MDL Ltd. Finance Report: Working Capital and Budgeting Methods

VerifiedAdded on 2023/01/12

|13

|3471

|41

Report

AI Summary

This report provides a comprehensive analysis of key business finance concepts, focusing on the differences between profit and cash flow and the importance of effective working capital management. It examines the impact of changes in working capital on a business's cash flow, offering practical steps to improve cash flow through strategic management of receivables, inventory, and payables. The report also delves into various budgeting methods, evaluating their strengths and weaknesses, and recommends the most appropriate budgeting approach, specifically activity-based budgeting, for Second Sight Plc's future business plan. The report uses the scenario of MDL Ltd. to illustrate financial challenges and propose solutions, including improving accounts receivable, negotiating with suppliers, and optimizing inventory levels to ensure financial stability and growth. The analysis underscores the importance of proactive financial management and the adoption of suitable budgeting techniques to achieve financial goals.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1.........................................................................................................................................................3

a. Difference between profit and cash flow.............................................................................................3

b. Meaning of working capital, receivables, inventory and payables......................................................3

c. Effect of change in working capital on cash flow of the business........................................................4

How company is managed that might affect its financial results............................................................4

Steps that can be taken to improve the cash flow by effective management of working capital............4

PART 2.........................................................................................................................................................7

Different methods of preparing budget..................................................................................................7

Application of budgeting methods on Second Sight Plc for future plan..................................................8

Analysing the appropriate method of budgeting.....................................................................................9

REFERENCES..............................................................................................................................................11

PART 1.........................................................................................................................................................3

a. Difference between profit and cash flow.............................................................................................3

b. Meaning of working capital, receivables, inventory and payables......................................................3

c. Effect of change in working capital on cash flow of the business........................................................4

How company is managed that might affect its financial results............................................................4

Steps that can be taken to improve the cash flow by effective management of working capital............4

PART 2.........................................................................................................................................................7

Different methods of preparing budget..................................................................................................7

Application of budgeting methods on Second Sight Plc for future plan..................................................8

Analysing the appropriate method of budgeting.....................................................................................9

REFERENCES..............................................................................................................................................11

EXECUTIVE SUMMARY

In this report, the basic financial are discussed with respect the scenario of MDL Ltd. It presents

the impact of change in working capital on the cash flow of the business and also what are the

steps that can eb taken to improve the cash flow position of the business. Based on the various

strategies were identified which should be used by MDL Ltd.

In this report, the basic financial are discussed with respect the scenario of MDL Ltd. It presents

the impact of change in working capital on the cash flow of the business and also what are the

steps that can eb taken to improve the cash flow position of the business. Based on the various

strategies were identified which should be used by MDL Ltd.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART 1

i.

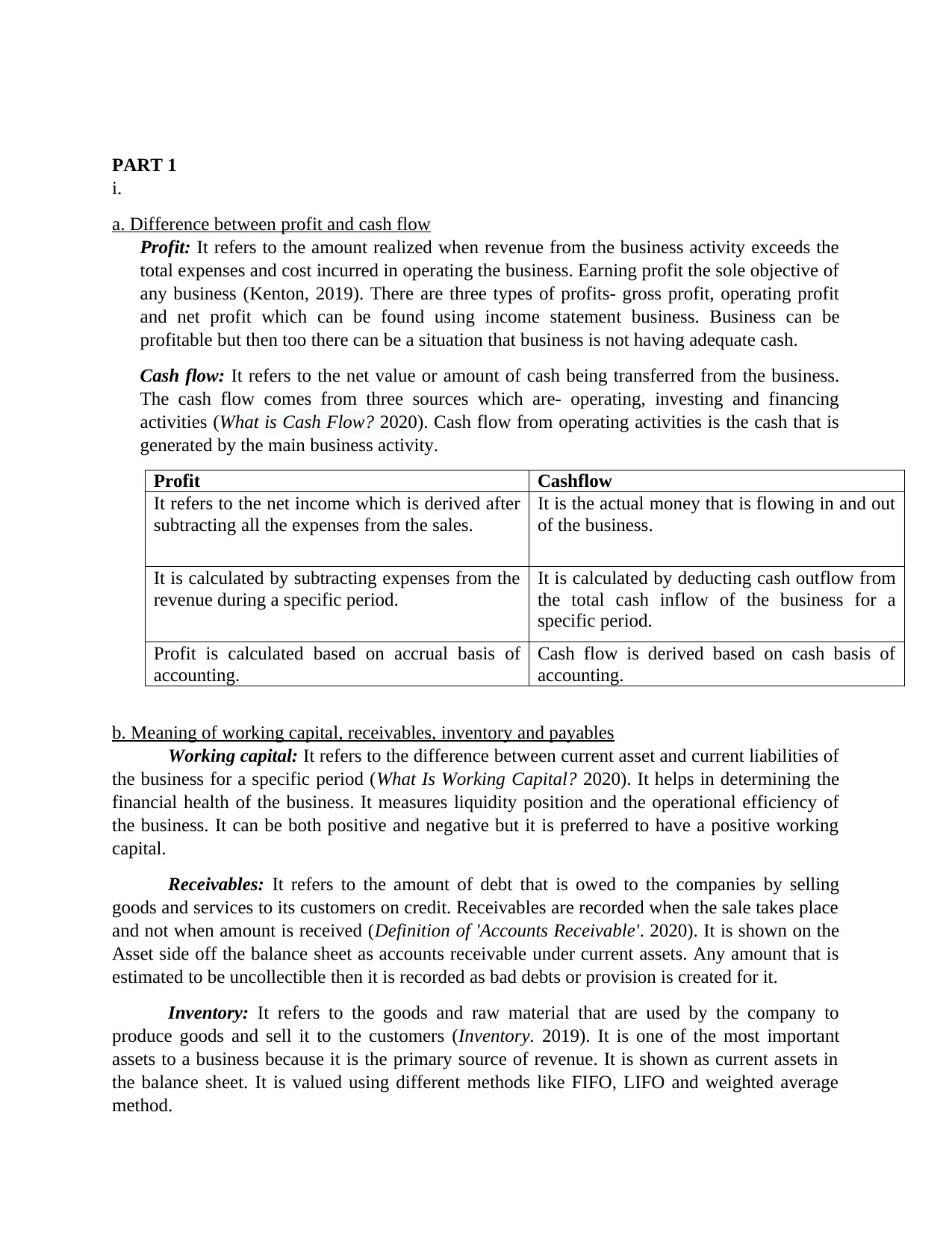

a. Difference between profit and cash flow

Profit: It refers to the amount realized when revenue from the business activity exceeds the

total expenses and cost incurred in operating the business. Earning profit the sole objective of

any business (Kenton, 2019). There are three types of profits- gross profit, operating profit

and net profit which can be found using income statement business. Business can be

profitable but then too there can be a situation that business is not having adequate cash.

Cash flow: It refers to the net value or amount of cash being transferred from the business.

The cash flow comes from three sources which are- operating, investing and financing

activities (What is Cash Flow? 2020). Cash flow from operating activities is the cash that is

generated by the main business activity.

Profit Cashflow

It refers to the net income which is derived after

subtracting all the expenses from the sales.

It is the actual money that is flowing in and out

of the business.

It is calculated by subtracting expenses from the

revenue during a specific period.

It is calculated by deducting cash outflow from

the total cash inflow of the business for a

specific period.

Profit is calculated based on accrual basis of

accounting.

Cash flow is derived based on cash basis of

accounting.

b. Meaning of working capital, receivables, inventory and payables

Working capital: It refers to the difference between current asset and current liabilities of

the business for a specific period (What Is Working Capital? 2020). It helps in determining the

financial health of the business. It measures liquidity position and the operational efficiency of

the business. It can be both positive and negative but it is preferred to have a positive working

capital.

Receivables: It refers to the amount of debt that is owed to the companies by selling

goods and services to its customers on credit. Receivables are recorded when the sale takes place

and not when amount is received (Definition of 'Accounts Receivable'. 2020). It is shown on the

Asset side off the balance sheet as accounts receivable under current assets. Any amount that is

estimated to be uncollectible then it is recorded as bad debts or provision is created for it.

Inventory: It refers to the goods and raw material that are used by the company to

produce goods and sell it to the customers (Inventory. 2019). It is one of the most important

assets to a business because it is the primary source of revenue. It is shown as current assets in

the balance sheet. It is valued using different methods like FIFO, LIFO and weighted average

method.

i.

a. Difference between profit and cash flow

Profit: It refers to the amount realized when revenue from the business activity exceeds the

total expenses and cost incurred in operating the business. Earning profit the sole objective of

any business (Kenton, 2019). There are three types of profits- gross profit, operating profit

and net profit which can be found using income statement business. Business can be

profitable but then too there can be a situation that business is not having adequate cash.

Cash flow: It refers to the net value or amount of cash being transferred from the business.

The cash flow comes from three sources which are- operating, investing and financing

activities (What is Cash Flow? 2020). Cash flow from operating activities is the cash that is

generated by the main business activity.

Profit Cashflow

It refers to the net income which is derived after

subtracting all the expenses from the sales.

It is the actual money that is flowing in and out

of the business.

It is calculated by subtracting expenses from the

revenue during a specific period.

It is calculated by deducting cash outflow from

the total cash inflow of the business for a

specific period.

Profit is calculated based on accrual basis of

accounting.

Cash flow is derived based on cash basis of

accounting.

b. Meaning of working capital, receivables, inventory and payables

Working capital: It refers to the difference between current asset and current liabilities of

the business for a specific period (What Is Working Capital? 2020). It helps in determining the

financial health of the business. It measures liquidity position and the operational efficiency of

the business. It can be both positive and negative but it is preferred to have a positive working

capital.

Receivables: It refers to the amount of debt that is owed to the companies by selling

goods and services to its customers on credit. Receivables are recorded when the sale takes place

and not when amount is received (Definition of 'Accounts Receivable'. 2020). It is shown on the

Asset side off the balance sheet as accounts receivable under current assets. Any amount that is

estimated to be uncollectible then it is recorded as bad debts or provision is created for it.

Inventory: It refers to the goods and raw material that are used by the company to

produce goods and sell it to the customers (Inventory. 2019). It is one of the most important

assets to a business because it is the primary source of revenue. It is shown as current assets in

the balance sheet. It is valued using different methods like FIFO, LIFO and weighted average

method.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Payables: It is the reverse of receivables. It presents the company’s obligation to pay the debt to

it’s creditors and other vendors from whom materials are purchased on credit. In big

organizations, there is a separate department for it for making payment to the creditors as and

when due date comes (Accounts Payable. 2020). It appears in the balance sheet as accounts

payable under current liabilities. It is very essential to manage accounts payable which will result

effective management of cash.

c. Effect of change in working capital on cash flow of the business

There is a direct impact of change in working capital on the cashflow of the business. A

positive change in working capital means that there is a cash inflow for that period. On the other

hand, a negative change in working capital will mean that the company has spend more cash.

The increase in working capital shows that management is investing its resources in the short

term which results in decrease in cash flow (Afrifa and Tingbani, 2018). On the contrast,

negative change in working capital will show that it business has heavily relied on short term

borrowings in order to finance its business which resulted in increase in cashflow. For example,

purchase of inventory with cash would have no impact on the working capital as both cash and

inventory are current assets but the cashflow for the business will be reduced by the amount of

inventory purchased. Thus, analyzing working capital is very important.

ii.

How company is managed that might affect its financial results

MDL Ltd is currently having reasonable amount of profits from its business but on the

other hand it has increased its debt to £18 million. Also, it has acquired 40% stake in Italian

company and has further invested £10 million for acquiring shares of it. MDL Ltd has an dispute

of about £2 million. There are chances that another legal dispute may arise as it has refused to

pay Valetta for providing poor quality of materials. It also has large stock of materials and other

supplies which things will be required after resolving the disputes. MDL is also very lenient in

terms of collecting money from the customers. After considering the current situation of the

company it can be said that if the company does not take any initiative then it will have negative

impact on its financial position. For example, it should be hard enough to recover money blocked

by customers and look for other investors for paying back its debt. Another important thing it can

do is to stop making any further investment. Otherwise, it will be left with no cash and negative

working capital.

iii.

Steps that can be taken to improve the cash flow by effective management of working capital

Working capital is very important for the daily operation of the business. It becomes very

crucial for businesses to effectively manage it’s working capital and maintaining the balance

(Singhania and Mehta, 2017). Below are the few essential steps that can be taken by the

company in order to improve its working capital which will further lead to positive cash flow

management.

MDL Ltd can implement an automated system which will help the company in effective

management of account receivables by reminding the customers to pay on time.

it’s creditors and other vendors from whom materials are purchased on credit. In big

organizations, there is a separate department for it for making payment to the creditors as and

when due date comes (Accounts Payable. 2020). It appears in the balance sheet as accounts

payable under current liabilities. It is very essential to manage accounts payable which will result

effective management of cash.

c. Effect of change in working capital on cash flow of the business

There is a direct impact of change in working capital on the cashflow of the business. A

positive change in working capital means that there is a cash inflow for that period. On the other

hand, a negative change in working capital will mean that the company has spend more cash.

The increase in working capital shows that management is investing its resources in the short

term which results in decrease in cash flow (Afrifa and Tingbani, 2018). On the contrast,

negative change in working capital will show that it business has heavily relied on short term

borrowings in order to finance its business which resulted in increase in cashflow. For example,

purchase of inventory with cash would have no impact on the working capital as both cash and

inventory are current assets but the cashflow for the business will be reduced by the amount of

inventory purchased. Thus, analyzing working capital is very important.

ii.

How company is managed that might affect its financial results

MDL Ltd is currently having reasonable amount of profits from its business but on the

other hand it has increased its debt to £18 million. Also, it has acquired 40% stake in Italian

company and has further invested £10 million for acquiring shares of it. MDL Ltd has an dispute

of about £2 million. There are chances that another legal dispute may arise as it has refused to

pay Valetta for providing poor quality of materials. It also has large stock of materials and other

supplies which things will be required after resolving the disputes. MDL is also very lenient in

terms of collecting money from the customers. After considering the current situation of the

company it can be said that if the company does not take any initiative then it will have negative

impact on its financial position. For example, it should be hard enough to recover money blocked

by customers and look for other investors for paying back its debt. Another important thing it can

do is to stop making any further investment. Otherwise, it will be left with no cash and negative

working capital.

iii.

Steps that can be taken to improve the cash flow by effective management of working capital

Working capital is very important for the daily operation of the business. It becomes very

crucial for businesses to effectively manage it’s working capital and maintaining the balance

(Singhania and Mehta, 2017). Below are the few essential steps that can be taken by the

company in order to improve its working capital which will further lead to positive cash flow

management.

MDL Ltd can implement an automated system which will help the company in effective

management of account receivables by reminding the customers to pay on time.

The company motivate and encourage its customers to pay before due date by offering

them incentives. Also, it should motivate its collection team by offering them incentives

by collecting outstanding invoices on time.

MDL Ltd should review different suppliers and negotiate for better pricing and if if the

supplier is not willing to come to a favorable term Then it should look for other suppliers.

The company should look for better payment terms with suppliers and other vendors

which will help in effective management of payment process. Also, balance should be

maintained in the payment terms for both accounts payable and accounts receivable.

It should use electronic payment system which will help in in ensuring that timely

payments are done and also helps in avoiding the situation of delay payments which will

attract penalty.

MDL should examine the amount of interest on the loans taken and also if possible can

any modification in interest rate and installment payment can be done or not. This will

help in reducing the cost of paying principal amount which can be termed as savings and

added to working capital.

It should avoid the situation of overstocking of inventory and it should make sure that

finished products are sold as soon as possible. It helps in further minimizing the cost

associated with inventory in terms of handling and carrying cost.

The company should work on maintaining good relationship with its customers and

suppliers which can help it at the time of crisis. At the same time, it can also help in

avoiding any disputes.

MDL Ltd is also required to establish a good relationship with its major customers and

not doing the same is the very serious concern for the company.

them incentives. Also, it should motivate its collection team by offering them incentives

by collecting outstanding invoices on time.

MDL Ltd should review different suppliers and negotiate for better pricing and if if the

supplier is not willing to come to a favorable term Then it should look for other suppliers.

The company should look for better payment terms with suppliers and other vendors

which will help in effective management of payment process. Also, balance should be

maintained in the payment terms for both accounts payable and accounts receivable.

It should use electronic payment system which will help in in ensuring that timely

payments are done and also helps in avoiding the situation of delay payments which will

attract penalty.

MDL should examine the amount of interest on the loans taken and also if possible can

any modification in interest rate and installment payment can be done or not. This will

help in reducing the cost of paying principal amount which can be termed as savings and

added to working capital.

It should avoid the situation of overstocking of inventory and it should make sure that

finished products are sold as soon as possible. It helps in further minimizing the cost

associated with inventory in terms of handling and carrying cost.

The company should work on maintaining good relationship with its customers and

suppliers which can help it at the time of crisis. At the same time, it can also help in

avoiding any disputes.

MDL Ltd is also required to establish a good relationship with its major customers and

not doing the same is the very serious concern for the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EXECUTIVE SUMMARY

In this report, the different budgetary methods that can be used by the organization are analyzed

based on their strengths and weaknesses. After conducting proper evaluation, the best and

appropriate method for Second Sight Plc is determined which is activity-based budgeting method

for its new business plan.

In this report, the different budgetary methods that can be used by the organization are analyzed

based on their strengths and weaknesses. After conducting proper evaluation, the best and

appropriate method for Second Sight Plc is determined which is activity-based budgeting method

for its new business plan.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART 2

i.

Different methods of preparing budget

Budget refers to the statement in which revenue and expenditure for a specific period is

forecasted. Basically, an incremental budget is prepared which is based on the previous year’s

budget and actual performance. The incremental amount is added to the new budget. The

different types of budgets are stated below.

Traditional budgeting approach

In this method, budget is prepared by taking previous year’s budget as the base and only

changes are made in terms of expenses with respect to inflation, market situation etc. It is exactly

dependent on the previous year’s budget (Weigel and Hiebl, 2018). This method cannot be used

for the newly established businesses as it requires last year’s data.

Strengths

Solid framework as it is based on the reference point which helps in easy management of

the business activities.

It encourages decentralization as everyone can look into the budget.

It helps in better decision making as problems can be identified easily.

Weaknesses

It may lead to budget slack as changes can be done by anyone as per the need.

It is a time-consuming process as it requires a lot of time in sorting out the things with the

expected expenditure.

This budget is completely relied on previous year’s budget which can get wrong.

Other alternative budgeting methods

Rolling budgets

This budget is a continuous budget which is updated in a regular period of time as and

when the earlier budget expires (Shum, 2019). It can be said as an extension of earlier budget.

Using this approach, a business always has budget for one year in the future. It is also known as

budget rollover.

Strengths

It does not involve much time as it is an extension of earlier budget.

In this method, budget is very flexible so that changes can be made because of any

unexpected events.

It also helps in identifying the strength and weaknesses of the business.

Weaknesses

i.

Different methods of preparing budget

Budget refers to the statement in which revenue and expenditure for a specific period is

forecasted. Basically, an incremental budget is prepared which is based on the previous year’s

budget and actual performance. The incremental amount is added to the new budget. The

different types of budgets are stated below.

Traditional budgeting approach

In this method, budget is prepared by taking previous year’s budget as the base and only

changes are made in terms of expenses with respect to inflation, market situation etc. It is exactly

dependent on the previous year’s budget (Weigel and Hiebl, 2018). This method cannot be used

for the newly established businesses as it requires last year’s data.

Strengths

Solid framework as it is based on the reference point which helps in easy management of

the business activities.

It encourages decentralization as everyone can look into the budget.

It helps in better decision making as problems can be identified easily.

Weaknesses

It may lead to budget slack as changes can be done by anyone as per the need.

It is a time-consuming process as it requires a lot of time in sorting out the things with the

expected expenditure.

This budget is completely relied on previous year’s budget which can get wrong.

Other alternative budgeting methods

Rolling budgets

This budget is a continuous budget which is updated in a regular period of time as and

when the earlier budget expires (Shum, 2019). It can be said as an extension of earlier budget.

Using this approach, a business always has budget for one year in the future. It is also known as

budget rollover.

Strengths

It does not involve much time as it is an extension of earlier budget.

In this method, budget is very flexible so that changes can be made because of any

unexpected events.

It also helps in identifying the strength and weaknesses of the business.

Weaknesses

It requires highly skilled personnel.

It is very costly.

This method can be used by the businesses where conditions keeps on changing

frequently.

Zero based budgets

In this method, budget is prepared from the initial stage or in other words from the

scratch. In this, all the expenditures are justified for the new period. Nothing is taken from the

previous period. Each and every function of the organization is analysed with respect to the

needs and costs (Dokulil, 2016). Based on the analysis, budget is prepared and resources are

allocated to the departments for implementing their activities. Implementing it requires to follow

certain steps such as identifying the organizational goals, formulating ways for achieving those

goals, identifying the sources of funds and prioritizing it.

Strengths

It provides clear picture of the resources available.

It also helps in eliminating unnecessary activities.

This method helps in establishing effective communication and coordination among the

departments.

Weaknesses

It is a time-consuming process as everything starts from the scratch.

It requires highly skilled and experience team.

This method is very costly.

Activity-based budgets

Under this method, budget is prepared after taking into account overhead cost.in this

method, previous year’s data s not used but a complete cost analysis is carried out. Based on this,

resources are allocated to different activities (Amirkhani, Aghaz and Sheikh, 2019). This method

is used in order to bring efficiency in the activities and also it prepared after justifying the cost

with the cost drivers. Thus, it is an activity-oriented budgeting method.

Strengths

It helps in saving cost by eliminating unnecessary activities which helps in saving costs.

This method helps in exercising more control over the activities.

It has the scope of making changes in the business as per the situation.

Weaknesses

It is very lengthy process and it requires a lot of time.

This method requires very talented team for analysing different activities.

This process is very expensive.

ii.

Application of budgeting methods on Second Sight Plc for future plan

The application of different budgeting methods to the Second Sight Plc is stated below.

Traditional budgeting approach

This method of budgeting is currently used by the Second Sight Plc. This method uses

previous year’s budget for preparing the current year’s budget (Karpenko, Voronzhak and

Sapron, 2017). This method is most suitable for businesses having no major changes in the

working conditions. For example, if there is any error in the actual performance then it can be

It is very costly.

This method can be used by the businesses where conditions keeps on changing

frequently.

Zero based budgets

In this method, budget is prepared from the initial stage or in other words from the

scratch. In this, all the expenditures are justified for the new period. Nothing is taken from the

previous period. Each and every function of the organization is analysed with respect to the

needs and costs (Dokulil, 2016). Based on the analysis, budget is prepared and resources are

allocated to the departments for implementing their activities. Implementing it requires to follow

certain steps such as identifying the organizational goals, formulating ways for achieving those

goals, identifying the sources of funds and prioritizing it.

Strengths

It provides clear picture of the resources available.

It also helps in eliminating unnecessary activities.

This method helps in establishing effective communication and coordination among the

departments.

Weaknesses

It is a time-consuming process as everything starts from the scratch.

It requires highly skilled and experience team.

This method is very costly.

Activity-based budgets

Under this method, budget is prepared after taking into account overhead cost.in this

method, previous year’s data s not used but a complete cost analysis is carried out. Based on this,

resources are allocated to different activities (Amirkhani, Aghaz and Sheikh, 2019). This method

is used in order to bring efficiency in the activities and also it prepared after justifying the cost

with the cost drivers. Thus, it is an activity-oriented budgeting method.

Strengths

It helps in saving cost by eliminating unnecessary activities which helps in saving costs.

This method helps in exercising more control over the activities.

It has the scope of making changes in the business as per the situation.

Weaknesses

It is very lengthy process and it requires a lot of time.

This method requires very talented team for analysing different activities.

This process is very expensive.

ii.

Application of budgeting methods on Second Sight Plc for future plan

The application of different budgeting methods to the Second Sight Plc is stated below.

Traditional budgeting approach

This method of budgeting is currently used by the Second Sight Plc. This method uses

previous year’s budget for preparing the current year’s budget (Karpenko, Voronzhak and

Sapron, 2017). This method is most suitable for businesses having no major changes in the

working conditions. For example, if there is any error in the actual performance then it can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

easily figured out from the budget as only necessary changes are done. It has other benefits as

well which the Second Sight Plc is taking advantage of it like better decision-making process.

Rolling budgets

If this method is implemented by the Second Sight Plc. it will be very beneficial as it a

continuous budget which can be revised from time to time as per the requirement or changing

conditions. For example, if Second Sight Plc. Adopted a 12 month planning budget which starts

from January to December. As the January month completes, the budget will add another budget

for the following January. So, the budget still remains the same 12 month but now it has

extended from current year’s February to January of the next year. This method is very helpful as

it helps in identifying the strength and weaknesses of eth business and also changes can be made

easily.

Zero based budgets

If Second Sight Plc uses this method of budgeting then it requires to start its budgeting

process from the zero base and the respective manager of the process has to justify each and

every expense (Miller, 2018). The major aim of the businesses for using this method is to

optimize the cost and then revenue. For example, Second Sight Plc manufactures special type of

glasses which requires special parts. the company will analyse the cost of certain parts which are

outsourced to another increases the cost by 5%. After analysis, company is of the view that it can

manufacture it itself which will help in controlling and reducing the cost. Thus, this method is

very useful.

Activity-based budgets

In this method of budgeting, budget is prepared on the basis of the different cost such as

direct material and labour and overhead expenses (Oyadomari and et.al, 2018). It helps in

analysing the cost pertaining to different activities involved. For example, the company Second

Sight Plc estimated the sales for the next year of 100,000 units, each unit cost £5 for processing.

Therefore, the total budget for the expenses will be £500,000. Thus, this method of budgeting

can be used by Second Sight Plc.

iii.

Analysing the appropriate method of budgeting

The Second Sight Plc should switch from traditional method of budgeting to the

alternative methods because traditional method is just an adjustment to the past year’s budget

and that too on the part of inflation or increase in revenue. On the other hand, in order to

overcome such challenges, it should help use activity-based budgeting method. It will Second

Sight Plc in identifying the cost associated with the different activities carried out by it. Since,

Second Sight Plc is looking for expanding its business in other nations as well so it is best

method as it will help in evaluating the performance based on the activities and cost involved. It

will also help it identifying the unnecessary activities which can be eliminated which will

consequently lead to reduction in cost. Also, it will help in establishing an effective control over

the activities in order to improve the efficiency level. Another important point is that it will very

well which the Second Sight Plc is taking advantage of it like better decision-making process.

Rolling budgets

If this method is implemented by the Second Sight Plc. it will be very beneficial as it a

continuous budget which can be revised from time to time as per the requirement or changing

conditions. For example, if Second Sight Plc. Adopted a 12 month planning budget which starts

from January to December. As the January month completes, the budget will add another budget

for the following January. So, the budget still remains the same 12 month but now it has

extended from current year’s February to January of the next year. This method is very helpful as

it helps in identifying the strength and weaknesses of eth business and also changes can be made

easily.

Zero based budgets

If Second Sight Plc uses this method of budgeting then it requires to start its budgeting

process from the zero base and the respective manager of the process has to justify each and

every expense (Miller, 2018). The major aim of the businesses for using this method is to

optimize the cost and then revenue. For example, Second Sight Plc manufactures special type of

glasses which requires special parts. the company will analyse the cost of certain parts which are

outsourced to another increases the cost by 5%. After analysis, company is of the view that it can

manufacture it itself which will help in controlling and reducing the cost. Thus, this method is

very useful.

Activity-based budgets

In this method of budgeting, budget is prepared on the basis of the different cost such as

direct material and labour and overhead expenses (Oyadomari and et.al, 2018). It helps in

analysing the cost pertaining to different activities involved. For example, the company Second

Sight Plc estimated the sales for the next year of 100,000 units, each unit cost £5 for processing.

Therefore, the total budget for the expenses will be £500,000. Thus, this method of budgeting

can be used by Second Sight Plc.

iii.

Analysing the appropriate method of budgeting

The Second Sight Plc should switch from traditional method of budgeting to the

alternative methods because traditional method is just an adjustment to the past year’s budget

and that too on the part of inflation or increase in revenue. On the other hand, in order to

overcome such challenges, it should help use activity-based budgeting method. It will Second

Sight Plc in identifying the cost associated with the different activities carried out by it. Since,

Second Sight Plc is looking for expanding its business in other nations as well so it is best

method as it will help in evaluating the performance based on the activities and cost involved. It

will also help it identifying the unnecessary activities which can be eliminated which will

consequently lead to reduction in cost. Also, it will help in establishing an effective control over

the activities in order to improve the efficiency level. Another important point is that it will very

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

flexible which is beneficial as changes can be made very easily as per changing business

conditions and situations. Thus, this method is appropriate for the Second Sight Plc for

implementing it in its business.

conditions and situations. Thus, this method is appropriate for the Second Sight Plc for

implementing it in its business.

REFERENCES

Books and Journals

Afrifa, G. and Tingbani, I., 2018. Working capital management, cash flow and SMEs’

performance. Int. J. Banking, Accounting and Finance. 9(1).

Amirkhani, T., Aghaz, A. and Sheikh, A., 2019. An implementation model of performance-based

budgeting. International Journal of Productivity and Performance Management.

Dokulil, J., 2016. Budgeting Process in the Business Environment. In Conference Proceedings

DOKBAT (p. 111).

Karpenko, L. M., Voronzhak, P. V. and Sapron, N. O., 2017. FEATURES OF THE

ORGANIZATION AND ESTABLISHMENT OF THE BUDGETING

MANAGEMENT AT THE ENTERPRISE IN GLOBALIZATION CHANGES

CONDITIONS. Science and practice: an innovative approach. p.110.

Miller, G., 2018. Performance based budgeting. Routledge.

Oyadomari, J. C. T. and et.al, 2018. Flexible budgeting influence on organizational inertia and

flexibility. International Journal of Productivity and Performance Management.

Shum, D., 2019. Effective Budgeting for Businesses Today. Partridge Publishing Singapore.

Singhania, M. and Mehta, P., 2017. Working capital management and firms’ profitability:

evidence from emerging Asian countries. South Asian Journal of Business Studies.

Weigel, C. and Hiebl, M. R., 2018. Beyond budgeting: review and research agenda. Journal of

Accounting & Organizational Change.

Online

Accounts Payable. 2020. [Online]. Available Through:< https://cleartax.in/s/accounts-payable-

management>.

Definition of 'Accounts Receivable'. 2020. [Online]. Available Through:<

https://economictimes.indiatimes.com/definition/accounts-receivable>.

Inventory. 2019. [Online]. Available Through:<

https://investinganswers.com/dictionary/i/inventory>.

Kenton, W., 2019. Profit Definition. [Online]. Available Through:<

https://www.investopedia.com/terms/p/profit.asp >.

What is Cash Flow? 2020. [Online]. Available Through:<

https://corporatefinanceinstitute.com/resources/knowledge/finance/cash-flow/>.

What Is Working Capital? 2020. [Online]. Available Through:<

https://www.bajajfinserv.in/what-is-working-capital>.

Books and Journals

Afrifa, G. and Tingbani, I., 2018. Working capital management, cash flow and SMEs’

performance. Int. J. Banking, Accounting and Finance. 9(1).

Amirkhani, T., Aghaz, A. and Sheikh, A., 2019. An implementation model of performance-based

budgeting. International Journal of Productivity and Performance Management.

Dokulil, J., 2016. Budgeting Process in the Business Environment. In Conference Proceedings

DOKBAT (p. 111).

Karpenko, L. M., Voronzhak, P. V. and Sapron, N. O., 2017. FEATURES OF THE

ORGANIZATION AND ESTABLISHMENT OF THE BUDGETING

MANAGEMENT AT THE ENTERPRISE IN GLOBALIZATION CHANGES

CONDITIONS. Science and practice: an innovative approach. p.110.

Miller, G., 2018. Performance based budgeting. Routledge.

Oyadomari, J. C. T. and et.al, 2018. Flexible budgeting influence on organizational inertia and

flexibility. International Journal of Productivity and Performance Management.

Shum, D., 2019. Effective Budgeting for Businesses Today. Partridge Publishing Singapore.

Singhania, M. and Mehta, P., 2017. Working capital management and firms’ profitability:

evidence from emerging Asian countries. South Asian Journal of Business Studies.

Weigel, C. and Hiebl, M. R., 2018. Beyond budgeting: review and research agenda. Journal of

Accounting & Organizational Change.

Online

Accounts Payable. 2020. [Online]. Available Through:< https://cleartax.in/s/accounts-payable-

management>.

Definition of 'Accounts Receivable'. 2020. [Online]. Available Through:<

https://economictimes.indiatimes.com/definition/accounts-receivable>.

Inventory. 2019. [Online]. Available Through:<

https://investinganswers.com/dictionary/i/inventory>.

Kenton, W., 2019. Profit Definition. [Online]. Available Through:<

https://www.investopedia.com/terms/p/profit.asp >.

What is Cash Flow? 2020. [Online]. Available Through:<

https://corporatefinanceinstitute.com/resources/knowledge/finance/cash-flow/>.

What Is Working Capital? 2020. [Online]. Available Through:<

https://www.bajajfinserv.in/what-is-working-capital>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.