Comprehensive Financial Analysis Report: Wesfarmers Limited

VerifiedAdded on 2021/02/20

|9

|2102

|29

Report

AI Summary

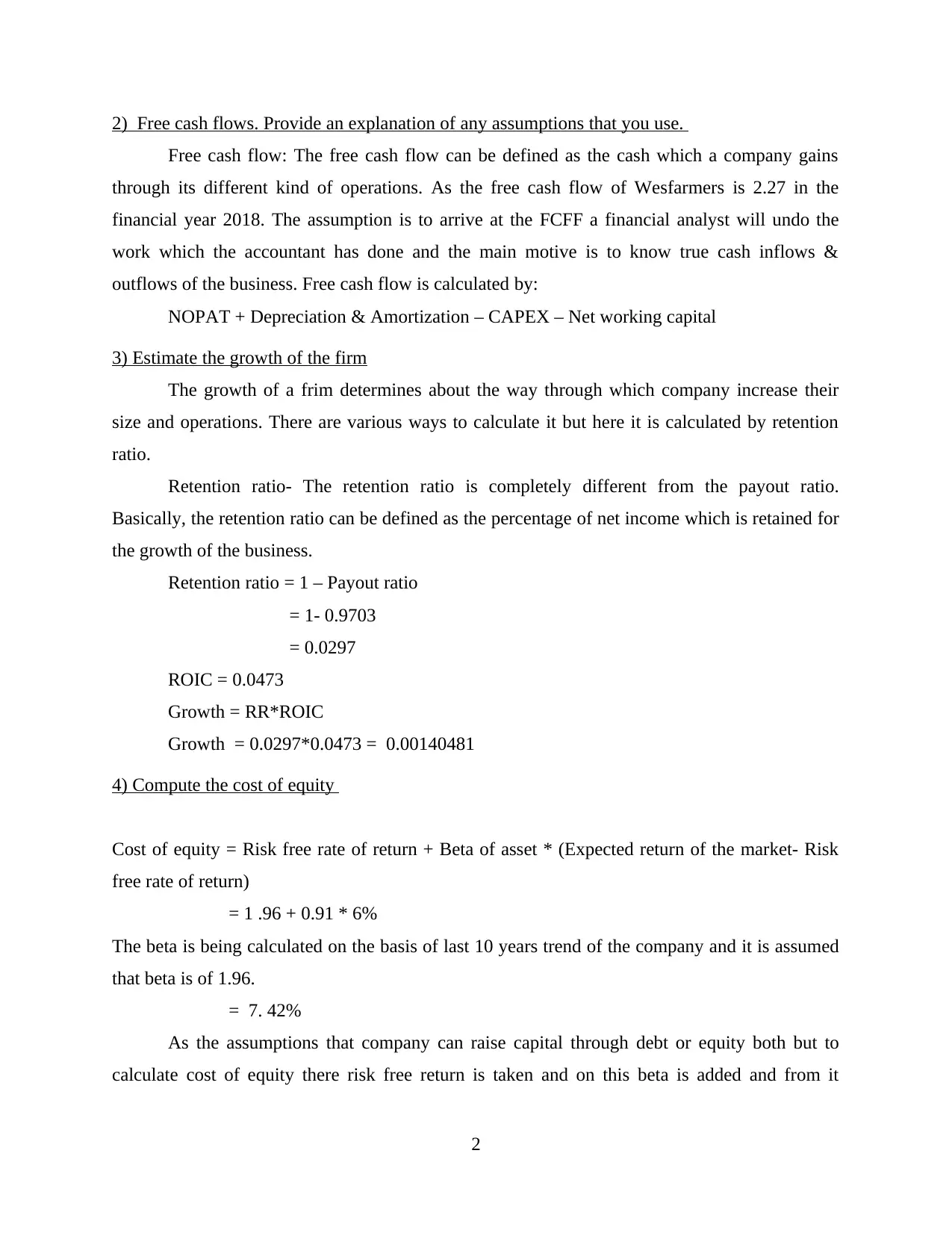

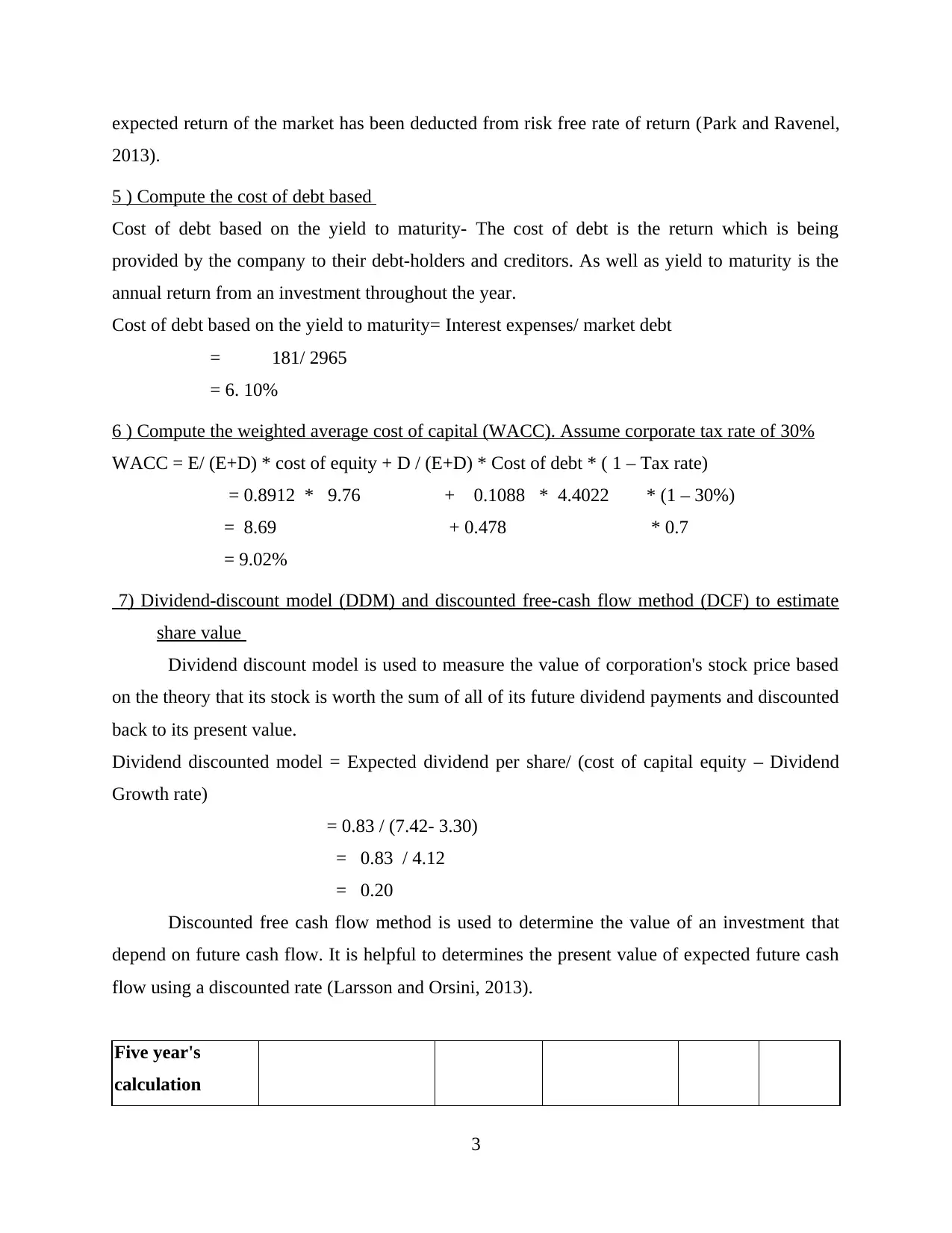

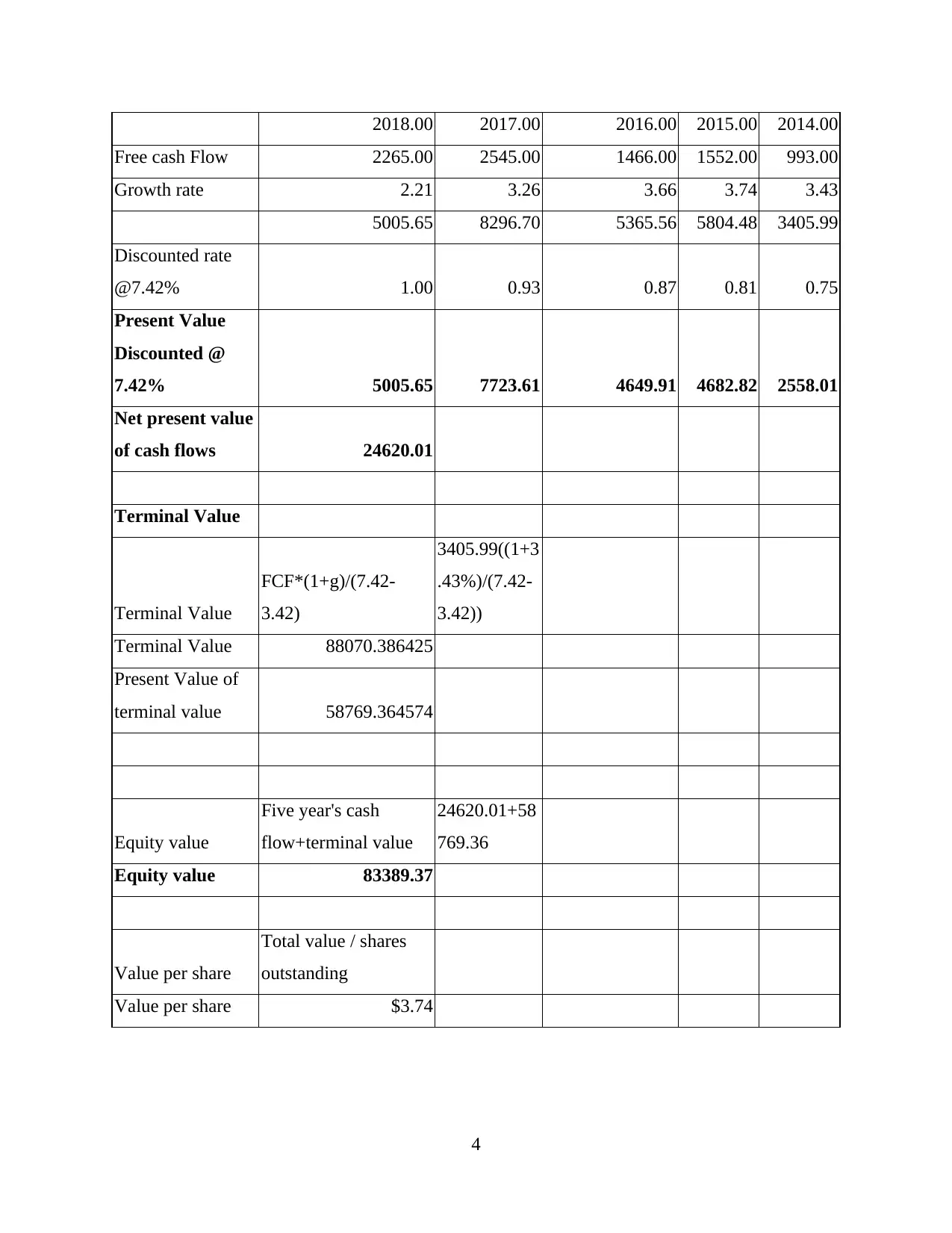

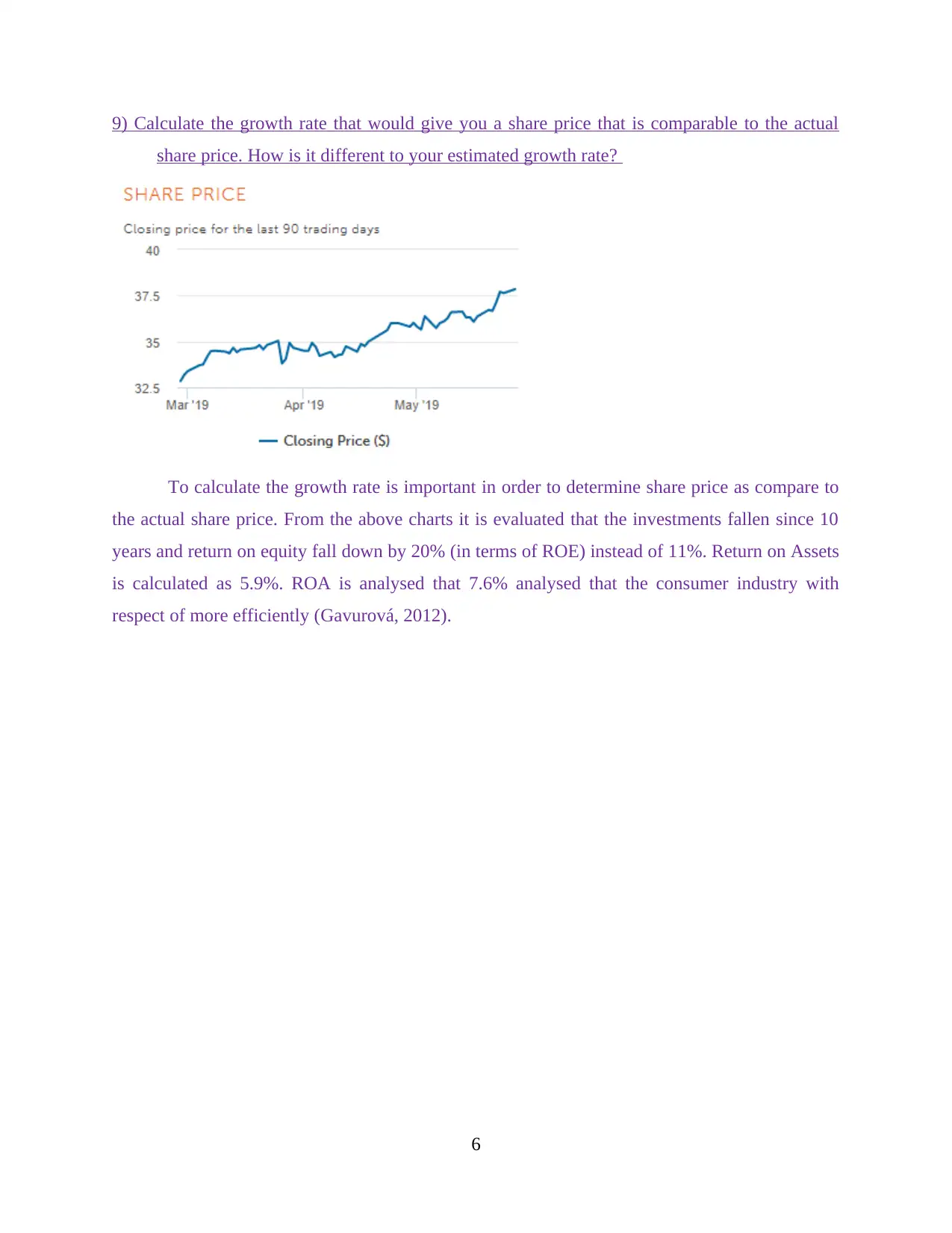

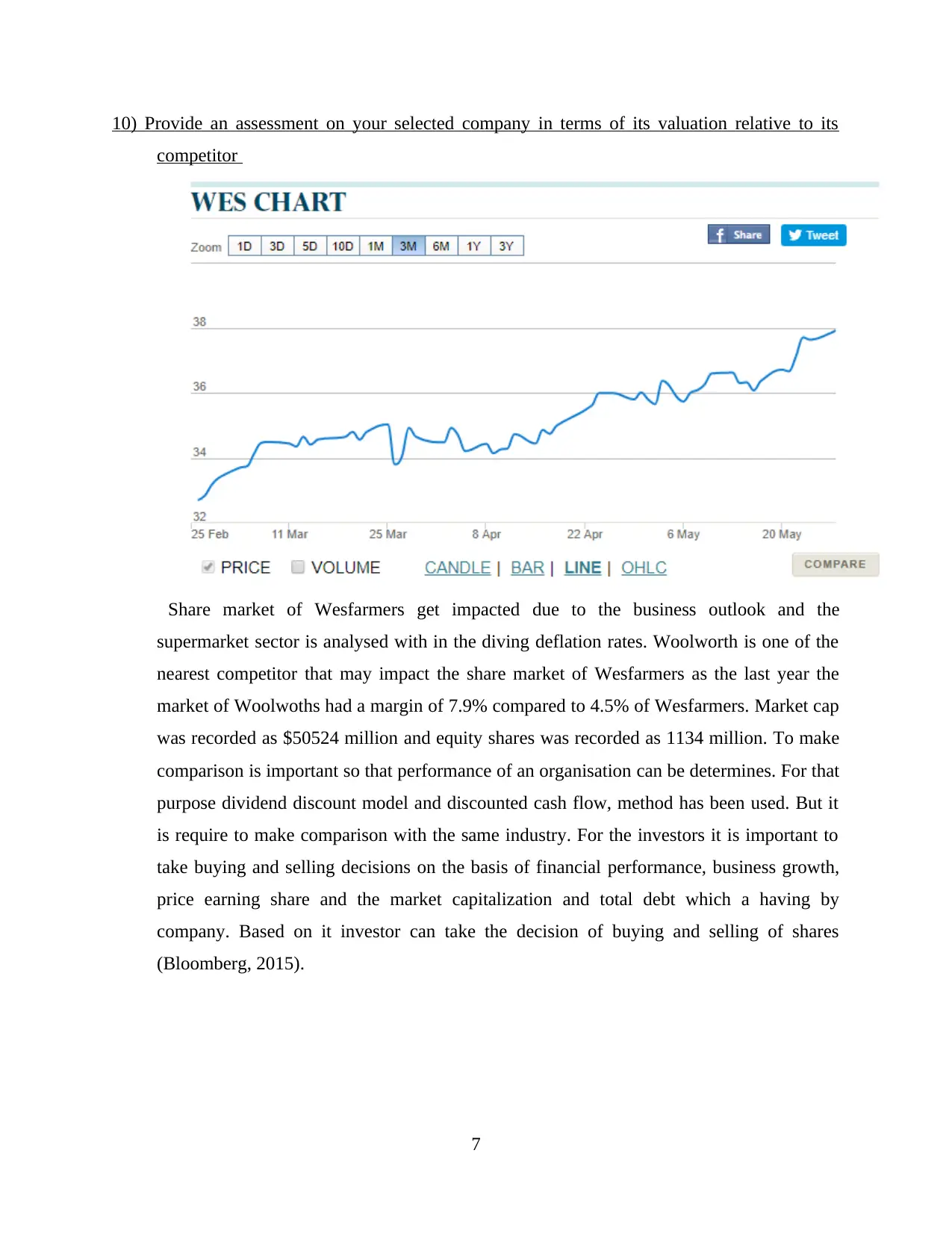

This report provides a comprehensive financial analysis of Wesfarmers Limited, an Australian-based company involved in chemicals, coal mining, and safety products. The analysis includes the calculation of free cash flow, cost of equity using the Capital Asset Pricing Model (CAPM), cost of debt based on yield to maturity, and the weighted average cost of capital (WACC). The report further explores the dividend discount model (DDM) and the discounted free cash flow (DCF) method to estimate share value, along with the growth rate calculation. Comparisons are made between DDM and DCF valuations, along with the current market value, and an assessment of the company's valuation relative to its competitor, Woolworths. The report also examines the company's business operations, growth, and financial performance, supported by relevant financial data and industry comparisons. The report also includes an analysis of the growth rate that would give a share price comparable to the actual share price.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.