Comprehensive Auditing Report: Woolworths Ltd Financial Analysis

VerifiedAdded on 2023/03/23

|20

|4370

|22

Report

AI Summary

This report provides a comprehensive auditing analysis of Woolworths Ltd, a leading supermarket chain in Australia. It begins with an introduction outlining the report's purpose: to analyze the company's business from an audit perspective. The report delves into the background and industry analysis, highlighting the competitive pressures, liquidity conditions, and regulatory risks faced by the business. It then proceeds to analyze the financial statements, examining the profit and loss statement and balance sheet, and discussing potential misstatements in key accounts like sales, cost of sales, and inventory. The report further applies the audit risk model to assess inherent, control, and detection risks. An analytical review of the business involves computation of key financial ratios. Estimation of planning materiality is also discussed, followed by an examination of audit assertions and planning for various accounts, including cash, inventory, and sales. The report concludes with a discussion of audit work steps and sampling plans for each account, ensuring a thorough audit process. The report aims to provide a detailed overview of the auditing process and its application to a real-world business scenario.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Author’s Note

Auditing

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Background and Industry Analysis..............................................................................................2

Analysis of Financial Statement of the Business.........................................................................3

Analytical Review of the Business..............................................................................................5

Estimation of Planning Materiality..............................................................................................8

Audit Assertions and Planning........................................................................................................9

Reference.......................................................................................................................................17

AUDITING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Background and Industry Analysis..............................................................................................2

Analysis of Financial Statement of the Business.........................................................................3

Analytical Review of the Business..............................................................................................5

Estimation of Planning Materiality..............................................................................................8

Audit Assertions and Planning........................................................................................................9

Reference.......................................................................................................................................17

2

AUDITING

Introduction

The main purpose of the assessment is to analyse the business of Woolworths Ltd which

is engaged in the business of providing different varieties of products in Australia. Woolworths

ltd operates supermarket business in Australia. The assessment would be analysing different

risks which is faced by the business from the perspective of audit. The assessment would be

computing appropriate financial ratios which can show the performance of the business over the

past three years. The assessment would be discussing the materiality of different items which are

presented in the financial statements of the business (Woolworthsgroup.com.au. 2019). In

addition to this, the report would be identifying ten accounts which can be affected by material

misstatement and also provide necessary assertion regarding the same. The assessment would

also be covering a sampling plan for testing each of the accounts which are identified from the

financial statements.

Discussion

Background and Industry Analysis

The company which is selected for this assessment is Woolworths ltd which operates in

chain of supermarket and the same is considered to be the leading supermarket of Australia. As

per the recent market conditions, the supermarket industry is at its growth phase which is evident

from the number of customers which Woolworths is serving on a r weekly basis. The annual

report of the company shows that the business is serving around 29 million customers on a

weekly basis on an average. This shows that the industry is growing one and it is anticipated to

grow even more in future years. The annual report further shows that the earnings of the business

AUDITING

Introduction

The main purpose of the assessment is to analyse the business of Woolworths Ltd which

is engaged in the business of providing different varieties of products in Australia. Woolworths

ltd operates supermarket business in Australia. The assessment would be analysing different

risks which is faced by the business from the perspective of audit. The assessment would be

computing appropriate financial ratios which can show the performance of the business over the

past three years. The assessment would be discussing the materiality of different items which are

presented in the financial statements of the business (Woolworthsgroup.com.au. 2019). In

addition to this, the report would be identifying ten accounts which can be affected by material

misstatement and also provide necessary assertion regarding the same. The assessment would

also be covering a sampling plan for testing each of the accounts which are identified from the

financial statements.

Discussion

Background and Industry Analysis

The company which is selected for this assessment is Woolworths ltd which operates in

chain of supermarket and the same is considered to be the leading supermarket of Australia. As

per the recent market conditions, the supermarket industry is at its growth phase which is evident

from the number of customers which Woolworths is serving on a r weekly basis. The annual

report of the company shows that the business is serving around 29 million customers on a

weekly basis on an average. This shows that the industry is growing one and it is anticipated to

grow even more in future years. The annual report further shows that the earnings of the business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING

has grown by 9.5% in 2018 in comparison to previous year. The management of the company

anticipates that the business would be achieving sales at a higher rate in future.

The different types of risks which are faced by the business are listed below:

Competitive Pressure: The industry of supermarket is competitive in nature as

Woolworth ltd has a close competitor Coles Group which is also performing

appropriately which makes the market divided. This affect the revenue which is

generated by the company and also has an affect on the profitability of the business.

Liquidity Conditions: This is another major risk which is faced by the business which

relates to the inability of the business to collect necessary funds from the market so as

finance different projects. The nature of the business demands that an appropriate portion

of liquid cash needs to maintained at all times so that any current obligations of the

business can be met effectively.

Regulation and Government Regulations: The business also faces risks which is

associated with change in regulations of the business. In many cases, the business enters

into tie up agreements with other organization. A change in regulations of the business

would affect such tie up agreement with the business.

Analysis of Financial Statement of the Business

The financial reports of the business for the period 2018 is considered for the purpose of

analysis whether the estimates which are presented in the financial statement are showing true

and fair view or not. The profit and loss statement show that the profits of the business have

slightly increased in comparison to previous year which may be due to increase in the sales

revenue of the business or reduction in costs. However, the financial statement of the business

shows an increase in the both the sales figure and costs of sales. In such a case, the auditor of the

AUDITING

has grown by 9.5% in 2018 in comparison to previous year. The management of the company

anticipates that the business would be achieving sales at a higher rate in future.

The different types of risks which are faced by the business are listed below:

Competitive Pressure: The industry of supermarket is competitive in nature as

Woolworth ltd has a close competitor Coles Group which is also performing

appropriately which makes the market divided. This affect the revenue which is

generated by the company and also has an affect on the profitability of the business.

Liquidity Conditions: This is another major risk which is faced by the business which

relates to the inability of the business to collect necessary funds from the market so as

finance different projects. The nature of the business demands that an appropriate portion

of liquid cash needs to maintained at all times so that any current obligations of the

business can be met effectively.

Regulation and Government Regulations: The business also faces risks which is

associated with change in regulations of the business. In many cases, the business enters

into tie up agreements with other organization. A change in regulations of the business

would affect such tie up agreement with the business.

Analysis of Financial Statement of the Business

The financial reports of the business for the period 2018 is considered for the purpose of

analysis whether the estimates which are presented in the financial statement are showing true

and fair view or not. The profit and loss statement show that the profits of the business have

slightly increased in comparison to previous year which may be due to increase in the sales

revenue of the business or reduction in costs. However, the financial statement of the business

shows an increase in the both the sales figure and costs of sales. In such a case, the auditor of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING

business needs to be careful as there is a high chance that either or both sales and costs of sales

might be misstated. This would create a risk of material misstatement which would affect the

accuracy of the financial statements. In the balance sheet of the company, there has been

significant decrease in the borrowings of the business which indicates that the management of

the company has repaid a part of the loan of the business (Kumar and Sharma 2015). However,

the auditor needs to check in order to confirm there are no discrepancies in the situation. In

addition to this, the figure of inventory shows significant rise in comparison to previous year

estimate which needs to be assessed by the auditor as there might be a material misstatement in

the financial records of the business.

The risks which are faced by the business are classified as inherent risks and control risks

of a business. The inherent risks of the business are those risks which takes place due to a

material misstatement or omission which is not caused due to the fault of the internal control

system. On the other hand, control risks occur when the internal control which is established has

some weakness. In the case of Woolworths company, there might be inherent risks as well as

control risks which the auditor needs to considering while undertaking the audit process

(Wow2017ar.qreports.com.au 2019). In order to assess the control risks, detection risks and

inherent risks, audit risk model can be applied by the management of the company. The audit

risk model which is followed by the business applies the following formula which explains the

relationship between audit risks of a business and inherent risks, control risks and detection risks

of the business (Toy and Hay 2014). The audit risk model uses the following formula which

establishes the relationship between control risks, detection risks and inherent risks of a business.

AR=DR × CR× IR

AR – Audit Risks

AUDITING

business needs to be careful as there is a high chance that either or both sales and costs of sales

might be misstated. This would create a risk of material misstatement which would affect the

accuracy of the financial statements. In the balance sheet of the company, there has been

significant decrease in the borrowings of the business which indicates that the management of

the company has repaid a part of the loan of the business (Kumar and Sharma 2015). However,

the auditor needs to check in order to confirm there are no discrepancies in the situation. In

addition to this, the figure of inventory shows significant rise in comparison to previous year

estimate which needs to be assessed by the auditor as there might be a material misstatement in

the financial records of the business.

The risks which are faced by the business are classified as inherent risks and control risks

of a business. The inherent risks of the business are those risks which takes place due to a

material misstatement or omission which is not caused due to the fault of the internal control

system. On the other hand, control risks occur when the internal control which is established has

some weakness. In the case of Woolworths company, there might be inherent risks as well as

control risks which the auditor needs to considering while undertaking the audit process

(Wow2017ar.qreports.com.au 2019). In order to assess the control risks, detection risks and

inherent risks, audit risk model can be applied by the management of the company. The audit

risk model which is followed by the business applies the following formula which explains the

relationship between audit risks of a business and inherent risks, control risks and detection risks

of the business (Toy and Hay 2014). The audit risk model uses the following formula which

establishes the relationship between control risks, detection risks and inherent risks of a business.

AR=DR × CR× IR

AR – Audit Risks

5

AUDITING

DR – Detection Risks

CR – Control Risks

IR- Inherent Risks

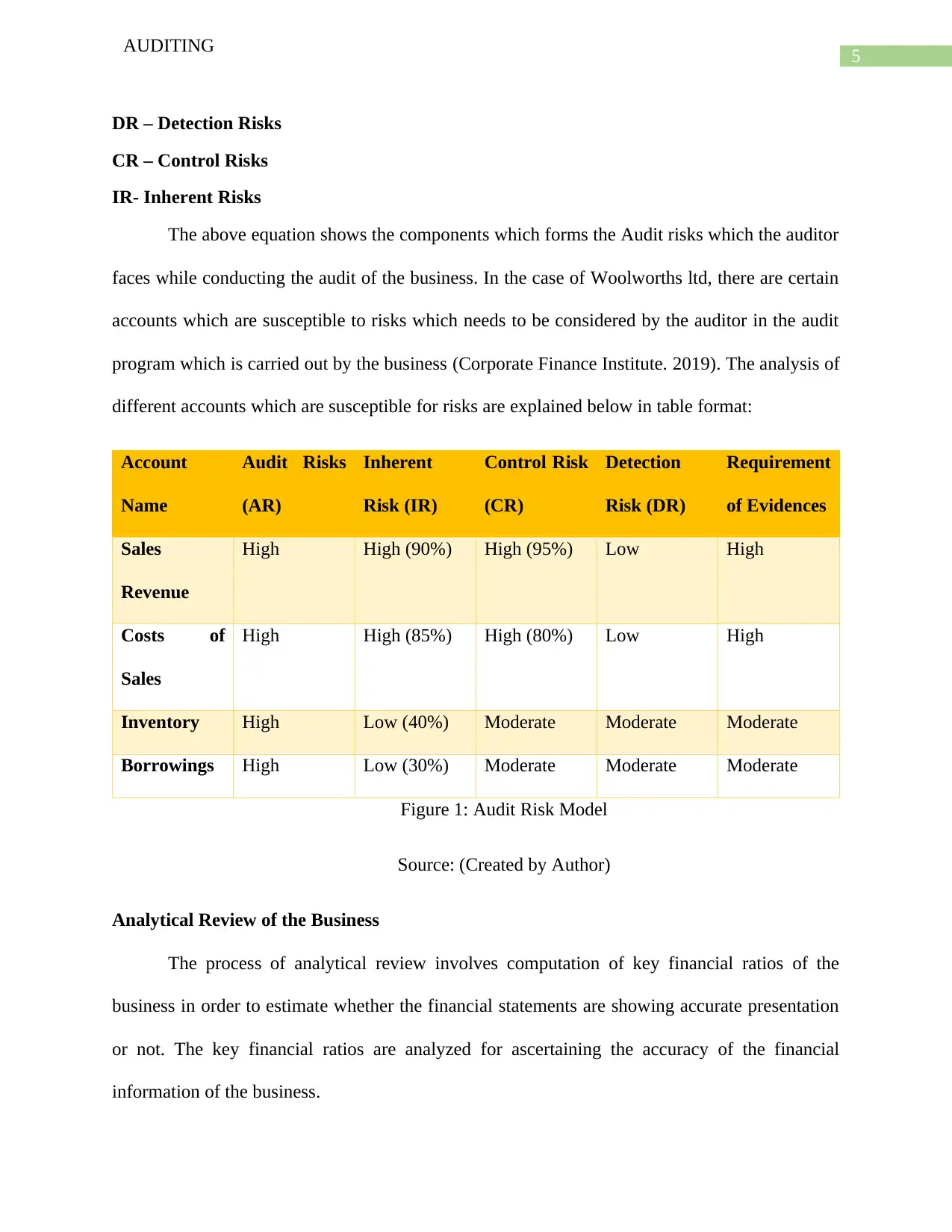

The above equation shows the components which forms the Audit risks which the auditor

faces while conducting the audit of the business. In the case of Woolworths ltd, there are certain

accounts which are susceptible to risks which needs to be considered by the auditor in the audit

program which is carried out by the business (Corporate Finance Institute. 2019). The analysis of

different accounts which are susceptible for risks are explained below in table format:

Account

Name

Audit Risks

(AR)

Inherent

Risk (IR)

Control Risk

(CR)

Detection

Risk (DR)

Requirement

of Evidences

Sales

Revenue

High High (90%) High (95%) Low High

Costs of

Sales

High High (85%) High (80%) Low High

Inventory High Low (40%) Moderate Moderate Moderate

Borrowings High Low (30%) Moderate Moderate Moderate

Figure 1: Audit Risk Model

Source: (Created by Author)

Analytical Review of the Business

The process of analytical review involves computation of key financial ratios of the

business in order to estimate whether the financial statements are showing accurate presentation

or not. The key financial ratios are analyzed for ascertaining the accuracy of the financial

information of the business.

AUDITING

DR – Detection Risks

CR – Control Risks

IR- Inherent Risks

The above equation shows the components which forms the Audit risks which the auditor

faces while conducting the audit of the business. In the case of Woolworths ltd, there are certain

accounts which are susceptible to risks which needs to be considered by the auditor in the audit

program which is carried out by the business (Corporate Finance Institute. 2019). The analysis of

different accounts which are susceptible for risks are explained below in table format:

Account

Name

Audit Risks

(AR)

Inherent

Risk (IR)

Control Risk

(CR)

Detection

Risk (DR)

Requirement

of Evidences

Sales

Revenue

High High (90%) High (95%) Low High

Costs of

Sales

High High (85%) High (80%) Low High

Inventory High Low (40%) Moderate Moderate Moderate

Borrowings High Low (30%) Moderate Moderate Moderate

Figure 1: Audit Risk Model

Source: (Created by Author)

Analytical Review of the Business

The process of analytical review involves computation of key financial ratios of the

business in order to estimate whether the financial statements are showing accurate presentation

or not. The key financial ratios are analyzed for ascertaining the accuracy of the financial

information of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING

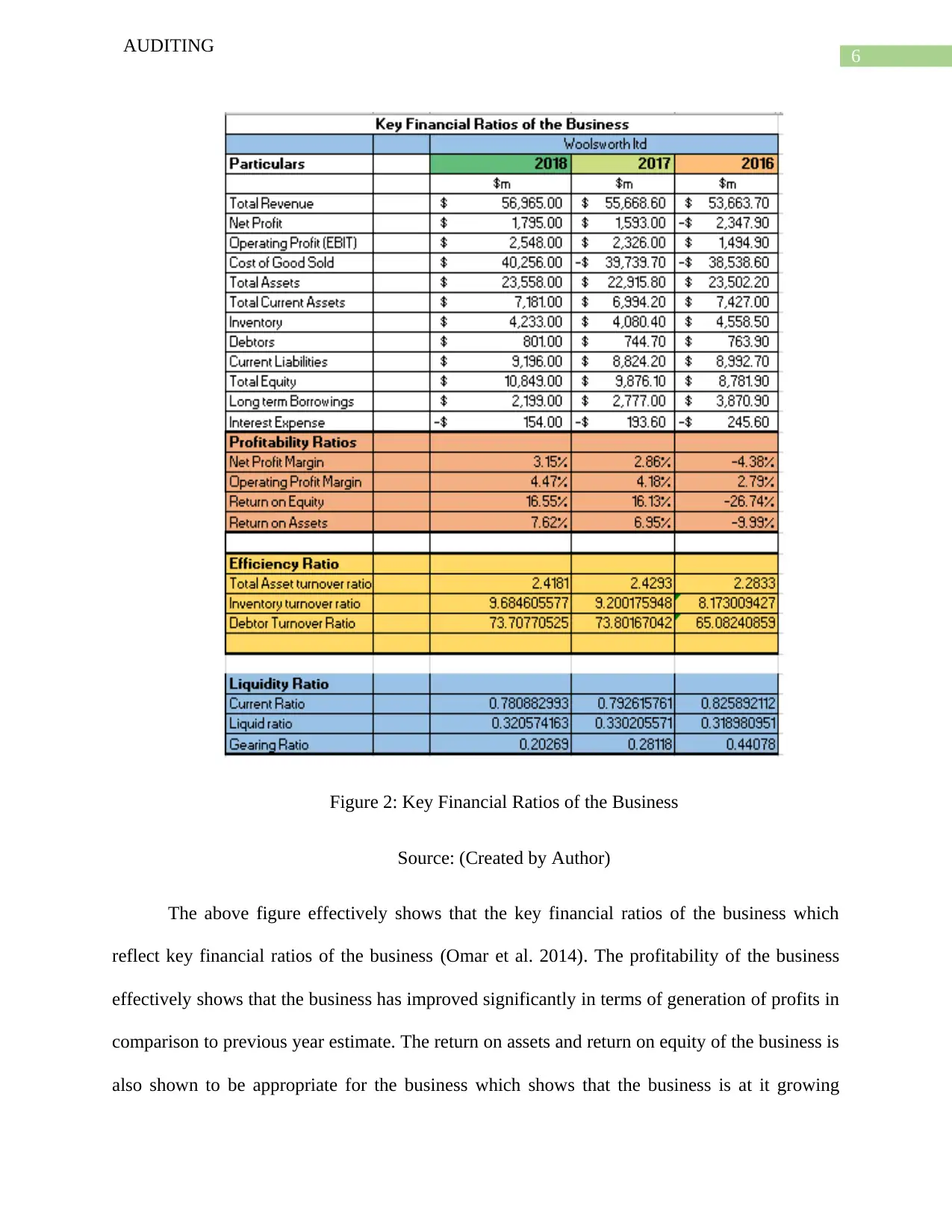

Figure 2: Key Financial Ratios of the Business

Source: (Created by Author)

The above figure effectively shows that the key financial ratios of the business which

reflect key financial ratios of the business (Omar et al. 2014). The profitability of the business

effectively shows that the business has improved significantly in terms of generation of profits in

comparison to previous year estimate. The return on assets and return on equity of the business is

also shown to be appropriate for the business which shows that the business is at it growing

AUDITING

Figure 2: Key Financial Ratios of the Business

Source: (Created by Author)

The above figure effectively shows that the key financial ratios of the business which

reflect key financial ratios of the business (Omar et al. 2014). The profitability of the business

effectively shows that the business has improved significantly in terms of generation of profits in

comparison to previous year estimate. The return on assets and return on equity of the business is

also shown to be appropriate for the business which shows that the business is at it growing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

phase. The auditor needs to assess the net profit figure in order to ensure that the sane are

accurate. The auditor needs to apply substantive procedure for assessing the income and

expenses of the business.

The efficiency ratio of the business also shows total asset turnover ratio, inventory

turnover ratio and debtors turnover ratio. The estimates which are shown for 2018 shows an

overall decline in the estimates which means that the efficiency of the business has declined. The

inventory turnover ratio has improved slightly but the management of the company needs to take

steps to make more improvements to the same (Delen, Kuzey and Uyar 2013). The debtor policy

of the business also shows changes as the estimate which is computed above has declined in

comparison to previous year estimate. The auditor of the business needs to review the debtors

and inventory of the business appropriately so that the same are representing true and fair view

of the financial statements of the business. The auditor would be applying verification

procedures for ascertaining whether the financial statement is showing appropriate view of the

financial position of the business (Sin, Moroney and Strydom 2015).

The liquidity ratio of the business is represented by current ratio, quick ratio and gearing

ratio. The current ratio and quick ratio of the business shows significant decline and the same is

shown to be below 1 which means that the current liabilities of the business are much more than

the current assets of the business (Babalola and Abiola 2013). The auditor of the business needs

to take appropriate steps for the purpose assessing the financial activities of the business so that

an opinion can be formed on the same. The gearing ratio of the business shows a decline which

indicates that the management of the company is trying to reduce the overall debts of the

business and ensure that a proper capital structure is maintained by the business. The auditor

AUDITING

phase. The auditor needs to assess the net profit figure in order to ensure that the sane are

accurate. The auditor needs to apply substantive procedure for assessing the income and

expenses of the business.

The efficiency ratio of the business also shows total asset turnover ratio, inventory

turnover ratio and debtors turnover ratio. The estimates which are shown for 2018 shows an

overall decline in the estimates which means that the efficiency of the business has declined. The

inventory turnover ratio has improved slightly but the management of the company needs to take

steps to make more improvements to the same (Delen, Kuzey and Uyar 2013). The debtor policy

of the business also shows changes as the estimate which is computed above has declined in

comparison to previous year estimate. The auditor of the business needs to review the debtors

and inventory of the business appropriately so that the same are representing true and fair view

of the financial statements of the business. The auditor would be applying verification

procedures for ascertaining whether the financial statement is showing appropriate view of the

financial position of the business (Sin, Moroney and Strydom 2015).

The liquidity ratio of the business is represented by current ratio, quick ratio and gearing

ratio. The current ratio and quick ratio of the business shows significant decline and the same is

shown to be below 1 which means that the current liabilities of the business are much more than

the current assets of the business (Babalola and Abiola 2013). The auditor of the business needs

to take appropriate steps for the purpose assessing the financial activities of the business so that

an opinion can be formed on the same. The gearing ratio of the business shows a decline which

indicates that the management of the company is trying to reduce the overall debts of the

business and ensure that a proper capital structure is maintained by the business. The auditor

8

AUDITING

needs to check whether the business actually pays of the loan or not and also ascertain the

amount for the same.

Estimation of Planning Materiality

The process of auditing involves estimation of materiality which is an integral part of the

audit process of the business (William Jr, Glover and Prawitt 2016). The materiality of an item is

the basis on which the auditor decides whether the item is misstated or not. The materiality of an

item represented in the financial statement is estimated on the basis of nature of the item,

recurrence of the item, complexity of the item. In other words, an item which is represented in

the financial statement would be considered to be material if misstatement of the same can affect

the financial position of the business (Eilifsen and Messier Jr 2014). As per the analysis of the

annual report of Woolworths ltd, the material items which are presented in the financial

statements are sales, cost of sales, net profit, total assets and several other items as well

depending on the nature of the business.

The auditor prior to commencing audit of a business needs to formulate an audit program

which requires computation of planning materiality on the basis of which performance

materiality is to be computed. The planning materiality computation requires the auditor to

consider a base which can be the largest figures in terms of numeric presented in the financial

statements of the business (Christensen, Glover and Wood 2013). The estimate is then multiplied

with a fixed rate of percent for computing the planning materiality of the business (Vîlsănoiu and

Buzenche 2014). In the case of Woolworths ltd, percentage which is used for computing

planning materiality is considered to be 5% while the item which is considered for the base

would be total asset figure. The computation of planning materiality is shown below:

Planning Materiality=Total Asset∗5 %

AUDITING

needs to check whether the business actually pays of the loan or not and also ascertain the

amount for the same.

Estimation of Planning Materiality

The process of auditing involves estimation of materiality which is an integral part of the

audit process of the business (William Jr, Glover and Prawitt 2016). The materiality of an item is

the basis on which the auditor decides whether the item is misstated or not. The materiality of an

item represented in the financial statement is estimated on the basis of nature of the item,

recurrence of the item, complexity of the item. In other words, an item which is represented in

the financial statement would be considered to be material if misstatement of the same can affect

the financial position of the business (Eilifsen and Messier Jr 2014). As per the analysis of the

annual report of Woolworths ltd, the material items which are presented in the financial

statements are sales, cost of sales, net profit, total assets and several other items as well

depending on the nature of the business.

The auditor prior to commencing audit of a business needs to formulate an audit program

which requires computation of planning materiality on the basis of which performance

materiality is to be computed. The planning materiality computation requires the auditor to

consider a base which can be the largest figures in terms of numeric presented in the financial

statements of the business (Christensen, Glover and Wood 2013). The estimate is then multiplied

with a fixed rate of percent for computing the planning materiality of the business (Vîlsănoiu and

Buzenche 2014). In the case of Woolworths ltd, percentage which is used for computing

planning materiality is considered to be 5% while the item which is considered for the base

would be total asset figure. The computation of planning materiality is shown below:

Planning Materiality=Total Asset∗5 %

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING

¿ $ 23,558∗5 %

¿ $ 1,177.9 million

The above equation shows computation of planning materiality of the business and the

same is shown to be $ 1,179.9 million which is computed considering the total assets as the base.

The materiality estimate would help the auditor to compute performance materiality of different

items which can then be used for identifying the material misstatement in the annual report of the

business.

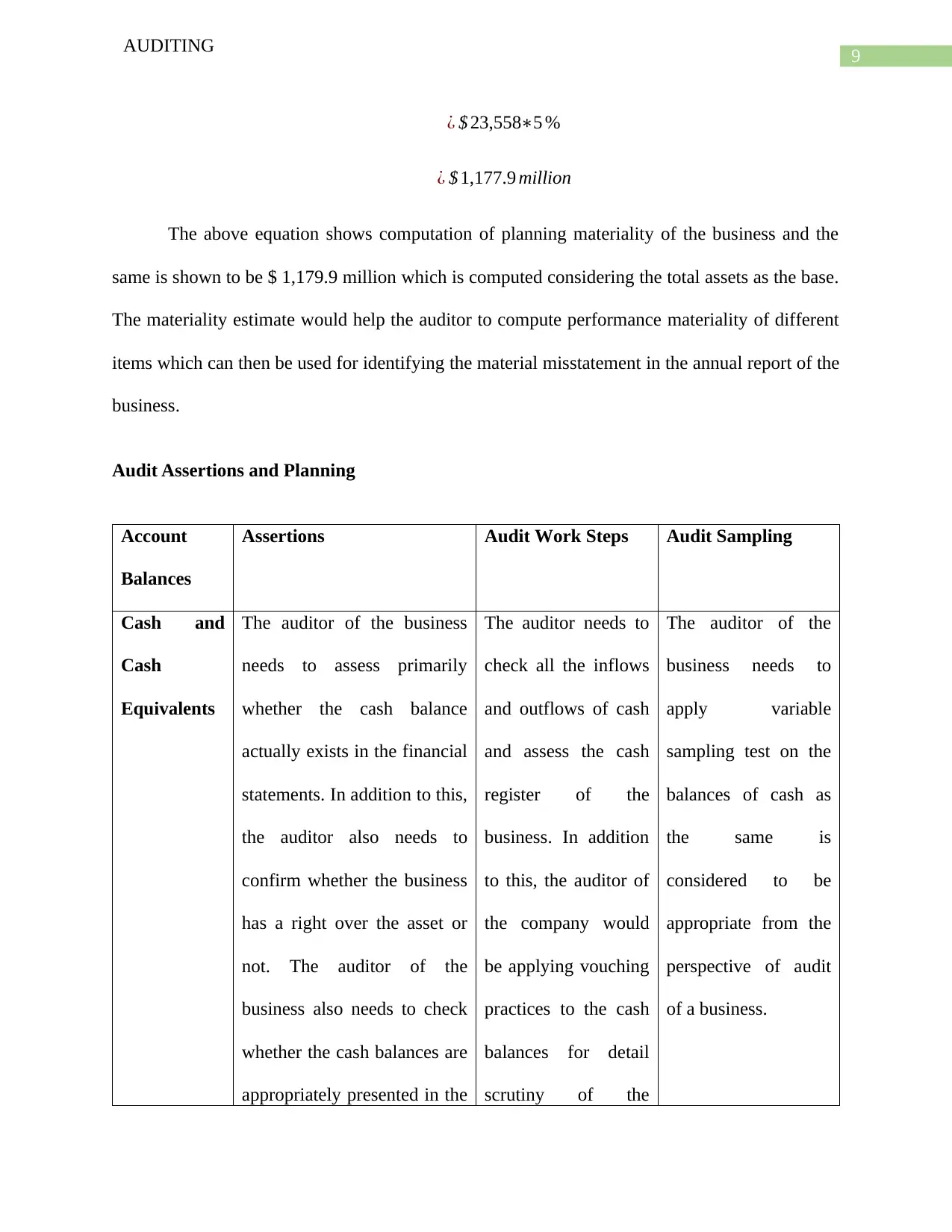

Audit Assertions and Planning

Account

Balances

Assertions Audit Work Steps Audit Sampling

Cash and

Cash

Equivalents

The auditor of the business

needs to assess primarily

whether the cash balance

actually exists in the financial

statements. In addition to this,

the auditor also needs to

confirm whether the business

has a right over the asset or

not. The auditor of the

business also needs to check

whether the cash balances are

appropriately presented in the

The auditor needs to

check all the inflows

and outflows of cash

and assess the cash

register of the

business. In addition

to this, the auditor of

the company would

be applying vouching

practices to the cash

balances for detail

scrutiny of the

The auditor of the

business needs to

apply variable

sampling test on the

balances of cash as

the same is

considered to be

appropriate from the

perspective of audit

of a business.

AUDITING

¿ $ 23,558∗5 %

¿ $ 1,177.9 million

The above equation shows computation of planning materiality of the business and the

same is shown to be $ 1,179.9 million which is computed considering the total assets as the base.

The materiality estimate would help the auditor to compute performance materiality of different

items which can then be used for identifying the material misstatement in the annual report of the

business.

Audit Assertions and Planning

Account

Balances

Assertions Audit Work Steps Audit Sampling

Cash and

Cash

Equivalents

The auditor of the business

needs to assess primarily

whether the cash balance

actually exists in the financial

statements. In addition to this,

the auditor also needs to

confirm whether the business

has a right over the asset or

not. The auditor of the

business also needs to check

whether the cash balances are

appropriately presented in the

The auditor needs to

check all the inflows

and outflows of cash

and assess the cash

register of the

business. In addition

to this, the auditor of

the company would

be applying vouching

practices to the cash

balances for detail

scrutiny of the

The auditor of the

business needs to

apply variable

sampling test on the

balances of cash as

the same is

considered to be

appropriate from the

perspective of audit

of a business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING

financial statements of the

business.

transaction and

ensuring the same are

not misstated in any

manner.

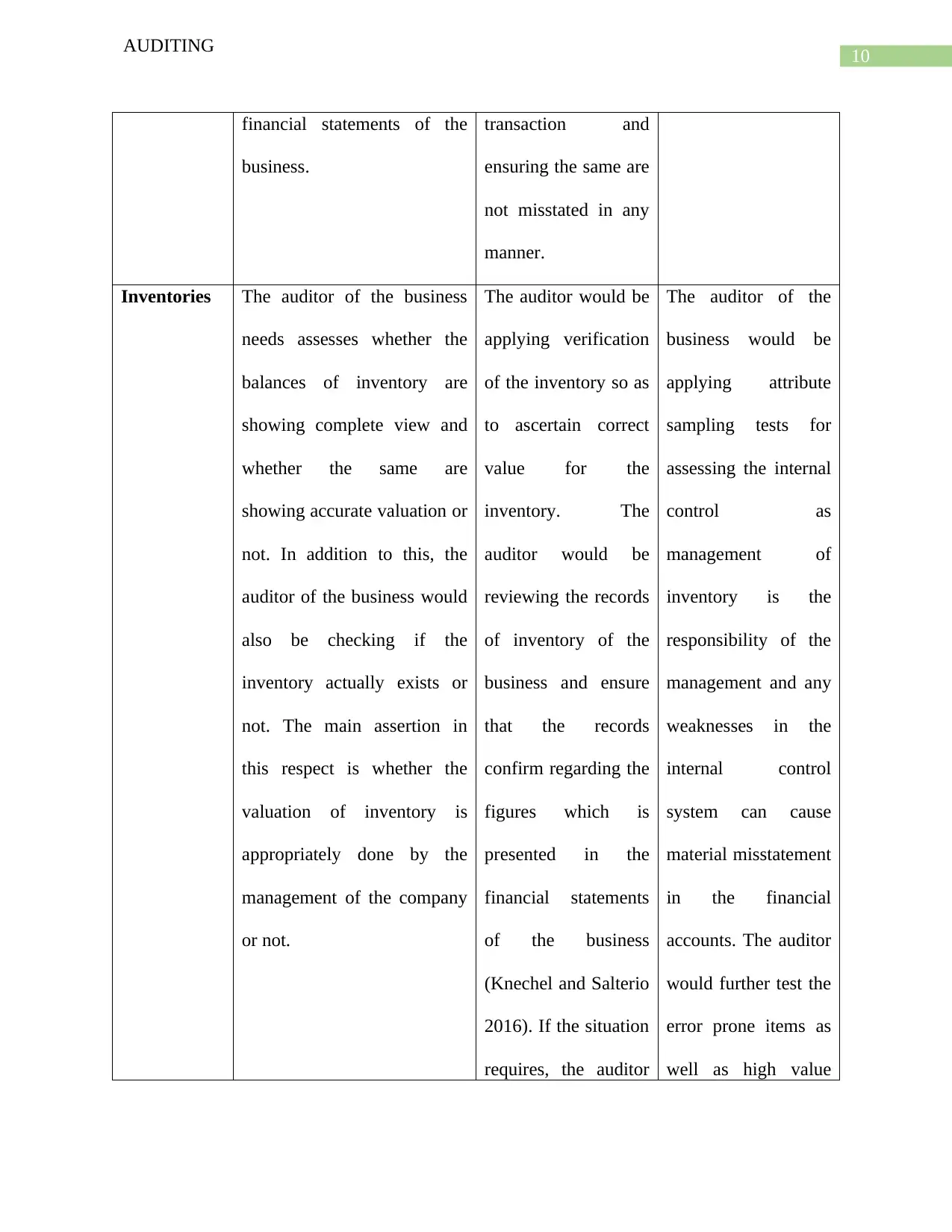

Inventories The auditor of the business

needs assesses whether the

balances of inventory are

showing complete view and

whether the same are

showing accurate valuation or

not. In addition to this, the

auditor of the business would

also be checking if the

inventory actually exists or

not. The main assertion in

this respect is whether the

valuation of inventory is

appropriately done by the

management of the company

or not.

The auditor would be

applying verification

of the inventory so as

to ascertain correct

value for the

inventory. The

auditor would be

reviewing the records

of inventory of the

business and ensure

that the records

confirm regarding the

figures which is

presented in the

financial statements

of the business

(Knechel and Salterio

2016). If the situation

requires, the auditor

The auditor of the

business would be

applying attribute

sampling tests for

assessing the internal

control as

management of

inventory is the

responsibility of the

management and any

weaknesses in the

internal control

system can cause

material misstatement

in the financial

accounts. The auditor

would further test the

error prone items as

well as high value

AUDITING

financial statements of the

business.

transaction and

ensuring the same are

not misstated in any

manner.

Inventories The auditor of the business

needs assesses whether the

balances of inventory are

showing complete view and

whether the same are

showing accurate valuation or

not. In addition to this, the

auditor of the business would

also be checking if the

inventory actually exists or

not. The main assertion in

this respect is whether the

valuation of inventory is

appropriately done by the

management of the company

or not.

The auditor would be

applying verification

of the inventory so as

to ascertain correct

value for the

inventory. The

auditor would be

reviewing the records

of inventory of the

business and ensure

that the records

confirm regarding the

figures which is

presented in the

financial statements

of the business

(Knechel and Salterio

2016). If the situation

requires, the auditor

The auditor of the

business would be

applying attribute

sampling tests for

assessing the internal

control as

management of

inventory is the

responsibility of the

management and any

weaknesses in the

internal control

system can cause

material misstatement

in the financial

accounts. The auditor

would further test the

error prone items as

well as high value

11

AUDITING

can also engage in

physical stock count

so that appropriate

valuation can be done

for the asset.

items of inventory

which contains

maximum

misstatements. The

auditor would also

assess inventory

which are in transit

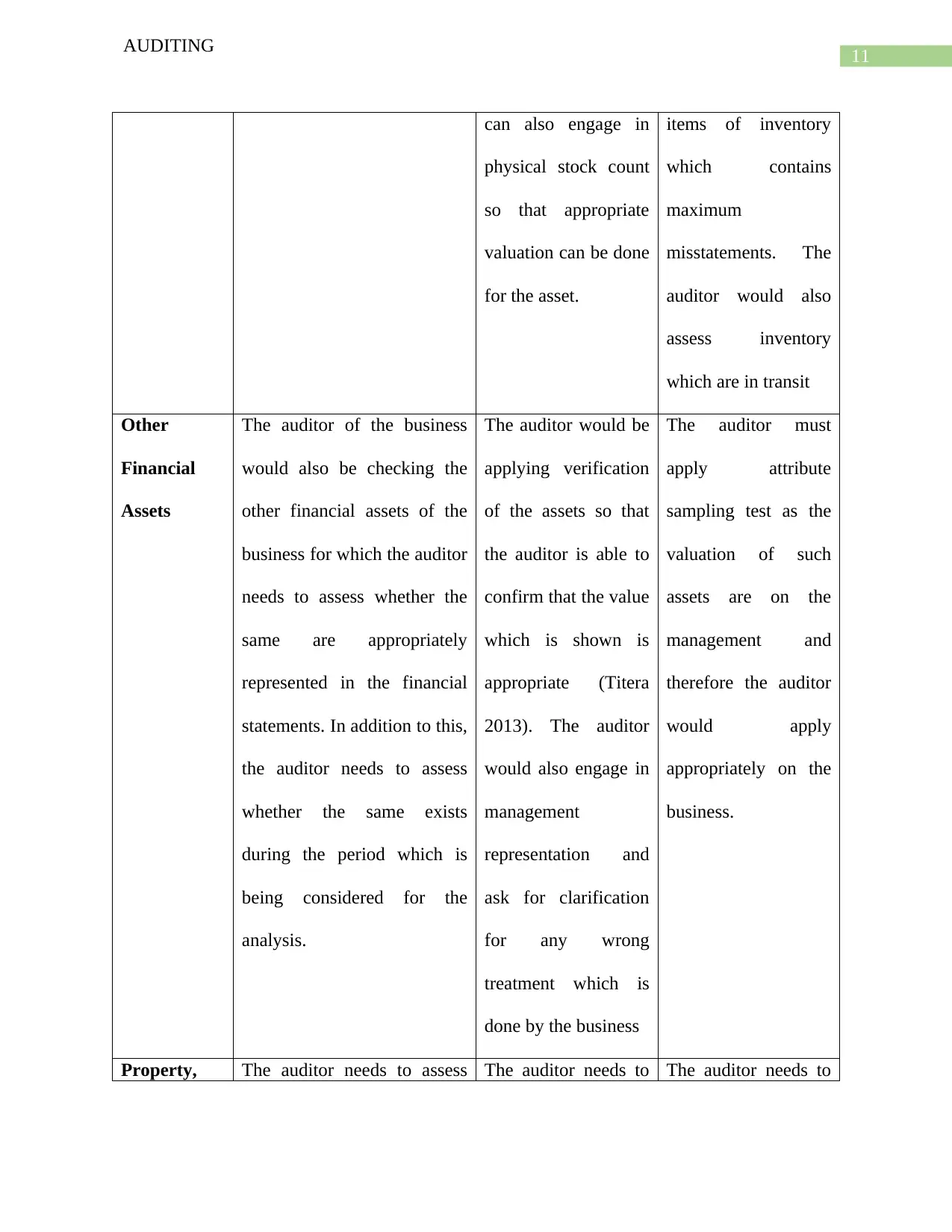

Other

Financial

Assets

The auditor of the business

would also be checking the

other financial assets of the

business for which the auditor

needs to assess whether the

same are appropriately

represented in the financial

statements. In addition to this,

the auditor needs to assess

whether the same exists

during the period which is

being considered for the

analysis.

The auditor would be

applying verification

of the assets so that

the auditor is able to

confirm that the value

which is shown is

appropriate (Titera

2013). The auditor

would also engage in

management

representation and

ask for clarification

for any wrong

treatment which is

done by the business

The auditor must

apply attribute

sampling test as the

valuation of such

assets are on the

management and

therefore the auditor

would apply

appropriately on the

business.

Property, The auditor needs to assess The auditor needs to The auditor needs to

AUDITING

can also engage in

physical stock count

so that appropriate

valuation can be done

for the asset.

items of inventory

which contains

maximum

misstatements. The

auditor would also

assess inventory

which are in transit

Other

Financial

Assets

The auditor of the business

would also be checking the

other financial assets of the

business for which the auditor

needs to assess whether the

same are appropriately

represented in the financial

statements. In addition to this,

the auditor needs to assess

whether the same exists

during the period which is

being considered for the

analysis.

The auditor would be

applying verification

of the assets so that

the auditor is able to

confirm that the value

which is shown is

appropriate (Titera

2013). The auditor

would also engage in

management

representation and

ask for clarification

for any wrong

treatment which is

done by the business

The auditor must

apply attribute

sampling test as the

valuation of such

assets are on the

management and

therefore the auditor

would apply

appropriately on the

business.

Property, The auditor needs to assess The auditor needs to The auditor needs to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.