Impairment Write-Downs in Australian Companies: Wesfarmers Analysis

VerifiedAdded on 2021/05/31

|11

|2012

|56

Report

AI Summary

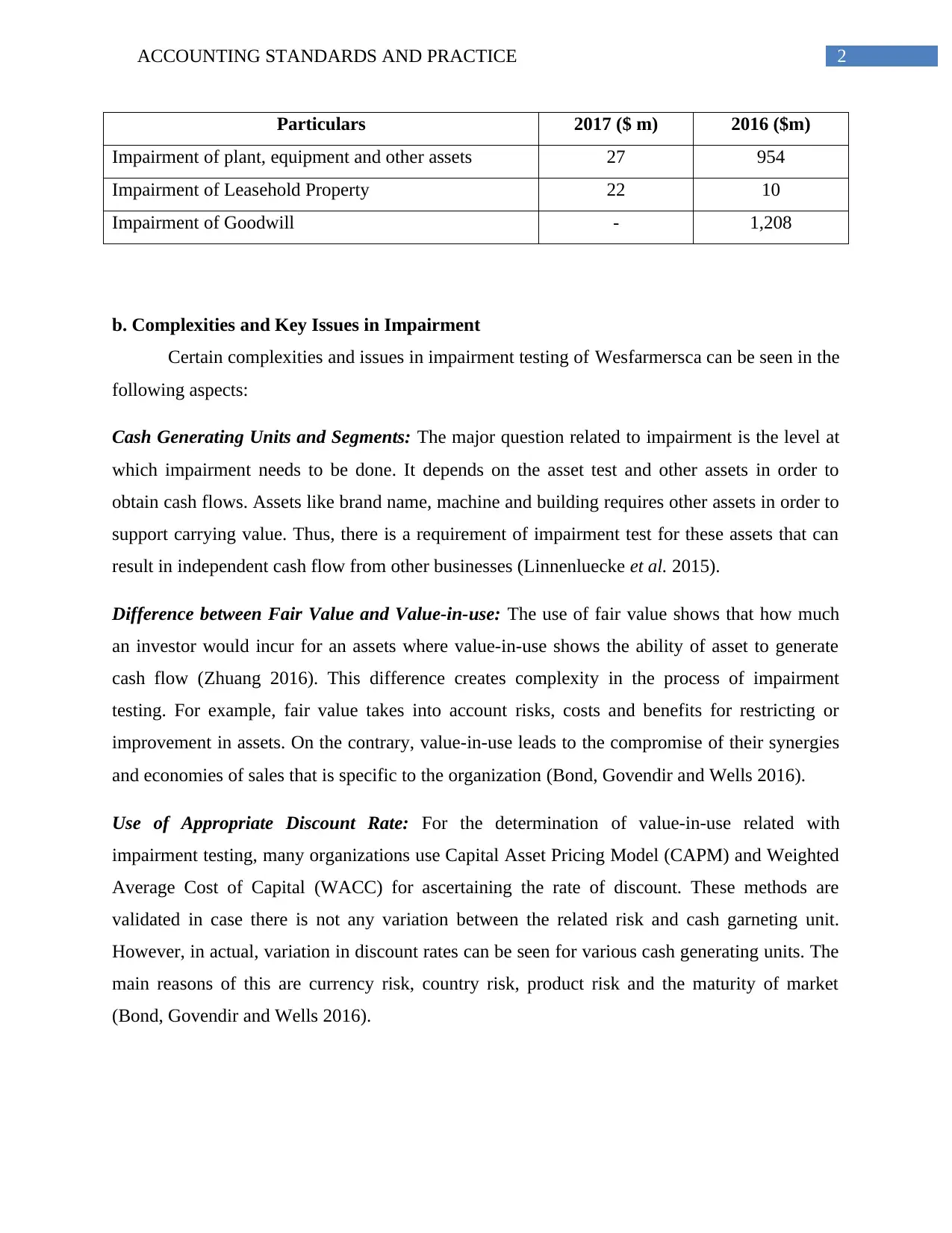

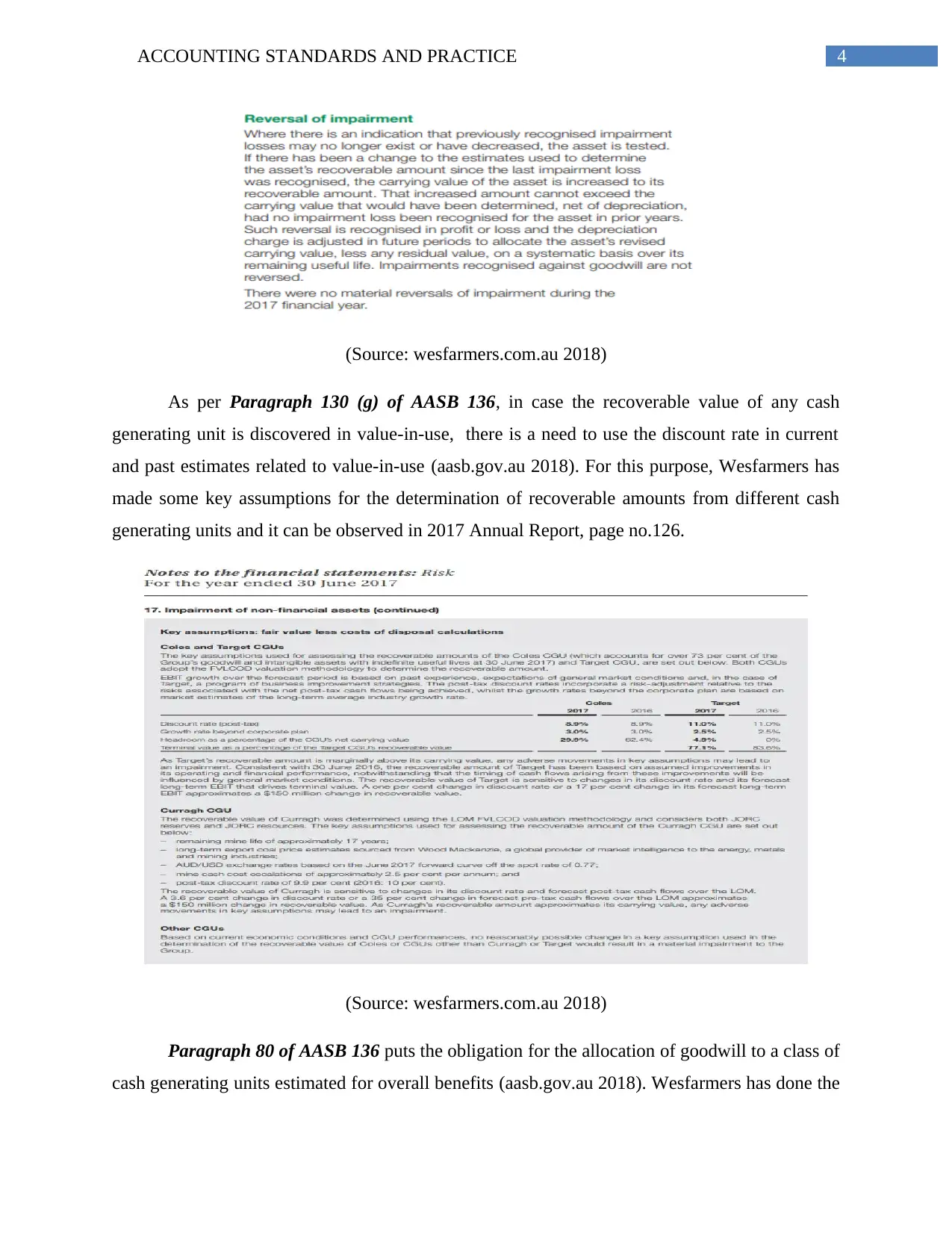

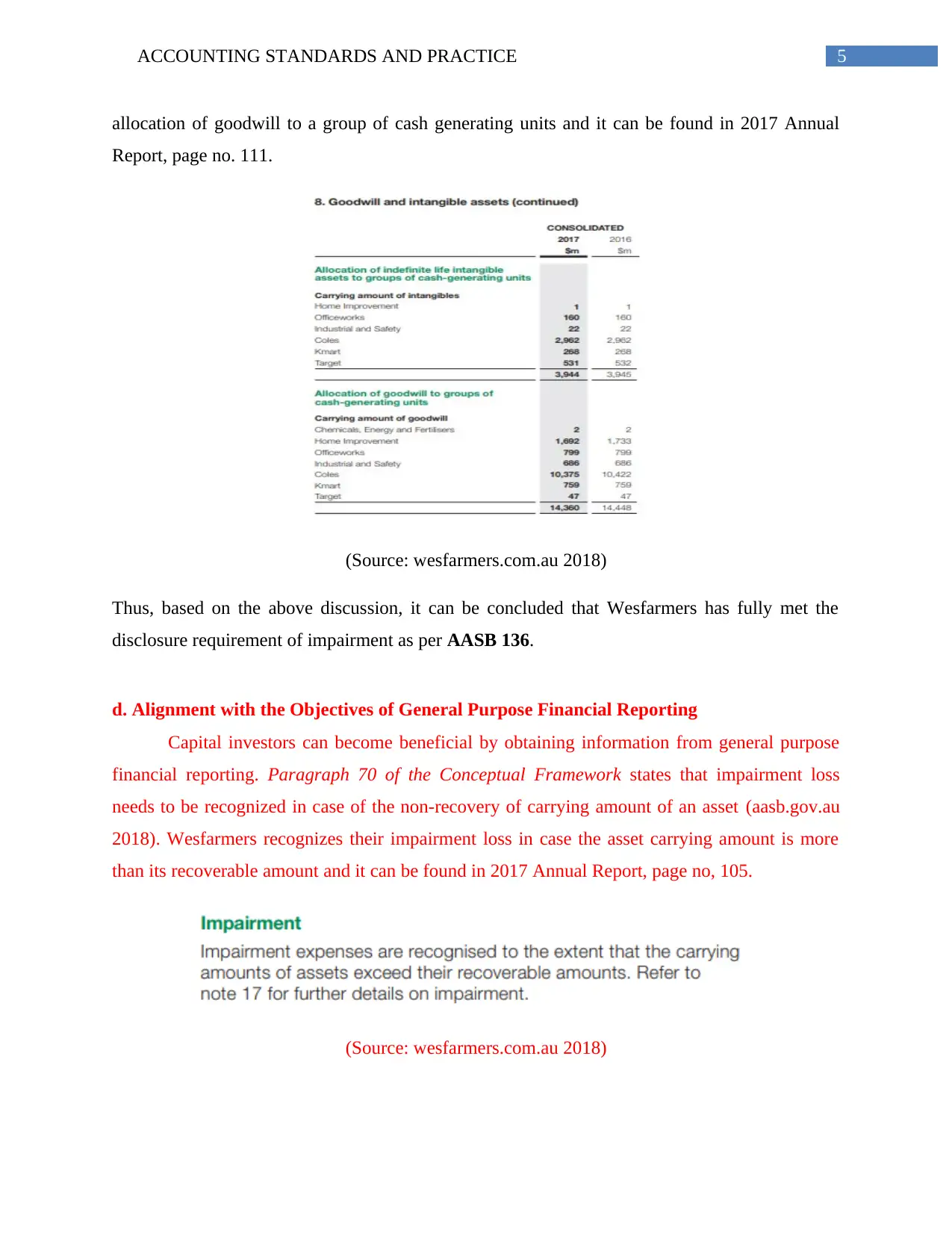

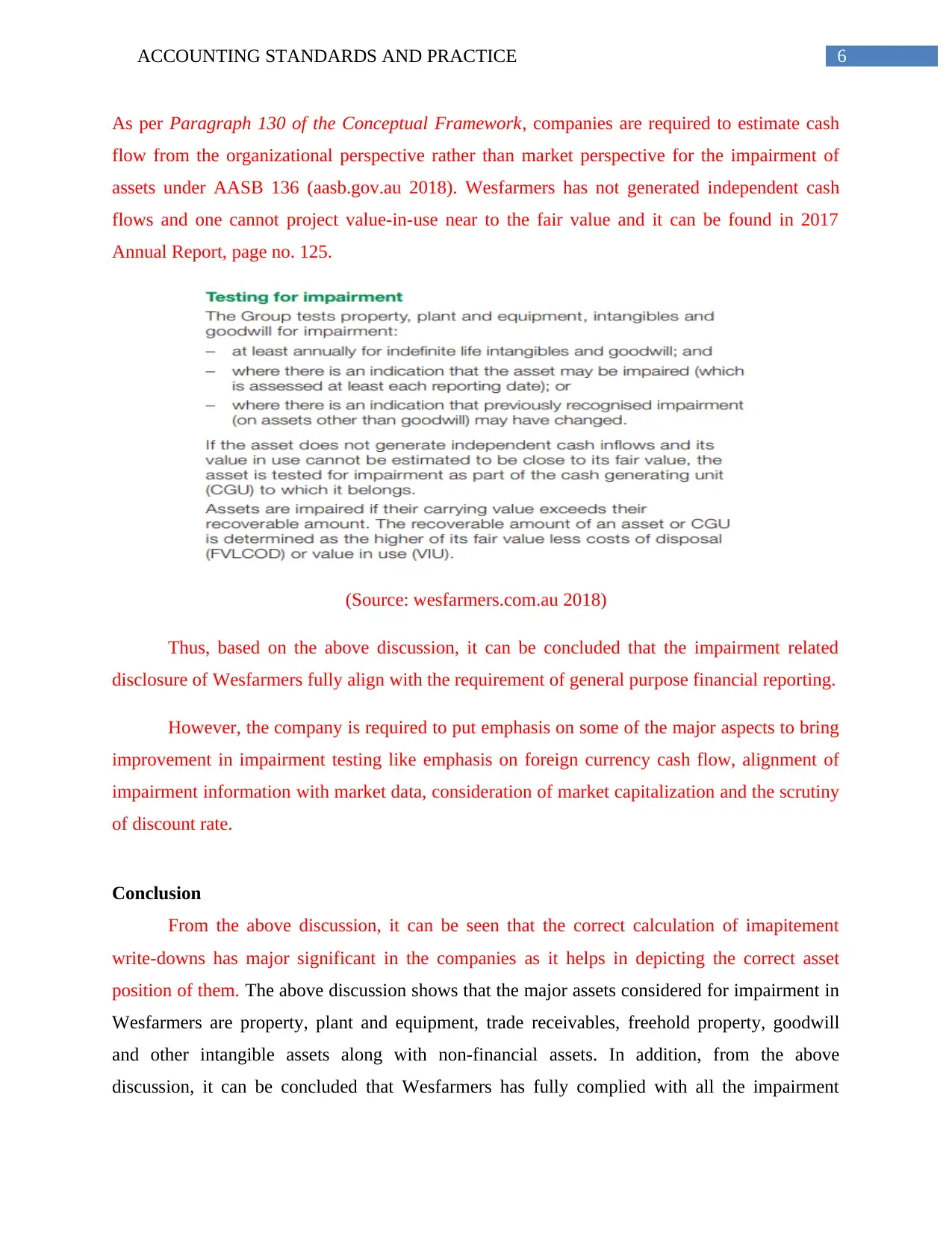

This report provides a comprehensive analysis of impairment write-downs for Wesfarmers Limited, a prominent Australian retailer. The report begins with an overview of impairment write-downs, detailing the specific assets tested, including property, plant, and equipment, trade receivables, goodwill, and other intangible assets. It then delves into the complexities and key issues in impairment accounting, focusing on cash-generating units, the differences between fair value and value-in-use, and the use of appropriate discount rates. The report subsequently assesses Wesfarmers' compliance with AASB 136 disclosure requirements, providing specific examples from the company's annual report. Finally, it evaluates the alignment of Wesfarmers' impairment accounting with the objectives of general-purpose financial reporting, highlighting areas of compliance and suggesting potential improvements. The report concludes by emphasizing the importance of accurate impairment calculations in portraying a company's true asset position and overall financial health, while also suggesting areas for future improvement in Wesfarmers' impairment testing practices.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.