Environmental Sustainability Analysis: Wesfarmers Reports (2016-2018)

VerifiedAdded on 2022/12/09

|18

|3586

|233

Report

AI Summary

This report provides an in-depth analysis of Wesfarmers' sustainability reports from 2016 to 2018, examining the company's efforts in environmental sustainability. The study begins with a research question addressing corporate awareness of climate change and resource usage, followed by a comprehensive literature review of relevant journal articles focusing on climate change accounting, financial performance impacts, carbon business accounting, and the challenges of climate change to accounting. The methodology involves analyzing Wesfarmers' sustainability reports, focusing on climate change resilience, water usage, and waste management, with data presented graphically and in tables. Findings reveal Wesfarmers' commitment to reducing GHG emissions, carbon accounting practices, and risk management strategies. The discussion interprets these findings in light of the literature and stakeholder theory, concluding with an assessment of the company's progress and its impact on society. The report emphasizes the role of accounting in measuring and driving corporate environmental responsibility, offering insights for stakeholders and future research.

Theoretical Foundations of Accounting

1 | P a g e

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

Purpose- The purpose of this study is to find out corporate effort towards environmental

sustainability with accounting as its scale of measurement; as a part of CSR program with the

example of Wesfarmers, an Australian ASX listed company.

Design/ Methodology- The methodology of this study is initiated with identification of research

question followed by literature review of journals and consideration of corporate data on the

subject to analyze their report for last three years.

Findings- The objective of this study is to find out the efforts and approaches of Wesfarmers

towards sustainability of environment for the stakeholders. Three years reports are analyzed to

identify the areas of progress in the aspects of environmental sustainability effort by the

company by accounting parameter set by regulatory bodies.

Discussion- The findings of the study are discussed as per the report and data of the company

related to sustainability effort towards environment with perspective of literature review.

Key Words - Wesfarmers, Sustainability Report, Water and waste usage, Climate Change

Resilience, CO2 emission.

2 | P a g e

Purpose- The purpose of this study is to find out corporate effort towards environmental

sustainability with accounting as its scale of measurement; as a part of CSR program with the

example of Wesfarmers, an Australian ASX listed company.

Design/ Methodology- The methodology of this study is initiated with identification of research

question followed by literature review of journals and consideration of corporate data on the

subject to analyze their report for last three years.

Findings- The objective of this study is to find out the efforts and approaches of Wesfarmers

towards sustainability of environment for the stakeholders. Three years reports are analyzed to

identify the areas of progress in the aspects of environmental sustainability effort by the

company by accounting parameter set by regulatory bodies.

Discussion- The findings of the study are discussed as per the report and data of the company

related to sustainability effort towards environment with perspective of literature review.

Key Words - Wesfarmers, Sustainability Report, Water and waste usage, Climate Change

Resilience, CO2 emission.

2 | P a g e

Table of Contents

Introduction.................................................................................................................................................4

Research Question.......................................................................................................................................4

Literature Review........................................................................................................................................5

Literature Review 1.................................................................................................................................5

Literature Review 2.................................................................................................................................6

Literature Review 3.................................................................................................................................7

Literature Review 4.................................................................................................................................8

Methods......................................................................................................................................................8

Findings.......................................................................................................................................................9

Climate Change........................................................................................................................................9

Water Usage and Waste Management..................................................................................................11

Discussion..................................................................................................................................................13

Conclusion.................................................................................................................................................14

References:................................................................................................................................................16

3 | P a g e

Introduction.................................................................................................................................................4

Research Question.......................................................................................................................................4

Literature Review........................................................................................................................................5

Literature Review 1.................................................................................................................................5

Literature Review 2.................................................................................................................................6

Literature Review 3.................................................................................................................................7

Literature Review 4.................................................................................................................................8

Methods......................................................................................................................................................8

Findings.......................................................................................................................................................9

Climate Change........................................................................................................................................9

Water Usage and Waste Management..................................................................................................11

Discussion..................................................................................................................................................13

Conclusion.................................................................................................................................................14

References:................................................................................................................................................16

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This research paper will emphasize on the implication of Corporate Social Responsibility

Program of the corporate in perspective of environment sustainability action and its relevance

from accounting viewpoint. The research will evolve with the case study of an ASX listed

corporate named Wesfarmers. For this purpose of research, the Sustainability report of

Wesfarmers is considered for the last three financial years ranging from 2016 to 2018.

Sustainability report of Wesfarmers emphasizes on different aspects of corporate operation for its

stakeholders including environment with specific focus on issues like climate change resilience

and waste and water use. These reports will be analyzed in perspective of literature review on the

subject emphasizing on the issues of environment restoration for greener future world from

accounting perspective. The sustainability reports of the company highlight the domains of Key

Result Area to ensure environmental sustainability by Wesfarmers for the community as a part of

its CSR program. This article needs to generate a research question related to the subject.

Through literature review on the subject and the respective corporate disclosure about

environment sustainability, specific research question is set related to the corporate effort to

ensure environmental sustainability with specific focus on reduction of green gas emission

through the effort initiated by the company for their stakeholders. The findings of research are to

be valued by one theory known as Stakeholder theory. At the end, conclusion is to be drawn to

point out the objective of environmental sustainability effort by the company with its success to

facilitate the society and human kind, at large.

Research Question

Are the corporate bodies aware of climate change and use of natural resources for the society?

4 | P a g e

This research paper will emphasize on the implication of Corporate Social Responsibility

Program of the corporate in perspective of environment sustainability action and its relevance

from accounting viewpoint. The research will evolve with the case study of an ASX listed

corporate named Wesfarmers. For this purpose of research, the Sustainability report of

Wesfarmers is considered for the last three financial years ranging from 2016 to 2018.

Sustainability report of Wesfarmers emphasizes on different aspects of corporate operation for its

stakeholders including environment with specific focus on issues like climate change resilience

and waste and water use. These reports will be analyzed in perspective of literature review on the

subject emphasizing on the issues of environment restoration for greener future world from

accounting perspective. The sustainability reports of the company highlight the domains of Key

Result Area to ensure environmental sustainability by Wesfarmers for the community as a part of

its CSR program. This article needs to generate a research question related to the subject.

Through literature review on the subject and the respective corporate disclosure about

environment sustainability, specific research question is set related to the corporate effort to

ensure environmental sustainability with specific focus on reduction of green gas emission

through the effort initiated by the company for their stakeholders. The findings of research are to

be valued by one theory known as Stakeholder theory. At the end, conclusion is to be drawn to

point out the objective of environmental sustainability effort by the company with its success to

facilitate the society and human kind, at large.

Research Question

Are the corporate bodies aware of climate change and use of natural resources for the society?

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Literature Review

The preliminary task to conduct this research is to do literature review on the subject of

environmental sustainability by corporate in respect of their disclosures with respect to

accounting practices. Four literatures are selected for this purpose from eminent journals to

highlight the need of this issue for future generation and respective stakeholders.

Literature Review 1

First literature considered for review is Climate change accounting: the challenge of uncertainty

in Pacific islands by Umesh Sharma, Vida Lucia Botes, Dani Foo and Ram Karan (January,

2017) published in International Journal of Critical Accounting. (Sharma et al., 2017) This article

is aiming towards setting out different key factors related to research on climate change in

respect of accounting and accountability. This research is based on the case study of specific

Pacific islands regarding climate change with main emphasis on increased water level due to

increased temperature of the region occurred by increased level of Green House Gas (GHG)

emission. This research is made on the basis of historical data of climate change of the region

and respective literature of climate change accounting. Interviews of stakeholders of the region

in the form of farmers were also conducted. It is observed that despite sincere effort on corporate

level to reduce GHG emission considering Kyoto emission reduction parameter, (Nations, 1997)

no significant improvement was found due to lack of strong policy implementation in the subject

with corporate business runs as usual. It is known that Paris agreement (Commission, 2015) had

specified required measures for maintenance of climate change status-quo parameter for

developed countries with identification of this problem as a major global problem for living

objects of the planet. The objective is to maintain the temperature increase within 1.5 degrees

5 | P a g e

The preliminary task to conduct this research is to do literature review on the subject of

environmental sustainability by corporate in respect of their disclosures with respect to

accounting practices. Four literatures are selected for this purpose from eminent journals to

highlight the need of this issue for future generation and respective stakeholders.

Literature Review 1

First literature considered for review is Climate change accounting: the challenge of uncertainty

in Pacific islands by Umesh Sharma, Vida Lucia Botes, Dani Foo and Ram Karan (January,

2017) published in International Journal of Critical Accounting. (Sharma et al., 2017) This article

is aiming towards setting out different key factors related to research on climate change in

respect of accounting and accountability. This research is based on the case study of specific

Pacific islands regarding climate change with main emphasis on increased water level due to

increased temperature of the region occurred by increased level of Green House Gas (GHG)

emission. This research is made on the basis of historical data of climate change of the region

and respective literature of climate change accounting. Interviews of stakeholders of the region

in the form of farmers were also conducted. It is observed that despite sincere effort on corporate

level to reduce GHG emission considering Kyoto emission reduction parameter, (Nations, 1997)

no significant improvement was found due to lack of strong policy implementation in the subject

with corporate business runs as usual. It is known that Paris agreement (Commission, 2015) had

specified required measures for maintenance of climate change status-quo parameter for

developed countries with identification of this problem as a major global problem for living

objects of the planet. The objective is to maintain the temperature increase within 1.5 degrees

5 | P a g e

with comparison to the pre-industrial period. It is observed that relatively very small effort was

done for climate change accounting in this area with lesser projection of accountability from the

responsible stakeholders. This research is based on the information of Pacific Islands but

provides good scope for future study in global context.

Literature Review 2

The second literature considered for review is Impact of Climate Change Disclosure on Financial

Performance: An Analysis of Indian Firms by Praveen Kumar and Mohammed Firoz published

in Journal of Environmental Accounting and Management (2018). (Kumar et al., 2018) This

research article tried to investigate the inherent relationship between disclosure of corporate

regarding climate change and the financial performance of the firm in the context of Indian

corporate scenario. For this purpose, 44 Indian firms are considered to assess their disclosure

related to climate change in perspective of Carbon Disclosure Project through a survey for the

period 2011 to 2015. Moreover their return on equity (ROE) (CFI, nd) and return on assets

(ROA) (Hargrave, 2019) are considered to understand their financial activities. With the control

of variables related to industry and firm specification, it is noticed that ROE is higher for the

corporate bodies with higher scores on environmental disclosure comparing to the entities with

lower scores of environmental disclosure. Further, the outcome of regression analysis proved that

the market endorses the concept of voluntary disclosure of climate change by corporate as

positive initiative resulting to positive coefficient of regression significantly. But there is no

significant proof that ROA is decided by climate change disclosures by corporate. The above

findings proved their significance for stakeholders like managers and investors to evaluate the

financial consequences of voluntary disclosure of climate change by the entities operating in

emerging economy.

6 | P a g e

done for climate change accounting in this area with lesser projection of accountability from the

responsible stakeholders. This research is based on the information of Pacific Islands but

provides good scope for future study in global context.

Literature Review 2

The second literature considered for review is Impact of Climate Change Disclosure on Financial

Performance: An Analysis of Indian Firms by Praveen Kumar and Mohammed Firoz published

in Journal of Environmental Accounting and Management (2018). (Kumar et al., 2018) This

research article tried to investigate the inherent relationship between disclosure of corporate

regarding climate change and the financial performance of the firm in the context of Indian

corporate scenario. For this purpose, 44 Indian firms are considered to assess their disclosure

related to climate change in perspective of Carbon Disclosure Project through a survey for the

period 2011 to 2015. Moreover their return on equity (ROE) (CFI, nd) and return on assets

(ROA) (Hargrave, 2019) are considered to understand their financial activities. With the control

of variables related to industry and firm specification, it is noticed that ROE is higher for the

corporate bodies with higher scores on environmental disclosure comparing to the entities with

lower scores of environmental disclosure. Further, the outcome of regression analysis proved that

the market endorses the concept of voluntary disclosure of climate change by corporate as

positive initiative resulting to positive coefficient of regression significantly. But there is no

significant proof that ROA is decided by climate change disclosures by corporate. The above

findings proved their significance for stakeholders like managers and investors to evaluate the

financial consequences of voluntary disclosure of climate change by the entities operating in

emerging economy.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Literature Review 3

The third literature reviewed for this purpose is Carbon Business Accounting: The Impact of

Global Warming on the Cost and Management Accounting Profession by Janek T.D. Ratnatunga

and Kashi R. Balachandran published in Journal of Accounting, Auditing and Finance (2009)

(Ratnatunga & Balachandran, 2009) The literature emphasizes on the gradual increase of GHG

emission resulting to disastrous climate change for the global environment. This problem needs

to attract greater attention by the corporate entities to implement different precautionary steps in

global and regional level. Stakeholders like governments, corporate and individual would be

seriously affected by this phenomenon and the needs of precautionary steps are to be enforced by

the entities in their decision-making system. Of all the entities, corporate entities have to ensure

proper measures in perspective of trading of carbon allowances, (Expert, nd) ensuring

investments in technologies for lower GHG emission, with assurance to regulate CO2 through

cost effective approaches giving effect of this extra cost in the product prices to be borne by the

consumers. (Direct, nd) This article did qualitative research study to follow Kyoto Protocol

system in the perspective of changing information pattern of cost and respective managerial tools

of accounting. This paper had shown the usefulness of strategic cost management process to

ensure carbon reduction management with special attention to ‘whole-life cost’ of products or

services in relation to carbon emission. (Öker & Adıgüzel, 2017) At the same time, this article

highlighted the process of participation of strategic cost management through accounting

activities to ensure facilitation of business decision making in business operation like HR

management, Supply Chain management, strategies of financial management with the resultant

assessment of corporate performance.

7 | P a g e

The third literature reviewed for this purpose is Carbon Business Accounting: The Impact of

Global Warming on the Cost and Management Accounting Profession by Janek T.D. Ratnatunga

and Kashi R. Balachandran published in Journal of Accounting, Auditing and Finance (2009)

(Ratnatunga & Balachandran, 2009) The literature emphasizes on the gradual increase of GHG

emission resulting to disastrous climate change for the global environment. This problem needs

to attract greater attention by the corporate entities to implement different precautionary steps in

global and regional level. Stakeholders like governments, corporate and individual would be

seriously affected by this phenomenon and the needs of precautionary steps are to be enforced by

the entities in their decision-making system. Of all the entities, corporate entities have to ensure

proper measures in perspective of trading of carbon allowances, (Expert, nd) ensuring

investments in technologies for lower GHG emission, with assurance to regulate CO2 through

cost effective approaches giving effect of this extra cost in the product prices to be borne by the

consumers. (Direct, nd) This article did qualitative research study to follow Kyoto Protocol

system in the perspective of changing information pattern of cost and respective managerial tools

of accounting. This paper had shown the usefulness of strategic cost management process to

ensure carbon reduction management with special attention to ‘whole-life cost’ of products or

services in relation to carbon emission. (Öker & Adıgüzel, 2017) At the same time, this article

highlighted the process of participation of strategic cost management through accounting

activities to ensure facilitation of business decision making in business operation like HR

management, Supply Chain management, strategies of financial management with the resultant

assessment of corporate performance.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Literature Review 4

The fourth literature considered for review is Climate Change Challenges to Accounting by

Constancio Zamora Ramírez and José María González published in Journal of Low Carbon

Economy (20013). (Ramírez & González, 2013) This article has emphasized on the role of

professional accountants to manage the issue of low carbon economy in corporate sector. Low

carbon economy is posing challenge to the accounting professional globally. There are two

aspects of managing accounting and preparing financial statements by the corporate with

consideration of low carbon economy. First is to understand the implication of financial

statements in perspective of low carbon economy imposed by both regulatory body and the

company. (everblue, 2017) The second aspect is to analyze the impact of accounting treatment

related to this criterion of low carbon economy with identification of real practical problems

raised while implanting this concept of report on emission of CO2 physically. This article

highlighted the probable accounting treatments of assets and liabilities of new carbon

ingredients, which are not controlled by external information. Along with that, the article also

emphasizes on the new relationship created by contract with regard to complex structure of

derivatives, procurement of carbon units through Emission Reduction Purchase Agreements or

EPRAs; monetization and collateralization of carbon and Carbon Funds. Concluding portion

raised the need of new reports to be generated like carbon accounting, respective risk

management with fixation of strategies using upgraded technology to combat climate change

through proper preparation and study of Carbon Reporting. (Trust, 2019)

Methods

The collection of data for this article is based upon the sustainability report of Wesfarmers for

2016 to 2018. The sustainability report for three years have quantitative data related to company

8 | P a g e

The fourth literature considered for review is Climate Change Challenges to Accounting by

Constancio Zamora Ramírez and José María González published in Journal of Low Carbon

Economy (20013). (Ramírez & González, 2013) This article has emphasized on the role of

professional accountants to manage the issue of low carbon economy in corporate sector. Low

carbon economy is posing challenge to the accounting professional globally. There are two

aspects of managing accounting and preparing financial statements by the corporate with

consideration of low carbon economy. First is to understand the implication of financial

statements in perspective of low carbon economy imposed by both regulatory body and the

company. (everblue, 2017) The second aspect is to analyze the impact of accounting treatment

related to this criterion of low carbon economy with identification of real practical problems

raised while implanting this concept of report on emission of CO2 physically. This article

highlighted the probable accounting treatments of assets and liabilities of new carbon

ingredients, which are not controlled by external information. Along with that, the article also

emphasizes on the new relationship created by contract with regard to complex structure of

derivatives, procurement of carbon units through Emission Reduction Purchase Agreements or

EPRAs; monetization and collateralization of carbon and Carbon Funds. Concluding portion

raised the need of new reports to be generated like carbon accounting, respective risk

management with fixation of strategies using upgraded technology to combat climate change

through proper preparation and study of Carbon Reporting. (Trust, 2019)

Methods

The collection of data for this article is based upon the sustainability report of Wesfarmers for

2016 to 2018. The sustainability report for three years have quantitative data related to company

8 | P a g e

action on environment preservation with specific focus on climate change and waste and water

management. These data are discussed with the basic concept of preservation of environment

with accounting treatment and ensure future provision of better future global environment.

Findings

The above literature reviews projected the consciousness of global stakeholders with particular

emphasis on accounting practices and respective reaction of accounting professional regarding

sustainable practice for environment. When we assess the evaluation of the literature reviews in

perspective of Wesfarmers, an Australian company, we have to consider their sustainability

reports published and endorsed by their board of directors for last three years related to their

awareness and respective actions regarding environment. It is observed that the company has

major concern about climate change caused by increased global warming and water usage and

waste management. The sustainability reports considered for this article are of 2016 to 2018 of

Wesfarmers.

Climate Change

In the sustainability report of Wesfarmers, 2016-2018 Wesfarmers has emphasized on the

company position about climate change with concern of global temperature to be maintained

within 1.5 degrees to 2 degrees in perspective of pre-industrial levels. The company urged upon

the need of joint effort by government and company to maintain the living environment of the

planet to minimize carbon emission through adapting long term policy and respective

implementation. Then the company emphasized management of GHG through adaptation of

advanced technology. The company declared their total emission of CO2 as 3.9, 4.1 and 3.9

million tons in 2016, 2017 and 2018, which was in lower trend than previous years. The below

chart can give clear idea about reduction of GHG emission in respect of last five years (2014-

9 | P a g e

management. These data are discussed with the basic concept of preservation of environment

with accounting treatment and ensure future provision of better future global environment.

Findings

The above literature reviews projected the consciousness of global stakeholders with particular

emphasis on accounting practices and respective reaction of accounting professional regarding

sustainable practice for environment. When we assess the evaluation of the literature reviews in

perspective of Wesfarmers, an Australian company, we have to consider their sustainability

reports published and endorsed by their board of directors for last three years related to their

awareness and respective actions regarding environment. It is observed that the company has

major concern about climate change caused by increased global warming and water usage and

waste management. The sustainability reports considered for this article are of 2016 to 2018 of

Wesfarmers.

Climate Change

In the sustainability report of Wesfarmers, 2016-2018 Wesfarmers has emphasized on the

company position about climate change with concern of global temperature to be maintained

within 1.5 degrees to 2 degrees in perspective of pre-industrial levels. The company urged upon

the need of joint effort by government and company to maintain the living environment of the

planet to minimize carbon emission through adapting long term policy and respective

implementation. Then the company emphasized management of GHG through adaptation of

advanced technology. The company declared their total emission of CO2 as 3.9, 4.1 and 3.9

million tons in 2016, 2017 and 2018, which was in lower trend than previous years. The below

chart can give clear idea about reduction of GHG emission in respect of last five years (2014-

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2018). It is evident from the graphical presentation that the company is gradually decreasing its

GHG emission with rigorous effort and adaptation of latest technology.

Refer to fourth literature reviewed, the company practiced carbon accounting with carbon fund

and carbon reporting. Respective adaptation of measures by the company includes better risk

management planning, ecosystem resilience and exercise of shadow pricing of carbon. The

disclosure of environment report by the company includes carbon disclosure project, national

pollutant inventory and potential environmental non-conformances. (Wesfarmers, 2016)

(Wesfarmers, 2017) (Wesfarmers, 2018)

10 | P a g e

GHG emission with rigorous effort and adaptation of latest technology.

Refer to fourth literature reviewed, the company practiced carbon accounting with carbon fund

and carbon reporting. Respective adaptation of measures by the company includes better risk

management planning, ecosystem resilience and exercise of shadow pricing of carbon. The

disclosure of environment report by the company includes carbon disclosure project, national

pollutant inventory and potential environmental non-conformances. (Wesfarmers, 2016)

(Wesfarmers, 2017) (Wesfarmers, 2018)

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

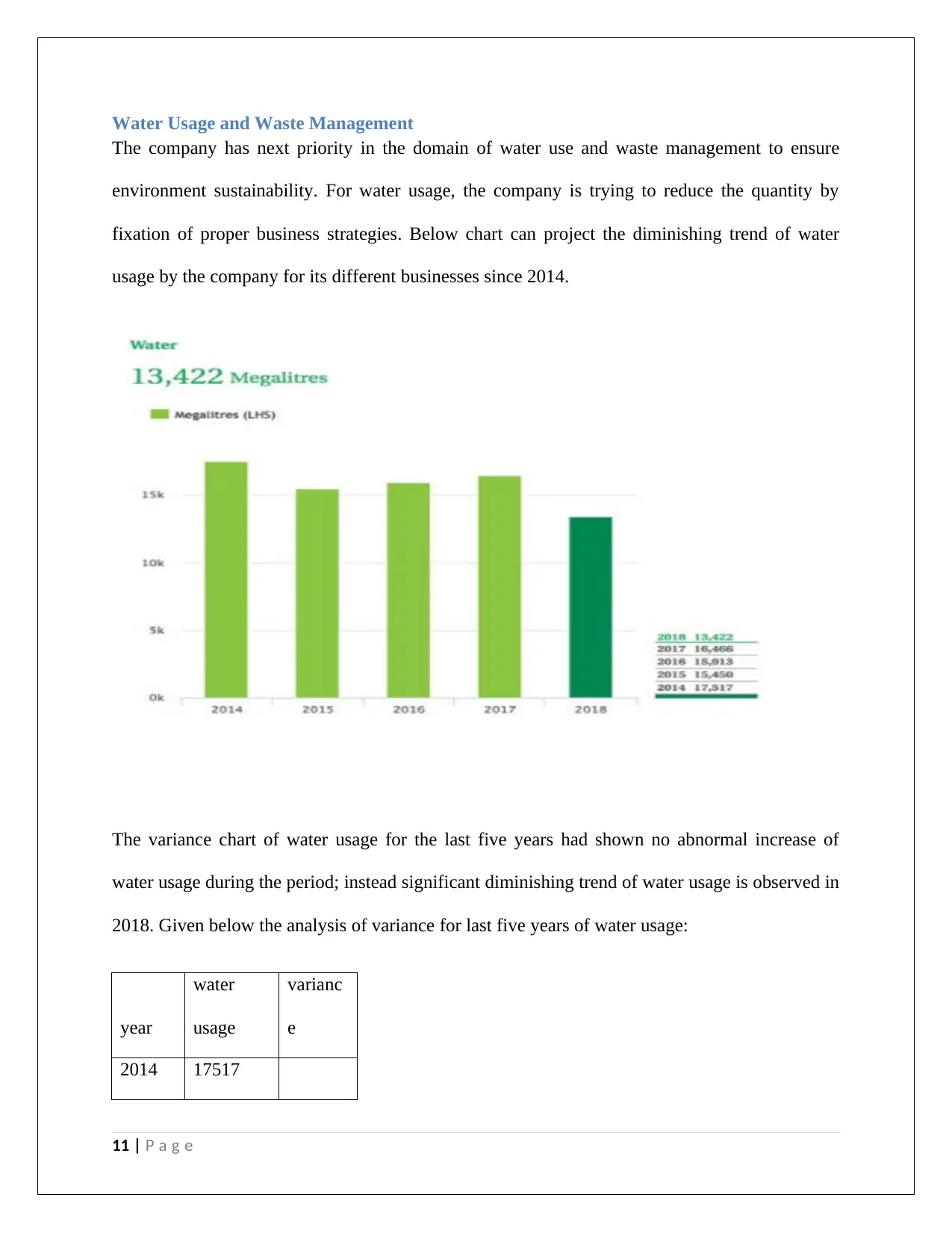

Water Usage and Waste Management

The company has next priority in the domain of water use and waste management to ensure

environment sustainability. For water usage, the company is trying to reduce the quantity by

fixation of proper business strategies. Below chart can project the diminishing trend of water

usage by the company for its different businesses since 2014.

The variance chart of water usage for the last five years had shown no abnormal increase of

water usage during the period; instead significant diminishing trend of water usage is observed in

2018. Given below the analysis of variance for last five years of water usage:

year

water

usage

varianc

e

2014 17517

11 | P a g e

The company has next priority in the domain of water use and waste management to ensure

environment sustainability. For water usage, the company is trying to reduce the quantity by

fixation of proper business strategies. Below chart can project the diminishing trend of water

usage by the company for its different businesses since 2014.

The variance chart of water usage for the last five years had shown no abnormal increase of

water usage during the period; instead significant diminishing trend of water usage is observed in

2018. Given below the analysis of variance for last five years of water usage:

year

water

usage

varianc

e

2014 17517

11 | P a g e

2015 15450

(11.

80)

2016 15913

3.

00

2017 16466

3.

48

2018 13422

(18.

49)

The company used water for its operation from three different sources- municipal supply,

recycled source and ground source. The percentage of municipal supply of water for the

company usage is around 60%, while recycled and reclaimed water resource is 29% and water

from ground sources are 11%. The same is accounted as per prevailing accounting practices set

by regulatory bodies.

For waste management, the company mainly uses the system of recycling and disposal of waste.

To ensure effective practice of efficient waste management, the company identified the packing

materials and found the technological help to make that disposable waste reusable through

recycling method. The below chart can give ideas about the quantity of recycled and disposed

waste as per company disclosure. It is observed that the company has waste management

strategy to ensure recycling method more preferable than disposing waste for the last five years.

12 | P a g e

(11.

80)

2016 15913

3.

00

2017 16466

3.

48

2018 13422

(18.

49)

The company used water for its operation from three different sources- municipal supply,

recycled source and ground source. The percentage of municipal supply of water for the

company usage is around 60%, while recycled and reclaimed water resource is 29% and water

from ground sources are 11%. The same is accounted as per prevailing accounting practices set

by regulatory bodies.

For waste management, the company mainly uses the system of recycling and disposal of waste.

To ensure effective practice of efficient waste management, the company identified the packing

materials and found the technological help to make that disposable waste reusable through

recycling method. The below chart can give ideas about the quantity of recycled and disposed

waste as per company disclosure. It is observed that the company has waste management

strategy to ensure recycling method more preferable than disposing waste for the last five years.

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.