ACCT6004 Group Case Study: Wilkerson Company Profitability Analysis

VerifiedAdded on 2022/10/14

|20

|3753

|480

Case Study

AI Summary

This case study report analyzes the Wilkerson Company's financial performance, addressing issues in management accounting, cost behaviors, and estimation techniques. It explores ethical and organizational challenges, categorizes costs, and examines the relevance of quantitative and qualitative costing methods in decision-making. The report focuses on the company's competitive situations, particularly regarding overhead assignment and the implementation of an Activity-Based Costing (ABC) model. It provides detailed calculations and comparisons of product costs and profitability under both traditional and ABC costing systems. The analysis includes recommendations for improving the company's profitability and reducing production costs, along with a discussion of concerns about the ABC system and changes in incentive structures. The study aims to provide insights into strategic decision-making and cost management within the context of the Wilkerson Company's operations.

RUNNING HEAD: MANAGEMENT ACCOUNTING 1

UNIVERSITY NAME

STUDENT NAME

STUDENT ID

COURSE

DATE

UNIVERSITY NAME

STUDENT NAME

STUDENT ID

COURSE

DATE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 2

Executive summary

The purpose of this report is to shed light on the issues impacting management accounting,

identify the various types of costs, cost behaviours cost estimation techniques, their usefulness in

decision making. The report further acknowledges the importance of ABC costing system as a

modern method of accounting for costs by the management accounting, which is increasingly

becoming part of the modern accounting system.

Executive summary

The purpose of this report is to shed light on the issues impacting management accounting,

identify the various types of costs, cost behaviours cost estimation techniques, their usefulness in

decision making. The report further acknowledges the importance of ABC costing system as a

modern method of accounting for costs by the management accounting, which is increasingly

becoming part of the modern accounting system.

MANAGEMENT ACCOUNTING 3

Table of Contents

INTRODUCTION...........................................................................................................................................4

ETHICAL ISSUES AFFECTING MANAGEMENT ACCOUNTING.......................................................5

ORGANISATIONAL ISSUES...................................................................................................................5

COST BEHAVIOURS................................................................................................................................6

VARIABLE COSTS................................................................................................................................6

FIXED COSTS........................................................................................................................................7

COST ESTIMATION TECHNIQUES........................................................................................................7

RELEVANCE OF QUANTITATIVE AND QUALITATIVE COSTING METHODS IN DECISION

MAKING....................................................................................................................................................7

COMPETITIVE SITUATIONS FACING WILKERSON'S COMPANY EXECUTIVES..........................8

DECISION ON WHETHER TO ABANDON OVERHEAD ASSIGNMENT............................................8

COST FLOW DIAGRAM...........................................................................................................................9

HOW COSTS FLOW FROM FACTORY EXPENSE ACCOUNTS TO PRODUCTS..............................9

ACTIVITY BASED COSTING MODEL.................................................................................................10

A-B-C AS PER PRODUCT LINE............................................................................................................10

ABC HIERARCHY CATEGORIES.........................................................................................................11

ACTIVITY RATES CALCULATION......................................................................................................12

COSTS ESTIMATION.............................................................................................................................13

COMPARISON OF PRODUCT COSTS AND PROFITABILTY............................................................13

ACTIONS TO IMPROVE COMPANYS PROFITABILTY.....................................................................14

ACTIONS TAKEN TO REDUCE PRODUCTION COSTS.....................................................................15

CONCERNS ABOUT ABC SYSTEM.....................................................................................................15

CHANGE IN THE INCENTIVE STRUCTURE.......................................................................................16

CONCLUSION.........................................................................................................................................16

Table of Contents

INTRODUCTION...........................................................................................................................................4

ETHICAL ISSUES AFFECTING MANAGEMENT ACCOUNTING.......................................................5

ORGANISATIONAL ISSUES...................................................................................................................5

COST BEHAVIOURS................................................................................................................................6

VARIABLE COSTS................................................................................................................................6

FIXED COSTS........................................................................................................................................7

COST ESTIMATION TECHNIQUES........................................................................................................7

RELEVANCE OF QUANTITATIVE AND QUALITATIVE COSTING METHODS IN DECISION

MAKING....................................................................................................................................................7

COMPETITIVE SITUATIONS FACING WILKERSON'S COMPANY EXECUTIVES..........................8

DECISION ON WHETHER TO ABANDON OVERHEAD ASSIGNMENT............................................8

COST FLOW DIAGRAM...........................................................................................................................9

HOW COSTS FLOW FROM FACTORY EXPENSE ACCOUNTS TO PRODUCTS..............................9

ACTIVITY BASED COSTING MODEL.................................................................................................10

A-B-C AS PER PRODUCT LINE............................................................................................................10

ABC HIERARCHY CATEGORIES.........................................................................................................11

ACTIVITY RATES CALCULATION......................................................................................................12

COSTS ESTIMATION.............................................................................................................................13

COMPARISON OF PRODUCT COSTS AND PROFITABILTY............................................................13

ACTIONS TO IMPROVE COMPANYS PROFITABILTY.....................................................................14

ACTIONS TAKEN TO REDUCE PRODUCTION COSTS.....................................................................15

CONCERNS ABOUT ABC SYSTEM.....................................................................................................15

CHANGE IN THE INCENTIVE STRUCTURE.......................................................................................16

CONCLUSION.........................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 4

REFERENCES..............................................................................................................................................18

REFERENCES..............................................................................................................................................18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 5

INTRODUCTION

Management accounting is still a new concept of accounting in the world. Due to this, the sector

is faced with certain challenges in the process of implementation which encompasses both

ethical and organisational challenges. Organisationally, the senior management may not be fully

aware of the importance of the management accounting, thus not fully embraced it. They are

several types of costs which include manufacturing and non-manufacturing costs.

Manufacturing costs are costs are directly traceable to the products they include cost of direct

labour, cost of direct expenses and cost of direct materials use. while non-manufacturing is not

traceable on the products. They include cost of indirect labour, cost of indirect expenses. Cost

behaviours can be fixed, variable or semi-variable. Variable costs vary with the level of

productuonwhile fixed costs do not vary with the level of productions semi variable costs have

both a variable and a fixed element which are categorised during cost computations. The cost

estimation techniques include both engineering and account analysis methods. Account analysis

production.

involves the classification of costs as variable, fixed costs or semi variable costs and developing

a cost function in the form of y=a+bx, where a, is the fixed cost of production while b, is the

variable cost of production

Management accounting information is useful in decision making by senior and final decision

makers in an organization.

ETHICAL ISSUES AFFECTING MANAGEMENT ACCOUNTING.

Ethical issues that include corporate social responsibility which is a legal and professional

requirement of the business impact the management accountants as they are always involved in

offering information that facilitates and supports the efficiency and effectiveness of this social

responsibility. The management accountants are tasked with advising the management of the

efficiency of the corporate social responsibility with a harmonised cost with management goals

and objectives (Zimmerman & Yahya, 2011).

INTRODUCTION

Management accounting is still a new concept of accounting in the world. Due to this, the sector

is faced with certain challenges in the process of implementation which encompasses both

ethical and organisational challenges. Organisationally, the senior management may not be fully

aware of the importance of the management accounting, thus not fully embraced it. They are

several types of costs which include manufacturing and non-manufacturing costs.

Manufacturing costs are costs are directly traceable to the products they include cost of direct

labour, cost of direct expenses and cost of direct materials use. while non-manufacturing is not

traceable on the products. They include cost of indirect labour, cost of indirect expenses. Cost

behaviours can be fixed, variable or semi-variable. Variable costs vary with the level of

productuonwhile fixed costs do not vary with the level of productions semi variable costs have

both a variable and a fixed element which are categorised during cost computations. The cost

estimation techniques include both engineering and account analysis methods. Account analysis

production.

involves the classification of costs as variable, fixed costs or semi variable costs and developing

a cost function in the form of y=a+bx, where a, is the fixed cost of production while b, is the

variable cost of production

Management accounting information is useful in decision making by senior and final decision

makers in an organization.

ETHICAL ISSUES AFFECTING MANAGEMENT ACCOUNTING.

Ethical issues that include corporate social responsibility which is a legal and professional

requirement of the business impact the management accountants as they are always involved in

offering information that facilitates and supports the efficiency and effectiveness of this social

responsibility. The management accountants are tasked with advising the management of the

efficiency of the corporate social responsibility with a harmonised cost with management goals

and objectives (Zimmerman & Yahya, 2011).

MANAGEMENT ACCOUNTING 6

ORGANISATIONAL ISSUES.

These issues include organisation strategy and products. They affect the management

accountant’s product quality. For example, introduction of a new management style causes the

sudden changes in the management sector i.e. the sequence of work and the attitudes of the

workers in the management sector to these new style of administration. Changes in the financial

position of a company also affects the scope of work to be handled by the management

accountants. For instance, expansion in the financial position overloads the work of the cost

accountants in the company (Schaltegger & Burritt, 2017).

TYPES OF COSTS.

Manufacturing costs; are costs directly involved in manufacturing products i.e. direct labour

costs. None manufacturing costs; costs that are not directly involved in the manufacturing

process i.e. selling and administration costs (Callahan, Stetz & Brooks, 2011).

COST OBJECTS.

Output; this involves company’s products and services.

Operational; cost objects can be within department, machining operation and production line.

Business relationship this arises when there is need to accumulate costs for a supplier.

COST BEHAVIOURS.

Variable costs; costs that varies with the level of production i.e. manufacturing costs.

Fixed costs; costs that do not vary with the level of production i.e. rental costs.

semi variable costs costs with a fixed and a variable element (DRURY, 2013).

ORGANISATIONAL ISSUES.

These issues include organisation strategy and products. They affect the management

accountant’s product quality. For example, introduction of a new management style causes the

sudden changes in the management sector i.e. the sequence of work and the attitudes of the

workers in the management sector to these new style of administration. Changes in the financial

position of a company also affects the scope of work to be handled by the management

accountants. For instance, expansion in the financial position overloads the work of the cost

accountants in the company (Schaltegger & Burritt, 2017).

TYPES OF COSTS.

Manufacturing costs; are costs directly involved in manufacturing products i.e. direct labour

costs. None manufacturing costs; costs that are not directly involved in the manufacturing

process i.e. selling and administration costs (Callahan, Stetz & Brooks, 2011).

COST OBJECTS.

Output; this involves company’s products and services.

Operational; cost objects can be within department, machining operation and production line.

Business relationship this arises when there is need to accumulate costs for a supplier.

COST BEHAVIOURS.

Variable costs; costs that varies with the level of production i.e. manufacturing costs.

Fixed costs; costs that do not vary with the level of production i.e. rental costs.

semi variable costs costs with a fixed and a variable element (DRURY, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 7

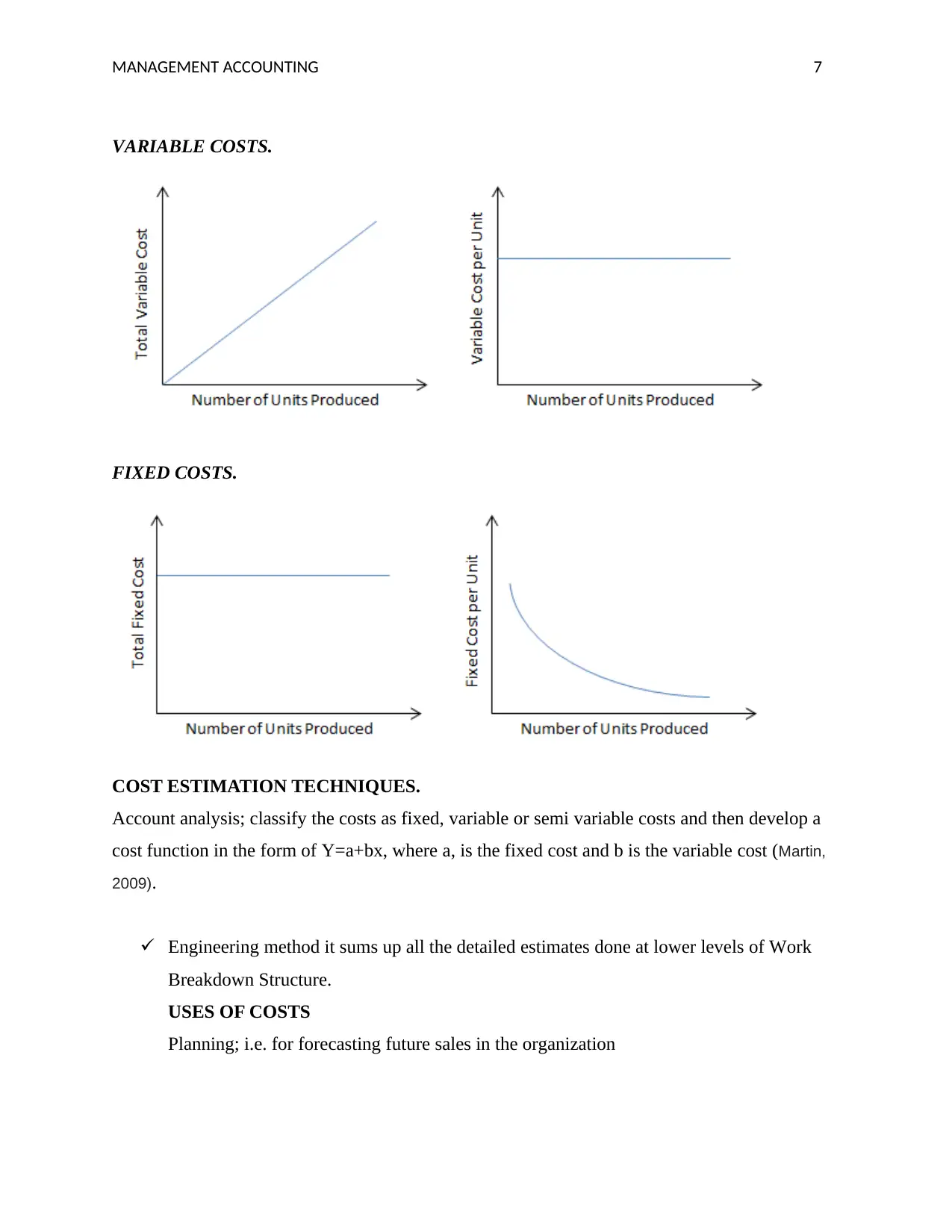

VARIABLE COSTS.

FIXED COSTS.

COST ESTIMATION TECHNIQUES.

Account analysis; classify the costs as fixed, variable or semi variable costs and then develop a

cost function in the form of Y=a+bx, where a, is the fixed cost and b is the variable cost (Martin,

2009).

Engineering method it sums up all the detailed estimates done at lower levels of Work

Breakdown Structure.

USES OF COSTS

Planning; i.e. for forecasting future sales in the organization

VARIABLE COSTS.

FIXED COSTS.

COST ESTIMATION TECHNIQUES.

Account analysis; classify the costs as fixed, variable or semi variable costs and then develop a

cost function in the form of Y=a+bx, where a, is the fixed cost and b is the variable cost (Martin,

2009).

Engineering method it sums up all the detailed estimates done at lower levels of Work

Breakdown Structure.

USES OF COSTS

Planning; i.e. for forecasting future sales in the organization

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 8

Controlling; this is keeping costs within prescribed rates i.e. controlling stock costs and

expenses.

Decision making; this includes using information for evaluating market and product

profitability, evaluating financial effect of strategies and plans.

RELEVANCE OF QUANTITATIVE AND QUALITATIVE COSTING METHODS IN

DECISION MAKING.

Quantitative encompasses the methods which aimed at objective measurement. It is

applicable in solving business problems, choosing a relevant strategy to advance the

market share, enforcing discipline thinking among employees of a company, decision on

how to lower the waiting time in an organisation especially service industry, proper

allocation of resources to save time and reaching decision on which inventory

management system should be adopted by the organisation (Lipshitz, 2010).

Qualitative factors are useful in decision making pertaining which product's components

can be produced at a harmonised cost by the firm. It is also used on deciding on which

type of investor and what number could possibly invest in the company. It is applicable

also when measuring the performance of the employees of the company and making

decision on promotion of the company's staff (Avazzadehfath & Raiashekar, 2011).

QUESTION 1.

COMPETITIVE SITUATIONS FACING WILKERSON'S COMPANY EXECUTIVES

The production overhead method of allocating cost is archaic, if it includes deprecation then it

will obvious contort figures as it is not a good method since depression is a" sunk cost" that

cannot be used for decision making purposes. Thus the bottom line would obviously be warped

and is not comparable with others who may not take such an expense (Oliveira & Werther 2013).

QUESTION 2.

DECISION ON WHETHER TO ABANDON OVERHEAD ASSIGNMENT.

The company should abandon the overhead assignment because the variable + fixed

manufacturing overhead expense could be taken to the income statement for financial accounting

Controlling; this is keeping costs within prescribed rates i.e. controlling stock costs and

expenses.

Decision making; this includes using information for evaluating market and product

profitability, evaluating financial effect of strategies and plans.

RELEVANCE OF QUANTITATIVE AND QUALITATIVE COSTING METHODS IN

DECISION MAKING.

Quantitative encompasses the methods which aimed at objective measurement. It is

applicable in solving business problems, choosing a relevant strategy to advance the

market share, enforcing discipline thinking among employees of a company, decision on

how to lower the waiting time in an organisation especially service industry, proper

allocation of resources to save time and reaching decision on which inventory

management system should be adopted by the organisation (Lipshitz, 2010).

Qualitative factors are useful in decision making pertaining which product's components

can be produced at a harmonised cost by the firm. It is also used on deciding on which

type of investor and what number could possibly invest in the company. It is applicable

also when measuring the performance of the employees of the company and making

decision on promotion of the company's staff (Avazzadehfath & Raiashekar, 2011).

QUESTION 1.

COMPETITIVE SITUATIONS FACING WILKERSON'S COMPANY EXECUTIVES

The production overhead method of allocating cost is archaic, if it includes deprecation then it

will obvious contort figures as it is not a good method since depression is a" sunk cost" that

cannot be used for decision making purposes. Thus the bottom line would obviously be warped

and is not comparable with others who may not take such an expense (Oliveira & Werther 2013).

QUESTION 2.

DECISION ON WHETHER TO ABANDON OVERHEAD ASSIGNMENT.

The company should abandon the overhead assignment because the variable + fixed

manufacturing overhead expense could be taken to the income statement for financial accounting

MANAGEMENT ACCOUNTING 9

purposes and not for decision making. For decision making only variable expenses need to be

taken because such expenses are cash and would have to be paid for relevant costing.

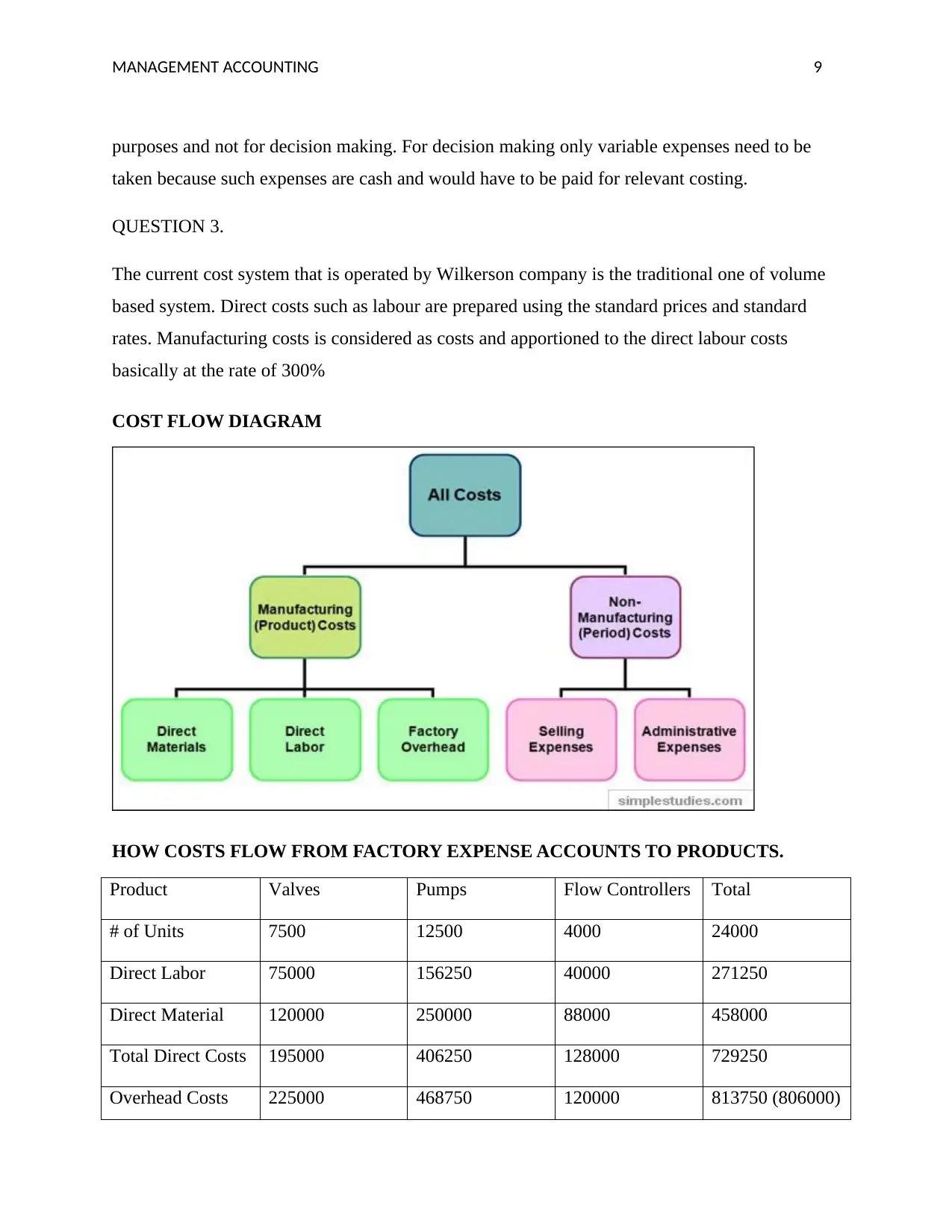

QUESTION 3.

The current cost system that is operated by Wilkerson company is the traditional one of volume

based system. Direct costs such as labour are prepared using the standard prices and standard

rates. Manufacturing costs is considered as costs and apportioned to the direct labour costs

basically at the rate of 300%

COST FLOW DIAGRAM

HOW COSTS FLOW FROM FACTORY EXPENSE ACCOUNTS TO PRODUCTS.

Product Valves Pumps Flow Controllers Total

# of Units 7500 12500 4000 24000

Direct Labor 75000 156250 40000 271250

Direct Material 120000 250000 88000 458000

Total Direct Costs 195000 406250 128000 729250

Overhead Costs 225000 468750 120000 813750 (806000)

purposes and not for decision making. For decision making only variable expenses need to be

taken because such expenses are cash and would have to be paid for relevant costing.

QUESTION 3.

The current cost system that is operated by Wilkerson company is the traditional one of volume

based system. Direct costs such as labour are prepared using the standard prices and standard

rates. Manufacturing costs is considered as costs and apportioned to the direct labour costs

basically at the rate of 300%

COST FLOW DIAGRAM

HOW COSTS FLOW FROM FACTORY EXPENSE ACCOUNTS TO PRODUCTS.

Product Valves Pumps Flow Controllers Total

# of Units 7500 12500 4000 24000

Direct Labor 75000 156250 40000 271250

Direct Material 120000 250000 88000 458000

Total Direct Costs 195000 406250 128000 729250

Overhead Costs 225000 468750 120000 813750 (806000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 10

(300% of DL)

Total Cost

Allocation

420000 875000 248000 1543000

QUESTION 4.

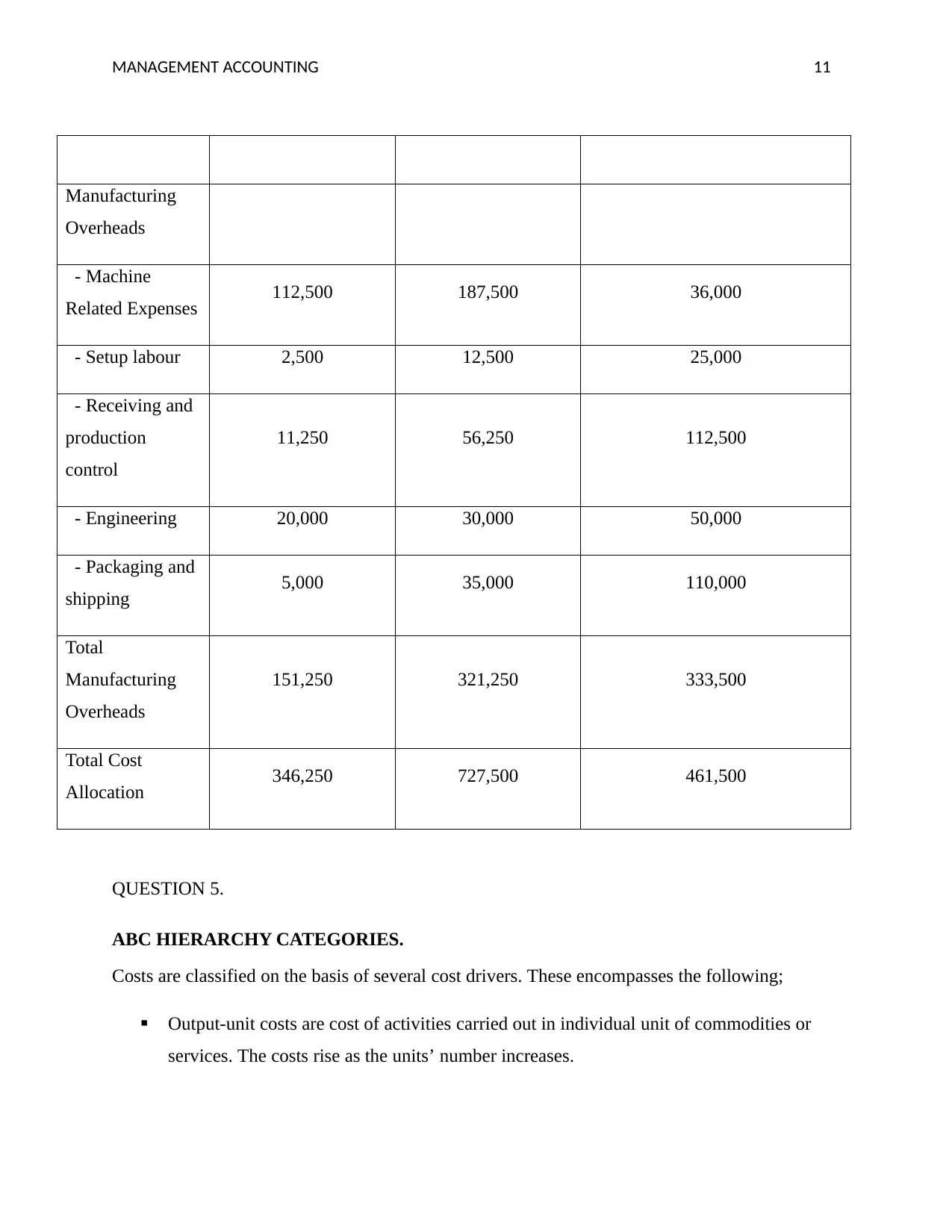

ACTIVITY BASED COSTING MODEL.

Unlike the traditional volume based cost system, ABC system potrays a true relationship

between the quantity produced and the overhead costs (Askarany, Yazdifar & Askary, 2010).

A-B-C AS PER PRODUCT LINE.

Product Valves Pumps Flow Controllers

Units 7500 12500 4000

Direct Labour 75,000 156,250 40,000

Direct Material 120,000 250,000 88,000

Total Direct Costs 195,000 406,250 128,000

(300% of DL)

Total Cost

Allocation

420000 875000 248000 1543000

QUESTION 4.

ACTIVITY BASED COSTING MODEL.

Unlike the traditional volume based cost system, ABC system potrays a true relationship

between the quantity produced and the overhead costs (Askarany, Yazdifar & Askary, 2010).

A-B-C AS PER PRODUCT LINE.

Product Valves Pumps Flow Controllers

Units 7500 12500 4000

Direct Labour 75,000 156,250 40,000

Direct Material 120,000 250,000 88,000

Total Direct Costs 195,000 406,250 128,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 11

Manufacturing

Overheads

- Machine

Related Expenses 112,500 187,500 36,000

- Setup labour 2,500 12,500 25,000

- Receiving and

production

control

11,250 56,250 112,500

- Engineering 20,000 30,000 50,000

- Packaging and

shipping 5,000 35,000 110,000

Total

Manufacturing

Overheads

151,250 321,250 333,500

Total Cost

Allocation 346,250 727,500 461,500

QUESTION 5.

ABC HIERARCHY CATEGORIES.

Costs are classified on the basis of several cost drivers. These encompasses the following;

Output-unit costs are cost of activities carried out in individual unit of commodities or

services. The costs rise as the units’ number increases.

Manufacturing

Overheads

- Machine

Related Expenses 112,500 187,500 36,000

- Setup labour 2,500 12,500 25,000

- Receiving and

production

control

11,250 56,250 112,500

- Engineering 20,000 30,000 50,000

- Packaging and

shipping 5,000 35,000 110,000

Total

Manufacturing

Overheads

151,250 321,250 333,500

Total Cost

Allocation 346,250 727,500 461,500

QUESTION 5.

ABC HIERARCHY CATEGORIES.

Costs are classified on the basis of several cost drivers. These encompasses the following;

Output-unit costs are cost of activities carried out in individual unit of commodities or

services. The costs rise as the units’ number increases.

MANAGEMENT ACCOUNTING 12

Batch levels costs of activities pertaining to a group of units of commodities or services

which is not and individual unit for instance, set up costs which involves batch levels.

Product sustaining costs are costs incurred to advance individual commodities or services

irrespective of the quantity of units produced, for instance design costs.

Facility sustaining costs. Are costs of activities not traceable to individual commodities

or services as whole for instance general administration costs and rent. These costs do not

have a cause -and impact relationship between the costs and allocation base (Johanson,

Faulkner & Ray, 2010).

QUESTION 6.

ACTIVITY RATES CALCULATION

Overhead expenses are not proportional to production volume therefore the system currently in

use by Wilkerson is not appropriate which involves use of different assumptions when

calculating the viability of the concern resulting in wrong valuation of products and inaccurate

decision making. Activity base system is the bests since it shows a clear relationship between the

volumes produced and the production cost for instance, it is crucial to show the costs pool and

define their associated costs drivers as indicated in the table below (Casini, Marone & Scozzafava,

2014).

Cost Pools -> Cost Drivers -> Activity-Based Cost Rate

Cost Pool

Amount

($) Cost Driver Amount Activity-Based Cost

Rate

Machine Related Expenses 336,000 Machine hours 11,200 machine

hours $30 per machine hour

Setup labour 40,000 Production runs 160 production runs $250 per production

run

Batch levels costs of activities pertaining to a group of units of commodities or services

which is not and individual unit for instance, set up costs which involves batch levels.

Product sustaining costs are costs incurred to advance individual commodities or services

irrespective of the quantity of units produced, for instance design costs.

Facility sustaining costs. Are costs of activities not traceable to individual commodities

or services as whole for instance general administration costs and rent. These costs do not

have a cause -and impact relationship between the costs and allocation base (Johanson,

Faulkner & Ray, 2010).

QUESTION 6.

ACTIVITY RATES CALCULATION

Overhead expenses are not proportional to production volume therefore the system currently in

use by Wilkerson is not appropriate which involves use of different assumptions when

calculating the viability of the concern resulting in wrong valuation of products and inaccurate

decision making. Activity base system is the bests since it shows a clear relationship between the

volumes produced and the production cost for instance, it is crucial to show the costs pool and

define their associated costs drivers as indicated in the table below (Casini, Marone & Scozzafava,

2014).

Cost Pools -> Cost Drivers -> Activity-Based Cost Rate

Cost Pool

Amount

($) Cost Driver Amount Activity-Based Cost

Rate

Machine Related Expenses 336,000 Machine hours 11,200 machine

hours $30 per machine hour

Setup labour 40,000 Production runs 160 production runs $250 per production

run

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.