Financial Statement Analysis of Webjet (ASX) - FIN5FSA Report

VerifiedAdded on 2023/01/04

|11

|2903

|99

Report

AI Summary

This report presents a comprehensive financial statement analysis of Webjet Limited, a digital business travel company listed on the Australian Stock Exchange (ASX). The analysis covers the company's background, mission, and key accounting policies, including revenue recognition, income tax, lease accounting, and treatment of various financial assets and liabilities. The report examines the company's financial performance, including its share price growth and the impact of acquisitions. It also delves into the accounting practices, judgments, and estimates used by Webjet, referencing relevant accounting standards like AASB 9, AASB 15, and AASB 16. The analysis includes details on functional currency, revenue recognition, income tax, lease accounting, trade receivables, investments, derivatives, plant property and equipment, intangible assets, borrowings, and provisions. The report highlights the company's disclosures and presentation practices in its financial statements. The assignment was completed as part of a Financial Statement Analysis course (FIN5FSA) at La Trobe University, and involved the collection and analysis of financial data over a ten-year period. The report provides insights into Webjet's financial health, accounting methods, and compliance with accounting standards.

financial statement analysis

ASX - WEBJET

Student’s Name

[Email address]

ASX - WEBJET

Student’s Name

[Email address]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Company Background and Mission.............................................................................................................2

Accounting Analysis.....................................................................................................................................2

Key Accounting Policies...........................................................................................................................4

Functional currency.................................................................................................................................4

Revenue Recognition...............................................................................................................................4

Income tax...............................................................................................................................................4

Lease Accounting.....................................................................................................................................4

Trade Receivables....................................................................................................................................5

Investment and other financial assets.....................................................................................................5

Derivatives and Hedging activities...........................................................................................................5

Plant property and equipment................................................................................................................6

Intangible assets......................................................................................................................................6

Borrowings..............................................................................................................................................7

Provisions................................................................................................................................................7

Presentation and disclosures...................................................................................................................7

Judgements and estimates......................................................................................................................8

Bibliography................................................................................................................................................9

Company Background and Mission.............................................................................................................2

Accounting Analysis.....................................................................................................................................2

Key Accounting Policies...........................................................................................................................4

Functional currency.................................................................................................................................4

Revenue Recognition...............................................................................................................................4

Income tax...............................................................................................................................................4

Lease Accounting.....................................................................................................................................4

Trade Receivables....................................................................................................................................5

Investment and other financial assets.....................................................................................................5

Derivatives and Hedging activities...........................................................................................................5

Plant property and equipment................................................................................................................6

Intangible assets......................................................................................................................................6

Borrowings..............................................................................................................................................7

Provisions................................................................................................................................................7

Presentation and disclosures...................................................................................................................7

Judgements and estimates......................................................................................................................8

Bibliography................................................................................................................................................9

Company Background and Mission

Webjet Limited is one of the digital business travel company based out of Australia. The company serves

both the global consumer market (B2C) as well as the wholesale segment (B2B). The company is

registered in Australia but has business operations in New Zealand, Hong Kong, North America and

Singapore as well. The company was founded in 1998 and is listed on the Australian Stock Exchange. The

company has several brands like that of Online Republic, Lots of Hotels, WebBeds, Sunhotels, JacTravel,

FIT Ruums, Totalstay all of which is engaged in providing some or the other web based service, be it

hotel accommodation or travel booking. The company has also made few acquisition in the last few

years in the bid to globalize and expand its services and area of services1. Some of the major acquisitions

have been Zuji in Australia, Singapore and Hong Kong, Online Republic, Jac Travel and DOTW.

The has a whole lot of tools and technologies which enable the company to compare and combine the

domestic and international flight bookings, hotel accommodations, travel insurance, holiday and tour

packages and car hire worldwide. Some of the unique selling propositions of the company which has

been driving its growth and profitability strategy are unparalleled travel choice, 24/7 customer care

support, safe and secure transactions along with the number of choice of payment options. It has won

several awards and has been the most visited online travel agency of the year in Australia2.

The company’s mission has been to be a leader in the online travel agent business and serve more and

more customers. The company also aims to improve the CAGR along with maintaining the cash flows

and ensuring governance. It aims to continue to being the number one ranked OTC in Australia and New

Zealand.

Accounting Analysis

The accounting of the company states the internal policies and how the accounting is done within the

company. It shows what are the standards used in accounting, whether the appropriate rules and

regulations are being used and if the company is following the internal financial controls while

accounting. Accounting in general may be defined as the process of book-keeping and maintenance of

the accounting records of the company. It also includes the reporting aspect of the company and if the

company is enabling the appropriate notes on accounts and disclosures for the public for enabling the

decision making3.

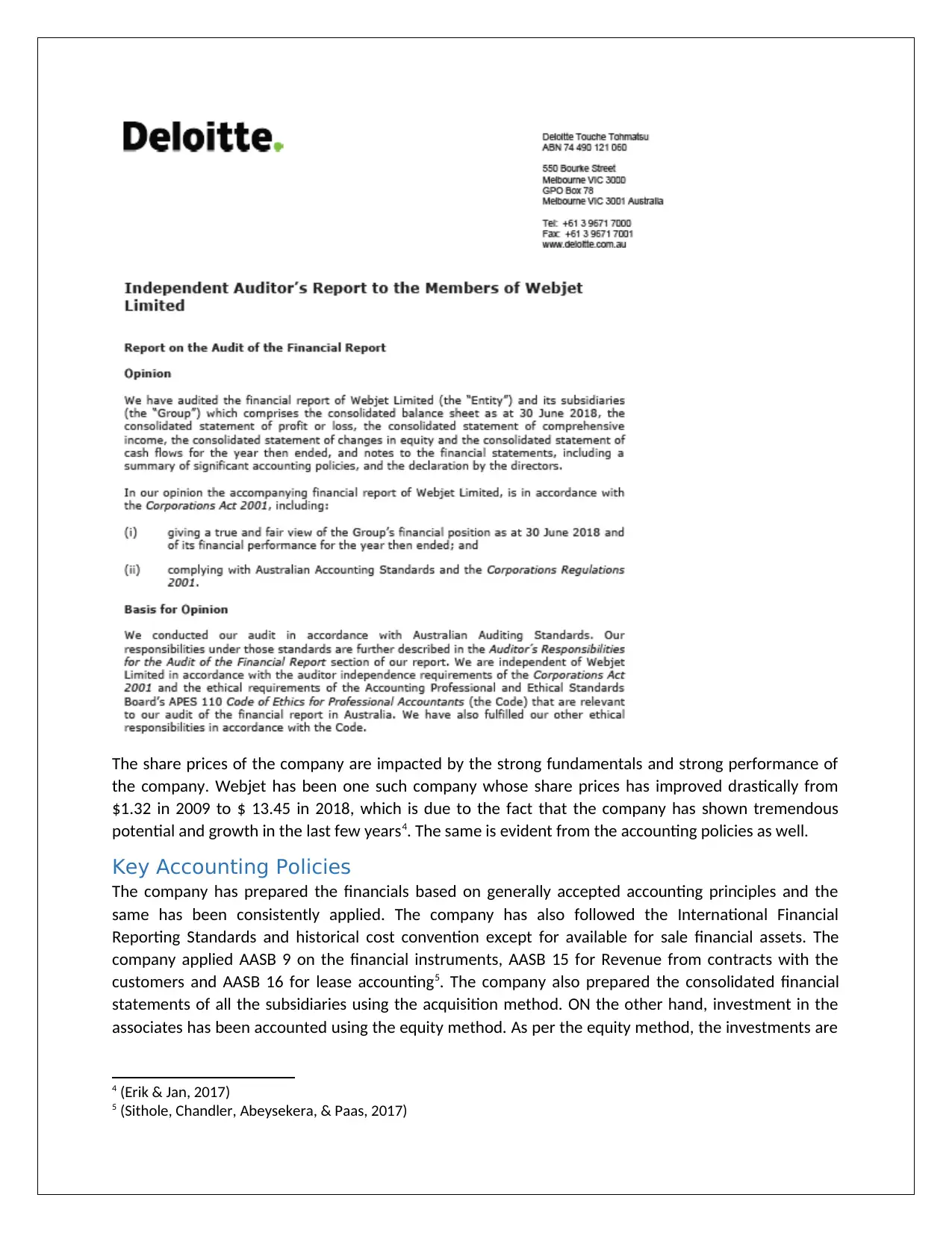

In the given case, it has been certified by the auditors of the company, that the annual accounts of the

company has been prepared by the management in accordance with the Corporation Act, 2001 and the

Australian Accounting Standards. The screenshot of the same has been shown below.

1 (Alexander, 2016)

2 (Alieid, 2016)

3 (Choy, 2018)

Webjet Limited is one of the digital business travel company based out of Australia. The company serves

both the global consumer market (B2C) as well as the wholesale segment (B2B). The company is

registered in Australia but has business operations in New Zealand, Hong Kong, North America and

Singapore as well. The company was founded in 1998 and is listed on the Australian Stock Exchange. The

company has several brands like that of Online Republic, Lots of Hotels, WebBeds, Sunhotels, JacTravel,

FIT Ruums, Totalstay all of which is engaged in providing some or the other web based service, be it

hotel accommodation or travel booking. The company has also made few acquisition in the last few

years in the bid to globalize and expand its services and area of services1. Some of the major acquisitions

have been Zuji in Australia, Singapore and Hong Kong, Online Republic, Jac Travel and DOTW.

The has a whole lot of tools and technologies which enable the company to compare and combine the

domestic and international flight bookings, hotel accommodations, travel insurance, holiday and tour

packages and car hire worldwide. Some of the unique selling propositions of the company which has

been driving its growth and profitability strategy are unparalleled travel choice, 24/7 customer care

support, safe and secure transactions along with the number of choice of payment options. It has won

several awards and has been the most visited online travel agency of the year in Australia2.

The company’s mission has been to be a leader in the online travel agent business and serve more and

more customers. The company also aims to improve the CAGR along with maintaining the cash flows

and ensuring governance. It aims to continue to being the number one ranked OTC in Australia and New

Zealand.

Accounting Analysis

The accounting of the company states the internal policies and how the accounting is done within the

company. It shows what are the standards used in accounting, whether the appropriate rules and

regulations are being used and if the company is following the internal financial controls while

accounting. Accounting in general may be defined as the process of book-keeping and maintenance of

the accounting records of the company. It also includes the reporting aspect of the company and if the

company is enabling the appropriate notes on accounts and disclosures for the public for enabling the

decision making3.

In the given case, it has been certified by the auditors of the company, that the annual accounts of the

company has been prepared by the management in accordance with the Corporation Act, 2001 and the

Australian Accounting Standards. The screenshot of the same has been shown below.

1 (Alexander, 2016)

2 (Alieid, 2016)

3 (Choy, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The share prices of the company are impacted by the strong fundamentals and strong performance of

the company. Webjet has been one such company whose share prices has improved drastically from

$1.32 in 2009 to $ 13.45 in 2018, which is due to the fact that the company has shown tremendous

potential and growth in the last few years4. The same is evident from the accounting policies as well.

Key Accounting Policies

The company has prepared the financials based on generally accepted accounting principles and the

same has been consistently applied. The company has also followed the International Financial

Reporting Standards and historical cost convention except for available for sale financial assets. The

company applied AASB 9 on the financial instruments, AASB 15 for Revenue from contracts with the

customers and AASB 16 for lease accounting5. The company also prepared the consolidated financial

statements of all the subsidiaries using the acquisition method. ON the other hand, investment in the

associates has been accounted using the equity method. As per the equity method, the investments are

4 (Erik & Jan, 2017)

5 (Sithole, Chandler, Abeysekera, & Paas, 2017)

the company. Webjet has been one such company whose share prices has improved drastically from

$1.32 in 2009 to $ 13.45 in 2018, which is due to the fact that the company has shown tremendous

potential and growth in the last few years4. The same is evident from the accounting policies as well.

Key Accounting Policies

The company has prepared the financials based on generally accepted accounting principles and the

same has been consistently applied. The company has also followed the International Financial

Reporting Standards and historical cost convention except for available for sale financial assets. The

company applied AASB 9 on the financial instruments, AASB 15 for Revenue from contracts with the

customers and AASB 16 for lease accounting5. The company also prepared the consolidated financial

statements of all the subsidiaries using the acquisition method. ON the other hand, investment in the

associates has been accounted using the equity method. As per the equity method, the investments are

4 (Erik & Jan, 2017)

5 (Sithole, Chandler, Abeysekera, & Paas, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

first accounted at cost and then adjusted thereafter to show the profit or loss on account of the same in

the other comprehensive income.

Functional currency

The functional currency of the company has been considered to be Australian Dollars. Foreign exchange

losses or gain arising on account of the borrowings are shown along with the finance expenses in the

profit and loss account which is line with the accounting standards6.

Revenue Recognition

The company recognizes revenue both as the principal as well as in the role of agent in provision of

online travel booking services and the same is measured at fair value of the consideration received or

receivable. The company recognizes the revenue in the books only when the amount is certain and can

be reliably measured and it is quite probable that the economic benefits will flow to the entity. When

acting as agent, the revenue is recognized when the booking is made and the payment is received from

the customer and when acting as principal, the revenue is recognized only on the date of travel. IN case

the advance has been received the same is shown in deferred revenue7. Some of the other streams of

revenue include dividend income which is recognized when the right to receive the same has been

established and the interest income which is recognized in the books using the effective interest rate

method.

Income tax

The income tax is accounted for in the books in line with tax laws governing the state in which the

business operates. Deferred income tax is calculated based on the liability method and the temporary

differences arising on account of the tax base of the assets and liabilities are shown in the deferred tax

asset and deferred tax liability account8.

Lease Accounting

The leases are classified as the finance lease in the balance sheet when the significant risk and reward

and the ownership of the asset has been transferred to the lessee. ON the other hand, if the risk and

rewards of ownership are not transferred to the lessee, the same is classified as operating lease by the

entity. The income and expense on account of the operating leases are shown in the profit and loss

account of the entity. The same is being recognized on the straight line basis and in case of the finance

lease, the assets are being shown in the balance sheet – assets side9.

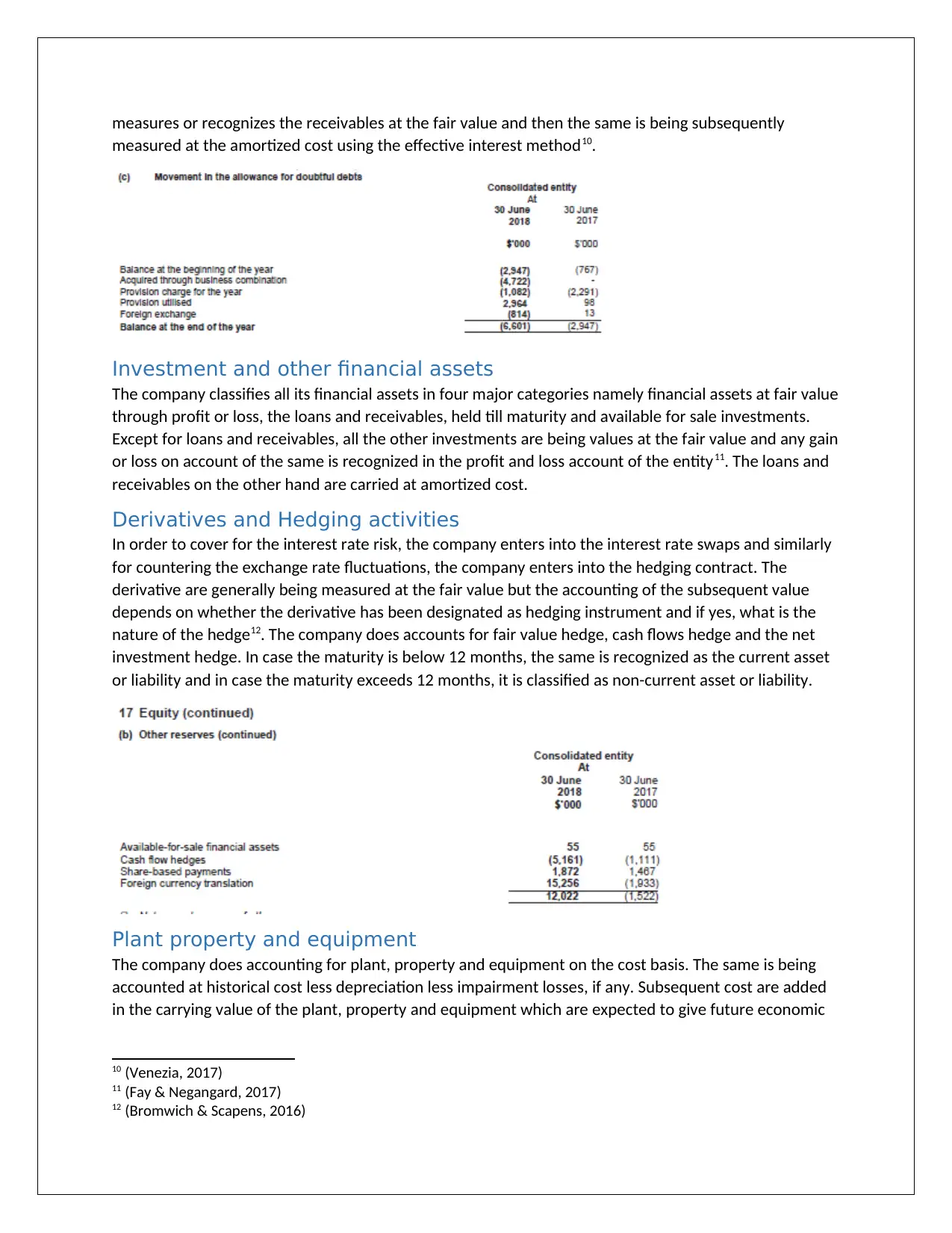

Trade Receivables

In terms of the receivables of the company, the total outstanding and the amount of provision for

impairment has been shown in the notes to accounts. It is also accompanied by the ageing of the

receivables of the company in 3 categories namely 30-90 days, 90-180 days and greater than 180 days.

In the last disclosure w.r.t. the receivables, the movement of bad debt allowance has been shown which

helps the users in understanding the provision creation and provision reversal. The company initially

6 (Dichev, 2017)

7 (Goldmann, 2016)

8 (Heminway, 2017)

9 (Werner, 2017)

the other comprehensive income.

Functional currency

The functional currency of the company has been considered to be Australian Dollars. Foreign exchange

losses or gain arising on account of the borrowings are shown along with the finance expenses in the

profit and loss account which is line with the accounting standards6.

Revenue Recognition

The company recognizes revenue both as the principal as well as in the role of agent in provision of

online travel booking services and the same is measured at fair value of the consideration received or

receivable. The company recognizes the revenue in the books only when the amount is certain and can

be reliably measured and it is quite probable that the economic benefits will flow to the entity. When

acting as agent, the revenue is recognized when the booking is made and the payment is received from

the customer and when acting as principal, the revenue is recognized only on the date of travel. IN case

the advance has been received the same is shown in deferred revenue7. Some of the other streams of

revenue include dividend income which is recognized when the right to receive the same has been

established and the interest income which is recognized in the books using the effective interest rate

method.

Income tax

The income tax is accounted for in the books in line with tax laws governing the state in which the

business operates. Deferred income tax is calculated based on the liability method and the temporary

differences arising on account of the tax base of the assets and liabilities are shown in the deferred tax

asset and deferred tax liability account8.

Lease Accounting

The leases are classified as the finance lease in the balance sheet when the significant risk and reward

and the ownership of the asset has been transferred to the lessee. ON the other hand, if the risk and

rewards of ownership are not transferred to the lessee, the same is classified as operating lease by the

entity. The income and expense on account of the operating leases are shown in the profit and loss

account of the entity. The same is being recognized on the straight line basis and in case of the finance

lease, the assets are being shown in the balance sheet – assets side9.

Trade Receivables

In terms of the receivables of the company, the total outstanding and the amount of provision for

impairment has been shown in the notes to accounts. It is also accompanied by the ageing of the

receivables of the company in 3 categories namely 30-90 days, 90-180 days and greater than 180 days.

In the last disclosure w.r.t. the receivables, the movement of bad debt allowance has been shown which

helps the users in understanding the provision creation and provision reversal. The company initially

6 (Dichev, 2017)

7 (Goldmann, 2016)

8 (Heminway, 2017)

9 (Werner, 2017)

measures or recognizes the receivables at the fair value and then the same is being subsequently

measured at the amortized cost using the effective interest method10.

Investment and other financial assets

The company classifies all its financial assets in four major categories namely financial assets at fair value

through profit or loss, the loans and receivables, held till maturity and available for sale investments.

Except for loans and receivables, all the other investments are being values at the fair value and any gain

or loss on account of the same is recognized in the profit and loss account of the entity11. The loans and

receivables on the other hand are carried at amortized cost.

Derivatives and Hedging activities

In order to cover for the interest rate risk, the company enters into the interest rate swaps and similarly

for countering the exchange rate fluctuations, the company enters into the hedging contract. The

derivative are generally being measured at the fair value but the accounting of the subsequent value

depends on whether the derivative has been designated as hedging instrument and if yes, what is the

nature of the hedge12. The company does accounts for fair value hedge, cash flows hedge and the net

investment hedge. In case the maturity is below 12 months, the same is recognized as the current asset

or liability and in case the maturity exceeds 12 months, it is classified as non-current asset or liability.

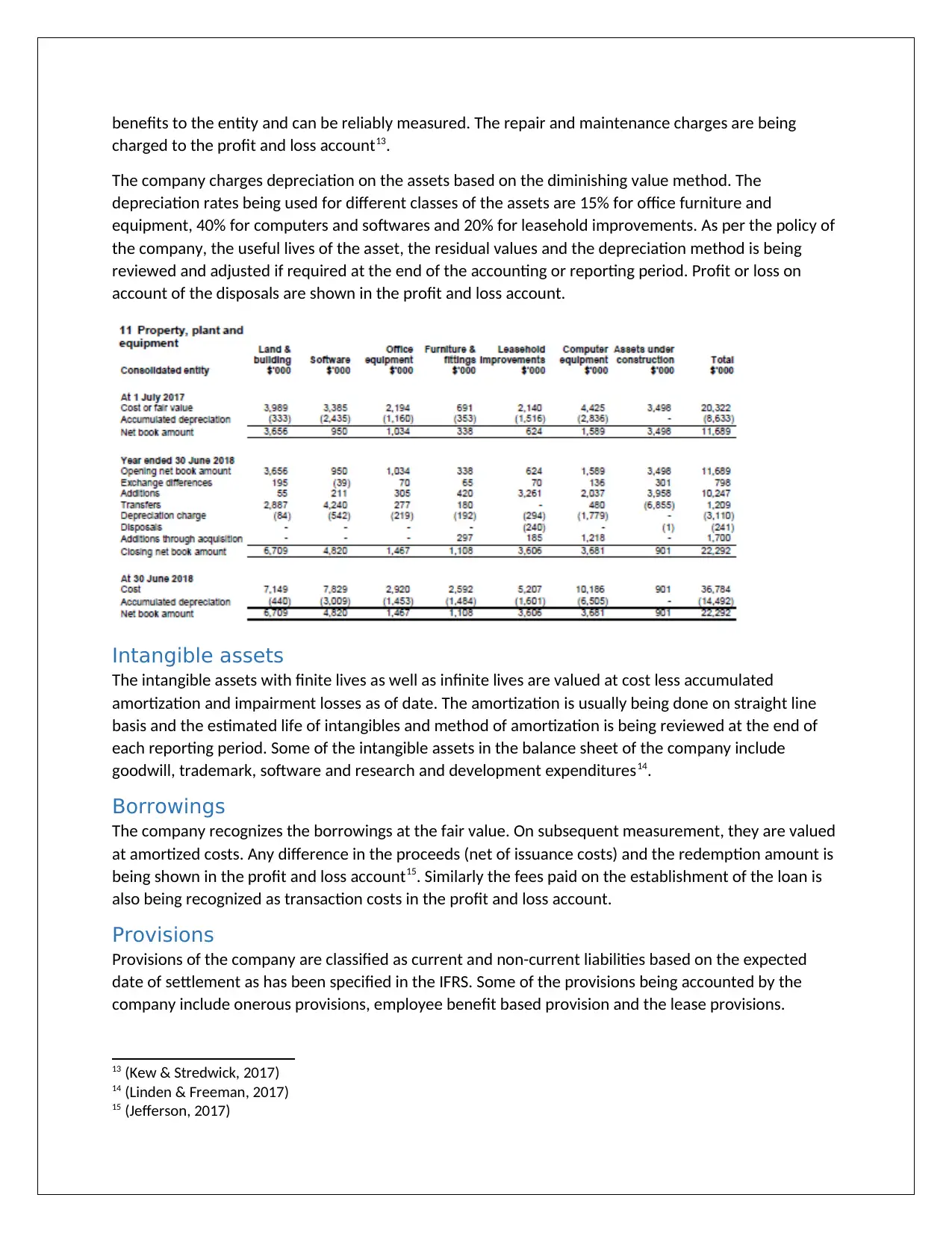

Plant property and equipment

The company does accounting for plant, property and equipment on the cost basis. The same is being

accounted at historical cost less depreciation less impairment losses, if any. Subsequent cost are added

in the carrying value of the plant, property and equipment which are expected to give future economic

10 (Venezia, 2017)

11 (Fay & Negangard, 2017)

12 (Bromwich & Scapens, 2016)

measured at the amortized cost using the effective interest method10.

Investment and other financial assets

The company classifies all its financial assets in four major categories namely financial assets at fair value

through profit or loss, the loans and receivables, held till maturity and available for sale investments.

Except for loans and receivables, all the other investments are being values at the fair value and any gain

or loss on account of the same is recognized in the profit and loss account of the entity11. The loans and

receivables on the other hand are carried at amortized cost.

Derivatives and Hedging activities

In order to cover for the interest rate risk, the company enters into the interest rate swaps and similarly

for countering the exchange rate fluctuations, the company enters into the hedging contract. The

derivative are generally being measured at the fair value but the accounting of the subsequent value

depends on whether the derivative has been designated as hedging instrument and if yes, what is the

nature of the hedge12. The company does accounts for fair value hedge, cash flows hedge and the net

investment hedge. In case the maturity is below 12 months, the same is recognized as the current asset

or liability and in case the maturity exceeds 12 months, it is classified as non-current asset or liability.

Plant property and equipment

The company does accounting for plant, property and equipment on the cost basis. The same is being

accounted at historical cost less depreciation less impairment losses, if any. Subsequent cost are added

in the carrying value of the plant, property and equipment which are expected to give future economic

10 (Venezia, 2017)

11 (Fay & Negangard, 2017)

12 (Bromwich & Scapens, 2016)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

benefits to the entity and can be reliably measured. The repair and maintenance charges are being

charged to the profit and loss account13.

The company charges depreciation on the assets based on the diminishing value method. The

depreciation rates being used for different classes of the assets are 15% for office furniture and

equipment, 40% for computers and softwares and 20% for leasehold improvements. As per the policy of

the company, the useful lives of the asset, the residual values and the depreciation method is being

reviewed and adjusted if required at the end of the accounting or reporting period. Profit or loss on

account of the disposals are shown in the profit and loss account.

Intangible assets

The intangible assets with finite lives as well as infinite lives are valued at cost less accumulated

amortization and impairment losses as of date. The amortization is usually being done on straight line

basis and the estimated life of intangibles and method of amortization is being reviewed at the end of

each reporting period. Some of the intangible assets in the balance sheet of the company include

goodwill, trademark, software and research and development expenditures14.

Borrowings

The company recognizes the borrowings at the fair value. On subsequent measurement, they are valued

at amortized costs. Any difference in the proceeds (net of issuance costs) and the redemption amount is

being shown in the profit and loss account15. Similarly the fees paid on the establishment of the loan is

also being recognized as transaction costs in the profit and loss account.

Provisions

Provisions of the company are classified as current and non-current liabilities based on the expected

date of settlement as has been specified in the IFRS. Some of the provisions being accounted by the

company include onerous provisions, employee benefit based provision and the lease provisions.

13 (Kew & Stredwick, 2017)

14 (Linden & Freeman, 2017)

15 (Jefferson, 2017)

charged to the profit and loss account13.

The company charges depreciation on the assets based on the diminishing value method. The

depreciation rates being used for different classes of the assets are 15% for office furniture and

equipment, 40% for computers and softwares and 20% for leasehold improvements. As per the policy of

the company, the useful lives of the asset, the residual values and the depreciation method is being

reviewed and adjusted if required at the end of the accounting or reporting period. Profit or loss on

account of the disposals are shown in the profit and loss account.

Intangible assets

The intangible assets with finite lives as well as infinite lives are valued at cost less accumulated

amortization and impairment losses as of date. The amortization is usually being done on straight line

basis and the estimated life of intangibles and method of amortization is being reviewed at the end of

each reporting period. Some of the intangible assets in the balance sheet of the company include

goodwill, trademark, software and research and development expenditures14.

Borrowings

The company recognizes the borrowings at the fair value. On subsequent measurement, they are valued

at amortized costs. Any difference in the proceeds (net of issuance costs) and the redemption amount is

being shown in the profit and loss account15. Similarly the fees paid on the establishment of the loan is

also being recognized as transaction costs in the profit and loss account.

Provisions

Provisions of the company are classified as current and non-current liabilities based on the expected

date of settlement as has been specified in the IFRS. Some of the provisions being accounted by the

company include onerous provisions, employee benefit based provision and the lease provisions.

13 (Kew & Stredwick, 2017)

14 (Linden & Freeman, 2017)

15 (Jefferson, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Presentation and disclosures

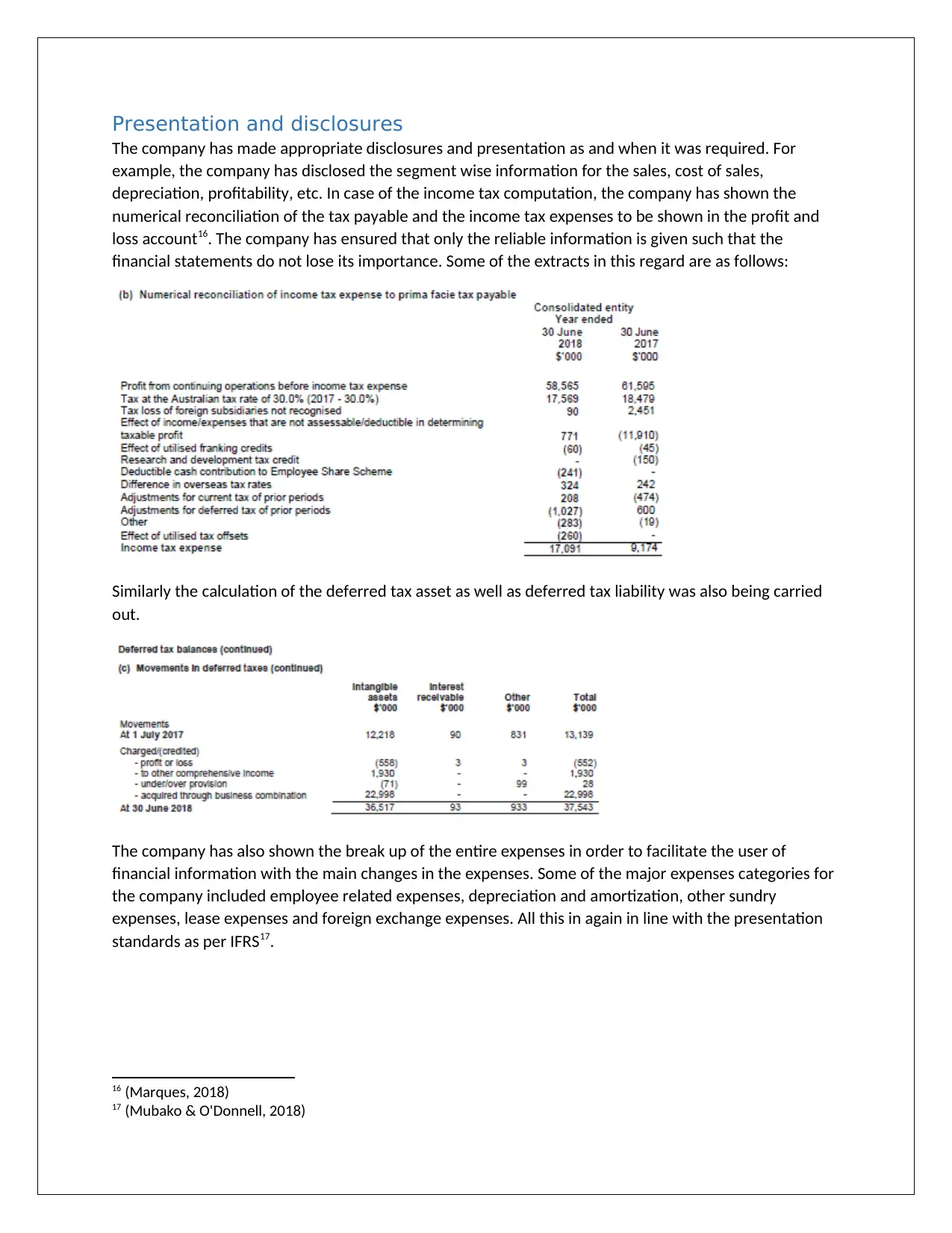

The company has made appropriate disclosures and presentation as and when it was required. For

example, the company has disclosed the segment wise information for the sales, cost of sales,

depreciation, profitability, etc. In case of the income tax computation, the company has shown the

numerical reconciliation of the tax payable and the income tax expenses to be shown in the profit and

loss account16. The company has ensured that only the reliable information is given such that the

financial statements do not lose its importance. Some of the extracts in this regard are as follows:

Similarly the calculation of the deferred tax asset as well as deferred tax liability was also being carried

out.

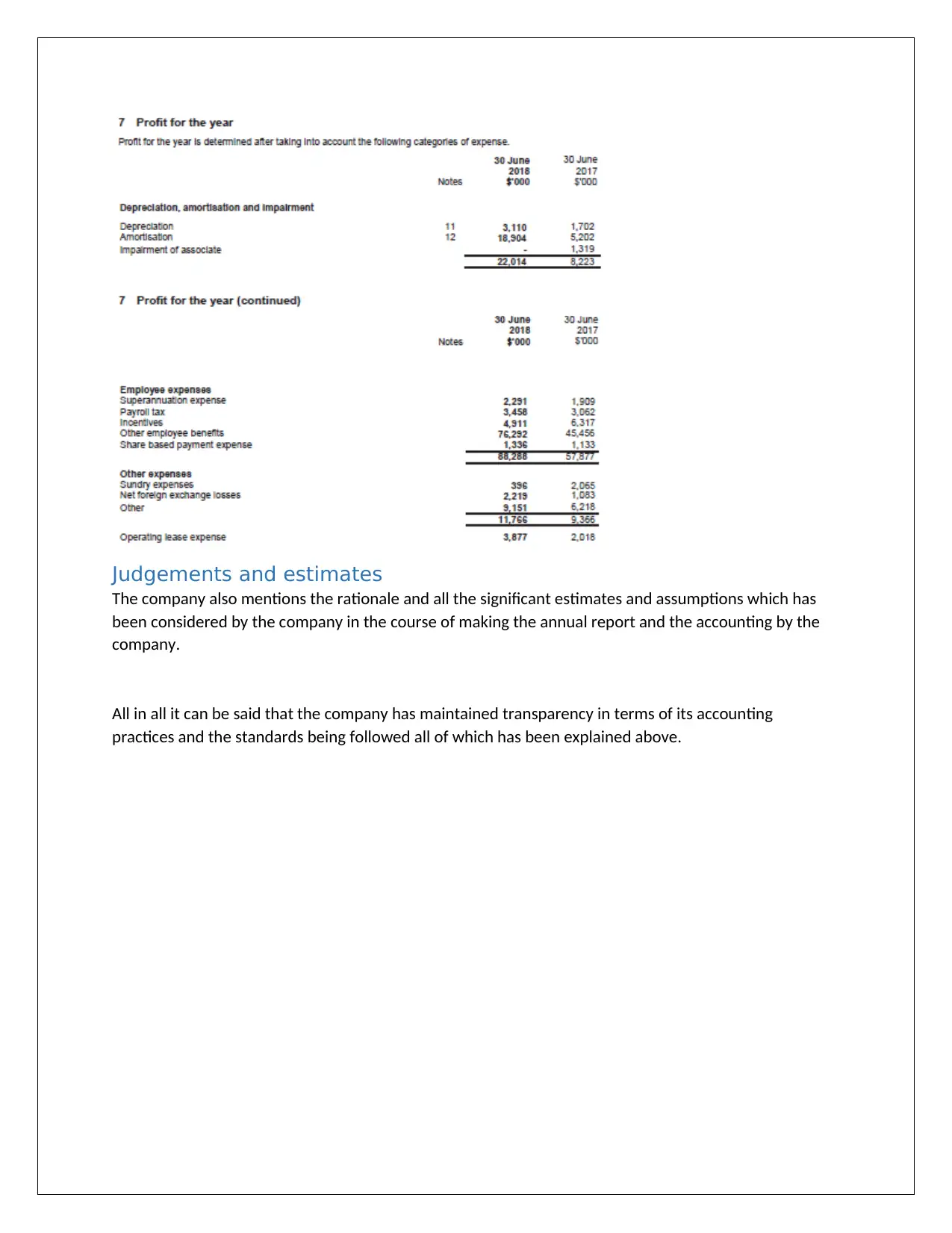

The company has also shown the break up of the entire expenses in order to facilitate the user of

financial information with the main changes in the expenses. Some of the major expenses categories for

the company included employee related expenses, depreciation and amortization, other sundry

expenses, lease expenses and foreign exchange expenses. All this in again in line with the presentation

standards as per IFRS17.

16 (Marques, 2018)

17 (Mubako & O'Donnell, 2018)

The company has made appropriate disclosures and presentation as and when it was required. For

example, the company has disclosed the segment wise information for the sales, cost of sales,

depreciation, profitability, etc. In case of the income tax computation, the company has shown the

numerical reconciliation of the tax payable and the income tax expenses to be shown in the profit and

loss account16. The company has ensured that only the reliable information is given such that the

financial statements do not lose its importance. Some of the extracts in this regard are as follows:

Similarly the calculation of the deferred tax asset as well as deferred tax liability was also being carried

out.

The company has also shown the break up of the entire expenses in order to facilitate the user of

financial information with the main changes in the expenses. Some of the major expenses categories for

the company included employee related expenses, depreciation and amortization, other sundry

expenses, lease expenses and foreign exchange expenses. All this in again in line with the presentation

standards as per IFRS17.

16 (Marques, 2018)

17 (Mubako & O'Donnell, 2018)

Judgements and estimates

The company also mentions the rationale and all the significant estimates and assumptions which has

been considered by the company in the course of making the annual report and the accounting by the

company.

All in all it can be said that the company has maintained transparency in terms of its accounting

practices and the standards being followed all of which has been explained above.

The company also mentions the rationale and all the significant estimates and assumptions which has

been considered by the company in the course of making the annual report and the accounting by the

company.

All in all it can be said that the company has maintained transparency in terms of its accounting

practices and the standards being followed all of which has been explained above.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bibliography

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Alieid, E. E. (2016). The Role of Accounting Information Systems in Making Investment Decisions.

Internal Auditing & Risk Management, 11(2), 233-242.

Bromwich, M., & Scapens, R. (2016). Management Accounting Research: 25 years on. Management

Accounting Research, 31(1), 1-9.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 3(1), 145. doi:https://doi.org/10.1016/j.ecolecon.2017.08.005

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Erik, H., & Jan, B. (2017). Supply chain management and activity-based costing: Current status and

directions for the future. International Journal of Physical Distribution & Logistics Management,

47(8), 712-735.

Fay, R., & Negangard, E. (2017). Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, 38, 37-49.

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 1-35.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Kew, J., & Stredwick, J. (2017). Business Environment: Managing in a Strategic Context (2nd ed.).

London: Chartered Institute of Personnel and Development.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Marques, R. P. (2018). Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, 820-830.

Mubako, G., & O'Donnell, E. (2018). Effect of fraud risk assessments on auditor skepticism: Unintended

consequences on evidence evaluation. International Journal of Auditing, 22(1), 55-64.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Alieid, E. E. (2016). The Role of Accounting Information Systems in Making Investment Decisions.

Internal Auditing & Risk Management, 11(2), 233-242.

Bromwich, M., & Scapens, R. (2016). Management Accounting Research: 25 years on. Management

Accounting Research, 31(1), 1-9.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 3(1), 145. doi:https://doi.org/10.1016/j.ecolecon.2017.08.005

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Erik, H., & Jan, B. (2017). Supply chain management and activity-based costing: Current status and

directions for the future. International Journal of Physical Distribution & Logistics Management,

47(8), 712-735.

Fay, R., & Negangard, E. (2017). Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, 38, 37-49.

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 1-35.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Kew, J., & Stredwick, J. (2017). Business Environment: Managing in a Strategic Context (2nd ed.).

London: Chartered Institute of Personnel and Development.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Marques, R. P. (2018). Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, 820-830.

Mubako, G., & O'Donnell, E. (2018). Effect of fraud risk assessments on auditor skepticism: Unintended

consequences on evidence evaluation. International Journal of Auditing, 22(1), 55-64.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Venezia, I. (2017). Behavioral Finance: 'Where Do Investors'' Biases Come From?'. Singapore: WORLD

SCIENTIFIC.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), 57-80.

SCIENTIFIC.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), 57-80.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.