ACC2CAD Module: Cost and Profit Analysis of Wooden Study Table Report

VerifiedAdded on 2023/03/20

|7

|1478

|75

Report

AI Summary

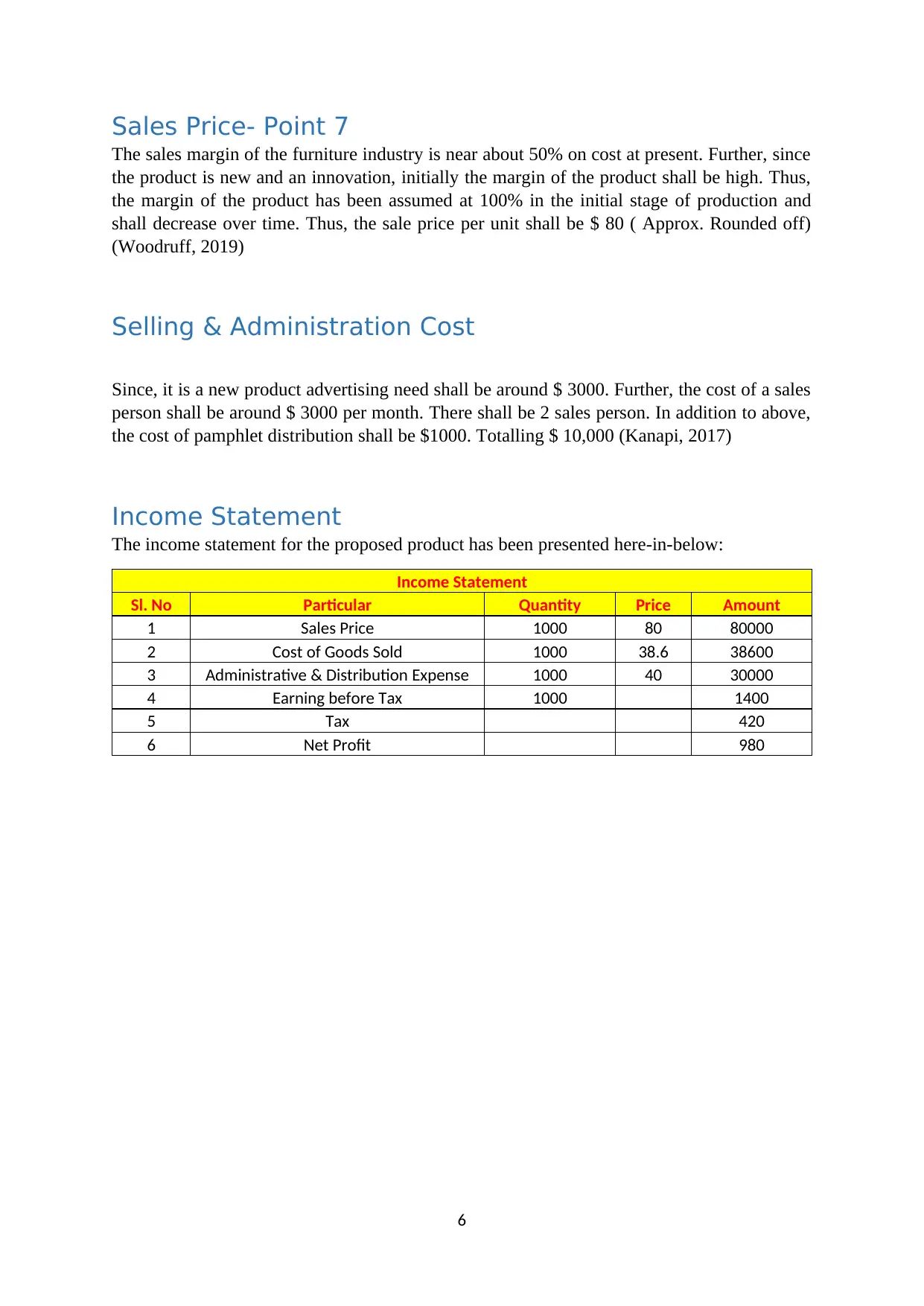

This report presents a detailed cost and profit analysis of a wooden study table. It begins with an introduction outlining the product's design, purpose, and key features, emphasizing its multi-functional use, space-saving design, and affordability. The report then breaks down the costs associated with manufacturing, including research and development (which is stated as minimal in this case), materials (wood, nails, and Fevicol), labor, and manufacturing overheads. It calculates the cost per unit, differentiates between variable and semi-fixed costs, and outlines production details, including beginning and closing inventory of raw materials, work in process, and finished goods. The sales price is determined based on industry profit margins, and selling and administrative costs, including advertising and sales personnel expenses, are estimated. Finally, the report presents an income statement, summarizing sales, cost of goods sold, administrative expenses, and profit, providing a comprehensive financial overview of the product's potential profitability. The report concludes with a list of cited references.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.