Business Finance: Profit, Cash Flow, Working Capital Analysis Report

VerifiedAdded on 2022/12/27

|13

|3223

|83

Report

AI Summary

This report delves into key concepts in business finance, differentiating between profit and cash flow, and exploring the components of working capital, including receivables, inventory, and payables. It examines how changes in working capital affect cash flow and applies financial accounting concepts to improve company management, using Trend Ltd as a case study. The report also provides practical steps to enhance cash flow through working capital management, such as cash flow forecasting, electronic invoicing, and inventory management. Furthermore, it includes a cash budget analysis for Thorne Estates Limited over four consecutive months, highlighting the advantages of cash budgeting, such as controlling spending and fostering critical thinking within an organization. The analysis provides observations and recommendations for Thorne Estates Limited based on the cash budget data.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 1............................................................................................................................................3

Profit and Cash flow and their difference...................................................................................3

Working Capital, Receivables, Inventory and Payables.............................................................3

Effect on Cash Flow due to working capital changes.................................................................4

Application of financial accounting concepts which can improve the management of the

company:.....................................................................................................................................4

Steps that can be taken to improve the cash flow of the company through working capital

management:...............................................................................................................................5

TASK 2............................................................................................................................................6

Cash Budget of Thorne Estates Limited for four consecutive months.......................................6

Observation and recommendation to Thorne Estates Limited arising from this analysis.........11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

TASK 1............................................................................................................................................3

Profit and Cash flow and their difference...................................................................................3

Working Capital, Receivables, Inventory and Payables.............................................................3

Effect on Cash Flow due to working capital changes.................................................................4

Application of financial accounting concepts which can improve the management of the

company:.....................................................................................................................................4

Steps that can be taken to improve the cash flow of the company through working capital

management:...............................................................................................................................5

TASK 2............................................................................................................................................6

Cash Budget of Thorne Estates Limited for four consecutive months.......................................6

Observation and recommendation to Thorne Estates Limited arising from this analysis.........11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

TASK 1

Profit and Cash flow and their difference

Cash flow and profit are important tools used in financial accounting of various

organisations and businesses. Cash flow and profit are two different concepts of financial

accounting and it is important for an individual to understand the difference between these

concepts.

Cash flow: There is a frequent flow of cash in any business or organisation. When a

company buys raw material for the production of its products the cash flows out of the business

to its suppliers. When the company sells its finished goods and additional services to its

customers (wholesalers, retailers, government etc.) then there is an inflow of cash in the

business. Other activities like paying of salaries, utility bills, maintenance bills, rent consists of

inflow and outflow of cash in the business. Cash flow refers to the net amount of cash inflow and

outflow of a business in a specific period or at a certain point of time (Jouirou and Lakhal, 2020).

Profit: Profit refers to the balance obtained by subtracting all the operating expenses

from the revenues of the business. It is the remaining amount that is left after subtracting

expenses from the proceeds of the business.

Working Capital, Receivables, Inventory and Payables

Working Capital: Working capital refers to the deviation between all the current assets

and current liabilities of the business. Current consists of ; inventories of raw material, cash,

debtors, inventories of work in progress and stock of finished goods etc. Current liabilities

consists of; short-term borrowings, account payables, creditors, bank overdraft etc. With the help

of working capital the management is able to calculate the liquidity of the business by using

current assets and current liabilities.

Receivables: Receivables refers to the personal accounts that are maintained by the

business in its financial accounts which displays the amount due from the people ( generally

customers) in favour of the business. Receivables or debtors are generally customers who have

paid for the products and services which he will receive from the business and availed the same

with the promise to pay such amount in the future (Ciola, Gaffeo and Gallegati, 2020).

Inventory: Inventory is the stock of goods which the business holds or manufactures and

sells the same with or without value addition. Inventory can be further classified into three basic

Profit and Cash flow and their difference

Cash flow and profit are important tools used in financial accounting of various

organisations and businesses. Cash flow and profit are two different concepts of financial

accounting and it is important for an individual to understand the difference between these

concepts.

Cash flow: There is a frequent flow of cash in any business or organisation. When a

company buys raw material for the production of its products the cash flows out of the business

to its suppliers. When the company sells its finished goods and additional services to its

customers (wholesalers, retailers, government etc.) then there is an inflow of cash in the

business. Other activities like paying of salaries, utility bills, maintenance bills, rent consists of

inflow and outflow of cash in the business. Cash flow refers to the net amount of cash inflow and

outflow of a business in a specific period or at a certain point of time (Jouirou and Lakhal, 2020).

Profit: Profit refers to the balance obtained by subtracting all the operating expenses

from the revenues of the business. It is the remaining amount that is left after subtracting

expenses from the proceeds of the business.

Working Capital, Receivables, Inventory and Payables

Working Capital: Working capital refers to the deviation between all the current assets

and current liabilities of the business. Current consists of ; inventories of raw material, cash,

debtors, inventories of work in progress and stock of finished goods etc. Current liabilities

consists of; short-term borrowings, account payables, creditors, bank overdraft etc. With the help

of working capital the management is able to calculate the liquidity of the business by using

current assets and current liabilities.

Receivables: Receivables refers to the personal accounts that are maintained by the

business in its financial accounts which displays the amount due from the people ( generally

customers) in favour of the business. Receivables or debtors are generally customers who have

paid for the products and services which he will receive from the business and availed the same

with the promise to pay such amount in the future (Ciola, Gaffeo and Gallegati, 2020).

Inventory: Inventory is the stock of goods which the business holds or manufactures and

sells the same with or without value addition. Inventory can be further classified into three basic

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

types; raw material, work in progress and finished goods. This is considered as current asset for

the organisation.

Payables: Payables refer to the personal accounts that are recorded by the organisation in

its financial statement which displays the balance remaining and due which the business has to

pay to the suppliers or a third party outside the business who provides the business with some

type of inventory. Payables or creditors are generally suppliers who have supplied the business

with some sought of inventory. The business promises to pay such amount to the creditors in the

future. It is recorded as current liability in the books of business.

Effect on Cash Flow due to working capital changes

In businesses there are frequent transactions in cash which implies inflow and outflow of

cash. Inflow and outflow of cash changes the working capital and as a result cash flow of

business is greatly affected as cash is of great significance in the calculation of working capital

and cash flow.

For example if the business advances a long term debt from a bank then there will be a

change in the working capital due to the inflow of cash in the business. As a result inflow of cash

will also increase resulting in a positive cash flow (Ujah, Tarkom and Okafor, 2020).

Another example can be considered in which the business buys a fixed asset, let's say a

machine or a building. There will be an outflow of cash which will result in decreased balance of

current assets which will further decrease the working capital of the business. Also as a result

outflow of cash will increase resulting in negative cash flow.

Application of financial accounting concepts which can improve the management of the

company:

Trend Ltd (TL) is manufacturer of gym clothing and footwear. The management have

basic knowledge about the above enlisted and briefed concepts of financial accounting but this

knowledge is nor applied and tasks are not executed with efficiency and effectiveness.

The company has a positive cash flow but most of the cash inflow is from the financing

activities of the business. Trend Ltd has borrowed £35 million more as long-term debt. Which

has certainly boosted up the cash inflow of the business.

TL ha made few investing decisions as well which has certainly increased the profit of

the company. With new facilities and new machines, the company will be able to produce more

of the specified products and increase the cash flow of the business.

the organisation.

Payables: Payables refer to the personal accounts that are recorded by the organisation in

its financial statement which displays the balance remaining and due which the business has to

pay to the suppliers or a third party outside the business who provides the business with some

type of inventory. Payables or creditors are generally suppliers who have supplied the business

with some sought of inventory. The business promises to pay such amount to the creditors in the

future. It is recorded as current liability in the books of business.

Effect on Cash Flow due to working capital changes

In businesses there are frequent transactions in cash which implies inflow and outflow of

cash. Inflow and outflow of cash changes the working capital and as a result cash flow of

business is greatly affected as cash is of great significance in the calculation of working capital

and cash flow.

For example if the business advances a long term debt from a bank then there will be a

change in the working capital due to the inflow of cash in the business. As a result inflow of cash

will also increase resulting in a positive cash flow (Ujah, Tarkom and Okafor, 2020).

Another example can be considered in which the business buys a fixed asset, let's say a

machine or a building. There will be an outflow of cash which will result in decreased balance of

current assets which will further decrease the working capital of the business. Also as a result

outflow of cash will increase resulting in negative cash flow.

Application of financial accounting concepts which can improve the management of the

company:

Trend Ltd (TL) is manufacturer of gym clothing and footwear. The management have

basic knowledge about the above enlisted and briefed concepts of financial accounting but this

knowledge is nor applied and tasks are not executed with efficiency and effectiveness.

The company has a positive cash flow but most of the cash inflow is from the financing

activities of the business. Trend Ltd has borrowed £35 million more as long-term debt. Which

has certainly boosted up the cash inflow of the business.

TL ha made few investing decisions as well which has certainly increased the profit of

the company. With new facilities and new machines, the company will be able to produce more

of the specified products and increase the cash flow of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debtors of the company also owes the company an amount of £10 million and £12.5

million, which reflects poor account receivables management system and long term account

receivable conversion period.

Steps that can be taken to improve the cash flow of the company through working capital

management:

Management of working capital assists the management in maintaining adequate balance

of cash with analysing and modulating cash flow of the business, this cash balance is further

used to comply with the short term financial obligations and short term monetary needs of the

business. Working capital management requires the organisation to effectively use current assets

so the business can be more profitable which and has enough cash flow to carry out its

operations. It prevents the business from using external borrowings which helps in decreasing the

financial obligations of the company. These funds can be used in the growth of the business

(Bamfo-Debrah, 2019).

Working capital is truly important for every business and organisation. Trend Ltd needs

to maintain enough cash so that it can cover expenses which will arise in the future. The

company must also use the available funds with efficiency so that these funds can be allotted for

the activities which are of a greater significance. All of this can be achieved by managing

receivables, payables, inventories and cash.

Working capital management is exercised by using certain tools and methods. These

methods are:

Cash Flow Forecasting: This method identifies and predicts the cash inflow and

outflow of the business which can occur in the future. For example, by assessing

the past performance of the company it can be identified how much cash will be

received from debtors and how much cash will be used in order to settle account

payables.. By assessing this the company can plan and predict the cash that it will

need in the future and also determine the shortfall or excess of cash. The more

accurate the prediction, the better will be the company's working capital

decisions.

Electronic Invoicing: Electronic invoicing is the process of furnishing an

electronic invoice for the customers. This type of activity can surely benefit Trend

Ltd as electronic invoicing process will reduce the risk of errors and

million, which reflects poor account receivables management system and long term account

receivable conversion period.

Steps that can be taken to improve the cash flow of the company through working capital

management:

Management of working capital assists the management in maintaining adequate balance

of cash with analysing and modulating cash flow of the business, this cash balance is further

used to comply with the short term financial obligations and short term monetary needs of the

business. Working capital management requires the organisation to effectively use current assets

so the business can be more profitable which and has enough cash flow to carry out its

operations. It prevents the business from using external borrowings which helps in decreasing the

financial obligations of the company. These funds can be used in the growth of the business

(Bamfo-Debrah, 2019).

Working capital is truly important for every business and organisation. Trend Ltd needs

to maintain enough cash so that it can cover expenses which will arise in the future. The

company must also use the available funds with efficiency so that these funds can be allotted for

the activities which are of a greater significance. All of this can be achieved by managing

receivables, payables, inventories and cash.

Working capital management is exercised by using certain tools and methods. These

methods are:

Cash Flow Forecasting: This method identifies and predicts the cash inflow and

outflow of the business which can occur in the future. For example, by assessing

the past performance of the company it can be identified how much cash will be

received from debtors and how much cash will be used in order to settle account

payables.. By assessing this the company can plan and predict the cash that it will

need in the future and also determine the shortfall or excess of cash. The more

accurate the prediction, the better will be the company's working capital

decisions.

Electronic Invoicing: Electronic invoicing is the process of furnishing an

electronic invoice for the customers. This type of activity can surely benefit Trend

Ltd as electronic invoicing process will reduce the risk of errors and

miscalculation. This will automate the invoice cycle and the customers will

receive invoices as soon as possible. This will further help the company to receive

the payments quickly and increase its cash flow (Göransson, Lundqvist and

Svensson, 2020). This method is more convenient than the traditional one as

Trend Ltd can easily record inventory purchased, finished goods produced, work

in progress and also finished goods sold. The system will generate invoices by

itself as per the sale data provided by the employee.

Inventory Management: Inventory management is one of a major element of

working capital management which assists the organisation to carry out its

operations with high efficiency along with managing high working capital. This

method enables the company to maintain sufficient level of inventory available on

demand so that consumers' demand can be met and excess inventory stock can be

avoided as it blocks cash and makes working capital more rigid. Trend Ltd can

use inventory turnover ratio to monitor and maintain the stock of inventory. The

inventory turnover ratio is calculated by dividing revenues by inventory cost. This

ratio determines how quickly can inventory of the company be replenished and

sold. The ratio is further compared to other businesses in the same industry.

Comparatively high ratio indicate low or inadequate level of inventory and low

ratio indicates high level of inventory.

TASK 2

Cash Budget of Thorne Estates Limited for four consecutive months

Cash Budgets are made to predict the future cash position of the company. Cash budget

records expected cash inflow and outflow which occurs in a certain time duration. Cash inflow

and outflow may contain revenues collected, investments made, expenses paid and loans receipts

and payments.

Management uses cash budget in order to manage the cash inflow and outflow of the

organisation. Through cash budget, the management ensures that the organisation has adequate

cash balance which will aid the business in carrying out its operations and even pay bills when

they come due (Honková, 2019). For example utility bills are required to be paid every month

receive invoices as soon as possible. This will further help the company to receive

the payments quickly and increase its cash flow (Göransson, Lundqvist and

Svensson, 2020). This method is more convenient than the traditional one as

Trend Ltd can easily record inventory purchased, finished goods produced, work

in progress and also finished goods sold. The system will generate invoices by

itself as per the sale data provided by the employee.

Inventory Management: Inventory management is one of a major element of

working capital management which assists the organisation to carry out its

operations with high efficiency along with managing high working capital. This

method enables the company to maintain sufficient level of inventory available on

demand so that consumers' demand can be met and excess inventory stock can be

avoided as it blocks cash and makes working capital more rigid. Trend Ltd can

use inventory turnover ratio to monitor and maintain the stock of inventory. The

inventory turnover ratio is calculated by dividing revenues by inventory cost. This

ratio determines how quickly can inventory of the company be replenished and

sold. The ratio is further compared to other businesses in the same industry.

Comparatively high ratio indicate low or inadequate level of inventory and low

ratio indicates high level of inventory.

TASK 2

Cash Budget of Thorne Estates Limited for four consecutive months

Cash Budgets are made to predict the future cash position of the company. Cash budget

records expected cash inflow and outflow which occurs in a certain time duration. Cash inflow

and outflow may contain revenues collected, investments made, expenses paid and loans receipts

and payments.

Management uses cash budget in order to manage the cash inflow and outflow of the

organisation. Through cash budget, the management ensures that the organisation has adequate

cash balance which will aid the business in carrying out its operations and even pay bills when

they come due (Honková, 2019). For example utility bills are required to be paid every month

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

along with other monthly expenses. The management use cash budget to determine the shortfall

in the cash balance of the organisation so that the gap can be filled before payments are to be

made.

Cash Budget has following advantages:

It restrict the spends of an organisation: Cash budget assist businesses and

companies to manage their cash balance which further limit their spendings so

that they have enough finances available which will prevent them from borrowing

funds from the market or any other lender. Cash budget is the estimation and

prediction of the future cash inflow and outflow of the upcoming period. With the

help of this prediction and forecast, the management will be able to determine

how much money the business has available with it. From this assessment

management can identify and allocate funds to different department and activities.

This restricts the business from spending cash on insignificant activities so that it

can be used on other items and processes which are of a greater importance.

It empowers critical thinking within the organisation: Cash budget stimulate

the organisation and its employees to evaluate the financial statements and assess

the financial position of the organisation so that they can formulate strategies

which helps in improving the financial situation and position of the company.

Employees have limited finances available with them, in order to complete

various activities in the given budget they have to allocate funds carefully to

minimise unnecessary use of cash on insignificant activities. This will improve

their decision making skills and make them more effective and motivated to

accept such challenges.

Following are the cash budgets of Throne Estates Limited for the months of January, February,

March and April of the year 2021 (working notes are at the end of the budget):

Cash Budget of Thorne Estates Limited for the month of January 2021

Particulars January(£)

Cash Inflow:

Income via Fees charged 54000

Receipts via sale of vehicle -

in the cash balance of the organisation so that the gap can be filled before payments are to be

made.

Cash Budget has following advantages:

It restrict the spends of an organisation: Cash budget assist businesses and

companies to manage their cash balance which further limit their spendings so

that they have enough finances available which will prevent them from borrowing

funds from the market or any other lender. Cash budget is the estimation and

prediction of the future cash inflow and outflow of the upcoming period. With the

help of this prediction and forecast, the management will be able to determine

how much money the business has available with it. From this assessment

management can identify and allocate funds to different department and activities.

This restricts the business from spending cash on insignificant activities so that it

can be used on other items and processes which are of a greater importance.

It empowers critical thinking within the organisation: Cash budget stimulate

the organisation and its employees to evaluate the financial statements and assess

the financial position of the organisation so that they can formulate strategies

which helps in improving the financial situation and position of the company.

Employees have limited finances available with them, in order to complete

various activities in the given budget they have to allocate funds carefully to

minimise unnecessary use of cash on insignificant activities. This will improve

their decision making skills and make them more effective and motivated to

accept such challenges.

Following are the cash budgets of Throne Estates Limited for the months of January, February,

March and April of the year 2021 (working notes are at the end of the budget):

Cash Budget of Thorne Estates Limited for the month of January 2021

Particulars January(£)

Cash Inflow:

Income via Fees charged 54000

Receipts via sale of vehicle -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

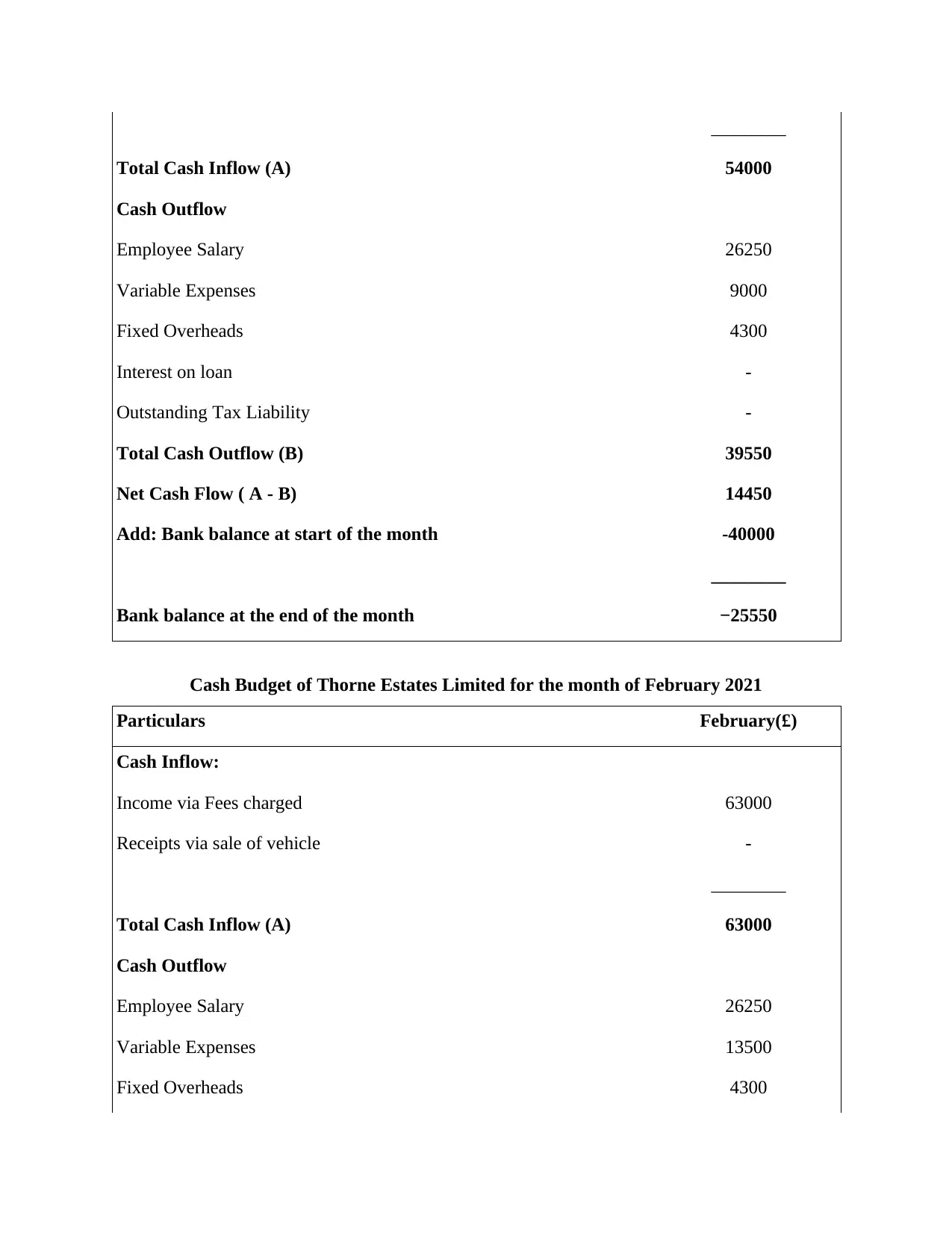

________

Total Cash Inflow (A) 54000

Cash Outflow

Employee Salary 26250

Variable Expenses 9000

Fixed Overheads 4300

Interest on loan -

Outstanding Tax Liability -

Total Cash Outflow (B) 39550

Net Cash Flow ( A - B) 14450

Add: Bank balance at start of the month -40000

________

Bank balance at the end of the month −25550

Cash Budget of Thorne Estates Limited for the month of February 2021

Particulars February(£)

Cash Inflow:

Income via Fees charged 63000

Receipts via sale of vehicle -

________

Total Cash Inflow (A) 63000

Cash Outflow

Employee Salary 26250

Variable Expenses 13500

Fixed Overheads 4300

Total Cash Inflow (A) 54000

Cash Outflow

Employee Salary 26250

Variable Expenses 9000

Fixed Overheads 4300

Interest on loan -

Outstanding Tax Liability -

Total Cash Outflow (B) 39550

Net Cash Flow ( A - B) 14450

Add: Bank balance at start of the month -40000

________

Bank balance at the end of the month −25550

Cash Budget of Thorne Estates Limited for the month of February 2021

Particulars February(£)

Cash Inflow:

Income via Fees charged 63000

Receipts via sale of vehicle -

________

Total Cash Inflow (A) 63000

Cash Outflow

Employee Salary 26250

Variable Expenses 13500

Fixed Overheads 4300

Interest on loan -

Outstanding Tax Liability -

Total Cash Outflow (B) 44050

Net Cash Flow ( A - B) 18950

Add: Bank balance at start of the month −25550

________

Bank balance at the end of the month −6600

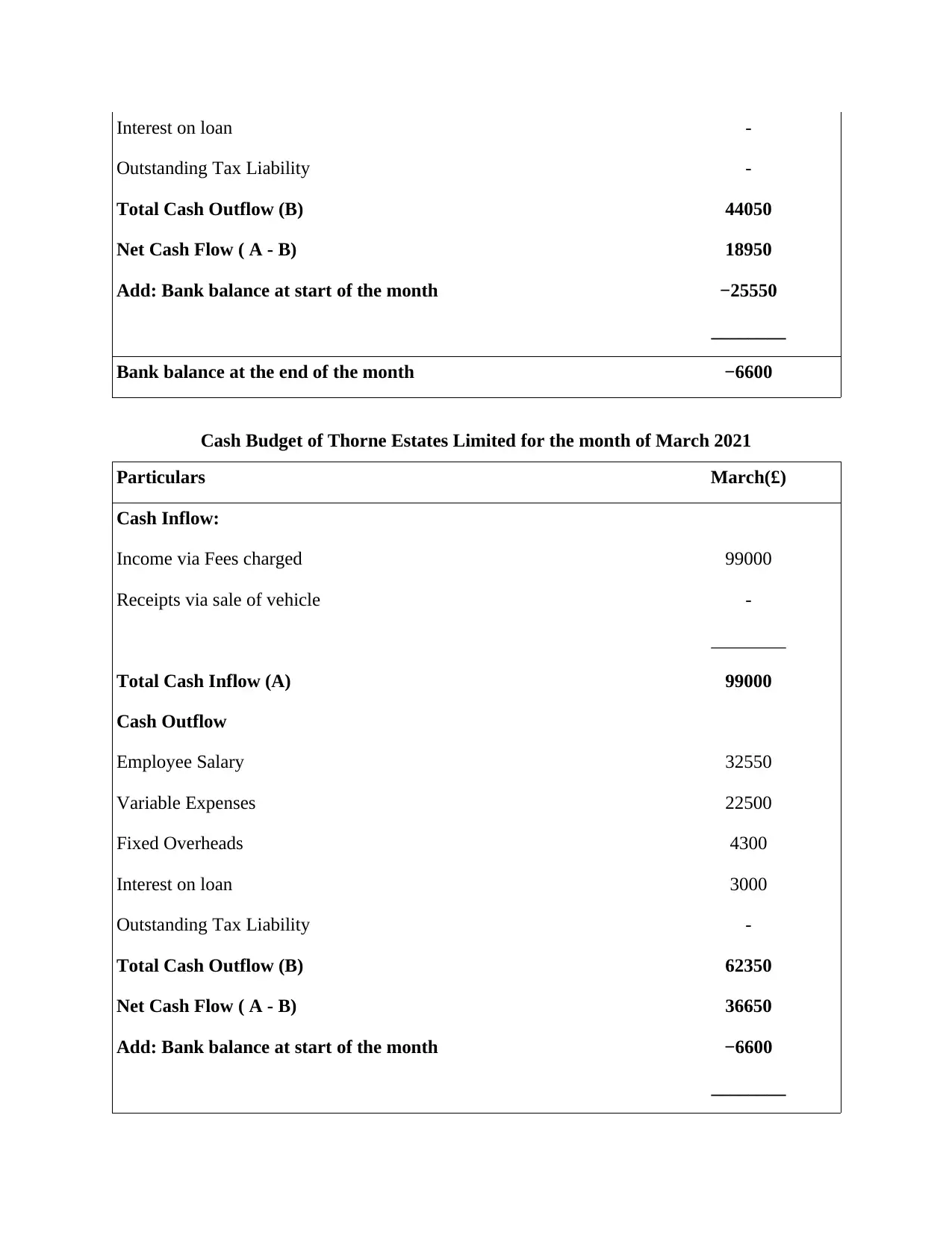

Cash Budget of Thorne Estates Limited for the month of March 2021

Particulars March(£)

Cash Inflow:

Income via Fees charged 99000

Receipts via sale of vehicle -

________

Total Cash Inflow (A) 99000

Cash Outflow

Employee Salary 32550

Variable Expenses 22500

Fixed Overheads 4300

Interest on loan 3000

Outstanding Tax Liability -

Total Cash Outflow (B) 62350

Net Cash Flow ( A - B) 36650

Add: Bank balance at start of the month −6600

________

Outstanding Tax Liability -

Total Cash Outflow (B) 44050

Net Cash Flow ( A - B) 18950

Add: Bank balance at start of the month −25550

________

Bank balance at the end of the month −6600

Cash Budget of Thorne Estates Limited for the month of March 2021

Particulars March(£)

Cash Inflow:

Income via Fees charged 99000

Receipts via sale of vehicle -

________

Total Cash Inflow (A) 99000

Cash Outflow

Employee Salary 32550

Variable Expenses 22500

Fixed Overheads 4300

Interest on loan 3000

Outstanding Tax Liability -

Total Cash Outflow (B) 62350

Net Cash Flow ( A - B) 36650

Add: Bank balance at start of the month −6600

________

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bank balance at the end of the month 30050

Cash Budget of Thorne Estates Limited for the month of April 2021

Particulars April(£)

Cash Inflow:

Income via Fees charged 144000

Receipts via sale of vehicle 20000

________

Total Cash Inflow (A) 164000

Cash Outflow

Employee Salary 38850

Variable Expenses 27000

Fixed Overheads 4300

Interest on loan -

Outstanding Tax Liability 95800

Total Cash Outflow (B) 165950

Net Cash Flow ( A - B) −1950

Add: Bank balance at start of the month 30050

________

Bank balance at the end of the month 28100

Working Notes:

1. Calculation of Income via Fees charged:

1. For the month of January = (2% of 180000*10) + ( 1% of 180000*10)

= £54000

2. For the month of February= (2% of 180000*10) + ( 1% of 180000*15)

Cash Budget of Thorne Estates Limited for the month of April 2021

Particulars April(£)

Cash Inflow:

Income via Fees charged 144000

Receipts via sale of vehicle 20000

________

Total Cash Inflow (A) 164000

Cash Outflow

Employee Salary 38850

Variable Expenses 27000

Fixed Overheads 4300

Interest on loan -

Outstanding Tax Liability 95800

Total Cash Outflow (B) 165950

Net Cash Flow ( A - B) −1950

Add: Bank balance at start of the month 30050

________

Bank balance at the end of the month 28100

Working Notes:

1. Calculation of Income via Fees charged:

1. For the month of January = (2% of 180000*10) + ( 1% of 180000*10)

= £54000

2. For the month of February= (2% of 180000*10) + ( 1% of 180000*15)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

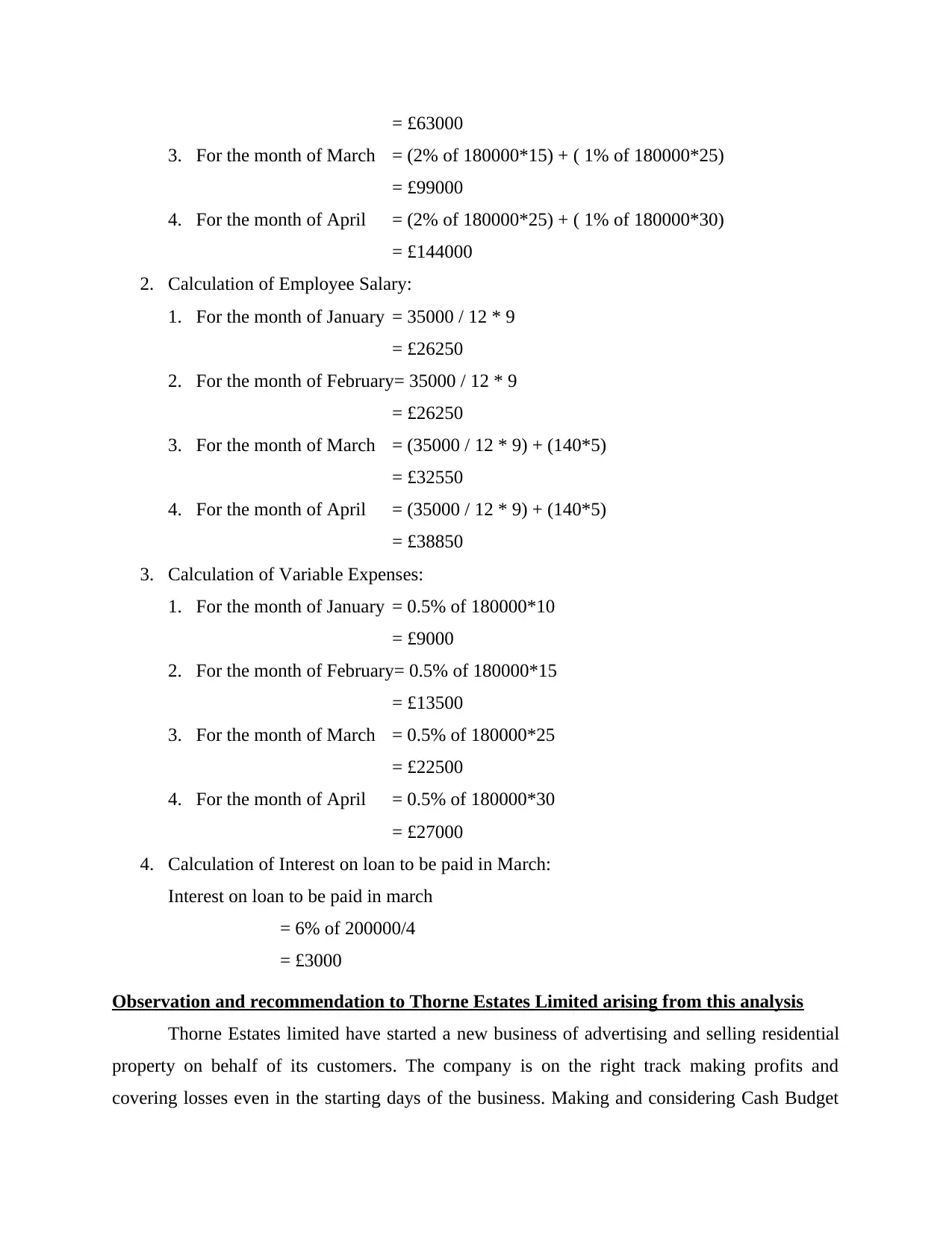

= £63000

3. For the month of March = (2% of 180000*15) + ( 1% of 180000*25)

= £99000

4. For the month of April = (2% of 180000*25) + ( 1% of 180000*30)

= £144000

2. Calculation of Employee Salary:

1. For the month of January = 35000 / 12 * 9

= £26250

2. For the month of February= 35000 / 12 * 9

= £26250

3. For the month of March = (35000 / 12 * 9) + (140*5)

= £32550

4. For the month of April = (35000 / 12 * 9) + (140*5)

= £38850

3. Calculation of Variable Expenses:

1. For the month of January = 0.5% of 180000*10

= £9000

2. For the month of February= 0.5% of 180000*15

= £13500

3. For the month of March = 0.5% of 180000*25

= £22500

4. For the month of April = 0.5% of 180000*30

= £27000

4. Calculation of Interest on loan to be paid in March:

Interest on loan to be paid in march

= 6% of 200000/4

= £3000

Observation and recommendation to Thorne Estates Limited arising from this analysis

Thorne Estates limited have started a new business of advertising and selling residential

property on behalf of its customers. The company is on the right track making profits and

covering losses even in the starting days of the business. Making and considering Cash Budget

3. For the month of March = (2% of 180000*15) + ( 1% of 180000*25)

= £99000

4. For the month of April = (2% of 180000*25) + ( 1% of 180000*30)

= £144000

2. Calculation of Employee Salary:

1. For the month of January = 35000 / 12 * 9

= £26250

2. For the month of February= 35000 / 12 * 9

= £26250

3. For the month of March = (35000 / 12 * 9) + (140*5)

= £32550

4. For the month of April = (35000 / 12 * 9) + (140*5)

= £38850

3. Calculation of Variable Expenses:

1. For the month of January = 0.5% of 180000*10

= £9000

2. For the month of February= 0.5% of 180000*15

= £13500

3. For the month of March = 0.5% of 180000*25

= £22500

4. For the month of April = 0.5% of 180000*30

= £27000

4. Calculation of Interest on loan to be paid in March:

Interest on loan to be paid in march

= 6% of 200000/4

= £3000

Observation and recommendation to Thorne Estates Limited arising from this analysis

Thorne Estates limited have started a new business of advertising and selling residential

property on behalf of its customers. The company is on the right track making profits and

covering losses even in the starting days of the business. Making and considering Cash Budget

was a really good decision as it will help the business in managing inflow and outflow of the

cash.

As per the analysis and observation of the author it is clear that there are some changes

which can be made in the approach and management of the company to be more profitable ,

generate more revenue and increase cash inflow. The company can increase its commission from

3% to 4-5%. A nominal change like this can have a huge impact over the cash inflow and

profitability of the business. It can further make a new policy of receiving the entire commission

in the month of sale, so that it can have more funds to spare and carry out all the necessary

business operations.

CONCLUSION

The above report concludes and describes the importance of analysing cash flow and

profit for any business organisation. Multiple tools and methods are used by various

organisations which helps them in stabilising the business and increasing profitability and cash

flow. Working capital management is on of the above said tools which helps in managing the

working capital of the business. Cash Budget play a significant role in the management of cash

in the organisation. It helps predict all the necessary areas where cash will be needed and by

what source will the business receive cash.

cash.

As per the analysis and observation of the author it is clear that there are some changes

which can be made in the approach and management of the company to be more profitable ,

generate more revenue and increase cash inflow. The company can increase its commission from

3% to 4-5%. A nominal change like this can have a huge impact over the cash inflow and

profitability of the business. It can further make a new policy of receiving the entire commission

in the month of sale, so that it can have more funds to spare and carry out all the necessary

business operations.

CONCLUSION

The above report concludes and describes the importance of analysing cash flow and

profit for any business organisation. Multiple tools and methods are used by various

organisations which helps them in stabilising the business and increasing profitability and cash

flow. Working capital management is on of the above said tools which helps in managing the

working capital of the business. Cash Budget play a significant role in the management of cash

in the organisation. It helps predict all the necessary areas where cash will be needed and by

what source will the business receive cash.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.