Accounting Theory and Current Issues: Wesfarmers Ltd Report

VerifiedAdded on 2020/02/18

|12

|3549

|51

Report

AI Summary

This report provides an in-depth analysis of the accounting policies and reporting strategies of Wesfarmers Ltd, an ASX-listed Australian retail giant. It examines the company's compliance with Australian Accounting Standards (AASB) and compares its accounting practices with those of competitors like Woolworths. The report identifies key accounting policies, assesses the flexibility within the accounting framework, and evaluates the quality of financial disclosures. It explores the accounting strategies employed by Wesfarmers, including the use of fair value accounting and hedge accounting, and identifies potential red flags in the financial reports. The analysis covers areas such as asset valuation, depreciation, and the structure of financial statements, providing insights into how Wesfarmers manages its financial reporting to meet stakeholder needs and comply with accounting standards. The report highlights differences in accounting methods between Wesfarmers and its competitors and discusses the impact of accounting choices on the company's financial performance and strategic objectives.

Accounting theory and current issues

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The present report has been prepared for evaluating and analyzing the managers’

accounting strategy and reporting strategy choices of an ASX listed firm for ensuring their

compliance with the internationally accepted accounting rules and standards. The firm selected

for the purpose is Wesfarmers Ltd, a retail giant of Australia. As such, the report has

demonstrated the significance of adopting standard accounting policies for developing quality

financial reports and meeting the needs of end-users.

The present report has been prepared for evaluating and analyzing the managers’

accounting strategy and reporting strategy choices of an ASX listed firm for ensuring their

compliance with the internationally accepted accounting rules and standards. The firm selected

for the purpose is Wesfarmers Ltd, a retail giant of Australia. As such, the report has

demonstrated the significance of adopting standard accounting policies for developing quality

financial reports and meeting the needs of end-users.

Introduction

The accounting department is a critical part of a business organization that is involved in

controlling and monitoring of its monetary resources. The accounting professionals of a business

entity need to prepare their financial statements as per the accounting policies and procedures

developed by the IASB (International Accounting Standards Board). These accounting policies

are major principles, rules and procedures that need to be followed by the management of a

business entity for developing and presenting its financial statements. The adoption of the IASB

developed accounting policies and procedures are essential for a business entity for meeting the

different needs and demands of its various stakeholders. The accounting policies and procedures

are developed on the basis of various accounting theories such as positive and normative

accounting theories (Henderson et al., 2015). In this context, the present report aims to analyze

and examine the importance of the accounting policies and procedures in a business entity

through selecting an ASX listed firm, that is, Wesfarmers Ltd. The report evaluates the

accounting policies used by a firm and analyze it with the accounting procedures used by its

competitor. In addition to this, the report evaluates the quality of accounting policies of the firm

by considering the impact of political pressures on standard-setting of accounting bodies.

Assessing accounting policies and estimates of Wesfarmers Ltd

Section 1: Identify Key Accounting Policies

Wesfarmers Limited is a recognized Australian company that along with its subsidiaries

is involved in retailing of chemicals, fertilizers, coal mining, industrial and safety products. The

Group composition consists of subsidiaries, joint ventures and associates. As per the annual

report of the company, it has effectively adopted and complied with the accounting policies of

AASB (Australian Accounting Standards) and the Corporations Act 2001. The Group has

mentioned the basics accounting policies adopted for developing its consolidated financial

statements as per the AASB standards. The Group has adopted the accounting policies such as

principles of consolidation, recognition and measurement policies for fixed assets on cost basis,

implementing accounting estimates and judgments as per the GAAP principles. The Group has

also disclosed proper policies in relation to risk management programs for minimizing the

occurrence of risk hazards. The Board has complied with all the necessary environmental

The accounting department is a critical part of a business organization that is involved in

controlling and monitoring of its monetary resources. The accounting professionals of a business

entity need to prepare their financial statements as per the accounting policies and procedures

developed by the IASB (International Accounting Standards Board). These accounting policies

are major principles, rules and procedures that need to be followed by the management of a

business entity for developing and presenting its financial statements. The adoption of the IASB

developed accounting policies and procedures are essential for a business entity for meeting the

different needs and demands of its various stakeholders. The accounting policies and procedures

are developed on the basis of various accounting theories such as positive and normative

accounting theories (Henderson et al., 2015). In this context, the present report aims to analyze

and examine the importance of the accounting policies and procedures in a business entity

through selecting an ASX listed firm, that is, Wesfarmers Ltd. The report evaluates the

accounting policies used by a firm and analyze it with the accounting procedures used by its

competitor. In addition to this, the report evaluates the quality of accounting policies of the firm

by considering the impact of political pressures on standard-setting of accounting bodies.

Assessing accounting policies and estimates of Wesfarmers Ltd

Section 1: Identify Key Accounting Policies

Wesfarmers Limited is a recognized Australian company that along with its subsidiaries

is involved in retailing of chemicals, fertilizers, coal mining, industrial and safety products. The

Group composition consists of subsidiaries, joint ventures and associates. As per the annual

report of the company, it has effectively adopted and complied with the accounting policies of

AASB (Australian Accounting Standards) and the Corporations Act 2001. The Group has

mentioned the basics accounting policies adopted for developing its consolidated financial

statements as per the AASB standards. The Group has adopted the accounting policies such as

principles of consolidation, recognition and measurement policies for fixed assets on cost basis,

implementing accounting estimates and judgments as per the GAAP principles. The Group has

also disclosed proper policies in relation to risk management programs for minimizing the

occurrence of risk hazards. The Board has complied with all the necessary environmental

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

policies and legislations through developing a risk management program that has maintained

adequate provisions for meeting the associated costs due to violation of any Australian or

international environmental regulations. The auditor’s report has also advocated that the Group

has implemented a code of professional conduct that guides its overall business process and

procedures. The Group has also provided all the relevant information in relation to its future

compliance with new accounting standards such as IFRS 15 and AASB 15 (Wesfarmers: Annual

Report, 2016).

Section 2: Assess Accounting Flexibility

The accounting policies provide a framework to a business entity for developing its

financial accounts such a deprecation, goodwill recognition, inventory valuation and

consolidation of financial accounts (Sheridan, 2016). However, the business entities possess the

authority to select the accounting methods that proves beneficial for improving their profitability

and growth. However, the business entities need to conform to the Generally Accepted

Accounting Principles (GAAP) and IFRS while the adoption of specific accounting policies

during financial reporting. The Wesfarmers Ltd has implemented some flexibility in selection of

its accounting framework policies for maintaining its accounts such as deprecation, inventory,

goodwill and assets. The management of the Group has exercised some discretion in selection of

the accounting policies for valuing its assets, liabilities, leases and goodwill as per the fair value

accounting model. However, the board has adopted strict policies and procedure for monitoring

and controlling the managers operations so that they don’t take undue advantage of their

freedom. The management of the group through has the authority to select the accounting

policies as per the nature of business operations but the board ensures that the policies adopted

are in compliance with the AASB standards and Corporations Act (Wesfarmers: Annual Report,

2016).

Section 3: Accounting policies and estimates used by their competitors and comparison of

accounting policies and estimates used by the firm with one of its rival company

The major competitors of Wesfarmers Limited is Woolworths, Billabong, Coles can be

regarded to be a major rivals of the Group. The Group is recognized a global leader in retail

industry of Australia with its main competitor of Woolworths Limited. The Woolworths Limited

adequate provisions for meeting the associated costs due to violation of any Australian or

international environmental regulations. The auditor’s report has also advocated that the Group

has implemented a code of professional conduct that guides its overall business process and

procedures. The Group has also provided all the relevant information in relation to its future

compliance with new accounting standards such as IFRS 15 and AASB 15 (Wesfarmers: Annual

Report, 2016).

Section 2: Assess Accounting Flexibility

The accounting policies provide a framework to a business entity for developing its

financial accounts such a deprecation, goodwill recognition, inventory valuation and

consolidation of financial accounts (Sheridan, 2016). However, the business entities possess the

authority to select the accounting methods that proves beneficial for improving their profitability

and growth. However, the business entities need to conform to the Generally Accepted

Accounting Principles (GAAP) and IFRS while the adoption of specific accounting policies

during financial reporting. The Wesfarmers Ltd has implemented some flexibility in selection of

its accounting framework policies for maintaining its accounts such as deprecation, inventory,

goodwill and assets. The management of the Group has exercised some discretion in selection of

the accounting policies for valuing its assets, liabilities, leases and goodwill as per the fair value

accounting model. However, the board has adopted strict policies and procedure for monitoring

and controlling the managers operations so that they don’t take undue advantage of their

freedom. The management of the group through has the authority to select the accounting

policies as per the nature of business operations but the board ensures that the policies adopted

are in compliance with the AASB standards and Corporations Act (Wesfarmers: Annual Report,

2016).

Section 3: Accounting policies and estimates used by their competitors and comparison of

accounting policies and estimates used by the firm with one of its rival company

The major competitors of Wesfarmers Limited is Woolworths, Billabong, Coles can be

regarded to be a major rivals of the Group. The Group is recognized a global leader in retail

industry of Australia with its main competitor of Woolworths Limited. The Woolworths Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is also a retail giant in Australia with its main operations in supermarket, liquor retailing, hotels

and pubs and discount department stores. The analysis of the annual report of both Wesfarmers

and Woolworths reveals that they have adopted and implemented accounting policies and

estimates in accordance with the AASB standards. However, there exist some significant

differences between the accounting policies and estimated of Woolworths and Wesfarmers as

evident from their notes to the financial statements section. The net carrying value of assets and

liabilities are valued at their fair value and incorporates the use of hedge accounting for hedging

the risks (Wesfarmers: Annual Report, 2016).

On the contrary, Woolworths does not implement the use of hedge accounting for

recognizing any gain or loss in the consolidated financial statements. Also, the structure of

income statements prepared for both the groups has major differences. The income statement of

Wesfarmers have clearly defined the main elements such as income, expense and profit while in

case of Woolworths the structure of the statement is not very clear. The Wesfarmers have

recorded expenditure in their income statement on the basis of employee benefits and

considering the depreciation and amortization. On the other hand, Woolworths have recorded

expenses on the basis of administration expenses and not considered the depreciation and

amortization. However, both the firms have adopted the changed accounting policies and

estimates but the policies implemented are as per the AASB standards and thus are agreeable and

acceptable (Hussey and Ong, 2017).

Section 4: Accounting Strategy

The analysis of accounting policies and estimates of Wesfarmers with that of industry

peers such as Woolworths have indicated that there exists flexibility in the accounting

framework of business corporations. The business corporations select the accounting methods as

per their nature of operational activities as evident form the difference in accounting policies and

estimates adopted by Woolworths and Wesfarmers. However, there is only minor difference

between the accounting policies of Wesfarmers as compared to that of its peers such as

Woolworths as analyzed from their financial reporting system. Both the Groups have adopted

similar accounting methods in preparation of cash flow statement, statement of changes in equity

and also adopt the use of fair value accounting model in developing their balance sheet and

income statement. Thus, it can be said that Wesfarmers and its peer group select the accounting

and pubs and discount department stores. The analysis of the annual report of both Wesfarmers

and Woolworths reveals that they have adopted and implemented accounting policies and

estimates in accordance with the AASB standards. However, there exist some significant

differences between the accounting policies and estimated of Woolworths and Wesfarmers as

evident from their notes to the financial statements section. The net carrying value of assets and

liabilities are valued at their fair value and incorporates the use of hedge accounting for hedging

the risks (Wesfarmers: Annual Report, 2016).

On the contrary, Woolworths does not implement the use of hedge accounting for

recognizing any gain or loss in the consolidated financial statements. Also, the structure of

income statements prepared for both the groups has major differences. The income statement of

Wesfarmers have clearly defined the main elements such as income, expense and profit while in

case of Woolworths the structure of the statement is not very clear. The Wesfarmers have

recorded expenditure in their income statement on the basis of employee benefits and

considering the depreciation and amortization. On the other hand, Woolworths have recorded

expenses on the basis of administration expenses and not considered the depreciation and

amortization. However, both the firms have adopted the changed accounting policies and

estimates but the policies implemented are as per the AASB standards and thus are agreeable and

acceptable (Hussey and Ong, 2017).

Section 4: Accounting Strategy

The analysis of accounting policies and estimates of Wesfarmers with that of industry

peers such as Woolworths have indicated that there exists flexibility in the accounting

framework of business corporations. The business corporations select the accounting methods as

per their nature of operational activities as evident form the difference in accounting policies and

estimates adopted by Woolworths and Wesfarmers. However, there is only minor difference

between the accounting policies of Wesfarmers as compared to that of its peers such as

Woolworths as analyzed from their financial reporting system. Both the Groups have adopted

similar accounting methods in preparation of cash flow statement, statement of changes in equity

and also adopt the use of fair value accounting model in developing their balance sheet and

income statement. Thus, it can be said that Wesfarmers and its peer group select the accounting

policies as per their business operations but follow the standard accounting norms directed by

AASB. The change in the accounting policies in respect to that of industry norms is explained

adequately in the annual report of the Group (Wesfarmers: Annual Report, 2016).

As analyzed from the financial report of Wesfarmers Limited, the change in the structure

of the accounting transactions is as per the accounting objectives of the group. The Wesfarmers

is placing emphasis on enhancing the cash flow by selling its assets while Woolworths is

increase its cash flow by enhancing its asset base. Thus, Wesfarmers are incorporating the use of

hedge accounting and fair value model for increasing the revenue by selling the asset base. The

flexibility in the accounting framework is implemented by the managing directors of the

Wesfarmers Limited for improving its profitability position. The Board has introduced short-

term and long-term incentives plan for the management depending on the firm’s financial

position. The incentives plan is developed to provide motivation to the management to

implement the accounting policies that help in increasing the financial performance of the Group

but by complying effectively with all the AASB accounting principles (Mirza and Ankarath,

2012). The Board ensures that flexibility in accounting choices provided to the managing

directors is in accordance with the standard accounting rules for restricting the occurrence of any

fraudulent activities (Wesfarmers: Annual Report, 2016).

Section 5: Evaluating the Quality of Disclosure

The Wesfarmers Limited have strictly implemented and adopted the standard accounting

policies and regulations for improving its quality of financial reporting. The Group have

disclosed effectively the AASB standards implemented for valuing its financial instruments and

also the future compliance with the new AASB standards. The notes to the financial statements

section of the annual report have provided all the necessary information about the accounting

policies and estimates used by the Group for developing its financial statement by explaining the

significance of each. The notes to the financial statements section have sufficiently explained the

financial performance of the firm and are in consistence with its current financial position. The

accounting policies depicted in the notes and that adopted for preparing the financial statements

are same without any differences. There is adequate disclosure in the notes section relating to

board composition, remuneration policies, risk management policies and policies adopted for

promoting the sustainable growth of the Group. Also, there is sufficient information relating to

AASB. The change in the accounting policies in respect to that of industry norms is explained

adequately in the annual report of the Group (Wesfarmers: Annual Report, 2016).

As analyzed from the financial report of Wesfarmers Limited, the change in the structure

of the accounting transactions is as per the accounting objectives of the group. The Wesfarmers

is placing emphasis on enhancing the cash flow by selling its assets while Woolworths is

increase its cash flow by enhancing its asset base. Thus, Wesfarmers are incorporating the use of

hedge accounting and fair value model for increasing the revenue by selling the asset base. The

flexibility in the accounting framework is implemented by the managing directors of the

Wesfarmers Limited for improving its profitability position. The Board has introduced short-

term and long-term incentives plan for the management depending on the firm’s financial

position. The incentives plan is developed to provide motivation to the management to

implement the accounting policies that help in increasing the financial performance of the Group

but by complying effectively with all the AASB accounting principles (Mirza and Ankarath,

2012). The Board ensures that flexibility in accounting choices provided to the managing

directors is in accordance with the standard accounting rules for restricting the occurrence of any

fraudulent activities (Wesfarmers: Annual Report, 2016).

Section 5: Evaluating the Quality of Disclosure

The Wesfarmers Limited have strictly implemented and adopted the standard accounting

policies and regulations for improving its quality of financial reporting. The Group have

disclosed effectively the AASB standards implemented for valuing its financial instruments and

also the future compliance with the new AASB standards. The notes to the financial statements

section of the annual report have provided all the necessary information about the accounting

policies and estimates used by the Group for developing its financial statement by explaining the

significance of each. The notes to the financial statements section have sufficiently explained the

financial performance of the firm and are in consistence with its current financial position. The

accounting policies depicted in the notes and that adopted for preparing the financial statements

are same without any differences. There is adequate disclosure in the notes section relating to

board composition, remuneration policies, risk management policies and policies adopted for

promoting the sustainable growth of the Group. Also, there is sufficient information relating to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the key judgments and estimates used by the Group relating to recognition and measurement of

income, inventories, PPE, goodwill and other accounting information (Wesfarmers: Annual

Report, 2016).

The GAAP principles has assisted the Group in reflecting its key measures of success

such as basis of consolidation, the accounting policy adopted for measuring the foreign currency

transactions, goodwill, impairment and other funding activities. These all activities are carried

out by the Group as per the AASB and IFRS standards advocated by the Generally Accepted

Accounting Principles (Mirza and Ankarath, 2012). The notes to the financial statements section

of the Group has also disclosed adequate information relating to the functions of its operating

segments. The Group has organized and managed separately its operating segments as per the

nature of products and services. Each segment if the Group represents a strategic business unit

that is involved in providing different products and services as per the external marketplace. The

financial performance of each of its operating segments is evaluated on the basis of operating

profit or loss while interest income and expenditure is not allocated to each of its operating

segments that is managed on group basis (Wesfarmers: Annual Report, 2016).

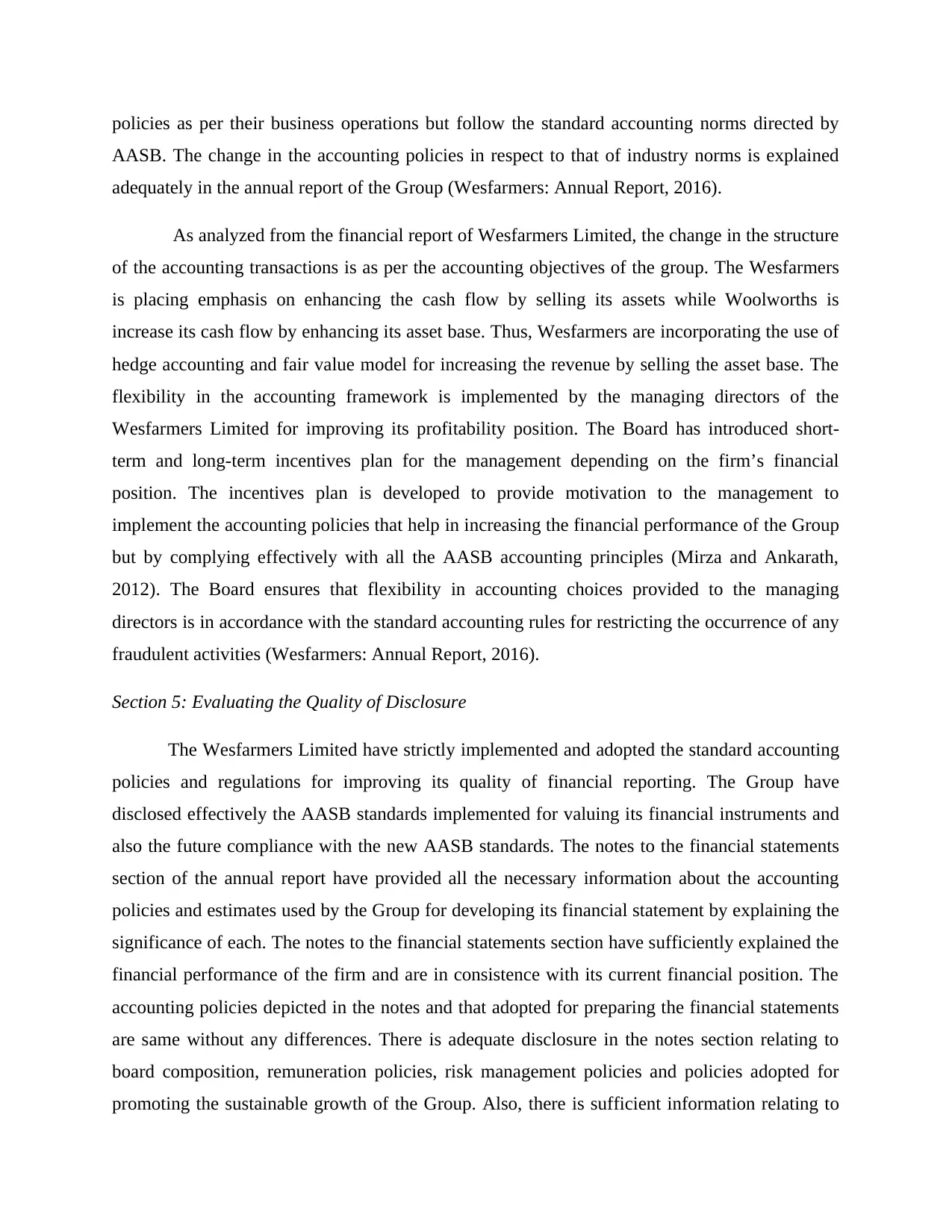

Section 6: Identifying Potential Red Flags

The annual reports of the Group over the last two years have indicated that it has strong

financial position in the year 2015 and 2016. The financial reporting of the Group has been done

as per the basis of historical cost except for some financial instruments that are measured at fair

value. This change in the accounting policies of the Group has not been adequately explained by

the Group in its financial reports. Thus, there is not appropriate explanation about the change in

the accounting adopted by the Group in different set of circumstances. The Group has

implemented different method of recording its accounting transactions related to its expenditure

in the income statement without its adequate disclosure as compared to the industry norms. The

expenses are classified on the basis of employee benefits, depreciation and amortization unlike

the normal categorization of administration, operating and interest expenses on the income

statement (Pietra, McLeay and Ronen, 2013). Thus, all these other expenses of the Group are not

able to quantify as per the normal expenditures listed across the income statements and thus it is

required to provide a proper explanation of such expenses in the notes to accounts section as

evident from the screenshot:

income, inventories, PPE, goodwill and other accounting information (Wesfarmers: Annual

Report, 2016).

The GAAP principles has assisted the Group in reflecting its key measures of success

such as basis of consolidation, the accounting policy adopted for measuring the foreign currency

transactions, goodwill, impairment and other funding activities. These all activities are carried

out by the Group as per the AASB and IFRS standards advocated by the Generally Accepted

Accounting Principles (Mirza and Ankarath, 2012). The notes to the financial statements section

of the Group has also disclosed adequate information relating to the functions of its operating

segments. The Group has organized and managed separately its operating segments as per the

nature of products and services. Each segment if the Group represents a strategic business unit

that is involved in providing different products and services as per the external marketplace. The

financial performance of each of its operating segments is evaluated on the basis of operating

profit or loss while interest income and expenditure is not allocated to each of its operating

segments that is managed on group basis (Wesfarmers: Annual Report, 2016).

Section 6: Identifying Potential Red Flags

The annual reports of the Group over the last two years have indicated that it has strong

financial position in the year 2015 and 2016. The financial reporting of the Group has been done

as per the basis of historical cost except for some financial instruments that are measured at fair

value. This change in the accounting policies of the Group has not been adequately explained by

the Group in its financial reports. Thus, there is not appropriate explanation about the change in

the accounting adopted by the Group in different set of circumstances. The Group has

implemented different method of recording its accounting transactions related to its expenditure

in the income statement without its adequate disclosure as compared to the industry norms. The

expenses are classified on the basis of employee benefits, depreciation and amortization unlike

the normal categorization of administration, operating and interest expenses on the income

statement (Pietra, McLeay and Ronen, 2013). Thus, all these other expenses of the Group are not

able to quantify as per the normal expenditures listed across the income statements and thus it is

required to provide a proper explanation of such expenses in the notes to accounts section as

evident from the screenshot:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is also evident from the financial reports of the Group that it has maintained a huge

inventory level and thus leading to decline in its liquidity position. The monetary fund’s of the

Group has been tied up in the accounts receivable and thus resulting in increase in its accounts

receivables as comparison to the sales. Also, the Group is increasing its cash flows by selling its

assets that can result in enhancing the gap between net income and cash flows. This is due to

increase in the cash flows of the Group resulting in accounting profit higher than the taxable

income and thus creating a gap between net income and taxable income. However, the annual

report of the Group does not indicate any presence of R& D partnerships for financing its

operations but the group is utilizing the cash received from sale of its assets for carrying its

business operations. The Group has also recorded a decrease in its operating cash flow of about

11% as compared to that in the year 2015. This can be regarded as a point of major concern for

the Group as it needs to increase its investment in acquiring assets for maintaining its cash

inflows. However, there is no evidence of fourth-quarter adjustments or related-party

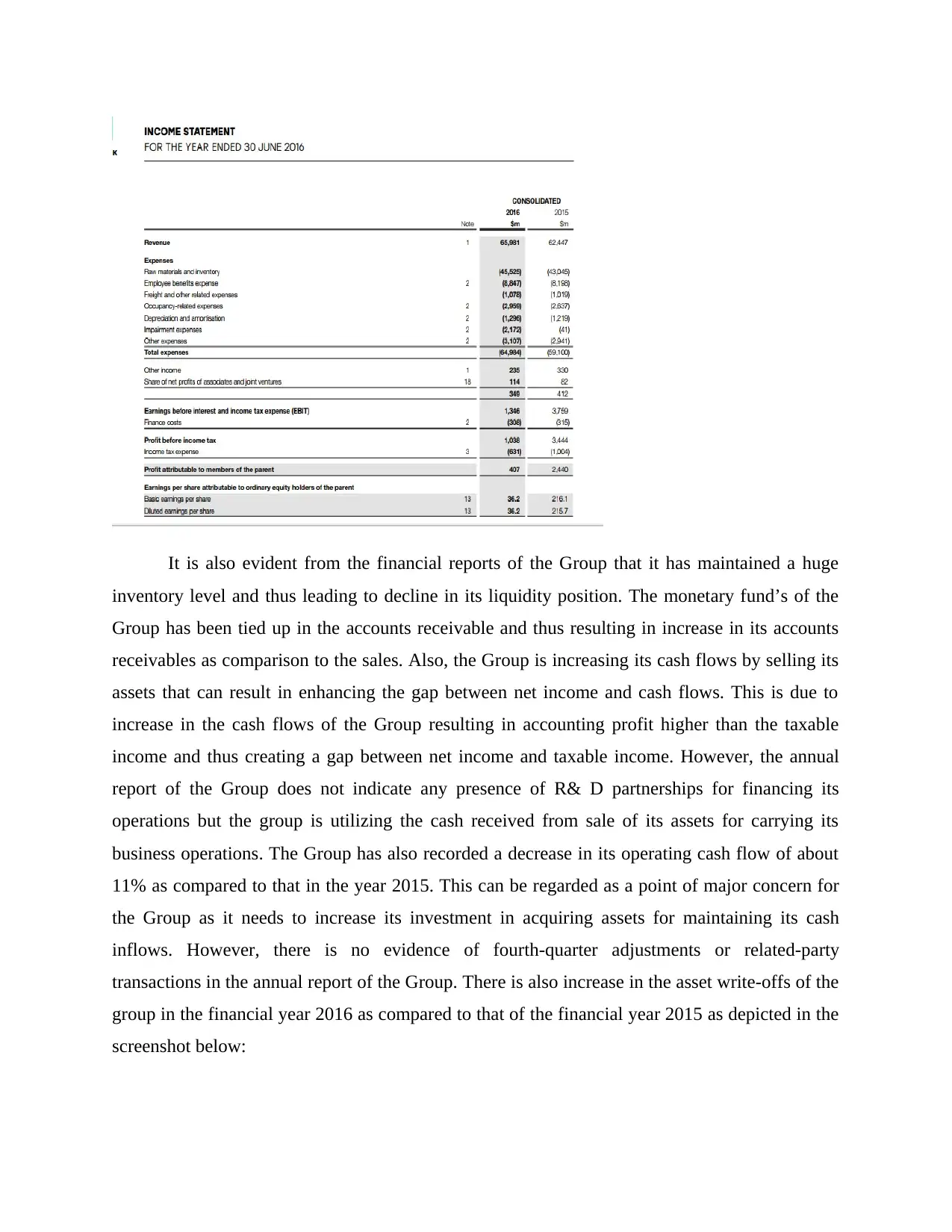

transactions in the annual report of the Group. There is also increase in the asset write-offs of the

group in the financial year 2016 as compared to that of the financial year 2015 as depicted in the

screenshot below:

inventory level and thus leading to decline in its liquidity position. The monetary fund’s of the

Group has been tied up in the accounts receivable and thus resulting in increase in its accounts

receivables as comparison to the sales. Also, the Group is increasing its cash flows by selling its

assets that can result in enhancing the gap between net income and cash flows. This is due to

increase in the cash flows of the Group resulting in accounting profit higher than the taxable

income and thus creating a gap between net income and taxable income. However, the annual

report of the Group does not indicate any presence of R& D partnerships for financing its

operations but the group is utilizing the cash received from sale of its assets for carrying its

business operations. The Group has also recorded a decrease in its operating cash flow of about

11% as compared to that in the year 2015. This can be regarded as a point of major concern for

the Group as it needs to increase its investment in acquiring assets for maintaining its cash

inflows. However, there is no evidence of fourth-quarter adjustments or related-party

transactions in the annual report of the Group. There is also increase in the asset write-offs of the

group in the financial year 2016 as compared to that of the financial year 2015 as depicted in the

screenshot below:

Section 6: Compliant with the Conceptual Framework

The financial reports of Wesfarmers have been prepared by the management in strict

compliance with the AASB and IFRS standards as directed by the accounting standard-setting

bodies. The Australian Securities and Investment Commission (ASIC) have directed the

corporations listed on ASX to carry out their operational activities as per the AASB accounting

rules and conventions. The IFRS have been developed by the IASB (International Accounting

Standards Bodies) for promoting harmonization between the financial reporting standards of

corporations across the world (Wolk, Dodd and Rozycki, 2012). As such, the Wesfarmers is

complying with both the accounting standards as indicated from its financial reports. The notes

to the financial statements section of the group has effectively disclosed all the accounting

policies adopted in preparation of its consolidated statements as per the mandates of AASB and

IASB. The proper accounting disclosures have been mandated by the accounting standard-setting

bodies for improving the transparency in business operations and protecting the interests of all its

overall stakeholders. As such, business corporations listed on ASX in Australia are bound to

follow the principle of conceptual accounting framework in development of their financial

The financial reports of Wesfarmers have been prepared by the management in strict

compliance with the AASB and IFRS standards as directed by the accounting standard-setting

bodies. The Australian Securities and Investment Commission (ASIC) have directed the

corporations listed on ASX to carry out their operational activities as per the AASB accounting

rules and conventions. The IFRS have been developed by the IASB (International Accounting

Standards Bodies) for promoting harmonization between the financial reporting standards of

corporations across the world (Wolk, Dodd and Rozycki, 2012). As such, the Wesfarmers is

complying with both the accounting standards as indicated from its financial reports. The notes

to the financial statements section of the group has effectively disclosed all the accounting

policies adopted in preparation of its consolidated statements as per the mandates of AASB and

IASB. The proper accounting disclosures have been mandated by the accounting standard-setting

bodies for improving the transparency in business operations and protecting the interests of all its

overall stakeholders. As such, business corporations listed on ASX in Australia are bound to

follow the principle of conceptual accounting framework in development of their financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reports. The principles are relevance, reliability, comparability and completeness. These

principles are required to be integrated in the financial reporting system of business entities for

ensuring the development of quality financial reports that effectively meet the needs of all the

end-users (Wesfarmers: Annual Report, 2016).

The group has also adopted some flexibility in its accounting framework as per the nature

of its business operations as discussed in the above sections of the report. These accounting

choices have been made by the group for improving its financial conditions as per its operational

activities. However, the Group has maintained its compliance with the standard accounting rules

while implementing particular accounting choices and disclosures. The difference in the

accounting choices of Wesfarmers and the business corporations in other parts of the world are

due to the impact of political factors in the external marketplace (Kenny, 2009). The difference

in the disclosure process of the corporations around the world is due to lack of development of a

comprehensive conceptual theory of accounting that can result in harmonization of accounting

standards. The accounting choices made by the business entities are significantly influenced by

the economic conditions present in the external market place. The government institutions,

professional associations, industry groups and also ASX influences the accounting choices and

estimates made by the corporations operating in Australia. The Wesfarmers have adopted fair

value rules and changed lease rules as per the economic conditions of the Australia. As such, the

changed accounting rules can help the group to get a favorable treatment by the auditors and thus

improve their financial performance (Knight, 2004).

The FASB and IASB have mandated the firms to adopt the accounting standards that help

them to produce economic favorable results. However, the lack of harmonization of accounting

policies is creating need for adopting different accounting choices by the firms across the world.

Thus, it can be said that accounting rules adopted by a business entity can provide an undue

advantage to one party as compared to the other due to the absence of a comprehensive

conceptual theory of accounting (Albrecht, 2010). However, ASX have prioritized the need of

investors over those of the companies and therefore it is required on the part of Australian

companies to adopt the accounting standards that are in accordance with the conceptual

accounting framework. This is essential to provide maximum value to the stakeholders including

investors and creditors by providing them all the necessary and realistic financial information. As

principles are required to be integrated in the financial reporting system of business entities for

ensuring the development of quality financial reports that effectively meet the needs of all the

end-users (Wesfarmers: Annual Report, 2016).

The group has also adopted some flexibility in its accounting framework as per the nature

of its business operations as discussed in the above sections of the report. These accounting

choices have been made by the group for improving its financial conditions as per its operational

activities. However, the Group has maintained its compliance with the standard accounting rules

while implementing particular accounting choices and disclosures. The difference in the

accounting choices of Wesfarmers and the business corporations in other parts of the world are

due to the impact of political factors in the external marketplace (Kenny, 2009). The difference

in the disclosure process of the corporations around the world is due to lack of development of a

comprehensive conceptual theory of accounting that can result in harmonization of accounting

standards. The accounting choices made by the business entities are significantly influenced by

the economic conditions present in the external market place. The government institutions,

professional associations, industry groups and also ASX influences the accounting choices and

estimates made by the corporations operating in Australia. The Wesfarmers have adopted fair

value rules and changed lease rules as per the economic conditions of the Australia. As such, the

changed accounting rules can help the group to get a favorable treatment by the auditors and thus

improve their financial performance (Knight, 2004).

The FASB and IASB have mandated the firms to adopt the accounting standards that help

them to produce economic favorable results. However, the lack of harmonization of accounting

policies is creating need for adopting different accounting choices by the firms across the world.

Thus, it can be said that accounting rules adopted by a business entity can provide an undue

advantage to one party as compared to the other due to the absence of a comprehensive

conceptual theory of accounting (Albrecht, 2010). However, ASX have prioritized the need of

investors over those of the companies and therefore it is required on the part of Australian

companies to adopt the accounting standards that are in accordance with the conceptual

accounting framework. This is essential to provide maximum value to the stakeholders including

investors and creditors by providing them all the necessary and realistic financial information. As

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

such, it can be stated that Wesfarmers have complied with all the principles of conceptual

accounting framework by providing all the necessary financial information in its annul

disclosures (Mirza and Ankarath, 2012).

Conclusion

It can be inferred from the overall discussion held in the report that Wesfarmers has

implemented accounting and financial reporting strategies as per the international accounting

standards and policies. The difference in the accounting policies and estimated used by the

Group are due to the impact of political pressure present in the external marketplace where it

operates.

accounting framework by providing all the necessary financial information in its annul

disclosures (Mirza and Ankarath, 2012).

Conclusion

It can be inferred from the overall discussion held in the report that Wesfarmers has

implemented accounting and financial reporting strategies as per the international accounting

standards and policies. The difference in the accounting policies and estimated used by the

Group are due to the impact of political pressure present in the external marketplace where it

operates.

References

Albrecht, D. 2010. Economic Consequences and the Political Nature of Accounting Standard

Setting. [Online]. Available at: https://profalbrecht.wordpress.com/2010/01/06/economic-

consequences-and-the-political-nature-of-accounting-standard-setting/ [Accessed on: 13

September, 2017].

Henderson, S. et al. 2015. Issues in Financial Accounting. Pearson Higher Education AU.

Hoffman, C.W. 2016. Revising the Conceptual Framework of the International Standards: IASB

Proposals Met with Support and Skepticism. World Journal of Business and Management 2 (1),

pp. 1-32.

Hussey, R. and Ong, A. 2017. Corporate Financial Reporting. Springer.

Kenny, G. 2009. Diversification Strategy: How to Grow a Business by Diversifying Successfully.

Kogan Page Publishers.

Knight, J. 2004. Internationalization Remodeled: Definition, Approaches, and Rationales.

Journal of Studies in International Education 8 (5), pp. 5-29.

Mirza, A. and Ankarath, N. 2012. Wiley International Trends in Financial Reporting under

IFRS: Including Comparisons with US GAAP, China GAAP, and India Accounting Standards.

John Wiley & Sons.

Pietra, R., McLeay, S and Ronen, J. 2013. Accounting and Regulation: New Insights on

Governance, Markets and Institutions. Springer Science & Business Media.

Sheridan, T. 2016. Managerial Fraud: Executive Impression Management, Beyond Red Flags.

Routledge.

Wesfarmers: Annual Report. 2015. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/2015-annual-report.pdf?sfvrsn=4

[Accessed on: 13 September, 2017].

Wesfarmers: Annual Report. 2016. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/2016-annual-report.pdf?sfvrsn=4

[Accessed on: 13 September, 2017].

Wolk, H., Dodd, J. and Rozycki. J. 2012. Accounting Theory: Conceptual Issues in a Political

and Economic Environment. SAGE.

Albrecht, D. 2010. Economic Consequences and the Political Nature of Accounting Standard

Setting. [Online]. Available at: https://profalbrecht.wordpress.com/2010/01/06/economic-

consequences-and-the-political-nature-of-accounting-standard-setting/ [Accessed on: 13

September, 2017].

Henderson, S. et al. 2015. Issues in Financial Accounting. Pearson Higher Education AU.

Hoffman, C.W. 2016. Revising the Conceptual Framework of the International Standards: IASB

Proposals Met with Support and Skepticism. World Journal of Business and Management 2 (1),

pp. 1-32.

Hussey, R. and Ong, A. 2017. Corporate Financial Reporting. Springer.

Kenny, G. 2009. Diversification Strategy: How to Grow a Business by Diversifying Successfully.

Kogan Page Publishers.

Knight, J. 2004. Internationalization Remodeled: Definition, Approaches, and Rationales.

Journal of Studies in International Education 8 (5), pp. 5-29.

Mirza, A. and Ankarath, N. 2012. Wiley International Trends in Financial Reporting under

IFRS: Including Comparisons with US GAAP, China GAAP, and India Accounting Standards.

John Wiley & Sons.

Pietra, R., McLeay, S and Ronen, J. 2013. Accounting and Regulation: New Insights on

Governance, Markets and Institutions. Springer Science & Business Media.

Sheridan, T. 2016. Managerial Fraud: Executive Impression Management, Beyond Red Flags.

Routledge.

Wesfarmers: Annual Report. 2015. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/2015-annual-report.pdf?sfvrsn=4

[Accessed on: 13 September, 2017].

Wesfarmers: Annual Report. 2016. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/2016-annual-report.pdf?sfvrsn=4

[Accessed on: 13 September, 2017].

Wolk, H., Dodd, J. and Rozycki. J. 2012. Accounting Theory: Conceptual Issues in a Political

and Economic Environment. SAGE.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.