Detailed Investment Appraisal Report: Wonder Pump Project Analysis

VerifiedAdded on 2019/12/04

|34

|2502

|174

Report

AI Summary

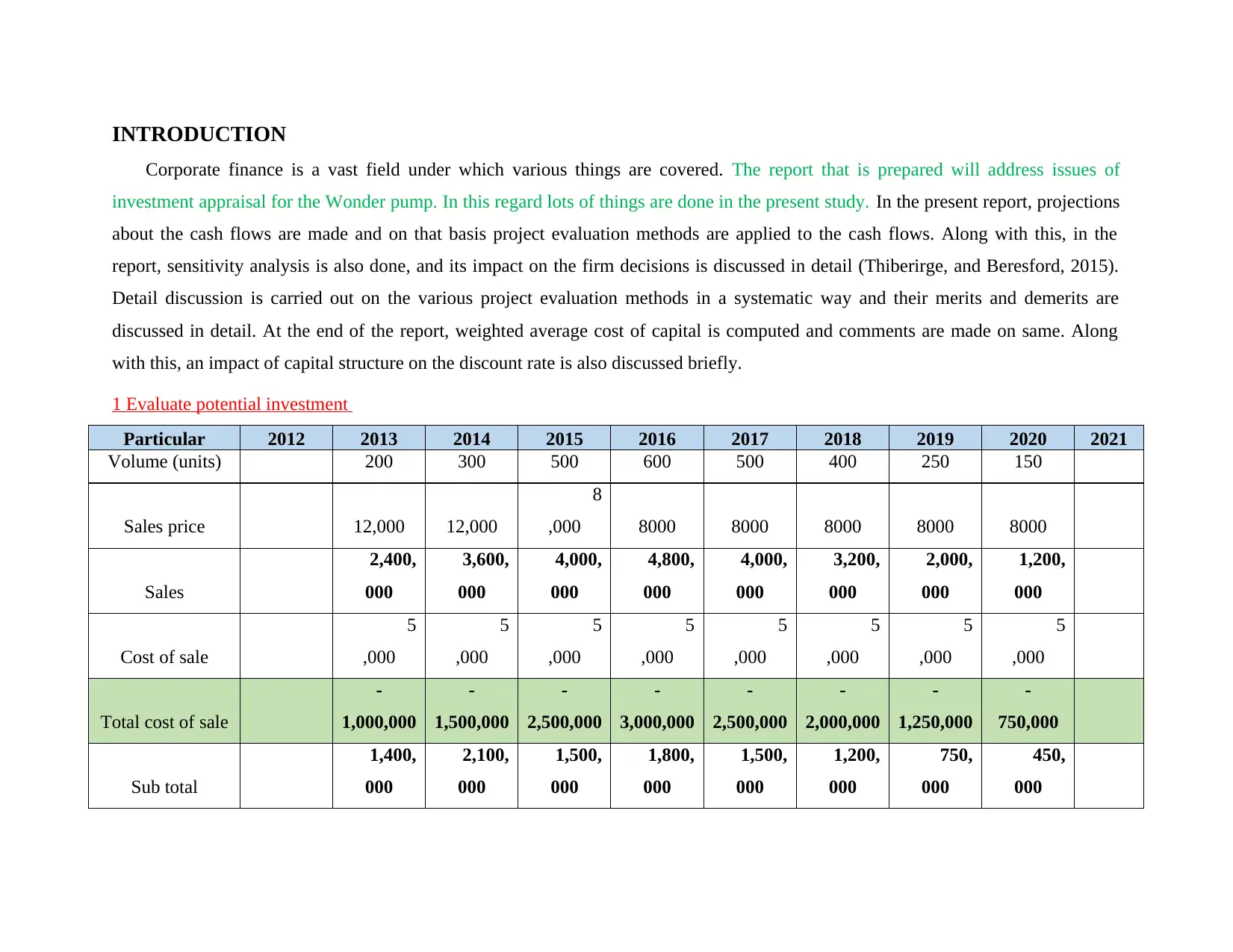

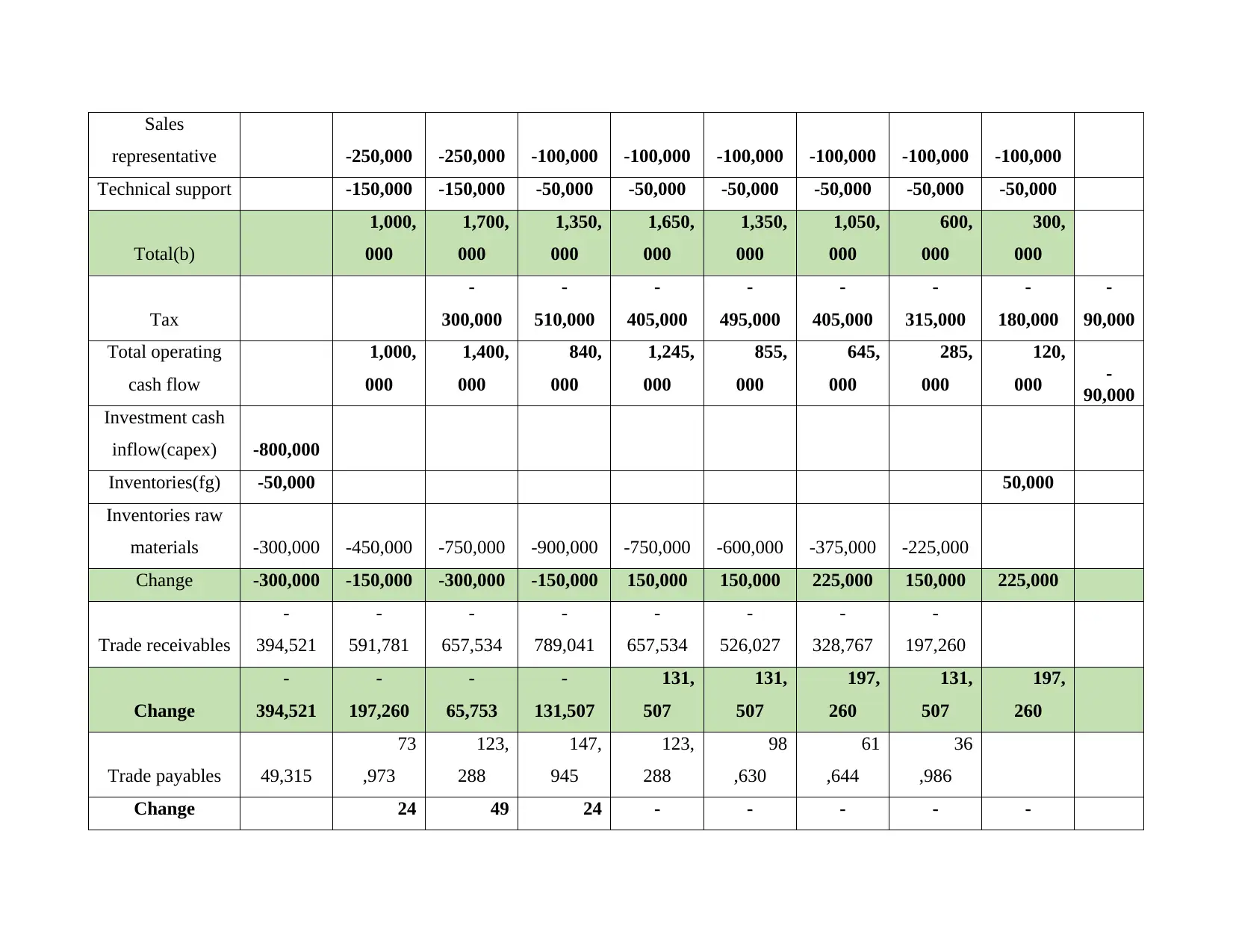

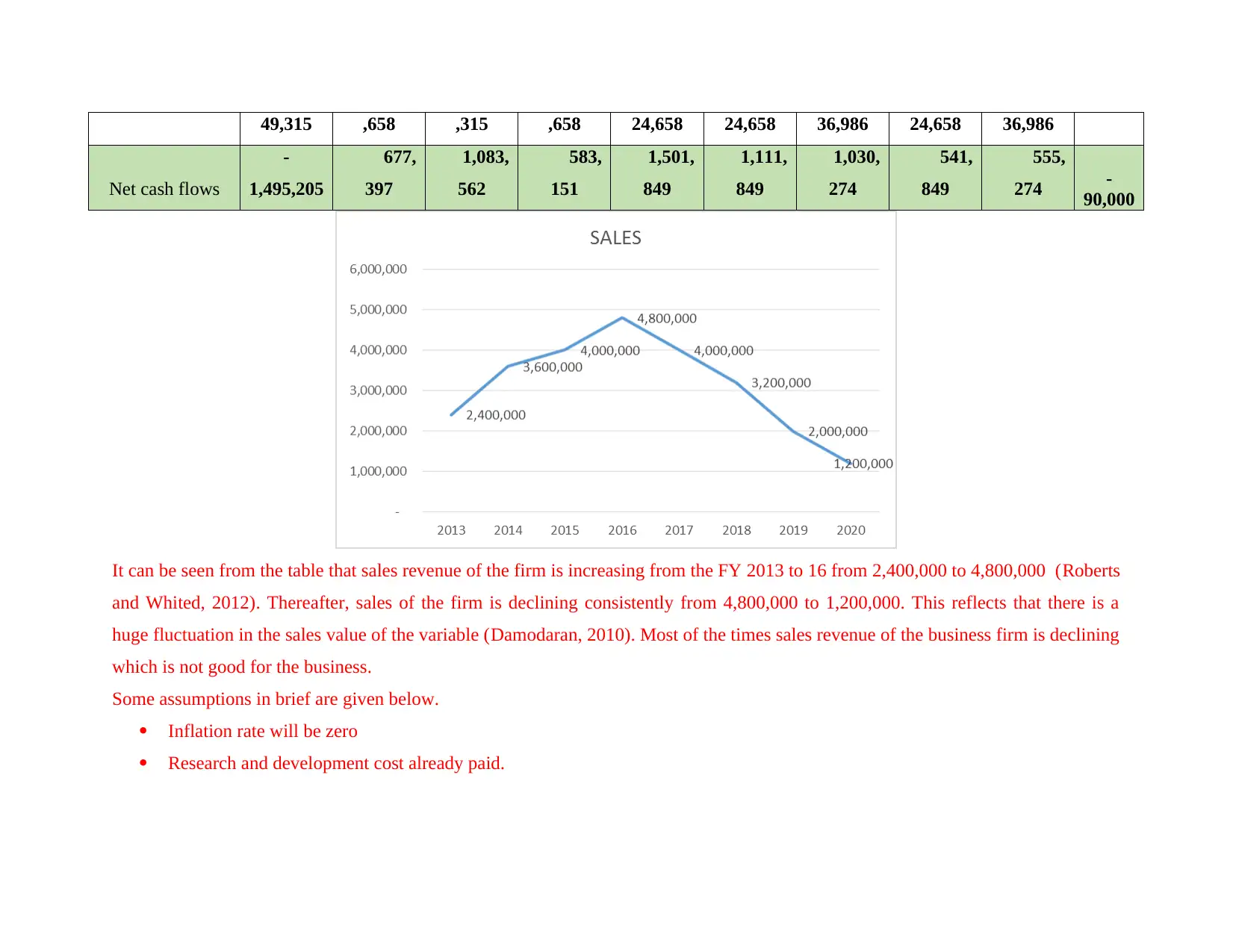

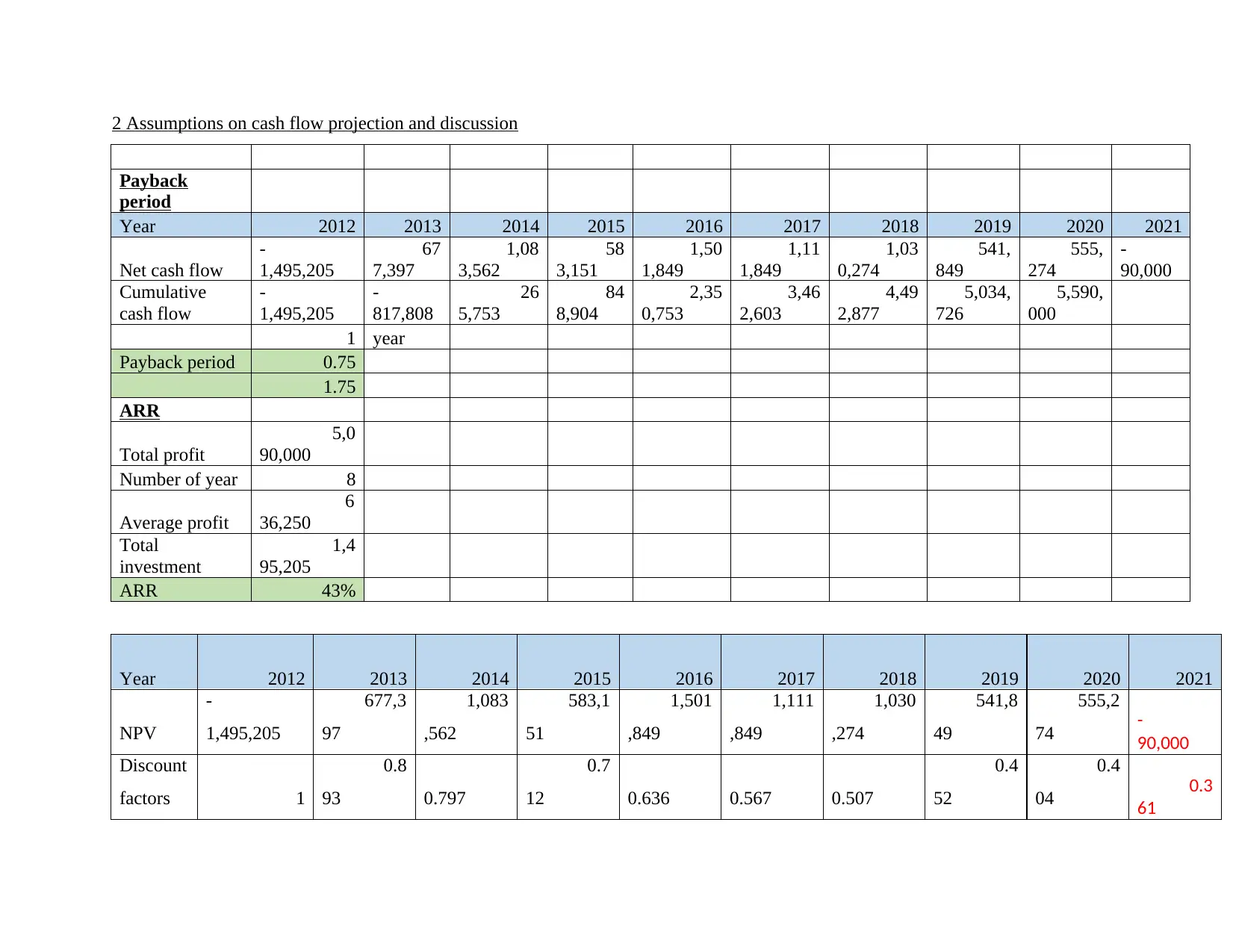

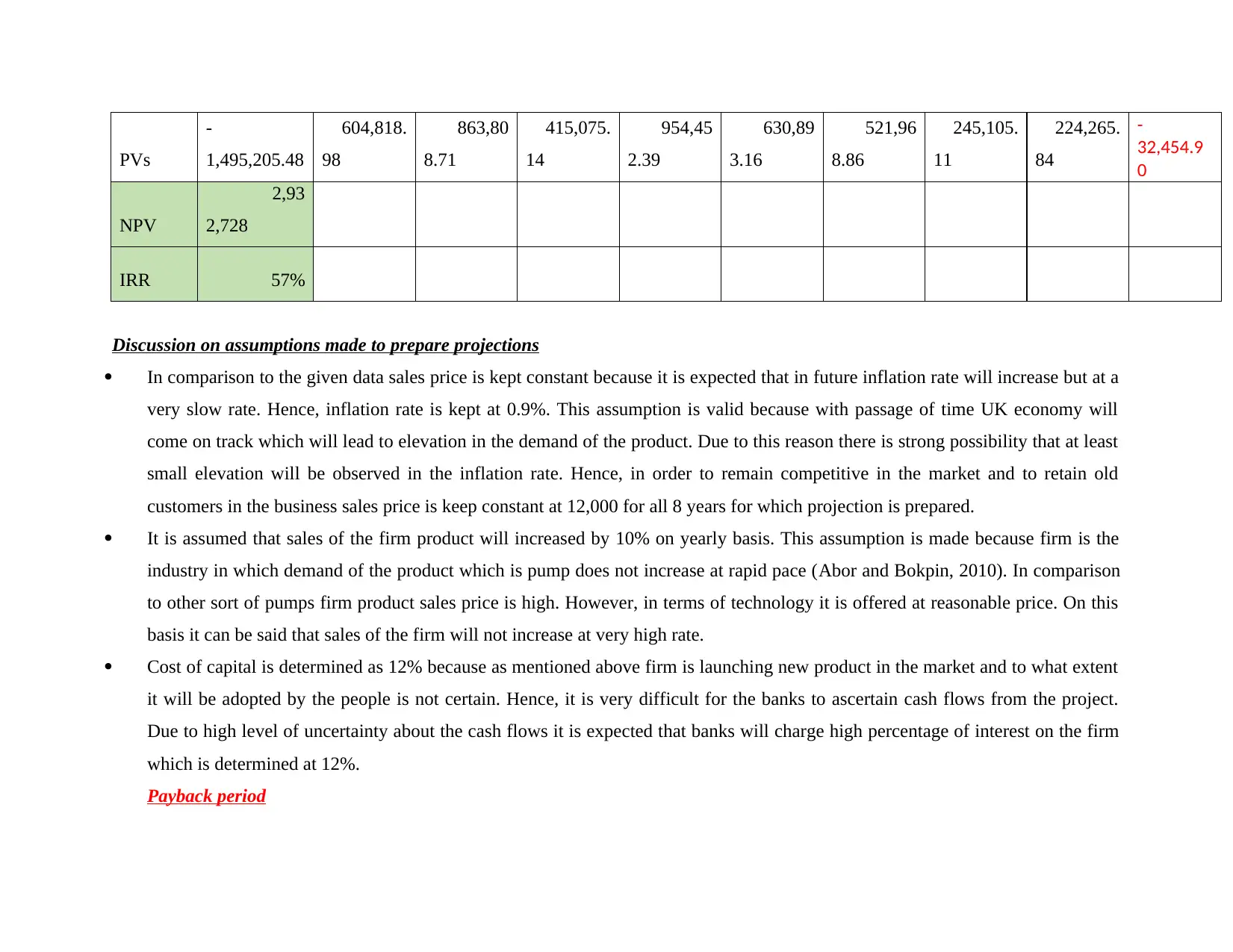

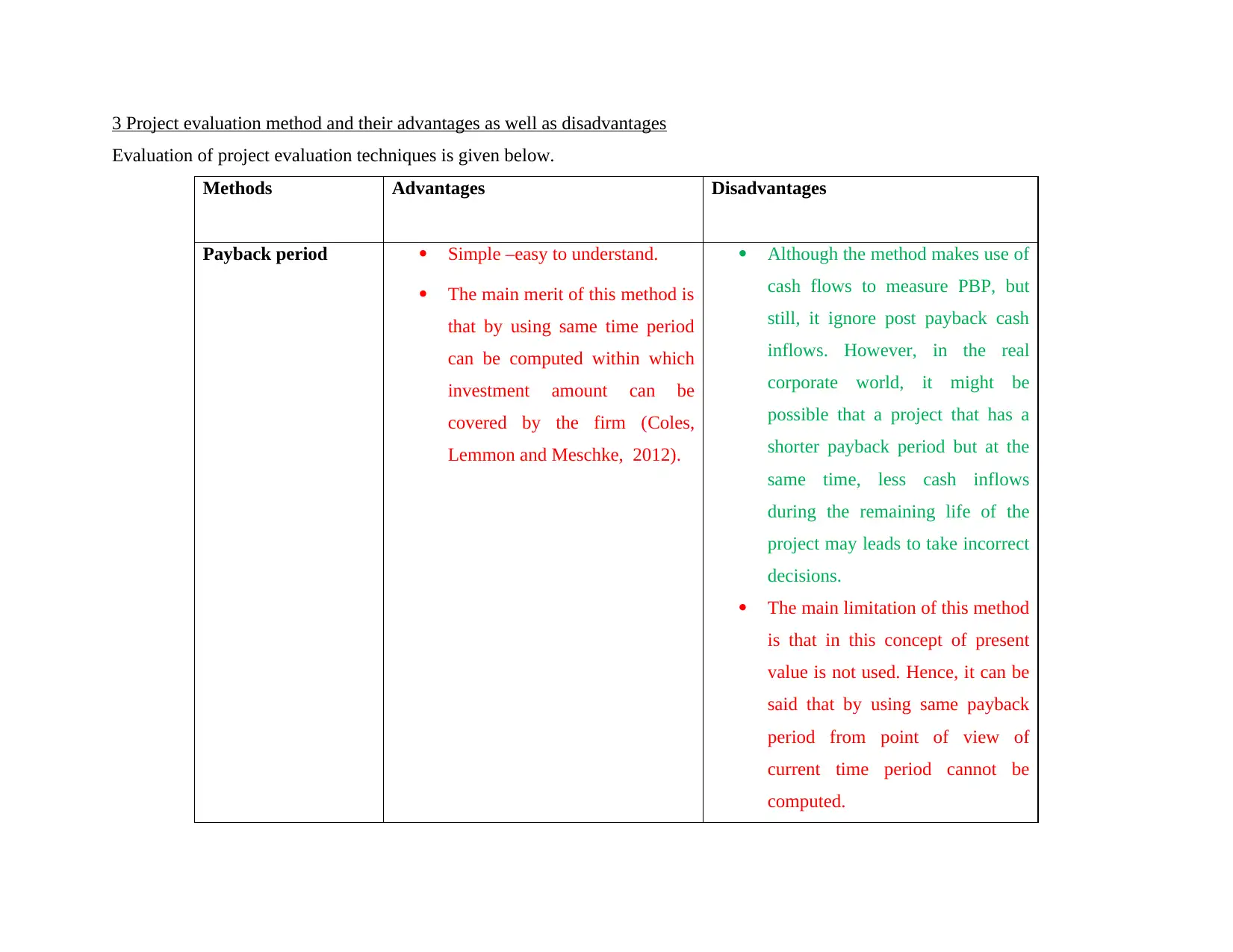

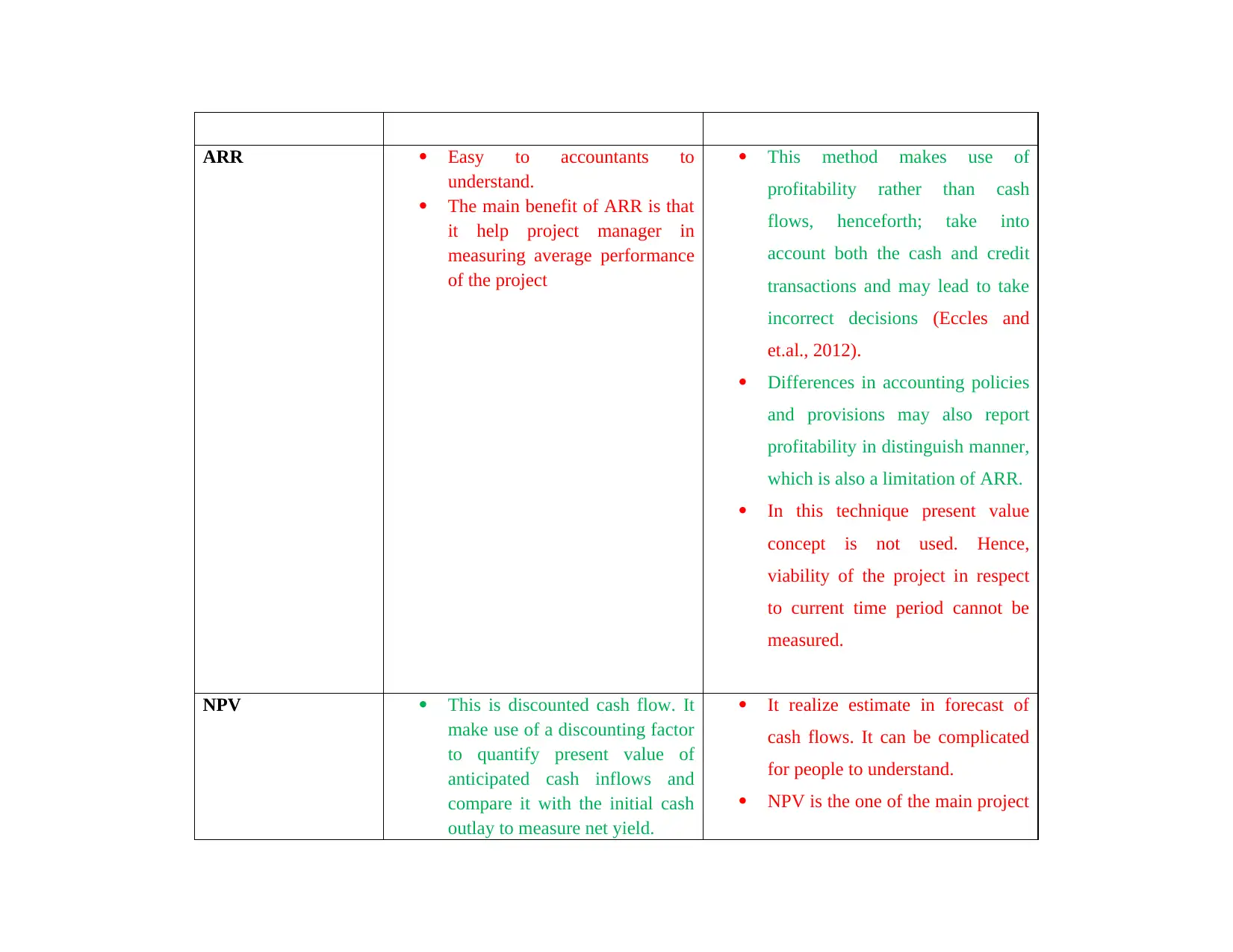

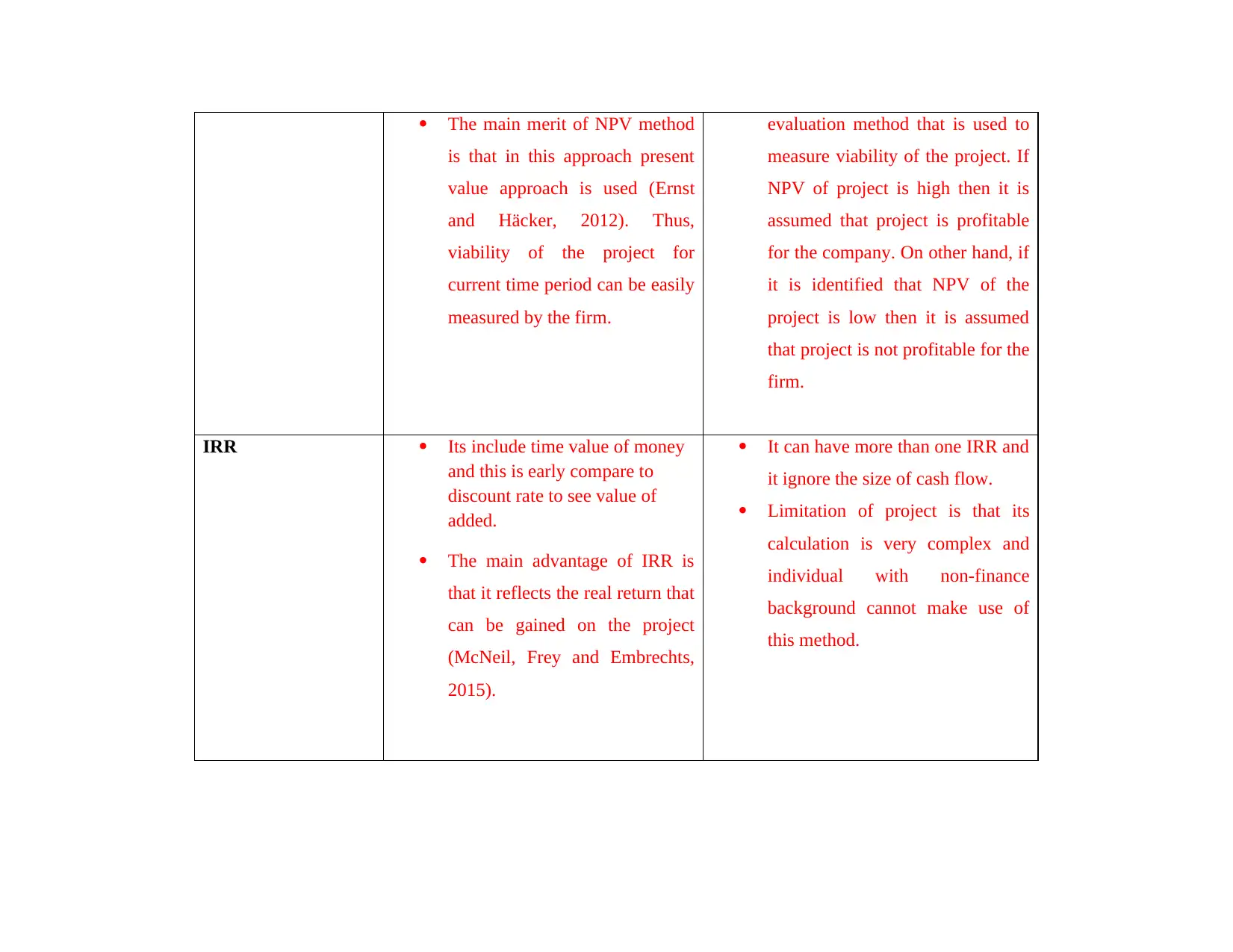

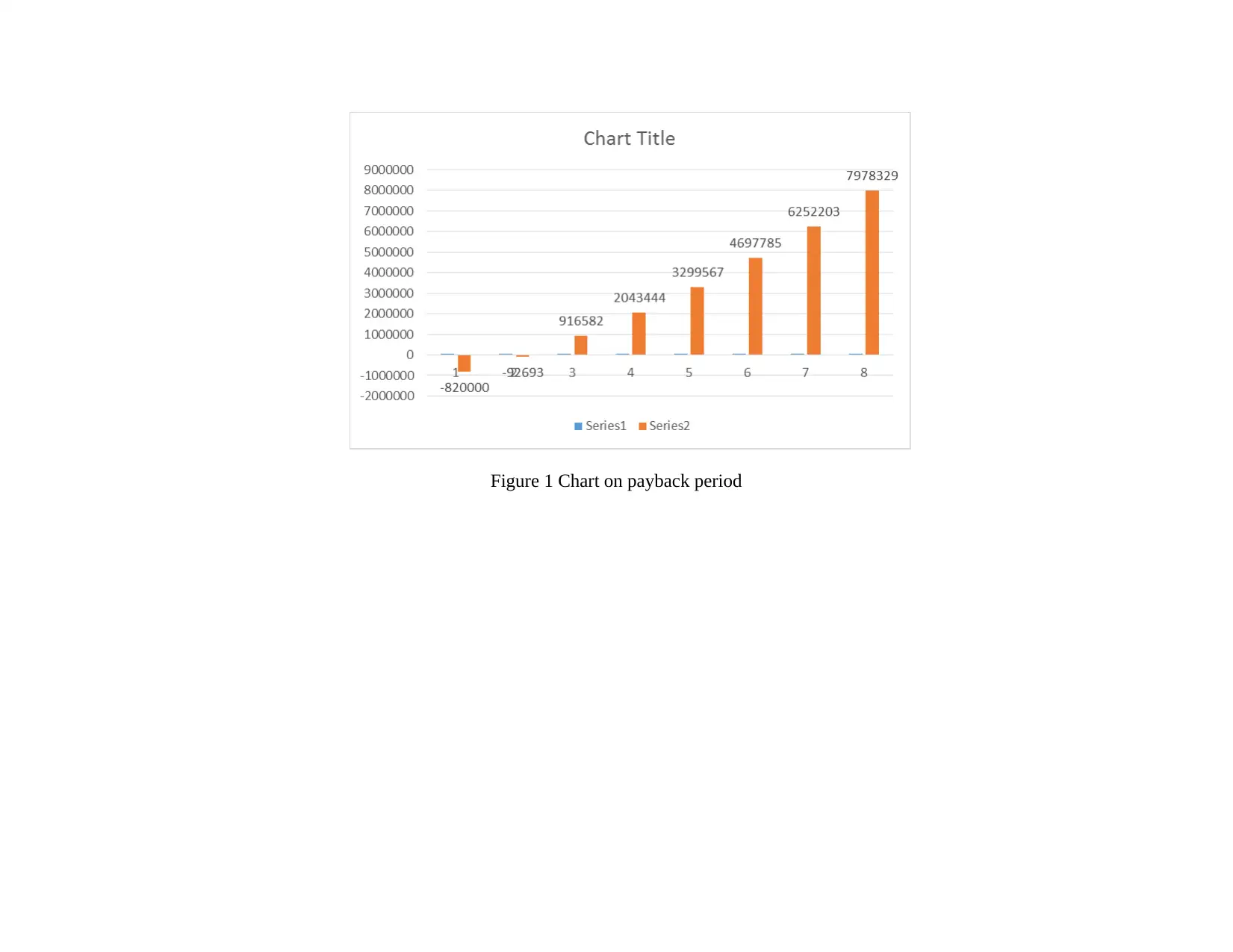

This report provides a comprehensive corporate finance analysis of the Wonder Pump project. It begins with an evaluation of potential investments, followed by assumptions on cash flow projections and a detailed discussion of various project evaluation methods, including payback period, average rate of return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR). The report then delves into sensitivity analysis, examining its impact on decisions, and assesses the effect of the discount rate on project viability. Furthermore, it covers capital structure considerations and concludes with a calculation of the weighted average cost of capital (WACC) and an analysis of its implications. The report includes tables and figures to support the financial analysis and provides a critical comparison of the project evaluation methods, highlighting the preference for NPV and IRR over payback period and ARR due to their consideration of the time value of money. Finally, the report includes several tables with calculations of payback period, ARR, NPV, IRR, sensitivity analysis of profit, CAPM, and enterprise value calculations.

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.