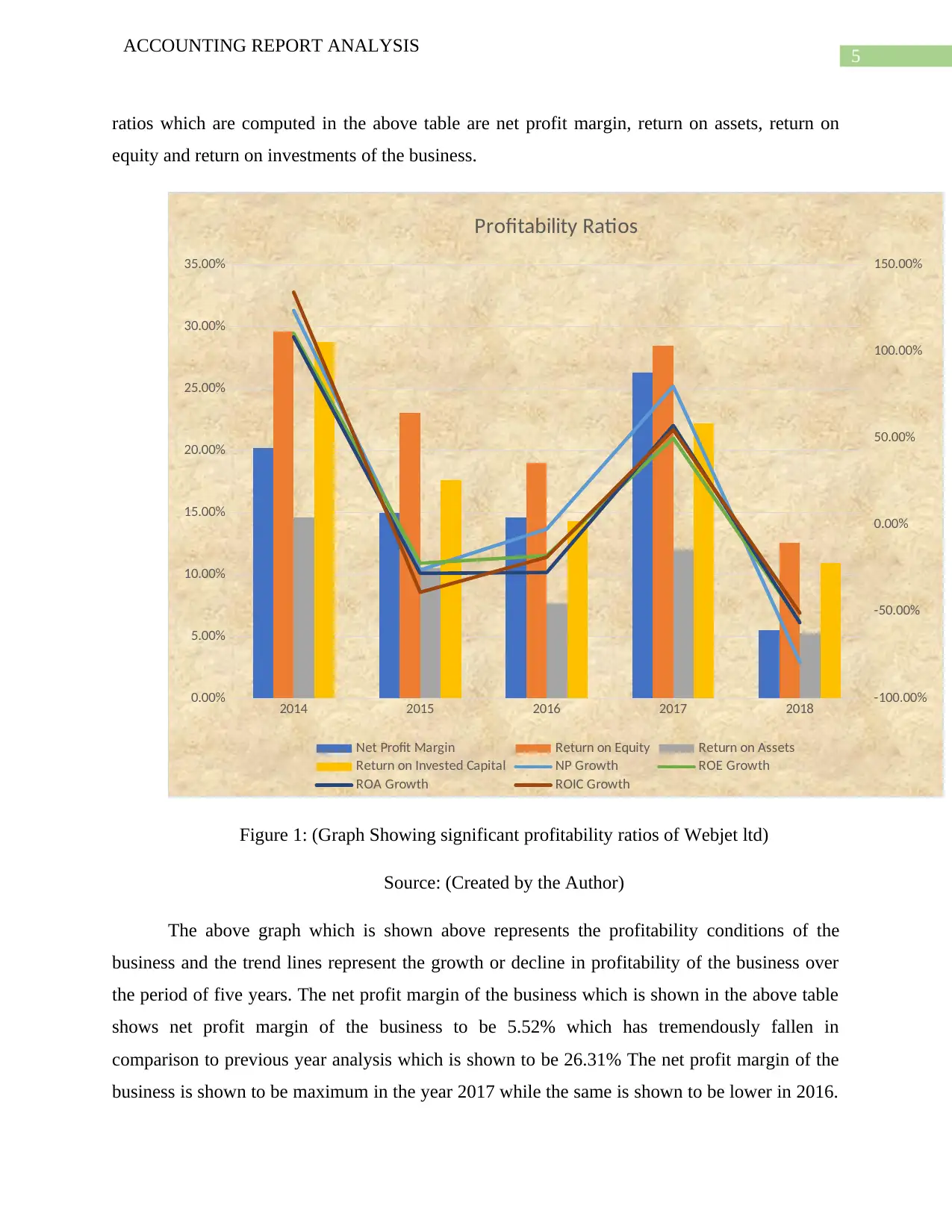

ratios which are computed in the above table are net profit margin, return on assets, return on

equity and return on investments of the business.

2014 2015 2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

Profitability Ratios

Net Profit Margin Return on Equity Return on Assets

Return on Invested Capital NP Growth ROE Growth

ROA Growth ROIC Growth

Figure 1: (Graph Showing significant profitability ratios of Webjet ltd)

Source: (Created by the Author)

The above graph which is shown above represents the profitability conditions of the

business and the trend lines represent the growth or decline in profitability of the business over

the period of five years. The net profit margin of the business which is shown in the above table

shows net profit margin of the business to be 5.52% which has tremendously fallen in

comparison to previous year analysis which is shown to be 26.31% The net profit margin of the

business is shown to be maximum in the year 2017 while the same is shown to be lower in 2016.

ACCOUNTING REPORT ANALYSIS

ratios which are computed in the above table are net profit margin, return on assets, return on

equity and return on investments of the business.

2014 2015 2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

Profitability Ratios

Net Profit Margin Return on Equity Return on Assets

Return on Invested Capital NP Growth ROE Growth

ROA Growth ROIC Growth

Figure 1: (Graph Showing significant profitability ratios of Webjet ltd)

Source: (Created by the Author)

The above graph which is shown above represents the profitability conditions of the

business and the trend lines represent the growth or decline in profitability of the business over

the period of five years. The net profit margin of the business which is shown in the above table

shows net profit margin of the business to be 5.52% which has tremendously fallen in

comparison to previous year analysis which is shown to be 26.31% The net profit margin of the

business is shown to be maximum in the year 2017 while the same is shown to be lower in 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING REPORT ANALYSIS

The analysis of 2018 results suggest that the management of the company needs to formulate a

strategy in order to improve the net profit margin of the business. The strategy of the business

can be to either go for sales maximization policy or cost reduction policy both of which have

direct impact on the profitability of the company. The return on equity and return on assets

which are shown in the table above are considered to financial indicators for a success of a

business. The return on equity represent the amount which the business can generate from the

use of equity capital in the business and similarly the return which the business can generate with

the application of the assets of the business (Heikal et al., 2014). The return on equity of the

business as per the table above is shown to be 12.58% which is much lower than the return on

equity which the business had generated in previous year. The return on equity of the business

needs to be improved in order to live up to the expectations of the shareholders of the company.

The return on assets if the business is shown to be 5.56% which was around 12% in 2017 which

is also not a positive sign for the business. The return on investments for the business is shown in

the table above which is also one of the financial indicators which is shown to have reduced

during the year. The overall analysis shows that the profitability of the business shows that in

2018 all the profitability indexes have fallen which signifies that the business is having difficult

in increasing the overall profitability of the business.

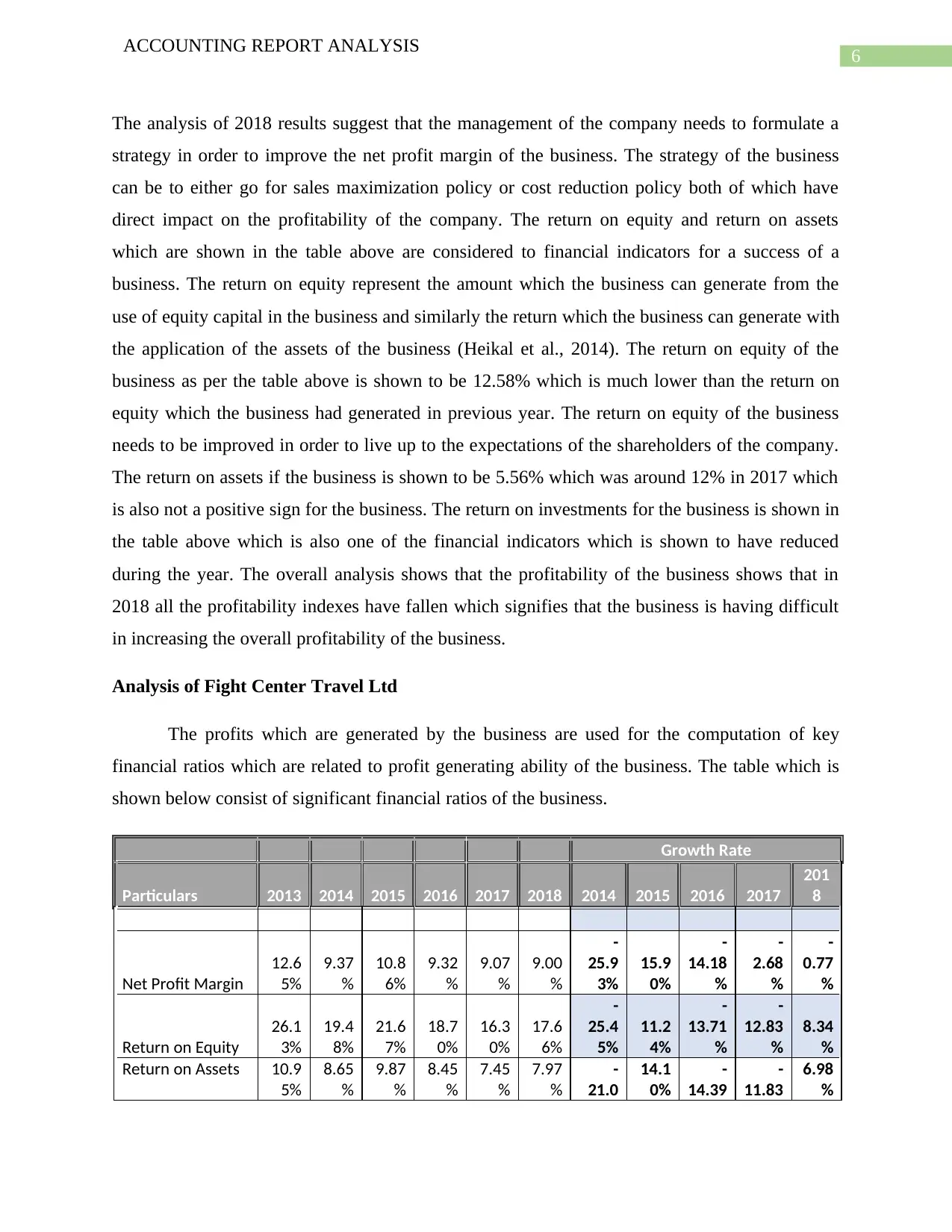

Analysis of Fight Center Travel Ltd

The profits which are generated by the business are used for the computation of key

financial ratios which are related to profit generating ability of the business. The table which is

shown below consist of significant financial ratios of the business.

Growth Rate

Particulars 2013 2014 2015 2016 2017 2018 2014 2015 2016 2017

201

8

Net Profit Margin

12.6

5%

9.37

%

10.8

6%

9.32

%

9.07

%

9.00

%

-

25.9

3%

15.9

0%

-

14.18

%

-

2.68

%

-

0.77

%

Return on Equity

26.1

3%

19.4

8%

21.6

7%

18.7

0%

16.3

0%

17.6

6%

-

25.4

5%

11.2

4%

-

13.71

%

-

12.83

%

8.34

%

Return on Assets 10.9

5%

8.65

%

9.87

%

8.45

%

7.45

%

7.97

%

-

21.0

14.1

0%

-

14.39

-

11.83

6.98

%

ACCOUNTING REPORT ANALYSIS

The analysis of 2018 results suggest that the management of the company needs to formulate a

strategy in order to improve the net profit margin of the business. The strategy of the business

can be to either go for sales maximization policy or cost reduction policy both of which have

direct impact on the profitability of the company. The return on equity and return on assets

which are shown in the table above are considered to financial indicators for a success of a

business. The return on equity represent the amount which the business can generate from the

use of equity capital in the business and similarly the return which the business can generate with

the application of the assets of the business (Heikal et al., 2014). The return on equity of the

business as per the table above is shown to be 12.58% which is much lower than the return on

equity which the business had generated in previous year. The return on equity of the business

needs to be improved in order to live up to the expectations of the shareholders of the company.

The return on assets if the business is shown to be 5.56% which was around 12% in 2017 which

is also not a positive sign for the business. The return on investments for the business is shown in

the table above which is also one of the financial indicators which is shown to have reduced

during the year. The overall analysis shows that the profitability of the business shows that in

2018 all the profitability indexes have fallen which signifies that the business is having difficult

in increasing the overall profitability of the business.

Analysis of Fight Center Travel Ltd

The profits which are generated by the business are used for the computation of key

financial ratios which are related to profit generating ability of the business. The table which is

shown below consist of significant financial ratios of the business.

Growth Rate

Particulars 2013 2014 2015 2016 2017 2018 2014 2015 2016 2017

201

8

Net Profit Margin

12.6

5%

9.37

%

10.8

6%

9.32

%

9.07

%

9.00

%

-

25.9

3%

15.9

0%

-

14.18

%

-

2.68

%

-

0.77

%

Return on Equity

26.1

3%

19.4

8%

21.6

7%

18.7

0%

16.3

0%

17.6

6%

-

25.4

5%

11.2

4%

-

13.71

%

-

12.83

%

8.34

%

Return on Assets 10.9

5%

8.65

%

9.87

%

8.45

%

7.45

%

7.97

%

-

21.0

14.1

0%

-

14.39

-

11.83

6.98

%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING REPORT ANALYSIS

0% % %

Return on

Invested Capital

23.9

0%

18.7

3%

20.8

0%

18.0

9%

15.9

6%

17.1

4%

-

21.6

3%

11.0

5%

-

13.03

%

-

11.77

%

7.39

%

2014 2015 2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

-30.00%

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Profitability Ratios

Net Profit Margin Return on Equity Return on Assets Return on Invested Capital

NP Growth ROE Growth ROA Growth ROIC Growth

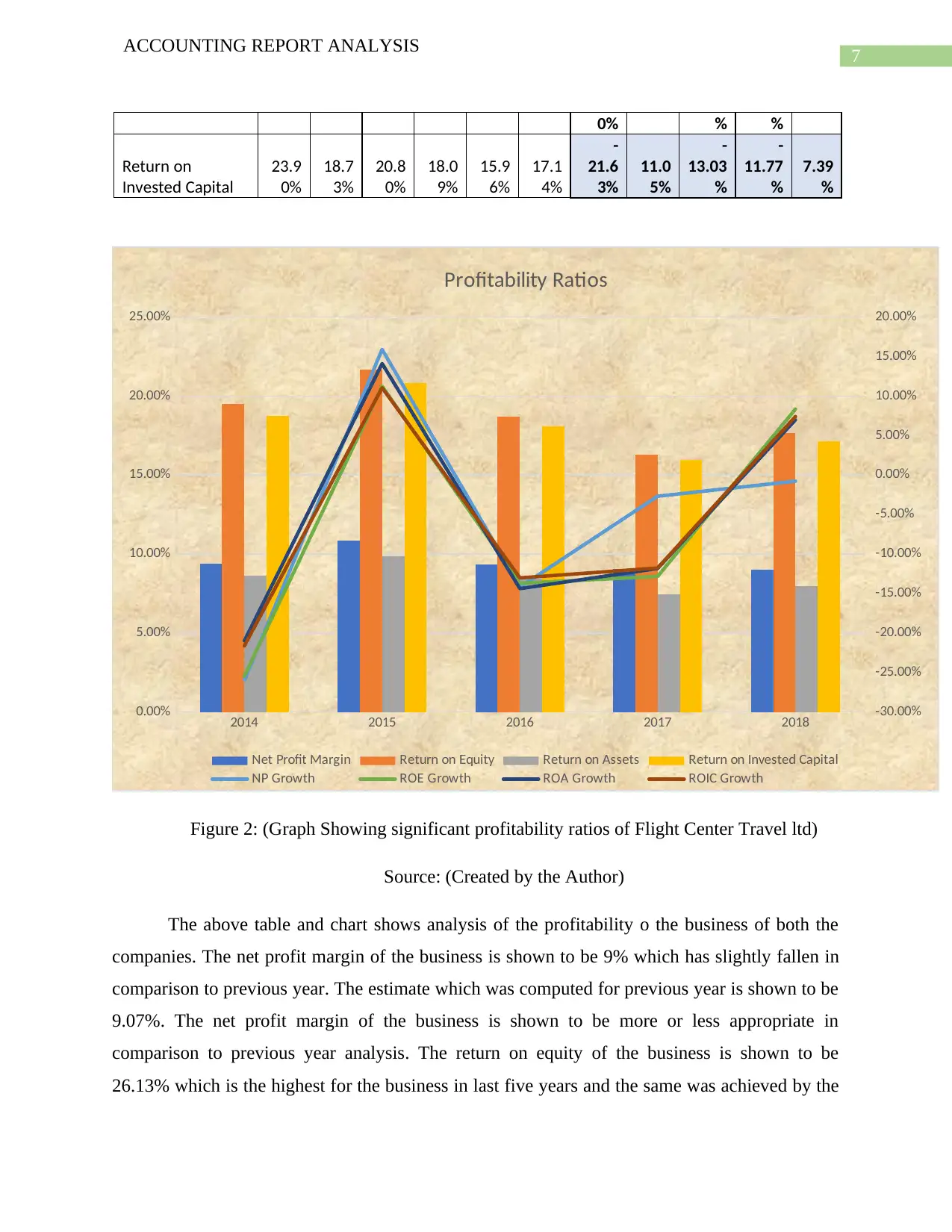

Figure 2: (Graph Showing significant profitability ratios of Flight Center Travel ltd)

Source: (Created by the Author)

The above table and chart shows analysis of the profitability o the business of both the

companies. The net profit margin of the business is shown to be 9% which has slightly fallen in

comparison to previous year. The estimate which was computed for previous year is shown to be

9.07%. The net profit margin of the business is shown to be more or less appropriate in

comparison to previous year analysis. The return on equity of the business is shown to be

26.13% which is the highest for the business in last five years and the same was achieved by the

ACCOUNTING REPORT ANALYSIS

0% % %

Return on

Invested Capital

23.9

0%

18.7

3%

20.8

0%

18.0

9%

15.9

6%

17.1

4%

-

21.6

3%

11.0

5%

-

13.03

%

-

11.77

%

7.39

%

2014 2015 2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

-30.00%

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Profitability Ratios

Net Profit Margin Return on Equity Return on Assets Return on Invested Capital

NP Growth ROE Growth ROA Growth ROIC Growth

Figure 2: (Graph Showing significant profitability ratios of Flight Center Travel ltd)

Source: (Created by the Author)

The above table and chart shows analysis of the profitability o the business of both the

companies. The net profit margin of the business is shown to be 9% which has slightly fallen in

comparison to previous year. The estimate which was computed for previous year is shown to be

9.07%. The net profit margin of the business is shown to be more or less appropriate in

comparison to previous year analysis. The return on equity of the business is shown to be

26.13% which is the highest for the business in last five years and the same was achieved by the

8

ACCOUNTING REPORT ANALYSIS

business in 2013. The return on equity for the current year which is 2018 is shown to be 17.6%

which shows the estimate has increased significantly in comparison to previous year which

suggest that the management of the company is paying heeds to the interest of the shareholders

of the company. The return on assets of the business is shown to have improved as well in

comparison to previous year’s estimates which signifies that the company is in the right track

and the financial indicators displays a positive image (Muda, Shaharuddin & Embaya, 2013).

The return on invested capital o the business is also shown to have improved in comparison to

previous year figures which is good sign for the business. In an overall estimate it can be said

that the profitability position of the business of Flight Center Travel Ltd has improved

significantly in comparison to past years analysis and the same is a sign that the business is going

through a good phase of business cycle.

Comparative Analysis

The analysis of the profitability for both the companies are explained with the help of

tables and graphs which is shown above. The comparative analysis of the profitability of the

business aims to relate and compare the performance of Webjet ltd with performance of Flight

Center Travel Ltd. This will be help the management of Webjet ltd to get insights about the

positioning of the company in terms of close competitor of the business (Almazari, 2014). In

order to compare the performance of both the companies net profit margin is considered which is

the most important profitability ratio and the same is analyzed by the potential investors before

taking any investment decision for the business (Bhamorasathit & Katawandee, 2014). In order

to make a comparative study appropriately the following table and graphs are used for

demonstrating the changes in net profit margin for the companies.

Net Profit Margin

2013 2014 2015 2016 2017 2018

Flight Center Travel Limited 12.65% 9.37% 10.86% 9.32% 9.07% 9.00%

Webjet Limited 9.04% 20.22% 14.97% 14.62% 26.31% 5.52%

ACCOUNTING REPORT ANALYSIS

business in 2013. The return on equity for the current year which is 2018 is shown to be 17.6%

which shows the estimate has increased significantly in comparison to previous year which

suggest that the management of the company is paying heeds to the interest of the shareholders

of the company. The return on assets of the business is shown to have improved as well in

comparison to previous year’s estimates which signifies that the company is in the right track

and the financial indicators displays a positive image (Muda, Shaharuddin & Embaya, 2013).

The return on invested capital o the business is also shown to have improved in comparison to

previous year figures which is good sign for the business. In an overall estimate it can be said

that the profitability position of the business of Flight Center Travel Ltd has improved

significantly in comparison to past years analysis and the same is a sign that the business is going

through a good phase of business cycle.

Comparative Analysis

The analysis of the profitability for both the companies are explained with the help of

tables and graphs which is shown above. The comparative analysis of the profitability of the

business aims to relate and compare the performance of Webjet ltd with performance of Flight

Center Travel Ltd. This will be help the management of Webjet ltd to get insights about the

positioning of the company in terms of close competitor of the business (Almazari, 2014). In

order to compare the performance of both the companies net profit margin is considered which is

the most important profitability ratio and the same is analyzed by the potential investors before

taking any investment decision for the business (Bhamorasathit & Katawandee, 2014). In order

to make a comparative study appropriately the following table and graphs are used for

demonstrating the changes in net profit margin for the companies.

Net Profit Margin

2013 2014 2015 2016 2017 2018

Flight Center Travel Limited 12.65% 9.37% 10.86% 9.32% 9.07% 9.00%

Webjet Limited 9.04% 20.22% 14.97% 14.62% 26.31% 5.52%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

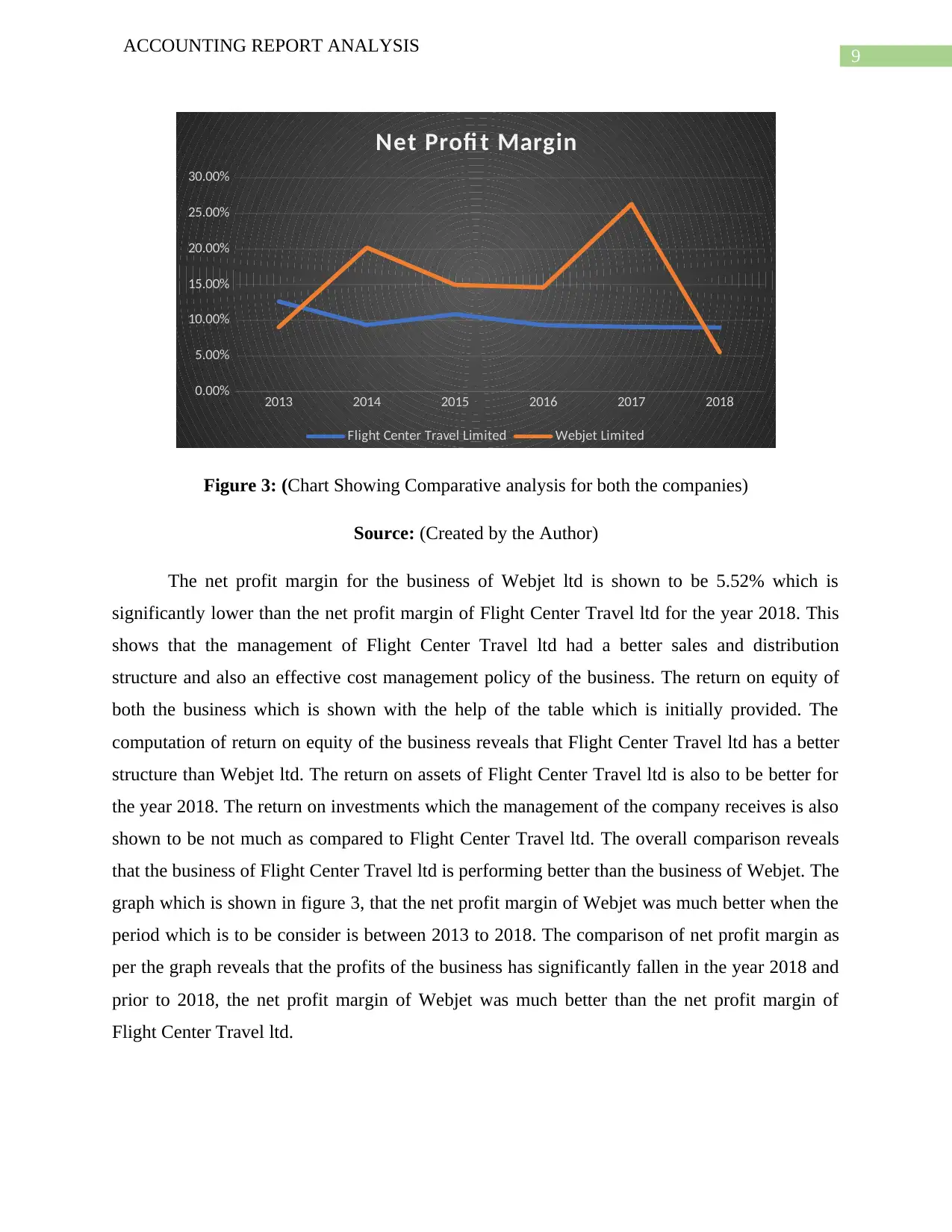

9

ACCOUNTING REPORT ANALYSIS

2013 2014 2015 2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Net Profi t Margin

Flight Center Travel Limited Webjet Limited

Figure 3: (Chart Showing Comparative analysis for both the companies)

Source: (Created by the Author)

The net profit margin for the business of Webjet ltd is shown to be 5.52% which is

significantly lower than the net profit margin of Flight Center Travel ltd for the year 2018. This

shows that the management of Flight Center Travel ltd had a better sales and distribution

structure and also an effective cost management policy of the business. The return on equity of

both the business which is shown with the help of the table which is initially provided. The

computation of return on equity of the business reveals that Flight Center Travel ltd has a better

structure than Webjet ltd. The return on assets of Flight Center Travel ltd is also to be better for

the year 2018. The return on investments which the management of the company receives is also

shown to be not much as compared to Flight Center Travel ltd. The overall comparison reveals

that the business of Flight Center Travel ltd is performing better than the business of Webjet. The

graph which is shown in figure 3, that the net profit margin of Webjet was much better when the

period which is to be consider is between 2013 to 2018. The comparison of net profit margin as

per the graph reveals that the profits of the business has significantly fallen in the year 2018 and

prior to 2018, the net profit margin of Webjet was much better than the net profit margin of

Flight Center Travel ltd.

ACCOUNTING REPORT ANALYSIS

2013 2014 2015 2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Net Profi t Margin

Flight Center Travel Limited Webjet Limited

Figure 3: (Chart Showing Comparative analysis for both the companies)

Source: (Created by the Author)

The net profit margin for the business of Webjet ltd is shown to be 5.52% which is

significantly lower than the net profit margin of Flight Center Travel ltd for the year 2018. This

shows that the management of Flight Center Travel ltd had a better sales and distribution

structure and also an effective cost management policy of the business. The return on equity of

both the business which is shown with the help of the table which is initially provided. The

computation of return on equity of the business reveals that Flight Center Travel ltd has a better

structure than Webjet ltd. The return on assets of Flight Center Travel ltd is also to be better for

the year 2018. The return on investments which the management of the company receives is also

shown to be not much as compared to Flight Center Travel ltd. The overall comparison reveals

that the business of Flight Center Travel ltd is performing better than the business of Webjet. The

graph which is shown in figure 3, that the net profit margin of Webjet was much better when the

period which is to be consider is between 2013 to 2018. The comparison of net profit margin as

per the graph reveals that the profits of the business has significantly fallen in the year 2018 and

prior to 2018, the net profit margin of Webjet was much better than the net profit margin of

Flight Center Travel ltd.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING REPORT ANALYSIS

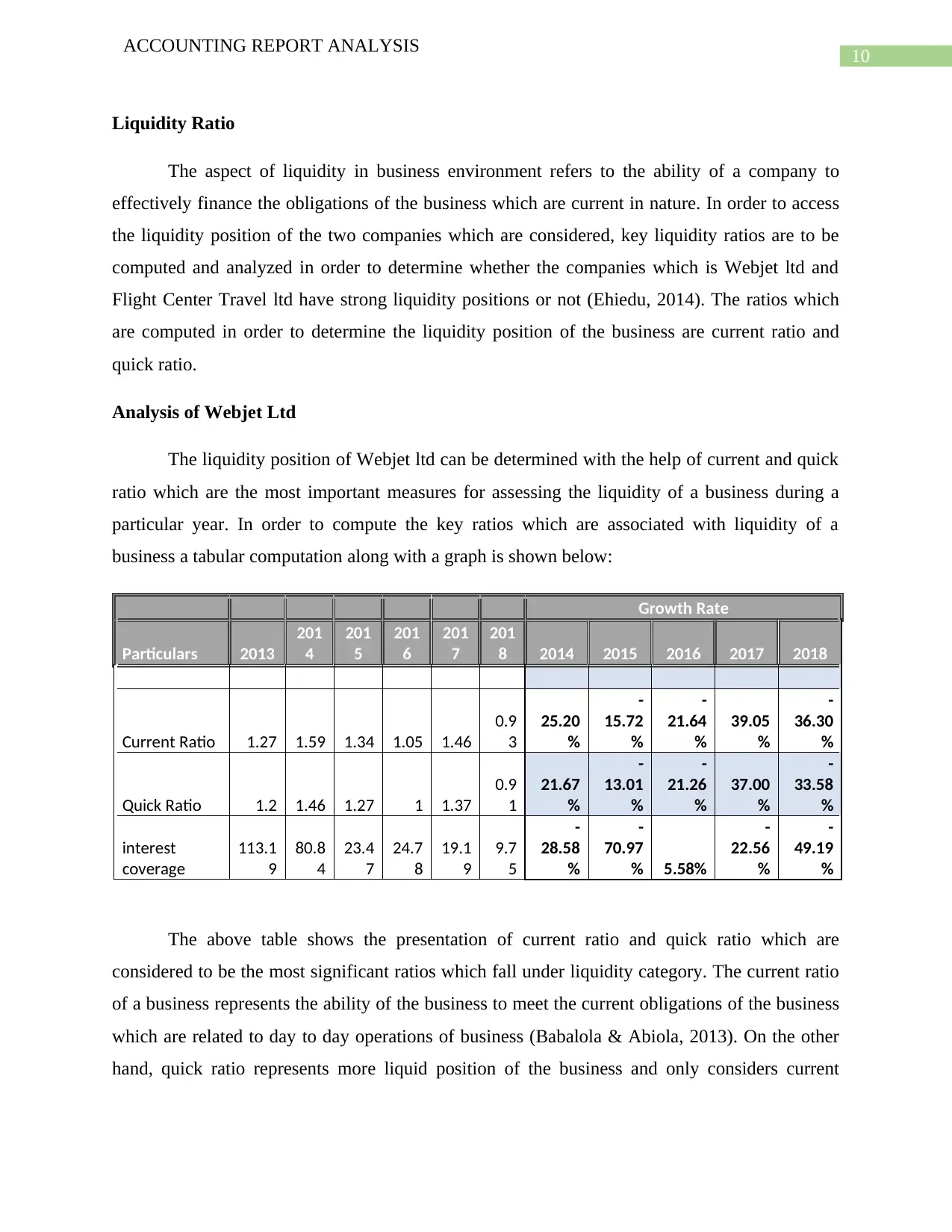

Liquidity Ratio

The aspect of liquidity in business environment refers to the ability of a company to

effectively finance the obligations of the business which are current in nature. In order to access

the liquidity position of the two companies which are considered, key liquidity ratios are to be

computed and analyzed in order to determine whether the companies which is Webjet ltd and

Flight Center Travel ltd have strong liquidity positions or not (Ehiedu, 2014). The ratios which

are computed in order to determine the liquidity position of the business are current ratio and

quick ratio.

Analysis of Webjet Ltd

The liquidity position of Webjet ltd can be determined with the help of current and quick

ratio which are the most important measures for assessing the liquidity of a business during a

particular year. In order to compute the key ratios which are associated with liquidity of a

business a tabular computation along with a graph is shown below:

Growth Rate

Particulars 2013

201

4

201

5

201

6

201

7

201

8 2014 2015 2016 2017 2018

Current Ratio 1.27 1.59 1.34 1.05 1.46

0.9

3

25.20

%

-

15.72

%

-

21.64

%

39.05

%

-

36.30

%

Quick Ratio 1.2 1.46 1.27 1 1.37

0.9

1

21.67

%

-

13.01

%

-

21.26

%

37.00

%

-

33.58

%

interest

coverage

113.1

9

80.8

4

23.4

7

24.7

8

19.1

9

9.7

5

-

28.58

%

-

70.97

% 5.58%

-

22.56

%

-

49.19

%

The above table shows the presentation of current ratio and quick ratio which are

considered to be the most significant ratios which fall under liquidity category. The current ratio

of a business represents the ability of the business to meet the current obligations of the business

which are related to day to day operations of business (Babalola & Abiola, 2013). On the other

hand, quick ratio represents more liquid position of the business and only considers current

ACCOUNTING REPORT ANALYSIS

Liquidity Ratio

The aspect of liquidity in business environment refers to the ability of a company to

effectively finance the obligations of the business which are current in nature. In order to access

the liquidity position of the two companies which are considered, key liquidity ratios are to be

computed and analyzed in order to determine whether the companies which is Webjet ltd and

Flight Center Travel ltd have strong liquidity positions or not (Ehiedu, 2014). The ratios which

are computed in order to determine the liquidity position of the business are current ratio and

quick ratio.

Analysis of Webjet Ltd

The liquidity position of Webjet ltd can be determined with the help of current and quick

ratio which are the most important measures for assessing the liquidity of a business during a

particular year. In order to compute the key ratios which are associated with liquidity of a

business a tabular computation along with a graph is shown below:

Growth Rate

Particulars 2013

201

4

201

5

201

6

201

7

201

8 2014 2015 2016 2017 2018

Current Ratio 1.27 1.59 1.34 1.05 1.46

0.9

3

25.20

%

-

15.72

%

-

21.64

%

39.05

%

-

36.30

%

Quick Ratio 1.2 1.46 1.27 1 1.37

0.9

1

21.67

%

-

13.01

%

-

21.26

%

37.00

%

-

33.58

%

interest

coverage

113.1

9

80.8

4

23.4

7

24.7

8

19.1

9

9.7

5

-

28.58

%

-

70.97

% 5.58%

-

22.56

%

-

49.19

%

The above table shows the presentation of current ratio and quick ratio which are

considered to be the most significant ratios which fall under liquidity category. The current ratio

of a business represents the ability of the business to meet the current obligations of the business

which are related to day to day operations of business (Babalola & Abiola, 2013). On the other

hand, quick ratio represents more liquid position of the business and only considers current

11

ACCOUNTING REPORT ANALYSIS

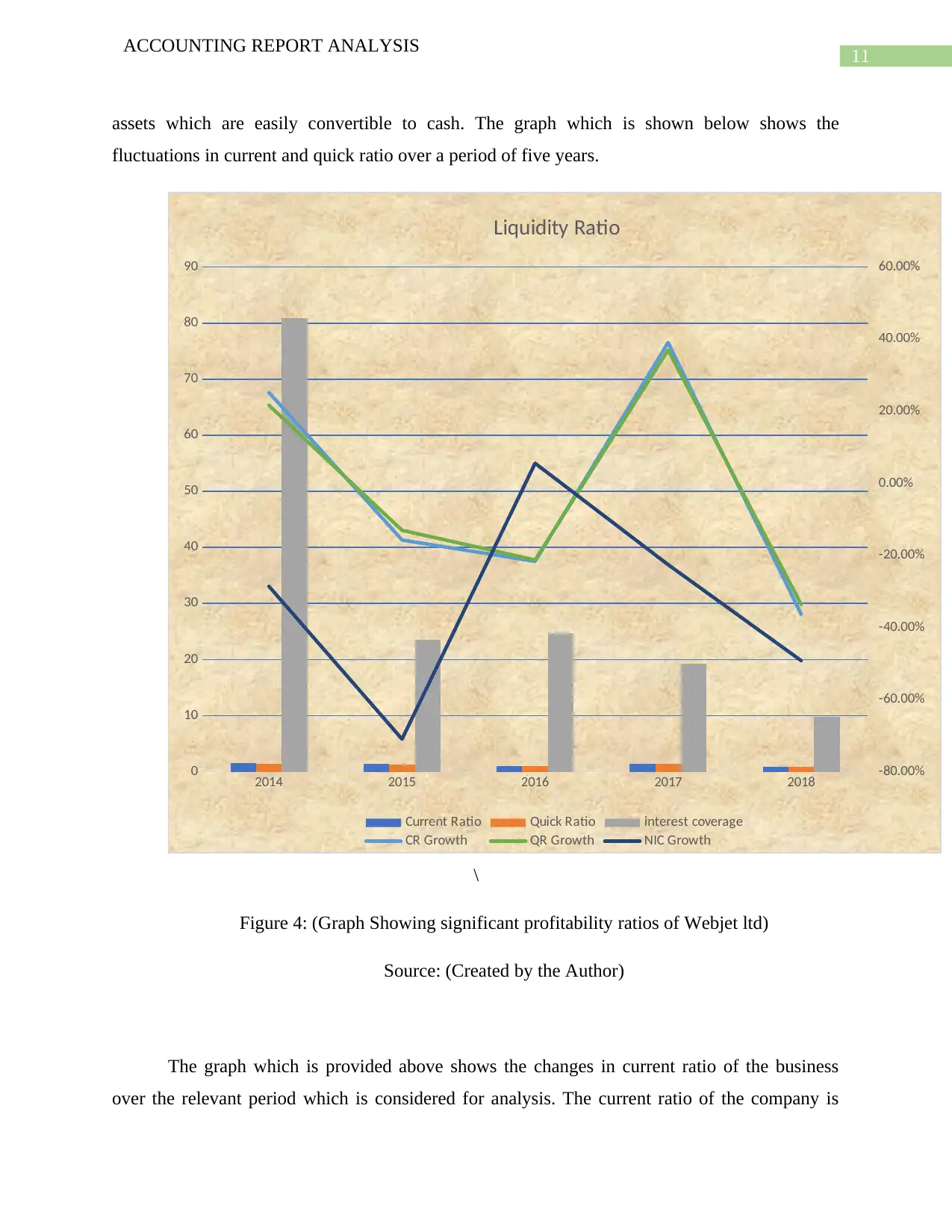

assets which are easily convertible to cash. The graph which is shown below shows the

fluctuations in current and quick ratio over a period of five years.

2014 2015 2016 2017 2018

0

10

20

30

40

50

60

70

80

90

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

Liquidity Ratio

Current Ratio Quick Ratio interest coverage

CR Growth QR Growth NIC Growth

\

Figure 4: (Graph Showing significant profitability ratios of Webjet ltd)

Source: (Created by the Author)

The graph which is provided above shows the changes in current ratio of the business

over the relevant period which is considered for analysis. The current ratio of the company is

ACCOUNTING REPORT ANALYSIS

assets which are easily convertible to cash. The graph which is shown below shows the

fluctuations in current and quick ratio over a period of five years.

2014 2015 2016 2017 2018

0

10

20

30

40

50

60

70

80

90

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

Liquidity Ratio

Current Ratio Quick Ratio interest coverage

CR Growth QR Growth NIC Growth

\

Figure 4: (Graph Showing significant profitability ratios of Webjet ltd)

Source: (Created by the Author)

The graph which is provided above shows the changes in current ratio of the business

over the relevant period which is considered for analysis. The current ratio of the company is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.