Accounting for Management Decisions: Financial Statement Analysis

VerifiedAdded on 2021/05/31

|18

|3150

|21

Report

AI Summary

This report presents a quantitative analysis of the financial statements of Wesfarmers Ltd and Woolworths Ltd. It begins by outlining the methods used to present cash flow statements for both companies, focusing on the direct method. The analysis examines cash flows from operating, investing, and financing activities, drawing data from the companies' financial reports. A comprehensive ratio analysis is conducted, including liquidity, solvency, profitability, and efficiency ratios. The report offers recommendations regarding short-term credit risk, cash resource adequacy, long-term survival, and cash generation from sales revenue. The findings indicate that both companies use the direct method for cash flow presentation, with Wesfarmers Ltd demonstrating a stronger position in net cash generation from operating activities, investing activities, and cash equivalents. Additionally, Wesfarmers Ltd outperforms Woolworths Ltd in profitability, efficiency, short-term liquidity, and solvency ratios.

Running head: ACCOUNTING FOR MANAGEMENT DECISIONS

Accounting for Management Decisions

Name of Student:

Name of University:

Author’s Note:

Accounting for Management Decisions

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR MANAGEMENT DECISIONS

Executive Summary

The discussions of the report have stated about quantitative analysis of financial statement of

Wesfarmers Ltd and Woolworths Ltd. The first section has outlined the method used in depicting

the statement of cash flows for each company. The second section has considered the examining

the information in relation to cash flow from “operating activities, cash flow from investing

activities and cash flow from financing activities retrieved from the Wesfarmers Ltd and

Woolworths Ltd financial reports”. The third section of the study has showed a ratio analysis.

This analysis has computed the liquidity ratio, solvency ratio, profitability ratio and efficiency

ratio. The recommendations are specified with the company having expected better short-term

credit risk, rationale whether both the companies are having adequate cash resources, assessment

of ability to survive in the long term and identifying the company having a better ability of

generating cash from the sales revenue. The overall findings of the discourse have been able to

state that both the company uses direct method of cash flow presentation. However, Wesfarmers

Ltd is clearly in a better positioning in terms of generating “net cash from operating activities,

net cash used in investing activities and for the cash and cash equivalents” in compared to

Woolworths Ltd. In addition to this, Wesfarmers Ltd outperforms Woolworths Ltd. in terms of

“profitability, efficiency, short-term liquidity and solvency ratios”.

Executive Summary

The discussions of the report have stated about quantitative analysis of financial statement of

Wesfarmers Ltd and Woolworths Ltd. The first section has outlined the method used in depicting

the statement of cash flows for each company. The second section has considered the examining

the information in relation to cash flow from “operating activities, cash flow from investing

activities and cash flow from financing activities retrieved from the Wesfarmers Ltd and

Woolworths Ltd financial reports”. The third section of the study has showed a ratio analysis.

This analysis has computed the liquidity ratio, solvency ratio, profitability ratio and efficiency

ratio. The recommendations are specified with the company having expected better short-term

credit risk, rationale whether both the companies are having adequate cash resources, assessment

of ability to survive in the long term and identifying the company having a better ability of

generating cash from the sales revenue. The overall findings of the discourse have been able to

state that both the company uses direct method of cash flow presentation. However, Wesfarmers

Ltd is clearly in a better positioning in terms of generating “net cash from operating activities,

net cash used in investing activities and for the cash and cash equivalents” in compared to

Woolworths Ltd. In addition to this, Wesfarmers Ltd outperforms Woolworths Ltd. in terms of

“profitability, efficiency, short-term liquidity and solvency ratios”.

2ACCOUNTING FOR MANAGEMENT DECISIONS

Table of Contents

Introduction......................................................................................................................................3

Method used in presenting the statement of cash flows for Wesfarmers Ltd..................................3

Method used in presenting the statement of cash flows for Woolworths Ltd.................................6

Examining the information in relation to cash flow for Wesfarmers Ltd........................................8

Examining the information in relation to cash flow for Woolworths Ltd.......................................8

Ratio analysis of Wesfarmers Ltd and Woolworths Ltd.................................................................9

Conclusions and recommendation.................................................................................................16

References......................................................................................................................................17

Table of Contents

Introduction......................................................................................................................................3

Method used in presenting the statement of cash flows for Wesfarmers Ltd..................................3

Method used in presenting the statement of cash flows for Woolworths Ltd.................................6

Examining the information in relation to cash flow for Wesfarmers Ltd........................................8

Examining the information in relation to cash flow for Woolworths Ltd.......................................8

Ratio analysis of Wesfarmers Ltd and Woolworths Ltd.................................................................9

Conclusions and recommendation.................................................................................................16

References......................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR MANAGEMENT DECISIONS

Introduction

The report aims to perform quantitative analysis to interpret the financial statement of

Wesfarmers Ltd and Woolworths Ltd. The first section of the report will outline the method used

in depicting the cash flow statement for each corporation. The second section will consider the

examining the evidence in relation to cash flow from “operating activities, cash flow from

investing activities and cash flow from financing activities retrieved from the Wesfarmers Ltd

and Woolworths Ltd financial reports”. The third section of the study will conduct a ratio

analysis. This analysis would include computation for measuring the “liquidity ratio, solvency

ratio, profitability ratio and efficiency ratio”. The recommendations will be stated with the

company having expected better short-term credit risk, rationale whether both the companies are

having adequate cash resources, assessment of ability to survive in the long term and identifying

the company having a better ability of generating cash from the sales revenue (Adedeji, 2014).

Method used in presenting the statement of cash flows for Wesfarmers Ltd

In general, the presentation of financial statement is based on segregating the statements into

parts- “balance sheet, income statement, and cash flow statement”. In addition to this, the “cash

flow statement” comprises of three sections including “cash flow from operating (CFO or OCF),

financing, and investing activities”. The use of indirect method involves computation of cash

flows from “accrual accounting information” and starts with “net income value”. The net income

is then adjusted for the various types of changes in assets and liabilities by adding or deducting

from net “income to derive the operating cash flow”. In the direct method the cash flow

statement list is prepared as per cash receipts and payments made during a period of business

operations. The cash flows are subtracted from the “cash inflows” for calculating the “net cash

flow” from “operating activities” (Fitri, Hosen, & Muhari, 2016).

Based on the depictions made from the financial statement of Wesfarmers Ltd it has been

seen that the company uses direct method of cash flows. This is evident with listing the cash

flows from operating activities, investing activities and financing activities during the year and

calculating the “net cash flow from operating activities” before the cash from “investing and

financing activities” are computed.

Introduction

The report aims to perform quantitative analysis to interpret the financial statement of

Wesfarmers Ltd and Woolworths Ltd. The first section of the report will outline the method used

in depicting the cash flow statement for each corporation. The second section will consider the

examining the evidence in relation to cash flow from “operating activities, cash flow from

investing activities and cash flow from financing activities retrieved from the Wesfarmers Ltd

and Woolworths Ltd financial reports”. The third section of the study will conduct a ratio

analysis. This analysis would include computation for measuring the “liquidity ratio, solvency

ratio, profitability ratio and efficiency ratio”. The recommendations will be stated with the

company having expected better short-term credit risk, rationale whether both the companies are

having adequate cash resources, assessment of ability to survive in the long term and identifying

the company having a better ability of generating cash from the sales revenue (Adedeji, 2014).

Method used in presenting the statement of cash flows for Wesfarmers Ltd

In general, the presentation of financial statement is based on segregating the statements into

parts- “balance sheet, income statement, and cash flow statement”. In addition to this, the “cash

flow statement” comprises of three sections including “cash flow from operating (CFO or OCF),

financing, and investing activities”. The use of indirect method involves computation of cash

flows from “accrual accounting information” and starts with “net income value”. The net income

is then adjusted for the various types of changes in assets and liabilities by adding or deducting

from net “income to derive the operating cash flow”. In the direct method the cash flow

statement list is prepared as per cash receipts and payments made during a period of business

operations. The cash flows are subtracted from the “cash inflows” for calculating the “net cash

flow” from “operating activities” (Fitri, Hosen, & Muhari, 2016).

Based on the depictions made from the financial statement of Wesfarmers Ltd it has been

seen that the company uses direct method of cash flows. This is evident with listing the cash

flows from operating activities, investing activities and financing activities during the year and

calculating the “net cash flow from operating activities” before the cash from “investing and

financing activities” are computed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR MANAGEMENT DECISIONS

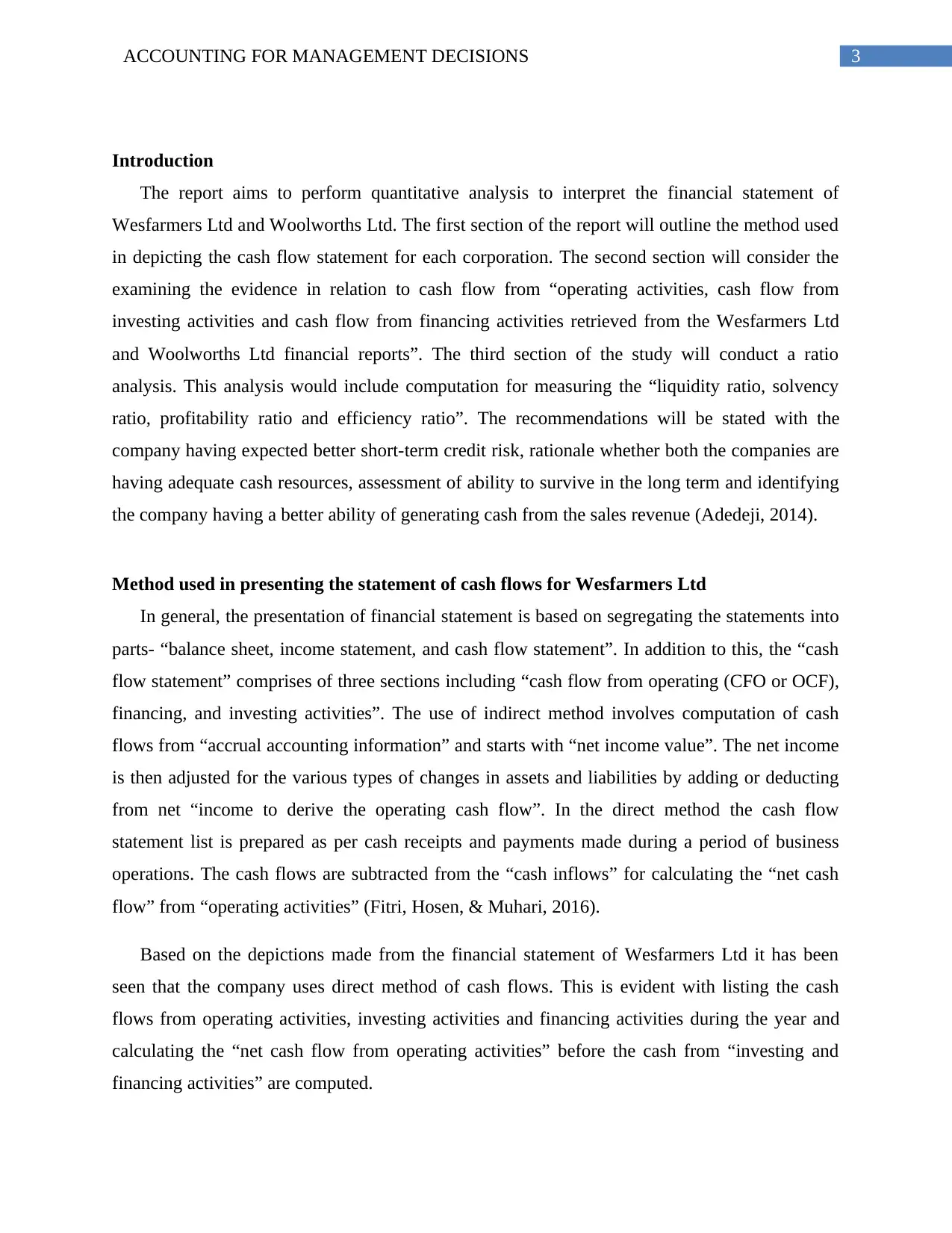

Figure: Direct method of cash flows used by Wesfarmers Limited

(Source: Wesfarmers.com.au, 2018)

As the company uses direct method, the notes to the financial statements has included the

accrual accounting information, which is evident with net profit of $ 2873 million in 2017. The

net income has been further adjusted for changes in assets such as receivables, inventories,

prepayments, deferred tax assets and other assets. Similarly, the adjustment for the

increase/decrease in liabilities is accounted with items such as current tax payable, provisions,

other liabilities, trade and other payables (Qi et al., 2015). The notes to the financial statement

for appropriate reconciliation of the cash flows for Wesfarmers Ltd. has been shown below as

follows:

Figure: Direct method of cash flows used by Wesfarmers Limited

(Source: Wesfarmers.com.au, 2018)

As the company uses direct method, the notes to the financial statements has included the

accrual accounting information, which is evident with net profit of $ 2873 million in 2017. The

net income has been further adjusted for changes in assets such as receivables, inventories,

prepayments, deferred tax assets and other assets. Similarly, the adjustment for the

increase/decrease in liabilities is accounted with items such as current tax payable, provisions,

other liabilities, trade and other payables (Qi et al., 2015). The notes to the financial statement

for appropriate reconciliation of the cash flows for Wesfarmers Ltd. has been shown below as

follows:

5ACCOUNTING FOR MANAGEMENT DECISIONS

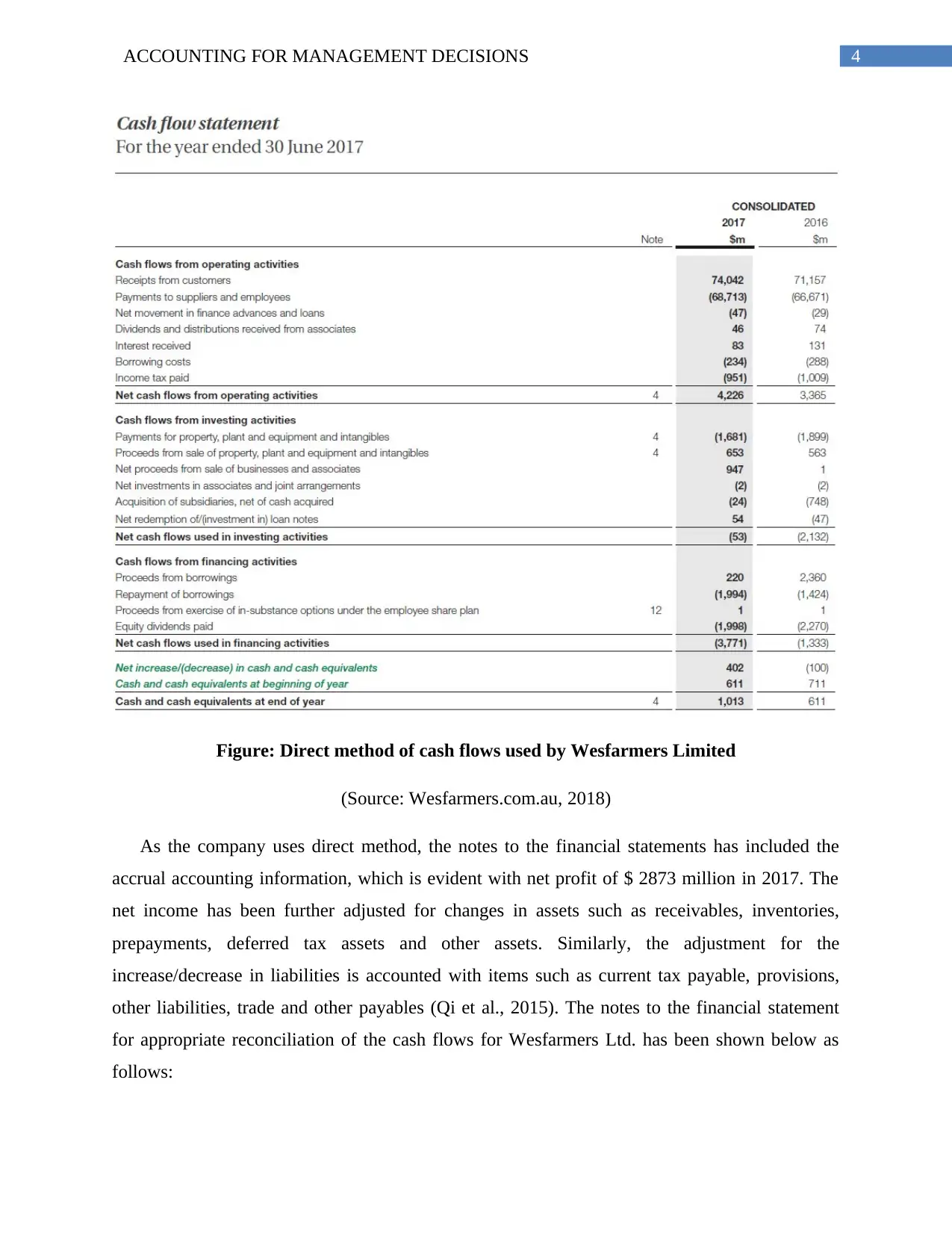

Figure: Notes to the financial statement for direct method used by Wesfarmers Limited

(Source: Wesfarmers.com.au, 2018)

Figure: Notes to the financial statement for direct method used by Wesfarmers Limited

(Source: Wesfarmers.com.au, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR MANAGEMENT DECISIONS

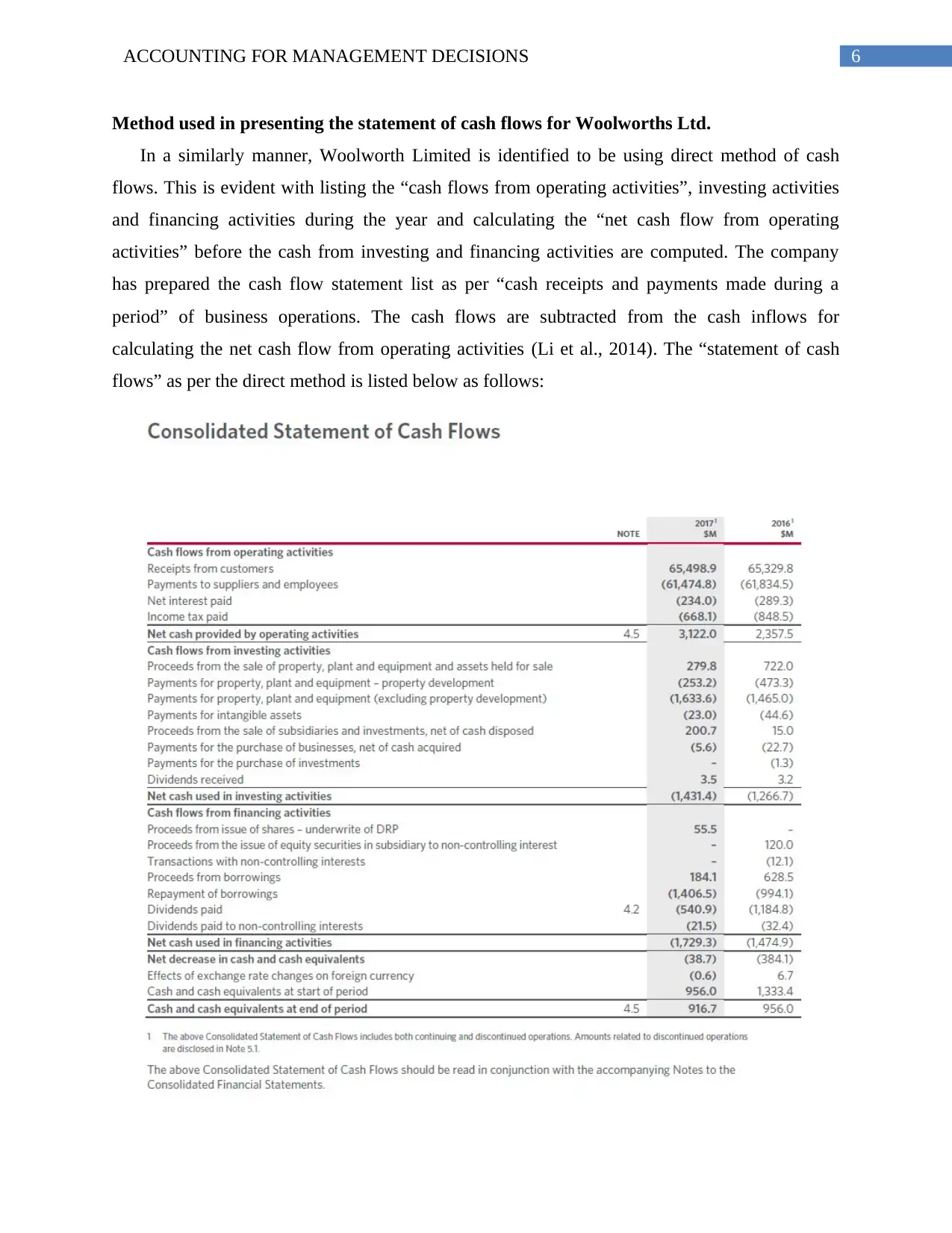

Method used in presenting the statement of cash flows for Woolworths Ltd.

In a similarly manner, Woolworth Limited is identified to be using direct method of cash

flows. This is evident with listing the “cash flows from operating activities”, investing activities

and financing activities during the year and calculating the “net cash flow from operating

activities” before the cash from investing and financing activities are computed. The company

has prepared the cash flow statement list as per “cash receipts and payments made during a

period” of business operations. The cash flows are subtracted from the cash inflows for

calculating the net cash flow from operating activities (Li et al., 2014). The “statement of cash

flows” as per the direct method is listed below as follows:

Method used in presenting the statement of cash flows for Woolworths Ltd.

In a similarly manner, Woolworth Limited is identified to be using direct method of cash

flows. This is evident with listing the “cash flows from operating activities”, investing activities

and financing activities during the year and calculating the “net cash flow from operating

activities” before the cash from investing and financing activities are computed. The company

has prepared the cash flow statement list as per “cash receipts and payments made during a

period” of business operations. The cash flows are subtracted from the cash inflows for

calculating the net cash flow from operating activities (Li et al., 2014). The “statement of cash

flows” as per the direct method is listed below as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR MANAGEMENT DECISIONS

Figure: Direct method of cash flows used by Woolworths Limited

(Source: Woolworthsgroup.com.au, 2018)

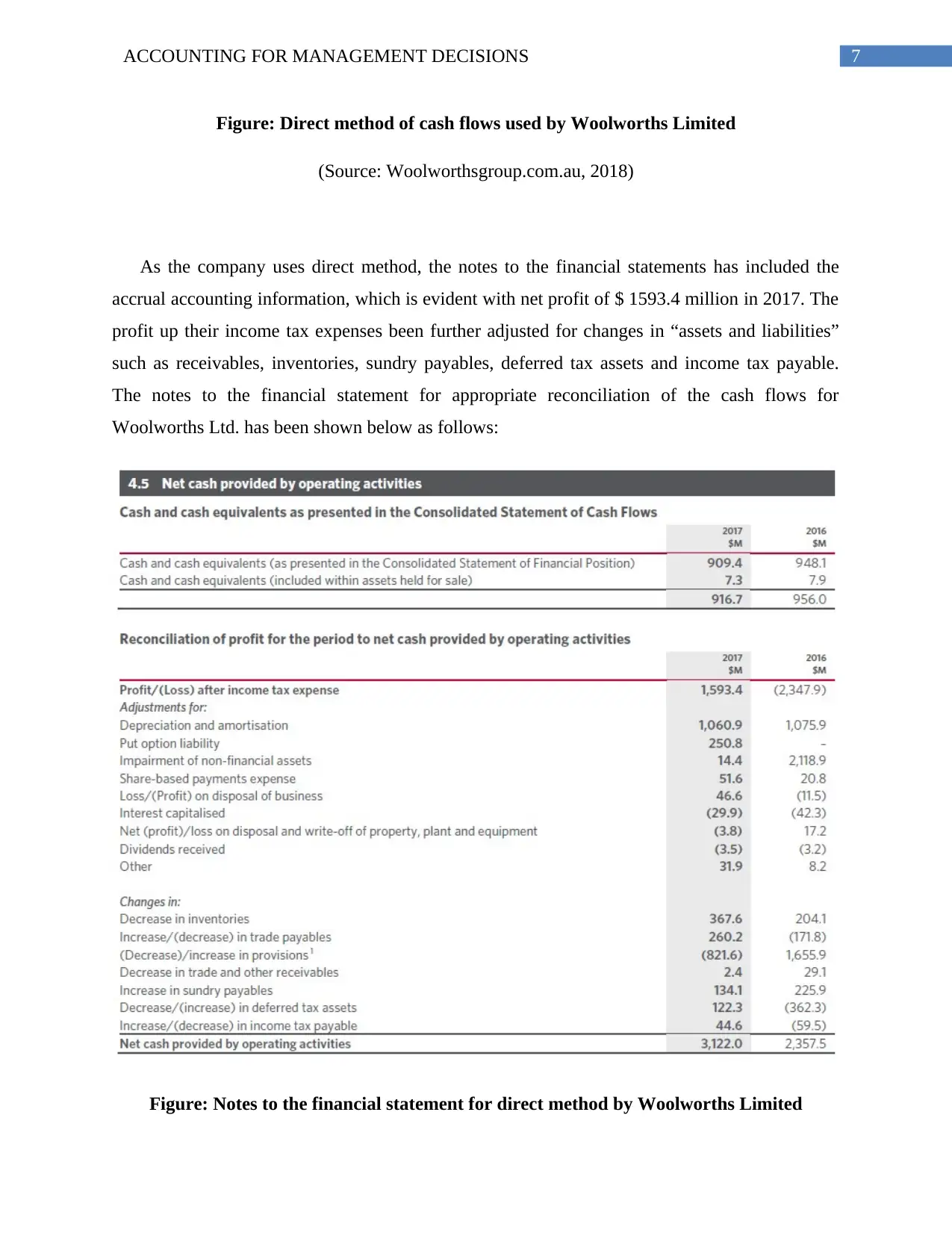

As the company uses direct method, the notes to the financial statements has included the

accrual accounting information, which is evident with net profit of $ 1593.4 million in 2017. The

profit up their income tax expenses been further adjusted for changes in “assets and liabilities”

such as receivables, inventories, sundry payables, deferred tax assets and income tax payable.

The notes to the financial statement for appropriate reconciliation of the cash flows for

Woolworths Ltd. has been shown below as follows:

Figure: Notes to the financial statement for direct method by Woolworths Limited

Figure: Direct method of cash flows used by Woolworths Limited

(Source: Woolworthsgroup.com.au, 2018)

As the company uses direct method, the notes to the financial statements has included the

accrual accounting information, which is evident with net profit of $ 1593.4 million in 2017. The

profit up their income tax expenses been further adjusted for changes in “assets and liabilities”

such as receivables, inventories, sundry payables, deferred tax assets and income tax payable.

The notes to the financial statement for appropriate reconciliation of the cash flows for

Woolworths Ltd. has been shown below as follows:

Figure: Notes to the financial statement for direct method by Woolworths Limited

8ACCOUNTING FOR MANAGEMENT DECISIONS

(Source: Woolworthsgroup.com.au, 2018)

Examining the information in relation to cash flow for Wesfarmers Ltd

The depictions made from the financial statement of Wesfarmers Limited has revealed that

there had been a significant increase in “net cash from operating activities, net cash used in

investing activities and for the cash and cash equivalents” at the end of the year. Despite of the

areas of the aforementioned increases, the company has suffered in a major way as per “net cash

flows used in financing activities”.

The increase in “net cash flows from the operating activities” is evident with $ 4226 million

in 2017 from $ 3365 million in 2016. The most noted areas of significant increase can be seen

with receipts from customers ($ 74,042 million in 2017 from $ 71,157 million in 2016). The “net

cash flows used in the investing activities” have increased from $ (2132) million in 2016 to $

(53) million in 2017. This is evident with payments for “property plant and equipment and

intangibles” reducing from $ (1899) million in 2016 to $ (1681) million in 2017.

In addition to this, the “net proceeds from sale of business and Associates” has increased

from $ 1 million in 2016 to $ 947 million in 2017. Another significant area of increase in the

investing activities is observed with “increase in acquisition of subsidiaries, net of cash acquired”

from $ (748) million in 2016 to $ (74) million in 2017. The decrease in the “net cash flows used

in financing activities” is evident with $ (1333) in 2016 to $ (3771) in 2017. The proceeds from

borrowing have decreased from $ 2360 million in 2016 to $ 220 million in 2017. Additionally,

the repayment of borrowings has increased from “$ (1424) million in 2016 to $ (1994)” million

in 2017. The aforementioned depictions show that the company has used considerable amount of

cash for paying its borrower and unable to keep up with the proceeds from borrowings. The

overall increase “in cash and cash equivalents” at the end of the year is identified with $ 611

million in 2016 to $ 1013 million in 2017. The net increase in the cash and cash equivalent has

been recognized with $ (100) million in 2016 to $ 402 million in 2017 (Kapelevich, 2014).

Examining the information in relation to cash flow for Woolworths Ltd.

On examining the consolidated statement of cash flows for Woolworth Limited it has

been observed that there is a considerable increase in the “net cash provided by operating

(Source: Woolworthsgroup.com.au, 2018)

Examining the information in relation to cash flow for Wesfarmers Ltd

The depictions made from the financial statement of Wesfarmers Limited has revealed that

there had been a significant increase in “net cash from operating activities, net cash used in

investing activities and for the cash and cash equivalents” at the end of the year. Despite of the

areas of the aforementioned increases, the company has suffered in a major way as per “net cash

flows used in financing activities”.

The increase in “net cash flows from the operating activities” is evident with $ 4226 million

in 2017 from $ 3365 million in 2016. The most noted areas of significant increase can be seen

with receipts from customers ($ 74,042 million in 2017 from $ 71,157 million in 2016). The “net

cash flows used in the investing activities” have increased from $ (2132) million in 2016 to $

(53) million in 2017. This is evident with payments for “property plant and equipment and

intangibles” reducing from $ (1899) million in 2016 to $ (1681) million in 2017.

In addition to this, the “net proceeds from sale of business and Associates” has increased

from $ 1 million in 2016 to $ 947 million in 2017. Another significant area of increase in the

investing activities is observed with “increase in acquisition of subsidiaries, net of cash acquired”

from $ (748) million in 2016 to $ (74) million in 2017. The decrease in the “net cash flows used

in financing activities” is evident with $ (1333) in 2016 to $ (3771) in 2017. The proceeds from

borrowing have decreased from $ 2360 million in 2016 to $ 220 million in 2017. Additionally,

the repayment of borrowings has increased from “$ (1424) million in 2016 to $ (1994)” million

in 2017. The aforementioned depictions show that the company has used considerable amount of

cash for paying its borrower and unable to keep up with the proceeds from borrowings. The

overall increase “in cash and cash equivalents” at the end of the year is identified with $ 611

million in 2016 to $ 1013 million in 2017. The net increase in the cash and cash equivalent has

been recognized with $ (100) million in 2016 to $ 402 million in 2017 (Kapelevich, 2014).

Examining the information in relation to cash flow for Woolworths Ltd.

On examining the consolidated statement of cash flows for Woolworth Limited it has

been observed that there is a considerable increase in the “net cash provided by operating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR MANAGEMENT DECISIONS

activities but decreasing area of net cash used in investing activities, net cash used in financing

activities and net cash and cash equivalents at the end of period”. The increase in the “net cash

provided by operating activities” is evident with an increase of $ 3122 million in 2017 to $

2357.5 million in 2018. The overall increase in this section is because of increase in receipts

from customers and decrease in net interest paid on income tax paid. It has been discerned that

the income tax payments have reduced from $ (848.5) million in 2016 to $ (668.1) million in

2017. The decrease in the “net cash used in investing activities” is evident with $ (1266.7)

million in 2016 to $ (1431.4) in 2017. It needs to be noted that the reason for such a decrease is

identified with decreasing “Proceeds from the sale of property, plant and equipment and assets

held for sale” from $ 722 million in 2016 to $ 279.8 million in 2017. In addition to this,

“Payments for property, plant and equipment – property development” has “decreased from

(473.3) million in 2016 to (253.2)” million in 2017. Additionally, “Payments for property, plant

and equipment (excluding property development)” has gone down from $ (1465) million in 2016

to $ (1633.6) million in 2017 (Templeton et al., 2014).

The decreasing “net cash used in financing activities” is identified with $ (1474.9)

million in 2016 to (1729.3) million in 2017. The proceeds from borrowings have reduced on

from $ 628.5 million in 2016 to $ 184.1 million in 2017. In addition to this, there has been a

considerable amount of decrease in “Repayment of borrowings” which has been evident with $

(994.1) million in 2016 to $ (1406.5) million in 2017. The decrease in “Cash and cash

equivalents at end of period” can be identified with $ 956 million in 2016 to $ 916.7 million in

2017. The main reason for this decrease is due to “Cash and cash equivalents at start of period”

which was $ 1333.4 in 2016 and $ 956 in 2017.

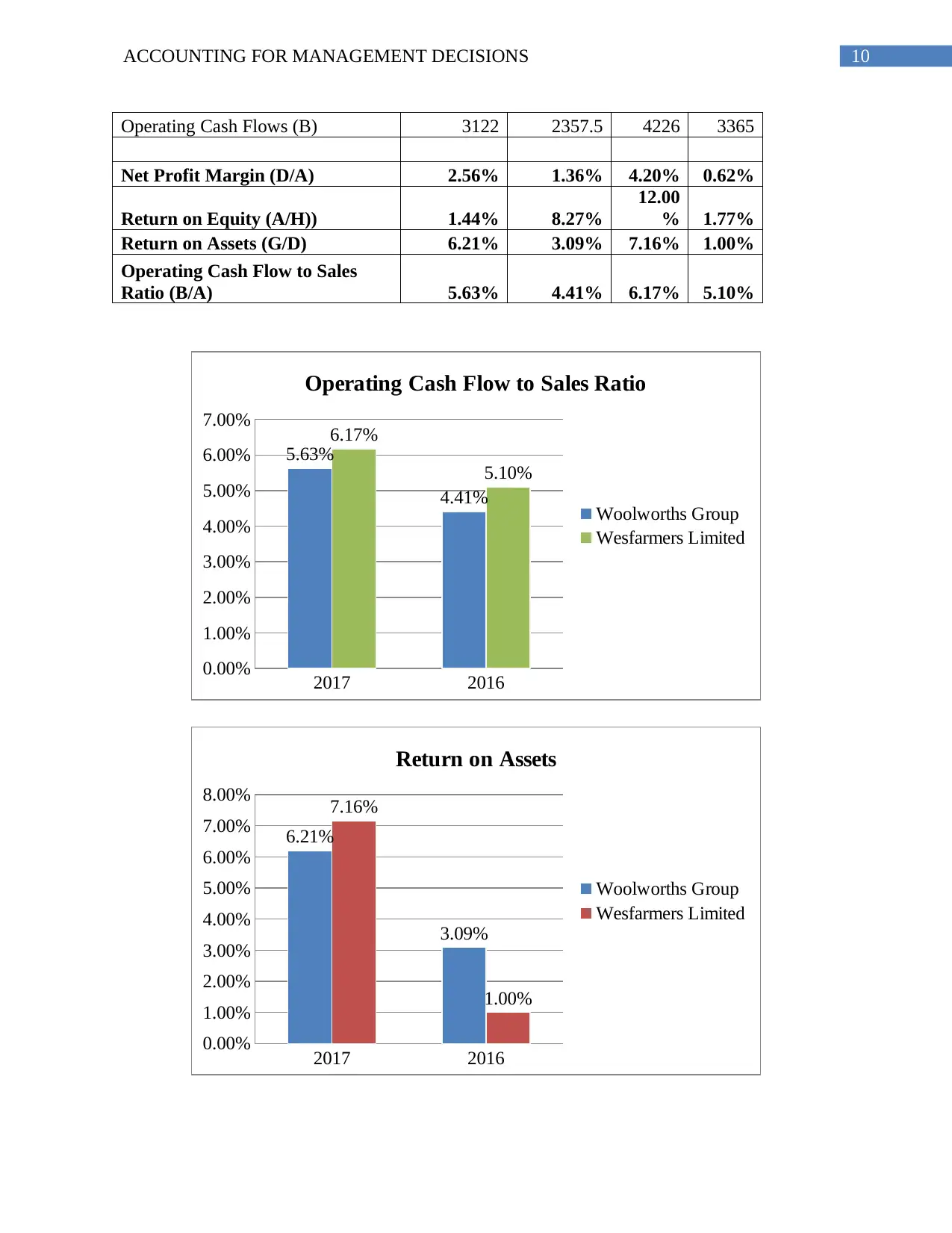

Ratio analysis of Wesfarmers Ltd and Woolworths Ltd.

Profitability Ratio Analysis: -

Woolworths Group

Wesfarmers

Limited

Particulars 2017 2016 2017 2016

Revenue (A) 55475 53473 68444 65981

Net Profit/Loss after Tax (D) 1422.1 726.3 2873 407

Ordinary Equity(H) 98761.5 8781.9 23941 22949

Total Assets (G) 22915.8 23502.2 40115 40783

activities but decreasing area of net cash used in investing activities, net cash used in financing

activities and net cash and cash equivalents at the end of period”. The increase in the “net cash

provided by operating activities” is evident with an increase of $ 3122 million in 2017 to $

2357.5 million in 2018. The overall increase in this section is because of increase in receipts

from customers and decrease in net interest paid on income tax paid. It has been discerned that

the income tax payments have reduced from $ (848.5) million in 2016 to $ (668.1) million in

2017. The decrease in the “net cash used in investing activities” is evident with $ (1266.7)

million in 2016 to $ (1431.4) in 2017. It needs to be noted that the reason for such a decrease is

identified with decreasing “Proceeds from the sale of property, plant and equipment and assets

held for sale” from $ 722 million in 2016 to $ 279.8 million in 2017. In addition to this,

“Payments for property, plant and equipment – property development” has “decreased from

(473.3) million in 2016 to (253.2)” million in 2017. Additionally, “Payments for property, plant

and equipment (excluding property development)” has gone down from $ (1465) million in 2016

to $ (1633.6) million in 2017 (Templeton et al., 2014).

The decreasing “net cash used in financing activities” is identified with $ (1474.9)

million in 2016 to (1729.3) million in 2017. The proceeds from borrowings have reduced on

from $ 628.5 million in 2016 to $ 184.1 million in 2017. In addition to this, there has been a

considerable amount of decrease in “Repayment of borrowings” which has been evident with $

(994.1) million in 2016 to $ (1406.5) million in 2017. The decrease in “Cash and cash

equivalents at end of period” can be identified with $ 956 million in 2016 to $ 916.7 million in

2017. The main reason for this decrease is due to “Cash and cash equivalents at start of period”

which was $ 1333.4 in 2016 and $ 956 in 2017.

Ratio analysis of Wesfarmers Ltd and Woolworths Ltd.

Profitability Ratio Analysis: -

Woolworths Group

Wesfarmers

Limited

Particulars 2017 2016 2017 2016

Revenue (A) 55475 53473 68444 65981

Net Profit/Loss after Tax (D) 1422.1 726.3 2873 407

Ordinary Equity(H) 98761.5 8781.9 23941 22949

Total Assets (G) 22915.8 23502.2 40115 40783

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR MANAGEMENT DECISIONS

Operating Cash Flows (B) 3122 2357.5 4226 3365

Net Profit Margin (D/A) 2.56% 1.36% 4.20% 0.62%

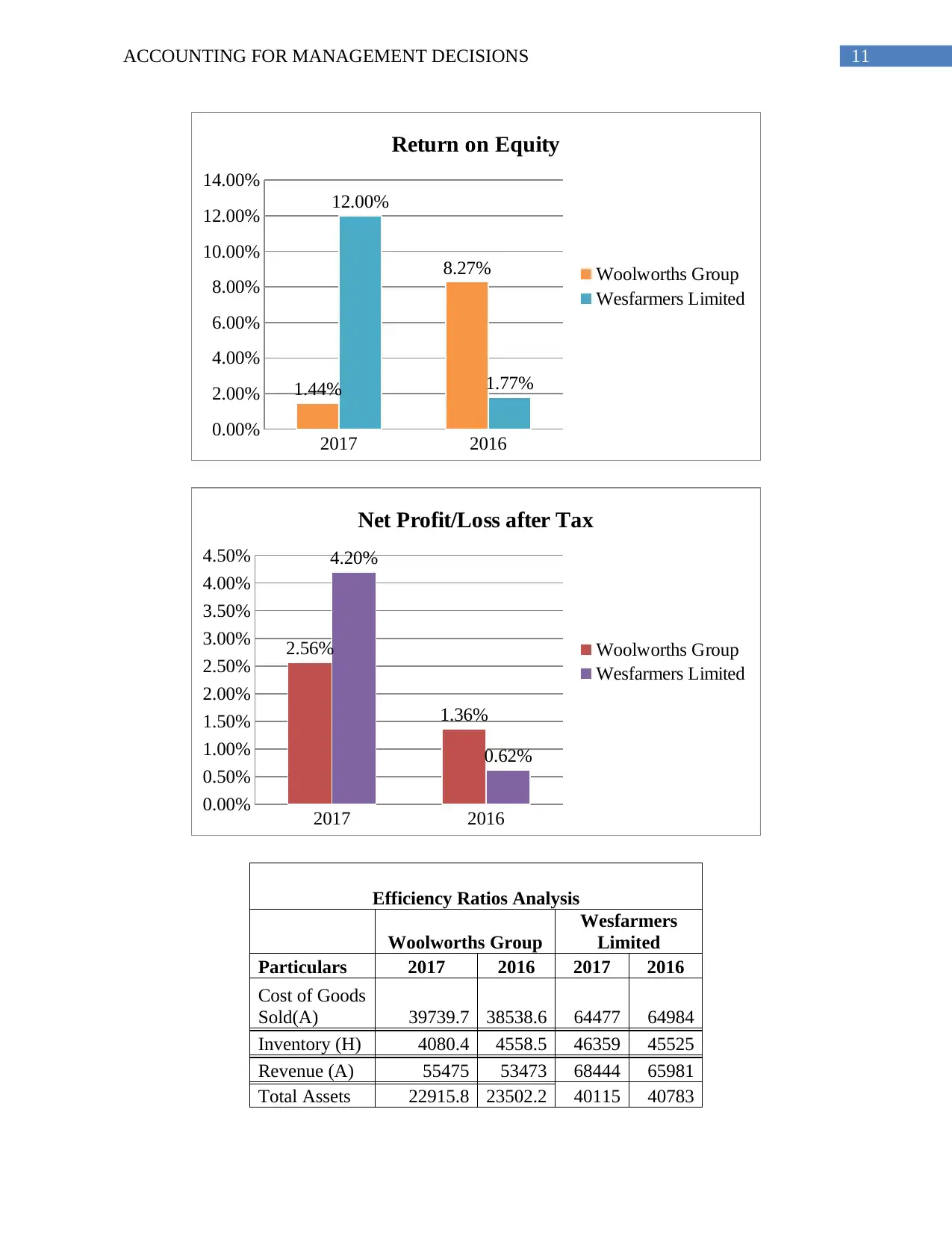

Return on Equity (A/H)) 1.44% 8.27%

12.00

% 1.77%

Return on Assets (G/D) 6.21% 3.09% 7.16% 1.00%

Operating Cash Flow to Sales

Ratio (B/A) 5.63% 4.41% 6.17% 5.10%

2017 2016

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

5.63%

4.41%

6.17%

5.10%

Operating Cash Flow to Sales Ratio

Woolworths Group

Wesfarmers Limited

2017 2016

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

6.21%

3.09%

7.16%

1.00%

Return on Assets

Woolworths Group

Wesfarmers Limited

Operating Cash Flows (B) 3122 2357.5 4226 3365

Net Profit Margin (D/A) 2.56% 1.36% 4.20% 0.62%

Return on Equity (A/H)) 1.44% 8.27%

12.00

% 1.77%

Return on Assets (G/D) 6.21% 3.09% 7.16% 1.00%

Operating Cash Flow to Sales

Ratio (B/A) 5.63% 4.41% 6.17% 5.10%

2017 2016

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

5.63%

4.41%

6.17%

5.10%

Operating Cash Flow to Sales Ratio

Woolworths Group

Wesfarmers Limited

2017 2016

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

6.21%

3.09%

7.16%

1.00%

Return on Assets

Woolworths Group

Wesfarmers Limited

11ACCOUNTING FOR MANAGEMENT DECISIONS

2017 2016

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

1.44%

8.27%

12.00%

1.77%

Return on Equity

Woolworths Group

Wesfarmers Limited

2017 2016

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

2.56%

1.36%

4.20%

0.62%

Net Profit/Loss after Tax

Woolworths Group

Wesfarmers Limited

Efficiency Ratios Analysis

Woolworths Group

Wesfarmers

Limited

Particulars 2017 2016 2017 2016

Cost of Goods

Sold(A) 39739.7 38538.6 64477 64984

Inventory (H) 4080.4 4558.5 46359 45525

Revenue (A) 55475 53473 68444 65981

Total Assets 22915.8 23502.2 40115 40783

2017 2016

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

1.44%

8.27%

12.00%

1.77%

Return on Equity

Woolworths Group

Wesfarmers Limited

2017 2016

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

2.56%

1.36%

4.20%

0.62%

Net Profit/Loss after Tax

Woolworths Group

Wesfarmers Limited

Efficiency Ratios Analysis

Woolworths Group

Wesfarmers

Limited

Particulars 2017 2016 2017 2016

Cost of Goods

Sold(A) 39739.7 38538.6 64477 64984

Inventory (H) 4080.4 4558.5 46359 45525

Revenue (A) 55475 53473 68444 65981

Total Assets 22915.8 23502.2 40115 40783

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.