Analysis of Woolworths' Financial Performance and Board Composition

VerifiedAdded on 2021/06/18

|15

|1757

|388

Report

AI Summary

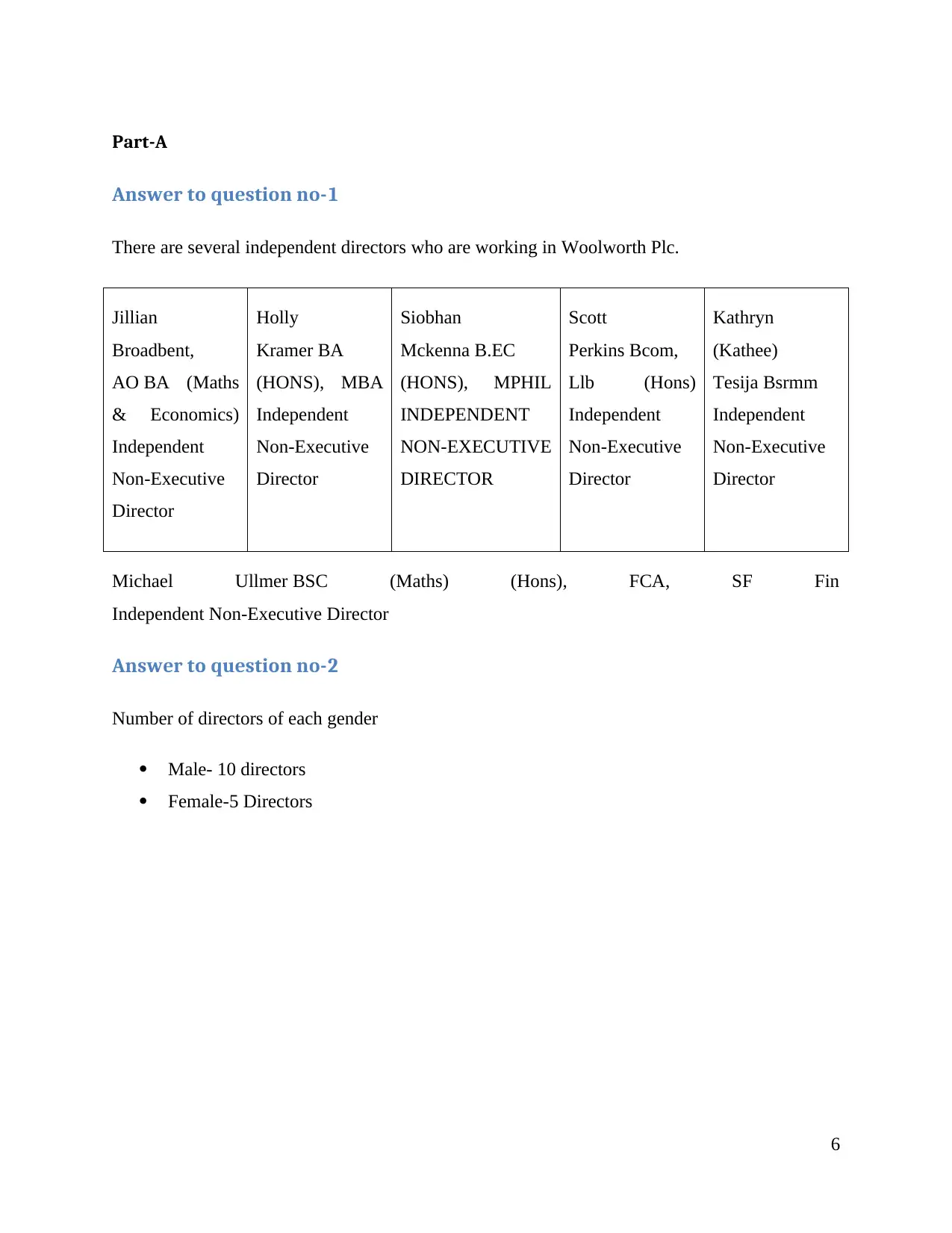

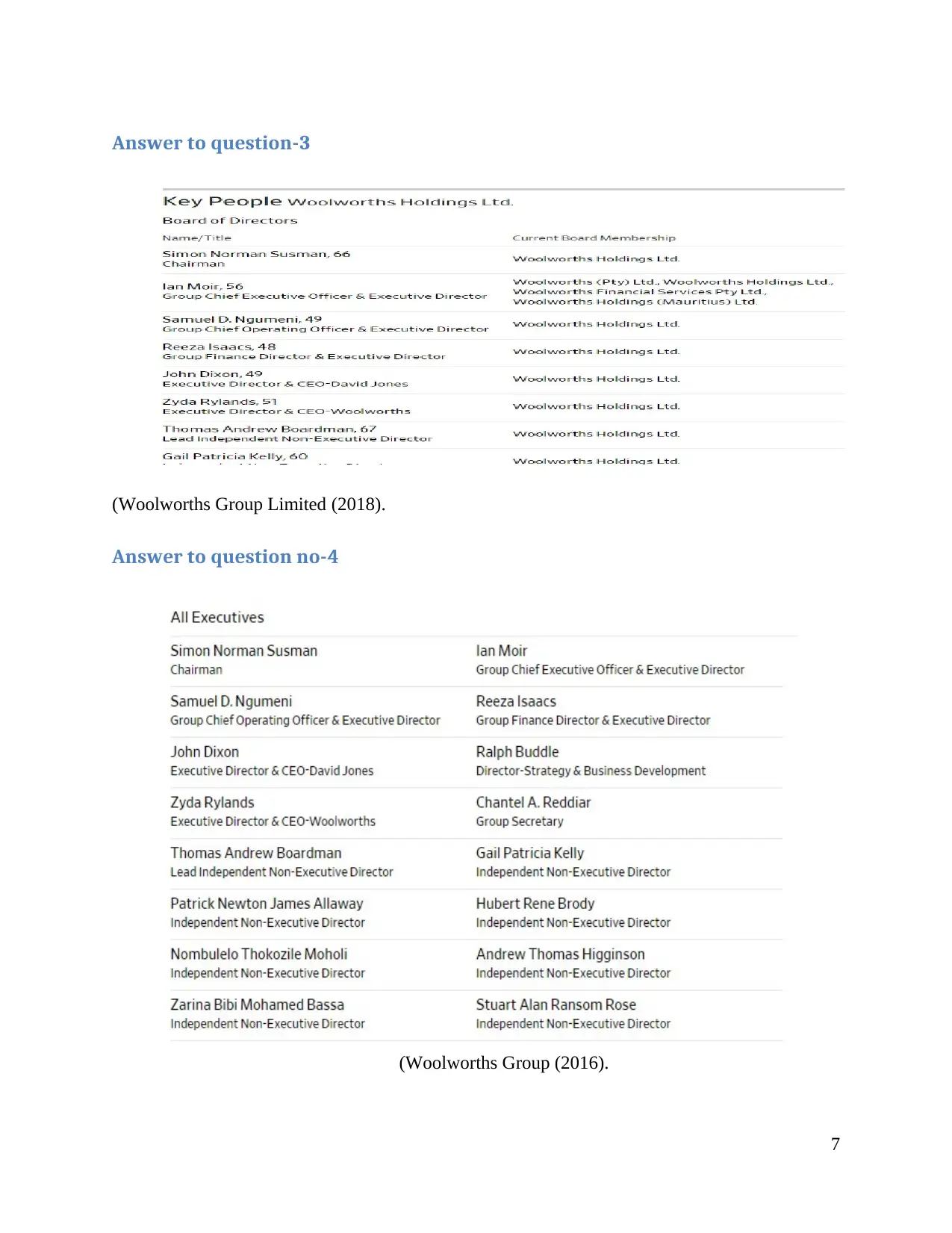

This report presents a comprehensive financial analysis of Woolworths, examining its business operations, board composition, and financial performance. The report is divided into two main parts. Part A focuses on the independent directors, gender distribution, and key financial data points such as borrowing costs and interest rates. Part B delves into the company's profitability, dividend payments, growth opportunities, and challenges, analyzing financial ratios like the net profit ratio and gross profit ratio. The analysis also includes an income statement for Orion Ltd, assessing revenue, expenses, and net profit. The report further discusses the prime users of consolidated financial statements and the implications of non-controlling interest, and also the impact of debt on financial leverage. The conclusion summarizes key findings and emphasizes the importance of regulatory compliance for long-term business stability, referencing various financial and auditing standards and reports.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.