Financial Analysis Report: Wesfarmers Financial Statements 2017

VerifiedAdded on 2020/05/16

|10

|1475

|37

Report

AI Summary

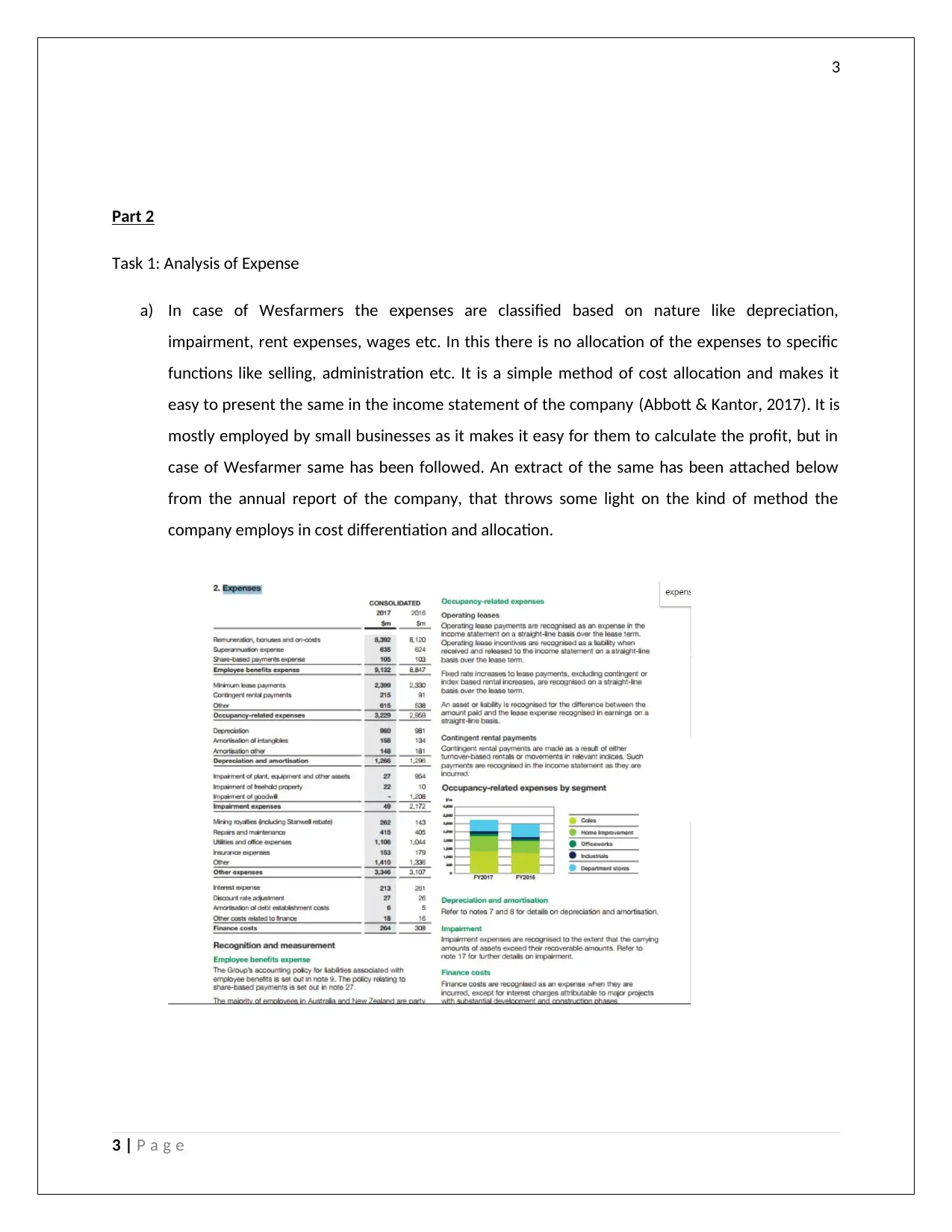

This report provides a financial analysis of Wesfarmers, examining its expense classification methods, which are based on the nature of expenses rather than functional allocation. It delves into the company's accounting policies, particularly focusing on AASB 108/IAS 8, including valuation methods for goodwill, intangible assets, and provisions, along with revenue recognition practices related to loyalty programs. The report also analyzes the notes to the 2016 financial statements, detailing depreciation and impairment methods for assets, including the use of the straight-line method for depreciation and impairment testing procedures. Key management assumptions and the treatment of asset derecognition are also discussed, providing a comprehensive overview of Wesfarmers' financial reporting practices.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.