Financial Instrument Analysis Report - Woolworths Case Study

VerifiedAdded on 2022/11/13

|9

|646

|180

Report

AI Summary

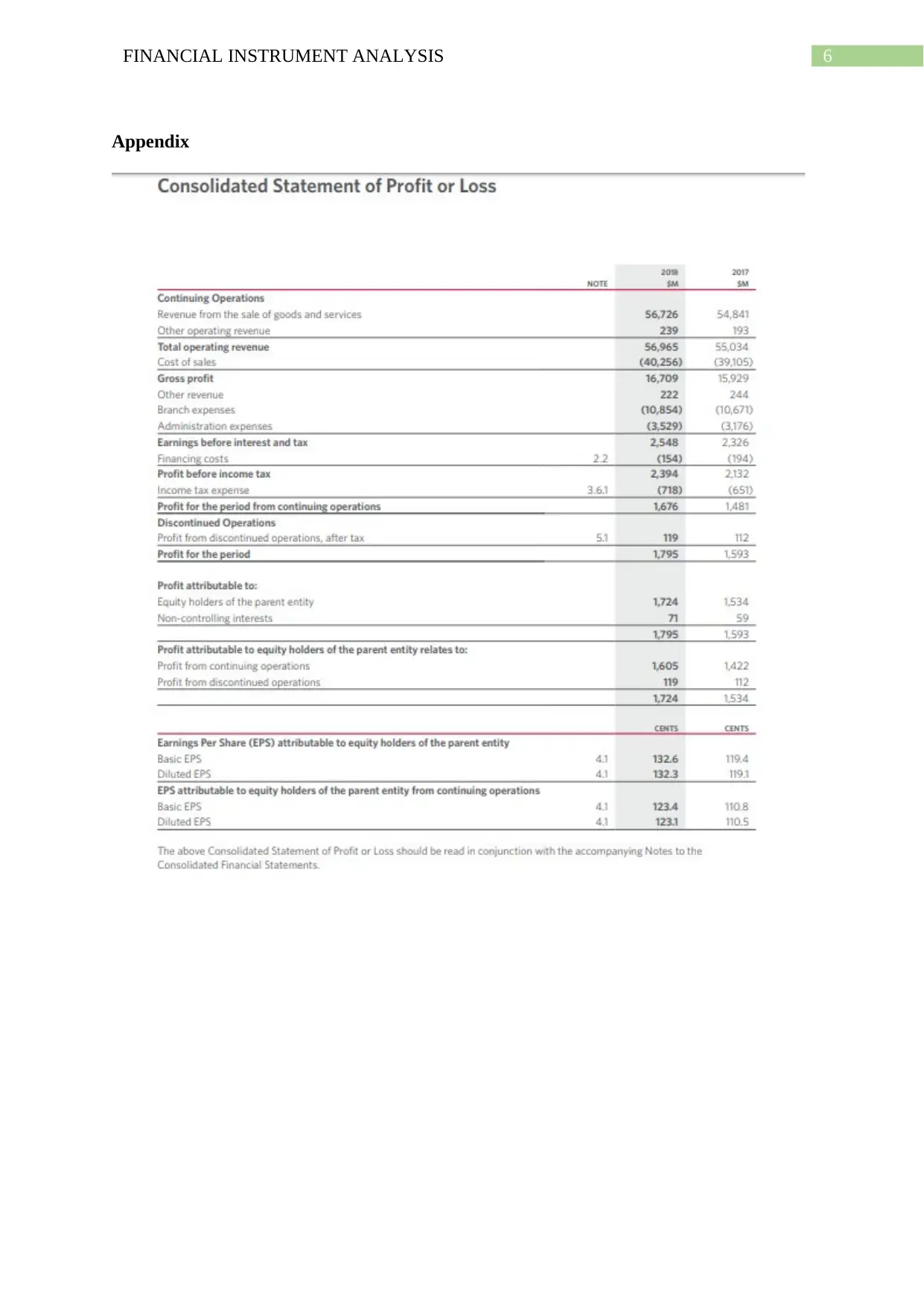

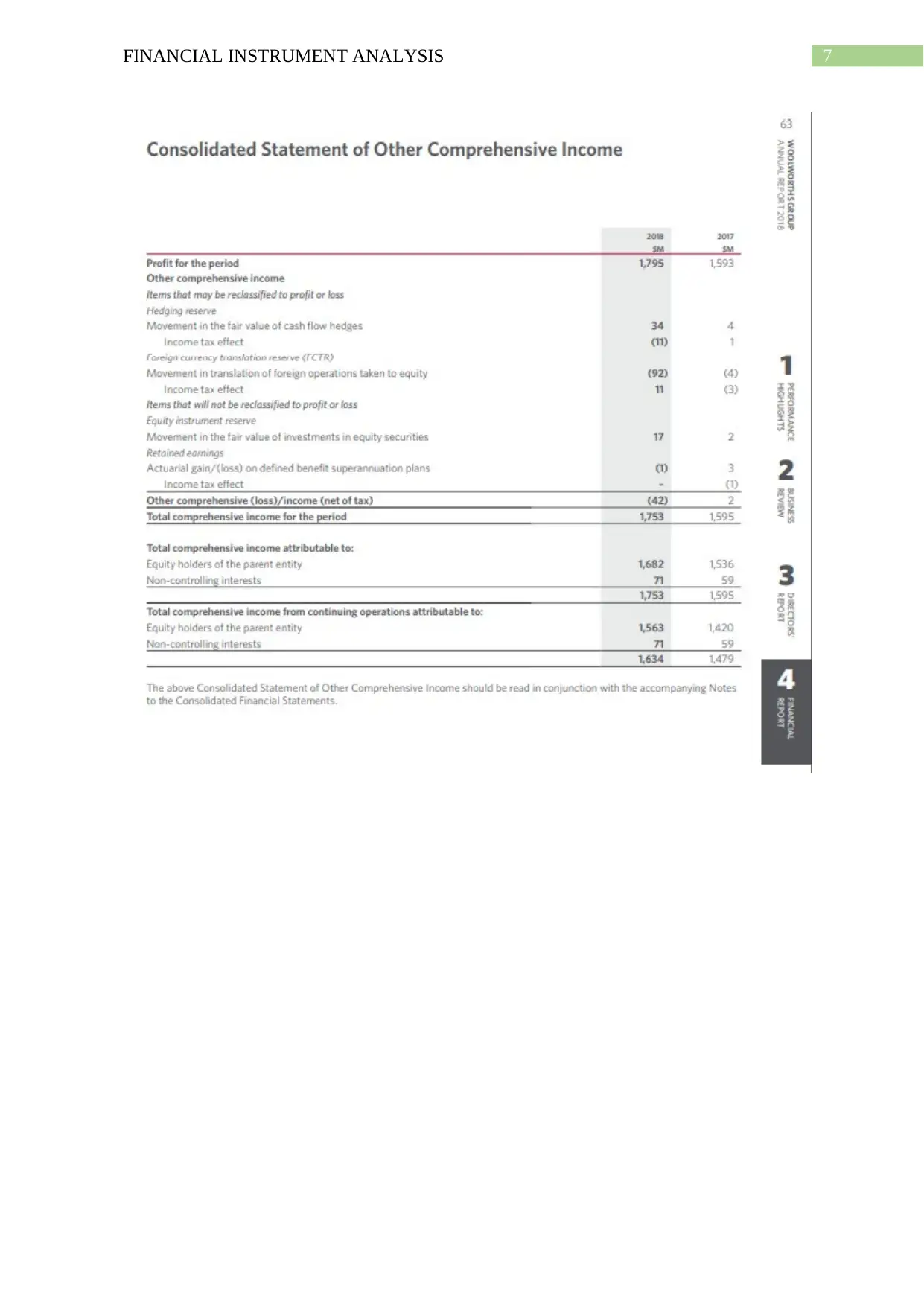

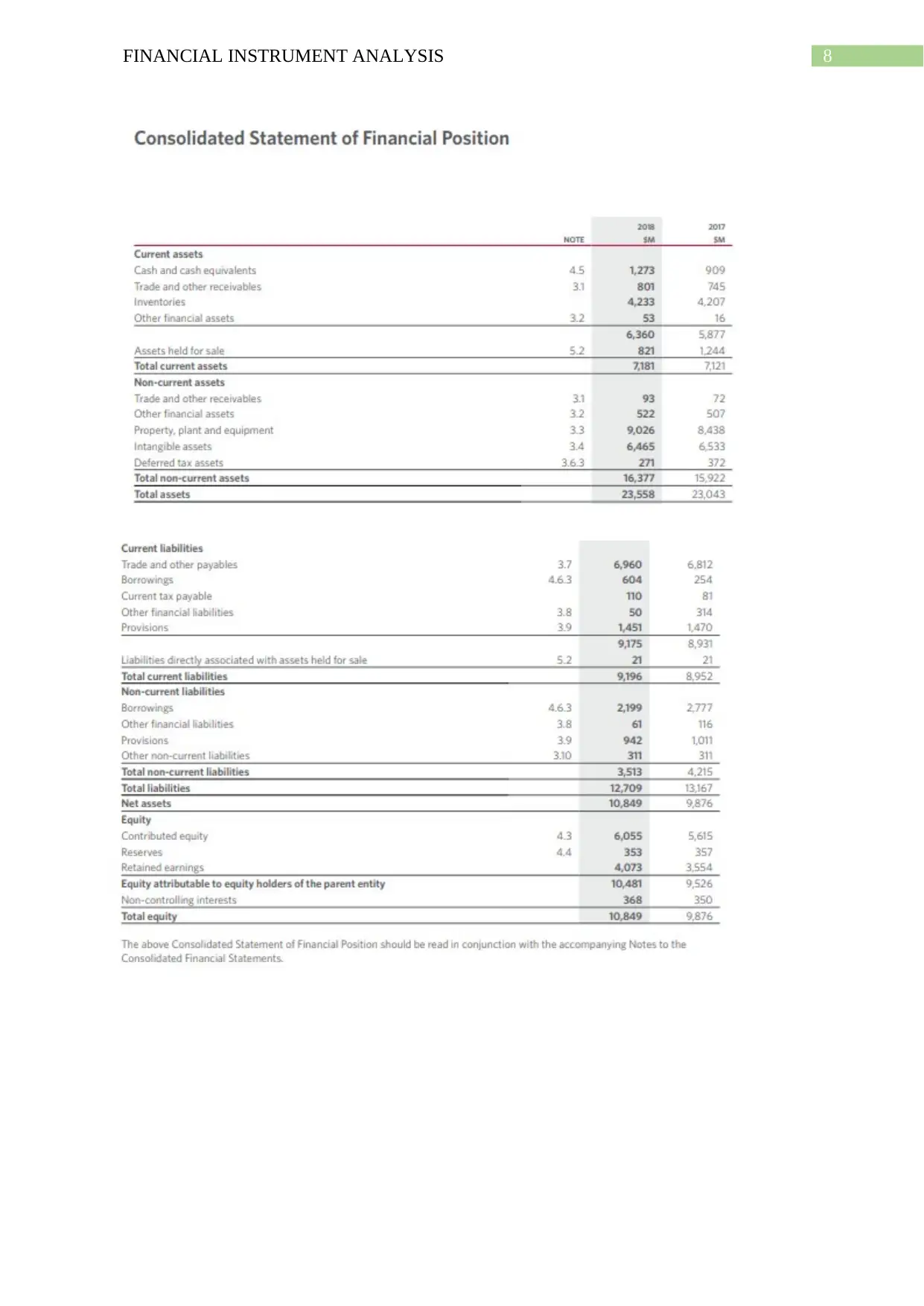

This report provides a detailed analysis of Woolworths' financial instruments. It examines the company's on-balance sheet instruments, including short-term loans, non-current borrowings, and cross-currency swaps, and how they are used. The analysis also covers the company's hedging strategies, including the use of cross-currency swaps, interest rate swaps, and foreign exchange contracts to manage risks associated with foreign exchange rates and interest rates. Furthermore, the report delves into Woolworths' off-balance sheet activities, specifically its operating lease agreements. The analysis highlights the impact of AASB 16 Leases on the company's financial statements and the recognition of right-of-use assets and lease liabilities. The report also references the 2018 Balance Sheet and Income Statements of Woolworths, attached as an exhibit, and includes a reference list of relevant sources.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.