West Bridgford Pension Fund: Portfolio Strategy & Structure (2018)

VerifiedAdded on 2023/03/21

|13

|3442

|98

Report

AI Summary

This report provides a comprehensive analysis of the West Bridgford Pension Fund portfolio, valued at £2.6 billion as of December 2018. The portfolio consists of offices, retail, industrial, hotels, residential properties, and cash, with a significant portion invested in non-UK assets. The report addresses the trustees' request for advice on the future structure and strategy of the portfolio over the next five years, focusing on sector and geographical distribution. It considers the current state of the European property market, identifies potential opportunities in different geographic regions and sectors like logistics in Southern Europe and residential properties in Berlin, and evaluates the risks and uncertainties associated with various investment options. The report also emphasizes the importance of responsible property management and strategic decision-making to meet the firm's objectives, including achieving a net inflow of £200 million and outperforming the IPD local authority pension fund performance.

Real Estate Investment 1

REAL ESTATE INVESTMENT

By [Name]

Course

Professor’s Name

Institution

Location of Institution

Date

REAL ESTATE INVESTMENT

By [Name]

Course

Professor’s Name

Institution

Location of Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Real Estate Investment 2

Overview

The current state of the European Property Market when compared to the overall

global performance index overs a variety of real estate investment options with promising

positive returns. However, it needs a good approach when selecting the type of market as

offered by the giant macroeconomic portrait, the trends, and other logistic sectors that bid for

a favorable environment for investment. Like, the past cases have shown proliferation

concerns in the UK, but 2018financial predictions show a promising overall growth level

marked at 1.3% in the UK market but still with increased uncertainties (BNB Paribas Real

Estate 2019). The same inefficiency applies to the Eurozone, especially considering the

reduced foreign trading that has affected the entire real estate market operations. This

examination will review the current company portfolio with other issues identified in the

sector, geographic regions, and offer an opinion on strategized procedures that will best work

for the company.

Sector Distribution

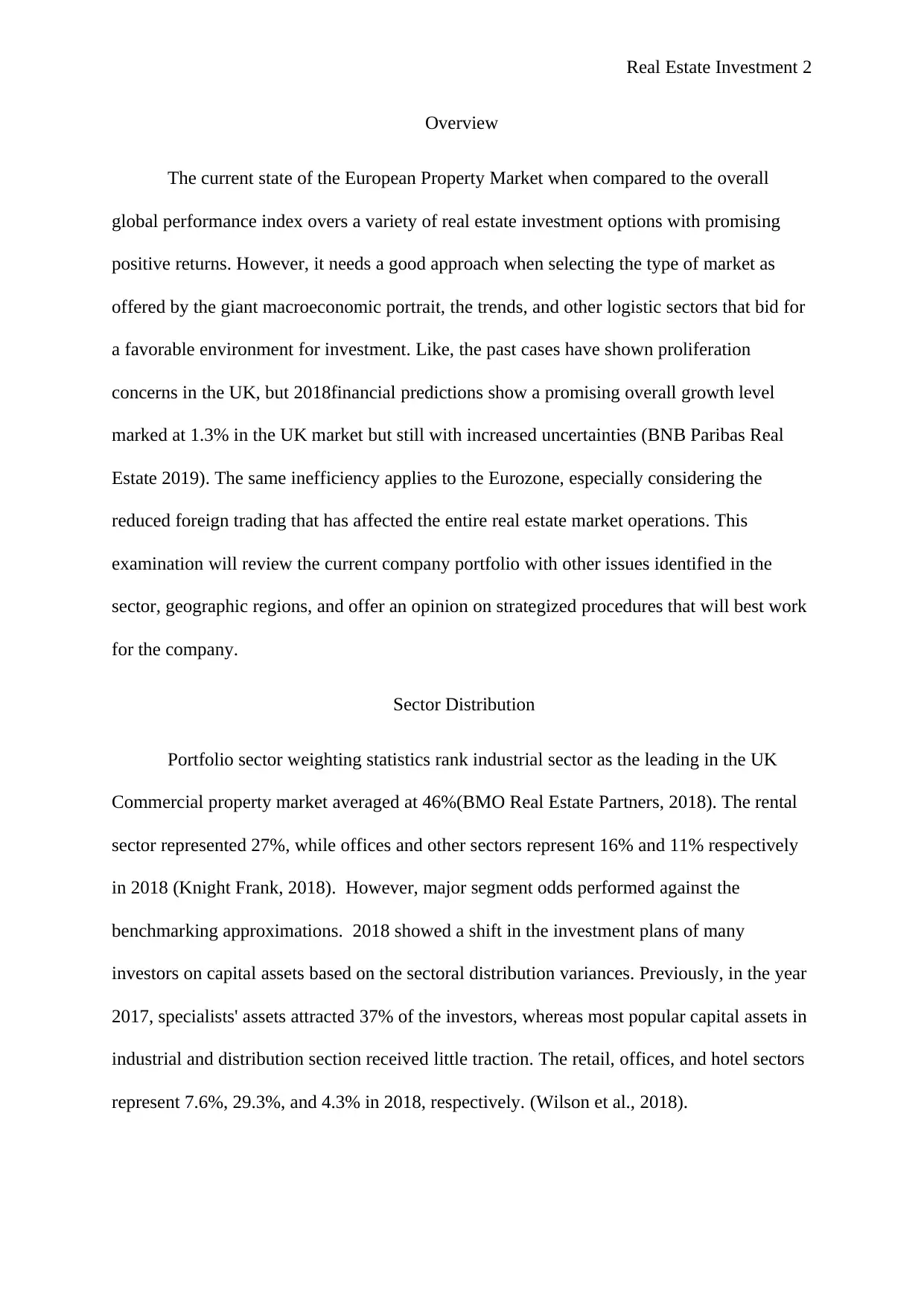

Portfolio sector weighting statistics rank industrial sector as the leading in the UK

Commercial property market averaged at 46%(BMO Real Estate Partners, 2018). The rental

sector represented 27%, while offices and other sectors represent 16% and 11% respectively

in 2018 (Knight Frank, 2018). However, major segment odds performed against the

benchmarking approximations. 2018 showed a shift in the investment plans of many

investors on capital assets based on the sectoral distribution variances. Previously, in the year

2017, specialists' assets attracted 37% of the investors, whereas most popular capital assets in

industrial and distribution section received little traction. The retail, offices, and hotel sectors

represent 7.6%, 29.3%, and 4.3% in 2018, respectively. (Wilson et al., 2018).

Overview

The current state of the European Property Market when compared to the overall

global performance index overs a variety of real estate investment options with promising

positive returns. However, it needs a good approach when selecting the type of market as

offered by the giant macroeconomic portrait, the trends, and other logistic sectors that bid for

a favorable environment for investment. Like, the past cases have shown proliferation

concerns in the UK, but 2018financial predictions show a promising overall growth level

marked at 1.3% in the UK market but still with increased uncertainties (BNB Paribas Real

Estate 2019). The same inefficiency applies to the Eurozone, especially considering the

reduced foreign trading that has affected the entire real estate market operations. This

examination will review the current company portfolio with other issues identified in the

sector, geographic regions, and offer an opinion on strategized procedures that will best work

for the company.

Sector Distribution

Portfolio sector weighting statistics rank industrial sector as the leading in the UK

Commercial property market averaged at 46%(BMO Real Estate Partners, 2018). The rental

sector represented 27%, while offices and other sectors represent 16% and 11% respectively

in 2018 (Knight Frank, 2018). However, major segment odds performed against the

benchmarking approximations. 2018 showed a shift in the investment plans of many

investors on capital assets based on the sectoral distribution variances. Previously, in the year

2017, specialists' assets attracted 37% of the investors, whereas most popular capital assets in

industrial and distribution section received little traction. The retail, offices, and hotel sectors

represent 7.6%, 29.3%, and 4.3% in 2018, respectively. (Wilson et al., 2018).

Real Estate Investment 3

Source: Wilson, et al., 2018)

Other cities in other European regions showed varying yields as attached to three

primary sectors namely retail, logistics and office, Based on the current investment portfolio

plan identified with the company, Berlin, Paris, Warsaw and Milan office prime yield was

2.75%, 3%,4.75% and 3.40% (Wilson et al. 2018). The rental portfolio, which included the

company non-UK shopping centers, represented a prime yield of 3.5% in Barcelona ( PWC

2018). The average performance of each sectoral formation as represented by the yield value

and price variances as provided by each sectoral distribution proves the potential of

improvement in different megacities in Europe and the UK.

The current investment plan of the company has included other major sectoral

segments that perform better in megacities in the UK but again debarred the cities and other

sectors that also perform better. The logistics lead in potential opportunities identified to

include critical cities in southern Europe and significant transport corridors. The effect comes

with the double-digit commerce growth that influenced the variances of sectoral property

prices in the year 2018; thus, the shifts in the investments plans of many investors (Williams,

2018). The potential of investment in different sectors may require the company to include

an alternating investment plan that will need to increase portfolios in non-UK regions. The

Source: Wilson, et al., 2018)

Other cities in other European regions showed varying yields as attached to three

primary sectors namely retail, logistics and office, Based on the current investment portfolio

plan identified with the company, Berlin, Paris, Warsaw and Milan office prime yield was

2.75%, 3%,4.75% and 3.40% (Wilson et al. 2018). The rental portfolio, which included the

company non-UK shopping centers, represented a prime yield of 3.5% in Barcelona ( PWC

2018). The average performance of each sectoral formation as represented by the yield value

and price variances as provided by each sectoral distribution proves the potential of

improvement in different megacities in Europe and the UK.

The current investment plan of the company has included other major sectoral

segments that perform better in megacities in the UK but again debarred the cities and other

sectors that also perform better. The logistics lead in potential opportunities identified to

include critical cities in southern Europe and significant transport corridors. The effect comes

with the double-digit commerce growth that influenced the variances of sectoral property

prices in the year 2018; thus, the shifts in the investments plans of many investors (Williams,

2018). The potential of investment in different sectors may require the company to include

an alternating investment plan that will need to increase portfolios in non-UK regions. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Real Estate Investment 4

primary focus should be on the projected investment yield identified in different areas as

recognized with the value of the risk that may affect the yield value.

In the UK, office and retails sectors shows a significant increase in yield amounts.

The sectors have also earned a better lure from the minority groups. However, they offer a

more risk for uncertainties, which may result from the low market value of the assets and the

future stagnations of the asset prices. The deterioration of the industry sector, as provided in

the 2018 analysis reports does not create a potential outlook of the continual future worsening

of capital asset prices traded in the sector (Santos 2018). 2019 shows the potential of another

shift, which may promote these sectoral levels. Though, the slowing price growth levels in

former hotspots do not offer a possibility for future increase investment opportunities

Geographical Distribution

In 2018, the southeast region led with 37% of the total capital value. London,

Scotland, West Midlands, East Midlands, Yorks/Humber, North East, and North West

consisted of approximately 19%,9%,9%.8%.7%.6%.4%, and 1% respectively (Knight Frank,

2018). The global rising uncertainty has seen Europe continuing to house among the most

liquid and trusted commercial real estate market globally. International investors and

domestic operators receive similar benefits offered by these variances identified in the Europe

geographical region. The entire Property European Investment volume of assets above EUR

5M totaled to EUR 277.7 billion in the year 2018 (BMO Real Estate Partners, 2018). This

valuation shows a large market with many investment opportunities that are only identical to

a significant player in different geographical regions.

The significant concerns involving the real estate investment in the broader

geographical region consists of determining suitable assets. The most active markets are

valued for offering high-quality real estate assets, but as identified with the company

primary focus should be on the projected investment yield identified in different areas as

recognized with the value of the risk that may affect the yield value.

In the UK, office and retails sectors shows a significant increase in yield amounts.

The sectors have also earned a better lure from the minority groups. However, they offer a

more risk for uncertainties, which may result from the low market value of the assets and the

future stagnations of the asset prices. The deterioration of the industry sector, as provided in

the 2018 analysis reports does not create a potential outlook of the continual future worsening

of capital asset prices traded in the sector (Santos 2018). 2019 shows the potential of another

shift, which may promote these sectoral levels. Though, the slowing price growth levels in

former hotspots do not offer a possibility for future increase investment opportunities

Geographical Distribution

In 2018, the southeast region led with 37% of the total capital value. London,

Scotland, West Midlands, East Midlands, Yorks/Humber, North East, and North West

consisted of approximately 19%,9%,9%.8%.7%.6%.4%, and 1% respectively (Knight Frank,

2018). The global rising uncertainty has seen Europe continuing to house among the most

liquid and trusted commercial real estate market globally. International investors and

domestic operators receive similar benefits offered by these variances identified in the Europe

geographical region. The entire Property European Investment volume of assets above EUR

5M totaled to EUR 277.7 billion in the year 2018 (BMO Real Estate Partners, 2018). This

valuation shows a large market with many investment opportunities that are only identical to

a significant player in different geographical regions.

The significant concerns involving the real estate investment in the broader

geographical region consists of determining suitable assets. The most active markets are

valued for offering high-quality real estate assets, but as identified with the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Real Estate Investment 5

investment plan, there is a high propensity of taking more risk to increase the total yield from

the investment. Also, other investment plans of Mega Corporation may lead to overpricing of

prime assets. In 2018, the overpricing of top holdings in the London industrial sector led to

the shift of investment strategies resulting in an increased investment preference on offices by

many investors (Knight Frank, 2019).

A considerable outlook on the broader geographic region identifies emerging trends in

many sectoral formations. Like, German is a potential region for real estate investments in

Europe. The city of Berlin, according to PWC 2018, provided a better sport for investment

that offered an exclusive mixture of excellent priced residential properties with a high return

on capital assets, low uncertainty levels, and long-term growth prospects. The real estate

property value in Berlin increased by 2%, a significant change that influenced the preferences

of investors on the future potential increase in property value in Berlin (PWC, 2018). In two

years, the £85 million portfolios of the company will increase at a valuation of 2%, of which,

if the trend continues, the company will earn a maximum of more than 8% increase in its

office portfolio in Berlin for the next five years.

The property valuation trend in Berlin will increase due to the change of economic

dynamics that have led to the continual demands of the assets. The promising in the region

has shown an increased eagerness of many investors wanting to invest in German. A

considerable change in other regional settings offers global based opportunities for the

continual investment plans of the company in non-UK regions as compared to the local

market. The choice to investors will need to consider on sectoral performance. The

deterioration of industry prices in the UK in 2018 allowed the booming of offices and retail

sections as reflected in the company portfolio earning; office and retail pension fund

portfolios led by 30% and 40% of the total PFP respectively (BMO Real Estate Partners,

investment plan, there is a high propensity of taking more risk to increase the total yield from

the investment. Also, other investment plans of Mega Corporation may lead to overpricing of

prime assets. In 2018, the overpricing of top holdings in the London industrial sector led to

the shift of investment strategies resulting in an increased investment preference on offices by

many investors (Knight Frank, 2019).

A considerable outlook on the broader geographic region identifies emerging trends in

many sectoral formations. Like, German is a potential region for real estate investments in

Europe. The city of Berlin, according to PWC 2018, provided a better sport for investment

that offered an exclusive mixture of excellent priced residential properties with a high return

on capital assets, low uncertainty levels, and long-term growth prospects. The real estate

property value in Berlin increased by 2%, a significant change that influenced the preferences

of investors on the future potential increase in property value in Berlin (PWC, 2018). In two

years, the £85 million portfolios of the company will increase at a valuation of 2%, of which,

if the trend continues, the company will earn a maximum of more than 8% increase in its

office portfolio in Berlin for the next five years.

The property valuation trend in Berlin will increase due to the change of economic

dynamics that have led to the continual demands of the assets. The promising in the region

has shown an increased eagerness of many investors wanting to invest in German. A

considerable change in other regional settings offers global based opportunities for the

continual investment plans of the company in non-UK regions as compared to the local

market. The choice to investors will need to consider on sectoral performance. The

deterioration of industry prices in the UK in 2018 allowed the booming of offices and retail

sections as reflected in the company portfolio earning; office and retail pension fund

portfolios led by 30% and 40% of the total PFP respectively (BMO Real Estate Partners,

Real Estate Investment 6

2018). Current London price variances do offer the same situation for the potential increase

in the future yields of the two sectors due to fluctuating economic subtleties.

Considerations of Allowing the Investment of the Portfolio in Direct Real Estate

Expected Returns

Yield embroils the uncertainties in the market. The expected rate of return is also

determined with the market efficiencies and employed company investment procedures to

meet its target estimate (Ibbotson & Siegel, 2018). The firm aims to realize a return of £ 200.

Higher portfolio concentrations, as provided by the company 2018 data on Pension fund

portfolio, includes Offices and retails that consist of a 30% and 40% respectively. A reduced

percentage representation of the two sections will alter the current level of return.

Considering that the reason for improved levels in yields is due to the gained traction of

offices and Retails in the UK market due to a price change in the industrial section, the need

to consider the efficiencies of the two sects is to maintain the same level of return

(Gounopoulos et al.2019). This concern for an expected return, therefore, needs

consideration of a change of trends in other regional sections like Berlin in German. The

advantage of the consideration is that it will result in increased returns of the company at the

end of 2019.

Investment features

Investment features define the characteristics of a real estate investment option. An

option will include a type of capital asset, a geographical region, and sectoral conditions. The

study of London provides a stable market which has proved on its stability for a more

extended period (Boddy 2018). Therefore, the company has an advantage since it grounds in

an already established commercial property Market. Berlin characteristic shows a future

demand for houses, thus indicating an increased future trend on investment. The industrial

2018). Current London price variances do offer the same situation for the potential increase

in the future yields of the two sectors due to fluctuating economic subtleties.

Considerations of Allowing the Investment of the Portfolio in Direct Real Estate

Expected Returns

Yield embroils the uncertainties in the market. The expected rate of return is also

determined with the market efficiencies and employed company investment procedures to

meet its target estimate (Ibbotson & Siegel, 2018). The firm aims to realize a return of £ 200.

Higher portfolio concentrations, as provided by the company 2018 data on Pension fund

portfolio, includes Offices and retails that consist of a 30% and 40% respectively. A reduced

percentage representation of the two sections will alter the current level of return.

Considering that the reason for improved levels in yields is due to the gained traction of

offices and Retails in the UK market due to a price change in the industrial section, the need

to consider the efficiencies of the two sects is to maintain the same level of return

(Gounopoulos et al.2019). This concern for an expected return, therefore, needs

consideration of a change of trends in other regional sections like Berlin in German. The

advantage of the consideration is that it will result in increased returns of the company at the

end of 2019.

Investment features

Investment features define the characteristics of a real estate investment option. An

option will include a type of capital asset, a geographical region, and sectoral conditions. The

study of London provides a stable market which has proved on its stability for a more

extended period (Boddy 2018). Therefore, the company has an advantage since it grounds in

an already established commercial property Market. Berlin characteristic shows a future

demand for houses, thus indicating an increased future trend on investment. The industrial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Real Estate Investment 7

operation does not, however, show a possible performance in this region as relates to other

markets. The current portfolio value in the area will also show a reciprocating increase in

valuation.

On the other hand, German shows high potentials on real estate increase in property

value beside Berlin cities. There is a consequential change of valuations identified with a

region such as German (Dieterich 2018). These changes and opportunities will also affect the

from the distributions center due to increased economic activity (Zhou 2018). Investment

scale is also essential. It determines the magnitude of the commitment made by the company

based on the conditions identified in the market. For instance, a study may provide favorable

conditions that promote the operating efficiencies in the German as a whole thus implying

that if the company diversify to include other cities such as Frankfurt, the total yield value

will increase. The effects originate from the impacts created from regional efficiencies and

operations.

Variations and growth (Phase of the Real Estate cycle)

Asset valuation includes different aspects such as asset liquidity, risks, and change of

property features and reduced increase of property value. Assessments should also consider

external elements and the investment plans offered by the company. Change of prices results

from external forces that demand the preferences of the real estate investors as identified with

the potential return of the property and projected uncertainties (He et al., 2018). Other issues

such as competitions and aggressiveness of other investors may alter the actual valuation of

the property resulting in over or under-pricing. A scramble for investment involves the

growth levels that define the investment strategies that a company should employ to meet the

demands and benefit from the investment plan at all development levels of the real estate

operation does not, however, show a possible performance in this region as relates to other

markets. The current portfolio value in the area will also show a reciprocating increase in

valuation.

On the other hand, German shows high potentials on real estate increase in property

value beside Berlin cities. There is a consequential change of valuations identified with a

region such as German (Dieterich 2018). These changes and opportunities will also affect the

from the distributions center due to increased economic activity (Zhou 2018). Investment

scale is also essential. It determines the magnitude of the commitment made by the company

based on the conditions identified in the market. For instance, a study may provide favorable

conditions that promote the operating efficiencies in the German as a whole thus implying

that if the company diversify to include other cities such as Frankfurt, the total yield value

will increase. The effects originate from the impacts created from regional efficiencies and

operations.

Variations and growth (Phase of the Real Estate cycle)

Asset valuation includes different aspects such as asset liquidity, risks, and change of

property features and reduced increase of property value. Assessments should also consider

external elements and the investment plans offered by the company. Change of prices results

from external forces that demand the preferences of the real estate investors as identified with

the potential return of the property and projected uncertainties (He et al., 2018). Other issues

such as competitions and aggressiveness of other investors may alter the actual valuation of

the property resulting in over or under-pricing. A scramble for investment involves the

growth levels that define the investment strategies that a company should employ to meet the

demands and benefit from the investment plan at all development levels of the real estate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Real Estate Investment 8

cycle. The plan stabilizes the company operations in long duration and as well as enhance the

long-term establishment of a company in a particular real estate market.

Fulfillment of the Objectives

Responsible Property Investment

The need for responsible property management is to ensure that the company meets its

objectives. The current aim of the company is to ensure that it keeps its net inflow of £ 200

in the next five years and as well outperforms the IPD local authority pension fund

performance. A scramble for good investment opportunities characterizes a good market.

Equally, a property market demands for better and transparent management procedures of a

property. Strategic management, therefore, ensures responsible property management, and it

includes a projected decision-making system that will meet the demands of the firm

stakeholders.

Current firm operations are concentrated in the UK –London Market. A change to

include other new regions will introduce more concerns; increased risks and uncertainties

and challenges posed by the larger environmental, ethical, and social society and thus

jeopardizing the viability of the properties. Responsible property management, therefore, will

include abiding by the state rules to ensure accountable competition in the company

operations (Myers, 2018). Notably, the implementations of the process will require the firm

to establish better plans which will improve the conditions of the assets and the resulting

social, governance, and environmental issues. European shows a destabilized political

environmental despite its performing real estate sector. The company should consider the

operating variances and note on the argument that will alter the investment plans and result

in other more critical issues from different regional authorities

cycle. The plan stabilizes the company operations in long duration and as well as enhance the

long-term establishment of a company in a particular real estate market.

Fulfillment of the Objectives

Responsible Property Investment

The need for responsible property management is to ensure that the company meets its

objectives. The current aim of the company is to ensure that it keeps its net inflow of £ 200

in the next five years and as well outperforms the IPD local authority pension fund

performance. A scramble for good investment opportunities characterizes a good market.

Equally, a property market demands for better and transparent management procedures of a

property. Strategic management, therefore, ensures responsible property management, and it

includes a projected decision-making system that will meet the demands of the firm

stakeholders.

Current firm operations are concentrated in the UK –London Market. A change to

include other new regions will introduce more concerns; increased risks and uncertainties

and challenges posed by the larger environmental, ethical, and social society and thus

jeopardizing the viability of the properties. Responsible property management, therefore, will

include abiding by the state rules to ensure accountable competition in the company

operations (Myers, 2018). Notably, the implementations of the process will require the firm

to establish better plans which will improve the conditions of the assets and the resulting

social, governance, and environmental issues. European shows a destabilized political

environmental despite its performing real estate sector. The company should consider the

operating variances and note on the argument that will alter the investment plans and result

in other more critical issues from different regional authorities

Real Estate Investment 9

Implementing responsible Property investment will need the company to build an

investment rationale. Specific changes should be incorporated to develop new investment

plans. These needs require commitment and engagement in the executions of the company

strategies to reduce the associated investment risks and capitalize on the opportunities in

different regions and sectors (Read & Sanderford, 2018). The actions deal with inhibiting

potential direct and indirect effects on the property value. Investor preferences changes based

on property feature and the organization should ensure that it applies better differentials that

merge the market preferences and the type of product (Miller et al., 2018). Using responsible

property investment will also need an asset allocation plan, property section plan, and

property management actions. In investing in Berlin, the company should consider ways to

allocate properties to the potential clients and the procedures employed to assign such

property to the identified clients.

Environmental Agenda

Enhancing Sustainability

City investment and property development are one of the visionary outlook actions

that are aimed at sustainable development agendas of a given location. Assets are resources,

and their use should ensure safety to the ecosystem. Lack of sustainable management

procedures affects the future growth of the real estate market and as well as affect the future

price of real estate properties (Miller et al., 2018). Change of pricing in the market resulting

in shifts of real estate sectoral prices and return affecting the investors' preferences

(Benlemlih & Bitar, 2018). Change in preference results in s shifts in the investment plans as

witnessed in 2018 UK Market. The shifts affect other sectors, such as the industrial sector

which for a long time remains a giant in the UK and currently shows a low level of traction to

investors.

Implementing responsible Property investment will need the company to build an

investment rationale. Specific changes should be incorporated to develop new investment

plans. These needs require commitment and engagement in the executions of the company

strategies to reduce the associated investment risks and capitalize on the opportunities in

different regions and sectors (Read & Sanderford, 2018). The actions deal with inhibiting

potential direct and indirect effects on the property value. Investor preferences changes based

on property feature and the organization should ensure that it applies better differentials that

merge the market preferences and the type of product (Miller et al., 2018). Using responsible

property investment will also need an asset allocation plan, property section plan, and

property management actions. In investing in Berlin, the company should consider ways to

allocate properties to the potential clients and the procedures employed to assign such

property to the identified clients.

Environmental Agenda

Enhancing Sustainability

City investment and property development are one of the visionary outlook actions

that are aimed at sustainable development agendas of a given location. Assets are resources,

and their use should ensure safety to the ecosystem. Lack of sustainable management

procedures affects the future growth of the real estate market and as well as affect the future

price of real estate properties (Miller et al., 2018). Change of pricing in the market resulting

in shifts of real estate sectoral prices and return affecting the investors' preferences

(Benlemlih & Bitar, 2018). Change in preference results in s shifts in the investment plans as

witnessed in 2018 UK Market. The shifts affect other sectors, such as the industrial sector

which for a long time remains a giant in the UK and currently shows a low level of traction to

investors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Real Estate Investment 10

Reduced pollution menace

Pollutions implicate the value of a real estate property in the future. Increased

urbanizations have led to an increased level of pollution in megacities and thus affecting the

increase in real estate property value. This issue affects the future value of a property that

results in reduced future cash inflow from real estate investment portfolios (Devine &

Yonder, 2018). The effects may result in the company not to realize its objectives of a

positive net return of £ 200 peranuminthenextfiveyears. The organization should take a

participatory environmental role that will ensure the safeguarding of the natural resources to

help maintain the value of a real estate property in the future periods.

Reduced pollution menace

Pollutions implicate the value of a real estate property in the future. Increased

urbanizations have led to an increased level of pollution in megacities and thus affecting the

increase in real estate property value. This issue affects the future value of a property that

results in reduced future cash inflow from real estate investment portfolios (Devine &

Yonder, 2018). The effects may result in the company not to realize its objectives of a

positive net return of £ 200 peranuminthenextfiveyears. The organization should take a

participatory environmental role that will ensure the safeguarding of the natural resources to

help maintain the value of a real estate property in the future periods.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Real Estate Investment 11

References

PWC, 2018. Emerging Trends in Real Estate: Reshaping the future. [Online]

Available at: https://www.pwc.dk/da/publikationer/2017/pwc-etre-europe-

2018.pdf[Accessed 19 May, 2019].

Benlemlih, M. & Bitar, M., 2018. Corporate social responsibility and investment efficiency.

Journal of Business Ethics, 148(3), pp. 647-671.

BMO Real Estate Partners, 2018. UK Property Market Trends. [Online]

Available at: https://www.bmorep.com/wp-content/uploads/2018/10/cm17479-

property-market-review_new-office.pdf

[Accessed 19 May 2019].

BNP Paribas Real Estate, 2019. European Property Investment: Real Estate Market 2018

Overview and 2019 Predictions. [Online]

[Accessed 19 05 2019].

Boddy, M., 2018. 11 The property sector in late capitalism: the case of Britain. Urbanization

and urban planning in a capitalist society, Volume 7.

Devine, A. & Yonder, E., 2018. Decomposing the Cash Flow and Value Effects of

Sustainable Investment: A Test of Firm Perspective Theory. s.l.:s.n.

Dieterich, H. D. E. &. V. W., 2018. Urban land and property markets in Germany, s.l.:

Routledge.

Gounopoulos, D., Kosmidou, K., Kousenidis, D. & Patsika, V., 2019. The investigation of

the dynamic linkages between the real estate market and the stock market in Greece.,.

The European Journal of Finance, 25(7), pp. 647-669.

References

PWC, 2018. Emerging Trends in Real Estate: Reshaping the future. [Online]

Available at: https://www.pwc.dk/da/publikationer/2017/pwc-etre-europe-

2018.pdf[Accessed 19 May, 2019].

Benlemlih, M. & Bitar, M., 2018. Corporate social responsibility and investment efficiency.

Journal of Business Ethics, 148(3), pp. 647-671.

BMO Real Estate Partners, 2018. UK Property Market Trends. [Online]

Available at: https://www.bmorep.com/wp-content/uploads/2018/10/cm17479-

property-market-review_new-office.pdf

[Accessed 19 May 2019].

BNP Paribas Real Estate, 2019. European Property Investment: Real Estate Market 2018

Overview and 2019 Predictions. [Online]

[Accessed 19 05 2019].

Boddy, M., 2018. 11 The property sector in late capitalism: the case of Britain. Urbanization

and urban planning in a capitalist society, Volume 7.

Devine, A. & Yonder, E., 2018. Decomposing the Cash Flow and Value Effects of

Sustainable Investment: A Test of Firm Perspective Theory. s.l.:s.n.

Dieterich, H. D. E. &. V. W., 2018. Urban land and property markets in Germany, s.l.:

Routledge.

Gounopoulos, D., Kosmidou, K., Kousenidis, D. & Patsika, V., 2019. The investigation of

the dynamic linkages between the real estate market and the stock market in Greece.,.

The European Journal of Finance, 25(7), pp. 647-669.

Real Estate Investment 12

He, X., Lin, Z. & Liu, Y., 2018. Volatility and Liquidity in the Real Estate Market. Journal of

Real Estate Research, 40(4), pp. 523-550.

Ibbotson, R. G. & Siegel, L. B., 2018. Real Estate Returns. A Comparison with Other

Investments., 1(0), pp. 1-4.

Knight Frank, 2018. European real estate investors identify the UK as preferred investment

target for 2019. [Online]

Available at: https://www.knightfrank.com/blog/2018/11/19/european-real-estate-

investors-identify-uk-as-preferred-investment-target-for-2019[Accessed 19 May,

2019].

Knight Frank, 2019. European Commercial Property Outlook 2019. [Online]

Available at: https://content.knightfrank.com/research/743/documents/en/european-

property-outlook-2019-6234.pdf[Accessed 19 May, 2019].

Knight Frank, 2018. European Commercial property Outlook 2018. [Online]

Available at:

https://repositorio-aberto.up.pt/bitstream/10216/116510/2/296684.pdf[Accessed 05

May, 2019].

Miller, N., Sayce, S., Dixon, T. & Wilkinson, S., 2018. Sustainable real estate: A snapshot of

where we are. In Routledge Handbook of Sustainable Real Estate (pp. 3-18).. s.l.:

Routledge.

Myers, D., 2018. Economics and property. S .l. Routledge.

PWC, 2018. Emerging Trends in Real Estate®: Europe 2018. [Online]

Available at: https://www.pwc.com/gx/en/industries/financial-services/asset-

management/emerging-trends-real-estate/europe-2018.html[Accessed 19 May, 2019].

He, X., Lin, Z. & Liu, Y., 2018. Volatility and Liquidity in the Real Estate Market. Journal of

Real Estate Research, 40(4), pp. 523-550.

Ibbotson, R. G. & Siegel, L. B., 2018. Real Estate Returns. A Comparison with Other

Investments., 1(0), pp. 1-4.

Knight Frank, 2018. European real estate investors identify the UK as preferred investment

target for 2019. [Online]

Available at: https://www.knightfrank.com/blog/2018/11/19/european-real-estate-

investors-identify-uk-as-preferred-investment-target-for-2019[Accessed 19 May,

2019].

Knight Frank, 2019. European Commercial Property Outlook 2019. [Online]

Available at: https://content.knightfrank.com/research/743/documents/en/european-

property-outlook-2019-6234.pdf[Accessed 19 May, 2019].

Knight Frank, 2018. European Commercial property Outlook 2018. [Online]

Available at:

https://repositorio-aberto.up.pt/bitstream/10216/116510/2/296684.pdf[Accessed 05

May, 2019].

Miller, N., Sayce, S., Dixon, T. & Wilkinson, S., 2018. Sustainable real estate: A snapshot of

where we are. In Routledge Handbook of Sustainable Real Estate (pp. 3-18).. s.l.:

Routledge.

Myers, D., 2018. Economics and property. S .l. Routledge.

PWC, 2018. Emerging Trends in Real Estate®: Europe 2018. [Online]

Available at: https://www.pwc.com/gx/en/industries/financial-services/asset-

management/emerging-trends-real-estate/europe-2018.html[Accessed 19 May, 2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.