A Critical Evaluation of Westpac Institutional Bank's Credit Processes

VerifiedAdded on 2019/10/31

|27

|7914

|26

Thesis and Dissertation

AI Summary

This dissertation critically evaluates the operational and process management within Westpac Institutional Bank's credit processes in Singapore, focusing on increasing the speed to market from origination to execution. The research explores the background of Westpac's operations in Singapore, identifies the research problem of slow credit processes, and poses key research questions regarding control processes, the causes of sluggishness, methods to limit breakdowns, and the adequacy of credit management. The literature review covers process and operations management, credit process management, credit technology, and risk assessment. The methodology includes data collection via surveys and interviews, along with data analysis to identify undesirable outcomes and suggest improvements to the credit process. The findings aim to provide recommendations for enhancing Westpac's credit processes, ultimately contributing to improved efficiency and competitiveness in the Singapore market. The study also highlights the importance of technology, accountability, and process optimization in the banking sector.

Running Head: DISSERTATION

A critical evaluation of operational and process management across Westpac Institutional Bank’s

credit processes in order to increase the speed to market from origination to execution of

opportunities in Singapore

Name of the student

Name of the university

Author’s note

A critical evaluation of operational and process management across Westpac Institutional Bank’s

credit processes in order to increase the speed to market from origination to execution of

opportunities in Singapore

Name of the student

Name of the university

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1DISSERTATION

Table of Contents

Chapter 1: Introduction....................................................................................................................3

1.1 Background............................................................................................................................3

1.2 Research Problem..................................................................................................................3

1.3 Focus of the Paper..................................................................................................................4

1.4 Research Questions................................................................................................................5

1.5 Aims and Objectives..............................................................................................................5

Chapter 2: Literature Review...........................................................................................................6

2.1 Introduction............................................................................................................................6

2.2 Process and Operations management.....................................................................................6

2.3 Credit Process Management...................................................................................................7

2.4 Credit Technology..................................................................................................................7

2.5 Assessment of the Operations................................................................................................8

2.6 Risks.......................................................................................................................................9

2.7 Business Process Modelling...................................................................................................9

Research Methodology..................................................................................................................12

3.1 Introduction..........................................................................................................................12

3.2 Research Question................................................................................................................12

3.2 Research Choice...................................................................................................................12

3.3 Data Collection method.......................................................................................................13

3.4 Sampling & Data Access.....................................................................................................13

3.5 Ethical & Data Protection issues..........................................................................................13

3.6 Limitations...........................................................................................................................13

Data Analysis.................................................................................................................................14

4.1 Introduction..........................................................................................................................14

4.2 Analysis of the survey..........................................................................................................14

4.3 Analysis of Interview...........................................................................................................20

4.3.1 Undesirable outcome.....................................................................................................20

4.3.2 Stages at which the process map should be reworked...................................................21

Table of Contents

Chapter 1: Introduction....................................................................................................................3

1.1 Background............................................................................................................................3

1.2 Research Problem..................................................................................................................3

1.3 Focus of the Paper..................................................................................................................4

1.4 Research Questions................................................................................................................5

1.5 Aims and Objectives..............................................................................................................5

Chapter 2: Literature Review...........................................................................................................6

2.1 Introduction............................................................................................................................6

2.2 Process and Operations management.....................................................................................6

2.3 Credit Process Management...................................................................................................7

2.4 Credit Technology..................................................................................................................7

2.5 Assessment of the Operations................................................................................................8

2.6 Risks.......................................................................................................................................9

2.7 Business Process Modelling...................................................................................................9

Research Methodology..................................................................................................................12

3.1 Introduction..........................................................................................................................12

3.2 Research Question................................................................................................................12

3.2 Research Choice...................................................................................................................12

3.3 Data Collection method.......................................................................................................13

3.4 Sampling & Data Access.....................................................................................................13

3.5 Ethical & Data Protection issues..........................................................................................13

3.6 Limitations...........................................................................................................................13

Data Analysis.................................................................................................................................14

4.1 Introduction..........................................................................................................................14

4.2 Analysis of the survey..........................................................................................................14

4.3 Analysis of Interview...........................................................................................................20

4.3.1 Undesirable outcome.....................................................................................................20

4.3.2 Stages at which the process map should be reworked...................................................21

2DISSERTATION

4.3.3 Credit process affects speed to market..........................................................................21

4.3.4 Suggestion to the credit process....................................................................................22

4.4 Secondary Analysis..............................................................................................................22

Conclusion and recommendation..................................................................................................23

5.1 Introduction..............................................................................................................................23

5.2 Conclusion...............................................................................................................................23

5.3 Recommendations....................................................................................................................23

5.4 Further Research......................................................................................................................24

References......................................................................................................................................25

4.3.3 Credit process affects speed to market..........................................................................21

4.3.4 Suggestion to the credit process....................................................................................22

4.4 Secondary Analysis..............................................................................................................22

Conclusion and recommendation..................................................................................................23

5.1 Introduction..............................................................................................................................23

5.2 Conclusion...............................................................................................................................23

5.3 Recommendations....................................................................................................................23

5.4 Further Research......................................................................................................................24

References......................................................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3DISSERTATION

Chapter 1: Introduction

This paper has been constructed in order to evaluate the process design and analysis for

the credit process of Westpac Institutional Banks in Singapore. The development of the global

economy by taking help of the new and improved technologies has influenced the organizations

to expand their business in to the next level. The development of the organization is only

possible by undertaking credits from the banks and other financial institutions and hence it is

essential for the financial institutions and banks to design strategies that would lead to the

effective credit lending process. The paper would therefore discuss about the process of design

and analysis of the credit processes of Westpac so that the operational and functional of the

company would be analyzed.

1.1 Background

Westpac’s Institutional Bank has been one of the leading Australian banks and has been

providing financial services to the consumers, government, corporations and other organizations

operating in Australia, New Zealand and other Asian countries. Westpac has been functioning in

Singapore and has been one of the leading service providers who have been providing wholesale

financial services to the clients in Singapore with an intention to assist the customers with an

Australian relationship. The bank even provides several services such as trade financing, mergers

and acquisitions, debt structuring and financial market operations and even provides strategic

advices to the firms and the consumers of Singapore. Furthermore, they even the providers of

services of underwriting that concentrates on debt security, foreign exchange services, interest

derivatives and fixed interest on the commodities and the services provided (Bodie 2013). The

requirement of loans and credits by the organization and the consumers have motivated Westpac

to undertake various designs and evaluation of the designs related to the credit process so that

effective results can be obtained which would motivate them to provide effective services to the

companies and the individual consumers. The construction of the effective design for the credit

lending process and evaluation of the same would lead to effective control and credit lending

process.

1.2 Research Problem

This research paper would concentrate on the credit lending mechanism of Westpac

Institutional Bank in the market of Singapore in order to capture the innovative opportunities and

Chapter 1: Introduction

This paper has been constructed in order to evaluate the process design and analysis for

the credit process of Westpac Institutional Banks in Singapore. The development of the global

economy by taking help of the new and improved technologies has influenced the organizations

to expand their business in to the next level. The development of the organization is only

possible by undertaking credits from the banks and other financial institutions and hence it is

essential for the financial institutions and banks to design strategies that would lead to the

effective credit lending process. The paper would therefore discuss about the process of design

and analysis of the credit processes of Westpac so that the operational and functional of the

company would be analyzed.

1.1 Background

Westpac’s Institutional Bank has been one of the leading Australian banks and has been

providing financial services to the consumers, government, corporations and other organizations

operating in Australia, New Zealand and other Asian countries. Westpac has been functioning in

Singapore and has been one of the leading service providers who have been providing wholesale

financial services to the clients in Singapore with an intention to assist the customers with an

Australian relationship. The bank even provides several services such as trade financing, mergers

and acquisitions, debt structuring and financial market operations and even provides strategic

advices to the firms and the consumers of Singapore. Furthermore, they even the providers of

services of underwriting that concentrates on debt security, foreign exchange services, interest

derivatives and fixed interest on the commodities and the services provided (Bodie 2013). The

requirement of loans and credits by the organization and the consumers have motivated Westpac

to undertake various designs and evaluation of the designs related to the credit process so that

effective results can be obtained which would motivate them to provide effective services to the

companies and the individual consumers. The construction of the effective design for the credit

lending process and evaluation of the same would lead to effective control and credit lending

process.

1.2 Research Problem

This research paper would concentrate on the credit lending mechanism of Westpac

Institutional Bank in the market of Singapore in order to capture the innovative opportunities and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4DISSERTATION

deals and thereby increase their market share and maintain the competitive edge. The intention

has been to recognize and undertake researches on the numerous steps of the bank with respect to

the process of crediting with the help of execution and it has been observed that they have been

slow to critically breakdown the credit operations and even on the stages of boarding.

Furthermore, this paper would explain further the operations as well as their efficient holds,

proposals and accountabilities to construct the activities of the banks even more unified.

1.3 Focus of the Paper

The operational management of Westpac Institutional Bank is inclusive of the regulation

of the costs and developing the degree of services and even enhancing the service quality that

have been given out to the consumers. The process of credit in Westpac has been very sluggish

from the point of origin of the bank in Singapore and the execution of the process of execution.

The operations section of the bank will concentrate on the mechanisms that have been

constructed in order to supervise and handle the procedures within the service distribution. The

management associated with the process of credit chain in the service development and has been

very sluggish for the bank. It is essential for the bank to assess their intrinsic methods

specifically with respect to the vibrant economy where the bank functions. The bank has been

going through certain transitions and especially in the transformations in the culture in certain

branches in Asia. These transitions has had an impact on certain mechanisms of the banks and

hence the bank has been trying to familiarize with the new management along with maintaining

the current activities of the bank.

The process of credit in the bank has been very sluggish as the process of core banking

for the bank are complex and furthermore there has been an insufficiency of the accountability

and visibility as the prospects have been working through the processing chains. Moreover, the

core banking process of the bank is seen to be one of the oldest technology in accordance to the

banking industry. The process of core banking that is utilized in Australia has been looked down

as a historic one with respect to the age of technology. There have been concerns with respect to

cost of maintenance and manual workings, which exploits a lot of valuable resources that could

have been invested in order to further enhance the digital channels and other usage in the

banking companies. There has been existence of other concerns like the lack of responsibility

among the numerous chains of process which hinders the actual transaction method along with

deals and thereby increase their market share and maintain the competitive edge. The intention

has been to recognize and undertake researches on the numerous steps of the bank with respect to

the process of crediting with the help of execution and it has been observed that they have been

slow to critically breakdown the credit operations and even on the stages of boarding.

Furthermore, this paper would explain further the operations as well as their efficient holds,

proposals and accountabilities to construct the activities of the banks even more unified.

1.3 Focus of the Paper

The operational management of Westpac Institutional Bank is inclusive of the regulation

of the costs and developing the degree of services and even enhancing the service quality that

have been given out to the consumers. The process of credit in Westpac has been very sluggish

from the point of origin of the bank in Singapore and the execution of the process of execution.

The operations section of the bank will concentrate on the mechanisms that have been

constructed in order to supervise and handle the procedures within the service distribution. The

management associated with the process of credit chain in the service development and has been

very sluggish for the bank. It is essential for the bank to assess their intrinsic methods

specifically with respect to the vibrant economy where the bank functions. The bank has been

going through certain transitions and especially in the transformations in the culture in certain

branches in Asia. These transitions has had an impact on certain mechanisms of the banks and

hence the bank has been trying to familiarize with the new management along with maintaining

the current activities of the bank.

The process of credit in the bank has been very sluggish as the process of core banking

for the bank are complex and furthermore there has been an insufficiency of the accountability

and visibility as the prospects have been working through the processing chains. Moreover, the

core banking process of the bank is seen to be one of the oldest technology in accordance to the

banking industry. The process of core banking that is utilized in Australia has been looked down

as a historic one with respect to the age of technology. There have been concerns with respect to

cost of maintenance and manual workings, which exploits a lot of valuable resources that could

have been invested in order to further enhance the digital channels and other usage in the

banking companies. There has been existence of other concerns like the lack of responsibility

among the numerous chains of process which hinders the actual transaction method along with

5DISSERTATION

the update of the data, which the consumers require to be keeping intact before the conclusion of

any prospects (Liu 2015). The financial organizations even has the desire to give out services and

reduce the level of cost of processing and handle the financial assets. The core processes make

the bank operations slow and thereby becoming susceptible to the new competitors, new

organizational frameworks and establishing substantial operational challenges.

1.4 Research Questions

The research questions have been framed with respect to this topic comprises of the

issues that needs to be answered so that effective results can be obtained. The research questions

has been put forward as follows:

Q1. What control processes will Westpac Institutional Bank undertake in order to function

effectively?

Q2. What is the reason behind the sluggish nature of the credit process chain of Westpac Bank?

Q3. What mechanism will Westpac Institutional Bank initiate in order to limit the critical

breakdown within their credit process and on the boarding stage?

Q4. What is the extent of the adequacy of the credit management for the sustainable and

effective credit delivery?

1.5 Aims and Objectives

The objectives and aims of the paper has been undertaken in order to understand the credit

processing design and analysis of the same in order to gain knowledge about the aspects that can

be improved for an effective operations of Westpac. The aims and objectives are given as

follows:

To identify the control processes that would be essential for the successful operations

of Westpac

To identify the factors that has made the credit process slow

Techniques that can be used for the critical breakdown of their process credit

the update of the data, which the consumers require to be keeping intact before the conclusion of

any prospects (Liu 2015). The financial organizations even has the desire to give out services and

reduce the level of cost of processing and handle the financial assets. The core processes make

the bank operations slow and thereby becoming susceptible to the new competitors, new

organizational frameworks and establishing substantial operational challenges.

1.4 Research Questions

The research questions have been framed with respect to this topic comprises of the

issues that needs to be answered so that effective results can be obtained. The research questions

has been put forward as follows:

Q1. What control processes will Westpac Institutional Bank undertake in order to function

effectively?

Q2. What is the reason behind the sluggish nature of the credit process chain of Westpac Bank?

Q3. What mechanism will Westpac Institutional Bank initiate in order to limit the critical

breakdown within their credit process and on the boarding stage?

Q4. What is the extent of the adequacy of the credit management for the sustainable and

effective credit delivery?

1.5 Aims and Objectives

The objectives and aims of the paper has been undertaken in order to understand the credit

processing design and analysis of the same in order to gain knowledge about the aspects that can

be improved for an effective operations of Westpac. The aims and objectives are given as

follows:

To identify the control processes that would be essential for the successful operations

of Westpac

To identify the factors that has made the credit process slow

Techniques that can be used for the critical breakdown of their process credit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6DISSERTATION

Chapter 2: Literature Review

2.1 Introduction

The literature review with respect to this topic has been developed in order to identify the

aspects and the processes that has been used for effective functioning of the credit processing

chains of the financial institutions and the banks that are functioning in the global market. This

has been a fundamental factor as the loans and credits are provided by the company needs to be

recorded and a proper technique has to be maintained with the help of which the banks and the

financial institutions can understand the level of credit provided and the time that has been taken

in order to complete the process of crediting (Albanese, Caenazzo and Crépey 2017). Hence, this

section of the paper provides explanations and the suggestions that have been put forth by other

researchers who have undertaken research on similar topics and issues previously. These

explanations and suggestions have been fundamental for undertaking the research and gaining a

clear idea about the credit processes and the steps that can be undertaken to improve the credit

processing technique of Westpac in Singapore.

2.2 Process and Operations management

In the mechanism of process design concerns, payback for having an effective technique

is very crucial. Westpac has given out effort and time in the construction and the designing of the

processes, evaluating the performance of the substitute design in accordance to the quality,

effectiveness and the total time that has been utilised by the company. In accordance to the

quality of the bank, it has been beneficial for the accomplishment of the advantages from the cost

for the effective process mechanism design without sacrificing the quality and in this effect

would give the bank a key degree of competitive edge. In certain cases, it can be problematic to

distinguish on the design for the process from numerous service designs, which the bank

provides. The process of credit is constructed with the limitations as well as the authority to drive

through the mechanism that is in mind (Lachmann, Stefani and Wöhrmann 2015). There is a

requirement to make changes in their designs slightly in order to facilitate on their operational

activity. The mechanism and the processes should be constructed so that it can be suitable to the

economy and the market where they have been operating. It is even vital to make not that

numerous marketing strategies may be in need of the various techniques of the design. An

effective point of initiation for any of the activities can be understood with the help of the direct

relationship that has been existent among the strategic and the mechanisms for the objectives of

the performance (Tsai, Lu and Hung 2016). The process of gaining knowledge about the present

mechanisms of a firm would be useful in making developments especially in the process of

credit that is based on the practicality of what undertakes within the practice. It would be about

assigning the tasks as well as the related capacity in a careful manner to the suitable sections of

the mechanism to work. In most of the techniques, it will be inclusive of the design, which has

the capability of considering the variability that is existent to most of the personal tasks.

Chapter 2: Literature Review

2.1 Introduction

The literature review with respect to this topic has been developed in order to identify the

aspects and the processes that has been used for effective functioning of the credit processing

chains of the financial institutions and the banks that are functioning in the global market. This

has been a fundamental factor as the loans and credits are provided by the company needs to be

recorded and a proper technique has to be maintained with the help of which the banks and the

financial institutions can understand the level of credit provided and the time that has been taken

in order to complete the process of crediting (Albanese, Caenazzo and Crépey 2017). Hence, this

section of the paper provides explanations and the suggestions that have been put forth by other

researchers who have undertaken research on similar topics and issues previously. These

explanations and suggestions have been fundamental for undertaking the research and gaining a

clear idea about the credit processes and the steps that can be undertaken to improve the credit

processing technique of Westpac in Singapore.

2.2 Process and Operations management

In the mechanism of process design concerns, payback for having an effective technique

is very crucial. Westpac has given out effort and time in the construction and the designing of the

processes, evaluating the performance of the substitute design in accordance to the quality,

effectiveness and the total time that has been utilised by the company. In accordance to the

quality of the bank, it has been beneficial for the accomplishment of the advantages from the cost

for the effective process mechanism design without sacrificing the quality and in this effect

would give the bank a key degree of competitive edge. In certain cases, it can be problematic to

distinguish on the design for the process from numerous service designs, which the bank

provides. The process of credit is constructed with the limitations as well as the authority to drive

through the mechanism that is in mind (Lachmann, Stefani and Wöhrmann 2015). There is a

requirement to make changes in their designs slightly in order to facilitate on their operational

activity. The mechanism and the processes should be constructed so that it can be suitable to the

economy and the market where they have been operating. It is even vital to make not that

numerous marketing strategies may be in need of the various techniques of the design. An

effective point of initiation for any of the activities can be understood with the help of the direct

relationship that has been existent among the strategic and the mechanisms for the objectives of

the performance (Tsai, Lu and Hung 2016). The process of gaining knowledge about the present

mechanisms of a firm would be useful in making developments especially in the process of

credit that is based on the practicality of what undertakes within the practice. It would be about

assigning the tasks as well as the related capacity in a careful manner to the suitable sections of

the mechanism to work. In most of the techniques, it will be inclusive of the design, which has

the capability of considering the variability that is existent to most of the personal tasks.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7DISSERTATION

2.3 Credit Process Management

The credit process management can be considered to be the core line of business that has

been a significant factor for the rise in the income of the financial institutions. The credit process

of a financial institution is based on the credit teams and therefore it is the role of the credit team

to undertake various strategies which would be fundamental for effective credit processing for

the clients. The development of the financial institutions is dependent on the time taken to

approve the loan and and the credit processing chain has to be preside and fast in order to

enhance the operations of the company (Albanese, Caenazzo and Crépey 2017). The

understanding of the credit team plays a crucial role as it is seen that effective knowledge and

understanding leads to development of better credit processing chains and that in a way leads to

development of the financial institutions and banks. Barjaktarovic, Pindzo and Hanic (2016) has

even cited that having the precise and the correct access to the various levels of the credit value

chain can be fundamental for the development of the financial institutions. Wang et al. (2014)

has explained that it is essential for the credit value chain to have effective knowledge and

understanding of the responsibilities and the processes of the banks and the financial institutions.

The credit value chain with the help of the understanding of the responsibilities and the firm

helps in construction of plans and policies that would be implemented in order to improve the

credit processing chains. The understanding of the credit value chain with respect to the

responsibilities of the firm would provide mean that the credit processing is undertaken with

respect to the objectives of the firm. Lee and Yeo (2016) have opined that effective level of

accountability from the credit value chain is fundamentals for the development of timely

outcome of the results. The financial institutions in order to stay competent in the market have to

deliver their performance in a timely manner so that the customers can be satisfied and would

remain associated with the organizations.

2.4 Credit Technology

Credit processing has been dependent on the technology that is used by the financial

institutions. The core banking process plays a significant part that has been influential for the

development of the credit processing chain of the bank. The use of the advanced technologies

would be influential for the development of more advanced services to the customers. It has been

observed that Westpac has been operating with a technology that has been very old and therefore

has been facing certain issues with respect to the completion of the credit processing method.

Skoglund, Vestal and Chen (2013) have cited that financial institutions should make use

of advanced technologies with the help of which the core banking system of the banks and the

financial institutions could be improved. The credit processing chain is dependent on the

operational and process management of the financial institutions. Niccolini et al. (2013) has

explained that in order to create new opportunities it is important to re-validate the data because

revalidating the data would lead to the establishment of the new opportunities in the credit

processing chain. The credit processing chain requires to be transparent so that the various steps

associated with it can be known, which would enhance the consumers from gaining knowledge

2.3 Credit Process Management

The credit process management can be considered to be the core line of business that has

been a significant factor for the rise in the income of the financial institutions. The credit process

of a financial institution is based on the credit teams and therefore it is the role of the credit team

to undertake various strategies which would be fundamental for effective credit processing for

the clients. The development of the financial institutions is dependent on the time taken to

approve the loan and and the credit processing chain has to be preside and fast in order to

enhance the operations of the company (Albanese, Caenazzo and Crépey 2017). The

understanding of the credit team plays a crucial role as it is seen that effective knowledge and

understanding leads to development of better credit processing chains and that in a way leads to

development of the financial institutions and banks. Barjaktarovic, Pindzo and Hanic (2016) has

even cited that having the precise and the correct access to the various levels of the credit value

chain can be fundamental for the development of the financial institutions. Wang et al. (2014)

has explained that it is essential for the credit value chain to have effective knowledge and

understanding of the responsibilities and the processes of the banks and the financial institutions.

The credit value chain with the help of the understanding of the responsibilities and the firm

helps in construction of plans and policies that would be implemented in order to improve the

credit processing chains. The understanding of the credit value chain with respect to the

responsibilities of the firm would provide mean that the credit processing is undertaken with

respect to the objectives of the firm. Lee and Yeo (2016) have opined that effective level of

accountability from the credit value chain is fundamentals for the development of timely

outcome of the results. The financial institutions in order to stay competent in the market have to

deliver their performance in a timely manner so that the customers can be satisfied and would

remain associated with the organizations.

2.4 Credit Technology

Credit processing has been dependent on the technology that is used by the financial

institutions. The core banking process plays a significant part that has been influential for the

development of the credit processing chain of the bank. The use of the advanced technologies

would be influential for the development of more advanced services to the customers. It has been

observed that Westpac has been operating with a technology that has been very old and therefore

has been facing certain issues with respect to the completion of the credit processing method.

Skoglund, Vestal and Chen (2013) have cited that financial institutions should make use

of advanced technologies with the help of which the core banking system of the banks and the

financial institutions could be improved. The credit processing chain is dependent on the

operational and process management of the financial institutions. Niccolini et al. (2013) has

explained that in order to create new opportunities it is important to re-validate the data because

revalidating the data would lead to the establishment of the new opportunities in the credit

processing chain. The credit processing chain requires to be transparent so that the various steps

associated with it can be known, which would enhance the consumers from gaining knowledge

8DISSERTATION

about credit processing so that the consumers are aware that process are undertaken in an

effective manner.

2.5 Assessment of the Operations

The process of credit management has been deemed to be the effective process that

would be undertaken by the financial institutions and the banks with the help of which the credit

processing chain as well as the team that has been undertaken with the help of which the proper

modelling and supervising of the process can be undertaken so that the areas that require

developments and improvements can be undertaken. The process of credit management even

involves recovering the credits from the borrowers within the stipulated time. This management

function can be useful for maintaining the control credit policies in that manner would be useful

for enhancing the profits and the revenues for the organization (Li et al. 2014). The credit

management process has been looked down upon as the mechanism that would be influential as

this process even undermines the process management in relation to credit processing. The

process management looks in to the business process of the financial institutions. In this way the

process management tries to evaluate the credit process and in that manner would be influential

for the development of the financial institutions.

The credit risk manager as well as the portfolio manager has the responsibility of looking

into the mechanism of credit processing and in a manner evaluates the mechanism which is

helpful for the development of an effective process design.

Engelmann et al. (2015) has cited that process design plays a significant role in the

process of credit processing as the credit processing chain can be developed by looking at the

several factors that can be taken into consideration. The financial institutions should be looking

at the market trend along with the level of demand of credit in the market that would be

influential for the development of the credit processing chain. Saha, Bose and Mahanti (2016)

has explained that the numerous steps that are associated with the credit processing chains has an

impact on the speed of the market there are various steps in this process that gets affected. These

steps has to be identified in order to rectify them and in that manner would be influential for

making the process chain effective. The development of the process chain consists of analysing

the various aspects and in that manner develop strategies the credit process chain of the financial

institutions.

Kawada and Shiohama (2016) has opined that process map has a significant role to play

and in that manner aids in the construction of the credit process. Process mapping involves the

construction of the path and the course that would be developed in order to create develop the

credit operating chain. Process mapping even aids rectifying the areas that needs improvements

and in that manner develops the business operations.

The bank credit policy of the financial institutions is developed by looking at the internal

and the external environment of the organisation so that effective steps can be taken in order to

about credit processing so that the consumers are aware that process are undertaken in an

effective manner.

2.5 Assessment of the Operations

The process of credit management has been deemed to be the effective process that

would be undertaken by the financial institutions and the banks with the help of which the credit

processing chain as well as the team that has been undertaken with the help of which the proper

modelling and supervising of the process can be undertaken so that the areas that require

developments and improvements can be undertaken. The process of credit management even

involves recovering the credits from the borrowers within the stipulated time. This management

function can be useful for maintaining the control credit policies in that manner would be useful

for enhancing the profits and the revenues for the organization (Li et al. 2014). The credit

management process has been looked down upon as the mechanism that would be influential as

this process even undermines the process management in relation to credit processing. The

process management looks in to the business process of the financial institutions. In this way the

process management tries to evaluate the credit process and in that manner would be influential

for the development of the financial institutions.

The credit risk manager as well as the portfolio manager has the responsibility of looking

into the mechanism of credit processing and in a manner evaluates the mechanism which is

helpful for the development of an effective process design.

Engelmann et al. (2015) has cited that process design plays a significant role in the

process of credit processing as the credit processing chain can be developed by looking at the

several factors that can be taken into consideration. The financial institutions should be looking

at the market trend along with the level of demand of credit in the market that would be

influential for the development of the credit processing chain. Saha, Bose and Mahanti (2016)

has explained that the numerous steps that are associated with the credit processing chains has an

impact on the speed of the market there are various steps in this process that gets affected. These

steps has to be identified in order to rectify them and in that manner would be influential for

making the process chain effective. The development of the process chain consists of analysing

the various aspects and in that manner develop strategies the credit process chain of the financial

institutions.

Kawada and Shiohama (2016) has opined that process map has a significant role to play

and in that manner aids in the construction of the credit process. Process mapping involves the

construction of the path and the course that would be developed in order to create develop the

credit operating chain. Process mapping even aids rectifying the areas that needs improvements

and in that manner develops the business operations.

The bank credit policy of the financial institutions is developed by looking at the internal

and the external environment of the organisation so that effective steps can be taken in order to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9DISSERTATION

design the credit processing chain. The evaluation of the credit process design undertaken by the

credit managers as well as the portfolio managers. The managers scrutinise each and every

aspect of the design and tries to find out areas that are not providing adequate results. The

evaluation of the design is undertaken with respect to the aims and policies of the organization

(Źróbek and Grzesik, 2013). Hence, it is depicted that the credit process design aids the

management to understand the the amount of credit they can offer and the amount of balance

they can recover from the clients.

2.6 Risks

There exists credit management risks and it is essential for the credit team to assess the

risks that have been generated and the risks that may take place in the coming years. Therefore, it

is fundamental to consider the fact that credit processing design is constructed with the help of

mitigating the risks so that the process design is precise and effective in nature. The designing

and the analysis of the credit process design is useful for any financial organization and it is

essential for the companies to undertake assessment of time to time so that the policies can be

changed according to the changing needs in the market and incorporating the changes in the plan

so that new credit policies can be established with respect to the economy (Bank 2014). Credit

designing therefore plays a significant role and the effectiveness of the credit processing chain

would determine the efficiency of the financial institutions. Credit is demanded by each and

every organization and therefore it is the duty of the financial institutions to undertake to

construct effective policies and management strategies that would be influential for the financial

organizations to understand the each and every aspect of credit providing and recovering in order

to earn profit and maintain competitive edge for the organization.

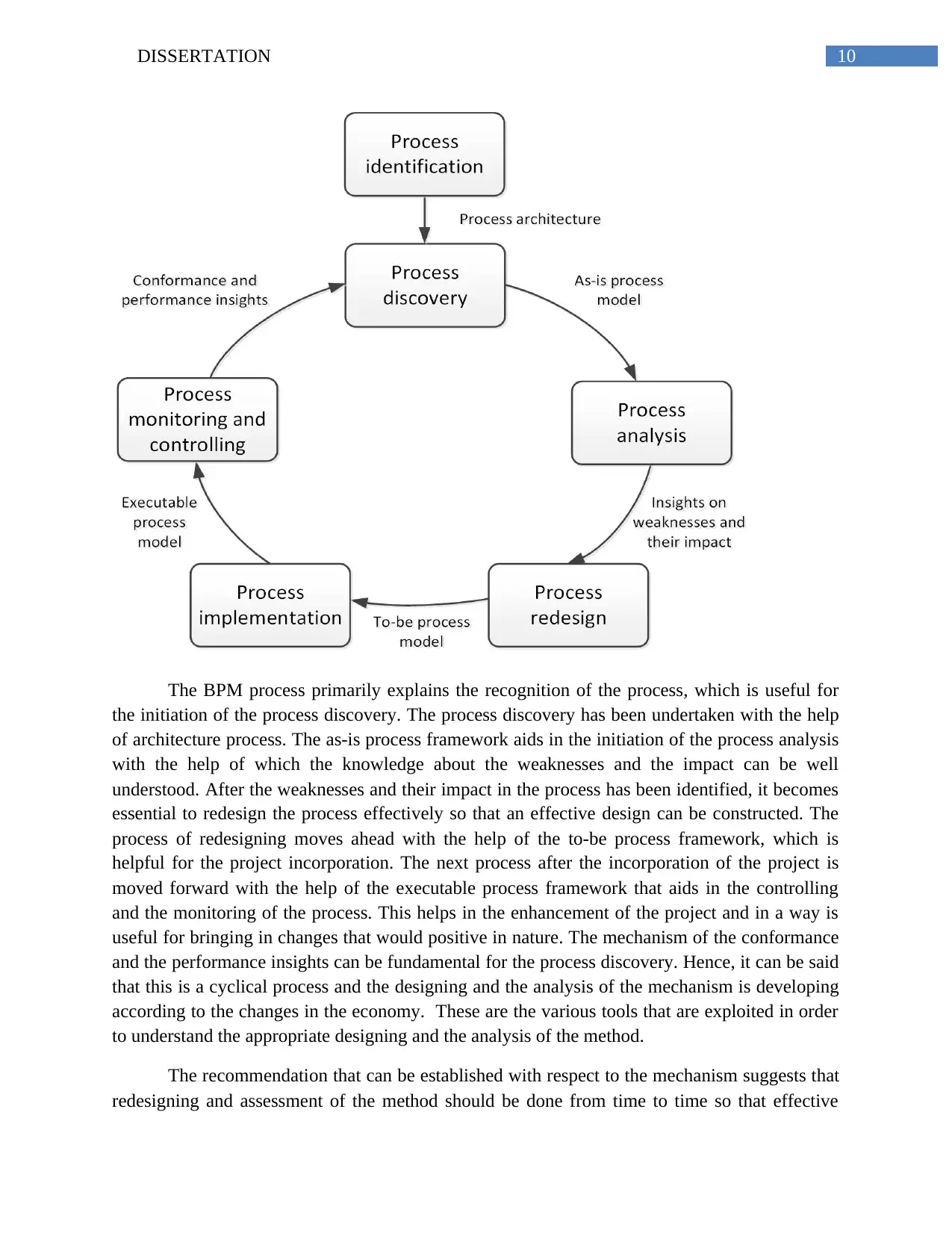

2.7 Business Process Modelling

The BPM lifecycle is fundamental for understanding the method used, the tools and the

approaches that would be useful for the development of effective design.

design the credit processing chain. The evaluation of the credit process design undertaken by the

credit managers as well as the portfolio managers. The managers scrutinise each and every

aspect of the design and tries to find out areas that are not providing adequate results. The

evaluation of the design is undertaken with respect to the aims and policies of the organization

(Źróbek and Grzesik, 2013). Hence, it is depicted that the credit process design aids the

management to understand the the amount of credit they can offer and the amount of balance

they can recover from the clients.

2.6 Risks

There exists credit management risks and it is essential for the credit team to assess the

risks that have been generated and the risks that may take place in the coming years. Therefore, it

is fundamental to consider the fact that credit processing design is constructed with the help of

mitigating the risks so that the process design is precise and effective in nature. The designing

and the analysis of the credit process design is useful for any financial organization and it is

essential for the companies to undertake assessment of time to time so that the policies can be

changed according to the changing needs in the market and incorporating the changes in the plan

so that new credit policies can be established with respect to the economy (Bank 2014). Credit

designing therefore plays a significant role and the effectiveness of the credit processing chain

would determine the efficiency of the financial institutions. Credit is demanded by each and

every organization and therefore it is the duty of the financial institutions to undertake to

construct effective policies and management strategies that would be influential for the financial

organizations to understand the each and every aspect of credit providing and recovering in order

to earn profit and maintain competitive edge for the organization.

2.7 Business Process Modelling

The BPM lifecycle is fundamental for understanding the method used, the tools and the

approaches that would be useful for the development of effective design.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10DISSERTATION

The BPM process primarily explains the recognition of the process, which is useful for

the initiation of the process discovery. The process discovery has been undertaken with the help

of architecture process. The as-is process framework aids in the initiation of the process analysis

with the help of which the knowledge about the weaknesses and the impact can be well

understood. After the weaknesses and their impact in the process has been identified, it becomes

essential to redesign the process effectively so that an effective design can be constructed. The

process of redesigning moves ahead with the help of the to-be process framework, which is

helpful for the project incorporation. The next process after the incorporation of the project is

moved forward with the help of the executable process framework that aids in the controlling

and the monitoring of the process. This helps in the enhancement of the project and in a way is

useful for bringing in changes that would positive in nature. The mechanism of the conformance

and the performance insights can be fundamental for the process discovery. Hence, it can be said

that this is a cyclical process and the designing and the analysis of the mechanism is developing

according to the changes in the economy. These are the various tools that are exploited in order

to understand the appropriate designing and the analysis of the method.

The recommendation that can be established with respect to the mechanism suggests that

redesigning and assessment of the method should be done from time to time so that effective

The BPM process primarily explains the recognition of the process, which is useful for

the initiation of the process discovery. The process discovery has been undertaken with the help

of architecture process. The as-is process framework aids in the initiation of the process analysis

with the help of which the knowledge about the weaknesses and the impact can be well

understood. After the weaknesses and their impact in the process has been identified, it becomes

essential to redesign the process effectively so that an effective design can be constructed. The

process of redesigning moves ahead with the help of the to-be process framework, which is

helpful for the project incorporation. The next process after the incorporation of the project is

moved forward with the help of the executable process framework that aids in the controlling

and the monitoring of the process. This helps in the enhancement of the project and in a way is

useful for bringing in changes that would positive in nature. The mechanism of the conformance

and the performance insights can be fundamental for the process discovery. Hence, it can be said

that this is a cyclical process and the designing and the analysis of the mechanism is developing

according to the changes in the economy. These are the various tools that are exploited in order

to understand the appropriate designing and the analysis of the method.

The recommendation that can be established with respect to the mechanism suggests that

redesigning and assessment of the method should be done from time to time so that effective

11DISSERTATION

measures can be taken in order to keep the mechanism updated and in line with the market so

that the process of BPM lifecycle can be used effectively.

measures can be taken in order to keep the mechanism updated and in line with the market so

that the process of BPM lifecycle can be used effectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.