Corporate Finance Report: Analysis of Woolworths Limited (2024)

VerifiedAdded on 2021/06/17

|15

|2427

|23

Report

AI Summary

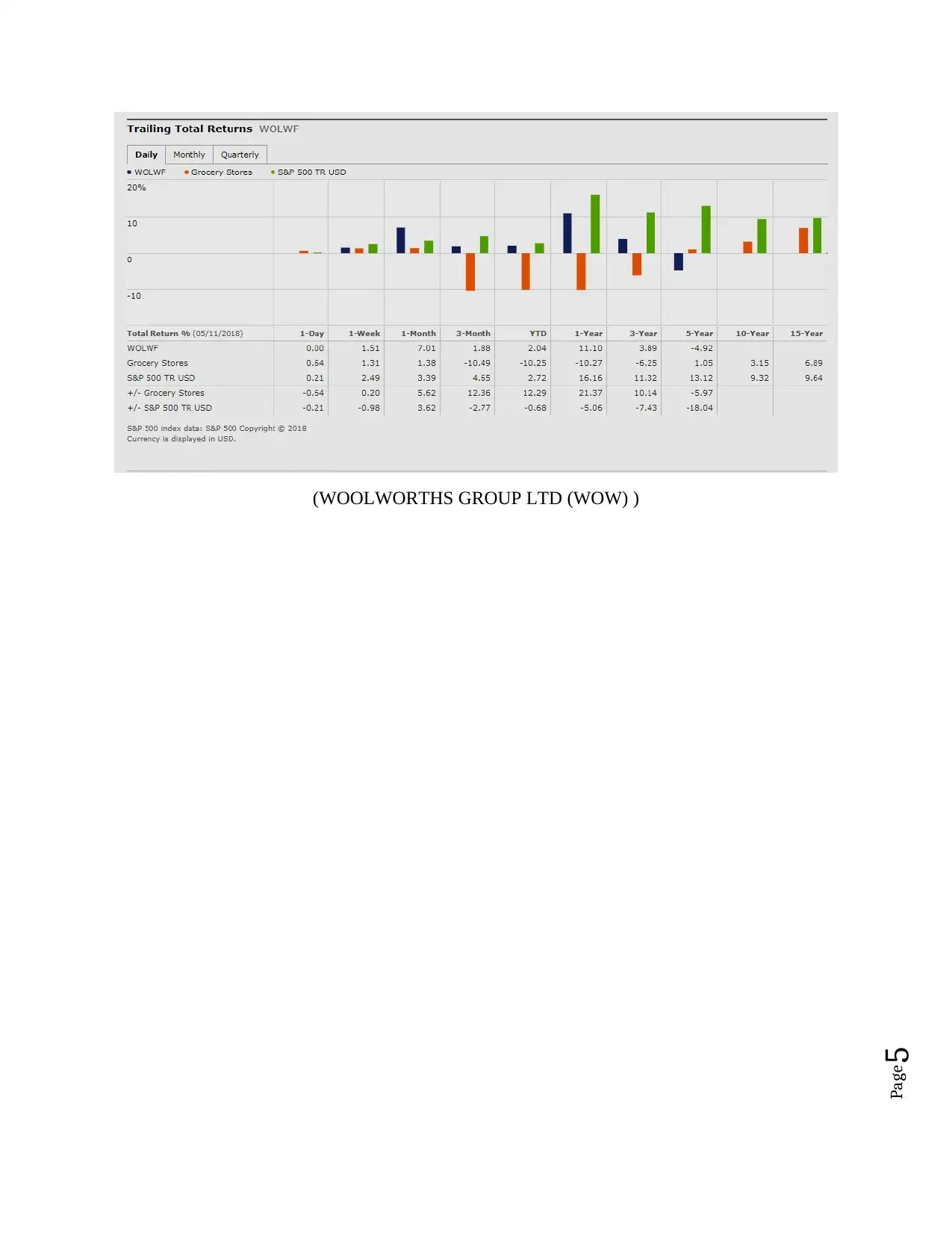

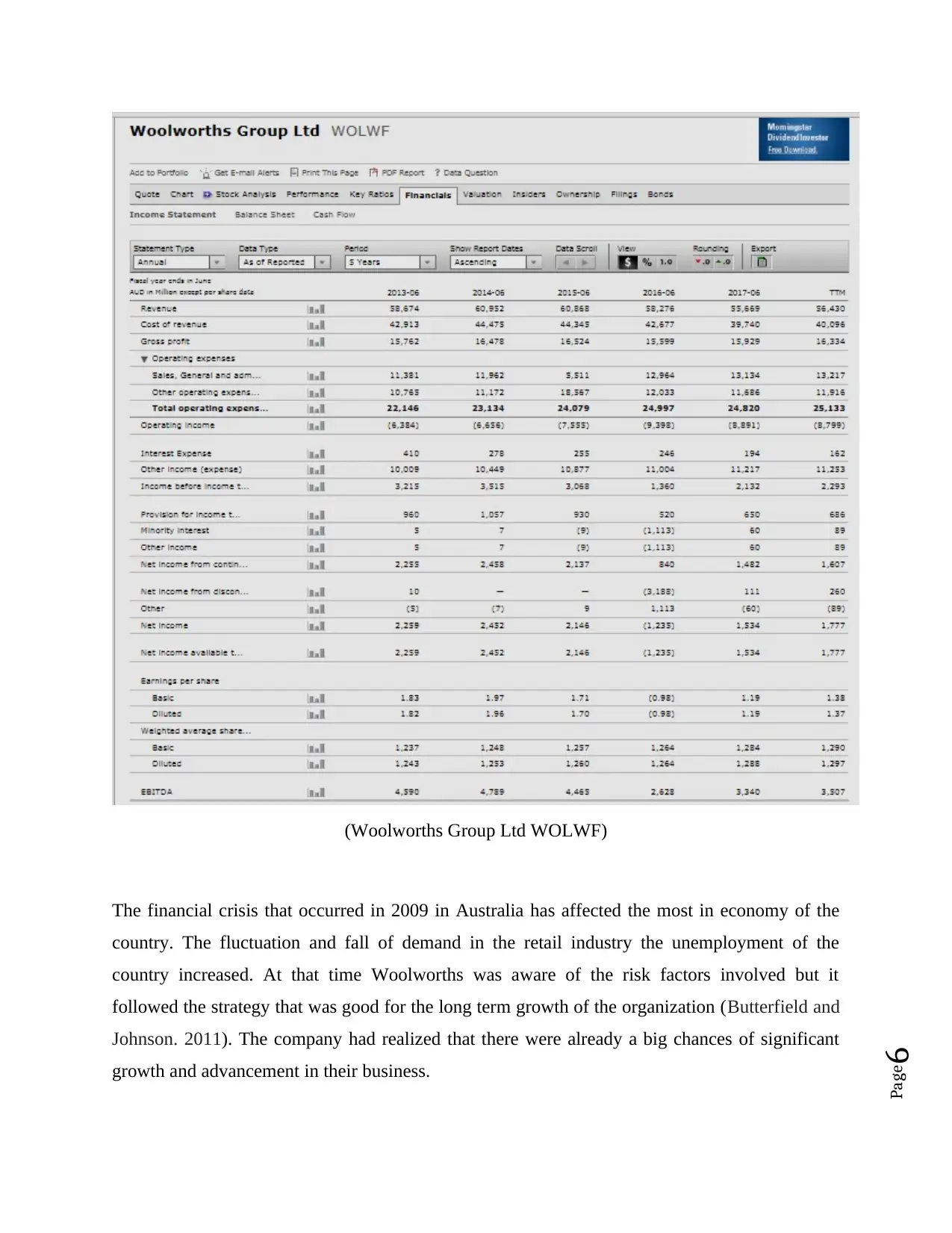

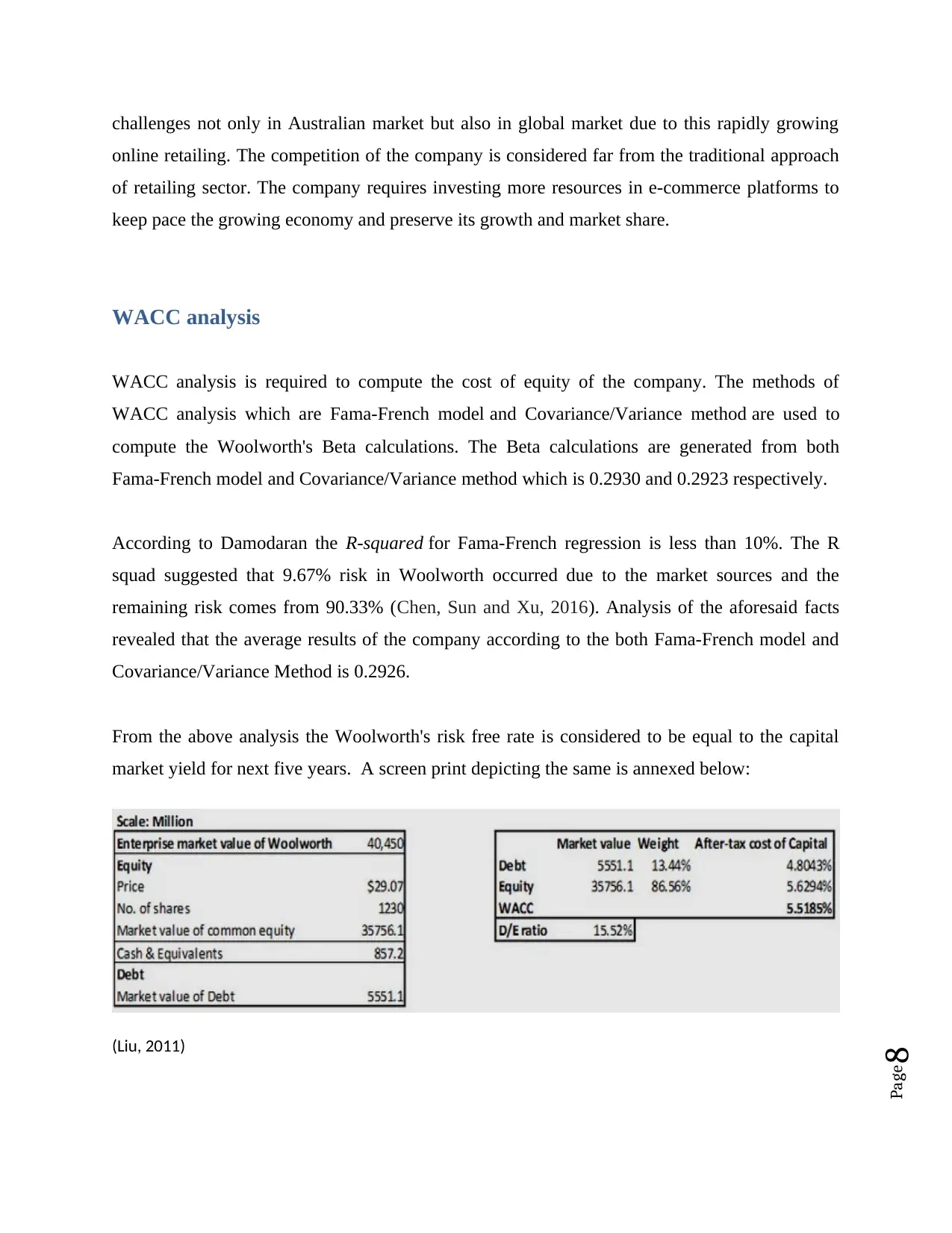

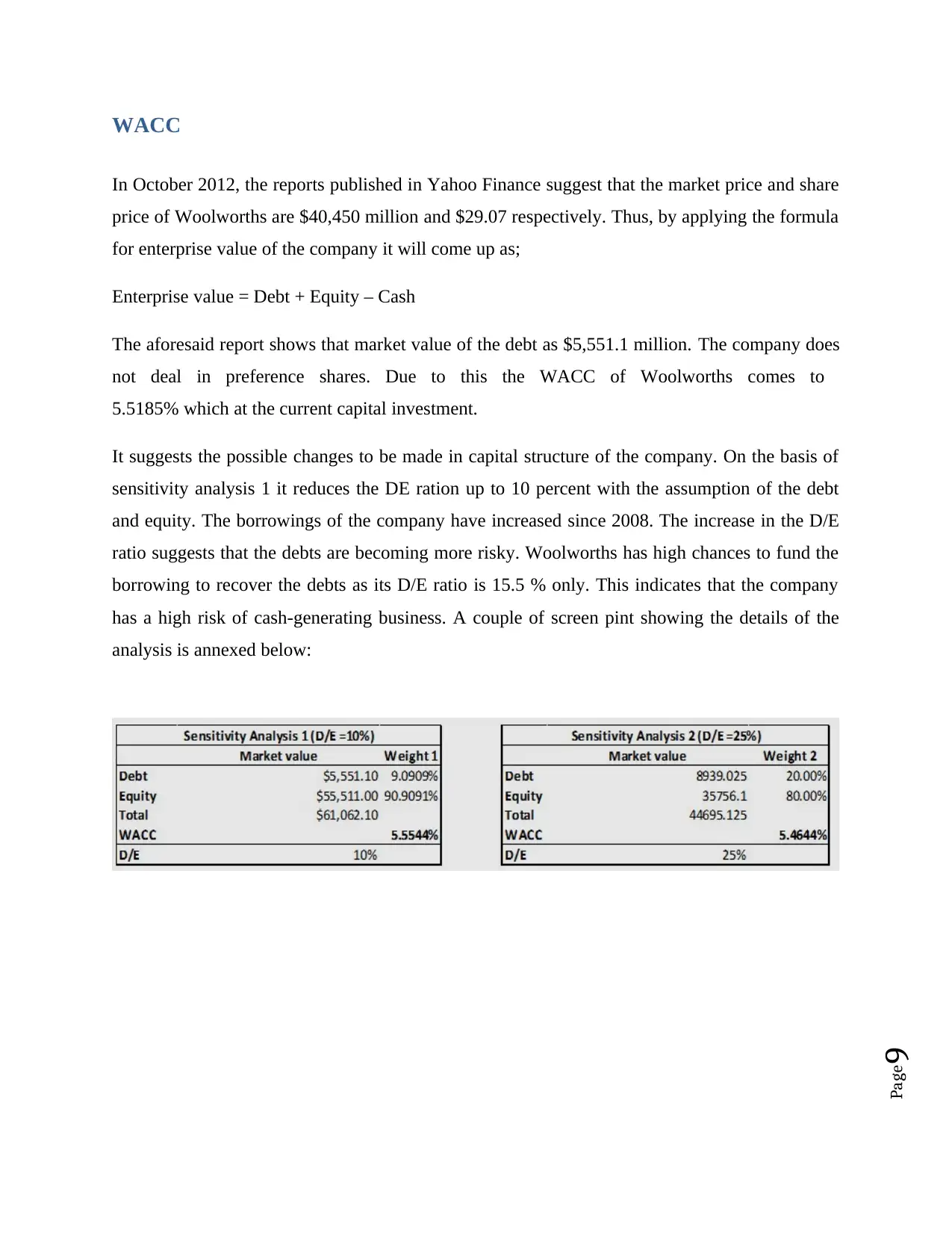

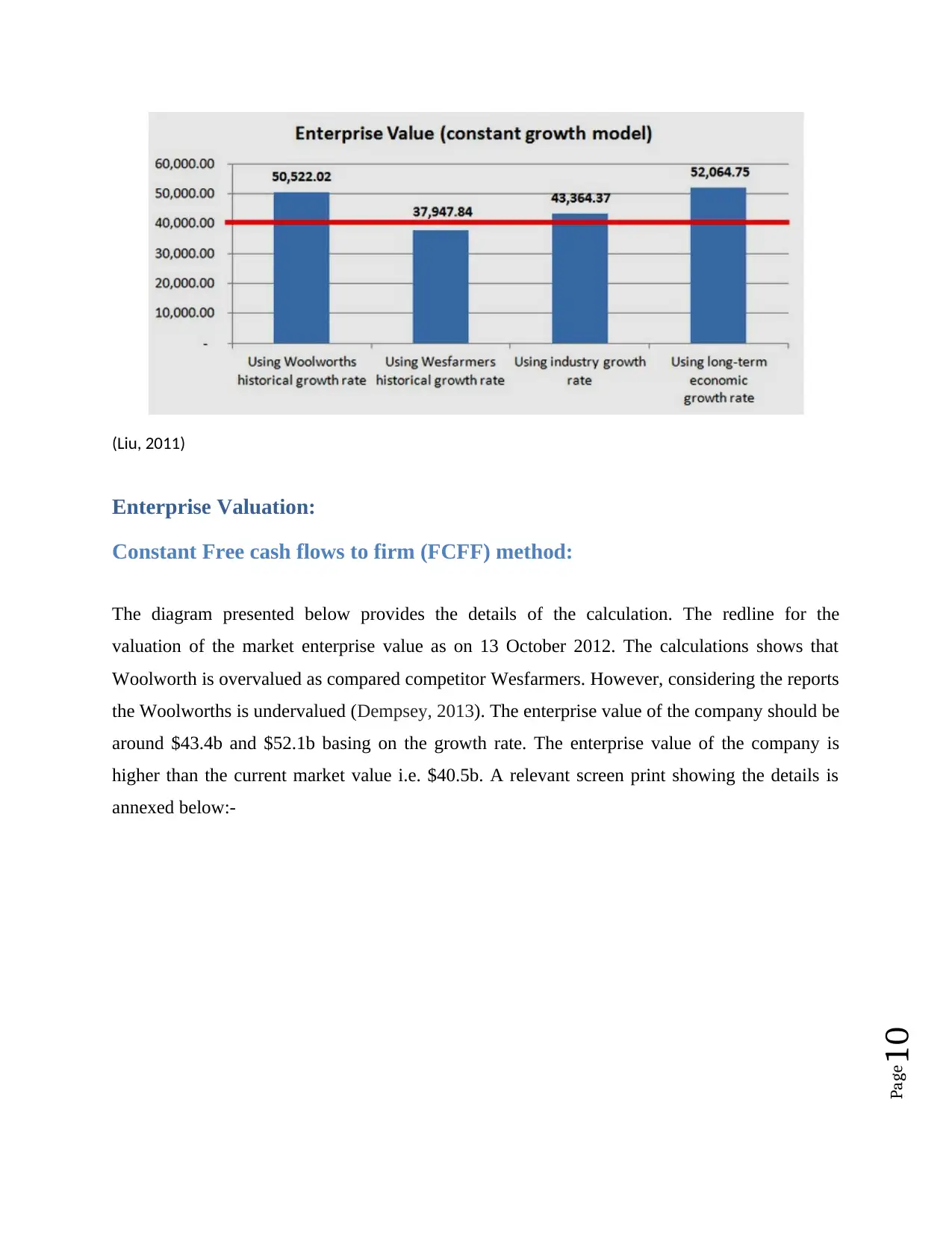

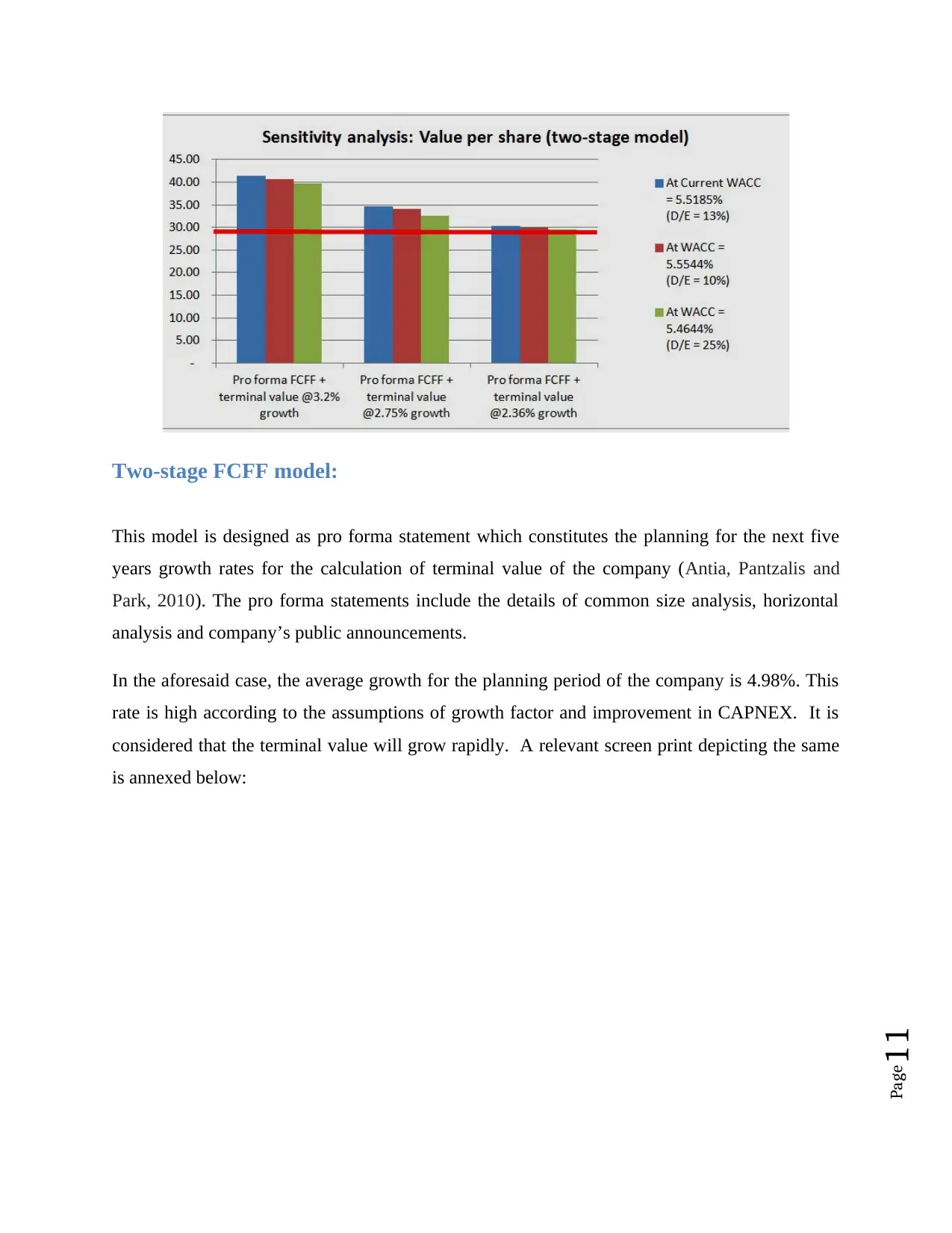

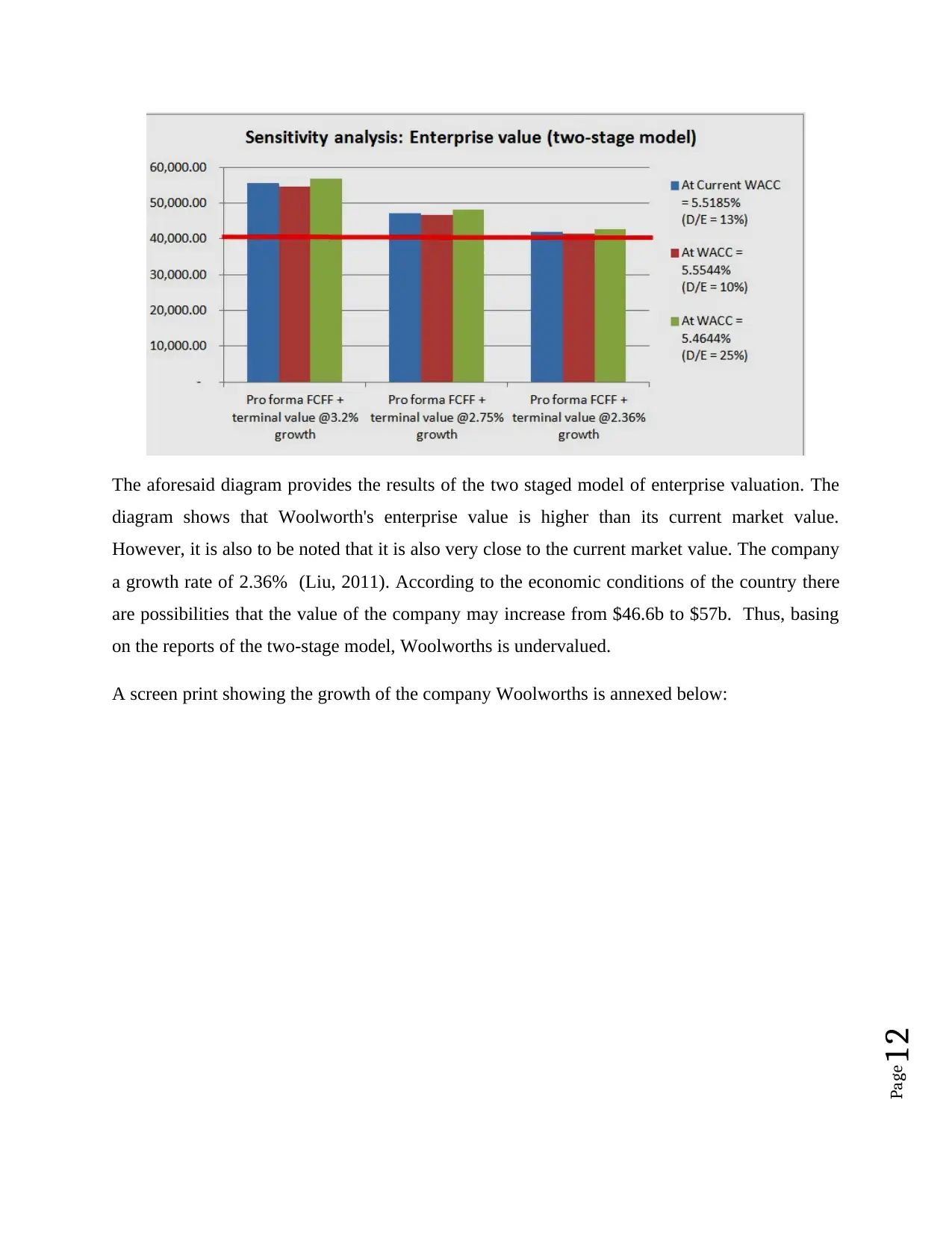

This report presents a corporate finance analysis of Woolworths Limited, a major Australian retail company. It begins with an introduction to corporate finance, followed by a case study of Woolworths, including a brief description of the company and its market analysis. The report examines the company's financial performance, including revenue, net income, and key financial ratios. It then delves into an industry overview, discussing challenges faced by Woolworths, such as market dominance and the rise of online retail. The core of the analysis involves WACC calculations, using the Fama-French model and Covariance/Variance method, and enterprise valuation using the constant free cash flows to firm (FCFF) method and a two-stage FCFF model. The report concludes with a summary of findings, suggesting that the company's capital structure and valuation models indicate potential investment opportunities. The report references various academic journals and online resources to support its analysis, providing a comprehensive overview of Woolworths' financial standing and future prospects.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.