Wesfarmers & Woolworths: Comprehensive Financial Accounting Analysis

VerifiedAdded on 2024/04/25

|14

|2711

|432

Homework Assignment

AI Summary

This assignment provides a detailed financial analysis of Wesfarmers and Woolworths, focusing on key aspects of their financial statements. For Wesfarmers, it examines current liabilities, including trade payables, income tax, derivatives, provisions, and interest-bearing loans, detailing their classifications and changes over the year. The analysis identifies major liabilities and delves into the nature of items under ‘Provisions,’ assessing their compliance with IAS37/AASB137. It also quantifies cash raised and repaid through interest-bearing loans, comparing these figures with the previous year, and identifies secured and non-current liabilities. For Woolworths, the assignment contrasts the income statement's tax expense with that of a partnership, explains the appropriation of total profit, differentiates issued capital from that of a typical partnership, and considers the necessity of preparing similar statements for partnerships. The document concludes by highlighting the key differences in financial reporting between large corporations and partnership firms.

Fundamentals of Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Part A:..............................................................................................................................................3

1. Information and detailed classification of current liabilities of Wesfarmers...........................3

2. Major liabilities of Wesfarmers at the end of the financial year?............................................4

3. Items included under the heading ‘Provisions’ in the ‘Current Liabilities’ section of the

statement of financial position and the nature of these items. Satisfaction with the definition of

provisions as contained in IAS37/AASB137...............................................................................5

4. How much cash has been raised by interest-bearing loans in the most recent financial year?

How much of such loans have been repaid? How do these amounts compare with the previous

year?.............................................................................................................................................7

5. Whether any of the non-current liabilities are secured............................................................8

6. Non-current provisions and the meaning.................................................................................9

Part B:............................................................................................................................................10

1. The Woolworth income statement shows a deduction (in brackets) for income tax expense.

Would this expense item be seen in the income statement of a partnership?............................10

2. How is the total profit available appropriated and the explanation of allocation of the total

profit available for appropriation in a partnership differ from that shown for Woolworth

Limited.......................................................................................................................................11

3. Issued capital’ of Woolworth and differentiation from that of a typical partnership............12

4. Would the typical partnership be required to prepare such a statement?...............................13

References:....................................................................................................................................14

2

Part A:..............................................................................................................................................3

1. Information and detailed classification of current liabilities of Wesfarmers...........................3

2. Major liabilities of Wesfarmers at the end of the financial year?............................................4

3. Items included under the heading ‘Provisions’ in the ‘Current Liabilities’ section of the

statement of financial position and the nature of these items. Satisfaction with the definition of

provisions as contained in IAS37/AASB137...............................................................................5

4. How much cash has been raised by interest-bearing loans in the most recent financial year?

How much of such loans have been repaid? How do these amounts compare with the previous

year?.............................................................................................................................................7

5. Whether any of the non-current liabilities are secured............................................................8

6. Non-current provisions and the meaning.................................................................................9

Part B:............................................................................................................................................10

1. The Woolworth income statement shows a deduction (in brackets) for income tax expense.

Would this expense item be seen in the income statement of a partnership?............................10

2. How is the total profit available appropriated and the explanation of allocation of the total

profit available for appropriation in a partnership differ from that shown for Woolworth

Limited.......................................................................................................................................11

3. Issued capital’ of Woolworth and differentiation from that of a typical partnership............12

4. Would the typical partnership be required to prepare such a statement?...............................13

References:....................................................................................................................................14

2

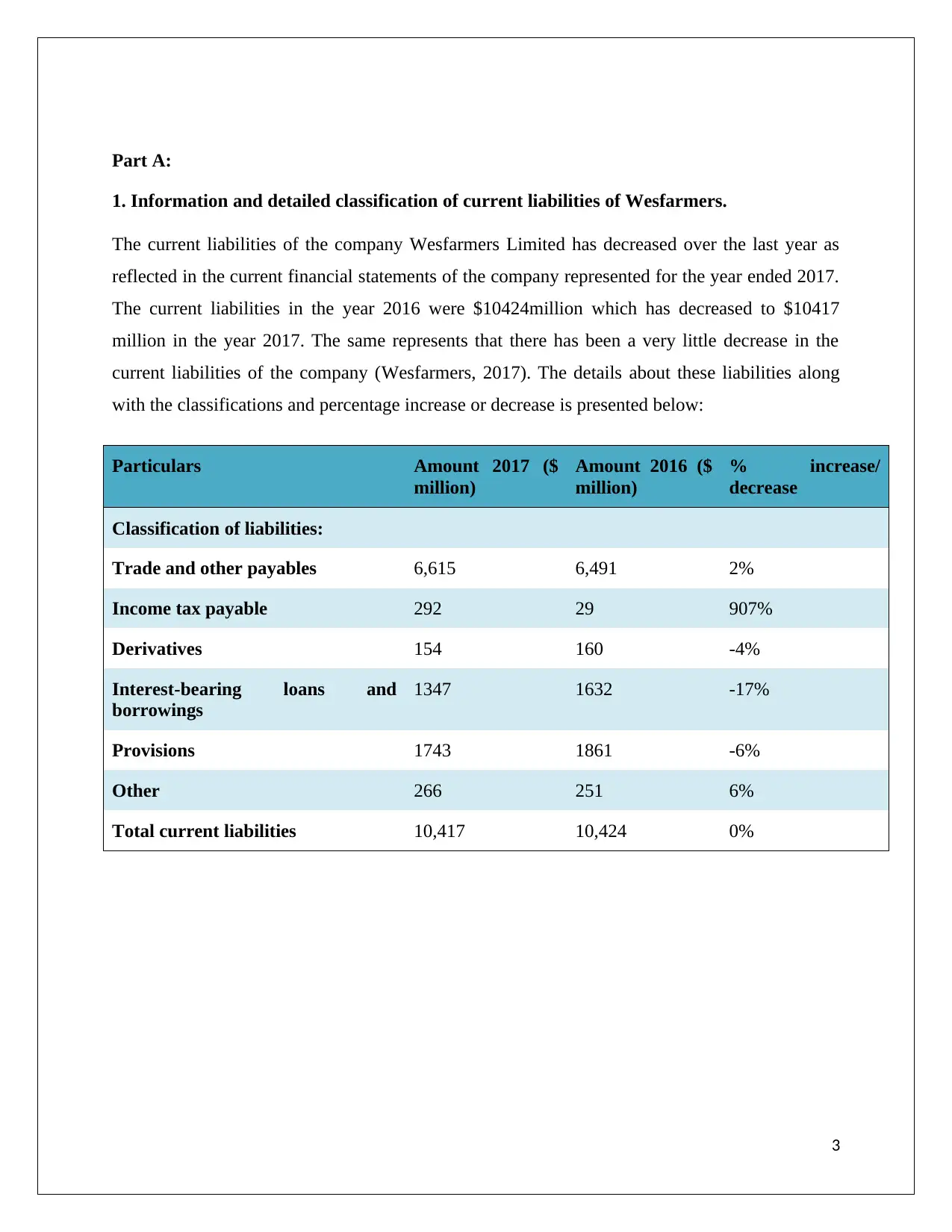

Part A:

1. Information and detailed classification of current liabilities of Wesfarmers.

The current liabilities of the company Wesfarmers Limited has decreased over the last year as

reflected in the current financial statements of the company represented for the year ended 2017.

The current liabilities in the year 2016 were $10424million which has decreased to $10417

million in the year 2017. The same represents that there has been a very little decrease in the

current liabilities of the company (Wesfarmers, 2017). The details about these liabilities along

with the classifications and percentage increase or decrease is presented below:

Particulars Amount 2017 ($

million)

Amount 2016 ($

million)

% increase/

decrease

Classification of liabilities:

Trade and other payables 6,615 6,491 2%

Income tax payable 292 29 907%

Derivatives 154 160 -4%

Interest-bearing loans and

borrowings

1347 1632 -17%

Provisions 1743 1861 -6%

Other 266 251 6%

Total current liabilities 10,417 10,424 0%

3

1. Information and detailed classification of current liabilities of Wesfarmers.

The current liabilities of the company Wesfarmers Limited has decreased over the last year as

reflected in the current financial statements of the company represented for the year ended 2017.

The current liabilities in the year 2016 were $10424million which has decreased to $10417

million in the year 2017. The same represents that there has been a very little decrease in the

current liabilities of the company (Wesfarmers, 2017). The details about these liabilities along

with the classifications and percentage increase or decrease is presented below:

Particulars Amount 2017 ($

million)

Amount 2016 ($

million)

% increase/

decrease

Classification of liabilities:

Trade and other payables 6,615 6,491 2%

Income tax payable 292 29 907%

Derivatives 154 160 -4%

Interest-bearing loans and

borrowings

1347 1632 -17%

Provisions 1743 1861 -6%

Other 266 251 6%

Total current liabilities 10,417 10,424 0%

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Major liabilities of Wesfarmers at the end of the financial year?

The major liabilities which are included in the current obligations of the company are as follows:

Trade and other payables = These are concerned with the amount which is payable as a due to

purchases made by the company and the credit obtained in lieu of those purchases and the

expenses incurred by the company. The same amounted to $6615 million (Adibah, et. al., 2013).

Provisions = The provision includes the liabilities that may be incurred in future due to

employee benefit expense, wages and salaries to be paid, annual leaves and long service leaves,

lase provisions, off market contracts, self-insured risk and mines and plants rehabilitation in the

company. The same amounted to $1743 million in total for the year 2017.

Interest bearing loans and borrowings = The interest bearing liabilities are concerned with the

unsecured portion of the bank debt and capital market debt of the company. In the year 2017 they

amounted to $1347 million (Wesfarmers, 2017).

4

The major liabilities which are included in the current obligations of the company are as follows:

Trade and other payables = These are concerned with the amount which is payable as a due to

purchases made by the company and the credit obtained in lieu of those purchases and the

expenses incurred by the company. The same amounted to $6615 million (Adibah, et. al., 2013).

Provisions = The provision includes the liabilities that may be incurred in future due to

employee benefit expense, wages and salaries to be paid, annual leaves and long service leaves,

lase provisions, off market contracts, self-insured risk and mines and plants rehabilitation in the

company. The same amounted to $1743 million in total for the year 2017.

Interest bearing loans and borrowings = The interest bearing liabilities are concerned with the

unsecured portion of the bank debt and capital market debt of the company. In the year 2017 they

amounted to $1347 million (Wesfarmers, 2017).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

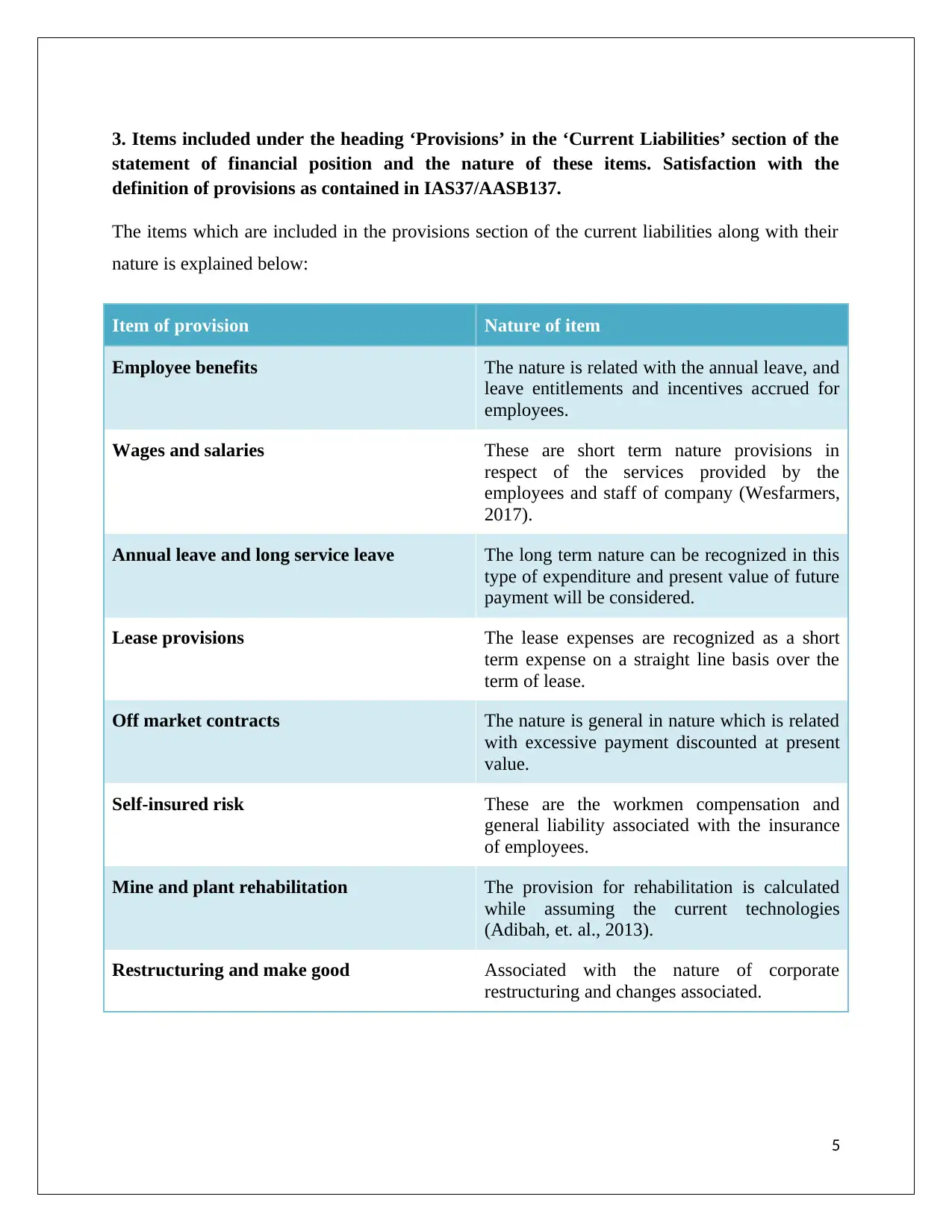

3. Items included under the heading ‘Provisions’ in the ‘Current Liabilities’ section of the

statement of financial position and the nature of these items. Satisfaction with the

definition of provisions as contained in IAS37/AASB137.

The items which are included in the provisions section of the current liabilities along with their

nature is explained below:

Item of provision Nature of item

Employee benefits The nature is related with the annual leave, and

leave entitlements and incentives accrued for

employees.

Wages and salaries These are short term nature provisions in

respect of the services provided by the

employees and staff of company (Wesfarmers,

2017).

Annual leave and long service leave The long term nature can be recognized in this

type of expenditure and present value of future

payment will be considered.

Lease provisions The lease expenses are recognized as a short

term expense on a straight line basis over the

term of lease.

Off market contracts The nature is general in nature which is related

with excessive payment discounted at present

value.

Self-insured risk These are the workmen compensation and

general liability associated with the insurance

of employees.

Mine and plant rehabilitation The provision for rehabilitation is calculated

while assuming the current technologies

(Adibah, et. al., 2013).

Restructuring and make good Associated with the nature of corporate

restructuring and changes associated.

5

statement of financial position and the nature of these items. Satisfaction with the

definition of provisions as contained in IAS37/AASB137.

The items which are included in the provisions section of the current liabilities along with their

nature is explained below:

Item of provision Nature of item

Employee benefits The nature is related with the annual leave, and

leave entitlements and incentives accrued for

employees.

Wages and salaries These are short term nature provisions in

respect of the services provided by the

employees and staff of company (Wesfarmers,

2017).

Annual leave and long service leave The long term nature can be recognized in this

type of expenditure and present value of future

payment will be considered.

Lease provisions The lease expenses are recognized as a short

term expense on a straight line basis over the

term of lease.

Off market contracts The nature is general in nature which is related

with excessive payment discounted at present

value.

Self-insured risk These are the workmen compensation and

general liability associated with the insurance

of employees.

Mine and plant rehabilitation The provision for rehabilitation is calculated

while assuming the current technologies

(Adibah, et. al., 2013).

Restructuring and make good Associated with the nature of corporate

restructuring and changes associated.

5

As per the rules contained in relevant provisions of IAS37/AASB137, a proviso shall be

recognized when the entity has a present obligation or debt due to past events incurred which

will; result in future outflow of benefits and a reliable estimate can be made for the obligation to

be paid. The same conditions are fulfilled while analysing each and every item and therefore the

same is in conformity with the relevant provisions (Mathuva, 2015).

The liability for employee benefit expense has been increased from $8847 million in the year

2016 to $9132 million in the year 2017. The same represents a significant increase in the

concerned liability.

6

recognized when the entity has a present obligation or debt due to past events incurred which

will; result in future outflow of benefits and a reliable estimate can be made for the obligation to

be paid. The same conditions are fulfilled while analysing each and every item and therefore the

same is in conformity with the relevant provisions (Mathuva, 2015).

The liability for employee benefit expense has been increased from $8847 million in the year

2016 to $9132 million in the year 2017. The same represents a significant increase in the

concerned liability.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

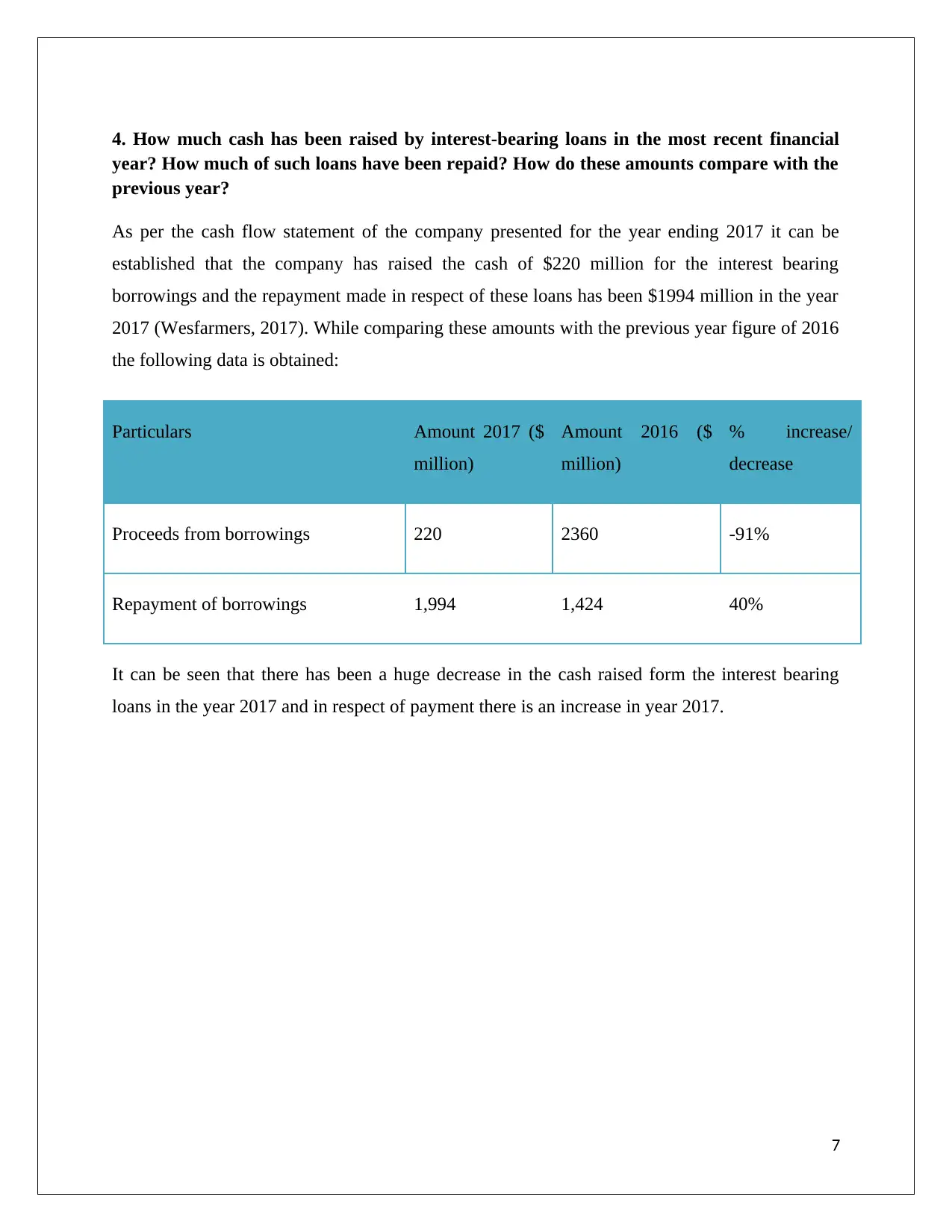

4. How much cash has been raised by interest-bearing loans in the most recent financial

year? How much of such loans have been repaid? How do these amounts compare with the

previous year?

As per the cash flow statement of the company presented for the year ending 2017 it can be

established that the company has raised the cash of $220 million for the interest bearing

borrowings and the repayment made in respect of these loans has been $1994 million in the year

2017 (Wesfarmers, 2017). While comparing these amounts with the previous year figure of 2016

the following data is obtained:

Particulars Amount 2017 ($

million)

Amount 2016 ($

million)

% increase/

decrease

Proceeds from borrowings 220 2360 -91%

Repayment of borrowings 1,994 1,424 40%

It can be seen that there has been a huge decrease in the cash raised form the interest bearing

loans in the year 2017 and in respect of payment there is an increase in year 2017.

7

year? How much of such loans have been repaid? How do these amounts compare with the

previous year?

As per the cash flow statement of the company presented for the year ending 2017 it can be

established that the company has raised the cash of $220 million for the interest bearing

borrowings and the repayment made in respect of these loans has been $1994 million in the year

2017 (Wesfarmers, 2017). While comparing these amounts with the previous year figure of 2016

the following data is obtained:

Particulars Amount 2017 ($

million)

Amount 2016 ($

million)

% increase/

decrease

Proceeds from borrowings 220 2360 -91%

Repayment of borrowings 1,994 1,424 40%

It can be seen that there has been a huge decrease in the cash raised form the interest bearing

loans in the year 2017 and in respect of payment there is an increase in year 2017.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

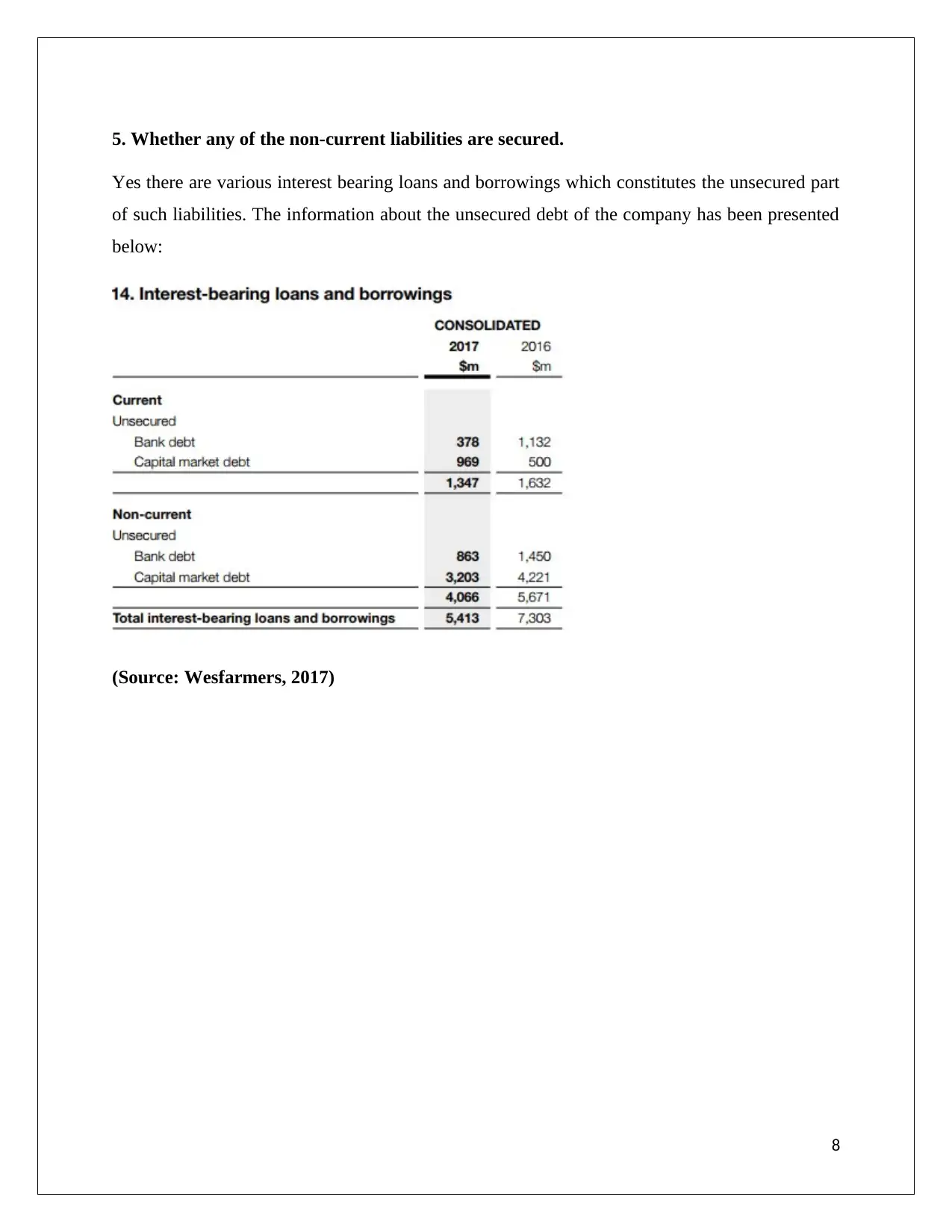

5. Whether any of the non-current liabilities are secured.

Yes there are various interest bearing loans and borrowings which constitutes the unsecured part

of such liabilities. The information about the unsecured debt of the company has been presented

below:

(Source: Wesfarmers, 2017)

8

Yes there are various interest bearing loans and borrowings which constitutes the unsecured part

of such liabilities. The information about the unsecured debt of the company has been presented

below:

(Source: Wesfarmers, 2017)

8

6. Non-current provisions and the meaning.

Yes there do exist the non-current provisions for the company in the year 2017 which

represented the amount of $1511 million. The non-current provisions in respect of the company

will refer to the long term financial obligations of the enterprise which will be due in the future

operations of the enterprise and a reliable estimate can be made about those liabilities in the

present only (Laudon & Traver, 2013).

9

Yes there do exist the non-current provisions for the company in the year 2017 which

represented the amount of $1511 million. The non-current provisions in respect of the company

will refer to the long term financial obligations of the enterprise which will be due in the future

operations of the enterprise and a reliable estimate can be made about those liabilities in the

present only (Laudon & Traver, 2013).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part B:

1. The Woolworth income statement shows a deduction (in brackets) for income tax

expense. Would this expense item be seen in the income statement of a partnership?

By referring to the income tax statement as produced for the year 2017 for Woolworth it can be

seen that the income tax expense amounted to $650.4 million. The income tax expense includes

the current tax as well as tax expense calculated for the deferred tax expenses of the company.

The tax expense for the company will be calculated by considering the consolidated statement of

the financial records and for the same purpose the parent entity along with its various

subsidiaries and associated are considered as consolidated group for tax calculation purposes.

The group has created a tax funding agreement with all its subsidiaries to identify the income tax

expense as a whole and each and every component of the group has agreed to pay their amount

of share as payable for income tax expense concerned with the profits obtained by them

(Mathuva, 2015).

By observing the current rules and regulations and the format adopted by the partnership

enterprise, the income tax expense cannot be seen in the income statement of the partnership

firm. The tax expense for the partnership firm is represented as the corporation tax. It can be seen

that in a partnership firm separate partners have different capital counts which contains the

amount represented as their capital including the profit or loss recognized for them as per their

share of profit and losses in the premiership deed. Similarly on the basis of profits and loss

sharing the taxes calculated for the firm will be allocated among the partners based on the share

of profits and losses contributed by them. Thus it can be analyse that there is no separate income

tax expense mentioned for the overall firm in the income statement of a partnership firm.

(Sutton, et. al., 2015).

10

1. The Woolworth income statement shows a deduction (in brackets) for income tax

expense. Would this expense item be seen in the income statement of a partnership?

By referring to the income tax statement as produced for the year 2017 for Woolworth it can be

seen that the income tax expense amounted to $650.4 million. The income tax expense includes

the current tax as well as tax expense calculated for the deferred tax expenses of the company.

The tax expense for the company will be calculated by considering the consolidated statement of

the financial records and for the same purpose the parent entity along with its various

subsidiaries and associated are considered as consolidated group for tax calculation purposes.

The group has created a tax funding agreement with all its subsidiaries to identify the income tax

expense as a whole and each and every component of the group has agreed to pay their amount

of share as payable for income tax expense concerned with the profits obtained by them

(Mathuva, 2015).

By observing the current rules and regulations and the format adopted by the partnership

enterprise, the income tax expense cannot be seen in the income statement of the partnership

firm. The tax expense for the partnership firm is represented as the corporation tax. It can be seen

that in a partnership firm separate partners have different capital counts which contains the

amount represented as their capital including the profit or loss recognized for them as per their

share of profit and losses in the premiership deed. Similarly on the basis of profits and loss

sharing the taxes calculated for the firm will be allocated among the partners based on the share

of profits and losses contributed by them. Thus it can be analyse that there is no separate income

tax expense mentioned for the overall firm in the income statement of a partnership firm.

(Sutton, et. al., 2015).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. How is the total profit available appropriated and the explanation of allocation of the

total profit available for appropriation in a partnership differ from that shown for

Woolworth Limited.

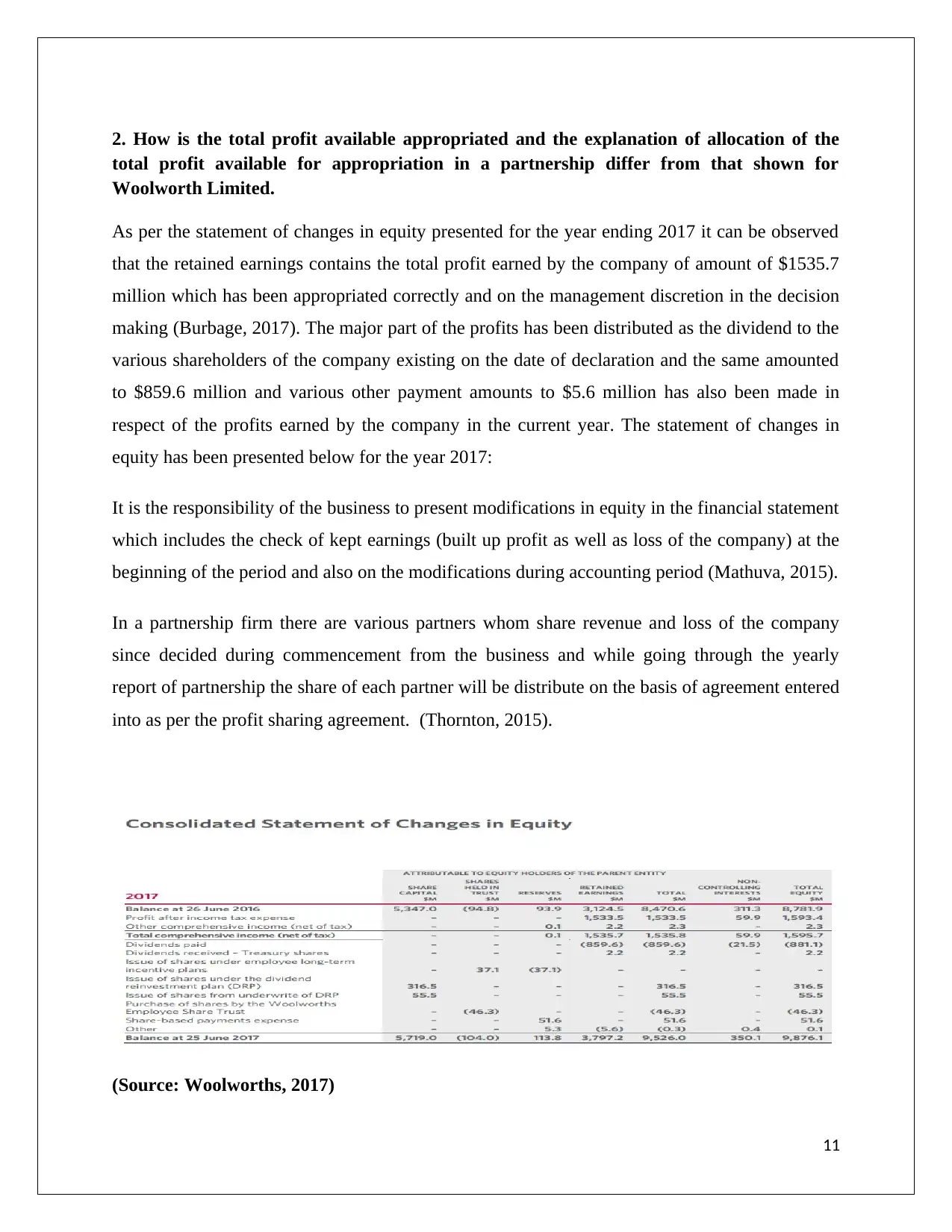

As per the statement of changes in equity presented for the year ending 2017 it can be observed

that the retained earnings contains the total profit earned by the company of amount of $1535.7

million which has been appropriated correctly and on the management discretion in the decision

making (Burbage, 2017). The major part of the profits has been distributed as the dividend to the

various shareholders of the company existing on the date of declaration and the same amounted

to $859.6 million and various other payment amounts to $5.6 million has also been made in

respect of the profits earned by the company in the current year. The statement of changes in

equity has been presented below for the year 2017:

It is the responsibility of the business to present modifications in equity in the financial statement

which includes the check of kept earnings (built up profit as well as loss of the company) at the

beginning of the period and also on the modifications during accounting period (Mathuva, 2015).

In a partnership firm there are various partners whom share revenue and loss of the company

since decided during commencement from the business and while going through the yearly

report of partnership the share of each partner will be distribute on the basis of agreement entered

into as per the profit sharing agreement. (Thornton, 2015).

(Source: Woolworths, 2017)

11

total profit available for appropriation in a partnership differ from that shown for

Woolworth Limited.

As per the statement of changes in equity presented for the year ending 2017 it can be observed

that the retained earnings contains the total profit earned by the company of amount of $1535.7

million which has been appropriated correctly and on the management discretion in the decision

making (Burbage, 2017). The major part of the profits has been distributed as the dividend to the

various shareholders of the company existing on the date of declaration and the same amounted

to $859.6 million and various other payment amounts to $5.6 million has also been made in

respect of the profits earned by the company in the current year. The statement of changes in

equity has been presented below for the year 2017:

It is the responsibility of the business to present modifications in equity in the financial statement

which includes the check of kept earnings (built up profit as well as loss of the company) at the

beginning of the period and also on the modifications during accounting period (Mathuva, 2015).

In a partnership firm there are various partners whom share revenue and loss of the company

since decided during commencement from the business and while going through the yearly

report of partnership the share of each partner will be distribute on the basis of agreement entered

into as per the profit sharing agreement. (Thornton, 2015).

(Source: Woolworths, 2017)

11

3. Issued capital’ of Woolworth and differentiation from that of a typical partnership.

In the balance sheet of company the contributed equity amounted to $5615 million for which the

notes have been presented in the notes to financial statements. The issued share capital as

represented in the financial statement of the company is very simple to understand and it refers to

the capital contributed or the long term source of finance obtained by the shareholders of the

company who has given some amount of money in consideration of the shares issued to them at

the issued share price. The issues share capital includes the issue price of the share as multiplied

with the total number of shares issued for the company. There can be varied number of shares

issued at different share prices which results in different classes of share capital in the company

(Woolworths, 2017).

However in a partnership firm, there are more than one but limited owners included in the capital

structure of the firm. The equity section or portion of the firm is very similar and same in respect

of the equity represented in the sole proprietorship. Instead of issued share capital the capital is

shown for each and every separately in the financial position of the frim so that all the partners

can keep track of their investment in the firm. Each partner thus has a separate capital account

and his share of capital comes in that section only along with the share of profits and losses

(Sutton, et. al., 2015).

12

In the balance sheet of company the contributed equity amounted to $5615 million for which the

notes have been presented in the notes to financial statements. The issued share capital as

represented in the financial statement of the company is very simple to understand and it refers to

the capital contributed or the long term source of finance obtained by the shareholders of the

company who has given some amount of money in consideration of the shares issued to them at

the issued share price. The issues share capital includes the issue price of the share as multiplied

with the total number of shares issued for the company. There can be varied number of shares

issued at different share prices which results in different classes of share capital in the company

(Woolworths, 2017).

However in a partnership firm, there are more than one but limited owners included in the capital

structure of the firm. The equity section or portion of the firm is very similar and same in respect

of the equity represented in the sole proprietorship. Instead of issued share capital the capital is

shown for each and every separately in the financial position of the frim so that all the partners

can keep track of their investment in the firm. Each partner thus has a separate capital account

and his share of capital comes in that section only along with the share of profits and losses

(Sutton, et. al., 2015).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.