Capital Market Reaction and Financial Reporting: Wesfarmers Plc

VerifiedAdded on 2020/02/19

|18

|3454

|240

Report

AI Summary

This report provides a comprehensive analysis of the accounting policies and estimates employed by Wesfarmers Plc. It delves into the company's adherence to International Financial Reporting Standards (IFRS), examining specific accounting policies like the written-down value method for assets, AASB16 lease recognition, and impairment tests for intangible assets. The report assesses the judgments and estimates made by Wesfarmers' management, including those related to income tax, inventory valuation, and commitments. A comparison with competitors like Morrison Plc is presented, highlighting differences in accounting treatments. The report also evaluates accounting flexibility, identifies potential red flags in Wesfarmers' financial reporting, and suggests improvements for accounting policies and estimates. The analysis covers how Wesfarmers has adapted to changes in accounting standards and provides a detailed overview of its financial reporting practices and their implications for the capital market.

RUNNING HEAD: Accounting policies and estimates used by firm

1

Name of the Student-

Title-Research proposal (Reaction of capital market to financial reporting)

University Name-

1

Name of the Student-

Title-Research proposal (Reaction of capital market to financial reporting)

University Name-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting policies and estimates used by firm 2

Table of Contents

Introduction.................................................................................................................................................3

Present description of company..................................................................................................................3

Accounting policies followed by Wesfarmers..............................................................................................4

Estimates used by Wesfarmers plc..........................................................................................................5

Estimates used by rivals...........................................................................................................................6

Comparison of accounting policies and estimates used by Wesfarmers and Morrison plc.....................6

Assesse accounting flexibility..................................................................................................................8

Evaluation of accounting strategies and policies.........................................................................................8

Changes in accounting estimates by the Wesfarmers.............................................................................9

Suggestion for accounting policies and estimates prepared by Wesfarmers........................................10

Red flag in accounting report of Wesfarmers Plc......................................................................................10

Conclusion.................................................................................................................................................13

References.................................................................................................................................................14

Table of Contents

Introduction.................................................................................................................................................3

Present description of company..................................................................................................................3

Accounting policies followed by Wesfarmers..............................................................................................4

Estimates used by Wesfarmers plc..........................................................................................................5

Estimates used by rivals...........................................................................................................................6

Comparison of accounting policies and estimates used by Wesfarmers and Morrison plc.....................6

Assesse accounting flexibility..................................................................................................................8

Evaluation of accounting strategies and policies.........................................................................................8

Changes in accounting estimates by the Wesfarmers.............................................................................9

Suggestion for accounting policies and estimates prepared by Wesfarmers........................................10

Red flag in accounting report of Wesfarmers Plc......................................................................................10

Conclusion.................................................................................................................................................13

References.................................................................................................................................................14

Accounting policies and estimates used by firm 3

Introduction

In this report, it is given that reporting frameworks of organization are depends upon the

accounting standards and reporting framework of organization. Accounting policies are the

standard and specific rules, procedure and accounting implication which are implemented by the

organizations to prepare their financial statements. This report reflects the study on the principles

rules, procedure and consistency in adoption of accounting policies used by organization. With a

view to understand the practical implication of accounting policies and measures, Wesfarmers

Plc has been taken into consideration in this report. This company has adopted international

financial reporting standards and establish harmonization in its GAAP rules and regulation and

application international accounting standard.

Present description of company

Wesfarmers plc is an Australian conglomerate company having headquartered in perth.

This company has increased its total turnover by 25% as compared to last five years data and

resulted to overall total revenue to 65.98 billion AUD in 2016. Company has been preparing its

financial statement by following GAAP rules and IFRS accounting standards in determined

approach. This level of compliance in preparation of financial statement helps company to

adhere with the international financial accounting system (Kieso, Weygandt and Warfield,

2010).

Introduction

In this report, it is given that reporting frameworks of organization are depends upon the

accounting standards and reporting framework of organization. Accounting policies are the

standard and specific rules, procedure and accounting implication which are implemented by the

organizations to prepare their financial statements. This report reflects the study on the principles

rules, procedure and consistency in adoption of accounting policies used by organization. With a

view to understand the practical implication of accounting policies and measures, Wesfarmers

Plc has been taken into consideration in this report. This company has adopted international

financial reporting standards and establish harmonization in its GAAP rules and regulation and

application international accounting standard.

Present description of company

Wesfarmers plc is an Australian conglomerate company having headquartered in perth.

This company has increased its total turnover by 25% as compared to last five years data and

resulted to overall total revenue to 65.98 billion AUD in 2016. Company has been preparing its

financial statement by following GAAP rules and IFRS accounting standards in determined

approach. This level of compliance in preparation of financial statement helps company to

adhere with the international financial accounting system (Kieso, Weygandt and Warfield,

2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting policies and estimates used by firm 4

With the increasing ramification of economic changes, adoption of international policies

for preparation of financial statement has become necessary. Accounting policies are very

important for the proper understanding of the information provided in the financial statements.

Accounting disclosure is also an important part as many international accounting policies and

standards allow companies to make alternative treatment for same transactions. However, an

entity is not allowed to change its adopted accounting policies for the particular transactions for

consecutive period (Cairns, et al. 2011).

Accounting policies followed by Wesfarmers

There are several accounting policies followed by Wesfarmers Plc while reporting its

transactions in the financial statements (Irvine and Moerman, 2017).

Wesfarmers plc has adopted written down value method to reflects the true value of its

assets as per the IFRS rules and standards (Hussey and Ong, 2017).

As per the AASB16 lease, Wesfarmers has made a provision to recognize the right-of-use

assets representing to use underlying leased assets.

All the consolidated financial statement of company and financial details shown would be

disclosed as per the AASB-5 IFRS rules and standard.

All the intangible assets will be gone through under the impairment test each and every

year. Loss arise from the impairment test firstly deducted from the goodwill amount then

after from the other cash generating units of company as per the adopted IAS 136 by

Wesfarmers (de Ricquebourg and Jonathan, 2013).

With the increasing ramification of economic changes, adoption of international policies

for preparation of financial statement has become necessary. Accounting policies are very

important for the proper understanding of the information provided in the financial statements.

Accounting disclosure is also an important part as many international accounting policies and

standards allow companies to make alternative treatment for same transactions. However, an

entity is not allowed to change its adopted accounting policies for the particular transactions for

consecutive period (Cairns, et al. 2011).

Accounting policies followed by Wesfarmers

There are several accounting policies followed by Wesfarmers Plc while reporting its

transactions in the financial statements (Irvine and Moerman, 2017).

Wesfarmers plc has adopted written down value method to reflects the true value of its

assets as per the IFRS rules and standards (Hussey and Ong, 2017).

As per the AASB16 lease, Wesfarmers has made a provision to recognize the right-of-use

assets representing to use underlying leased assets.

All the consolidated financial statement of company and financial details shown would be

disclosed as per the AASB-5 IFRS rules and standard.

All the intangible assets will be gone through under the impairment test each and every

year. Loss arise from the impairment test firstly deducted from the goodwill amount then

after from the other cash generating units of company as per the adopted IAS 136 by

Wesfarmers (de Ricquebourg and Jonathan, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting policies and estimates used by firm 5

As per the AASB 101 all the required details and basis of financial statements have been

shown in the notes to accounts of company.

Estimates used by Wesfarmers plc

In the process of applying the group’s accounting policies and standards management

department of Wesfarmers plc has applied number of judgments and estimates of future

events such as income tax payment, valuation of inventories, impairment of non-financial

assets, associated and joint ventures transactions and commitment of company and identified

contingencies (Clinton, Pinello and Skaife, 2014). In addition to this, Wesfarmers has relies

on the estimates given by its subsidiaries companies while preparing consolidated financial

statements. Company has also estimated that there will be no amendments and new

circulations of IFRS rules and standard and complied with the present IFRS standards and

accounting policies to prepare its financial statement as per the AASB 101. However there

are key success factors for the Wesfarmers after adoption of international accounting policies

and standards (Nobes and Stadler, 2015).

All the international investors would make easy interpretation of the financial data and

will showcase the international regulatory compliance

All the consolidated financial statement of company and financial details shown would be

disclosed as per the AASB-5 IFRS rules and standard (Steman, 2016).

Wesfarmers has adopted international financial reporting standards and establish

harmonization in its GAAP rules and regulation and application international accounting

standards.

Wesfarmers has estimated that after implementation of IFRS rules and IAS-136

impairment test, company has shown true and fair view of its assets to shareholders.

As per the AASB 101 all the required details and basis of financial statements have been

shown in the notes to accounts of company.

Estimates used by Wesfarmers plc

In the process of applying the group’s accounting policies and standards management

department of Wesfarmers plc has applied number of judgments and estimates of future

events such as income tax payment, valuation of inventories, impairment of non-financial

assets, associated and joint ventures transactions and commitment of company and identified

contingencies (Clinton, Pinello and Skaife, 2014). In addition to this, Wesfarmers has relies

on the estimates given by its subsidiaries companies while preparing consolidated financial

statements. Company has also estimated that there will be no amendments and new

circulations of IFRS rules and standard and complied with the present IFRS standards and

accounting policies to prepare its financial statement as per the AASB 101. However there

are key success factors for the Wesfarmers after adoption of international accounting policies

and standards (Nobes and Stadler, 2015).

All the international investors would make easy interpretation of the financial data and

will showcase the international regulatory compliance

All the consolidated financial statement of company and financial details shown would be

disclosed as per the AASB-5 IFRS rules and standard (Steman, 2016).

Wesfarmers has adopted international financial reporting standards and establish

harmonization in its GAAP rules and regulation and application international accounting

standards.

Wesfarmers has estimated that after implementation of IFRS rules and IAS-136

impairment test, company has shown true and fair view of its assets to shareholders.

Accounting policies and estimates used by firm 6

It has set estimation for liabilities for wages and salary including non-monetary

transactions and explained that all the transaction should be set off within 12 months

from the reporting period.

Estimates used by rivals

Tesco, Woolworth and Morrison plc has also implemented this proper level of IFRS rules

and accounting policies estimated for preparing their financial statement. However, as per

their management strategies, they have different basis for bifurcating their loss and expenses

as revenue and capital losses. In addition to this, these companies have also harmonized IFRS

rules and domestic accounting rules in their accounting policies to prepare financial

statements (Mardini, Crawford and Power, 2015).

Comparison of accounting policies and estimates used by Wesfarmers and

Morrison plc

Accounting rules Wesfarmers plc Morrison plc

IFRS-5 ( Rehabilitation of

funds

Company has treated this

transaction as capital nature

transaction and booked

entries to record the

rehabilitation of funds in

balance sheet of company

(Cline, Garner and Yore,

2014).

Treated as capital nature

transaction and created

provision for the same in

case of contingency.

It has set estimation for liabilities for wages and salary including non-monetary

transactions and explained that all the transaction should be set off within 12 months

from the reporting period.

Estimates used by rivals

Tesco, Woolworth and Morrison plc has also implemented this proper level of IFRS rules

and accounting policies estimated for preparing their financial statement. However, as per

their management strategies, they have different basis for bifurcating their loss and expenses

as revenue and capital losses. In addition to this, these companies have also harmonized IFRS

rules and domestic accounting rules in their accounting policies to prepare financial

statements (Mardini, Crawford and Power, 2015).

Comparison of accounting policies and estimates used by Wesfarmers and

Morrison plc

Accounting rules Wesfarmers plc Morrison plc

IFRS-5 ( Rehabilitation of

funds

Company has treated this

transaction as capital nature

transaction and booked

entries to record the

rehabilitation of funds in

balance sheet of company

(Cline, Garner and Yore,

2014).

Treated as capital nature

transaction and created

provision for the same in

case of contingency.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting policies and estimates used by firm 7

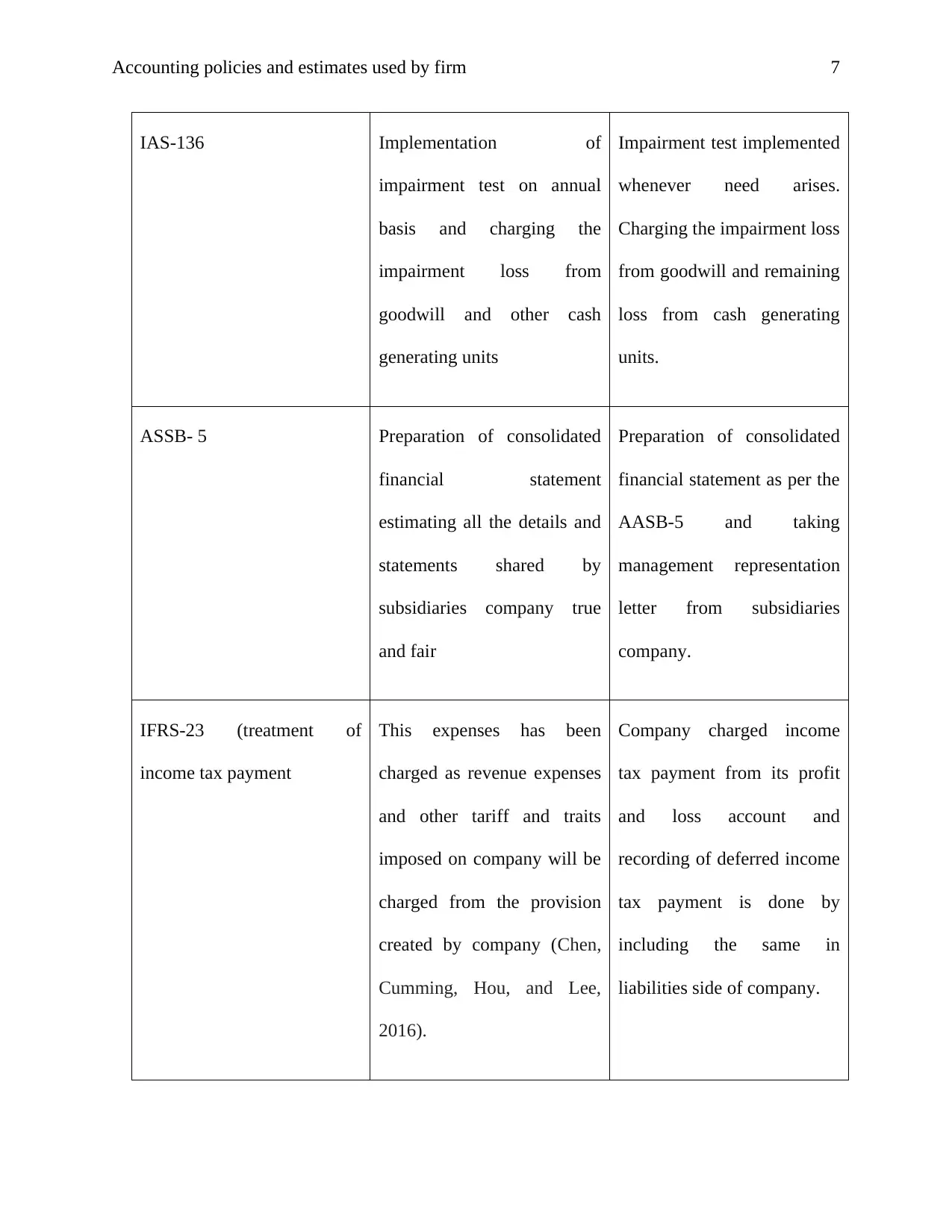

IAS-136 Implementation of

impairment test on annual

basis and charging the

impairment loss from

goodwill and other cash

generating units

Impairment test implemented

whenever need arises.

Charging the impairment loss

from goodwill and remaining

loss from cash generating

units.

ASSB- 5 Preparation of consolidated

financial statement

estimating all the details and

statements shared by

subsidiaries company true

and fair

Preparation of consolidated

financial statement as per the

AASB-5 and taking

management representation

letter from subsidiaries

company.

IFRS-23 (treatment of

income tax payment

This expenses has been

charged as revenue expenses

and other tariff and traits

imposed on company will be

charged from the provision

created by company (Chen,

Cumming, Hou, and Lee,

2016).

Company charged income

tax payment from its profit

and loss account and

recording of deferred income

tax payment is done by

including the same in

liabilities side of company.

IAS-136 Implementation of

impairment test on annual

basis and charging the

impairment loss from

goodwill and other cash

generating units

Impairment test implemented

whenever need arises.

Charging the impairment loss

from goodwill and remaining

loss from cash generating

units.

ASSB- 5 Preparation of consolidated

financial statement

estimating all the details and

statements shared by

subsidiaries company true

and fair

Preparation of consolidated

financial statement as per the

AASB-5 and taking

management representation

letter from subsidiaries

company.

IFRS-23 (treatment of

income tax payment

This expenses has been

charged as revenue expenses

and other tariff and traits

imposed on company will be

charged from the provision

created by company (Chen,

Cumming, Hou, and Lee,

2016).

Company charged income

tax payment from its profit

and loss account and

recording of deferred income

tax payment is done by

including the same in

liabilities side of company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting policies and estimates used by firm 8

Assesse accounting flexibility

After evaluating the financial statement of Wesfarmers plc, it is considered that management

department has allowed accountant of company to measure the value of assets as per the

estimated fair value (Christensen, et al. 2015). However, changes in the same could be made on

the basis of strong backup and invoices. Interest payment has also been deducted from the profit

and loss account of company which could be converted into capital expenses on the basis of

changes in accounting treatment and changes in treatment of banks charges. It is observed that

the self- insured risk liabilities of the Wesfarmers plc is based on number of management

estimates including future inflation, investment return, application of accounting standard and

valuing of fair value of assets of company (Ball, Li and Shivakumar, 2015).

Evaluation of accounting strategies and policies

The estimation adopted by management department of Wesfarmers plc allows them to

distort the information and manipulate the earned profit of company in easy and determined

approach. Management department has charged some of the hedge fund loss from it profit

and loss account which not only reduces the overall profit but also decrease the tax payment

to government. In addition to this, while preparation of consolidated financial statement,

Wesfarmers has estimated that all the information disclosed by company is based on the

financial and non-financial transaction of company. Wesfarmers has also faced problem due

to application of GAAP rules and accounting standard due to different international financial

accounting standard. Wesfarmers had problem in recording of its assets liabilities in its books

of account due to different rules and standards (Sytnik, 2014). For instance, plants and

Assesse accounting flexibility

After evaluating the financial statement of Wesfarmers plc, it is considered that management

department has allowed accountant of company to measure the value of assets as per the

estimated fair value (Christensen, et al. 2015). However, changes in the same could be made on

the basis of strong backup and invoices. Interest payment has also been deducted from the profit

and loss account of company which could be converted into capital expenses on the basis of

changes in accounting treatment and changes in treatment of banks charges. It is observed that

the self- insured risk liabilities of the Wesfarmers plc is based on number of management

estimates including future inflation, investment return, application of accounting standard and

valuing of fair value of assets of company (Ball, Li and Shivakumar, 2015).

Evaluation of accounting strategies and policies

The estimation adopted by management department of Wesfarmers plc allows them to

distort the information and manipulate the earned profit of company in easy and determined

approach. Management department has charged some of the hedge fund loss from it profit

and loss account which not only reduces the overall profit but also decrease the tax payment

to government. In addition to this, while preparation of consolidated financial statement,

Wesfarmers has estimated that all the information disclosed by company is based on the

financial and non-financial transaction of company. Wesfarmers has also faced problem due

to application of GAAP rules and accounting standard due to different international financial

accounting standard. Wesfarmers had problem in recording of its assets liabilities in its books

of account due to different rules and standards (Sytnik, 2014). For instance, plants and

Accounting policies and estimates used by firm 9

machinery has been booked by company at their cost value after deducting depreciation as

per the IFRS rules and standards. On the other hand, as per the GAAP rules these assets

would have shown at the market value or book value whichever is higher. This level of

conflict result to misinterpretation of financial statement to stakeholder of company.

Nonetheless, company has been disclosed material information of company on quarterly

basis and consolidated financial statement of company is filed on the annual basis to

domestic and international authority. The notes to accounts of company disclosed by the

company are as per the AASB 101 of the international accounting standard which discloses

all the material information about the company (Brochet, Naranjo and Yu, 2016).

Changes in accounting estimates by the Wesfarmers

After evaluating the financial statement of company, it is observed that company has

changed its accounting policies to books its hedge funds contracts and change in accounting

estimates shall be recognized by prospectively by including it in its profit and loss account. It

is observed that due to changes in accounting estimates if any loss arise in the valuation of

assets and liabilities of company then it will be treated as impairment loss and will be

deducted from the cash generating units of Wesfarmers plc (Bischof, Brüggemann and

Daske, 2014).

Suggestion for accounting policies and estimates prepared by Wesfarmers

It is evaluated that Wesfarmers plc has applied number of judgments and estimates of

future events such as income tax payment, valuation of inventories, impairment of non-

financial assets, associated and joint ventures transactions and commitment of company and

identified contingencies (Barth, 2013). This has shown that estimation of tax payment should

machinery has been booked by company at their cost value after deducting depreciation as

per the IFRS rules and standards. On the other hand, as per the GAAP rules these assets

would have shown at the market value or book value whichever is higher. This level of

conflict result to misinterpretation of financial statement to stakeholder of company.

Nonetheless, company has been disclosed material information of company on quarterly

basis and consolidated financial statement of company is filed on the annual basis to

domestic and international authority. The notes to accounts of company disclosed by the

company are as per the AASB 101 of the international accounting standard which discloses

all the material information about the company (Brochet, Naranjo and Yu, 2016).

Changes in accounting estimates by the Wesfarmers

After evaluating the financial statement of company, it is observed that company has

changed its accounting policies to books its hedge funds contracts and change in accounting

estimates shall be recognized by prospectively by including it in its profit and loss account. It

is observed that due to changes in accounting estimates if any loss arise in the valuation of

assets and liabilities of company then it will be treated as impairment loss and will be

deducted from the cash generating units of Wesfarmers plc (Bischof, Brüggemann and

Daske, 2014).

Suggestion for accounting policies and estimates prepared by Wesfarmers

It is evaluated that Wesfarmers plc has applied number of judgments and estimates of

future events such as income tax payment, valuation of inventories, impairment of non-

financial assets, associated and joint ventures transactions and commitment of company and

identified contingencies (Barth, 2013). This has shown that estimation of tax payment should

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting policies and estimates used by firm 10

be based on the past results and trend analysis of company. In addition to this, company has

also charged consideration payment in its strategic alliance as capital nature expenses.

Therefore, it could be inferred that if company have conflict in compliance with the domestic

and international financial reporting standard then it should comply with the IFRS rules and

standards. Nonetheless, all the estimates and provisions created by company should be based

on the actuaries’ method of calculation and their contingency plan should be based on past

result of organization (Aobdia, Lin and Petacchi, 2015).

Red flag in accounting report of Wesfarmers Plc

Red flag in accounting reporting of Wesfarmers plc could be defined as potential

problems and issues faced by company while accounting and reporting of its financial

statements. There are several factors that could be taken into account by the company to

identify the red flag in accounting report of Wesfarmers plc (Atkins and Maroun, 2015).

Monitor revenue and capital expenditure of company

One of the main problematic areas for Wesfarmers plc arises from the allocation of

revenue and capital expenditure. Accountant of Wesfarmers plc has charged all the

borrowing cost as revenue cost and charged the same from the profit and loss accountant.

This has shown that company has treated borrowing cost as revenue expenses with a view to

reduce the overall profit. However, as per the IFRS rules and standard, company could treat

their borrowing cost as revenue cost or capital cost. This has shown that Wesfarmers has

treated all of its borrowing cost as revenue expenses with a view to save tax payment to

government. This is one major Red Flag which reflects that company has followed particular

working process to reduce the tax payment.

be based on the past results and trend analysis of company. In addition to this, company has

also charged consideration payment in its strategic alliance as capital nature expenses.

Therefore, it could be inferred that if company have conflict in compliance with the domestic

and international financial reporting standard then it should comply with the IFRS rules and

standards. Nonetheless, all the estimates and provisions created by company should be based

on the actuaries’ method of calculation and their contingency plan should be based on past

result of organization (Aobdia, Lin and Petacchi, 2015).

Red flag in accounting report of Wesfarmers Plc

Red flag in accounting reporting of Wesfarmers plc could be defined as potential

problems and issues faced by company while accounting and reporting of its financial

statements. There are several factors that could be taken into account by the company to

identify the red flag in accounting report of Wesfarmers plc (Atkins and Maroun, 2015).

Monitor revenue and capital expenditure of company

One of the main problematic areas for Wesfarmers plc arises from the allocation of

revenue and capital expenditure. Accountant of Wesfarmers plc has charged all the

borrowing cost as revenue cost and charged the same from the profit and loss accountant.

This has shown that company has treated borrowing cost as revenue expenses with a view to

reduce the overall profit. However, as per the IFRS rules and standard, company could treat

their borrowing cost as revenue cost or capital cost. This has shown that Wesfarmers has

treated all of its borrowing cost as revenue expenses with a view to save tax payment to

government. This is one major Red Flag which reflects that company has followed particular

working process to reduce the tax payment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting policies and estimates used by firm 11

Determination of depreciation amount to identify the true value of assets

It is evaluated that companies in Australia are could follow different methods to charge

depreciation on the fixed assets of company. It is evaluated that some time it is necessary to

follow straight line method for charging depreciation on the fixed assets of company. For

instance, Wesfarmers has charged written down value method to charge depreciation on its

plant and machinery. It is observed that due to high complexity of machinery values and

determining the overall capital expenditure of plants and machinery, company should have

charged all of its assets by using straight line method. Wesfarmers has used written down

value method for charging its assets and determining the true and fair view of assets. This has

increased red flag in the accounting policies and issues of organization (Jaggi, et al. 2016).

Inventory valuation method

As per the IFRS rules and IAS-3 each and every listed company should follow FIFO and

LIFO method in inventory management. However, Wesfarmers has followed FIFO method

in its inventory management. It is considered after evaluating the annual report of

Wesfarmers that company has followed FIFO method in acquiring and managing inventories

in its warehouse. It becomes complex for the organization to maintain its inventory through

LIFO method. As per the IFRS rules, company has to follow particular inventory

management method for complete reporting year. However, Wesfarmers has been making

inventory management method by changing its FIFO method to LIFO method. Wesfarmers

has also manipulated its economic order quantity which could be found by computing overall

total turnover of company since last five years. This level of inventory management policies

has increased its overall total turnover by average 30% as compared to last five year data. In

Determination of depreciation amount to identify the true value of assets

It is evaluated that companies in Australia are could follow different methods to charge

depreciation on the fixed assets of company. It is evaluated that some time it is necessary to

follow straight line method for charging depreciation on the fixed assets of company. For

instance, Wesfarmers has charged written down value method to charge depreciation on its

plant and machinery. It is observed that due to high complexity of machinery values and

determining the overall capital expenditure of plants and machinery, company should have

charged all of its assets by using straight line method. Wesfarmers has used written down

value method for charging its assets and determining the true and fair view of assets. This has

increased red flag in the accounting policies and issues of organization (Jaggi, et al. 2016).

Inventory valuation method

As per the IFRS rules and IAS-3 each and every listed company should follow FIFO and

LIFO method in inventory management. However, Wesfarmers has followed FIFO method

in its inventory management. It is considered after evaluating the annual report of

Wesfarmers that company has followed FIFO method in acquiring and managing inventories

in its warehouse. It becomes complex for the organization to maintain its inventory through

LIFO method. As per the IFRS rules, company has to follow particular inventory

management method for complete reporting year. However, Wesfarmers has been making

inventory management method by changing its FIFO method to LIFO method. Wesfarmers

has also manipulated its economic order quantity which could be found by computing overall

total turnover of company since last five years. This level of inventory management policies

has increased its overall total turnover by average 30% as compared to last five year data. In

Accounting policies and estimates used by firm 12

addition to this costing of company has also increased by 20% by using this FIFO method

which will decrease the overall tax payment. Moreover, the impairment loss charged by

company from its cash generating units which has destructed the value of overall assets.

Changes in net income, cash flow and related party transactions impact

As per the IAS24, Wesfarmers plc should not enter into any transactions with the

company to which it has pecuniary and material relation. However, company has allowed

payment to directors without passing special resolutions. However, disclaimer for the same

has been given in the notes to accounts. This has reflected the biggest red flag for the

company. Company has also charged contingent amount of expenses from its profit and loss

which has decrease its overall profit but due to the no amount of cash outflow from the

business operation of Wesfarmers, it has shown no impact on the cash flow statement.

However, as per the accounting policies, recording of transactions in both case is relevant but

from the broader point of view it may allow auditors to pass auditors remark on the same.

addition to this costing of company has also increased by 20% by using this FIFO method

which will decrease the overall tax payment. Moreover, the impairment loss charged by

company from its cash generating units which has destructed the value of overall assets.

Changes in net income, cash flow and related party transactions impact

As per the IAS24, Wesfarmers plc should not enter into any transactions with the

company to which it has pecuniary and material relation. However, company has allowed

payment to directors without passing special resolutions. However, disclaimer for the same

has been given in the notes to accounts. This has reflected the biggest red flag for the

company. Company has also charged contingent amount of expenses from its profit and loss

which has decrease its overall profit but due to the no amount of cash outflow from the

business operation of Wesfarmers, it has shown no impact on the cash flow statement.

However, as per the accounting policies, recording of transactions in both case is relevant but

from the broader point of view it may allow auditors to pass auditors remark on the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.