Impact of Working Capital Management on UK Retail Profitability

VerifiedAdded on 2020/06/06

|46

|13033

|28

Report

AI Summary

This report delves into the impact of working capital management on the profitability of businesses within the UK retail sector, covering the period from 2013 to 2017. The study begins with an introduction outlining the background, aims, objectives, research questions, rationale, and significance of the investigation, followed by a structured literature review exploring working capital management, determinants of profitability, relevant theories, and the research gap. The topic description focuses on the UK retail sector and the necessity of working capital management. The methodology chapter details the research approach, philosophy, strategies, data collection, and analysis methods. The analysis and findings are presented in chapter five, followed by a discussion of the results. The report concludes with a summary of findings, recommendations, and a list of references and bibliography. The report examines factors affecting working capital management, the extent of its influence on profitability, and suggests strategies for effective management to enhance margins within the UK retail sector, utilizing data from major UK retailers such as Tesco, Sainsbury, Morrison’s, and OCADO.

IMPACT OF WORKING CAPITAL MANAGEMENT ON

BUSINESS PROFITABILITY INTHE UK

RETAILSECTOR

(A study of data covered the period 2013-2017)

1

BUSINESS PROFITABILITY INTHE UK

RETAILSECTOR

(A study of data covered the period 2013-2017)

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION....................................................................................................1

Background of the study..............................................................................................................1

Research aim and objectives........................................................................................................1

Research questions.......................................................................................................................2

Rationale of the study..................................................................................................................2

Significance of the study.............................................................................................................2

Structure of the dissertation.........................................................................................................3

CHAPTER 2: LITERATURE REVIEW.........................................................................................4

Working capital management and factors that have influence on it............................................4

Determinants of profitability in retail sector...............................................................................6

Theories of working capital.........................................................................................................7

Impact of working capital management on organizational profitability...................................11

Research gap..............................................................................................................................13

CHAPTER 3: TOPIC DESCRIPTION.........................................................................................14

UK retail sector..........................................................................................................................14

Need of working capital management in UK retail sector and factors that affect the same......14

CHAPTER 4: RESEARCH METHODOLOGY...........................................................................16

Research type.............................................................................................................................16

Research approach.....................................................................................................................16

Research philosophy..................................................................................................................17

Research problems.....................................................................................................................17

Research questions.....................................................................................................................17

Research strategies.....................................................................................................................17

Data collection...........................................................................................................................18

2

CHAPTER 1: INTRODUCTION....................................................................................................1

Background of the study..............................................................................................................1

Research aim and objectives........................................................................................................1

Research questions.......................................................................................................................2

Rationale of the study..................................................................................................................2

Significance of the study.............................................................................................................2

Structure of the dissertation.........................................................................................................3

CHAPTER 2: LITERATURE REVIEW.........................................................................................4

Working capital management and factors that have influence on it............................................4

Determinants of profitability in retail sector...............................................................................6

Theories of working capital.........................................................................................................7

Impact of working capital management on organizational profitability...................................11

Research gap..............................................................................................................................13

CHAPTER 3: TOPIC DESCRIPTION.........................................................................................14

UK retail sector..........................................................................................................................14

Need of working capital management in UK retail sector and factors that affect the same......14

CHAPTER 4: RESEARCH METHODOLOGY...........................................................................16

Research type.............................................................................................................................16

Research approach.....................................................................................................................16

Research philosophy..................................................................................................................17

Research problems.....................................................................................................................17

Research questions.....................................................................................................................17

Research strategies.....................................................................................................................17

Data collection...........................................................................................................................18

2

Data analysis..............................................................................................................................18

Ethical considerations................................................................................................................19

Reliability and validity..............................................................................................................19

Research limitations...................................................................................................................19

CHAPTER 5: ANALYSIS AND FINDINGS...............................................................................20

Findings.....................................................................................................................................20

CHAPTER 6: DISCUSSION........................................................................................................31

CHAPTER 7: CONCLUSION AND RECOMMENDATIONS...................................................34

7.1 Conclusion...........................................................................................................................34

7.2 Recommendations................................................................................................................36

REFERENCES..............................................................................................................................38

BIBLIOGRAPHY..........................................................................................................................42

3

Ethical considerations................................................................................................................19

Reliability and validity..............................................................................................................19

Research limitations...................................................................................................................19

CHAPTER 5: ANALYSIS AND FINDINGS...............................................................................20

Findings.....................................................................................................................................20

CHAPTER 6: DISCUSSION........................................................................................................31

CHAPTER 7: CONCLUSION AND RECOMMENDATIONS...................................................34

7.1 Conclusion...........................................................................................................................34

7.2 Recommendations................................................................................................................36

REFERENCES..............................................................................................................................38

BIBLIOGRAPHY..........................................................................................................................42

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CHAPTER 1: INTRODUCTION

Background of the study

Working capital management may be served as a managerial accounting strategy that lays

emphasis on ensuring efficient or smooth operations of the company. In the context of business

unit, the main motives of working capital management are to ensure high liquidity and maximise

both profitability as well as shareholders value. Hence, working capital management refers to the

ability of business unit in relation to controlling both current assets and liabilities prominently.

Effective management enables firm to generate high return from assets and facilitates reduction

in payment associated with the liabilities. Hence, effective management of working capital plays

a vital role in meeting shareholders objective regarding maximisation of value.It can be depicted

that working capital management has an impact on both liquidity as well as profitability aspect

of the company. However, companies face issue in relation to increasing profit margin at the cost

of liquidity. Thus, present study will examine the influence of working capital management on

organisational profitability.

For this dissertation, leading retail organisations of UK have been selected such as Tesco,

Sainsbury, Morrison’s and OCADO. All such business organisations offer retail products or

services to the customers at suitable prices. Further, all such companies are listed on the

recognised stock exchange of London such as FTSE 100. In this, dissertation will provide deeper

insight about the factors that affect working capital management of companies working in UK

retail sector. Such dissertation will also shed light on the level to which working capital

management practices undertaken by the firm has an influence on the profitability of retail

business units.

Research aim and objectives

Aim

The main aim or motive behind carry out present study is ‘To analyze the impact of

working capital management on business profitability in the context of UK retail sector.’

1

Background of the study

Working capital management may be served as a managerial accounting strategy that lays

emphasis on ensuring efficient or smooth operations of the company. In the context of business

unit, the main motives of working capital management are to ensure high liquidity and maximise

both profitability as well as shareholders value. Hence, working capital management refers to the

ability of business unit in relation to controlling both current assets and liabilities prominently.

Effective management enables firm to generate high return from assets and facilitates reduction

in payment associated with the liabilities. Hence, effective management of working capital plays

a vital role in meeting shareholders objective regarding maximisation of value.It can be depicted

that working capital management has an impact on both liquidity as well as profitability aspect

of the company. However, companies face issue in relation to increasing profit margin at the cost

of liquidity. Thus, present study will examine the influence of working capital management on

organisational profitability.

For this dissertation, leading retail organisations of UK have been selected such as Tesco,

Sainsbury, Morrison’s and OCADO. All such business organisations offer retail products or

services to the customers at suitable prices. Further, all such companies are listed on the

recognised stock exchange of London such as FTSE 100. In this, dissertation will provide deeper

insight about the factors that affect working capital management of companies working in UK

retail sector. Such dissertation will also shed light on the level to which working capital

management practices undertaken by the firm has an influence on the profitability of retail

business units.

Research aim and objectives

Aim

The main aim or motive behind carry out present study is ‘To analyze the impact of

working capital management on business profitability in the context of UK retail sector.’

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Objectives: Considering the above aim following objectives have been drafted by the scholar

such as:

To investigate the factors that affect working capital management.

To ascertain the influence of working capital management on the profitability of UK

retail sector.

To recommend ways through which firm operating in UK retail sector can ensure

effective working capital management and thereby enhance margin.

Research questions

Q.1 What kind of factors affect working capital management?

Q.2 What is the extent to which working capital management practices influence the profitability

of UK retail sector?

Rationale of the study

In the current times, UK retail sector is filled up with the high level of competition which

in turn has direct impact on the profitability of concerned units. Business units perform or carry

out activities with the motive to attain high profit margin. Hence, the main reason behind

conducting such investigation is to ascertain the level to working capital management impacts

organizational profitability. This is recognised as an issue because some firms maintain high

working capital over the ideal standards. Hence, through the means of quantitative evaluation

such study sheds light on the manner in which working capital management affects profitability

of business units working in UK retail sector.

Significance of the study

The present study and its findings are highly important for the firms operating in UK

retail sector. Such study will help the management team of retail units in understanding the

manner in which aspects of working capital management impact profitability. Besides this,

outcome of the concerned study will also help retail business organisations in developing

appropriate framework. In addition to this, study related to working capital management and

profitability will also help other scholars who want to conduct study on such topic. Hence, by

undertaking the concerned study, other scholars would become able to develop hypothesis for

further investigation.

2

such as:

To investigate the factors that affect working capital management.

To ascertain the influence of working capital management on the profitability of UK

retail sector.

To recommend ways through which firm operating in UK retail sector can ensure

effective working capital management and thereby enhance margin.

Research questions

Q.1 What kind of factors affect working capital management?

Q.2 What is the extent to which working capital management practices influence the profitability

of UK retail sector?

Rationale of the study

In the current times, UK retail sector is filled up with the high level of competition which

in turn has direct impact on the profitability of concerned units. Business units perform or carry

out activities with the motive to attain high profit margin. Hence, the main reason behind

conducting such investigation is to ascertain the level to working capital management impacts

organizational profitability. This is recognised as an issue because some firms maintain high

working capital over the ideal standards. Hence, through the means of quantitative evaluation

such study sheds light on the manner in which working capital management affects profitability

of business units working in UK retail sector.

Significance of the study

The present study and its findings are highly important for the firms operating in UK

retail sector. Such study will help the management team of retail units in understanding the

manner in which aspects of working capital management impact profitability. Besides this,

outcome of the concerned study will also help retail business organisations in developing

appropriate framework. In addition to this, study related to working capital management and

profitability will also help other scholars who want to conduct study on such topic. Hence, by

undertaking the concerned study, other scholars would become able to develop hypothesis for

further investigation.

2

Structure of the dissertation

Chapter 1: Introduction

In the first chapter of dissertation, background as well as aims and objectives have been

included by the researcher. Further, researcher has also mentioned motives or rationale behind

conducting present investigation. Under introductory chapter, structure of the whole dissertation

has also been included.

Chapter 2: Literature review

Under second chapter, brief thesis has been prepared by making evaluation of books,

journals and scholarly articles pertaining to working capital management. Hence, through

evaluating scholarly articles, aim such as ‘influence of working capital management on firm’s

profitability’ has been achieved briefly.

Chapter 3: Research methodology

This chapter of dissertation presents methods, tools and techniques that have been

employed for addressing research questions. Hence, in the 3rd chapter, research type and

approach as well as technique pertaining to data collection along with analysis has been

included.

Chapter 4: Data analysis and findings

Fourth chapter of dissertation is highly significant which reflects or presents the solution

of concerned issue. In this, all the findings have clearly been supported with the articles

evaluated in the literature review section.

Chapter 5: Conclusion & recommendations

Final chapter of dissertation presents overall findings or outcome in a conclusive

formatas per research aim and objectives. Along with this, it also includes recommendations or

suggestions that can be undertaken by retail units for making improvement in working capital

management and thereby profitability.

3

Chapter 1: Introduction

In the first chapter of dissertation, background as well as aims and objectives have been

included by the researcher. Further, researcher has also mentioned motives or rationale behind

conducting present investigation. Under introductory chapter, structure of the whole dissertation

has also been included.

Chapter 2: Literature review

Under second chapter, brief thesis has been prepared by making evaluation of books,

journals and scholarly articles pertaining to working capital management. Hence, through

evaluating scholarly articles, aim such as ‘influence of working capital management on firm’s

profitability’ has been achieved briefly.

Chapter 3: Research methodology

This chapter of dissertation presents methods, tools and techniques that have been

employed for addressing research questions. Hence, in the 3rd chapter, research type and

approach as well as technique pertaining to data collection along with analysis has been

included.

Chapter 4: Data analysis and findings

Fourth chapter of dissertation is highly significant which reflects or presents the solution

of concerned issue. In this, all the findings have clearly been supported with the articles

evaluated in the literature review section.

Chapter 5: Conclusion & recommendations

Final chapter of dissertation presents overall findings or outcome in a conclusive

formatas per research aim and objectives. Along with this, it also includes recommendations or

suggestions that can be undertaken by retail units for making improvement in working capital

management and thereby profitability.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CHAPTER 2: LITERATURE REVIEW

Literature review may be served as a scholarly paper that contains findings of different

articles related to the issue. In literature review section, varied books, journals and scholarly

articles are evaluated for the development of brief thesis. Under this, contradictory views are

recorded which in turn presented by different scholars. This chapter of dissertation is highly

important which develops understanding about topic and provides assistance in analysing data

set appropriately. In this, several books and scholarly articles have been analysed by the scholar

related to working capital management.

Working capital management and factors that have influence on it

Bhattacharya (2014) stated working capital as a fund that is required to meet day to day

financial needs for business concern. It includes payment to creditors, payment of salary to

workers, raw material purchase etc. According to the views of Pais and Gama (2015), working

capital management implies for the accounting strategy that helps in maintaining both the

components associated with it such as current assets and liabilities. It ensures or renders

information about the extent to which business unit has enough funds for meeting its short term

debt obligations and operating expenses. In the business unit, effectual implementation of

working capital management is highly required within the company for enhancing earnings.

Further, Aktas, Croci and Petmezas (2015) defined working capital management as a decision

and strategic framework employed by the business unit to deal with the obligation more

effectually. In the context of large sized business unit, prominent working capital management is

required because it not only reduces profitability but also impacts leverage position.

Baños-Caballero García-Teruel and Martínez-Solano (2014) assessed in the study that

both excessive and inadequate working capital is harmful for the business unit. The reason

behind this, in the case of excessive working capital firm would not be in position to generate

income from scare funds in the form of interest etc. In contrast to this, in the case of having

inadequate funds business unit would not be in position to carry out activities smoothly. Sagner

(2014) said that working capital management is highly associated with the planning and

controlling current assets as well as liabilities which in turn avoids inability in relation to

meeting debt or obligations. Hence, effectual working capital management can be ensured by

4

Literature review may be served as a scholarly paper that contains findings of different

articles related to the issue. In literature review section, varied books, journals and scholarly

articles are evaluated for the development of brief thesis. Under this, contradictory views are

recorded which in turn presented by different scholars. This chapter of dissertation is highly

important which develops understanding about topic and provides assistance in analysing data

set appropriately. In this, several books and scholarly articles have been analysed by the scholar

related to working capital management.

Working capital management and factors that have influence on it

Bhattacharya (2014) stated working capital as a fund that is required to meet day to day

financial needs for business concern. It includes payment to creditors, payment of salary to

workers, raw material purchase etc. According to the views of Pais and Gama (2015), working

capital management implies for the accounting strategy that helps in maintaining both the

components associated with it such as current assets and liabilities. It ensures or renders

information about the extent to which business unit has enough funds for meeting its short term

debt obligations and operating expenses. In the business unit, effectual implementation of

working capital management is highly required within the company for enhancing earnings.

Further, Aktas, Croci and Petmezas (2015) defined working capital management as a decision

and strategic framework employed by the business unit to deal with the obligation more

effectually. In the context of large sized business unit, prominent working capital management is

required because it not only reduces profitability but also impacts leverage position.

Baños-Caballero García-Teruel and Martínez-Solano (2014) assessed in the study that

both excessive and inadequate working capital is harmful for the business unit. The reason

behind this, in the case of excessive working capital firm would not be in position to generate

income from scare funds in the form of interest etc. In contrast to this, in the case of having

inadequate funds business unit would not be in position to carry out activities smoothly. Sagner

(2014) said that working capital management is highly associated with the planning and

controlling current assets as well as liabilities which in turn avoids inability in relation to

meeting debt or obligations. Hence, effectual working capital management can be ensured by

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business unit through understanding the factors which in turn have influence on it. Barth and

et.al., (2017)exhibited in their study that efficient or effective working capital management is

needed to create and enhance shareholder’s value. The main motives of the company behind

undertaking working capital management practices are to maximize profit margin. Thus,

effective management of working capital is highly required to fulfil organizational goals and

objectives.

Vernimmen and Quiry (2018) depicted in their study there is no specific set of rules that

can be used to determine working capital. However, there are several factors which in turn have

high level of influence on it. In the context of business unit, need of working capital is highly

significant for financing day to day activities of firm. On the other side, Afrifa and Tingbani

(2018) said that need regarding working capital of different business units vary significantly.

Moreover, when business unit grows then level of both output and current assets enhances

significantly. Apart from this, level of working capital is also highly dependent on the policies

employed by the firm to manage current assets. Companies with no inventory, debtors, creditors

and little investment generate low or no margin.

In their study, Lind, Pirttilä and Schupp (2018) revealed that nature of business is the

main factor that affects working capital requirement. For instance: In the case of retail business

manager does not require to maintain high working capital. Moreover, due to having small

operating cycle retail business owners do not require to maintain high working capital. Retail

business organizations usually sell products or services on cash terms or basis due to which their

operating cycle is less over others. However, it is to be critically evaluated by Enqvist, Graham

and Nikkinen (2014), who stated that not all kind of retail unit’s have small operating cycle. In

the current times, large sized retail units are involved in manufacturing of products with the

motive to enhance brand image. This aspect shows that not all retail business units require less

working capital. Large retail units, involve in manufacturing activities, have to convert raw

material into finished goods as well as need to maintain enough stock of the same.

Ukaegbu (2014) shared their views that scale of operations has significant impact on the

requirement of working capital. Firms which are operating at large level need to maintain enough

stock, cash, debtors etc and vice versa. In contrast to this, Agha (2014) suggested that at the time

of working capital determination manager needs to consider business cycle fluctuations. On the

5

et.al., (2017)exhibited in their study that efficient or effective working capital management is

needed to create and enhance shareholder’s value. The main motives of the company behind

undertaking working capital management practices are to maximize profit margin. Thus,

effective management of working capital is highly required to fulfil organizational goals and

objectives.

Vernimmen and Quiry (2018) depicted in their study there is no specific set of rules that

can be used to determine working capital. However, there are several factors which in turn have

high level of influence on it. In the context of business unit, need of working capital is highly

significant for financing day to day activities of firm. On the other side, Afrifa and Tingbani

(2018) said that need regarding working capital of different business units vary significantly.

Moreover, when business unit grows then level of both output and current assets enhances

significantly. Apart from this, level of working capital is also highly dependent on the policies

employed by the firm to manage current assets. Companies with no inventory, debtors, creditors

and little investment generate low or no margin.

In their study, Lind, Pirttilä and Schupp (2018) revealed that nature of business is the

main factor that affects working capital requirement. For instance: In the case of retail business

manager does not require to maintain high working capital. Moreover, due to having small

operating cycle retail business owners do not require to maintain high working capital. Retail

business organizations usually sell products or services on cash terms or basis due to which their

operating cycle is less over others. However, it is to be critically evaluated by Enqvist, Graham

and Nikkinen (2014), who stated that not all kind of retail unit’s have small operating cycle. In

the current times, large sized retail units are involved in manufacturing of products with the

motive to enhance brand image. This aspect shows that not all retail business units require less

working capital. Large retail units, involve in manufacturing activities, have to convert raw

material into finished goods as well as need to maintain enough stock of the same.

Ukaegbu (2014) shared their views that scale of operations has significant impact on the

requirement of working capital. Firms which are operating at large level need to maintain enough

stock, cash, debtors etc and vice versa. In contrast to this, Agha (2014) suggested that at the time

of working capital determination manager needs to consider business cycle fluctuations. On the

5

basis of such aspect, during boom period, flourishing market results into more demand,

production, inventory, debtors etc. It shows that high working capital is needed during

inflationary or boom period. Pais and Gama (2015) assessed technology and production cycle as

the main factor which in turn influences need of working capital. For instance: If business unit

undertakes labour intensive production technique then more working capital is required. Under

such situation, firm requires money for making payment to labours so it needs high fund to meet

daily needs. On the other side, in the case of machine intensive technique there is fixed capital

requirement which in turn resulted into less operating expenditure.

Iqbal, Ahmad and Riaz (2014) showcased operating efficiency as the main factor that

affects the need of working capital. Firms which maintain high level of efficiency have low

wastage so they need less funds for daily activities. Further, highly efficient firms can also

manage operations with lower level of inventory and bear less expense. All such aspects show

that as compared to lower, highly efficient firms need less money for carrying out daily

activities. In accordance with Yazdanfar and Öhman (2014), extent of competition may also be

served as a major factor that impacts the need of working capital. In the highly competitive

market, company is compelled to offer easy payment or credit policies to the customers. Further,

for gaining competitive edge over others, business unit needs to ensure that supply is on time. In

this, for providing customers with the product they need high stock requires to be maintained

within the firm. It presents positive relationship between level of competition and working

capital requirement. In other words, high funds are needed when competition level enhances

within the industry.

Determinants of profitability in retail sector

Ahmad, Ahmed and Samim (2018) found in their study that there are mainly four

components which in turn have significant impact on organisation’s working capital such as

cash, marketable securities, inventory and accounts receivable. Hence, for the management of

working capital, business unit needs to exert control on such aspects or variables. Afrifa and

Tingbani (2018) identified that inventory is one of the main element of working capital

management that affects profitability aspect of the firm to a great extent. The rationale behind

this, excessive inventory level places financial burden in front of firm. Moreover, excessive

inventory imposes holding cost and thereby impacts both expense level as well as margin. On the

6

production, inventory, debtors etc. It shows that high working capital is needed during

inflationary or boom period. Pais and Gama (2015) assessed technology and production cycle as

the main factor which in turn influences need of working capital. For instance: If business unit

undertakes labour intensive production technique then more working capital is required. Under

such situation, firm requires money for making payment to labours so it needs high fund to meet

daily needs. On the other side, in the case of machine intensive technique there is fixed capital

requirement which in turn resulted into less operating expenditure.

Iqbal, Ahmad and Riaz (2014) showcased operating efficiency as the main factor that

affects the need of working capital. Firms which maintain high level of efficiency have low

wastage so they need less funds for daily activities. Further, highly efficient firms can also

manage operations with lower level of inventory and bear less expense. All such aspects show

that as compared to lower, highly efficient firms need less money for carrying out daily

activities. In accordance with Yazdanfar and Öhman (2014), extent of competition may also be

served as a major factor that impacts the need of working capital. In the highly competitive

market, company is compelled to offer easy payment or credit policies to the customers. Further,

for gaining competitive edge over others, business unit needs to ensure that supply is on time. In

this, for providing customers with the product they need high stock requires to be maintained

within the firm. It presents positive relationship between level of competition and working

capital requirement. In other words, high funds are needed when competition level enhances

within the industry.

Determinants of profitability in retail sector

Ahmad, Ahmed and Samim (2018) found in their study that there are mainly four

components which in turn have significant impact on organisation’s working capital such as

cash, marketable securities, inventory and accounts receivable. Hence, for the management of

working capital, business unit needs to exert control on such aspects or variables. Afrifa and

Tingbani (2018) identified that inventory is one of the main element of working capital

management that affects profitability aspect of the firm to a great extent. The rationale behind

this, excessive inventory level places financial burden in front of firm. Moreover, excessive

inventory imposes holding cost and thereby impacts both expense level as well as margin. On the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other side, insufficient inventory places negative impact on brand image and customer

satisfaction. Thus, effective working capital management policy needs to be undertaken for

avoiding unnecessary investments.

Titman, Keown and Martin (2017) mentioned in their study that credit policies

undertaken by business unit also have greater influence on the management of working capital

via accounts receivable. Moreover, liberal credit policies act as a barrier in fund collection and

resulted into high debt. However, on the critical note, Singh, Kumar and Colombage (2017)

entailed that in the current times for enhancing sales or turnover companies have to grant credit

for longer terms. On the basis of such aspect, if credit policies of the firm are not in line with the

competitors then it will lose customers. Further, Singh, Kumar and Colombage (2017) stated that

cash is one of the main elements that needed for carry out day to day operations prominently.

Cash is considered as one of the main variable that impacts working capital and thereby overall

operations. Maintenance of optimal cash balance within the firm is the prior requirement for the

attainment of desired level of outcome or success. Moreover, in the case of holding excessive

cash balance firm will forego interest income. On the other side, inadequate cash balance impacts

operating and day to day activities of firm. Further, Tran, Abbott and Jin Yap (2017)claimed

thatcreditors are one of the main part of effectual or prominent cash management. Company

enjoys high financial benefit in term of margin when its credit turnover ratio is low.

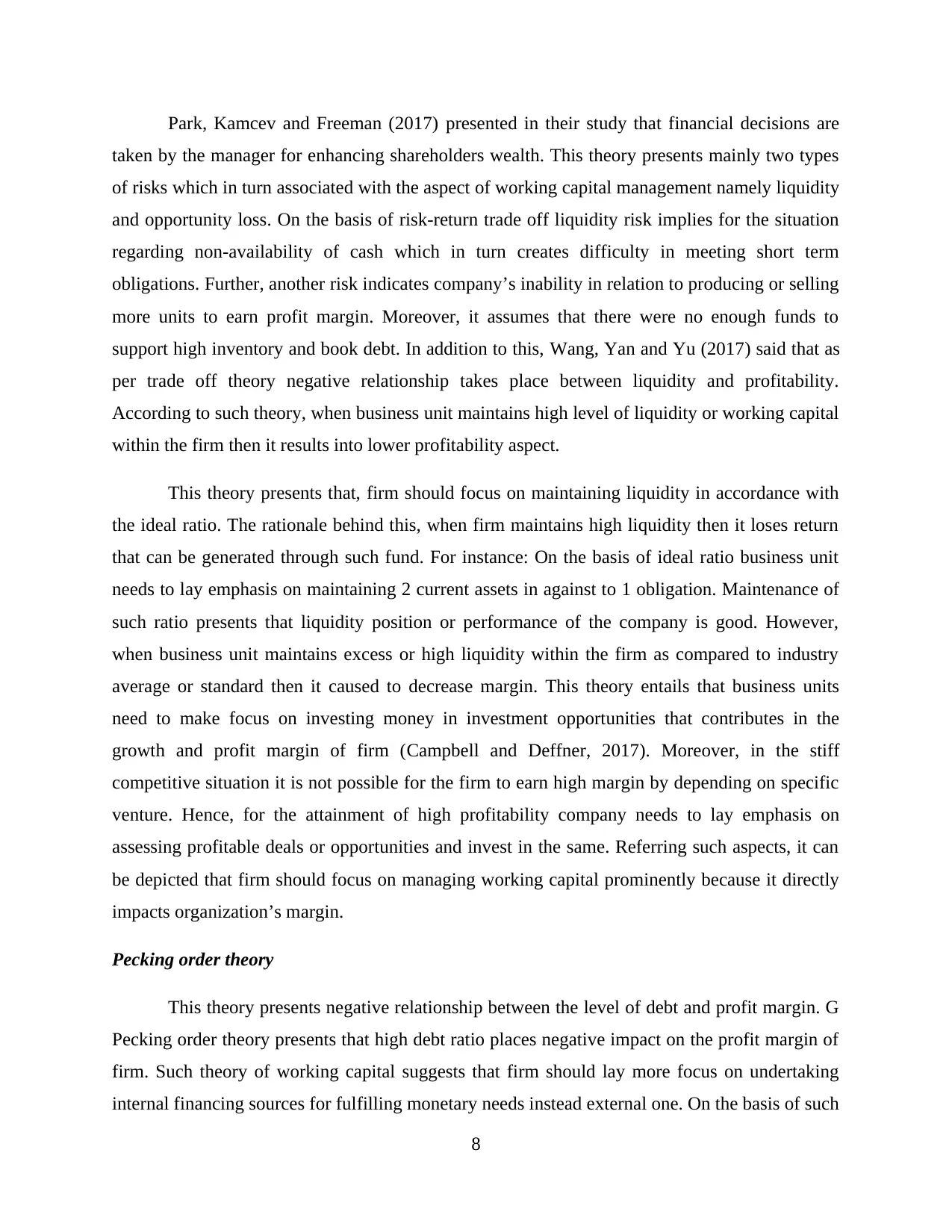

Theories of working capital

(Source: Wang, Yan and Yu, 2017)

Trade-off theory

7

satisfaction. Thus, effective working capital management policy needs to be undertaken for

avoiding unnecessary investments.

Titman, Keown and Martin (2017) mentioned in their study that credit policies

undertaken by business unit also have greater influence on the management of working capital

via accounts receivable. Moreover, liberal credit policies act as a barrier in fund collection and

resulted into high debt. However, on the critical note, Singh, Kumar and Colombage (2017)

entailed that in the current times for enhancing sales or turnover companies have to grant credit

for longer terms. On the basis of such aspect, if credit policies of the firm are not in line with the

competitors then it will lose customers. Further, Singh, Kumar and Colombage (2017) stated that

cash is one of the main elements that needed for carry out day to day operations prominently.

Cash is considered as one of the main variable that impacts working capital and thereby overall

operations. Maintenance of optimal cash balance within the firm is the prior requirement for the

attainment of desired level of outcome or success. Moreover, in the case of holding excessive

cash balance firm will forego interest income. On the other side, inadequate cash balance impacts

operating and day to day activities of firm. Further, Tran, Abbott and Jin Yap (2017)claimed

thatcreditors are one of the main part of effectual or prominent cash management. Company

enjoys high financial benefit in term of margin when its credit turnover ratio is low.

Theories of working capital

(Source: Wang, Yan and Yu, 2017)

Trade-off theory

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Park, Kamcev and Freeman (2017) presented in their study that financial decisions are

taken by the manager for enhancing shareholders wealth. This theory presents mainly two types

of risks which in turn associated with the aspect of working capital management namely liquidity

and opportunity loss. On the basis of risk-return trade off liquidity risk implies for the situation

regarding non-availability of cash which in turn creates difficulty in meeting short term

obligations. Further, another risk indicates company’s inability in relation to producing or selling

more units to earn profit margin. Moreover, it assumes that there were no enough funds to

support high inventory and book debt. In addition to this, Wang, Yan and Yu (2017) said that as

per trade off theory negative relationship takes place between liquidity and profitability.

According to such theory, when business unit maintains high level of liquidity or working capital

within the firm then it results into lower profitability aspect.

This theory presents that, firm should focus on maintaining liquidity in accordance with

the ideal ratio. The rationale behind this, when firm maintains high liquidity then it loses return

that can be generated through such fund. For instance: On the basis of ideal ratio business unit

needs to lay emphasis on maintaining 2 current assets in against to 1 obligation. Maintenance of

such ratio presents that liquidity position or performance of the company is good. However,

when business unit maintains excess or high liquidity within the firm as compared to industry

average or standard then it caused to decrease margin. This theory entails that business units

need to make focus on investing money in investment opportunities that contributes in the

growth and profit margin of firm (Campbell and Deffner, 2017). Moreover, in the stiff

competitive situation it is not possible for the firm to earn high margin by depending on specific

venture. Hence, for the attainment of high profitability company needs to lay emphasis on

assessing profitable deals or opportunities and invest in the same. Referring such aspects, it can

be depicted that firm should focus on managing working capital prominently because it directly

impacts organization’s margin.

Pecking order theory

This theory presents negative relationship between the level of debt and profit margin. G

Pecking order theory presents that high debt ratio places negative impact on the profit margin of

firm. Such theory of working capital suggests that firm should lay more focus on undertaking

internal financing sources for fulfilling monetary needs instead external one. On the basis of such

8

taken by the manager for enhancing shareholders wealth. This theory presents mainly two types

of risks which in turn associated with the aspect of working capital management namely liquidity

and opportunity loss. On the basis of risk-return trade off liquidity risk implies for the situation

regarding non-availability of cash which in turn creates difficulty in meeting short term

obligations. Further, another risk indicates company’s inability in relation to producing or selling

more units to earn profit margin. Moreover, it assumes that there were no enough funds to

support high inventory and book debt. In addition to this, Wang, Yan and Yu (2017) said that as

per trade off theory negative relationship takes place between liquidity and profitability.

According to such theory, when business unit maintains high level of liquidity or working capital

within the firm then it results into lower profitability aspect.

This theory presents that, firm should focus on maintaining liquidity in accordance with

the ideal ratio. The rationale behind this, when firm maintains high liquidity then it loses return

that can be generated through such fund. For instance: On the basis of ideal ratio business unit

needs to lay emphasis on maintaining 2 current assets in against to 1 obligation. Maintenance of

such ratio presents that liquidity position or performance of the company is good. However,

when business unit maintains excess or high liquidity within the firm as compared to industry

average or standard then it caused to decrease margin. This theory entails that business units

need to make focus on investing money in investment opportunities that contributes in the

growth and profit margin of firm (Campbell and Deffner, 2017). Moreover, in the stiff

competitive situation it is not possible for the firm to earn high margin by depending on specific

venture. Hence, for the attainment of high profitability company needs to lay emphasis on

assessing profitable deals or opportunities and invest in the same. Referring such aspects, it can

be depicted that firm should focus on managing working capital prominently because it directly

impacts organization’s margin.

Pecking order theory

This theory presents negative relationship between the level of debt and profit margin. G

Pecking order theory presents that high debt ratio places negative impact on the profit margin of

firm. Such theory of working capital suggests that firm should lay more focus on undertaking

internal financing sources for fulfilling monetary needs instead external one. On the basis of such

8

theory, manager follows a hierarchy while choosing financial sources. In this, hierarchy gives

high level of importance to internal financing (Radjamin and Sudana, 2017). On the basis of such

framework, external sources are used by the managers when internal aspects recognized as not

enough. The main reason behind using internal financial sources by the company is that it has no

financial burden. In other words, it can be presented that when business undertakes internal

financing source such as retained profit, then there is no need to make payment of any financial

cost. In this way, internal financing sources help in avoiding additional expenses and thereby

enhances profit margin. However, Allini, Rakha and Caldarelli (2017) criticised pecking order

theory on the basis of the aspect that if business unit fulfil all of its need through internal source

such as retained profit, then it would not become able to offer dividend to the shareholders at

higher rate. This in turn impacts brand image and market share of firm significantly.

De and Banerjee (2017) articulated in their study that as per the hierarchical structure,

company or manager gives high priority to debt over equity. The reason behind this, when

business unit issues new equity, then investors believe that managers think firm is overvalued. In

this, managers take benefit of such over-valuation so investors lay lower level of emphasis on

equity issuance. Ataünal and Aybars (2017) entailed that by taking into account pecking order

theory, firm needs to make focus on using internal sources rather than external to finance their

operations. Moreover, it has significant impact on firm’s value and profitability. As per such

theory, profitability aspect is negatively influenced when leverage of firm increases. Moreover,

debt places negative impact on the profit margin of firm as it imposes burden in terms of interest

payment. By taking into account such aspects, it can be depicted that profitability decreases

when level of leverage enhances.

9

high level of importance to internal financing (Radjamin and Sudana, 2017). On the basis of such

framework, external sources are used by the managers when internal aspects recognized as not

enough. The main reason behind using internal financial sources by the company is that it has no

financial burden. In other words, it can be presented that when business undertakes internal

financing source such as retained profit, then there is no need to make payment of any financial

cost. In this way, internal financing sources help in avoiding additional expenses and thereby

enhances profit margin. However, Allini, Rakha and Caldarelli (2017) criticised pecking order

theory on the basis of the aspect that if business unit fulfil all of its need through internal source

such as retained profit, then it would not become able to offer dividend to the shareholders at

higher rate. This in turn impacts brand image and market share of firm significantly.

De and Banerjee (2017) articulated in their study that as per the hierarchical structure,

company or manager gives high priority to debt over equity. The reason behind this, when

business unit issues new equity, then investors believe that managers think firm is overvalued. In

this, managers take benefit of such over-valuation so investors lay lower level of emphasis on

equity issuance. Ataünal and Aybars (2017) entailed that by taking into account pecking order

theory, firm needs to make focus on using internal sources rather than external to finance their

operations. Moreover, it has significant impact on firm’s value and profitability. As per such

theory, profitability aspect is negatively influenced when leverage of firm increases. Moreover,

debt places negative impact on the profit margin of firm as it imposes burden in terms of interest

payment. By taking into account such aspects, it can be depicted that profitability decreases

when level of leverage enhances.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 46

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.