Accounting and Financial Management: Westpac Group Reporting Analysis

VerifiedAdded on 2022/11/01

|14

|3758

|149

Report

AI Summary

This report provides a critical analysis of the external reporting practices of the Westpac Group, one of Australia's largest banking institutions. The analysis begins with an overview of the environmental and social effects of Westpac's operations, examining both positive contributions, such as financial programs and green energy projects, and potential negative impacts related to increased consumption and industrialization. The report then delves into the quality and depth of Westpac's environmental and social performance, discussing the challenges faced when applying the GRI framework and evaluating the potential benefits of compliance for stakeholders. Part B of the report outlines a strategic initiative, including a short internal briefing document, a balanced scorecard with key performance indicators across financial, customer, internal processes, and learning perspectives, and an evaluation of the initiative using break-even analysis to assess product viability. The conclusion summarizes the key findings and implications of the analysis.

Running head: ACCOUNTING AND FINANCIAL MANAGEMENT

1

External Reporting Of Westpac Group and Critique of Useful Information

Name of the Student

Name of the University

Author’s Note

1

External Reporting Of Westpac Group and Critique of Useful Information

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCIAL MANAGEMENT

2

Table of Contents

PART A: CRITICAL ANALYSIS..............................................................................3

Introduction.............................................................................................................3

An overview of the environmental and social effects of the operations..............3

Operations with a positive impact on the environment and the community....4

The negative impact of the operations.............................................................5

Quality and depth of the environmental and social performance........................6

Challenges faced with applying the GRI framework...........................................6

Whether compliance would benefit stakeholders................................................8

PART B: STRATEGIC INITIATIVE.........................................................................8

Short internal briefing document.........................................................................8

Balanced scorecard for a new initiative...............................................................9

A brief discussion of the key features on the scorecard................................11

Evaluating the initiative using break-even analysis...........................................12

Products need to break even.........................................................................12

Conclusion.........................................................................................................13

References........................................................................................................14

2

Table of Contents

PART A: CRITICAL ANALYSIS..............................................................................3

Introduction.............................................................................................................3

An overview of the environmental and social effects of the operations..............3

Operations with a positive impact on the environment and the community....4

The negative impact of the operations.............................................................5

Quality and depth of the environmental and social performance........................6

Challenges faced with applying the GRI framework...........................................6

Whether compliance would benefit stakeholders................................................8

PART B: STRATEGIC INITIATIVE.........................................................................8

Short internal briefing document.........................................................................8

Balanced scorecard for a new initiative...............................................................9

A brief discussion of the key features on the scorecard................................11

Evaluating the initiative using break-even analysis...........................................12

Products need to break even.........................................................................12

Conclusion.........................................................................................................13

References........................................................................................................14

ACCOUNTING AND FINANCIAL MANAGEMENT

3

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCIAL MANAGEMENT

4

PART A: CRITICAL ANALYSIS

Introduction

This section of the paper will majorly concentrate on assessing the information

provided by the company regarding the environmental concerns and other social

impacts that result from the firm's operations. Financial frameworks such as the GRI

(global reporting initiatives) will be used as the basis for making the analysis required in

this particular part of the paper. Summary covering the social impacts that result out of

the firm's operations challenges encountered while complying with the requirements of

the GRI framework and so on will be discussed. Evaluations regarding the possible

benefits to the different stakeholders such as investors, shareholders of the entity will be

provided.

An overview of the environmental and social effects of the operations

West Pac is one of Australia's oldest banks and it is among the four major

entities in Australia. The bank is also the largest banking institution in New Zealand

providing a wide range of consumer, business and institutional banking services among

others. In recent times, however, the bank has been involved in several operations that

have either positively or negatively affected the environment and the general community

(Nielsen and Nielsen, 2015).

Operations with a positive impact on the environment and the community

Among the most prevalent operations taken by the company is assisting various

individuals when it comes to making financial decisions. This is has been used as a way

of ensuring corporate social responsibility (Carp et al, 2018). In the long run, such an

activity will effectively rhyme with the requirements of the GRI framework thereby

ensuring sustainability. The west pac company has carried out such an operation

through activities such as making available products and services to aid customers with

decision making, implementing, financial health program, availing of financial training

among other activities. This has positively transformed the Australian community in

terms of financial knowledge and understanding. For instance, the bank through the

Davidson institute together with the managing your money program provided financial

education services to the citizens of both Australia and New Zealand.

West Pac Company limited has also undertaken various programs regarding

environmental conservation. This has made the company the largest financial provider

of different greenfield and renewable energy projects within Australia (Pro Bono News,

2013). For instance, the company lent out well over $6.2 billion in the year 2016

towards solving the problem of climate changes. This amount was increased to a total

of $ 7 billion in the following year of 2017(Chimtengo, Mkandawire and Hanif, 2017).

4

PART A: CRITICAL ANALYSIS

Introduction

This section of the paper will majorly concentrate on assessing the information

provided by the company regarding the environmental concerns and other social

impacts that result from the firm's operations. Financial frameworks such as the GRI

(global reporting initiatives) will be used as the basis for making the analysis required in

this particular part of the paper. Summary covering the social impacts that result out of

the firm's operations challenges encountered while complying with the requirements of

the GRI framework and so on will be discussed. Evaluations regarding the possible

benefits to the different stakeholders such as investors, shareholders of the entity will be

provided.

An overview of the environmental and social effects of the operations

West Pac is one of Australia's oldest banks and it is among the four major

entities in Australia. The bank is also the largest banking institution in New Zealand

providing a wide range of consumer, business and institutional banking services among

others. In recent times, however, the bank has been involved in several operations that

have either positively or negatively affected the environment and the general community

(Nielsen and Nielsen, 2015).

Operations with a positive impact on the environment and the community

Among the most prevalent operations taken by the company is assisting various

individuals when it comes to making financial decisions. This is has been used as a way

of ensuring corporate social responsibility (Carp et al, 2018). In the long run, such an

activity will effectively rhyme with the requirements of the GRI framework thereby

ensuring sustainability. The west pac company has carried out such an operation

through activities such as making available products and services to aid customers with

decision making, implementing, financial health program, availing of financial training

among other activities. This has positively transformed the Australian community in

terms of financial knowledge and understanding. For instance, the bank through the

Davidson institute together with the managing your money program provided financial

education services to the citizens of both Australia and New Zealand.

West Pac Company limited has also undertaken various programs regarding

environmental conservation. This has made the company the largest financial provider

of different greenfield and renewable energy projects within Australia (Pro Bono News,

2013). For instance, the company lent out well over $6.2 billion in the year 2016

towards solving the problem of climate changes. This amount was increased to a total

of $ 7 billion in the following year of 2017(Chimtengo, Mkandawire and Hanif, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCIAL MANAGEMENT

5

From such operations, the environmental conservation has been improved and

enhanced throughout Australia and New Zealand at large.

Together with the World Bank, west pac launched development sustainable

growth bonds throughout Australia. The major beneficiaries of such bonds were the

Australian investors who were interested in providing support to sustainable

development goals (SDGs) (West Pac, 2018). The other important aspect of such

development bonds is that they were also aiming at eliminating poverty and create

opportunities for a variety of individuals. The outcomes of such an arrangement with the

World Bank would sustainably result in improved standards of living for people hence

promoting social benefit in general.

The negative impact of the operations

The negative impacts that may are likely to result out of the company’s

operations are rather indirect. This is because the company operates under guidelines

to improve and support climate change conditions of the nearby future. However some

of the projects that the bank tend to increase or promote economic consumption.

Therefore, according to the environmentalists, an increased rate of consumption would

in an economy consequently and negatively affects the environment (The World Bank,

2018). An increase in economic growth implies that there is a higher consumption level

and purchasing power, however, high levels of purchasing power and consumption,

additional pressure is exerted on to the environmental resources. Ultimately this leads

to resource depletion in the long run. Alternatively, the increased and continued funding

of electricity programs would consequently result in environmental damage in the long

run (Zimmermann, 2019). The argument from such a perspective is that when these

huge amounts of electricity are generated the outcome is increased industrialization.

The result of such an increased rate of industrialization is environmental pollution

(Korzeb and Medina, 2019).

The need for increased innovation and technological advancement is a positive

operation that should be embraced; however, the excessive technological

advancements would result in negative impacts on the social well being of humanity.

With the need to reduce operating costs, banks such as west Pac Company have over

the years adapted technology as one way of reducing costs of operations. On the

negative side, however, continued use of such technological methods of operation is

most likely to result in tendencies of unemployment for the Australian citizens and the

general public. Socially unemployment, in the long run, would increase the cost of living

and reduced purchasing power.

Quality and depth of the environmental and social performance

In the finical sector banks have played a vital duty in achieving sustainable

development programs. It is through such operations that they have led to

improvements and changes in the environment and the ecological system together with

transforming the social perspective of humanity (Fonseca, 2010). With a major

emphasis on their role of providing financial services, banks such s wets pac and others

have also taken the concern to address the need for social and environmental

requirements. this is effectively done through providing ‘financial services and as the

5

From such operations, the environmental conservation has been improved and

enhanced throughout Australia and New Zealand at large.

Together with the World Bank, west pac launched development sustainable

growth bonds throughout Australia. The major beneficiaries of such bonds were the

Australian investors who were interested in providing support to sustainable

development goals (SDGs) (West Pac, 2018). The other important aspect of such

development bonds is that they were also aiming at eliminating poverty and create

opportunities for a variety of individuals. The outcomes of such an arrangement with the

World Bank would sustainably result in improved standards of living for people hence

promoting social benefit in general.

The negative impact of the operations

The negative impacts that may are likely to result out of the company’s

operations are rather indirect. This is because the company operates under guidelines

to improve and support climate change conditions of the nearby future. However some

of the projects that the bank tend to increase or promote economic consumption.

Therefore, according to the environmentalists, an increased rate of consumption would

in an economy consequently and negatively affects the environment (The World Bank,

2018). An increase in economic growth implies that there is a higher consumption level

and purchasing power, however, high levels of purchasing power and consumption,

additional pressure is exerted on to the environmental resources. Ultimately this leads

to resource depletion in the long run. Alternatively, the increased and continued funding

of electricity programs would consequently result in environmental damage in the long

run (Zimmermann, 2019). The argument from such a perspective is that when these

huge amounts of electricity are generated the outcome is increased industrialization.

The result of such an increased rate of industrialization is environmental pollution

(Korzeb and Medina, 2019).

The need for increased innovation and technological advancement is a positive

operation that should be embraced; however, the excessive technological

advancements would result in negative impacts on the social well being of humanity.

With the need to reduce operating costs, banks such as west Pac Company have over

the years adapted technology as one way of reducing costs of operations. On the

negative side, however, continued use of such technological methods of operation is

most likely to result in tendencies of unemployment for the Australian citizens and the

general public. Socially unemployment, in the long run, would increase the cost of living

and reduced purchasing power.

Quality and depth of the environmental and social performance

In the finical sector banks have played a vital duty in achieving sustainable

development programs. It is through such operations that they have led to

improvements and changes in the environment and the ecological system together with

transforming the social perspective of humanity (Fonseca, 2010). With a major

emphasis on their role of providing financial services, banks such s wets pac and others

have also taken the concern to address the need for social and environmental

requirements. this is effectively done through providing ‘financial services and as the

ACCOUNTING AND FINANCIAL MANAGEMENT

6

same supporting external sustainable projects. It is of no doubt that the wets Pac

Company is emphasizing such sustainable projects and operations aimed at achieving

sustainability and environmental conservation (Australian Government, 2017).

Challenges faced with applying the GRI framework

The growing demand and the prevailing variety of stakeholder needs and

interests effectively resulted in the need for a wider mode of reporting and presenting

financial data and information. It is such a scenario that rendered the conventional

approach of accounting weak and unable to satisfy stakeholder needs. However,

despite its numerous benefits and importance, the GRI reporting framework has been

associated with several shortcomings. The following discussions, present a detailed

presentation of the challenges associated with the GRI reporting framework.

The framework focuses on the internal aspects of organizational performance

and less on the need for detailed and complex analyses of the existing relationship

between the organization and the external environment. The concentration on the

internal performance of the entity or organization results in exposure to several risks.

Among such risks includes disclosing information that may violate the relationship

between the entities and the surrounding environment.

The other outstanding challenge that is associated with the GRI framework is the

failure to identify the exact audience addressed. For instance, certain companies

operate in a wide range of societies that have extremely different conditions and

environment. However, the framework does not provide a clear view that specifies the

exact community of environmental surrounding being addressed. This ultimately leaves

out a large number of stakeholders’ concerns unanswered (De Burgwal and Viera,

2014).

Whether compliance would benefit stakeholders

The evaluation to assess the possible benefits of the framework are sometimes

subjected to debate. However, besides the few pronounced shortcomings associated

with the framework, there is a high possibility that the framework would generate

benefits. For example stakeholder such as the surrounding community would effectively

benefit from such disclosures required by the GRI framework (Miralles-Quiros, Miralles-

Quiros, and Goncalves, 2018). This is due t the fact that an entity will ensure that social

responsibility is enhanced since the failure to observe this would lead to business

collapse. The community and general surrounding of business entity would find it most

important to understand the general performance of the organization (Lellahom, 2013).

In so the community is majorly interested in observing and protecting the environment

and perhaps the societal gains and objectives. Therefore, the need to live in harmony

with the surrounding community would result in corporate social responsibility in the

long run.

6

same supporting external sustainable projects. It is of no doubt that the wets Pac

Company is emphasizing such sustainable projects and operations aimed at achieving

sustainability and environmental conservation (Australian Government, 2017).

Challenges faced with applying the GRI framework

The growing demand and the prevailing variety of stakeholder needs and

interests effectively resulted in the need for a wider mode of reporting and presenting

financial data and information. It is such a scenario that rendered the conventional

approach of accounting weak and unable to satisfy stakeholder needs. However,

despite its numerous benefits and importance, the GRI reporting framework has been

associated with several shortcomings. The following discussions, present a detailed

presentation of the challenges associated with the GRI reporting framework.

The framework focuses on the internal aspects of organizational performance

and less on the need for detailed and complex analyses of the existing relationship

between the organization and the external environment. The concentration on the

internal performance of the entity or organization results in exposure to several risks.

Among such risks includes disclosing information that may violate the relationship

between the entities and the surrounding environment.

The other outstanding challenge that is associated with the GRI framework is the

failure to identify the exact audience addressed. For instance, certain companies

operate in a wide range of societies that have extremely different conditions and

environment. However, the framework does not provide a clear view that specifies the

exact community of environmental surrounding being addressed. This ultimately leaves

out a large number of stakeholders’ concerns unanswered (De Burgwal and Viera,

2014).

Whether compliance would benefit stakeholders

The evaluation to assess the possible benefits of the framework are sometimes

subjected to debate. However, besides the few pronounced shortcomings associated

with the framework, there is a high possibility that the framework would generate

benefits. For example stakeholder such as the surrounding community would effectively

benefit from such disclosures required by the GRI framework (Miralles-Quiros, Miralles-

Quiros, and Goncalves, 2018). This is due t the fact that an entity will ensure that social

responsibility is enhanced since the failure to observe this would lead to business

collapse. The community and general surrounding of business entity would find it most

important to understand the general performance of the organization (Lellahom, 2013).

In so the community is majorly interested in observing and protecting the environment

and perhaps the societal gains and objectives. Therefore, the need to live in harmony

with the surrounding community would result in corporate social responsibility in the

long run.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCIAL MANAGEMENT

7

PART B: STRATEGIC INITIATIVE

A short internal briefing document

The briefing document is simply an insight into the aspects surrounding the new

product line. It, therefore, involves an analysis of different factors that may affect the

demand and consumption of the products to be released on the market. The briefing

document for the new product line is therefore discussed below:

The new strategic initiative to develop a range of products that the company

intends s to offer on the market will involve several activities before the actual launch on

the market. There is a need to understand the different specifications that are very vital

before in the early stages of the product. For instance, the size, the pricing strategy that

will be used, the target market and so many other variables will require assessment.

Factors such as competition from the existing products already on the market will also

be an important aspect of consideration. Therefore, the marketing and sales department

will have the duty to devise all such necessary steps before the actual launch of the

product line. Some of the possible strategies that can be used to overcome these

constraints such as the existing competitors in the market may include the use of

promotional sales. This particular strategy will require aggressive advertisements to

create market awareness.

The costs involved in promoting the product on the market will include the fixed,

variable and semi-variable costs. The variable costs, for example, are those that will

change with the level of output, the fixed, on the other hand, will remain constant

irrespective of the level of output. For instance, payments made to marketing,

managers are some of the fixed costs that may not vary with the level of sales realized.

Salaries made to the production managers a well will not depend on the level of output

and the costs of research and development will be among the fixed costs of the new

initiative. Such costs are what are classified as the fixed costs of launching a new

product line on the market. The variable costs of the initiative will, however, include the

costs of raw materials, sales commissions that may be offered to the advertising and

promotional teams, utility costs such as water and electricity and so many others.

Balanced scorecard for the new initiative

A balanced scorecard is performance measure or metric that is used by

managers when carrying out processes of identifying and improving certain internal

aspects of a business as well as the resulting external outcomes. It is, therefore, a tool

used for measuring and providing feedback to organizations concerning the activities

undertaken. A balanced scored card for the new initiative will, therefore, be developed

and it will cover four major perspectives (Munoz, Zhao, and Yang, 2017). These will

include the customer perspective, the financial perspective, the learning and growth and

lastly the internal business processes. The objectives of each of these perspectives will

as well be present ted within the scorecard template that is provided as below:

balanced scorecard

pers

pective Objective measures

7

PART B: STRATEGIC INITIATIVE

A short internal briefing document

The briefing document is simply an insight into the aspects surrounding the new

product line. It, therefore, involves an analysis of different factors that may affect the

demand and consumption of the products to be released on the market. The briefing

document for the new product line is therefore discussed below:

The new strategic initiative to develop a range of products that the company

intends s to offer on the market will involve several activities before the actual launch on

the market. There is a need to understand the different specifications that are very vital

before in the early stages of the product. For instance, the size, the pricing strategy that

will be used, the target market and so many other variables will require assessment.

Factors such as competition from the existing products already on the market will also

be an important aspect of consideration. Therefore, the marketing and sales department

will have the duty to devise all such necessary steps before the actual launch of the

product line. Some of the possible strategies that can be used to overcome these

constraints such as the existing competitors in the market may include the use of

promotional sales. This particular strategy will require aggressive advertisements to

create market awareness.

The costs involved in promoting the product on the market will include the fixed,

variable and semi-variable costs. The variable costs, for example, are those that will

change with the level of output, the fixed, on the other hand, will remain constant

irrespective of the level of output. For instance, payments made to marketing,

managers are some of the fixed costs that may not vary with the level of sales realized.

Salaries made to the production managers a well will not depend on the level of output

and the costs of research and development will be among the fixed costs of the new

initiative. Such costs are what are classified as the fixed costs of launching a new

product line on the market. The variable costs of the initiative will, however, include the

costs of raw materials, sales commissions that may be offered to the advertising and

promotional teams, utility costs such as water and electricity and so many others.

Balanced scorecard for the new initiative

A balanced scorecard is performance measure or metric that is used by

managers when carrying out processes of identifying and improving certain internal

aspects of a business as well as the resulting external outcomes. It is, therefore, a tool

used for measuring and providing feedback to organizations concerning the activities

undertaken. A balanced scored card for the new initiative will, therefore, be developed

and it will cover four major perspectives (Munoz, Zhao, and Yang, 2017). These will

include the customer perspective, the financial perspective, the learning and growth and

lastly the internal business processes. The objectives of each of these perspectives will

as well be present ted within the scorecard template that is provided as below:

balanced scorecard

pers

pective Objective measures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCIAL MANAGEMENT

8

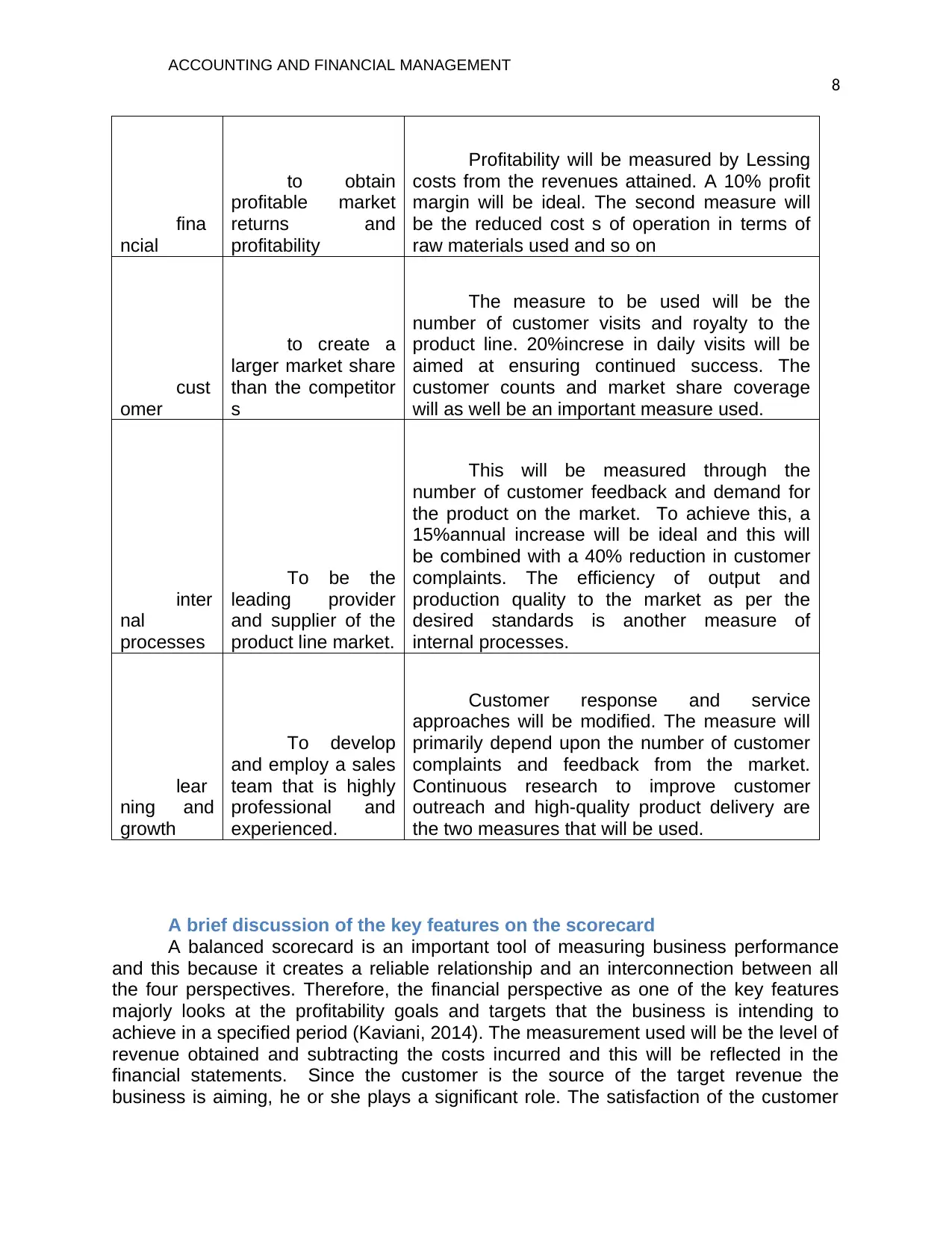

fina

ncial

to obtain

profitable market

returns and

profitability

Profitability will be measured by Lessing

costs from the revenues attained. A 10% profit

margin will be ideal. The second measure will

be the reduced cost s of operation in terms of

raw materials used and so on

cust

omer

to create a

larger market share

than the competitor

s

The measure to be used will be the

number of customer visits and royalty to the

product line. 20%increse in daily visits will be

aimed at ensuring continued success. The

customer counts and market share coverage

will as well be an important measure used.

inter

nal

processes

To be the

leading provider

and supplier of the

product line market.

This will be measured through the

number of customer feedback and demand for

the product on the market. To achieve this, a

15%annual increase will be ideal and this will

be combined with a 40% reduction in customer

complaints. The efficiency of output and

production quality to the market as per the

desired standards is another measure of

internal processes.

lear

ning and

growth

To develop

and employ a sales

team that is highly

professional and

experienced.

Customer response and service

approaches will be modified. The measure will

primarily depend upon the number of customer

complaints and feedback from the market.

Continuous research to improve customer

outreach and high-quality product delivery are

the two measures that will be used.

A brief discussion of the key features on the scorecard

A balanced scorecard is an important tool of measuring business performance

and this because it creates a reliable relationship and an interconnection between all

the four perspectives. Therefore, the financial perspective as one of the key features

majorly looks at the profitability goals and targets that the business is intending to

achieve in a specified period (Kaviani, 2014). The measurement used will be the level of

revenue obtained and subtracting the costs incurred and this will be reflected in the

financial statements. Since the customer is the source of the target revenue the

business is aiming, he or she plays a significant role. The satisfaction of the customer

8

fina

ncial

to obtain

profitable market

returns and

profitability

Profitability will be measured by Lessing

costs from the revenues attained. A 10% profit

margin will be ideal. The second measure will

be the reduced cost s of operation in terms of

raw materials used and so on

cust

omer

to create a

larger market share

than the competitor

s

The measure to be used will be the

number of customer visits and royalty to the

product line. 20%increse in daily visits will be

aimed at ensuring continued success. The

customer counts and market share coverage

will as well be an important measure used.

inter

nal

processes

To be the

leading provider

and supplier of the

product line market.

This will be measured through the

number of customer feedback and demand for

the product on the market. To achieve this, a

15%annual increase will be ideal and this will

be combined with a 40% reduction in customer

complaints. The efficiency of output and

production quality to the market as per the

desired standards is another measure of

internal processes.

lear

ning and

growth

To develop

and employ a sales

team that is highly

professional and

experienced.

Customer response and service

approaches will be modified. The measure will

primarily depend upon the number of customer

complaints and feedback from the market.

Continuous research to improve customer

outreach and high-quality product delivery are

the two measures that will be used.

A brief discussion of the key features on the scorecard

A balanced scorecard is an important tool of measuring business performance

and this because it creates a reliable relationship and an interconnection between all

the four perspectives. Therefore, the financial perspective as one of the key features

majorly looks at the profitability goals and targets that the business is intending to

achieve in a specified period (Kaviani, 2014). The measurement used will be the level of

revenue obtained and subtracting the costs incurred and this will be reflected in the

financial statements. Since the customer is the source of the target revenue the

business is aiming, he or she plays a significant role. The satisfaction of the customer

ACCOUNTING AND FINANCIAL MANAGEMENT

9

needs is one of the objectives for producing the product line. Satisfying the customer

needs wants will likewise lead to increase market share. The business processes as

another key feature specifically look at the activities that are carried out if customer

satisfaction is to be achieved. Therefore the measurement to assess whether

satisfaction is being achieved is the number of customer feedback and similarly the type

of feedback. The rate of customer feedback will be expected to increase by around 15%

and a reduction of complaints by 40% annually (Awadallah and Allam, 2015). Learning

and growth as one of the key features of the scorecard will focus on the ability to attain

sustainability.thi will therefore involve continuous market research so as to come up with

new and better way of promoting efficiency within the market and improve on the quality

of output (Jakupi et al,2017). The learning and growth, therefore, will be analyzed

through coming up with alternative methods of supplying as well as promoting more

intensive training of different individuals. With a highly trained workforce, output is much

likely to be of high quality and hence increasing market share.

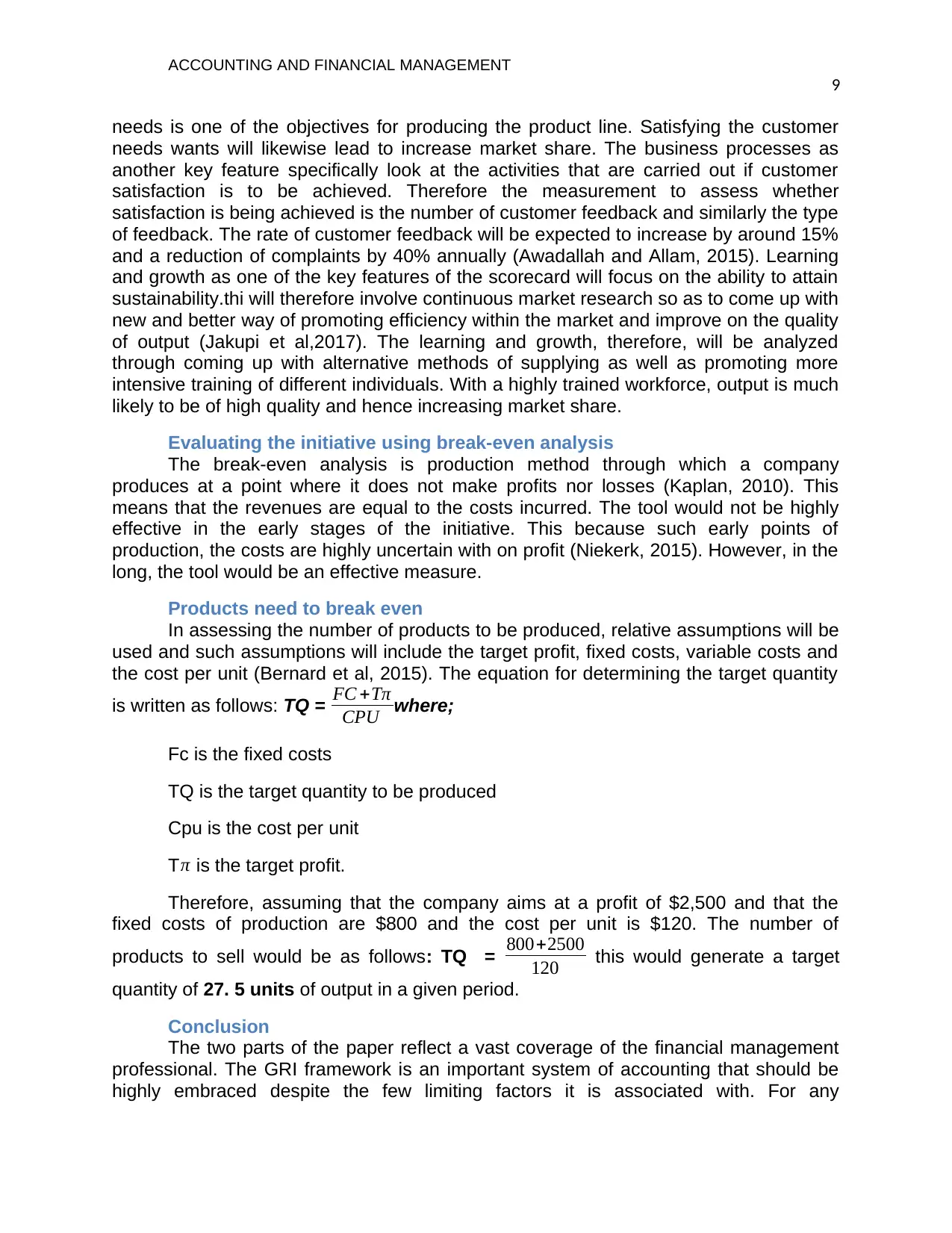

Evaluating the initiative using break-even analysis

The break-even analysis is production method through which a company

produces at a point where it does not make profits nor losses (Kaplan, 2010). This

means that the revenues are equal to the costs incurred. The tool would not be highly

effective in the early stages of the initiative. This because such early points of

production, the costs are highly uncertain with on profit (Niekerk, 2015). However, in the

long, the tool would be an effective measure.

Products need to break even

In assessing the number of products to be produced, relative assumptions will be

used and such assumptions will include the target profit, fixed costs, variable costs and

the cost per unit (Bernard et al, 2015). The equation for determining the target quantity

is written as follows: TQ = FC +Tπ

CPU where;

Fc is the fixed costs

TQ is the target quantity to be produced

Cpu is the cost per unit

Tπ is the target profit.

Therefore, assuming that the company aims at a profit of $2,500 and that the

fixed costs of production are $800 and the cost per unit is $120. The number of

products to sell would be as follows: TQ = 800+2500

120 this would generate a target

quantity of 27. 5 units of output in a given period.

Conclusion

The two parts of the paper reflect a vast coverage of the financial management

professional. The GRI framework is an important system of accounting that should be

highly embraced despite the few limiting factors it is associated with. For any

9

needs is one of the objectives for producing the product line. Satisfying the customer

needs wants will likewise lead to increase market share. The business processes as

another key feature specifically look at the activities that are carried out if customer

satisfaction is to be achieved. Therefore the measurement to assess whether

satisfaction is being achieved is the number of customer feedback and similarly the type

of feedback. The rate of customer feedback will be expected to increase by around 15%

and a reduction of complaints by 40% annually (Awadallah and Allam, 2015). Learning

and growth as one of the key features of the scorecard will focus on the ability to attain

sustainability.thi will therefore involve continuous market research so as to come up with

new and better way of promoting efficiency within the market and improve on the quality

of output (Jakupi et al,2017). The learning and growth, therefore, will be analyzed

through coming up with alternative methods of supplying as well as promoting more

intensive training of different individuals. With a highly trained workforce, output is much

likely to be of high quality and hence increasing market share.

Evaluating the initiative using break-even analysis

The break-even analysis is production method through which a company

produces at a point where it does not make profits nor losses (Kaplan, 2010). This

means that the revenues are equal to the costs incurred. The tool would not be highly

effective in the early stages of the initiative. This because such early points of

production, the costs are highly uncertain with on profit (Niekerk, 2015). However, in the

long, the tool would be an effective measure.

Products need to break even

In assessing the number of products to be produced, relative assumptions will be

used and such assumptions will include the target profit, fixed costs, variable costs and

the cost per unit (Bernard et al, 2015). The equation for determining the target quantity

is written as follows: TQ = FC +Tπ

CPU where;

Fc is the fixed costs

TQ is the target quantity to be produced

Cpu is the cost per unit

Tπ is the target profit.

Therefore, assuming that the company aims at a profit of $2,500 and that the

fixed costs of production are $800 and the cost per unit is $120. The number of

products to sell would be as follows: TQ = 800+2500

120 this would generate a target

quantity of 27. 5 units of output in a given period.

Conclusion

The two parts of the paper reflect a vast coverage of the financial management

professional. The GRI framework is an important system of accounting that should be

highly embraced despite the few limiting factors it is associated with. For any

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCIAL MANAGEMENT

10

organization intending to develop a new product line of the market chronological steps

to assess the viability are a vital requirement that must be taken into consideration if

success is to be achieved in the long run.

10

organization intending to develop a new product line of the market chronological steps

to assess the viability are a vital requirement that must be taken into consideration if

success is to be achieved in the long run.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCIAL MANAGEMENT

11

References

Pro Bono News,(2013). Sustainability Reporting – Challenges And Benefits. Retrieved

from https://probonoaustralia.com.au/news/2013/02/sustainability-reporting-

challenges-and-benefits/

Fonseca, A.(2010). Barriers to Strengthening the Global Reporting Initiative Framework:

Exploring The Perceptions Of Consultants, Practitioners, And Researchers.

Retrieved from

https://www.researchgate.net/publication/267247687_Barriers_to_Strengthening

_the_Global_Reporting_Initiative_Framework_Exploring_the_perceptions_of_co

nsultants_practitioners_and_researchers

Lellahom, M., B. (2013). Sustainability Reporting Challenges. retrieved from

https://www.sharnoffsglobalviews.com/sustainability-reports-100/

The World Bank. (2018). World Bank, Westpac Launch First Sustainable Growth Bonds

In Australia. Retrieved from

https://www.worldbank.org/en/news/press-release/2018/11/20/world-bank-

westpac-launch-first-sustainable-growth-bonds-in-australia

Australian Government; Department of the Environment And Energy (2017). Carbon

Neutral Stories- Westpac. Retrieved from

https://www.environment.gov.au/climate-change/government/carbon-neutral/

publications/factsheet-westpac

11

References

Pro Bono News,(2013). Sustainability Reporting – Challenges And Benefits. Retrieved

from https://probonoaustralia.com.au/news/2013/02/sustainability-reporting-

challenges-and-benefits/

Fonseca, A.(2010). Barriers to Strengthening the Global Reporting Initiative Framework:

Exploring The Perceptions Of Consultants, Practitioners, And Researchers.

Retrieved from

https://www.researchgate.net/publication/267247687_Barriers_to_Strengthening

_the_Global_Reporting_Initiative_Framework_Exploring_the_perceptions_of_co

nsultants_practitioners_and_researchers

Lellahom, M., B. (2013). Sustainability Reporting Challenges. retrieved from

https://www.sharnoffsglobalviews.com/sustainability-reports-100/

The World Bank. (2018). World Bank, Westpac Launch First Sustainable Growth Bonds

In Australia. Retrieved from

https://www.worldbank.org/en/news/press-release/2018/11/20/world-bank-

westpac-launch-first-sustainable-growth-bonds-in-australia

Australian Government; Department of the Environment And Energy (2017). Carbon

Neutral Stories- Westpac. Retrieved from

https://www.environment.gov.au/climate-change/government/carbon-neutral/

publications/factsheet-westpac

ACCOUNTING AND FINANCIAL MANAGEMENT

12

West Pac,(2018). $ 8.5 Bn Lent to Climate Change Solutions, An We’re Just Getting

Started. Retrieved from

https://www.westpac.com.au/about-westpac/sustainability/news-resources-and-

ratings/29-may-2018-climate/

De Burgwal, D., V., Viera, J., O., (2014). Environmental Disclosure Determinants In

Dutch Listed Companies. Retrieved from http://dx.doi.org/10.1590/S1519-

70772014000100006

Munoz, E., Zhao, L., Yang, D. (2017). Issues In Sustainability Accounting Reporting:

Accounting And Research. Retrieved from

file:///C:/Users/CLIENT/Downloads/Documents/11994-41474-1-SM.pdf

Miralles-Quiros, M., M., Miralles-Quiros, J., L., Goncalves, L., M., V. (2018). The Value

Relevance Of Environmental, Societal, And Governance Performance: The

Brazilian Case. Retrieved from

file:///C:/Users/CLIENT/Downloads/Documents/sustainability-10-00574.pdf

Carp, M., Pavaloaia, L., Afrasinei, M., B., Georgesu, L., E. (2018). Is Sustainability

Reporting A Business Strategy For Firm’s Growth? Empirical Study on the

Romanian Capital Market. Retrieved from

file:///C:/Users/CLIENT/Downloads/Documents/sustainability-11-00658.pdf

Zimmermann, S., (2019). Same Same But Different: How And Why Banks Approach

Sustainability. Retrieved from

file:///C:/Users/CLIENT/Downloads/Documents/sustainability-11-02267-v2.pdf

12

West Pac,(2018). $ 8.5 Bn Lent to Climate Change Solutions, An We’re Just Getting

Started. Retrieved from

https://www.westpac.com.au/about-westpac/sustainability/news-resources-and-

ratings/29-may-2018-climate/

De Burgwal, D., V., Viera, J., O., (2014). Environmental Disclosure Determinants In

Dutch Listed Companies. Retrieved from http://dx.doi.org/10.1590/S1519-

70772014000100006

Munoz, E., Zhao, L., Yang, D. (2017). Issues In Sustainability Accounting Reporting:

Accounting And Research. Retrieved from

file:///C:/Users/CLIENT/Downloads/Documents/11994-41474-1-SM.pdf

Miralles-Quiros, M., M., Miralles-Quiros, J., L., Goncalves, L., M., V. (2018). The Value

Relevance Of Environmental, Societal, And Governance Performance: The

Brazilian Case. Retrieved from

file:///C:/Users/CLIENT/Downloads/Documents/sustainability-10-00574.pdf

Carp, M., Pavaloaia, L., Afrasinei, M., B., Georgesu, L., E. (2018). Is Sustainability

Reporting A Business Strategy For Firm’s Growth? Empirical Study on the

Romanian Capital Market. Retrieved from

file:///C:/Users/CLIENT/Downloads/Documents/sustainability-11-00658.pdf

Zimmermann, S., (2019). Same Same But Different: How And Why Banks Approach

Sustainability. Retrieved from

file:///C:/Users/CLIENT/Downloads/Documents/sustainability-11-02267-v2.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.