Woodside Petroleum: Factor Models, CAPM, and Portfolio Analysis Report

VerifiedAdded on 2022/11/28

|13

|2093

|299

Report

AI Summary

This report analyzes Woodside Petroleum Limited, an Australian petroleum company, using financial modeling techniques. It begins with descriptive statistics of Woodside's stock returns, including mean, standard deviation, and skewness, comparing them to the ASX All Ordinaries Index. The report then applies the Capital Asset Pricing Model (CAPM) and Single Index Model (SIM) to assess systematic risk and alpha, concluding that Woodside's systematic risk is near the market average but overall risk is not stable. It further examines the Fama and French three-factor model, discussing its factors and implications. The report presents regression results and ANOVA analysis to evaluate the significance of coefficients like Beta, SMB, and HML. The analysis continues with portfolio analysis, including variance-covariance matrices and return data for various stocks, identifying GMG as having the highest return. Finally, the report briefly discusses the impact of holding stocks for a longer period on risk and return, highlighting the increased risk due to price fluctuations. The document references key financial research papers and models to support its analysis.

Table of Contents

Question 1: Returns, CAPM.................................................................................... 1

Woodside Petroleum Limited Description...........................................................1

Descriptive Statistics....................................................................................... 2

CAPM/Single Index Model................................................................................ 5

Answer 2.1............................................................................................................. 7

Answer 2.2............................................................................................................. 8

Answer 2.3............................................................................................................. 9

Part 2.................................................................................................................. 9

Part 3.................................................................................................................. 9

Question 3........................................................................................................... 11

Ans 3.1............................................................................................................. 11

Answer 3.5........................................................................................................ 11

Question 1: Returns, CAPM.................................................................................... 1

Woodside Petroleum Limited Description...........................................................1

Descriptive Statistics....................................................................................... 2

CAPM/Single Index Model................................................................................ 5

Answer 2.1............................................................................................................. 7

Answer 2.2............................................................................................................. 8

Answer 2.3............................................................................................................. 9

Part 2.................................................................................................................. 9

Part 3.................................................................................................................. 9

Question 3........................................................................................................... 11

Ans 3.1............................................................................................................. 11

Answer 3.5........................................................................................................ 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1: Returns, CAPM

Woodside Petroleum Limited Description

Woodside Petroleum Limited is a a petroleum production and exploration company based

in Australia. The company publicly listed in the Australian Securities Exchange (ASX)

market with the headquarter located in Perth, Western Australia. Woodside is the largest

independent dedicated oil and gas company in Australia. The original company known as

Woodside (Lakes Entrance) Oil Co NL was founded in 1954. The name was then

changed to Woodside Petroleum Limited. The company has an employee base of

approximately 3300. The annual revenue for the year 2018 stood at US$5.240 billion and

net annual income of US$1.364. The current CEO of the company is Peter John Coleman

who was appointed on 30th May, 2011.

In March 2019, Woodside Energy Ltd invested in Sapien Cyber Ltd, a Western

Australian cyber security firm. The main objective of the investment was to take ten

percent shareholding in Sapien Cyber. At the beginning of September 2019, Woodsides

Energy partnered with Orange Sky Australia to launch a new AUD450,000 three-year

partnership. The move will enable Woodside extend its support of the homelessness

service in Perth through sponsorship of ‘Karla’ mobile shower and laundry van.

Woodside Petroleum Limited Description

Woodside Petroleum Limited is a a petroleum production and exploration company based

in Australia. The company publicly listed in the Australian Securities Exchange (ASX)

market with the headquarter located in Perth, Western Australia. Woodside is the largest

independent dedicated oil and gas company in Australia. The original company known as

Woodside (Lakes Entrance) Oil Co NL was founded in 1954. The name was then

changed to Woodside Petroleum Limited. The company has an employee base of

approximately 3300. The annual revenue for the year 2018 stood at US$5.240 billion and

net annual income of US$1.364. The current CEO of the company is Peter John Coleman

who was appointed on 30th May, 2011.

In March 2019, Woodside Energy Ltd invested in Sapien Cyber Ltd, a Western

Australian cyber security firm. The main objective of the investment was to take ten

percent shareholding in Sapien Cyber. At the beginning of September 2019, Woodsides

Energy partnered with Orange Sky Australia to launch a new AUD450,000 three-year

partnership. The move will enable Woodside extend its support of the homelessness

service in Perth through sponsorship of ‘Karla’ mobile shower and laundry van.

Descriptive Statistics

The graphs below show the plot of daily close price for Woodside Petroleum Limited

stock, ASX all ordinaries Index, and the respective returns on the portfolios.

7/3/2017

8/8/2017

9/13/2017

10/19/2017

11/24/2017

12/30/2017

2/4/2018

3/12/2018

4/17/2018

5/23/2018

6/28/2018

8/3/2018

9/8/2018

10/14/2018

11/19/2018

12/25/2018

1/30/2019

3/7/2019

4/12/2019

5/18/2019

6/23/2019

0.0

10.0

20.0

30.0

40.0

50.0

Graph 1.2 (a): WPL Daily Close Price

Period

Close Price (AUD)

7/3/2017

8/9/2017

9/15/2017

10/22/2017

11/28/2017

1/4/2018

2/10/2018

3/19/2018

4/25/2018

6/1/2018

7/8/2018

8/14/2018

9/20/2018

10/27/2018

12/3/2018

1/9/2019

2/15/2019

3/24/2019

4/30/2019

6/6/2019

0.0

2000.0

4000.0

6000.0

8000.0

Graph 1.2 (b): AORD Daily Close Price

Period

Close Price (AUD)

The graphs below show the plot of daily close price for Woodside Petroleum Limited

stock, ASX all ordinaries Index, and the respective returns on the portfolios.

7/3/2017

8/8/2017

9/13/2017

10/19/2017

11/24/2017

12/30/2017

2/4/2018

3/12/2018

4/17/2018

5/23/2018

6/28/2018

8/3/2018

9/8/2018

10/14/2018

11/19/2018

12/25/2018

1/30/2019

3/7/2019

4/12/2019

5/18/2019

6/23/2019

0.0

10.0

20.0

30.0

40.0

50.0

Graph 1.2 (a): WPL Daily Close Price

Period

Close Price (AUD)

7/3/2017

8/9/2017

9/15/2017

10/22/2017

11/28/2017

1/4/2018

2/10/2018

3/19/2018

4/25/2018

6/1/2018

7/8/2018

8/14/2018

9/20/2018

10/27/2018

12/3/2018

1/9/2019

2/15/2019

3/24/2019

4/30/2019

6/6/2019

0.0

2000.0

4000.0

6000.0

8000.0

Graph 1.2 (b): AORD Daily Close Price

Period

Close Price (AUD)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7/4/2017

8/9/2017

9/14/2017

10/20/2017

11/25/2017

12/31/2017

2/5/2018

3/13/2018

4/18/2018

5/24/2018

6/29/2018

8/4/2018

9/9/2018

10/15/2018

11/20/2018

12/26/2018

1/31/2019

3/8/2019

4/13/2019

5/19/2019

6/24/2019

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

Graph 1.2 (c): WPL Return

WPL simple return 0.0 WPL log return 0

Period

Return (%)

7/4/2017

8/9/2017

9/14/2017

10/20/2017

11/25/2017

12/31/2017

2/5/2018

3/13/2018

4/18/2018

5/24/2018

6/29/2018

8/4/2018

9/9/2018

10/15/2018

11/20/2018

12/26/2018

1/31/2019

3/8/2019

4/13/2019

5/19/2019

6/24/2019

-4.00

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

Graph 1.2 (d): AORD Return

AORD simple return 0 AORD log return 0

Period

Return (%)

8/9/2017

9/14/2017

10/20/2017

11/25/2017

12/31/2017

2/5/2018

3/13/2018

4/18/2018

5/24/2018

6/29/2018

8/4/2018

9/9/2018

10/15/2018

11/20/2018

12/26/2018

1/31/2019

3/8/2019

4/13/2019

5/19/2019

6/24/2019

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

Graph 1.2 (c): WPL Return

WPL simple return 0.0 WPL log return 0

Period

Return (%)

7/4/2017

8/9/2017

9/14/2017

10/20/2017

11/25/2017

12/31/2017

2/5/2018

3/13/2018

4/18/2018

5/24/2018

6/29/2018

8/4/2018

9/9/2018

10/15/2018

11/20/2018

12/26/2018

1/31/2019

3/8/2019

4/13/2019

5/19/2019

6/24/2019

-4.00

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

Graph 1.2 (d): AORD Return

AORD simple return 0 AORD log return 0

Period

Return (%)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

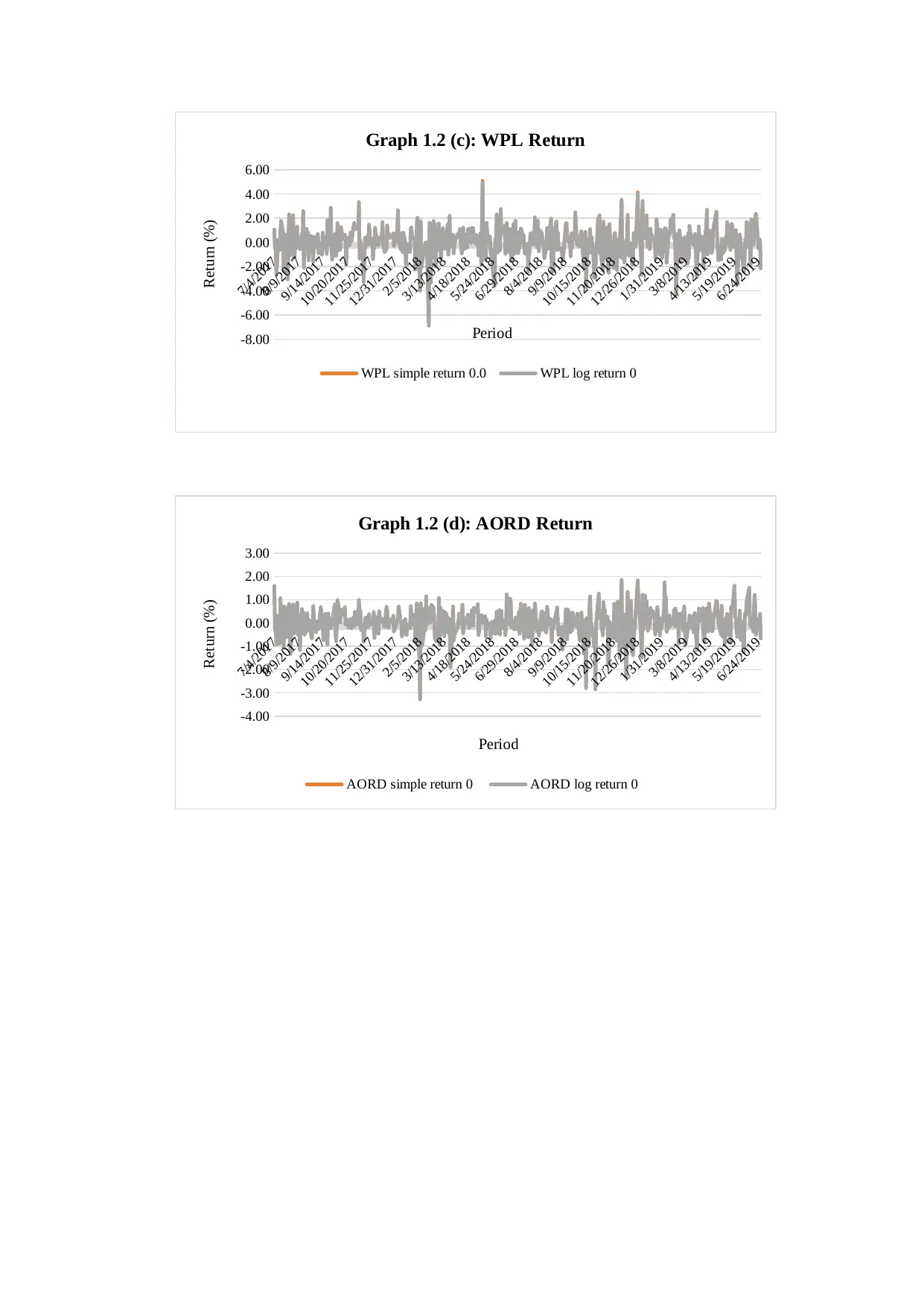

Descriptive Statistics

The table 1 shows the descriptive statistics of the return on the assets

Table 1: Descriptive Statistics for Returns

Statistics

WPL simple

return

WPL log

return

AORD simple

return

AORD log

return

Mean 0.0497 0.0413 0.0330 0.0311

Standard Error 0.0577 0.0578 0.0277 0.0278

Median 0.1355 0.1354 0.0449 0.0449

Standard

Deviation 1.2944 1.2973 0.6220 0.6234

Sample Variance 1.6755 1.6830 0.3869 0.3886

Kurtosis 1.9168 2.0730 3.1895 3.3428

Skewness -0.3668 -0.4410 -0.7862 -0.8292

Range 11.7580 11.8642 5.0952 5.1316

Minimum -6.6575 -6.8895 -3.2341 -3.2876

Maximum 5.1005 4.9747 1.8611 1.8440

Sum 25.0467 20.8157 16.6494 15.6709

Count 504 504 540 504

The average continuous return is 0.0413% with a standard deviation of 1.2973% for

Woodside Petroleum Limited. The large standard deviation shows that the returns are not

stable and the average fluctuation is more than the average fluctuation of market.

However, for the ASX all ordinaries index the average return is 0.0311% with a standard

deviation of 0.6234%. The deviation is twice the average which indicate that the returns

have not been stable for the last two years.

The table 1 shows the descriptive statistics of the return on the assets

Table 1: Descriptive Statistics for Returns

Statistics

WPL simple

return

WPL log

return

AORD simple

return

AORD log

return

Mean 0.0497 0.0413 0.0330 0.0311

Standard Error 0.0577 0.0578 0.0277 0.0278

Median 0.1355 0.1354 0.0449 0.0449

Standard

Deviation 1.2944 1.2973 0.6220 0.6234

Sample Variance 1.6755 1.6830 0.3869 0.3886

Kurtosis 1.9168 2.0730 3.1895 3.3428

Skewness -0.3668 -0.4410 -0.7862 -0.8292

Range 11.7580 11.8642 5.0952 5.1316

Minimum -6.6575 -6.8895 -3.2341 -3.2876

Maximum 5.1005 4.9747 1.8611 1.8440

Sum 25.0467 20.8157 16.6494 15.6709

Count 504 504 540 504

The average continuous return is 0.0413% with a standard deviation of 1.2973% for

Woodside Petroleum Limited. The large standard deviation shows that the returns are not

stable and the average fluctuation is more than the average fluctuation of market.

However, for the ASX all ordinaries index the average return is 0.0311% with a standard

deviation of 0.6234%. The deviation is twice the average which indicate that the returns

have not been stable for the last two years.

CAPM/Single Index Model

The mathematical expression of SIM is

ri , t−r f =α + β ( rm , t−rf ) + εi

where:

ri , t - is return to stock i in period t

r f - is the risk-free rate (i.e. the interest rate on treasury bills)

rm , t - is the return to the market portfolio in period t

α - is the stock's alpha, or abnormal return

β - is the stock’s beta, or responsiveness to the market return

Note that ri , t−r f is called the excess return on the stock, rm , t −rf the excess return on

the market and ε i are the residual (random) returns, which are assumed independent

normally distributed with mean zero and standard deviation.

For simplicity the model is defined as follows in excel:

Coefficient

s

Standar

d Error t Stat P-value

Intercept 0.0972 0.0899 1.0817 0.2799

rm , t −rf 1.0917 0.0792

13.792

3 0.0000

From the results of the analysis, it may be inferred that systematic risk of Woodside

Petroleum Limited is 1.0917 which is approximately near to the market which is 1. Thus,

it may be concluded that the stock is not risky from systematic risk point of view.

The mathematical expression of SIM is

ri , t−r f =α + β ( rm , t−rf ) + εi

where:

ri , t - is return to stock i in period t

r f - is the risk-free rate (i.e. the interest rate on treasury bills)

rm , t - is the return to the market portfolio in period t

α - is the stock's alpha, or abnormal return

β - is the stock’s beta, or responsiveness to the market return

Note that ri , t−r f is called the excess return on the stock, rm , t −rf the excess return on

the market and ε i are the residual (random) returns, which are assumed independent

normally distributed with mean zero and standard deviation.

For simplicity the model is defined as follows in excel:

Coefficient

s

Standar

d Error t Stat P-value

Intercept 0.0972 0.0899 1.0817 0.2799

rm , t −rf 1.0917 0.0792

13.792

3 0.0000

From the results of the analysis, it may be inferred that systematic risk of Woodside

Petroleum Limited is 1.0917 which is approximately near to the market which is 1. Thus,

it may be concluded that the stock is not risky from systematic risk point of view.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

However, when analysed from overall risk perspective, the said observation negates.

Further, the alpha of the stock is 9% which is good.

Further, the alpha of the stock is 9% which is good.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer 2.1

The fama and French model was discovered by Nobel laureates Eugene Fama with his junior

Kenneth French in the year 1990s.The Fama and French model has three principal important

factors like the firm size ,book to market values and excess return on market.The three

principal factors are small minus big(SMB),high minus low(HML) and the return on portfolio

minus the risk free rate of return.The small minus big mostly consider companies related to

public with a very small market cap and yield high rate of return.The other one high minus

low mostly consider the stocks with a very high book to market ratios that yield a very rate of

return as comparison to the market rate of return.The main three factor model of Fama French

is that it is an asset pricing model that expands on the CAPM model through addition of size

risk and value risk factor to the market factor. This model is essentially the outcome for an

econometric regression of the prices of stock which are historical. (Business and Economics

Research Journal, 2016)

The Fama and French model main highlight point is that the investors must be able to borne

the extra volatility which occur in the short term and the stock underperformance which could

also occur in the short span of time. The investors who go long for any particular stock must

be awarded with the benefits which could be adjusted with the short-term losses suffered. It is

also a very active tool to understand the performance of portfolio, to measure the impact of

active management, construction of portfolio, and to estimate the return in future. (Forbes

Media LLC, 2019)

The fama and French model was discovered by Nobel laureates Eugene Fama with his junior

Kenneth French in the year 1990s.The Fama and French model has three principal important

factors like the firm size ,book to market values and excess return on market.The three

principal factors are small minus big(SMB),high minus low(HML) and the return on portfolio

minus the risk free rate of return.The small minus big mostly consider companies related to

public with a very small market cap and yield high rate of return.The other one high minus

low mostly consider the stocks with a very high book to market ratios that yield a very rate of

return as comparison to the market rate of return.The main three factor model of Fama French

is that it is an asset pricing model that expands on the CAPM model through addition of size

risk and value risk factor to the market factor. This model is essentially the outcome for an

econometric regression of the prices of stock which are historical. (Business and Economics

Research Journal, 2016)

The Fama and French model main highlight point is that the investors must be able to borne

the extra volatility which occur in the short term and the stock underperformance which could

also occur in the short span of time. The investors who go long for any particular stock must

be awarded with the benefits which could be adjusted with the short-term losses suffered. It is

also a very active tool to understand the performance of portfolio, to measure the impact of

active management, construction of portfolio, and to estimate the return in future. (Forbes

Media LLC, 2019)

Answer 2.2

The regression results along with the fit summary is enclosed in excel. Further, a brief

snapshot is presented as under:

Regression Statistics

Multiple R 0.5303

R Square 0.2813

Adjusted R

Square 0.2769

Standard

Error 1.1042

Observatio

ns 503

ANOVA

df SS MS F

Significa

nce F

Regression 3 238.0889

79.3

630

65.0

872 0.0000

Residual 499 608.4473

1.21

93

Total 502 846.5362

Coeffic

ients

Standard

Error

t

Stat

P-

valu

e

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.0807 0.0901

0.89

56

0.37

09 -0.0963 0.2577 -0.0963 0.2577

X 1.0718 0.0796

13.4

699

0.00

00 0.9155 1.2282 0.9155 1.2282

SMB 0.7150 2.1244

0.33

65

0.73

66 -3.4590 4.8889 -3.4590 4.8889

HML

-

2.1541 5.5227

-

0.39

00

0.69

67 -13.0048 8.6966

-

13.0048 8.6966

The regression results along with the fit summary is enclosed in excel. Further, a brief

snapshot is presented as under:

Regression Statistics

Multiple R 0.5303

R Square 0.2813

Adjusted R

Square 0.2769

Standard

Error 1.1042

Observatio

ns 503

ANOVA

df SS MS F

Significa

nce F

Regression 3 238.0889

79.3

630

65.0

872 0.0000

Residual 499 608.4473

1.21

93

Total 502 846.5362

Coeffic

ients

Standard

Error

t

Stat

P-

valu

e

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.0807 0.0901

0.89

56

0.37

09 -0.0963 0.2577 -0.0963 0.2577

X 1.0718 0.0796

13.4

699

0.00

00 0.9155 1.2282 0.9155 1.2282

SMB 0.7150 2.1244

0.33

65

0.73

66 -3.4590 4.8889 -3.4590 4.8889

HML

-

2.1541 5.5227

-

0.39

00

0.69

67 -13.0048 8.6966

-

13.0048 8.6966

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Answer 2.3

On perusal of the ANOVA, it may be inferred that Alpha represented by Intercept has a P

Value of 0.3709 which is significantly high and indicates a poor strength of the

significance of the coefficient.

The Beta represented by X has a P Value of 0 which shows that the coefficient is

statistically significant and important for analysis purpose.

For SMB, the value of P is .7366 which is significantly high and indicates a poor strength

of the significance of the coefficient. Similarly for HML, the value of P is .6967 which is

significantly high and indicates a poor strength of the significance of the coefficient

The implications of the above P value shows the importance of the variable in the

equation and how accurately the variable of Y can be derived from the given variable.

Part 2

The largest significant coefficient out of Beta, SMB and HML is Beta as it has P value of

zero, an evidence of strong significance. It shows that observation probability of deviation

from the mean is zero. (John Wiley & Sons, 2019)

It means that Beta has significant predicting power on the variable Y and has the highest

impact on the outcome.

Part 3

R Squared is a statistical measure which helps in analysing the proportion of variance for

a dependent variable i.e. Y can be explained by an independent variable i.e. Beta, HML

and CMB in a regression model. In the current case, the R squared works out to be .2813

which is very low symbolising that the independent variable are not able to explain up to

72% of the variance of dependent variable movement and there are other significant

factors which needs to be considered in the analysis. (Frost, 2019)

On perusal of the ANOVA, it may be inferred that Alpha represented by Intercept has a P

Value of 0.3709 which is significantly high and indicates a poor strength of the

significance of the coefficient.

The Beta represented by X has a P Value of 0 which shows that the coefficient is

statistically significant and important for analysis purpose.

For SMB, the value of P is .7366 which is significantly high and indicates a poor strength

of the significance of the coefficient. Similarly for HML, the value of P is .6967 which is

significantly high and indicates a poor strength of the significance of the coefficient

The implications of the above P value shows the importance of the variable in the

equation and how accurately the variable of Y can be derived from the given variable.

Part 2

The largest significant coefficient out of Beta, SMB and HML is Beta as it has P value of

zero, an evidence of strong significance. It shows that observation probability of deviation

from the mean is zero. (John Wiley & Sons, 2019)

It means that Beta has significant predicting power on the variable Y and has the highest

impact on the outcome.

Part 3

R Squared is a statistical measure which helps in analysing the proportion of variance for

a dependent variable i.e. Y can be explained by an independent variable i.e. Beta, HML

and CMB in a regression model. In the current case, the R squared works out to be .2813

which is very low symbolising that the independent variable are not able to explain up to

72% of the variance of dependent variable movement and there are other significant

factors which needs to be considered in the analysis. (Frost, 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Residual means observed value of the dependent variable i.e Y and the predicted value of

Y. It represents the portion of the variability which is unexplained by the regression

model. In the current case, the value works out to be 72% and it is very high.

On the R Squared or coefficient of determination front, Fama French Model is better as

the variability is better explained in the Fama Model compared to CPM. Thus, on the

basis of coefficient of determination result it may be concluded that Fama- French Three

Factor Model is a better fit.

Y. It represents the portion of the variability which is unexplained by the regression

model. In the current case, the value works out to be 72% and it is very high.

On the R Squared or coefficient of determination front, Fama French Model is better as

the variability is better explained in the Fama Model compared to CPM. Thus, on the

basis of coefficient of determination result it may be concluded that Fama- French Three

Factor Model is a better fit.

Question 3

Ans 3.1

The variance Covariance Matrix has been presented here-in-below:

Variance Covariance Matrix

CSL BXB CBA GMG SYD WBC WPL NAB IAG RIO

CSL 0.00017 0.00005 0.00004 0.00004 0.00005 0.00004 0.00004 0.00003 0.00004 0.00003

BXB 0.00005 0.00011 0.00003 0.00003 0.00003 0.00003 0.00003 0.00003 0.00003 0.00001

CBA 0.00004 0.00003 0.00011 0.00002 0.00002 0.00009 0.00003 0.00007 0.00005 0.00003

GMG 0.00004 0.00003 0.00002 0.00012 0.00005 0.00003 0.00001 0.00002 0.00004 0.00000

SYD 0.00005 0.00003 0.00002 0.00005 0.00014 0.00003 0.00002 0.00002 0.00003 0.00000

WBC 0.00004 0.00003 0.00009 0.00003 0.00003 0.00013 0.00004 0.00009 0.00005 0.00003

WPL 0.00004 0.00003 0.00003 0.00001 0.00002 0.00004 0.00017 0.00003 0.00003 0.00006

NAB 0.00003 0.00003 0.00007 0.00002 0.00002 0.00009 0.00003 0.00010 0.00004 0.00002

IAG 0.00004 0.00003 0.00005 0.00004 0.00003 0.00005 0.00003 0.00004 0.00014 0.00003

RIO 0.00003 0.00001 0.00003 0.00000 0.00000 0.00003 0.00006 0.00002 0.00003 0.00021

The data for selected asset returns have been presented here-in-below:

CSL BXB CBA GMG SYD WBC WPL NAB IAG RIO

0.0009 0.0006 0.0000 0.0013 0.0003 -0.0001 0.0004 -0.0002 0.0004 0.0010

Based on the data presented, it can be concluded that GMG has the highest return among

the 10 stocks. Further, the data represents compounded return per day. On the variance

front, the highest variance is for Rio which has a variance of daily returns of 0.00021 with

a return of .0010. As far as covariance is concerned, the highest covariance, measure of

joint variability of data, among stocks is for WBC and NAB which stands at 0.0009.

Thus, on a prima facie glance the best stock among the given is GMG as the highest

return with a variance of .00012.

Answer 3.5

If the stocks are held for a period of two months, the risk shall increase on account of

rapid change in prices witnesses by the stock chosen over the period. Further, the return

Ans 3.1

The variance Covariance Matrix has been presented here-in-below:

Variance Covariance Matrix

CSL BXB CBA GMG SYD WBC WPL NAB IAG RIO

CSL 0.00017 0.00005 0.00004 0.00004 0.00005 0.00004 0.00004 0.00003 0.00004 0.00003

BXB 0.00005 0.00011 0.00003 0.00003 0.00003 0.00003 0.00003 0.00003 0.00003 0.00001

CBA 0.00004 0.00003 0.00011 0.00002 0.00002 0.00009 0.00003 0.00007 0.00005 0.00003

GMG 0.00004 0.00003 0.00002 0.00012 0.00005 0.00003 0.00001 0.00002 0.00004 0.00000

SYD 0.00005 0.00003 0.00002 0.00005 0.00014 0.00003 0.00002 0.00002 0.00003 0.00000

WBC 0.00004 0.00003 0.00009 0.00003 0.00003 0.00013 0.00004 0.00009 0.00005 0.00003

WPL 0.00004 0.00003 0.00003 0.00001 0.00002 0.00004 0.00017 0.00003 0.00003 0.00006

NAB 0.00003 0.00003 0.00007 0.00002 0.00002 0.00009 0.00003 0.00010 0.00004 0.00002

IAG 0.00004 0.00003 0.00005 0.00004 0.00003 0.00005 0.00003 0.00004 0.00014 0.00003

RIO 0.00003 0.00001 0.00003 0.00000 0.00000 0.00003 0.00006 0.00002 0.00003 0.00021

The data for selected asset returns have been presented here-in-below:

CSL BXB CBA GMG SYD WBC WPL NAB IAG RIO

0.0009 0.0006 0.0000 0.0013 0.0003 -0.0001 0.0004 -0.0002 0.0004 0.0010

Based on the data presented, it can be concluded that GMG has the highest return among

the 10 stocks. Further, the data represents compounded return per day. On the variance

front, the highest variance is for Rio which has a variance of daily returns of 0.00021 with

a return of .0010. As far as covariance is concerned, the highest covariance, measure of

joint variability of data, among stocks is for WBC and NAB which stands at 0.0009.

Thus, on a prima facie glance the best stock among the given is GMG as the highest

return with a variance of .00012.

Answer 3.5

If the stocks are held for a period of two months, the risk shall increase on account of

rapid change in prices witnesses by the stock chosen over the period. Further, the return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.