Business Finance Report: UberTools Ltd and Madagascar Industries

VerifiedAdded on 2020/10/22

|16

|3877

|340

Report

AI Summary

This report delves into the realm of business finance, specifically examining the financial performance of UberTools Ltd and Madagascar Industries Ltd. It begins by defining and differentiating profit and cash flow, exploring the components of working capital (receivables, inventory, payables), and analyzing how alterations in working capital impact a company's cash flow. The report then applies these concepts, discussing how effective management can influence financial outcomes. Part 2 focuses on financial ratio analysis, explaining key elements of financial performance such as sales growth, gross profit margin, operating profit margin, gearing ratio, interest coverage ratio, and liquidity ratios. The report calculates and interprets these ratios for the companies, providing recommendations for improving cash flow via better working capital management and assessing overall financial performance. The report concludes with recommendations for improving cash flow and financial performance, based on the case study analysis and the application of financial ratios.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1.1 Explain..................................................................................................................................1

1.1.a Profit and cash flow with their difference..........................................................................1

1.1.b Working capital, receivables, inventory and payables.......................................................1

1.1.c Impact of alteration in working capital on cash flow.........................................................2

1.2 Application of above concept and managing might impact financial outcome...................2

1.3 Analysing and recommending steps must be undertaken for improving cash flow of

company via better working capital management.......................................................................4

PART 2............................................................................................................................................5

2.1 On basis of financial ratios....................................................................................................5

2.1.a Explaining element of financial performance....................................................................5

2.1.b Calculating ratio of each year............................................................................................9

2.1.c Applying the outcome of ratios with appropriate interpretation........................................9

2.2 Analysing and recommending board for assessing business's financial performance........10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

2.1 (b) Ratio analysis................................................................................................................12

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1.1 Explain..................................................................................................................................1

1.1.a Profit and cash flow with their difference..........................................................................1

1.1.b Working capital, receivables, inventory and payables.......................................................1

1.1.c Impact of alteration in working capital on cash flow.........................................................2

1.2 Application of above concept and managing might impact financial outcome...................2

1.3 Analysing and recommending steps must be undertaken for improving cash flow of

company via better working capital management.......................................................................4

PART 2............................................................................................................................................5

2.1 On basis of financial ratios....................................................................................................5

2.1.a Explaining element of financial performance....................................................................5

2.1.b Calculating ratio of each year............................................................................................9

2.1.c Applying the outcome of ratios with appropriate interpretation........................................9

2.2 Analysing and recommending board for assessing business's financial performance........10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

2.1 (b) Ratio analysis................................................................................................................12

INTRODUCTION

Business finance is replicated as money and credit employed in business as its basic is

finance. Finance is need for buying assets, raw materials along with other flow of economic

activities. Generally business finance could be elaborated as provision of money at time when its

is essential through business. The present report is all about UberTools Ltd and Madagascar

Industries Ltd as with profit and Cash flow, working capital, receivables, inventory and payables.

It will reflect about impact on cash flow with changes in working capital and recommendation

about steps could be undertaken for improving cash flow of company via better working capital

management. On basis of Madagascar Industries Ltd each element of financial performance

would be described along with ratio analysis of over past three years. Lastly, this report would

analyse and recommendation with reference to business's financial performance.

PART 1

1.1 Explain

1.1.a Profit and cash flow with their difference

Cash flow is replicated as money which flows in and out of business by its investing,

operations and financing activities. This is the money which is required for accomplishing near

term and current obligations. Profit is also known as net income as it remains through sales

revenue as each expense of firm is excluded (Aktas, Croci and Petmezas, 2015).

The organization could have positive cash flow as with absence of margin if cash

originates through sources instead of income like when any owner puts their own money or for

undertaking loan. These types of particular transaction are not known as income but instead of

equity or liability transactions which is reflected on balance sheet.

1.1.b Working capital, receivables, inventory and payables

Working capital is referred as financial metric which reflects availability of liquidity to

business, organization along with other entity as well. It shows short term financial position of

organisation and measures overall efficiency (Working capital, 2014). Elements of working

capital mainly includes inventory, receivables and payable period.

Receivables is replicated as amount owned through company with outcome of company

offering goods, credit or services. Mostly, amount of company is directly owed and recorded in

general ledger account which is entitled in Accounts Receivable. Furthermore, unpaid balance in

these accounts is accounted as contribution of current assets listed on balance sheet of company.

1

Business finance is replicated as money and credit employed in business as its basic is

finance. Finance is need for buying assets, raw materials along with other flow of economic

activities. Generally business finance could be elaborated as provision of money at time when its

is essential through business. The present report is all about UberTools Ltd and Madagascar

Industries Ltd as with profit and Cash flow, working capital, receivables, inventory and payables.

It will reflect about impact on cash flow with changes in working capital and recommendation

about steps could be undertaken for improving cash flow of company via better working capital

management. On basis of Madagascar Industries Ltd each element of financial performance

would be described along with ratio analysis of over past three years. Lastly, this report would

analyse and recommendation with reference to business's financial performance.

PART 1

1.1 Explain

1.1.a Profit and cash flow with their difference

Cash flow is replicated as money which flows in and out of business by its investing,

operations and financing activities. This is the money which is required for accomplishing near

term and current obligations. Profit is also known as net income as it remains through sales

revenue as each expense of firm is excluded (Aktas, Croci and Petmezas, 2015).

The organization could have positive cash flow as with absence of margin if cash

originates through sources instead of income like when any owner puts their own money or for

undertaking loan. These types of particular transaction are not known as income but instead of

equity or liability transactions which is reflected on balance sheet.

1.1.b Working capital, receivables, inventory and payables

Working capital is referred as financial metric which reflects availability of liquidity to

business, organization along with other entity as well. It shows short term financial position of

organisation and measures overall efficiency (Working capital, 2014). Elements of working

capital mainly includes inventory, receivables and payable period.

Receivables is replicated as amount owned through company with outcome of company

offering goods, credit or services. Mostly, amount of company is directly owed and recorded in

general ledger account which is entitled in Accounts Receivable. Furthermore, unpaid balance in

these accounts is accounted as contribution of current assets listed on balance sheet of company.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory is considered as collection of unsold products which are waiting to be sold

and it is listed on balance sheet of company as current asset. This is common thought for finished

goods which are accumulated prior to selling to end users. Simultaneously, it could also describe

raw materials implied for generating finished goods and goods which go by process of

production or goods which are in transit.

Payables is short term obligation for repaying creditors and suppliers for purpose of

goods and services bought on credit rather than cash. This is referred as accounting entry which

reflects obligation of company for repaying short term debt and appears on balance sheet under

current liabilities.

1.1.c Impact of alteration in working capital on cash flow

Alterations in working capital impacts cash flow statement of business as if

transaction raises current assets and liabilities by similar amount then this would not impact. For

instance organization has purchased any fixed asset then cash flow of company would fall. In

this aspect, working capital of company would also fall as cash portion of current assets would

be deceased but there would be no change in current liabilities as it would be replicated as long

term debt. Simultaneously, selling of fixed asset would directly boost working capital and cash

flow. Conversely, organisation purchased any inventory with cash, then there would be absence

in working capital due to cash and inventory both are replicated as current assets (Analysing and

Interpreting Financial Statements, 2014). On the contrary, cash flow would be reduced through

purchase of inventory.

1.2 Application of above concept and managing might impact financial outcome

Managing cash flow:

Cash flows should be managed effectively it shows that debts must be collected by

aligning agreed credit terms along with cash on quickly banked. As prompt banking would either

decrease charged interest or with outstanding overdraft with increment in earned interest on cash

deposits. The credit offered through suppliers must be used to payments made as late as it could,

offered the benefit of particular actions are higher than benefit undertaking with availability of

payment discounts.

Managing Inventory:

The significant amount of working capital could be invested within inventories related to

raw materials, finished goods and work in progress. As inventories of raw materials and work in

2

and it is listed on balance sheet of company as current asset. This is common thought for finished

goods which are accumulated prior to selling to end users. Simultaneously, it could also describe

raw materials implied for generating finished goods and goods which go by process of

production or goods which are in transit.

Payables is short term obligation for repaying creditors and suppliers for purpose of

goods and services bought on credit rather than cash. This is referred as accounting entry which

reflects obligation of company for repaying short term debt and appears on balance sheet under

current liabilities.

1.1.c Impact of alteration in working capital on cash flow

Alterations in working capital impacts cash flow statement of business as if

transaction raises current assets and liabilities by similar amount then this would not impact. For

instance organization has purchased any fixed asset then cash flow of company would fall. In

this aspect, working capital of company would also fall as cash portion of current assets would

be deceased but there would be no change in current liabilities as it would be replicated as long

term debt. Simultaneously, selling of fixed asset would directly boost working capital and cash

flow. Conversely, organisation purchased any inventory with cash, then there would be absence

in working capital due to cash and inventory both are replicated as current assets (Analysing and

Interpreting Financial Statements, 2014). On the contrary, cash flow would be reduced through

purchase of inventory.

1.2 Application of above concept and managing might impact financial outcome

Managing cash flow:

Cash flows should be managed effectively it shows that debts must be collected by

aligning agreed credit terms along with cash on quickly banked. As prompt banking would either

decrease charged interest or with outstanding overdraft with increment in earned interest on cash

deposits. The credit offered through suppliers must be used to payments made as late as it could,

offered the benefit of particular actions are higher than benefit undertaking with availability of

payment discounts.

Managing Inventory:

The significant amount of working capital could be invested within inventories related to

raw materials, finished goods and work in progress. As inventories of raw materials and work in

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

progress might act as buffer among process multiple production stages as it ensures about

smooth operation. Furthermore, inventory of finished goods directly allows department of sales

for satisfying customer demand with absence of unreasonable delay along with potential loss of

sales. Alterations in inventory and inappropriate balance impact balance sheets, financial

statement which is snapshot of worth of company on basis of assets and liabilities. This could

give outcome in inaccurate reported assets value along with owner's equity on balance sheet.

Managing receivables:

The policy of credit management must help for maximising the expected margin. The

policy would account current and desired cash proportion of company as with ability for

satisfying the expected demand. On basis of adapting credit management policy, managers and

staff might be in need of training or new staff must be required. The key variables which are

impacting receivables level would be in terms for sale of prevailing in business area with ability

for matching the service comparable terms of sale. It would impact net worth on positive aspect

in financials, but it might run into difficulties to recoup daily expenses.

Managing payables:

The business which purchases supplies on credit might incur additional administration

along with accounting cost resulting through payment and scrutiny of invoices, updating and

maintaining payable accounts. In case customers who takes credit might be not treated well

comparatively to immediate payers.

By doing evaluation of case study, it has assessed that ineffectual working capital

management closely impacts financial results. Cited case situation clearly presents that

customers are not making payment on time. This is one of the main aspect which in turn affected

both Uber’s working capital management and thereby cash flow. Moreover, when company

receives payment from customers late then it faces difficulty in capitalizing opportunity. In other

words, when business unit receives payment from customers on time then it has opportunity to

invest money in other profitable activities. This in turn assists Uber Tools ltd in increasing the

level of income and thereby overall inflow. Further, high level of bad-debt is the main reason due

to which company’s cash position affected negatively. Hence, for better working capital

management emphasis needs to be placed on making lower inventory period and debtor’s

receivable period.

3

smooth operation. Furthermore, inventory of finished goods directly allows department of sales

for satisfying customer demand with absence of unreasonable delay along with potential loss of

sales. Alterations in inventory and inappropriate balance impact balance sheets, financial

statement which is snapshot of worth of company on basis of assets and liabilities. This could

give outcome in inaccurate reported assets value along with owner's equity on balance sheet.

Managing receivables:

The policy of credit management must help for maximising the expected margin. The

policy would account current and desired cash proportion of company as with ability for

satisfying the expected demand. On basis of adapting credit management policy, managers and

staff might be in need of training or new staff must be required. The key variables which are

impacting receivables level would be in terms for sale of prevailing in business area with ability

for matching the service comparable terms of sale. It would impact net worth on positive aspect

in financials, but it might run into difficulties to recoup daily expenses.

Managing payables:

The business which purchases supplies on credit might incur additional administration

along with accounting cost resulting through payment and scrutiny of invoices, updating and

maintaining payable accounts. In case customers who takes credit might be not treated well

comparatively to immediate payers.

By doing evaluation of case study, it has assessed that ineffectual working capital

management closely impacts financial results. Cited case situation clearly presents that

customers are not making payment on time. This is one of the main aspect which in turn affected

both Uber’s working capital management and thereby cash flow. Moreover, when company

receives payment from customers late then it faces difficulty in capitalizing opportunity. In other

words, when business unit receives payment from customers on time then it has opportunity to

invest money in other profitable activities. This in turn assists Uber Tools ltd in increasing the

level of income and thereby overall inflow. Further, high level of bad-debt is the main reason due

to which company’s cash position affected negatively. Hence, for better working capital

management emphasis needs to be placed on making lower inventory period and debtor’s

receivable period.

3

1.3 Analysing and recommending steps must be undertaken for improving cash flow of company

via better working capital management

It had been analysed that cash flow could be improved my management of working

capital and it has been recommended that:

Appropriate review of income statement and balance sheet is very significant but

understanding of cash flow would help business for better understanding of sources and

application of cash at specific time duration.

There must active management of cash payments as advantage could be undertaken for

discounted payment terms with allowance of cash flow. In this aspect, application of

credit cards must be performed with failure caution for paying bills of credit cards would

continue for draining cash flow (Working Capital, 2016).

On the basis of given case scenario, cash flow of the company negatively affected due to

the rising level of bad debt. Hence, Uber Tools Ltd should focus on checking the credit

rating of customers. This in turn helps in reducing the level of bad debts and ensure

proper management of cash flow.

Along with this, Uber Tools is recommended to employ inventory management aspects

and promotional tools. Through this, company would become able to sell and replace its

inventory quickly. This in turn facilitates high inflow and cash flow management as well.

Furthermore, monthly expense must be managed as per need it could be reduced.

The receivables could be collected on timely basis and clients must be ensure about

payment terms. Hence, manager of Uber tools ltd should focus on decreasing debtor’s

collection period, and increasing the time frame associated with payables. Through this,

business unit can manage its cash flow in the best possible way.

The collection process must be reviewed and each required information must be ensured

where per customer is on bill for eliminating confusion and payment delay.

Hence, by undertaking all the above depicted working capital management strategies Uber

tools ltd can improve its cash flow to a great extent.

4

via better working capital management

It had been analysed that cash flow could be improved my management of working

capital and it has been recommended that:

Appropriate review of income statement and balance sheet is very significant but

understanding of cash flow would help business for better understanding of sources and

application of cash at specific time duration.

There must active management of cash payments as advantage could be undertaken for

discounted payment terms with allowance of cash flow. In this aspect, application of

credit cards must be performed with failure caution for paying bills of credit cards would

continue for draining cash flow (Working Capital, 2016).

On the basis of given case scenario, cash flow of the company negatively affected due to

the rising level of bad debt. Hence, Uber Tools Ltd should focus on checking the credit

rating of customers. This in turn helps in reducing the level of bad debts and ensure

proper management of cash flow.

Along with this, Uber Tools is recommended to employ inventory management aspects

and promotional tools. Through this, company would become able to sell and replace its

inventory quickly. This in turn facilitates high inflow and cash flow management as well.

Furthermore, monthly expense must be managed as per need it could be reduced.

The receivables could be collected on timely basis and clients must be ensure about

payment terms. Hence, manager of Uber tools ltd should focus on decreasing debtor’s

collection period, and increasing the time frame associated with payables. Through this,

business unit can manage its cash flow in the best possible way.

The collection process must be reviewed and each required information must be ensured

where per customer is on bill for eliminating confusion and payment delay.

Hence, by undertaking all the above depicted working capital management strategies Uber

tools ltd can improve its cash flow to a great extent.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART 2

2.1 On basis of financial ratios

2.1.a Explaining element of financial performance

Ratio analysis may be presented as a quantitative tool which enables firm and its

stakeholders to evaluate financial performance from several perspective such as liquidity,

profitability, efficiency, gearing etc. Hence, using such technique firm can measure and evaluate

its performance over the years and thereby would become able to take strategic measure or

action within the suitable time period.

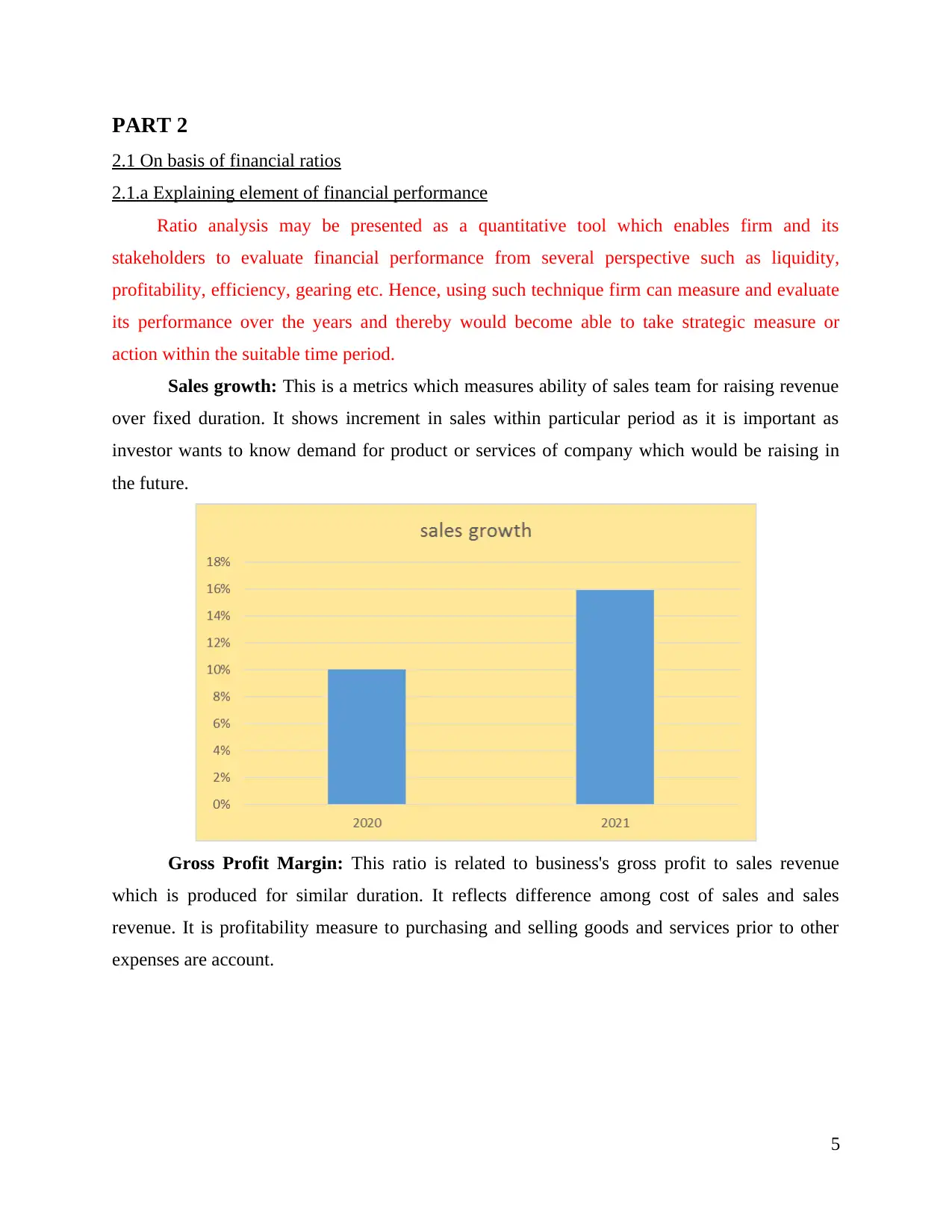

Sales growth: This is a metrics which measures ability of sales team for raising revenue

over fixed duration. It shows increment in sales within particular period as it is important as

investor wants to know demand for product or services of company which would be raising in

the future.

Gross Profit Margin: This ratio is related to business's gross profit to sales revenue

which is produced for similar duration. It reflects difference among cost of sales and sales

revenue. It is profitability measure to purchasing and selling goods and services prior to other

expenses are account.

5

2.1 On basis of financial ratios

2.1.a Explaining element of financial performance

Ratio analysis may be presented as a quantitative tool which enables firm and its

stakeholders to evaluate financial performance from several perspective such as liquidity,

profitability, efficiency, gearing etc. Hence, using such technique firm can measure and evaluate

its performance over the years and thereby would become able to take strategic measure or

action within the suitable time period.

Sales growth: This is a metrics which measures ability of sales team for raising revenue

over fixed duration. It shows increment in sales within particular period as it is important as

investor wants to know demand for product or services of company which would be raising in

the future.

Gross Profit Margin: This ratio is related to business's gross profit to sales revenue

which is produced for similar duration. It reflects difference among cost of sales and sales

revenue. It is profitability measure to purchasing and selling goods and services prior to other

expenses are account.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Operating Profit Margin: It is related to operating margin for duration to the sales

revenue. Generally, it is used in ratio which reflects profit by trading operation before interest

payable expense. Hence, it clearly presents profit margin generated by the firm over indirect

expenses incurred.

Gearing ratio: This ratio directly measures contribution for long term lenders to long

term structure of business (Ratio Analysis, 2017). Generally, level of gearing would not be

normally be considered as very high. Such ratio clearly presents the extent to which capital

structure followed by the firm is sound.

6

revenue. Generally, it is used in ratio which reflects profit by trading operation before interest

payable expense. Hence, it clearly presents profit margin generated by the firm over indirect

expenses incurred.

Gearing ratio: This ratio directly measures contribution for long term lenders to long

term structure of business (Ratio Analysis, 2017). Generally, level of gearing would not be

normally be considered as very high. Such ratio clearly presents the extent to which capital

structure followed by the firm is sound.

6

Interest Coverage ratio: This ratio measures availability of amount of operating profit

for purpose of covering interest payable. It elaborates that level of operating profit could incur

prior to level of operating profit failed for covering interest payable. There would be greater risk

to shareholders that lenders would undertake action to recouping due interest.

Liquidity Ratio: This is directly concerned with business ability for meeting short term

financial obligations as here it is performed with current ratio. This provides comparison of

liquid assets with context to current liabilities. The higher current ratio then there is more liquid

business as liquidity is vital for business survival. In other words, current ratio presents

company’s ability in relation meeting obligations from assets level maintained within the firm.

7

for purpose of covering interest payable. It elaborates that level of operating profit could incur

prior to level of operating profit failed for covering interest payable. There would be greater risk

to shareholders that lenders would undertake action to recouping due interest.

Liquidity Ratio: This is directly concerned with business ability for meeting short term

financial obligations as here it is performed with current ratio. This provides comparison of

liquid assets with context to current liabilities. The higher current ratio then there is more liquid

business as liquidity is vital for business survival. In other words, current ratio presents

company’s ability in relation meeting obligations from assets level maintained within the firm.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By taking into account such ratio firm can evaluate its working capital management and thereby

would become able to formulate competent strategic and policy framework.

Return on equity: It is measured as profitability of company of annual return which is

divided through value of total shareholder's equity. This helps in evaluating returns as it gives

insight about management of company with application of funding through equity for business

growth. ROE assists in measuring company’s ability in relation to using shareholders’ funds

while carry out business activities and functions.

Return on Capital Employed: This is fundamental measure of business performance as

it shows relationship among operating margin generated during period along with average long

8

would become able to formulate competent strategic and policy framework.

Return on equity: It is measured as profitability of company of annual return which is

divided through value of total shareholder's equity. This helps in evaluating returns as it gives

insight about management of company with application of funding through equity for business

growth. ROE assists in measuring company’s ability in relation to using shareholders’ funds

while carry out business activities and functions.

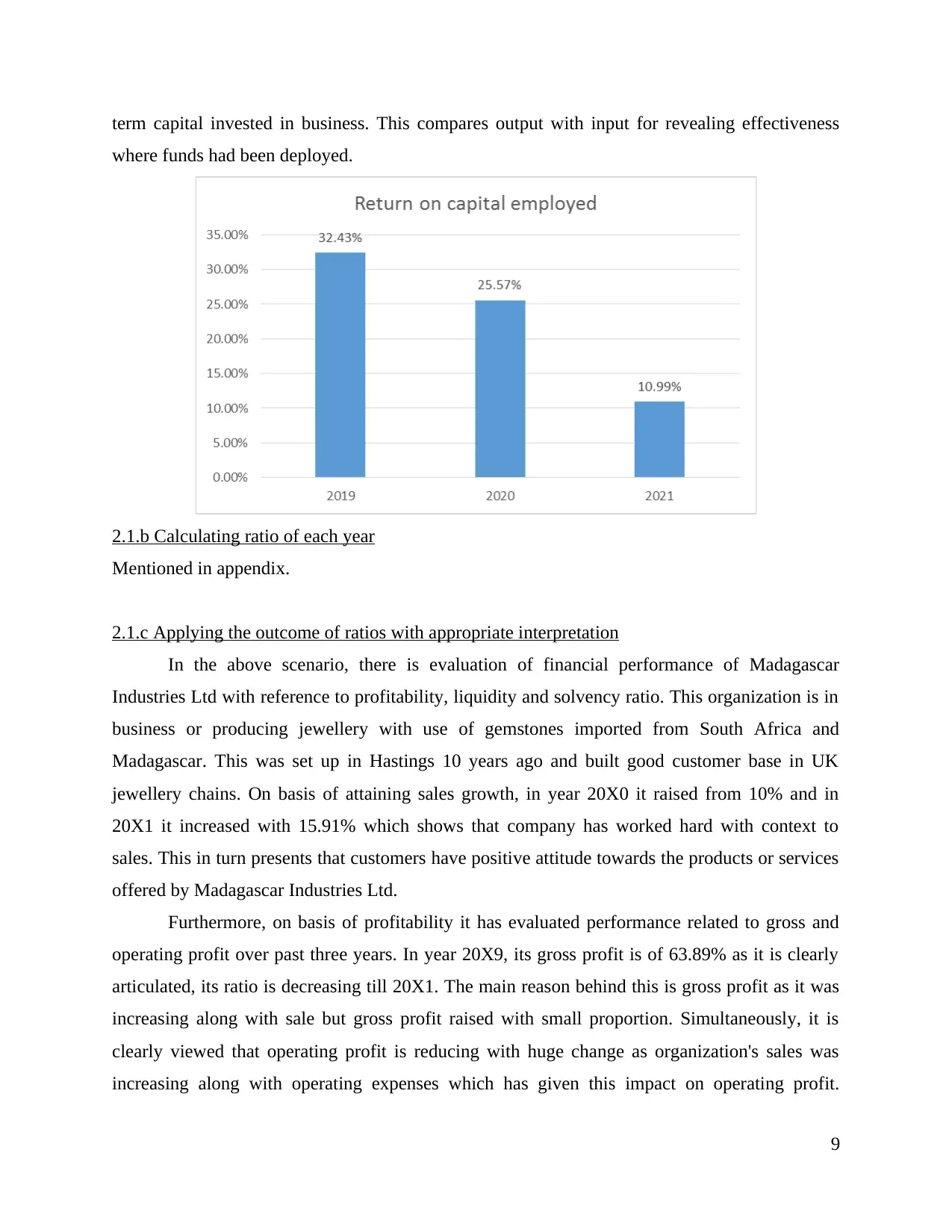

Return on Capital Employed: This is fundamental measure of business performance as

it shows relationship among operating margin generated during period along with average long

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

term capital invested in business. This compares output with input for revealing effectiveness

where funds had been deployed.

2.1.b Calculating ratio of each year

Mentioned in appendix.

2.1.c Applying the outcome of ratios with appropriate interpretation

In the above scenario, there is evaluation of financial performance of Madagascar

Industries Ltd with reference to profitability, liquidity and solvency ratio. This organization is in

business or producing jewellery with use of gemstones imported from South Africa and

Madagascar. This was set up in Hastings 10 years ago and built good customer base in UK

jewellery chains. On basis of attaining sales growth, in year 20X0 it raised from 10% and in

20X1 it increased with 15.91% which shows that company has worked hard with context to

sales. This in turn presents that customers have positive attitude towards the products or services

offered by Madagascar Industries Ltd.

Furthermore, on basis of profitability it has evaluated performance related to gross and

operating profit over past three years. In year 20X9, its gross profit is of 63.89% as it is clearly

articulated, its ratio is decreasing till 20X1. The main reason behind this is gross profit as it was

increasing along with sale but gross profit raised with small proportion. Simultaneously, it is

clearly viewed that operating profit is reducing with huge change as organization's sales was

increasing along with operating expenses which has given this impact on operating profit.

9

where funds had been deployed.

2.1.b Calculating ratio of each year

Mentioned in appendix.

2.1.c Applying the outcome of ratios with appropriate interpretation

In the above scenario, there is evaluation of financial performance of Madagascar

Industries Ltd with reference to profitability, liquidity and solvency ratio. This organization is in

business or producing jewellery with use of gemstones imported from South Africa and

Madagascar. This was set up in Hastings 10 years ago and built good customer base in UK

jewellery chains. On basis of attaining sales growth, in year 20X0 it raised from 10% and in

20X1 it increased with 15.91% which shows that company has worked hard with context to

sales. This in turn presents that customers have positive attitude towards the products or services

offered by Madagascar Industries Ltd.

Furthermore, on basis of profitability it has evaluated performance related to gross and

operating profit over past three years. In year 20X9, its gross profit is of 63.89% as it is clearly

articulated, its ratio is decreasing till 20X1. The main reason behind this is gross profit as it was

increasing along with sale but gross profit raised with small proportion. Simultaneously, it is

clearly viewed that operating profit is reducing with huge change as organization's sales was

increasing along with operating expenses which has given this impact on operating profit.

9

Referring the level of gross and net profit margin, it can be presented that direct as well indirect

expenses level of company is higher during the particular time frame.

By observing gearing ratio, it is increasing because of increasing debt and shareholder's

fund does not have major change. Its liquidity ratio says that in year 20X9 and 20X0 it was

capable but in 20X1, its current liabilities raise so current ratio was not optimum. In 2019,

current ratio of Madagascar Industries Ltd accounts for 2.24 respectively, whereas at the end of

2021 it reached on .92. On the basis of ideal liquidity framework, firm must have 2 current assets

in against to 1 liability. Accordingly, Madagascar Industries Ltd fails to maintain enough assets

within the firm in against to the present obligations. Moreover, return on equity was also

decreasing because in 20X1 company was not capable for give high returns comparatively to

previous year. Lastly, it was not able to produce high returns on employed capital because of

non-acceptable changes as decreasing operating profit and high debt but with constant

shareholders fund. Hence, outcome of ratio analysis clearly exhibits that Madagascar Industries

Ltd fails to generate suitable returns by using shareholders equity and capital employed.

2.2 Analysing and recommending board for assessing business's financial performance

It had been analysed that board should assess financial performance of Madagascar

Industries Ltd with evaluation of financial ratios over past three years. As it has been observed

that its sales has attained growth but rather than this each measure was decreasing. It has been

recommended that it should keep appropriate track of its cost of sales which is raised in 20X1

with high proportion (Assessing Financial Performance, 2016). Simultaneously, with reference

to operating profit margin, the company has incurred high operating expenses which is bad

signal for company so in all, it must be capable for monitoring its expenses in coming year.

In the same series, while evaluating financial performance of Madagascar Industries Ltd,

there is presence of high accumulated depreciation as its cash position in 20X1 was 0 which

shows poor liquidity. It has acquired more fixed assets which must adopt appropriate planning

however, it has undertaken huge debts which move towards decrement in losses. Thus, it had

been recommended that each ratio with financial standards must be in mind as it helps in

determining financial performance.

In addition to this, company should focus on undertaking promotional plans or campaign

which helps in influencing customer decision making and thereby ensures enhancement

of customer base.

10

expenses level of company is higher during the particular time frame.

By observing gearing ratio, it is increasing because of increasing debt and shareholder's

fund does not have major change. Its liquidity ratio says that in year 20X9 and 20X0 it was

capable but in 20X1, its current liabilities raise so current ratio was not optimum. In 2019,

current ratio of Madagascar Industries Ltd accounts for 2.24 respectively, whereas at the end of

2021 it reached on .92. On the basis of ideal liquidity framework, firm must have 2 current assets

in against to 1 liability. Accordingly, Madagascar Industries Ltd fails to maintain enough assets

within the firm in against to the present obligations. Moreover, return on equity was also

decreasing because in 20X1 company was not capable for give high returns comparatively to

previous year. Lastly, it was not able to produce high returns on employed capital because of

non-acceptable changes as decreasing operating profit and high debt but with constant

shareholders fund. Hence, outcome of ratio analysis clearly exhibits that Madagascar Industries

Ltd fails to generate suitable returns by using shareholders equity and capital employed.

2.2 Analysing and recommending board for assessing business's financial performance

It had been analysed that board should assess financial performance of Madagascar

Industries Ltd with evaluation of financial ratios over past three years. As it has been observed

that its sales has attained growth but rather than this each measure was decreasing. It has been

recommended that it should keep appropriate track of its cost of sales which is raised in 20X1

with high proportion (Assessing Financial Performance, 2016). Simultaneously, with reference

to operating profit margin, the company has incurred high operating expenses which is bad

signal for company so in all, it must be capable for monitoring its expenses in coming year.

In the same series, while evaluating financial performance of Madagascar Industries Ltd,

there is presence of high accumulated depreciation as its cash position in 20X1 was 0 which

shows poor liquidity. It has acquired more fixed assets which must adopt appropriate planning

however, it has undertaken huge debts which move towards decrement in losses. Thus, it had

been recommended that each ratio with financial standards must be in mind as it helps in

determining financial performance.

In addition to this, company should focus on undertaking promotional plans or campaign

which helps in influencing customer decision making and thereby ensures enhancement

of customer base.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.