JCU LB5230: Risk Assessment Report - Woolworths Financial Audit

VerifiedAdded on 2023/06/03

|11

|2756

|177

Report

AI Summary

This report is a comprehensive risk assessment of Woolworths Limited, prepared as part of an audit plan. It begins with an introduction outlining the context of risk management in today's business environment and a brief overview of Woolworths. The report then identifies and analyzes the significant risks faced by the company, including strategic, compliance, financial, operational, and reputational risks. It details analytical procedures used in the audit process and highlights the significant audit risks, such as going concern. The report also discusses the audit risk model, significant inherent risks (inventories, intangibles, fixed assets, and foreign exchange transactions), and control risks (corporate governance, independent directors, and the audit and risk committee). The impact of audit testing and the implications of inherent and control risks for audit planning are also addressed. The report references relevant auditing standards and concludes by emphasizing the importance of effective risk assessment in the audit process.

Running head: RISK ASSESSMENT

INDIVIDUAL TASK COVER SHEET

Student

Please sign, date and attach cover sheet to front of written assessment task OR

Submit as a separate document for non-written assessment task.

A cover sheet is to be completed for each assessment task.

SUBJECT CODE LB5230

STUDENT FAMILY NAME Student Given Name JCU Student Number

Kalra Chirag 1 3 3 0 7 3 9 6

ASSESSMENT TITLE Managing Strategic Resources and Operations

DUE DATE 27-04-2018

LECTURER NAME Dr. Max Boudan

TUTOR NAME Dwight K.Lemke

Student Declaration

1. This assignment is my original work and no part has been copied/ reproduced from any other person’s work or from any other

source, except where acknowledgement has been made (see Learning, Teaching and Assessment Policy 5.1).

2. This work has not been submitted for any other course/subject (see Learning, Teaching and Assessment Policy 5.9).

3. This assignment has not been written for me by anyone or by any organisation.

4. I hold a copy of this assignment and can produce a copy if requested.

5. This work may be used for the purposes of moderation and identifying plagiarism.

6. I give permission for a copy of this marked assignment to be retained by the College for benchmarking and course review and

accreditation purposes.

INDIVIDUAL TASK COVER SHEET

Student

Please sign, date and attach cover sheet to front of written assessment task OR

Submit as a separate document for non-written assessment task.

A cover sheet is to be completed for each assessment task.

SUBJECT CODE LB5230

STUDENT FAMILY NAME Student Given Name JCU Student Number

Kalra Chirag 1 3 3 0 7 3 9 6

ASSESSMENT TITLE Managing Strategic Resources and Operations

DUE DATE 27-04-2018

LECTURER NAME Dr. Max Boudan

TUTOR NAME Dwight K.Lemke

Student Declaration

1. This assignment is my original work and no part has been copied/ reproduced from any other person’s work or from any other

source, except where acknowledgement has been made (see Learning, Teaching and Assessment Policy 5.1).

2. This work has not been submitted for any other course/subject (see Learning, Teaching and Assessment Policy 5.9).

3. This assignment has not been written for me by anyone or by any organisation.

4. I hold a copy of this assignment and can produce a copy if requested.

5. This work may be used for the purposes of moderation and identifying plagiarism.

6. I give permission for a copy of this marked assignment to be retained by the College for benchmarking and course review and

accreditation purposes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1RISK ASSESSMENT

Learning, Teaching and Assessment Policy 5.1. A student who submits work containing plagiarised material for assessment

will be subject to the provisions of the Student Academic Misconduct Requirements.

Note definition of plagiarism and self-plagiarism in Learning, Teaching and Assessment Policy:

Plagiarism: reproduction without acknowledgement of another person’s words, work or expressed thoughts from any source. The

definition of words, works and thoughts includes such representations as diagrams, drawings, sketches, pictures, objects, text, lecture hand-

outs, artistic works and other such expressions of ideas, but hereafter the term ‘work’ is used to embrace all of these. Plagiarism comprises

not only direct copying of aspects of another person’s work but also the reproduction, even if slightly rewritten or adapted, of someone

else’s ideas. In both cases, someone else’s work is presented as the student’s own. Under the Australian Copyright Act 1968 a copyright

owner can take legal action in the courts against a party who has infringed their copyright.

Self-Plagiarism: theuse of one’s own previously assessed material being resubmitted without acknowledgement or citing of the original.

Student Signature

Chirag KalraSubmission date 27 / 04/ 2018

Learning, Teaching and Assessment Policy 5.1. A student who submits work containing plagiarised material for assessment

will be subject to the provisions of the Student Academic Misconduct Requirements.

Note definition of plagiarism and self-plagiarism in Learning, Teaching and Assessment Policy:

Plagiarism: reproduction without acknowledgement of another person’s words, work or expressed thoughts from any source. The

definition of words, works and thoughts includes such representations as diagrams, drawings, sketches, pictures, objects, text, lecture hand-

outs, artistic works and other such expressions of ideas, but hereafter the term ‘work’ is used to embrace all of these. Plagiarism comprises

not only direct copying of aspects of another person’s work but also the reproduction, even if slightly rewritten or adapted, of someone

else’s ideas. In both cases, someone else’s work is presented as the student’s own. Under the Australian Copyright Act 1968 a copyright

owner can take legal action in the courts against a party who has infringed their copyright.

Self-Plagiarism: theuse of one’s own previously assessed material being resubmitted without acknowledgement or citing of the original.

Student Signature

Chirag KalraSubmission date 27 / 04/ 2018

2RISK ASSESSMENT

Table of Contents

Introduction................................................................................................................................................3

Brief overview of the company..................................................................................................................3

The significant Risks in business...............................................................................................................4

Analytical procedures................................................................................................................................4

The significant audit risk of the organisation.............................................................................................5

Going concern............................................................................................................................................5

Audit risk model........................................................................................................................................5

Impact of audit testing................................................................................................................................7

Implications of Inherent risk and Control Risk for planning.....................................................................7

Reference...................................................................................................................................................8

Appendices.................................................................................................................................................9

Table of Contents

Introduction................................................................................................................................................3

Brief overview of the company..................................................................................................................3

The significant Risks in business...............................................................................................................4

Analytical procedures................................................................................................................................4

The significant audit risk of the organisation.............................................................................................5

Going concern............................................................................................................................................5

Audit risk model........................................................................................................................................5

Impact of audit testing................................................................................................................................7

Implications of Inherent risk and Control Risk for planning.....................................................................7

Reference...................................................................................................................................................8

Appendices.................................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3RISK ASSESSMENT

Introduction

In the recent time of fast-moving and interdependent world, the various organizations are

increasingly facing by several risks that can be in nature complex and has a worldwide consequence.

Such kinds of risks are very difficult to anticipate and deal with, even for the large business entities.

The Businesses all over have set their priorities on the basis of their own position as compared with the

related business in the market. The businesses primarily focus on the areas that the organisations expect

to have more risk in business (Hall, Mikes & Millo, 2015). However, the process may or may not be

so well structured and at times business risks are not efficiently understood or visualised. This is

because of the lack of formality and understanding of the same. There is also exists a risk of not

realising what are the greatest risks and which of them are needed to be focused upon by the particular

organisation. For improving the business decision making, the process of efficient risk management is

rapidly gaining acceptance and is aiding the organisations to manage their businesses more effectively.

Brief overview of the company

Woolworths is the largest Australian shopping that deals with food products and beverages in

Australia and New Zeeland. The company has also diversified its offerings by investing in gaming

poker. Woolworth’s financial goals, budget policies, and business policies are at the center of the

management. The company has succeeded in implementing its business policies and key performance

indicators by building a strong team of staff. The company has invested heavily in improving safety

governance to improve safety of staff (Born & Pfeifer, 2014). The main competitor of the organization

is Wesfarmers which is the largest retail industry firm in the current market.

The company of Woolworths Limited has been committed to the various ongoing strategic

developments and uses a consistent enterprise-wide approach for the management of risk by a culture

that is risk-aware. The risk management Policy applies to all the indivituals who works for Woolworths

Limited in, New Zealand, Australia and abroad.

Introduction

In the recent time of fast-moving and interdependent world, the various organizations are

increasingly facing by several risks that can be in nature complex and has a worldwide consequence.

Such kinds of risks are very difficult to anticipate and deal with, even for the large business entities.

The Businesses all over have set their priorities on the basis of their own position as compared with the

related business in the market. The businesses primarily focus on the areas that the organisations expect

to have more risk in business (Hall, Mikes & Millo, 2015). However, the process may or may not be

so well structured and at times business risks are not efficiently understood or visualised. This is

because of the lack of formality and understanding of the same. There is also exists a risk of not

realising what are the greatest risks and which of them are needed to be focused upon by the particular

organisation. For improving the business decision making, the process of efficient risk management is

rapidly gaining acceptance and is aiding the organisations to manage their businesses more effectively.

Brief overview of the company

Woolworths is the largest Australian shopping that deals with food products and beverages in

Australia and New Zeeland. The company has also diversified its offerings by investing in gaming

poker. Woolworth’s financial goals, budget policies, and business policies are at the center of the

management. The company has succeeded in implementing its business policies and key performance

indicators by building a strong team of staff. The company has invested heavily in improving safety

governance to improve safety of staff (Born & Pfeifer, 2014). The main competitor of the organization

is Wesfarmers which is the largest retail industry firm in the current market.

The company of Woolworths Limited has been committed to the various ongoing strategic

developments and uses a consistent enterprise-wide approach for the management of risk by a culture

that is risk-aware. The risk management Policy applies to all the indivituals who works for Woolworths

Limited in, New Zealand, Australia and abroad.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4RISK ASSESSMENT

The significant Risks in business

For the chosen company of Woolworths limited, the concept of Risk refers to the probability of

not getting sufficient return on the various investments made by the company. It involves an

anticipation of future loss. The general types of risk that are identified are as follows:

Strategic risk: The strategic risks are the risk of change in the reference of the customers or changes in

the technology that may lead to the company adapting a new strategy accordingly (Tricker & Tricker,

2014).

Compliance risk: the risk of the compliance refers to the risks that are related to the bureaucratic or

legislative regulations. Tis includes the various areas of regulations for employee protection like those

imposed by the Administration of Occupational Safety and Health, or environmental concerns like

those covered by the Environmental Protection Agency or even local agencies and state.

Financial risk: The financial risk is the anticipation of the loss that may take place due to the

operations of the business. The Financial risks also consider interest rates along with the various

international businesses, foreign exchange rates.

Operational risk: Operational risks are due to the various internal failures. From the various internal

processes, systems or people unexpectedly fail (Bromiley, McShane, Nair & Rustambekov, 2015).

The operational risks can take place from the external events that are unforeseen like transportation

breaking down of systems, or a fail to deliver goods by the supplier and many more.

Reputational risk: The reputational loss of the organiustion may take place from the product failures,

negative publicity or lawsuits. The Reputations are crucial for the company good will and profit.

Therefore a company must be aware of the same.

Analytical procedures

The analytical procedure refers to the financial audit process that would help the auditor to

understand the business of the company whose audit and verification of the financial reports they are

The significant Risks in business

For the chosen company of Woolworths limited, the concept of Risk refers to the probability of

not getting sufficient return on the various investments made by the company. It involves an

anticipation of future loss. The general types of risk that are identified are as follows:

Strategic risk: The strategic risks are the risk of change in the reference of the customers or changes in

the technology that may lead to the company adapting a new strategy accordingly (Tricker & Tricker,

2014).

Compliance risk: the risk of the compliance refers to the risks that are related to the bureaucratic or

legislative regulations. Tis includes the various areas of regulations for employee protection like those

imposed by the Administration of Occupational Safety and Health, or environmental concerns like

those covered by the Environmental Protection Agency or even local agencies and state.

Financial risk: The financial risk is the anticipation of the loss that may take place due to the

operations of the business. The Financial risks also consider interest rates along with the various

international businesses, foreign exchange rates.

Operational risk: Operational risks are due to the various internal failures. From the various internal

processes, systems or people unexpectedly fail (Bromiley, McShane, Nair & Rustambekov, 2015).

The operational risks can take place from the external events that are unforeseen like transportation

breaking down of systems, or a fail to deliver goods by the supplier and many more.

Reputational risk: The reputational loss of the organiustion may take place from the product failures,

negative publicity or lawsuits. The Reputations are crucial for the company good will and profit.

Therefore a company must be aware of the same.

Analytical procedures

The analytical procedure refers to the financial audit process that would help the auditor to

understand the business of the company whose audit and verification of the financial reports they are

5RISK ASSESSMENT

conducting. In the analytical process comparison is to be done of the various financial data of the

business wt respect to the prior periods, budgets and with similar industries

The significant audit risk of the organisation

Going concern

While preparing financial report of the company the directors are responsible to assess the

company’s ability regarding continuation as going concern. They are required to disclose the matters

applicable for going concern and using the same basis unless the company is intended to liquidate or

cease the operation. As per the report of the auditors and audit evidences till the date of auditor’s

report, the company is able to continue as the going concern (Woolworthsgroup.com.au, 2018).

Audit risk model

Audit risk model is associated with the concepts of materiality and audit risk. Audit risk is

likelihood that financial statements of the entity are misstated after it is determined by the auditor that

the financial reports are free from any material misstatement. Under this, the auditors develop the audit

procedures that focus on the greatest risk areas (Contessotto & Moroney, 2014). The auditors are

responsible for addressing that the audit risk model is sufficient and cast and time saving. Further, it

will improve the quality of audit and will add value to the client’s business.

Significant inherent risk –

Inventories – risk involved with the inventories are completeness and occurrence.

Completeness risk states signifies that the inventories may not have been recorded at the

amount at which it has been recognized (Kot & Dragon, 2015). The occurrence risk signifies

that the inventories may not have been existed actually at the closing of the period.

Intangibles – risk involved with intangibles are rights and obligation that is the company

actually have rights for the intangibles reported in the financial statement of the company.

conducting. In the analytical process comparison is to be done of the various financial data of the

business wt respect to the prior periods, budgets and with similar industries

The significant audit risk of the organisation

Going concern

While preparing financial report of the company the directors are responsible to assess the

company’s ability regarding continuation as going concern. They are required to disclose the matters

applicable for going concern and using the same basis unless the company is intended to liquidate or

cease the operation. As per the report of the auditors and audit evidences till the date of auditor’s

report, the company is able to continue as the going concern (Woolworthsgroup.com.au, 2018).

Audit risk model

Audit risk model is associated with the concepts of materiality and audit risk. Audit risk is

likelihood that financial statements of the entity are misstated after it is determined by the auditor that

the financial reports are free from any material misstatement. Under this, the auditors develop the audit

procedures that focus on the greatest risk areas (Contessotto & Moroney, 2014). The auditors are

responsible for addressing that the audit risk model is sufficient and cast and time saving. Further, it

will improve the quality of audit and will add value to the client’s business.

Significant inherent risk –

Inventories – risk involved with the inventories are completeness and occurrence.

Completeness risk states signifies that the inventories may not have been recorded at the

amount at which it has been recognized (Kot & Dragon, 2015). The occurrence risk signifies

that the inventories may not have been existed actually at the closing of the period.

Intangibles – risk involved with intangibles are rights and obligation that is the company

actually have rights for the intangibles reported in the financial statement of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6RISK ASSESSMENT

Another risk involved with the intangibles is valuation that is the intangibles have been valued

properly as per the valuation principle followed by the entity (Louwers et al., 2015).

Fixed assets – risk associated with fixed asset is right and obligation that is the company

actually have rights for the fixed assets reported in the financial statement of the company.

Another risk associated with fixed asset is completeness risk that is the fixed asset may not have

been recorded at appropriate amount after providing depreciation and amortization, if any.

Foreign exchange transactions – the company is exposed to movements in the exchange rate

of foreign currency through – (i) term borrowing that is denominated in the foreign currency (ii)

anticipated equipment and inventory purchase and (iii) translation regarding the net investment

in the foreign subsidiary that is denominated in the foreign currencies. To hedge against these

risks the company enters into the forward exchange contract and the agreements for cross

currency rate of interest (Cheng, Ioannou & Serafeim, 2014). Further, all the currency terms are

entirely hedged through swap agreements of cross currency rate of interest

Control risk –

Corporate governance – the company is subject to various corporate governance regulations,

laws and arrangements and is exposed to the adverse legislative or regulatory changes. Breaches

of the adverse changes may lead to negative impact on company’s reputation as well as on its

profitability. However, the company has the conceptual framework at place and various policies

are established for facilitating the internal protocols and regulatory as well as legal compliances

(McCahery, Sautner & Starks, 2016). Further, the company has code of conduct programs for

promoting awareness regarding the requirement of regulatory, internal and legal policies.

Independent director – the company has 8 directors in its board. Out of total members one

member is the independent chairman, one member is managing director and other 6 members

are independent director. As maximum number of members are independent that is more than 2,

the company is maintaining the prescribed limit with regard to independent directors.

Another risk involved with the intangibles is valuation that is the intangibles have been valued

properly as per the valuation principle followed by the entity (Louwers et al., 2015).

Fixed assets – risk associated with fixed asset is right and obligation that is the company

actually have rights for the fixed assets reported in the financial statement of the company.

Another risk associated with fixed asset is completeness risk that is the fixed asset may not have

been recorded at appropriate amount after providing depreciation and amortization, if any.

Foreign exchange transactions – the company is exposed to movements in the exchange rate

of foreign currency through – (i) term borrowing that is denominated in the foreign currency (ii)

anticipated equipment and inventory purchase and (iii) translation regarding the net investment

in the foreign subsidiary that is denominated in the foreign currencies. To hedge against these

risks the company enters into the forward exchange contract and the agreements for cross

currency rate of interest (Cheng, Ioannou & Serafeim, 2014). Further, all the currency terms are

entirely hedged through swap agreements of cross currency rate of interest

Control risk –

Corporate governance – the company is subject to various corporate governance regulations,

laws and arrangements and is exposed to the adverse legislative or regulatory changes. Breaches

of the adverse changes may lead to negative impact on company’s reputation as well as on its

profitability. However, the company has the conceptual framework at place and various policies

are established for facilitating the internal protocols and regulatory as well as legal compliances

(McCahery, Sautner & Starks, 2016). Further, the company has code of conduct programs for

promoting awareness regarding the requirement of regulatory, internal and legal policies.

Independent director – the company has 8 directors in its board. Out of total members one

member is the independent chairman, one member is managing director and other 6 members

are independent director. As maximum number of members are independent that is more than 2,

the company is maintaining the prescribed limit with regard to independent directors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7RISK ASSESSMENT

Audit and risk committee – main objective of this committee is providing assistance and

advice to the board related to governance framework of the entity that includes risk

management and internal control systems, compliance with the systems and policies and

functions related to external and internal audit. The committee is authorised for performing the

activities those are set out under the responsibilities and making proper suggestions to the

board. The committee is further authorised for meeting the internal as well as the external

auditors without the presence of other members. It is authorised for obtaining the independent

legal or any other professional advice those may be considered as appropriate for executing the

functions. The committee is further has responsibilities and duties regarding governance, risk

management, financial reports and compliance (Hematfar & Hemmati, 2013). The committee is

comprised of minimum 3 directors, majority of which are independent directors. Further, all the

members are financially literate and have acquired business expertise.

Impact of audit testing

The audit testing refers to the examination of the financial records and the transactions off the

company. In this case of Woolworths, at the time of audit testing the identification is done of the at

results of a test cycle, the process by which the results were obtained, and the tools and components a

test has used to obtain these results (Wu, Chen & Olson, 2014).

Implications of Inherent risk and Control Risk for planning

The inherent risk of planning refers to the risk of material misstatement that takes place due to

error or omission of the company data. On the other hand the control risk refers to the material

misstatement risk due to absence or failure of the company’s control or governance. For the company

of the chosen company of Woolworths, the analysis of the inherent and control risk has been discussed

in the above report.

Audit and risk committee – main objective of this committee is providing assistance and

advice to the board related to governance framework of the entity that includes risk

management and internal control systems, compliance with the systems and policies and

functions related to external and internal audit. The committee is authorised for performing the

activities those are set out under the responsibilities and making proper suggestions to the

board. The committee is further authorised for meeting the internal as well as the external

auditors without the presence of other members. It is authorised for obtaining the independent

legal or any other professional advice those may be considered as appropriate for executing the

functions. The committee is further has responsibilities and duties regarding governance, risk

management, financial reports and compliance (Hematfar & Hemmati, 2013). The committee is

comprised of minimum 3 directors, majority of which are independent directors. Further, all the

members are financially literate and have acquired business expertise.

Impact of audit testing

The audit testing refers to the examination of the financial records and the transactions off the

company. In this case of Woolworths, at the time of audit testing the identification is done of the at

results of a test cycle, the process by which the results were obtained, and the tools and components a

test has used to obtain these results (Wu, Chen & Olson, 2014).

Implications of Inherent risk and Control Risk for planning

The inherent risk of planning refers to the risk of material misstatement that takes place due to

error or omission of the company data. On the other hand the control risk refers to the material

misstatement risk due to absence or failure of the company’s control or governance. For the company

of the chosen company of Woolworths, the analysis of the inherent and control risk has been discussed

in the above report.

8RISK ASSESSMENT

Reference

Born, B., & Pfeifer, J. (2014). Policy risk and the business cycle. Journal of Monetary Economics, 68,

68-85.

Bromiley, P., McShane, M., Nair, A., & Rustambekov, E. (2015). Enterprise risk management:

Review, critique, and research directions. Long range planning, 48(4), 265-276.

Cheng, B., Ioannou, I., & Serafeim, G. (2014). Corporate social responsibility and access to

finance. Strategic management journal, 35(1), 1-23.

Contessotto, C., & Moroney, R. (2014). The association between audit committee effectiveness and

audit risk. Accounting & Finance, 54(2), 393-418.

Hall, M., Mikes, A., & Millo, Y. (2015). How do risk managers become influential? A field study of

toolmaking in two financial institutions. Management Accounting Research, 26, 3-22.

Hematfar, M., & Hemmati, M. (2013). A comparison of risk-based and traditional auditing and their

effect on the quality of audit reports. International Research Journal of Applied and Basic

Sciences, 4(8), 2088-2091.

Kot, S., & Dragon, P. (2015). Business risk management in international corporations. Procedia

Economics and Finance, 27, 102-108.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C. (2015). Auditing &

assurance services. McGraw-Hill Education.

McCahery, J.A., Sautner, Z. & Starks, L.T., (2016). Behind the scenes: The corporate governance

preferences of institutional investors. The Journal of Finance, 71(6), pp.2905-2932.

Tricker, B., & Tricker, G. (2014). Business Ethics: A stakeholder, governance and risk approach.

Routledge.

Woolworthsgroup.com.au. (2018). Retrieved 28 September 2018, from

https://www.woolworthsgroup.com.au/icms_docs/186100_audit-risk-management-and-

compliance-committee-charter.pdf

Reference

Born, B., & Pfeifer, J. (2014). Policy risk and the business cycle. Journal of Monetary Economics, 68,

68-85.

Bromiley, P., McShane, M., Nair, A., & Rustambekov, E. (2015). Enterprise risk management:

Review, critique, and research directions. Long range planning, 48(4), 265-276.

Cheng, B., Ioannou, I., & Serafeim, G. (2014). Corporate social responsibility and access to

finance. Strategic management journal, 35(1), 1-23.

Contessotto, C., & Moroney, R. (2014). The association between audit committee effectiveness and

audit risk. Accounting & Finance, 54(2), 393-418.

Hall, M., Mikes, A., & Millo, Y. (2015). How do risk managers become influential? A field study of

toolmaking in two financial institutions. Management Accounting Research, 26, 3-22.

Hematfar, M., & Hemmati, M. (2013). A comparison of risk-based and traditional auditing and their

effect on the quality of audit reports. International Research Journal of Applied and Basic

Sciences, 4(8), 2088-2091.

Kot, S., & Dragon, P. (2015). Business risk management in international corporations. Procedia

Economics and Finance, 27, 102-108.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C. (2015). Auditing &

assurance services. McGraw-Hill Education.

McCahery, J.A., Sautner, Z. & Starks, L.T., (2016). Behind the scenes: The corporate governance

preferences of institutional investors. The Journal of Finance, 71(6), pp.2905-2932.

Tricker, B., & Tricker, G. (2014). Business Ethics: A stakeholder, governance and risk approach.

Routledge.

Woolworthsgroup.com.au. (2018). Retrieved 28 September 2018, from

https://www.woolworthsgroup.com.au/icms_docs/186100_audit-risk-management-and-

compliance-committee-charter.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9RISK ASSESSMENT

Wu, D. D., Chen, S. H., & Olson, D. L. (2014). Business intelligence in risk management: Some recent

progresses. Information Sciences, 256, 1-7.

Appendices

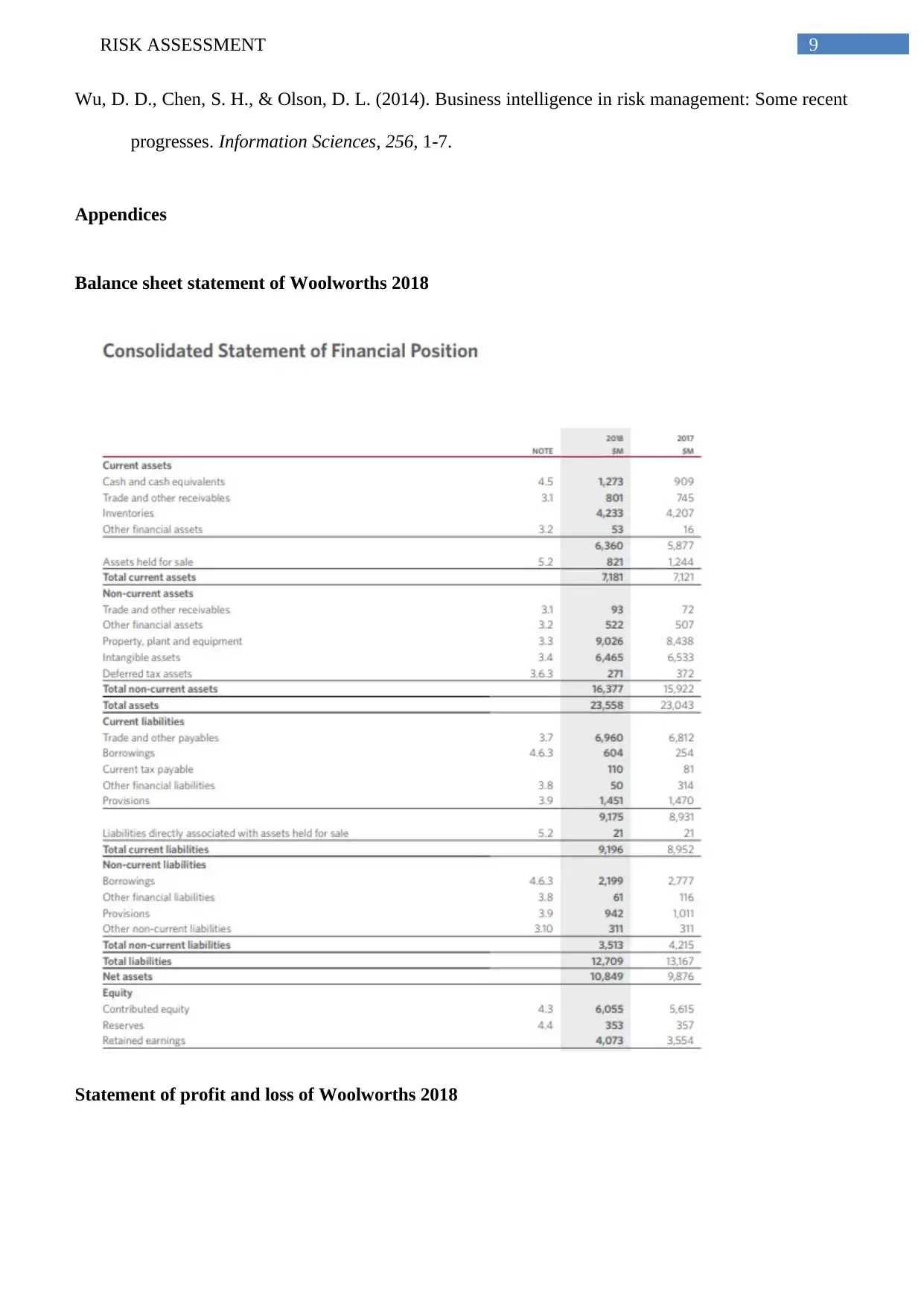

Balance sheet statement of Woolworths 2018

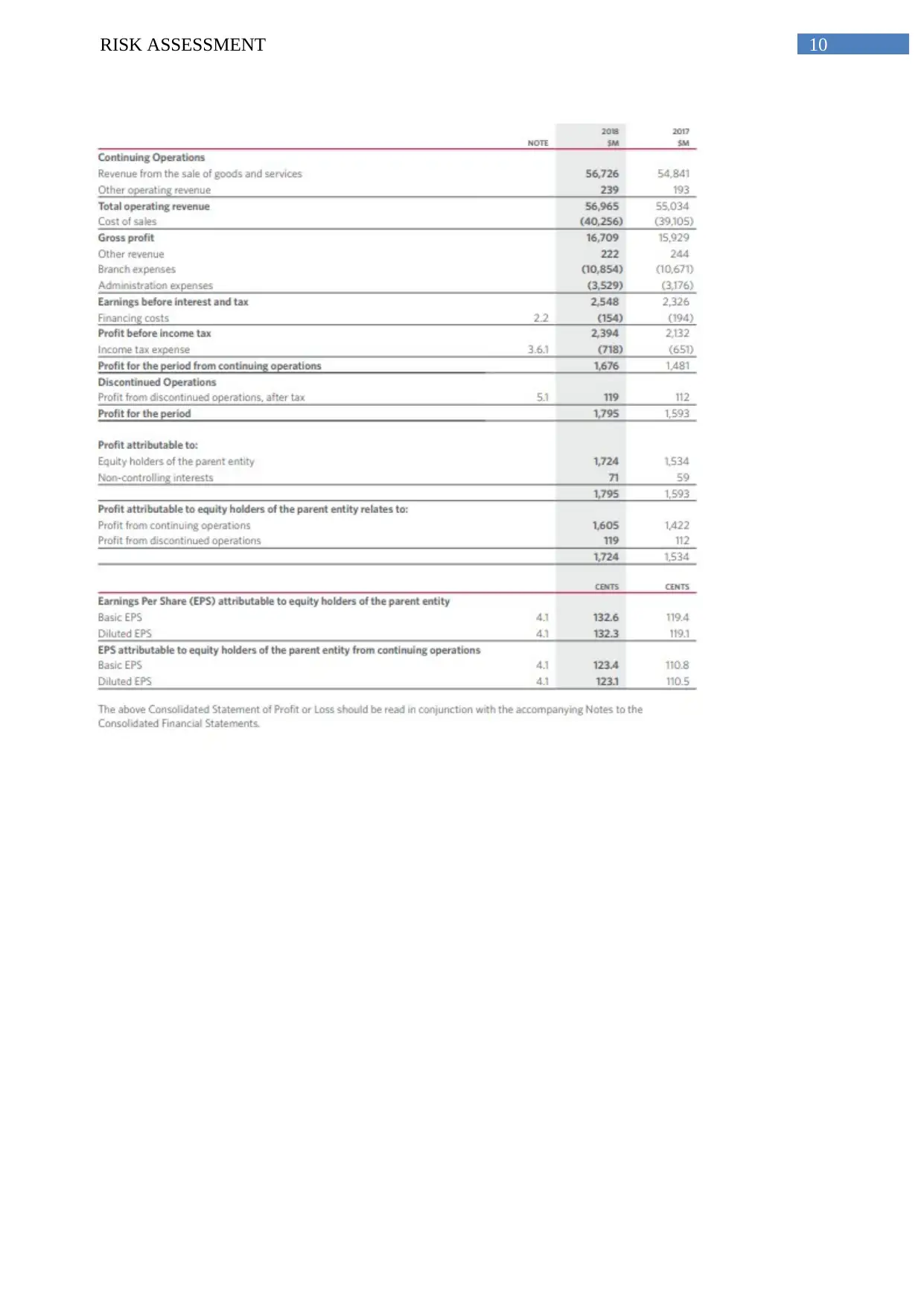

Statement of profit and loss of Woolworths 2018

Wu, D. D., Chen, S. H., & Olson, D. L. (2014). Business intelligence in risk management: Some recent

progresses. Information Sciences, 256, 1-7.

Appendices

Balance sheet statement of Woolworths 2018

Statement of profit and loss of Woolworths 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10RISK ASSESSMENT

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.