Strategic Management Accounting: Financial Analysis of Westpac

VerifiedAdded on 2023/06/12

|8

|1224

|311

Report

AI Summary

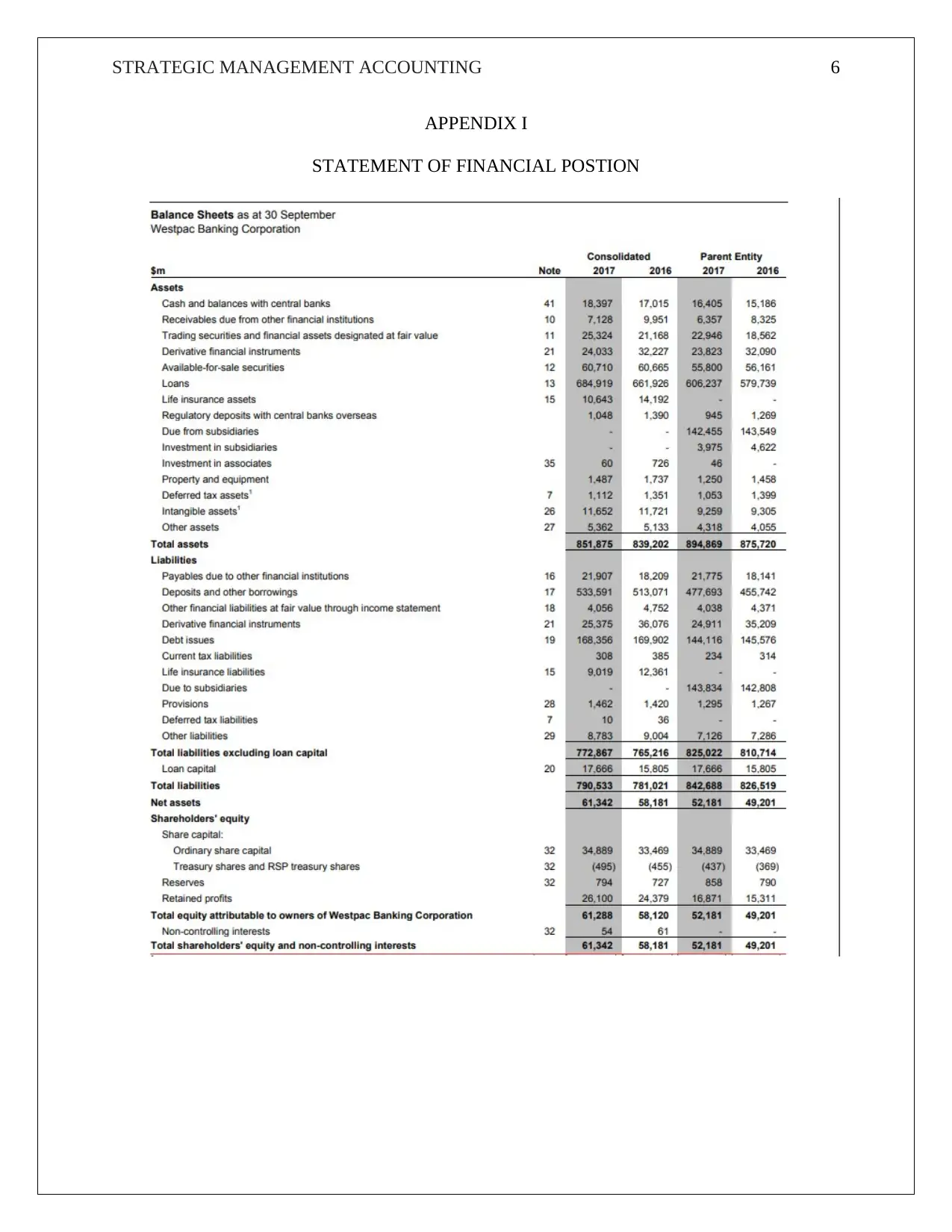

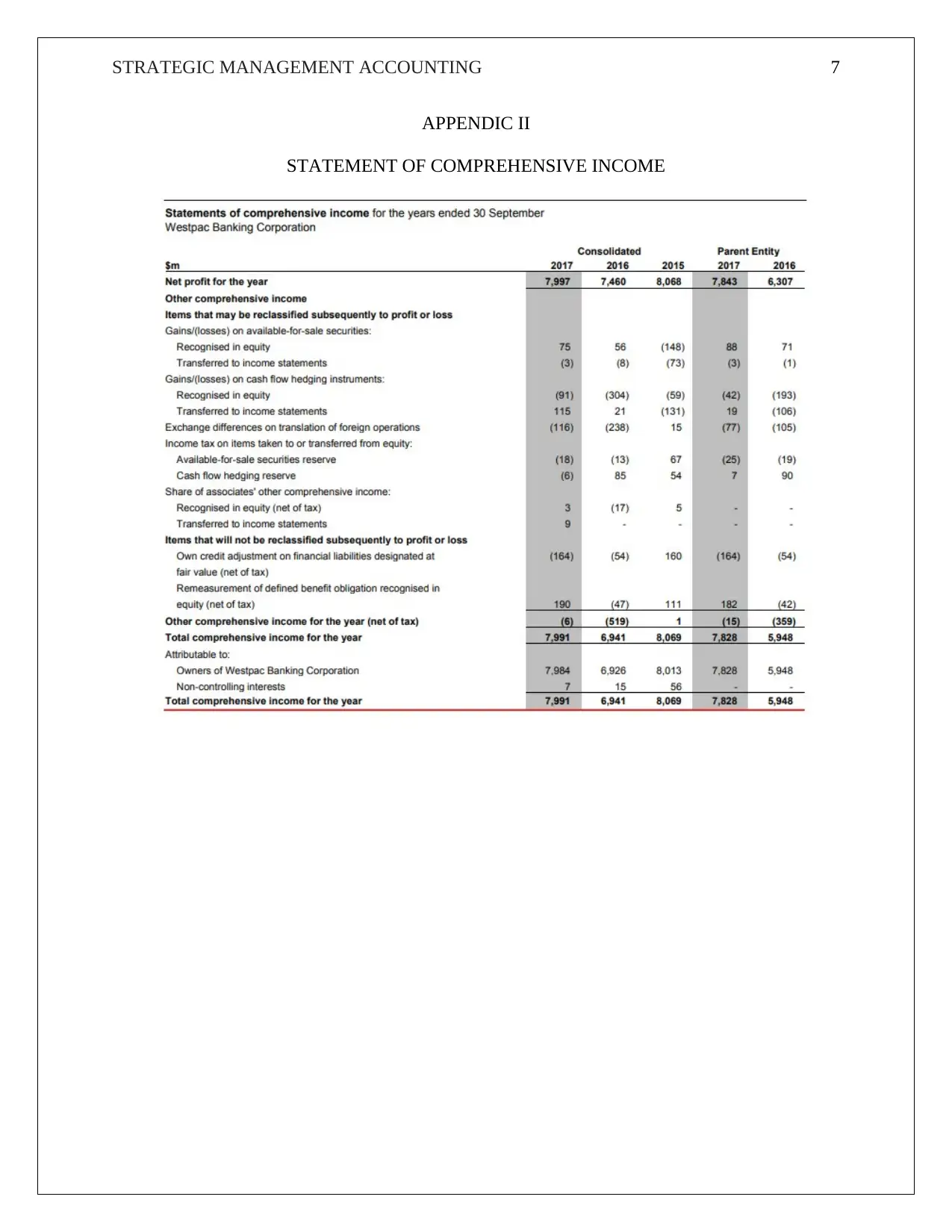

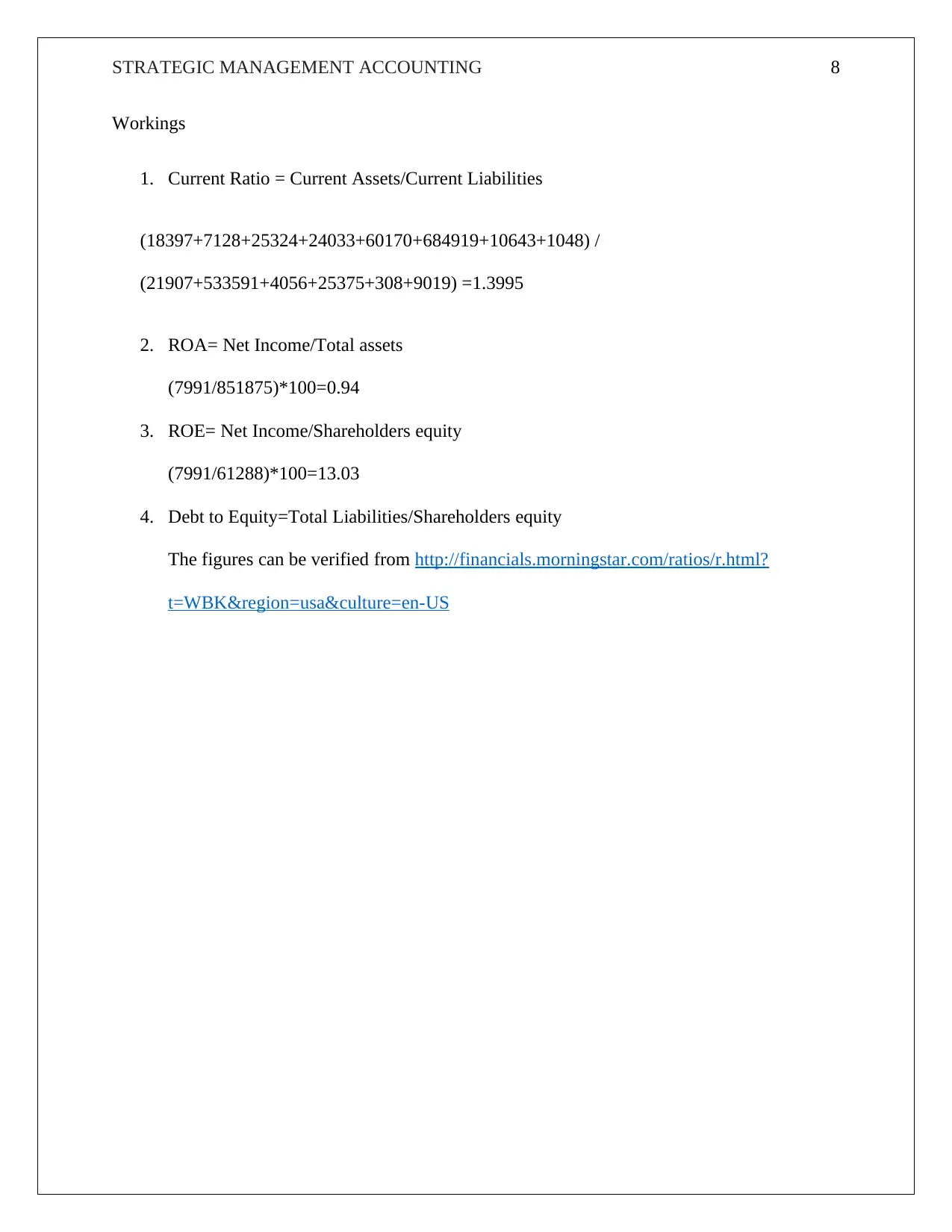

This report provides a comprehensive financial performance evaluation of Westpac Banking Corporation using strategic management accounting principles. It assesses liquidity, activity, profitability, and leverage ratios derived from Westpac's 2017 annual report, including the current ratio, ROA, ROE, and debt-to-equity ratio. The analysis interprets these ratios to provide insights into Westpac's ability to meet obligations, efficiently utilize assets, generate returns for shareholders, and manage debt. The report also emphasizes the importance of comparing these ratios with industry peers to gain a more meaningful understanding of Westpac's financial standing and strategic effectiveness. Financial statements are provided from the annual report with calculations to support the findings.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.