HA2032 Financial Analysis: Wesfarmers and Woolworth Report

VerifiedAdded on 2022/09/16

|21

|4292

|10

Report

AI Summary

This report provides a detailed financial analysis of Wesfarmers and Woolworth, two prominent ASX-listed companies. The analysis begins with an examination of owner's equity, including issued share capital, reserved shares, retained earnings, and reserves, providing insights into each component's characteristics and impact on the companies' financial positions. The report then delves into the liabilities of both companies, categorizing them into current and non-current liabilities and explaining key items like trade payables and interest-bearing loans. Furthermore, the report explores the advantages and disadvantages of debt and equity financing methods, offering a comparative analysis. Finally, it discusses the various compliance and reporting requirements for small companies, large proprietary companies, and reporting entities, providing a comprehensive overview of financial reporting standards and practices.

Running head: FINANCIAL ANALYSIS OF WESFARMER AND WOOLWORTH

Financial Analysis of Wesfarmer and Woolworth

Name of the Student

Name of the University

Author note

Financial Analysis of Wesfarmer and Woolworth

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1Financial analysis of Wesfarmer and Woolworth

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Part a...........................................................................................................................................3

Part b........................................................................................................................................15

Conclusion................................................................................................................................16

Reference..................................................................................................................................17

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Part a...........................................................................................................................................3

Part b........................................................................................................................................15

Conclusion................................................................................................................................16

Reference..................................................................................................................................17

2Financial analysis of Wesfarmer and Woolworth

Executive summary

The aim of the report is to explain the concept of owner’s equity and liability of the two ASX

listed companies. In addition to that the report also contains a detail of the advantages and

disadvantages of debt and equity financing methods. the report further contains the various

compliances and reporting requirements of small companies, large proprietary companies and

the reporting entity.

Executive summary

The aim of the report is to explain the concept of owner’s equity and liability of the two ASX

listed companies. In addition to that the report also contains a detail of the advantages and

disadvantages of debt and equity financing methods. the report further contains the various

compliances and reporting requirements of small companies, large proprietary companies and

the reporting entity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3Financial analysis of Wesfarmer and Woolworth

Introduction

The owner’s equity and the liability of any organization reflects the financial position

of a company. Both these items of the balance sheet provide information to the stakeholders

and based on that the stakeholders can take important decisions about investing in a

company. The Wesfarmer and Woolworth are two ASX listed companies which have strong

financial position and that can be easily observed from the financial position of the

companies. The report also provides a brief detail about the various compliances that are

required for small, large and reporting entities.

Discussion

Part a

Wesfarmers is one of the largest retail sector company in Australia. The owner’s

equity of the company includes the following items are recorded in the owner’s equity section

of the company are issued shares capital, reserved shares, retained earnings, and reserves

(Moritz Block and Heinz 2016). Each item of the company has its own unique features each

of the items are explained in brief:

Issued share capital:

The issued capital refers to the quantity of shares that are issues to the shareholders by

the company. In other words, it can be said that the share holders that are held by the

shareholders is called the issued capital.

Issued capital consists that part of an authorized capital, these are the shares which the

company can sell to the open market. The company use the issued capital to fulfill the need of

finance and by issuing the issued capital the company will be able to meet the capital

requirement. The issued capital is also known as subscribed capital, as the quantity of shares

Introduction

The owner’s equity and the liability of any organization reflects the financial position

of a company. Both these items of the balance sheet provide information to the stakeholders

and based on that the stakeholders can take important decisions about investing in a

company. The Wesfarmer and Woolworth are two ASX listed companies which have strong

financial position and that can be easily observed from the financial position of the

companies. The report also provides a brief detail about the various compliances that are

required for small, large and reporting entities.

Discussion

Part a

Wesfarmers is one of the largest retail sector company in Australia. The owner’s

equity of the company includes the following items are recorded in the owner’s equity section

of the company are issued shares capital, reserved shares, retained earnings, and reserves

(Moritz Block and Heinz 2016). Each item of the company has its own unique features each

of the items are explained in brief:

Issued share capital:

The issued capital refers to the quantity of shares that are issues to the shareholders by

the company. In other words, it can be said that the share holders that are held by the

shareholders is called the issued capital.

Issued capital consists that part of an authorized capital, these are the shares which the

company can sell to the open market. The company use the issued capital to fulfill the need of

finance and by issuing the issued capital the company will be able to meet the capital

requirement. The issued capital is also known as subscribed capital, as the quantity of shares

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4Financial analysis of Wesfarmer and Woolworth

purchased by the shareholders denotes the sum of money financed in the firm (Madra-

Sawicka and Wasilewski 2017).

This can be further explained by a illustration. Suppose a firm has an authorized

capital of 20000000 where the value of per share is 10. If the company receives an

application for 2000000 shares and the company issued 1800000 shares of 10 each. Then in

that case the issued capital would be $1800000. So the issued capital is that part of the capital

that the company requires and not the amount that is applied by the shareholders.

The issued capital denotes the shares that have been issued to the shareholders and

which will remain unpaid. Any shares redeemed or repurchased by the company itself for the

purpose of keeping it in the stock is not a part of the issued capital (Jackowicz, Mielcarz, and

Wnuczak, 2017).

The value of the share capital varies with the issue of the new shares to the current

new shareholders. Also, the company may repurchase or redeems its shares that consequence

in the alteration in the value of the subscribed capital.

Reserved shares

The reserve share capital is the part of the subscribed capital of a company which the

company decides not to call excepts in case of liquidation of the company. The reserve

capital is created out of the authorized capital. the reserve capital is used only at the

happening if the liquidation of the company (De Rassenfosse and Fischer 2016).

Retained earnings

The retained earnings is the part of profit that a company has earned during a financial

year, less any dividends or other distributions paid to investors. This amount is attuned each

time there is an admission to the accounting records that influences a revenue or expense

purchased by the shareholders denotes the sum of money financed in the firm (Madra-

Sawicka and Wasilewski 2017).

This can be further explained by a illustration. Suppose a firm has an authorized

capital of 20000000 where the value of per share is 10. If the company receives an

application for 2000000 shares and the company issued 1800000 shares of 10 each. Then in

that case the issued capital would be $1800000. So the issued capital is that part of the capital

that the company requires and not the amount that is applied by the shareholders.

The issued capital denotes the shares that have been issued to the shareholders and

which will remain unpaid. Any shares redeemed or repurchased by the company itself for the

purpose of keeping it in the stock is not a part of the issued capital (Jackowicz, Mielcarz, and

Wnuczak, 2017).

The value of the share capital varies with the issue of the new shares to the current

new shareholders. Also, the company may repurchase or redeems its shares that consequence

in the alteration in the value of the subscribed capital.

Reserved shares

The reserve share capital is the part of the subscribed capital of a company which the

company decides not to call excepts in case of liquidation of the company. The reserve

capital is created out of the authorized capital. the reserve capital is used only at the

happening if the liquidation of the company (De Rassenfosse and Fischer 2016).

Retained earnings

The retained earnings is the part of profit that a company has earned during a financial

year, less any dividends or other distributions paid to investors. This amount is attuned each

time there is an admission to the accounting records that influences a revenue or expense

5Financial analysis of Wesfarmer and Woolworth

account. A large retained earning balance suggests a financially fit company (Eliasson 2016).

The formula of retained earning is

Opening retained earnings + profit or loss – dividends = ending retained earnings.

If the retained earning of a company is negative then such amount will be treated as

accumulated deficit. This happens if the company experienced losses or declare more

dividend than the retained earning balance.

The retained earning balance is recorded in the stockholder’s equity section of the

balance sheet. To evaluate the retained earnings, it is required to consider the following

points:

The period of existence of the company

The longer the period of existence of a company in the market the more it will be able

to compile the retained earnings.

Dividend policy

A company that declares dividend on regular basis they failed to maintain higher

retained earnings.

Profitability

A high profit profitability ratio eventually yields a large amount of retained earnings

subject to the provision of the above-mentioned points.

Cyclical industry

The company that is engaged in a industry that is highly cyclical and requires high

liquid assets on regular interval then in that situation the company has to arrange large

account. A large retained earning balance suggests a financially fit company (Eliasson 2016).

The formula of retained earning is

Opening retained earnings + profit or loss – dividends = ending retained earnings.

If the retained earning of a company is negative then such amount will be treated as

accumulated deficit. This happens if the company experienced losses or declare more

dividend than the retained earning balance.

The retained earning balance is recorded in the stockholder’s equity section of the

balance sheet. To evaluate the retained earnings, it is required to consider the following

points:

The period of existence of the company

The longer the period of existence of a company in the market the more it will be able

to compile the retained earnings.

Dividend policy

A company that declares dividend on regular basis they failed to maintain higher

retained earnings.

Profitability

A high profit profitability ratio eventually yields a large amount of retained earnings

subject to the provision of the above-mentioned points.

Cyclical industry

The company that is engaged in a industry that is highly cyclical and requires high

liquid assets on regular interval then in that situation the company has to arrange large

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6Financial analysis of Wesfarmer and Woolworth

retained earning reserves during the profitable period of the cycle in order to protect the

company at the time of financial crisis (Lamb and Butler 2018).

Reserves

Reserves are created out of the retained earnings the reserves are classified into two

types the capital; reserve and the revenue reserve. The revenue reserve are portions of the

profits earned from the regular operation of the business. Revenue reserve is further classified

in to two types the general reserve and the specific reserve (Arifin 2017).

Capital reserve

The capital reserve are made out of the capital profits that is the profits that are

created from the sources which are different from the regular business operation.

From the accounting concepts, reserves are recorded by debiting the retained earnings

and crediting the amount in the reserve accounts. When the purpose for which the reserve is

created is fulfilled then after that if any balance is remained in the reserve account will be

transferred to the retained earnings account (Dhaene et al 2017).

For example, a business wants to keep aside reserves to fund the purchase of a new

premises for its office use. they credit the office reserve fund for $1000000 and debit the

retained earnings accounts with the same amount. Once the sale is fixed the entry will be

reversed and the office reserve will be debited and at the same time the retained earning

account will be credited (Moritz Block and Heinz 2016).

The reserve accounts are recorded as liabilities on the balance sheet under reserve and

surplus. if a company make losses then in that case no reserve is required to be made.

The Wes farmers owner’s equity for the last three years is analysed in the following points

retained earning reserves during the profitable period of the cycle in order to protect the

company at the time of financial crisis (Lamb and Butler 2018).

Reserves

Reserves are created out of the retained earnings the reserves are classified into two

types the capital; reserve and the revenue reserve. The revenue reserve are portions of the

profits earned from the regular operation of the business. Revenue reserve is further classified

in to two types the general reserve and the specific reserve (Arifin 2017).

Capital reserve

The capital reserve are made out of the capital profits that is the profits that are

created from the sources which are different from the regular business operation.

From the accounting concepts, reserves are recorded by debiting the retained earnings

and crediting the amount in the reserve accounts. When the purpose for which the reserve is

created is fulfilled then after that if any balance is remained in the reserve account will be

transferred to the retained earnings account (Dhaene et al 2017).

For example, a business wants to keep aside reserves to fund the purchase of a new

premises for its office use. they credit the office reserve fund for $1000000 and debit the

retained earnings accounts with the same amount. Once the sale is fixed the entry will be

reversed and the office reserve will be debited and at the same time the retained earning

account will be credited (Moritz Block and Heinz 2016).

The reserve accounts are recorded as liabilities on the balance sheet under reserve and

surplus. if a company make losses then in that case no reserve is required to be made.

The Wes farmers owner’s equity for the last three years is analysed in the following points

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7Financial analysis of Wesfarmer and Woolworth

Particulars 2016 2017 2018

Issued capital 21937 22268 22277

Reserved shares (28) (26) (43)

Retained earnings 874 1509 176

Reserves 166 190 344

From the above table all the items of the owner’s equity is classified and explained in details

Issued capital

The issued capital of wesfarmer has moved from 21937in the year 2016 to 22277 in

the year 2018. This indicates that the company has issued share capital in the last three years

to its existing shareholders to meet its capital requirement for the last three years.

Reserved shares

The reserved shares of the company are in negative figure which indicates that the

company is not intend to keep any fund that may be required during the time of liquidation.

Retained earnings

The company’s retained earning has failed drastically in the year 2018 which means

the company has failed to perform in the year 2018. In the year 2016 the company’s retained

earning was $874 which means that the company has performed very well in the year and has

been able to create a good amount in the retained earning account. In the year 2017 the

company made further improvement in its operation for which the company’s retained

earning increased by 42.08% that means that the company has performed extremely good

with full efficiency. But in the year 2018 the performance fall to 176 which means that the

Particulars 2016 2017 2018

Issued capital 21937 22268 22277

Reserved shares (28) (26) (43)

Retained earnings 874 1509 176

Reserves 166 190 344

From the above table all the items of the owner’s equity is classified and explained in details

Issued capital

The issued capital of wesfarmer has moved from 21937in the year 2016 to 22277 in

the year 2018. This indicates that the company has issued share capital in the last three years

to its existing shareholders to meet its capital requirement for the last three years.

Reserved shares

The reserved shares of the company are in negative figure which indicates that the

company is not intend to keep any fund that may be required during the time of liquidation.

Retained earnings

The company’s retained earning has failed drastically in the year 2018 which means

the company has failed to perform in the year 2018. In the year 2016 the company’s retained

earning was $874 which means that the company has performed very well in the year and has

been able to create a good amount in the retained earning account. In the year 2017 the

company made further improvement in its operation for which the company’s retained

earning increased by 42.08% that means that the company has performed extremely good

with full efficiency. But in the year 2018 the performance fall to 176 which means that the

8Financial analysis of Wesfarmer and Woolworth

company has made a loss of $1333 million during the financial year 2018 (Kim An and Kim

2015).

Reserves

The Wes farmers has increased its reserve account continuously during the last three

years which means that the it is setting aside funds to meet some obligations that may occur

in the future. Though the company does not transfer not huge percentage from the retained

earnings to the reserve fund but even the company make a loss of $1333 million in the year

2018 it has set aside a good amount from the retained earning this policy is not acceptable

from the view point of the company. In the year the company transferred $166 million and in

the year the company has $190 million in the reserve funds and in the year the company has

transferred $344 million which means the company consistently increased the reserve

(Ghouma Ben-Nasr and Yan 2018).

Woolworth

Particular 2016 2017 2018

Contributed equity 5252.20 5615 6055

Reserves 93.90 357 353

Retained earnings 3124.50 3554 4073

Contributed equity

The contributed equity of the company increased over the last three years which

indicates that the company issued capital from the market from its existing shareholders. In

the year 2016 the contributed equity was 5252.20 and it increased to 5615 in the year 2017

the amount of the contributed equity further increased to 6055 in the year 2018 which

company has made a loss of $1333 million during the financial year 2018 (Kim An and Kim

2015).

Reserves

The Wes farmers has increased its reserve account continuously during the last three

years which means that the it is setting aside funds to meet some obligations that may occur

in the future. Though the company does not transfer not huge percentage from the retained

earnings to the reserve fund but even the company make a loss of $1333 million in the year

2018 it has set aside a good amount from the retained earning this policy is not acceptable

from the view point of the company. In the year the company transferred $166 million and in

the year the company has $190 million in the reserve funds and in the year the company has

transferred $344 million which means the company consistently increased the reserve

(Ghouma Ben-Nasr and Yan 2018).

Woolworth

Particular 2016 2017 2018

Contributed equity 5252.20 5615 6055

Reserves 93.90 357 353

Retained earnings 3124.50 3554 4073

Contributed equity

The contributed equity of the company increased over the last three years which

indicates that the company issued capital from the market from its existing shareholders. In

the year 2016 the contributed equity was 5252.20 and it increased to 5615 in the year 2017

the amount of the contributed equity further increased to 6055 in the year 2018 which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9Financial analysis of Wesfarmer and Woolworth

indicates that in the last three years whenever the company requires fund it raised that fund

from the existing shareholders (Robinson et al 2015).

Reserves

The reserve of the company increased continuously in the last three years which

indicates that the company has been able to make profit continuously over the last three

years and that the company is very efficiently carrying on its business and at the same time

they are effectively managing the funds to meet their anticipated future expenditures.

Retained earnings

The company has been able to earn profit continuously in the last three years. In the

year 2016 the retained earning of the company is 3124.50 and that increased to 3554 in the

year 2017 and that further increased to $4073 this indicates that the company has been able to

generate profit over the last three years.

The liabilities are classified into two parts these are current liabilities and the non current

liabilities.

Under the current liabilities the following items are recorded

Trade and other payable

Interest bearing loans and borrowings

Income tax payable

Provisions

Derivatives

Other

Non current liabilities

Interest bearing loans and borrowings

indicates that in the last three years whenever the company requires fund it raised that fund

from the existing shareholders (Robinson et al 2015).

Reserves

The reserve of the company increased continuously in the last three years which

indicates that the company has been able to make profit continuously over the last three

years and that the company is very efficiently carrying on its business and at the same time

they are effectively managing the funds to meet their anticipated future expenditures.

Retained earnings

The company has been able to earn profit continuously in the last three years. In the

year 2016 the retained earning of the company is 3124.50 and that increased to 3554 in the

year 2017 and that further increased to $4073 this indicates that the company has been able to

generate profit over the last three years.

The liabilities are classified into two parts these are current liabilities and the non current

liabilities.

Under the current liabilities the following items are recorded

Trade and other payable

Interest bearing loans and borrowings

Income tax payable

Provisions

Derivatives

Other

Non current liabilities

Interest bearing loans and borrowings

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10Financial analysis of Wesfarmer and Woolworth

The items of the liabilities are explained in brief in the following points

Trade and other payables

The trade and other payables are the suppliers of the organization who supply the raw

materials to the company they are very vital for the company as without them the company

will not be able to carry on its operation. The suppliers or the trade payables by providing the

necessary resources to the company enables the organization to continue its business

operation.

Interest bearing loans borrowing

The interest-bearing loans and borrowing are the amount that company takes from the

banks or other financial institutes that help the company to meet its financial obligations. The

company takes the interest-bearing loans by paying interest on the borrowing amount. the

company must keep a collateral security for taking such loans from the banks (Pinder et al

2017).

Income tax payables

The income tax is the statutory obligation that a company must pay to the respective

government from the revenue that they have earned during the financial year. Its is very

essential to assess the correct amount of tax as the failure to pay the tax liability will attract

severe penalty and other consequences that can create adverse effect on the image of the

company (McBarnet 2019).

Provision

The provisions are created as a fund against any expense that may arise in the future.

The company used to set aside a company’s profit to cover an expected liability or a decrease

The items of the liabilities are explained in brief in the following points

Trade and other payables

The trade and other payables are the suppliers of the organization who supply the raw

materials to the company they are very vital for the company as without them the company

will not be able to carry on its operation. The suppliers or the trade payables by providing the

necessary resources to the company enables the organization to continue its business

operation.

Interest bearing loans borrowing

The interest-bearing loans and borrowing are the amount that company takes from the

banks or other financial institutes that help the company to meet its financial obligations. The

company takes the interest-bearing loans by paying interest on the borrowing amount. the

company must keep a collateral security for taking such loans from the banks (Pinder et al

2017).

Income tax payables

The income tax is the statutory obligation that a company must pay to the respective

government from the revenue that they have earned during the financial year. Its is very

essential to assess the correct amount of tax as the failure to pay the tax liability will attract

severe penalty and other consequences that can create adverse effect on the image of the

company (McBarnet 2019).

Provision

The provisions are created as a fund against any expense that may arise in the future.

The company used to set aside a company’s profit to cover an expected liability or a decrease

11Financial analysis of Wesfarmer and Woolworth

in the value of an assets even though the specific amount is unknown. A provision should not

be treated as a form of savings but it should be recognized as a upcoming liability in advance.

Derivatives

The derivatives are financial instruments that may create a obligation for the company in the

future.

Other liabilities

The other liabilities are insignificant amount of liabilities that are not recorded

separately in the balance sheet. The company used to combine all the miscellaneous liabilities

and recorded the amount in the balance sheet.

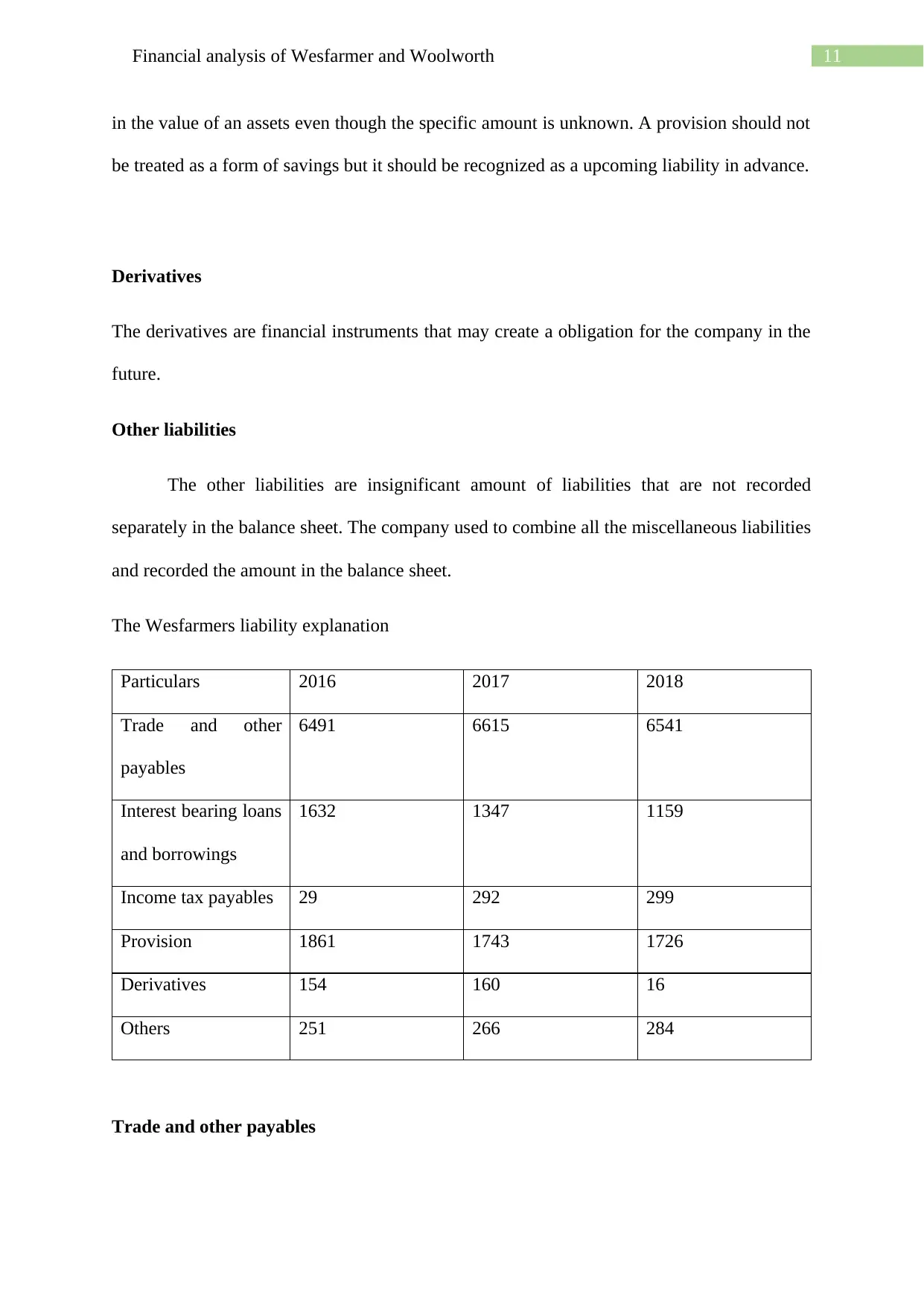

The Wesfarmers liability explanation

Particulars 2016 2017 2018

Trade and other

payables

6491 6615 6541

Interest bearing loans

and borrowings

1632 1347 1159

Income tax payables 29 292 299

Provision 1861 1743 1726

Derivatives 154 160 16

Others 251 266 284

Trade and other payables

in the value of an assets even though the specific amount is unknown. A provision should not

be treated as a form of savings but it should be recognized as a upcoming liability in advance.

Derivatives

The derivatives are financial instruments that may create a obligation for the company in the

future.

Other liabilities

The other liabilities are insignificant amount of liabilities that are not recorded

separately in the balance sheet. The company used to combine all the miscellaneous liabilities

and recorded the amount in the balance sheet.

The Wesfarmers liability explanation

Particulars 2016 2017 2018

Trade and other

payables

6491 6615 6541

Interest bearing loans

and borrowings

1632 1347 1159

Income tax payables 29 292 299

Provision 1861 1743 1726

Derivatives 154 160 16

Others 251 266 284

Trade and other payables

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.