Whitehaven Coal Ltd: Financial Ratio Analysis and Comparison Report

VerifiedAdded on 2021/06/17

|11

|2419

|34

Report

AI Summary

This report provides a comprehensive financial analysis of Whitehaven Coal Ltd, focusing on the calculation and interpretation of key financial ratios, including current ratio, quick ratio, gross profit margin, return on equity, and return on assets. The analysis compares Whitehaven Coal Ltd's performance with two other companies in the same industry, Wollongong Coal Ltd and White Energy Co Ltd, using data from 2016 and 2017. The report examines the company's liquidity, profitability, and efficiency, offering insights into its financial health and making recommendations to potential shareholders regarding investment decisions. The executive summary highlights the core objectives, including the analysis of financial statements, computation of key ratios, comparison with industry peers, and the provision of investment recommendations.

Running head: ACCOUNTING FOR BUSINESS

Accounting for Business

Name of the Student:

Name of the University:

Author’s Note:

Accounting for Business

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING FOR BUSINESS

Executive Summary

The main purpose of this assignment is to analyze the financial statements of Whitehaven Coal

ltd and compute significant key financial ratios of the business. The key ratios which are selected

are to be discussed and then analyzed for the purpose of this assignment. The assignment will

also be selecting two other companies which belong to the same Industry and the comparing the

performance of Whitehaven Coal ltd. The assignment will be recommending to potential

shareholders as to whether they should invest in the shares of the company.

ACCOUNTING FOR BUSINESS

Executive Summary

The main purpose of this assignment is to analyze the financial statements of Whitehaven Coal

ltd and compute significant key financial ratios of the business. The key ratios which are selected

are to be discussed and then analyzed for the purpose of this assignment. The assignment will

also be selecting two other companies which belong to the same Industry and the comparing the

performance of Whitehaven Coal ltd. The assignment will be recommending to potential

shareholders as to whether they should invest in the shares of the company.

2

ACCOUNTING FOR BUSINESS

Table of Contents

Introduction......................................................................................................................................3

Overview of the Company...............................................................................................................3

Ratio Analysis..................................................................................................................................3

Current Ratio...............................................................................................................................4

Quick Ratio..................................................................................................................................5

Gross Profit Margin.....................................................................................................................5

Return on Equity..........................................................................................................................6

Return on Assets..........................................................................................................................6

Reference.........................................................................................................................................9

ACCOUNTING FOR BUSINESS

Table of Contents

Introduction......................................................................................................................................3

Overview of the Company...............................................................................................................3

Ratio Analysis..................................................................................................................................3

Current Ratio...............................................................................................................................4

Quick Ratio..................................................................................................................................5

Gross Profit Margin.....................................................................................................................5

Return on Equity..........................................................................................................................6

Return on Assets..........................................................................................................................6

Reference.........................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING FOR BUSINESS

Introduction

The assignment will be focusing on the analysis of performance of Whitehaven coal ltd

and will be computing financial ratios for the purpose of analysis. The ratio which will be

computed will be of significance and will be analyzed as per the requirement of the assignment.

The companies which are selected for comparing the financial performance of the business are

Wollongong Coal Ltd and White Energy Co ltd. Both theses companies are listed in Australian

stock exchange and are is engaged in the same industry as Whitehaven Coal Ltd.

Overview of the Company

Whitehaven Coal ltd is engaged in the business of development and operation of coal

mines in Australia. The company has basically two business segments which are open cut

operations and underground operations. The business is recognized to be one of the leading

company in generation and operation in coals. The company has been able to generate net sales

of $ 1.77 billion and the company has achieved a growth of 52.28% in terms of sales growth.

Ratio Analysis

Ratio analysis is used by most of the businesses in analyzing the performance of the

business. Ratio analysis involves calculations of various ratios which are considered to be

financial indicators of the performance of the business (Delen, Kuzey and Uyar 2013). The ratio

analysis considers certain key elements of the business such as profitability, efficiency and

solvency of the business. A figure showing the computed ratios are given below:

2017 2016

Particular

s

Formu

las

Whitehav

en Coal

Ltd

Wollongo

ng Coal

Ltd

White

Energy

Co ltd

Whitehav

en Coal

Ltd

Wollongo

ng Coal

Ltd

White

Energy

Co ltd

Revenue A 1773 35820 341 1164 7705 0

Gross

Profit B 915 -21982.6 -10519 428 -36427 -13205

Net Profit C 406 -7217 -32335 20 -181934 -34077

Total

Assets D 4290 822 58751 4383 757 104889

Total

Equity E 3292 -7 17084 2889 -9 52075

ACCOUNTING FOR BUSINESS

Introduction

The assignment will be focusing on the analysis of performance of Whitehaven coal ltd

and will be computing financial ratios for the purpose of analysis. The ratio which will be

computed will be of significance and will be analyzed as per the requirement of the assignment.

The companies which are selected for comparing the financial performance of the business are

Wollongong Coal Ltd and White Energy Co ltd. Both theses companies are listed in Australian

stock exchange and are is engaged in the same industry as Whitehaven Coal Ltd.

Overview of the Company

Whitehaven Coal ltd is engaged in the business of development and operation of coal

mines in Australia. The company has basically two business segments which are open cut

operations and underground operations. The business is recognized to be one of the leading

company in generation and operation in coals. The company has been able to generate net sales

of $ 1.77 billion and the company has achieved a growth of 52.28% in terms of sales growth.

Ratio Analysis

Ratio analysis is used by most of the businesses in analyzing the performance of the

business. Ratio analysis involves calculations of various ratios which are considered to be

financial indicators of the performance of the business (Delen, Kuzey and Uyar 2013). The ratio

analysis considers certain key elements of the business such as profitability, efficiency and

solvency of the business. A figure showing the computed ratios are given below:

2017 2016

Particular

s

Formu

las

Whitehav

en Coal

Ltd

Wollongo

ng Coal

Ltd

White

Energy

Co ltd

Whitehav

en Coal

Ltd

Wollongo

ng Coal

Ltd

White

Energy

Co ltd

Revenue A 1773 35820 341 1164 7705 0

Gross

Profit B 915 -21982.6 -10519 428 -36427 -13205

Net Profit C 406 -7217 -32335 20 -181934 -34077

Total

Assets D 4290 822 58751 4383 757 104889

Total

Equity E 3292 -7 17084 2889 -9 52075

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING FOR BUSINESS

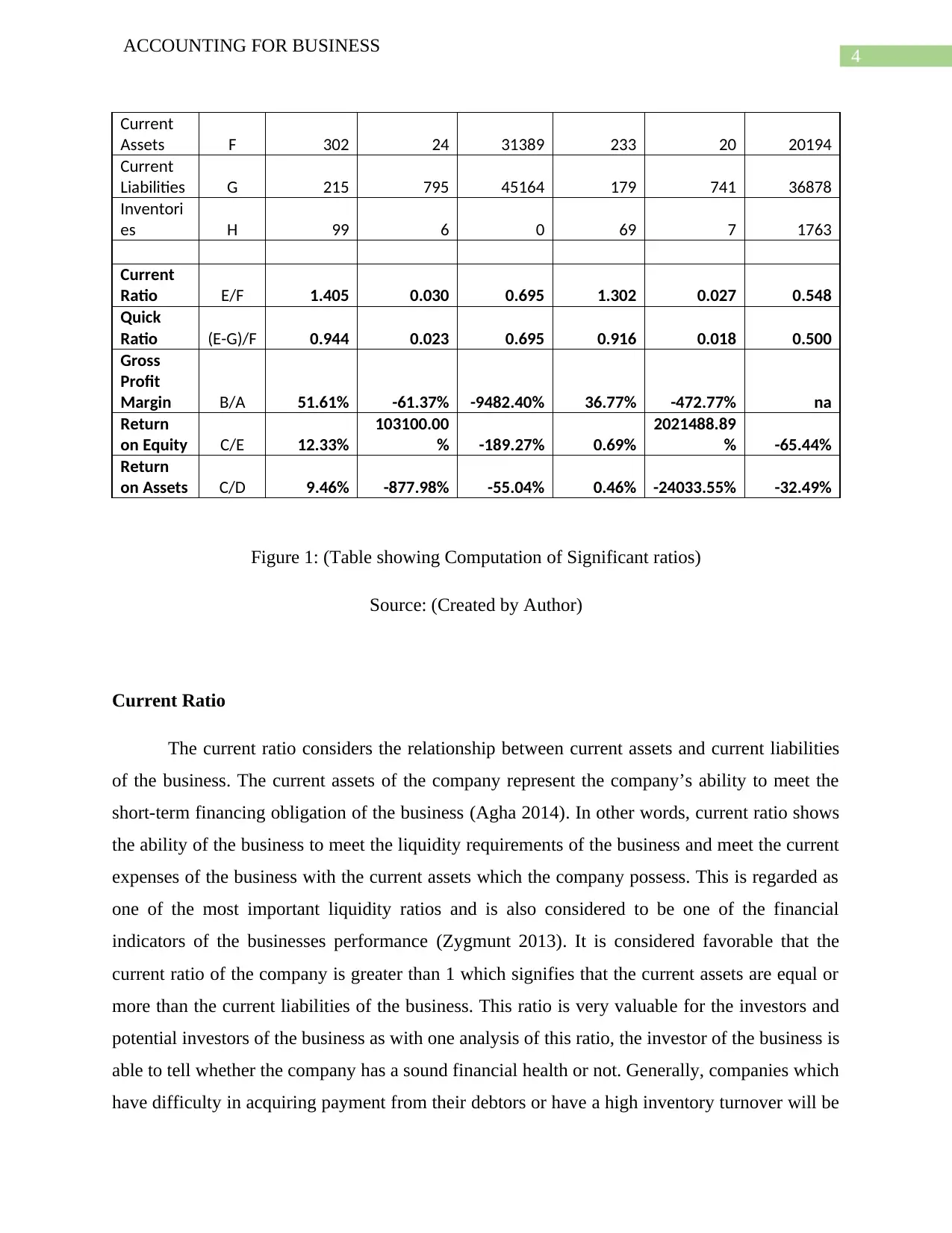

Current

Assets F 302 24 31389 233 20 20194

Current

Liabilities G 215 795 45164 179 741 36878

Inventori

es H 99 6 0 69 7 1763

Current

Ratio E/F 1.405 0.030 0.695 1.302 0.027 0.548

Quick

Ratio (E-G)/F 0.944 0.023 0.695 0.916 0.018 0.500

Gross

Profit

Margin B/A 51.61% -61.37% -9482.40% 36.77% -472.77% na

Return

on Equity C/E 12.33%

103100.00

% -189.27% 0.69%

2021488.89

% -65.44%

Return

on Assets C/D 9.46% -877.98% -55.04% 0.46% -24033.55% -32.49%

Figure 1: (Table showing Computation of Significant ratios)

Source: (Created by Author)

Current Ratio

The current ratio considers the relationship between current assets and current liabilities

of the business. The current assets of the company represent the company’s ability to meet the

short-term financing obligation of the business (Agha 2014). In other words, current ratio shows

the ability of the business to meet the liquidity requirements of the business and meet the current

expenses of the business with the current assets which the company possess. This is regarded as

one of the most important liquidity ratios and is also considered to be one of the financial

indicators of the businesses performance (Zygmunt 2013). It is considered favorable that the

current ratio of the company is greater than 1 which signifies that the current assets are equal or

more than the current liabilities of the business. This ratio is very valuable for the investors and

potential investors of the business as with one analysis of this ratio, the investor of the business is

able to tell whether the company has a sound financial health or not. Generally, companies which

have difficulty in acquiring payment from their debtors or have a high inventory turnover will be

ACCOUNTING FOR BUSINESS

Current

Assets F 302 24 31389 233 20 20194

Current

Liabilities G 215 795 45164 179 741 36878

Inventori

es H 99 6 0 69 7 1763

Current

Ratio E/F 1.405 0.030 0.695 1.302 0.027 0.548

Quick

Ratio (E-G)/F 0.944 0.023 0.695 0.916 0.018 0.500

Gross

Profit

Margin B/A 51.61% -61.37% -9482.40% 36.77% -472.77% na

Return

on Equity C/E 12.33%

103100.00

% -189.27% 0.69%

2021488.89

% -65.44%

Return

on Assets C/D 9.46% -877.98% -55.04% 0.46% -24033.55% -32.49%

Figure 1: (Table showing Computation of Significant ratios)

Source: (Created by Author)

Current Ratio

The current ratio considers the relationship between current assets and current liabilities

of the business. The current assets of the company represent the company’s ability to meet the

short-term financing obligation of the business (Agha 2014). In other words, current ratio shows

the ability of the business to meet the liquidity requirements of the business and meet the current

expenses of the business with the current assets which the company possess. This is regarded as

one of the most important liquidity ratios and is also considered to be one of the financial

indicators of the businesses performance (Zygmunt 2013). It is considered favorable that the

current ratio of the company is greater than 1 which signifies that the current assets are equal or

more than the current liabilities of the business. This ratio is very valuable for the investors and

potential investors of the business as with one analysis of this ratio, the investor of the business is

able to tell whether the company has a sound financial health or not. Generally, companies which

have difficulty in acquiring payment from their debtors or have a high inventory turnover will be

5

ACCOUNTING FOR BUSINESS

facing liquidity problem which can be depicted by current ratio (Ehiedu 2014). The formula of

current ratio which is used in the computation is shown below

Current Ratio= Current Assets

Current Liabilities

Quick Ratio

This ratio is quite similar to current ratio and it also deals with the liquidity condition of

the business. This ratio also is a measure of the ability of the company to meet the current

liabilities of the business which are short-term in nature. However, the difference lies in the

recognition of the quixk ratio of the company. The quick assets of the business include all the

current assets expect inventories of the business (Bhandari and Iyer 2013). In other words, quick

ratio takes into consideration the most liquid assets which a business possesses for the purpose of

calculations. Quick ratio is also known as acid test ratio and is an essential element of the ratio

analysis of the business. The quick ratio also informs the shareholders about the liquidity

position of the business. The formula which is used for the purpose of computing the ratio is

shown below:

Quick Ratio= Current Assets−Inventories

Current Lianilities

Gross Profit Margin

Gross Profit Margin is computed by dividing the gross profit which is generated by the

company with the total revenue which is generated by the business (Muhammad, Shah and ul

Islam 2014). In simple words it can be described as financial analysis tool which informs the

users about the financial health of the company and the ability of the company to generate profits

which are left out from revenues after deducting the cost of goods sold of the business (Garcia-

Castro and Aguilera 2014). The gross profit margin is also considered to be a financial indicator

of the performance of the business. The formula which is used for the computation of Gross

Profit margin is given below

Gross Profit Margin= Gross Profit

Total Sales

ACCOUNTING FOR BUSINESS

facing liquidity problem which can be depicted by current ratio (Ehiedu 2014). The formula of

current ratio which is used in the computation is shown below

Current Ratio= Current Assets

Current Liabilities

Quick Ratio

This ratio is quite similar to current ratio and it also deals with the liquidity condition of

the business. This ratio also is a measure of the ability of the company to meet the current

liabilities of the business which are short-term in nature. However, the difference lies in the

recognition of the quixk ratio of the company. The quick assets of the business include all the

current assets expect inventories of the business (Bhandari and Iyer 2013). In other words, quick

ratio takes into consideration the most liquid assets which a business possesses for the purpose of

calculations. Quick ratio is also known as acid test ratio and is an essential element of the ratio

analysis of the business. The quick ratio also informs the shareholders about the liquidity

position of the business. The formula which is used for the purpose of computing the ratio is

shown below:

Quick Ratio= Current Assets−Inventories

Current Lianilities

Gross Profit Margin

Gross Profit Margin is computed by dividing the gross profit which is generated by the

company with the total revenue which is generated by the business (Muhammad, Shah and ul

Islam 2014). In simple words it can be described as financial analysis tool which informs the

users about the financial health of the company and the ability of the company to generate profits

which are left out from revenues after deducting the cost of goods sold of the business (Garcia-

Castro and Aguilera 2014). The gross profit margin is also considered to be a financial indicator

of the performance of the business. The formula which is used for the computation of Gross

Profit margin is given below

Gross Profit Margin= Gross Profit

Total Sales

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING FOR BUSINESS

Return on Equity

The return on equity ratio refers to the amount of net returns which the shareholders of

the company receive from the company in respect of the shares which the investors hold. The

ratio demonstrates the profitability of the business and how much profit the business can

generates at their current (Hevert 2013). This ratio is very important as the investors decide

whether they want to invest in the shares of a company or not on the basis of the return on equity

of the company. The ratio is also considered to be financial indicator as to whether the business

is profitable or not. In addition to this, it reflects what percentage of return the investors are

getting or expected to get when profits of the business are distributed (Heikal, Khaddafi and

Ummah 2014). The formula which is used for the purpose of calculation are shown below:

Return on Equity= Net Profit

Total Shareholders Equity

Return on Assets

As per this ratio. It measures the profits which a business can generate while using the

resources which are available to the business. Such resources are assets of the business (Al

Nimer, Warrad and Al Mari 2015). This is also considered to one of the financial indicators of

the business as they reflect for which activities the assets of the business are being used and

whether the business is able to generates profits with the same. The return on assets is generally

computed when the net income of the business is divided by the total assets possessed by the

company. The formula which is used for the purpose of computing return on assets is shown

below:

Return on Assets= Net profit

Total Assets of the business

Ratio Analysis

Ratio analysis is the process of analyzing the company’s financial statements to evaluate

the aspects of the operating and the financial performance of the company with the help of the

efficiency, liquidity, profitability and solvency ratio (Ozcan 2014). In the given scenario the

analysis is to be made of the Whitehaven Coal Ltd by comparing the ratios with the two other

ACCOUNTING FOR BUSINESS

Return on Equity

The return on equity ratio refers to the amount of net returns which the shareholders of

the company receive from the company in respect of the shares which the investors hold. The

ratio demonstrates the profitability of the business and how much profit the business can

generates at their current (Hevert 2013). This ratio is very important as the investors decide

whether they want to invest in the shares of a company or not on the basis of the return on equity

of the company. The ratio is also considered to be financial indicator as to whether the business

is profitable or not. In addition to this, it reflects what percentage of return the investors are

getting or expected to get when profits of the business are distributed (Heikal, Khaddafi and

Ummah 2014). The formula which is used for the purpose of calculation are shown below:

Return on Equity= Net Profit

Total Shareholders Equity

Return on Assets

As per this ratio. It measures the profits which a business can generate while using the

resources which are available to the business. Such resources are assets of the business (Al

Nimer, Warrad and Al Mari 2015). This is also considered to one of the financial indicators of

the business as they reflect for which activities the assets of the business are being used and

whether the business is able to generates profits with the same. The return on assets is generally

computed when the net income of the business is divided by the total assets possessed by the

company. The formula which is used for the purpose of computing return on assets is shown

below:

Return on Assets= Net profit

Total Assets of the business

Ratio Analysis

Ratio analysis is the process of analyzing the company’s financial statements to evaluate

the aspects of the operating and the financial performance of the company with the help of the

efficiency, liquidity, profitability and solvency ratio (Ozcan 2014). In the given scenario the

analysis is to be made of the Whitehaven Coal Ltd by comparing the ratios with the two other

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING FOR BUSINESS

companies namely Wollongong coal ltd and white energy coal limited of the two years 2017 and

2016. The comparison has been made both year wise and company wise.

The current ratio of the Whitehaven coal ltd has been increased from the year 2016 which

was 1.302 to 1.405in the year 2017. This shows that there has been increase in the current ratio

indicating the enhancement of the company’s ability to pay off its obligations.

The current ratio of other company did not increase much as compared to Whitehaven

Coal Ltd, the Wollongong coal ltd increased from 0.027 in 2016 to 0.30 in 2017, which is much

less if compared to Whitehaven Coal. White energy coal limited also rose from 0.548 to 1.302 at

a much lesser rate. If the current ratio of Whitehaven coal ltd is compared with the other two, the

ratio is much greater in the present financial year.

Similarly, the quick ratio that deals with the ability of the company to meets its short-

term liabilities is much more in Whitehaven Coal Ltd that is 0.944 as compared to the other two

which are 0.023 for Wollongong coal ltd and 0.695 for white energy coal ltd. Moreover, as

compared to 2016 the ratio increased from 0.916 to 0.944in 2017. However, White energy coal

limited has increased more from 0.5 to 0.695 than Wollongong coal ltd and Whitehaven Coal

Ltd.

The net profit margin also is more in case of Whitehaven Coal Ltd that is 22.90%

whereas the other two companies has much less percentage or rather running in negative.

Wollongong coal ltd has -20.15% in 2017 and white energy coal ltd had -9482.40%. This

represents that the profitability of the company is higher. More over there has been a drastic

increase in the ratio in case of Whitehaven Coal Ltd from 1.72% in 2016 to 22.90% in 2017.

The return on Equity is quite more in case of Whitehaven Coal Ltd is 12.33% in 2017 as

compared to Wollongong coal ltd which is 103100.00% and for White energy Coal Ltd which is

-189.27%. The return on equity is the amount of net income returned as a percentage of

shareholders equity. Return on equity measures a corporation's profitability by revealing how

much profit a company generates with the money shareholders have invested. Therefore, as

compared to 2016 the return on equity has been improved from 0.69% in 2016.

ACCOUNTING FOR BUSINESS

companies namely Wollongong coal ltd and white energy coal limited of the two years 2017 and

2016. The comparison has been made both year wise and company wise.

The current ratio of the Whitehaven coal ltd has been increased from the year 2016 which

was 1.302 to 1.405in the year 2017. This shows that there has been increase in the current ratio

indicating the enhancement of the company’s ability to pay off its obligations.

The current ratio of other company did not increase much as compared to Whitehaven

Coal Ltd, the Wollongong coal ltd increased from 0.027 in 2016 to 0.30 in 2017, which is much

less if compared to Whitehaven Coal. White energy coal limited also rose from 0.548 to 1.302 at

a much lesser rate. If the current ratio of Whitehaven coal ltd is compared with the other two, the

ratio is much greater in the present financial year.

Similarly, the quick ratio that deals with the ability of the company to meets its short-

term liabilities is much more in Whitehaven Coal Ltd that is 0.944 as compared to the other two

which are 0.023 for Wollongong coal ltd and 0.695 for white energy coal ltd. Moreover, as

compared to 2016 the ratio increased from 0.916 to 0.944in 2017. However, White energy coal

limited has increased more from 0.5 to 0.695 than Wollongong coal ltd and Whitehaven Coal

Ltd.

The net profit margin also is more in case of Whitehaven Coal Ltd that is 22.90%

whereas the other two companies has much less percentage or rather running in negative.

Wollongong coal ltd has -20.15% in 2017 and white energy coal ltd had -9482.40%. This

represents that the profitability of the company is higher. More over there has been a drastic

increase in the ratio in case of Whitehaven Coal Ltd from 1.72% in 2016 to 22.90% in 2017.

The return on Equity is quite more in case of Whitehaven Coal Ltd is 12.33% in 2017 as

compared to Wollongong coal ltd which is 103100.00% and for White energy Coal Ltd which is

-189.27%. The return on equity is the amount of net income returned as a percentage of

shareholders equity. Return on equity measures a corporation's profitability by revealing how

much profit a company generates with the money shareholders have invested. Therefore, as

compared to 2016 the return on equity has been improved from 0.69% in 2016.

8

ACCOUNTING FOR BUSINESS

Return on assets that represents the profit percentage a company earns in relation to its

overall resources is 9.46% for Whitehaven Coal Ltd which is much higher as compared to the

other two company which is -877.98% for Wollongong coal ltd -55.04% for White energy Coal

Ltd. Therefore, Whitehaven earns more profit. Moreover, there has been a rise in the return on

assets from 2016 which was 0.46%. The rate of increase is also more than White Energy Coal

Ltd and Wollongong coal ltd.

ACCOUNTING FOR BUSINESS

Return on assets that represents the profit percentage a company earns in relation to its

overall resources is 9.46% for Whitehaven Coal Ltd which is much higher as compared to the

other two company which is -877.98% for Wollongong coal ltd -55.04% for White energy Coal

Ltd. Therefore, Whitehaven earns more profit. Moreover, there has been a rise in the return on

assets from 2016 which was 0.46%. The rate of increase is also more than White Energy Coal

Ltd and Wollongong coal ltd.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING FOR BUSINESS

Reference

Agha, H., 2014. Impact of working capital management on profitability. European Scientific

Journal, ESJ, 10(1).

Al Nimer, M., Warrad, L. and Al Mari, R., 2015. The Impact of liquidity on Jordanian banks

profitability through return on assets. European Journal of Business and Management, 7(7),

pp.229-232.

Bhandari, S.B. and Iyer, R., 2013. Predicting business failure using cash flow statement based

measures. Managerial Finance, 39(7), pp.667-676.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Ehiedu, V.C., 2014. The impact of liquidity on profitability of some selected companies: The

financial statement analysis (FSA) approach. Research Journal of Finance and Accounting, 5(5),

pp.81-90.

Garcia-Castro, R. and Aguilera, R.V., 2014. Family involvement in business and financial

performance: A set-theoretic cross-national inquiry. Journal of Family Business Strategy, 5(1),

pp.85-96.

Heikal, M., Khaddafi, M. and Ummah, A., 2014. Influence analysis of return on assets (ROA),

return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and current ratio

(CR), against corporate profit growth in automotive in Indonesia Stock Exchange. International

Journal of Academic Research in Business and Social Sciences, 4(12), p.101.

Hevert, S.R.B., 2013. Return on Equity.

Muhammad, H., Shah, B. and ul Islam, Z., 2014. The impact of capital structure on firm

performance: Evidence from Pakistan. Journal of Industrial Distribution & Business, 5(2),

pp.13-20.

ACCOUNTING FOR BUSINESS

Reference

Agha, H., 2014. Impact of working capital management on profitability. European Scientific

Journal, ESJ, 10(1).

Al Nimer, M., Warrad, L. and Al Mari, R., 2015. The Impact of liquidity on Jordanian banks

profitability through return on assets. European Journal of Business and Management, 7(7),

pp.229-232.

Bhandari, S.B. and Iyer, R., 2013. Predicting business failure using cash flow statement based

measures. Managerial Finance, 39(7), pp.667-676.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Ehiedu, V.C., 2014. The impact of liquidity on profitability of some selected companies: The

financial statement analysis (FSA) approach. Research Journal of Finance and Accounting, 5(5),

pp.81-90.

Garcia-Castro, R. and Aguilera, R.V., 2014. Family involvement in business and financial

performance: A set-theoretic cross-national inquiry. Journal of Family Business Strategy, 5(1),

pp.85-96.

Heikal, M., Khaddafi, M. and Ummah, A., 2014. Influence analysis of return on assets (ROA),

return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and current ratio

(CR), against corporate profit growth in automotive in Indonesia Stock Exchange. International

Journal of Academic Research in Business and Social Sciences, 4(12), p.101.

Hevert, S.R.B., 2013. Return on Equity.

Muhammad, H., Shah, B. and ul Islam, Z., 2014. The impact of capital structure on firm

performance: Evidence from Pakistan. Journal of Industrial Distribution & Business, 5(2),

pp.13-20.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING FOR BUSINESS

Ozcan, Y.A., 2014. Evaluation of Performance in Health Care. In Health Care Benchmarking

and Performance Evaluation(pp. 3-14). Springer, Boston, MA.

Zygmunt, J., 2013, March. Does liquidity impact on profitability. In Conference of informatics

and management sciences, March (pp. 38-49).

ACCOUNTING FOR BUSINESS

Ozcan, Y.A., 2014. Evaluation of Performance in Health Care. In Health Care Benchmarking

and Performance Evaluation(pp. 3-14). Springer, Boston, MA.

Zygmunt, J., 2013, March. Does liquidity impact on profitability. In Conference of informatics

and management sciences, March (pp. 38-49).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.