Woolworths Limited: Analysis of Financial Statements and Components

VerifiedAdded on 2021/05/31

|13

|2871

|83

Report

AI Summary

This report provides a detailed analysis of Woolworths Limited's financial statements for the years 2015-2017. It begins with an executive summary and introduction outlining the report's objectives, which include examining the cash flow statement, other comprehensive income (OCI) statement, and corporate income tax treatment. The analysis of the cash flow statement includes item bifurcation and a comparison of operating, investing, and financing activities over the three-year period. The report also delves into the components of the OCI statement, explaining the nature of items such as hedging reserves, foreign currency translation reserves, equity instrument reserves, and retained earnings, along with the rationale for their exclusion from the profit and loss statement. Furthermore, the report examines Woolworths' corporate income tax, including tax expense, accounting income and tax effects, deferred tax, and the tax treatment rating. The report concludes with recommendations based on the financial analysis. The report uses Woolworths Limited's annual reports and other reliable sources to support its analysis.

WOOLWORTHS LIMITED

ANALYSIS OF FINANCIAL STATEMENTS AND ITS COMPONENTS

Student Name: Student ID:

5/16/2018

ANALYSIS OF FINANCIAL STATEMENTS AND ITS COMPONENTS

Student Name: Student ID:

5/16/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.................................................................................................................................3

INTRODUCTION...........................................................................................................................................4

CHOSEN COMPANY DETAIL.........................................................................................................................5

CASH FLOW STATEMENT AND ITS ANALYSIS...............................................................................................5

Item bifurcation.......................................................................................................................................5

Comparison of board categories.............................................................................................................7

OTHER COMPREHENSIVE INCOME STATEMENT AND ITS ANALYSIS............................................................8

ITEMS DESCRIBE IN STATEMENT.............................................................................................................8

Detailed description of every item..........................................................................................................9

Reasons for not reporting in Statement of Profit or Loss......................................................................10

CORPORATE INCOME TAX AND ITS ANALYSIS...........................................................................................10

Tax Expense for Current Year................................................................................................................10

Accounting Income and tax effect.........................................................................................................11

Deferred Tax – Assets and Liabilities.....................................................................................................11

Income tax – Payable and Expense........................................................................................................12

Income Tax – Expense and Paid.............................................................................................................12

Tax Treatment - Rating..........................................................................................................................12

CONCLUSION AND RECOMMENDATION...................................................................................................12

REFERENCES..............................................................................................................................................13

EXECUTIVE SUMMARY.................................................................................................................................3

INTRODUCTION...........................................................................................................................................4

CHOSEN COMPANY DETAIL.........................................................................................................................5

CASH FLOW STATEMENT AND ITS ANALYSIS...............................................................................................5

Item bifurcation.......................................................................................................................................5

Comparison of board categories.............................................................................................................7

OTHER COMPREHENSIVE INCOME STATEMENT AND ITS ANALYSIS............................................................8

ITEMS DESCRIBE IN STATEMENT.............................................................................................................8

Detailed description of every item..........................................................................................................9

Reasons for not reporting in Statement of Profit or Loss......................................................................10

CORPORATE INCOME TAX AND ITS ANALYSIS...........................................................................................10

Tax Expense for Current Year................................................................................................................10

Accounting Income and tax effect.........................................................................................................11

Deferred Tax – Assets and Liabilities.....................................................................................................11

Income tax – Payable and Expense........................................................................................................12

Income Tax – Expense and Paid.............................................................................................................12

Tax Treatment - Rating..........................................................................................................................12

CONCLUSION AND RECOMMENDATION...................................................................................................12

REFERENCES..............................................................................................................................................13

EXECUTIVE SUMMARY

Financial Statement and their analysis is base for users of financial statements which helps in

decision making. The report has been prepared with an intention to analyze financial statements

and their part so that better decision making can happen. The major aim for which the report has

been prepared to understand the different items reported in Cash Flow statements and Other

Comprehensive Income statement of Company. The report also helps in understanding the

accounting treatment of corporation tax in financial accounting and their required disclosures as

taxes have major impact on decision making process. With theses intention, study has been

conducted in appropriate manner.

Financial Statement and their analysis is base for users of financial statements which helps in

decision making. The report has been prepared with an intention to analyze financial statements

and their part so that better decision making can happen. The major aim for which the report has

been prepared to understand the different items reported in Cash Flow statements and Other

Comprehensive Income statement of Company. The report also helps in understanding the

accounting treatment of corporation tax in financial accounting and their required disclosures as

taxes have major impact on decision making process. With theses intention, study has been

conducted in appropriate manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The title of the report – Analysis of Financial Statements suggests its purpose of preparation. The

study has been done to analyze the different of different statements which are part of financial

statements of company. The study has been prepared to assess the Cash Flow Statements and

Other Comprehensive Income Statement of chosen company. The report has been prepared in

major three parts. The first describes each item which has been reported in cash flow statement

of reported company along with comparison of each item of cash flow over past three years for

chosen company. The second part helps in understanding the components of Other

Comprehensive Income Statement and their exclusion from Profit and Loss account for chosen

company. The third part explains the concept f corporation tax and its treatment in accounting

books by the company and its management. The report has been ended with proper

recommendation and conclusion. For the purpose of report, Woolworths Limited has been

selected, a company registered in Australia and listed in ASX. The study has been prepared using

the Annual Reports available on the company’s website along with other information available

through reliable sources.

The title of the report – Analysis of Financial Statements suggests its purpose of preparation. The

study has been done to analyze the different of different statements which are part of financial

statements of company. The study has been prepared to assess the Cash Flow Statements and

Other Comprehensive Income Statement of chosen company. The report has been prepared in

major three parts. The first describes each item which has been reported in cash flow statement

of reported company along with comparison of each item of cash flow over past three years for

chosen company. The second part helps in understanding the components of Other

Comprehensive Income Statement and their exclusion from Profit and Loss account for chosen

company. The third part explains the concept f corporation tax and its treatment in accounting

books by the company and its management. The report has been ended with proper

recommendation and conclusion. For the purpose of report, Woolworths Limited has been

selected, a company registered in Australia and listed in ASX. The study has been prepared using

the Annual Reports available on the company’s website along with other information available

through reliable sources.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CHOSEN COMPANY DETAIL

Woolworths Limited has been selected, a company registered in Australia. The company has its

operations from 1924 in Australia and enhances its operations in New Zealand as time passes.

The company is second biggest company in terms of revenue in Australia in retail industry. It has

supermarket chains across Australia and New Zealand dealing with millions of customer on daily

basis. The company has been considered as full compliance company in relation to filings

required by SEC and other laws. Company’s Annual Report for three years – 2015, 2016 and

2017 has been taken into account in preparation of the report.

CASH FLOW STATEMENT AND ITS ANALYSIS

Cash Flows statement shows the total inflow and total outflow of cash and cash equivalent for

the reporting period. The cash flow statement has been prepared according to business activities

which are bifurcated into Operating activities, Investing Activities and Financing Activities.

Item bifurcation

The following items are reported in the statement of cash flow of Woolworths Limited which are

important for analysis:-

Revenue from customers: - This item describes the inflow of cash which is generated

from amount collected from customers of the company to whom goods and services

have been sold. The amount collected from customers of the company has been by

$169 millions in 2017 from 2016.

Amount paid to Creditors and Employees – This item relates to outflow of cash

which are required for operations of the company. It shows that cash paid to suppliers

from whom goods and services are purchased along with payments to be made to

employees for their services in form of salary and other perquisites. The amount paid

by company has been decreased by $ 360 million in 2017 from 2016.

Woolworths Limited has been selected, a company registered in Australia. The company has its

operations from 1924 in Australia and enhances its operations in New Zealand as time passes.

The company is second biggest company in terms of revenue in Australia in retail industry. It has

supermarket chains across Australia and New Zealand dealing with millions of customer on daily

basis. The company has been considered as full compliance company in relation to filings

required by SEC and other laws. Company’s Annual Report for three years – 2015, 2016 and

2017 has been taken into account in preparation of the report.

CASH FLOW STATEMENT AND ITS ANALYSIS

Cash Flows statement shows the total inflow and total outflow of cash and cash equivalent for

the reporting period. The cash flow statement has been prepared according to business activities

which are bifurcated into Operating activities, Investing Activities and Financing Activities.

Item bifurcation

The following items are reported in the statement of cash flow of Woolworths Limited which are

important for analysis:-

Revenue from customers: - This item describes the inflow of cash which is generated

from amount collected from customers of the company to whom goods and services

have been sold. The amount collected from customers of the company has been by

$169 millions in 2017 from 2016.

Amount paid to Creditors and Employees – This item relates to outflow of cash

which are required for operations of the company. It shows that cash paid to suppliers

from whom goods and services are purchased along with payments to be made to

employees for their services in form of salary and other perquisites. The amount paid

by company has been decreased by $ 360 million in 2017 from 2016.

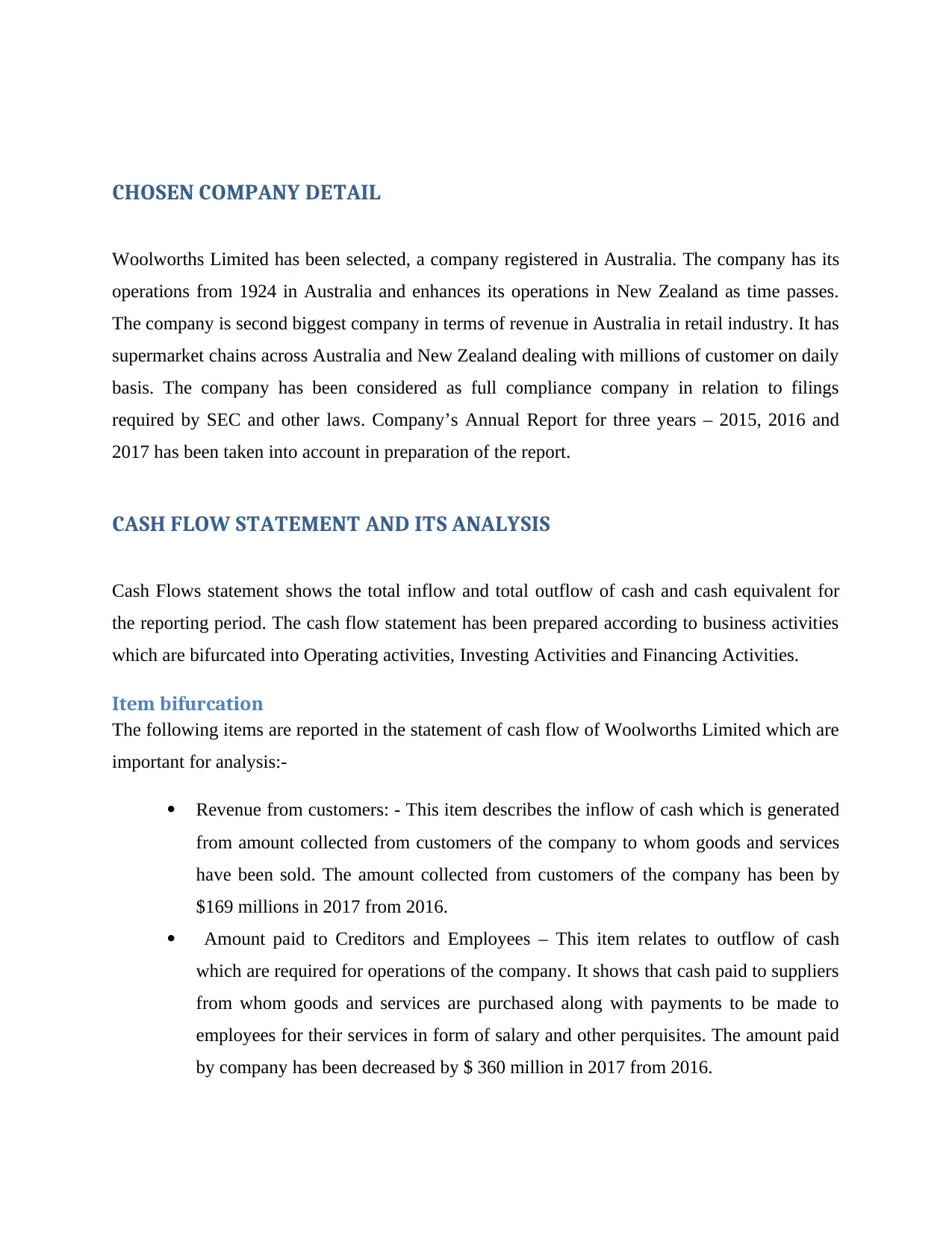

Payment of Income Tax: - This item describes the tax paid by the company on the

income earned as per Australian Taxation Laws. The income tax paid by company

has been decreased by $162 million in 2017 from 2016.

Receipts from property, plant and equipment sale: - This item shows the inflow of

cash from the sale of noncurrent assets which includes Property, Plant and

Equipment. It shows disposal of assets by company for cash or cash equivalents to

convert the investment in liquid assets.

Payment made for purchase of Non Current Asset: - This item consists of outflow of

cash or cash equivalent to procure and invest the funds of the company in noncurrent

assets such as Property, Plant and Equipments.

Amount paid for Business Acquisition: - To have more profits and to form synergies

in performances, business of other companies will acquired by paying the amount to

the owners of other business. This item in cash flow describes the outflow of cash or

cash equivalents in order to have net assets of the other company.

Amount received as dividend: - This item shows inflow of cash into the company

which is received by the company on the investment made in form of shares of other

companies.

Issue of Shares: - This item shows major inflow of cash or cash equivalent that is

received by the company by issuing shares in stock market. It is the major sources of

funds for generating funds for doing investment and operates business. In the cash

flow of Woolworths $ 55.5 million worth shares have been issued in 2017 and no

such inflow of cash in past year under consideration.

Receipts from loans: - This item shows the inflow of cash in form of liability creation

by having borrowings from Banks and financial institutions in order to have smooth

business function (Fraser, Ormiston and Fraser, 2010). The company has taken loans

in both years 2016 and 2017 but in 2017 the amount borrowed is $ 184 million in

comparison to $ 628 million.

Settlement of Loans: - This item is an outflow of cash which shows the amount repaid

for loans taken earlier to in order to have reduced liability for the company. The

company has paid more amounts in 2017 towards repayment of loan as compared to

in 2016 which was $ 994 million.

income earned as per Australian Taxation Laws. The income tax paid by company

has been decreased by $162 million in 2017 from 2016.

Receipts from property, plant and equipment sale: - This item shows the inflow of

cash from the sale of noncurrent assets which includes Property, Plant and

Equipment. It shows disposal of assets by company for cash or cash equivalents to

convert the investment in liquid assets.

Payment made for purchase of Non Current Asset: - This item consists of outflow of

cash or cash equivalent to procure and invest the funds of the company in noncurrent

assets such as Property, Plant and Equipments.

Amount paid for Business Acquisition: - To have more profits and to form synergies

in performances, business of other companies will acquired by paying the amount to

the owners of other business. This item in cash flow describes the outflow of cash or

cash equivalents in order to have net assets of the other company.

Amount received as dividend: - This item shows inflow of cash into the company

which is received by the company on the investment made in form of shares of other

companies.

Issue of Shares: - This item shows major inflow of cash or cash equivalent that is

received by the company by issuing shares in stock market. It is the major sources of

funds for generating funds for doing investment and operates business. In the cash

flow of Woolworths $ 55.5 million worth shares have been issued in 2017 and no

such inflow of cash in past year under consideration.

Receipts from loans: - This item shows the inflow of cash in form of liability creation

by having borrowings from Banks and financial institutions in order to have smooth

business function (Fraser, Ormiston and Fraser, 2010). The company has taken loans

in both years 2016 and 2017 but in 2017 the amount borrowed is $ 184 million in

comparison to $ 628 million.

Settlement of Loans: - This item is an outflow of cash which shows the amount repaid

for loans taken earlier to in order to have reduced liability for the company. The

company has paid more amounts in 2017 towards repayment of loan as compared to

in 2016 which was $ 994 million.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Amount paid as dividend: - This item shows outflow of cash and cash equivalent

which has been paid to the real owners of the company in return of the amount

invested by them in the company. The company has paid fewer dividends in 2017 of

$540 million as compared to $ 1184 million in 2016 which shows the distrust of

owners in company (Woolworths Limited, 2016).

Comparison of board categories

Cash flows statement has been prepared on the basis of business activities which are divided in

Operating Activities, Investing Activities and Financing Activities. Any inflow or outflow of

cash and cash equivalent has been recorded in Cash flow statement after identifying the same

into these three board categories. The cash flow statements the net result from these categories in

the form of net increase or decreased in cash. The Woolworths comparison of three board

categories has been listed below:

S.

No.

Categories 30th June

2017

30th June

2016

30th June

2015

which has been paid to the real owners of the company in return of the amount

invested by them in the company. The company has paid fewer dividends in 2017 of

$540 million as compared to $ 1184 million in 2016 which shows the distrust of

owners in company (Woolworths Limited, 2016).

Comparison of board categories

Cash flows statement has been prepared on the basis of business activities which are divided in

Operating Activities, Investing Activities and Financing Activities. Any inflow or outflow of

cash and cash equivalent has been recorded in Cash flow statement after identifying the same

into these three board categories. The cash flow statements the net result from these categories in

the form of net increase or decreased in cash. The Woolworths comparison of three board

categories has been listed below:

S.

No.

Categories 30th June

2017

30th June

2016

30th June

2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 Net Cash Flow from Operating

Activities

$ 3,122 $ 2,357 $ 3,345

2 Net Cash used in Investing Activities $ (1,432) $(1,266) $(1,335)

3 Net cash used in Financing Activities $ (1,729) $ (1,475) $ (1,610)

4 Net Increase or (Decrease) in Cash

and cash equivalent

$ (39) $ (384) $ 400

Operating Activities: - The cash flow from Operating Activities shows the increased from

2016 to 2017 but in three years comparison it has been decreased from 2015 which was $

3345 million. The main reason for reduction of the amount received from customers and

fluctuation in payment for purchases and payment to employees. Also, the income taxes

paid have decrease from past year showing lower revenue for the company.

Investing Activities: - The cash has been used in investing activities for all the past three

years showing that company is involved in procurement of new assets every year so that

more profits can be earned in future. On the other hand, the company is blocking up more

liquid funds into non liquid assets like Property, Plant and Equipment.

Financing Activities: - The company has negative funds from financing activities

showing more repayment of borrowings which was taken in past years. The company is

in the process of reducing the outside long term liabilities (Taylor, 2010).

OTHER COMPREHENSIVE INCOME STATEMENT AND ITS ANALYSIS

It is the statement which has been prepared after ascertaining the profit or loss for the period

detailed in statement of profit or loss.

ITEMS DESCRIBE IN STATEMENT

In statement of comprehensive income below are the items which have been describe and

mentioned in annual report:-

a. Reclassified Items

Activities

$ 3,122 $ 2,357 $ 3,345

2 Net Cash used in Investing Activities $ (1,432) $(1,266) $(1,335)

3 Net cash used in Financing Activities $ (1,729) $ (1,475) $ (1,610)

4 Net Increase or (Decrease) in Cash

and cash equivalent

$ (39) $ (384) $ 400

Operating Activities: - The cash flow from Operating Activities shows the increased from

2016 to 2017 but in three years comparison it has been decreased from 2015 which was $

3345 million. The main reason for reduction of the amount received from customers and

fluctuation in payment for purchases and payment to employees. Also, the income taxes

paid have decrease from past year showing lower revenue for the company.

Investing Activities: - The cash has been used in investing activities for all the past three

years showing that company is involved in procurement of new assets every year so that

more profits can be earned in future. On the other hand, the company is blocking up more

liquid funds into non liquid assets like Property, Plant and Equipment.

Financing Activities: - The company has negative funds from financing activities

showing more repayment of borrowings which was taken in past years. The company is

in the process of reducing the outside long term liabilities (Taylor, 2010).

OTHER COMPREHENSIVE INCOME STATEMENT AND ITS ANALYSIS

It is the statement which has been prepared after ascertaining the profit or loss for the period

detailed in statement of profit or loss.

ITEMS DESCRIBE IN STATEMENT

In statement of comprehensive income below are the items which have been describe and

mentioned in annual report:-

a. Reclassified Items

Hedging Reserve

Foreign Currency Translation Reserve

b. Non reclassified Items

Equity Instruments Reserve

Retained Earnings

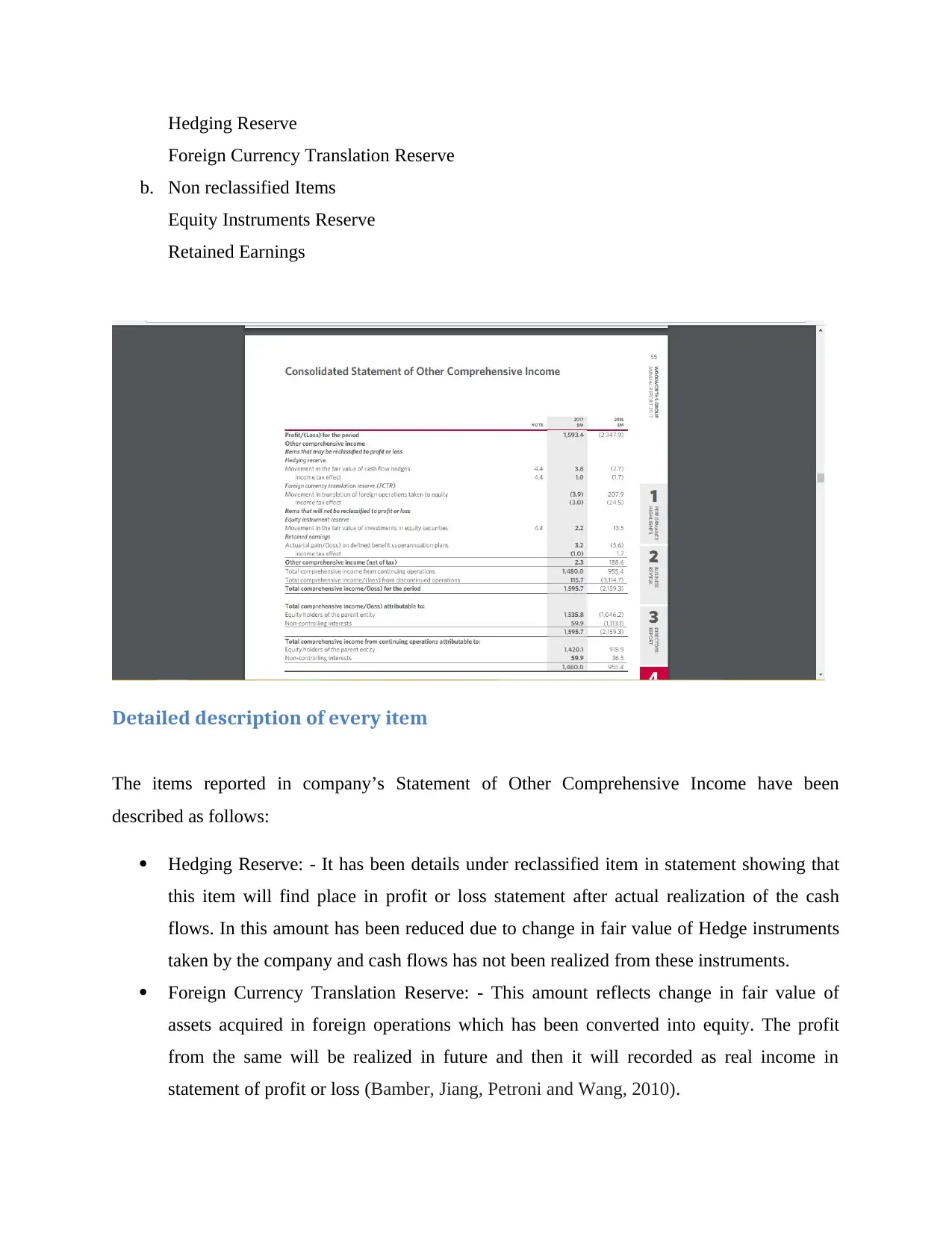

Detailed description of every item

The items reported in company’s Statement of Other Comprehensive Income have been

described as follows:

Hedging Reserve: - It has been details under reclassified item in statement showing that

this item will find place in profit or loss statement after actual realization of the cash

flows. In this amount has been reduced due to change in fair value of Hedge instruments

taken by the company and cash flows has not been realized from these instruments.

Foreign Currency Translation Reserve: - This amount reflects change in fair value of

assets acquired in foreign operations which has been converted into equity. The profit

from the same will be realized in future and then it will recorded as real income in

statement of profit or loss (Bamber, Jiang, Petroni and Wang, 2010).

Foreign Currency Translation Reserve

b. Non reclassified Items

Equity Instruments Reserve

Retained Earnings

Detailed description of every item

The items reported in company’s Statement of Other Comprehensive Income have been

described as follows:

Hedging Reserve: - It has been details under reclassified item in statement showing that

this item will find place in profit or loss statement after actual realization of the cash

flows. In this amount has been reduced due to change in fair value of Hedge instruments

taken by the company and cash flows has not been realized from these instruments.

Foreign Currency Translation Reserve: - This amount reflects change in fair value of

assets acquired in foreign operations which has been converted into equity. The profit

from the same will be realized in future and then it will recorded as real income in

statement of profit or loss (Bamber, Jiang, Petroni and Wang, 2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Equity Instrument Reserve: - This item of statement is considered as non reclassified as it

will not be recorded in Statement of profit or loss but the corresponding reserve has been

created in future under the head Reserve and Surplus. It shows the change in fair value of

equity assets owned by the company.

Retained Earnings: - It shows the gain or loss on actuarial valuation of superannuation

funds by the company. It will be recorded as no reclassified item in statement showing

gain or loss with effect the reserves of the company not the profit or loss (Chambers,

2011).

Reasons for not reporting in Statement of Profit or Loss

The items will not be reported in Statement of Profit or Loss as there is no actual gain or loss

from operating activities of the company rather the gain or loss have been generated in unusual

event happened in the company during reported period. Also, cash flows from or to be paid are

not fully certain to record the same under profit or loss statement. The reclassified and non

reclassified items has been reported by Woolworths Limited in compliance with AASB 101 and

other applicable accounting rules which suggest to report the item in Comprehensive Income

statement so that correct and full information can be communicated to different stakeholders of

the company for effective and efficient decision making.

CORPORATE INCOME TAX AND ITS ANALYSIS

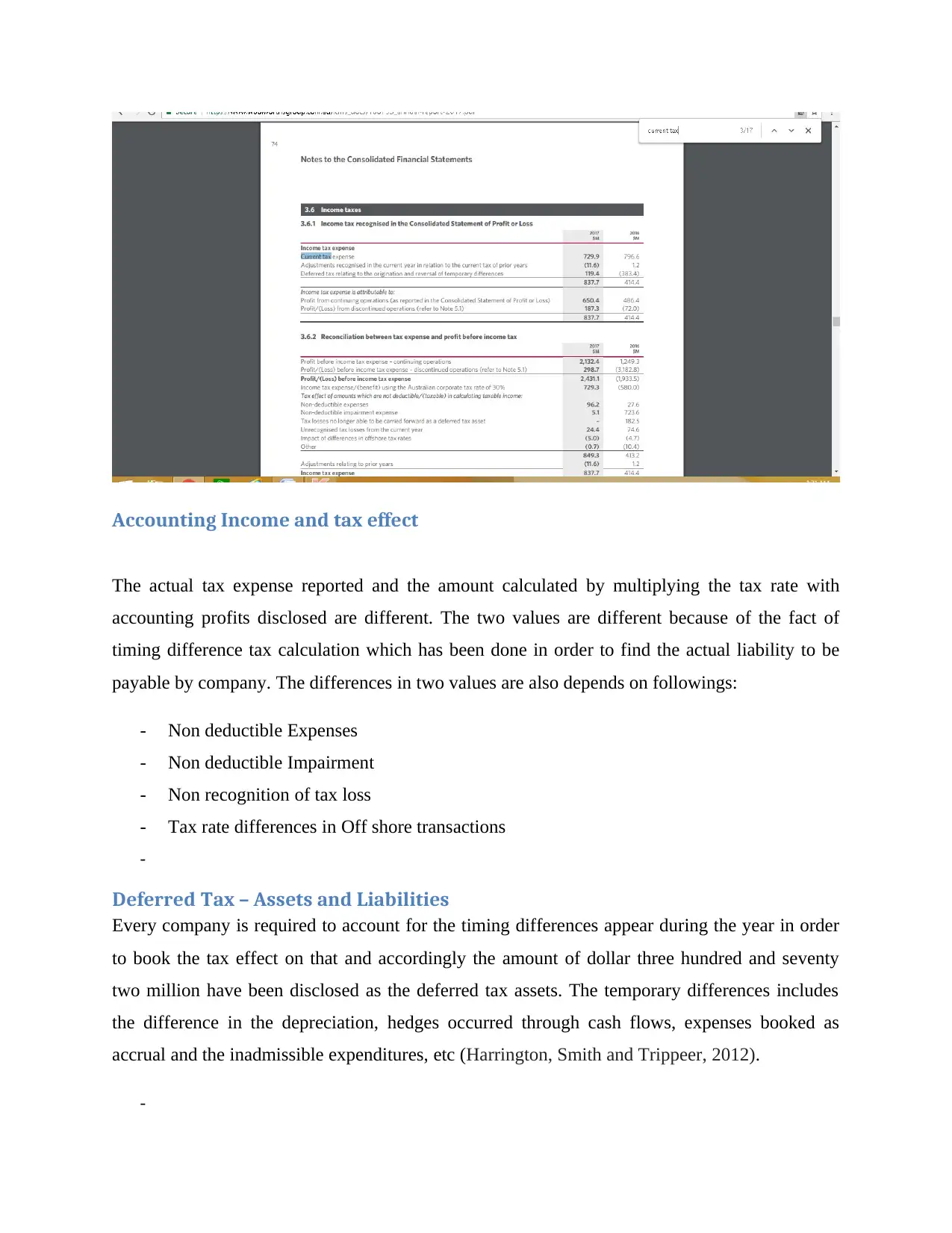

Tax Expense for Current Year

The firm’s current tax expense as reported in its latest financial statement for the period ending

on 30th June 2017 was $ 837.50 million which shows the current tax expense of the company is

$729.9 million and other is adjustment and deferred tax (Woolworths Limited, 2017).

will not be recorded in Statement of profit or loss but the corresponding reserve has been

created in future under the head Reserve and Surplus. It shows the change in fair value of

equity assets owned by the company.

Retained Earnings: - It shows the gain or loss on actuarial valuation of superannuation

funds by the company. It will be recorded as no reclassified item in statement showing

gain or loss with effect the reserves of the company not the profit or loss (Chambers,

2011).

Reasons for not reporting in Statement of Profit or Loss

The items will not be reported in Statement of Profit or Loss as there is no actual gain or loss

from operating activities of the company rather the gain or loss have been generated in unusual

event happened in the company during reported period. Also, cash flows from or to be paid are

not fully certain to record the same under profit or loss statement. The reclassified and non

reclassified items has been reported by Woolworths Limited in compliance with AASB 101 and

other applicable accounting rules which suggest to report the item in Comprehensive Income

statement so that correct and full information can be communicated to different stakeholders of

the company for effective and efficient decision making.

CORPORATE INCOME TAX AND ITS ANALYSIS

Tax Expense for Current Year

The firm’s current tax expense as reported in its latest financial statement for the period ending

on 30th June 2017 was $ 837.50 million which shows the current tax expense of the company is

$729.9 million and other is adjustment and deferred tax (Woolworths Limited, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Income and tax effect

The actual tax expense reported and the amount calculated by multiplying the tax rate with

accounting profits disclosed are different. The two values are different because of the fact of

timing difference tax calculation which has been done in order to find the actual liability to be

payable by company. The differences in two values are also depends on followings:

- Non deductible Expenses

- Non deductible Impairment

- Non recognition of tax loss

- Tax rate differences in Off shore transactions

-

Deferred Tax – Assets and Liabilities

Every company is required to account for the timing differences appear during the year in order

to book the tax effect on that and accordingly the amount of dollar three hundred and seventy

two million have been disclosed as the deferred tax assets. The temporary differences includes

the difference in the depreciation, hedges occurred through cash flows, expenses booked as

accrual and the inadmissible expenditures, etc (Harrington, Smith and Trippeer, 2012).

-

The actual tax expense reported and the amount calculated by multiplying the tax rate with

accounting profits disclosed are different. The two values are different because of the fact of

timing difference tax calculation which has been done in order to find the actual liability to be

payable by company. The differences in two values are also depends on followings:

- Non deductible Expenses

- Non deductible Impairment

- Non recognition of tax loss

- Tax rate differences in Off shore transactions

-

Deferred Tax – Assets and Liabilities

Every company is required to account for the timing differences appear during the year in order

to book the tax effect on that and accordingly the amount of dollar three hundred and seventy

two million have been disclosed as the deferred tax assets. The temporary differences includes

the difference in the depreciation, hedges occurred through cash flows, expenses booked as

accrual and the inadmissible expenditures, etc (Harrington, Smith and Trippeer, 2012).

-

Income tax – Payable and Expense

It is evident from the financial statements that the company has disclosed the amount of income

tax which is payable at the end of the year. Both the figures are not same with the reason thereof

that the payable includes the amount to be paid to the income tax office and expense includes the

tax and deferred tax amount. (Laux, 2013).

Income Tax – Expense and Paid

Difference has been observed in the income tax expense and the income tax paid because of the

fact that expense includes two components deferred and current. Paid part is only current and not

deferred. (Manzon, G.B. and Plesko, 2012).

Tax Treatment - Rating

On the basis of aforesaid discussion, the company has made the correct accounting treatment and

hence the rating will be good.

CONCLUSION AND RECOMMENDATION

Annual report of the company provides the statutory reports which in turn will help the users of

the financial to have an informed and meaningful decision. In the annual report of any company

four statements are majorly prepared but for the purpose of this report, cash flow statement and

the statement of other comprehensive income have been discussed. The annual report of

Woolworths Limited has been considered and accordingly its statements have been analysed in

detail. The cash flow statement has been discussed and then the reason for mentioning items

under the statement of other comprehensive income had been detailed and then the treatment of

tax expense has been made understood. The report is concluded with the end note that the

Woolworths limited are preparing all the statements in the true and fair manner.

Through the means of this report, the recommendation is being made to prepare the financial

statements with full transparency in order to provide the users of the financial statements with all

the details as required by them for decision making.

It is evident from the financial statements that the company has disclosed the amount of income

tax which is payable at the end of the year. Both the figures are not same with the reason thereof

that the payable includes the amount to be paid to the income tax office and expense includes the

tax and deferred tax amount. (Laux, 2013).

Income Tax – Expense and Paid

Difference has been observed in the income tax expense and the income tax paid because of the

fact that expense includes two components deferred and current. Paid part is only current and not

deferred. (Manzon, G.B. and Plesko, 2012).

Tax Treatment - Rating

On the basis of aforesaid discussion, the company has made the correct accounting treatment and

hence the rating will be good.

CONCLUSION AND RECOMMENDATION

Annual report of the company provides the statutory reports which in turn will help the users of

the financial to have an informed and meaningful decision. In the annual report of any company

four statements are majorly prepared but for the purpose of this report, cash flow statement and

the statement of other comprehensive income have been discussed. The annual report of

Woolworths Limited has been considered and accordingly its statements have been analysed in

detail. The cash flow statement has been discussed and then the reason for mentioning items

under the statement of other comprehensive income had been detailed and then the treatment of

tax expense has been made understood. The report is concluded with the end note that the

Woolworths limited are preparing all the statements in the true and fair manner.

Through the means of this report, the recommendation is being made to prepare the financial

statements with full transparency in order to provide the users of the financial statements with all

the details as required by them for decision making.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.