BUSN20019: Project on Working Capital and Profitability

VerifiedAdded on 2020/09/27

|18

|4777

|378

Project

AI Summary

This project report investigates the relationship between working capital management and profitability in ASX-listed construction companies in Australia. The study utilizes the cash conversion cycle (CCC) and its components (Average Collection Period, Average Payable Period, and Inventory Turnover) to measure working capital, with Return on Total Assets (ROTA) as the profitability measure. Secondary data from four ASX-listed construction firms were analyzed using Pearson’s Correlation and Linear Regression. The results reveal a negative relationship between working capital and profitability, although the statistical significance is not established. The research highlights a statistically significant negative correlation between the average collection period and profitability, suggesting that firms should focus on reducing this period to enhance profitability. The report includes an introduction, literature review, methodology, findings, discussion, and conclusion, along with limitations and suggestions for future research.

Assignment 2

BUSN20019: Professional Project

Term 2, 2018

A Project Report

On

Working Capital Management and its Impact on Profitability:

Evidence from ASX listed Construction Firms

BUSN20019: Professional Project

Term 2, 2018

A Project Report

On

Working Capital Management and its Impact on Profitability:

Evidence from ASX listed Construction Firms

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This research paper examine the relationship between working capital management and

profitability in ASX listed construction companies in Australia. Working capital management

has been measured using cash conversion cycle (CCC) and along with it the other

components such as Average Collection Period, Average Payable Period and Inventory

Turnover in days are analysed. The return on total assets (ROTA) is used as a measure of

profitability and is considered as a dependent variable.

To examine the statistical significance between dependent and independent variables,

Pearson’s Correlation and Linear Regression analysis were performed on secondary data

collected from sample of 4 ASX listed construction companies. The results indicate that

working capital and profitability has no statistical significance however both have negative

relationship. The research shows that average collection period is statistically negatively

significance to the profitability. So, in order to increase the profitability, the firms should

focus more on reducing the average collection period.

1 | P a g e

This research paper examine the relationship between working capital management and

profitability in ASX listed construction companies in Australia. Working capital management

has been measured using cash conversion cycle (CCC) and along with it the other

components such as Average Collection Period, Average Payable Period and Inventory

Turnover in days are analysed. The return on total assets (ROTA) is used as a measure of

profitability and is considered as a dependent variable.

To examine the statistical significance between dependent and independent variables,

Pearson’s Correlation and Linear Regression analysis were performed on secondary data

collected from sample of 4 ASX listed construction companies. The results indicate that

working capital and profitability has no statistical significance however both have negative

relationship. The research shows that average collection period is statistically negatively

significance to the profitability. So, in order to increase the profitability, the firms should

focus more on reducing the average collection period.

1 | P a g e

Contents

1.0 Introduction.....................................................................................................................3

1.1 Problem Statement.......................................................................................................3

1.2 Research Aim, Objectives and Research Questions....................................................4

2. Conceptual Framework..........................................................................................................4

2.1 Working Capital Management.........................................................................................4

2,2 Profitability.......................................................................................................................5

3.0 Literature Review............................................................................................................5

4.0 Methodology........................................................................................................................8

4.1 Data Collection.................................................................................................................8

4.2 Data Analysis...............................................................................................................8

5.0 Findings and analysis...........................................................................................................9

5.1 Descriptive Statistics........................................................................................................9

5.2 Bivariate Correlations Results........................................................................................10

5.3 Regression Analysis Results...........................................................................................11

6.0 Discussion..........................................................................................................................12

7.0 Conclusion..........................................................................................................................13

8.0 Limitations.........................................................................................................................13

9.0 Future research...................................................................................................................14

References................................................................................................................................15

2 | P a g e

1.0 Introduction.....................................................................................................................3

1.1 Problem Statement.......................................................................................................3

1.2 Research Aim, Objectives and Research Questions....................................................4

2. Conceptual Framework..........................................................................................................4

2.1 Working Capital Management.........................................................................................4

2,2 Profitability.......................................................................................................................5

3.0 Literature Review............................................................................................................5

4.0 Methodology........................................................................................................................8

4.1 Data Collection.................................................................................................................8

4.2 Data Analysis...............................................................................................................8

5.0 Findings and analysis...........................................................................................................9

5.1 Descriptive Statistics........................................................................................................9

5.2 Bivariate Correlations Results........................................................................................10

5.3 Regression Analysis Results...........................................................................................11

6.0 Discussion..........................................................................................................................12

7.0 Conclusion..........................................................................................................................13

8.0 Limitations.........................................................................................................................13

9.0 Future research...................................................................................................................14

References................................................................................................................................15

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.0 Introduction

Working Capital Management is a part of everyday life of business managers,

accountants and company directors. It is very crucial for carrying out the daily operations of

the organization as it falls under short term finance of the firm. The failure of business can

result due to inefficiency of working capital management (Zhao, 2011). Being an accounting

student, the study in this topic will definitely uplift my knowledge regarding whether

effective working capital management results in increasing profitability or not in terms of

ASX listed Australian Construction firms as construction industry has the lowest survival rate

among all other industry in Australia. The report starts with the background of the project

along with research aim, objectives and research questions. The second part is the literature

review which is followed by methodology of the study, findings and analysis then discussion

and conclusion.

1.1 Problem Statement

According to Australian Bureau of Statistics (ABS,2016), the construction industry is the

third largest industry in Australia and second largest employer providing jobs opportunities to

people of Australia. However, from the recent survey of Australian Bureau of statistics (ABS,

2016-17), it has been revealed that the survival of Construction Industry in Australia is low in

terms of other industry as the survival rate is rapidly decreasing from 85.7% in 2014 to 60.7%

in 2017. This shows that the number of exits in this industry is very high.

It has been studied that the undercapitalized firms i.e. the firms which are financially weak is

one of the main reasons behind the failure or insolvency of Construction industry (Coggins, J.

et al., 2016). Construction companies have to run various projects at the same time which

may result in the requirement for appropriate level of working capital. And if the project

doesn’t complete on projected time then it leads to increased requirement for capital. So, the

management of the working capital i.e. the short-term capital is very crucial for business

survival, solvency and profitability (Mukhopadhyay, 2004). The development of working

capital optimisation which would suit the construction industry has not been developed yet as

the management of working capital goes far beyond the financial sphere (Meszek, W., &

Polewski, M.,2006).

For a business to survive in a long run, the business must be profitable. As the Australian

construction industry is the third largest industry to provide employment, its survival matters

a lot to the whole industry. No study has been done to know whether effective working

3 | P a g e

Working Capital Management is a part of everyday life of business managers,

accountants and company directors. It is very crucial for carrying out the daily operations of

the organization as it falls under short term finance of the firm. The failure of business can

result due to inefficiency of working capital management (Zhao, 2011). Being an accounting

student, the study in this topic will definitely uplift my knowledge regarding whether

effective working capital management results in increasing profitability or not in terms of

ASX listed Australian Construction firms as construction industry has the lowest survival rate

among all other industry in Australia. The report starts with the background of the project

along with research aim, objectives and research questions. The second part is the literature

review which is followed by methodology of the study, findings and analysis then discussion

and conclusion.

1.1 Problem Statement

According to Australian Bureau of Statistics (ABS,2016), the construction industry is the

third largest industry in Australia and second largest employer providing jobs opportunities to

people of Australia. However, from the recent survey of Australian Bureau of statistics (ABS,

2016-17), it has been revealed that the survival of Construction Industry in Australia is low in

terms of other industry as the survival rate is rapidly decreasing from 85.7% in 2014 to 60.7%

in 2017. This shows that the number of exits in this industry is very high.

It has been studied that the undercapitalized firms i.e. the firms which are financially weak is

one of the main reasons behind the failure or insolvency of Construction industry (Coggins, J.

et al., 2016). Construction companies have to run various projects at the same time which

may result in the requirement for appropriate level of working capital. And if the project

doesn’t complete on projected time then it leads to increased requirement for capital. So, the

management of the working capital i.e. the short-term capital is very crucial for business

survival, solvency and profitability (Mukhopadhyay, 2004). The development of working

capital optimisation which would suit the construction industry has not been developed yet as

the management of working capital goes far beyond the financial sphere (Meszek, W., &

Polewski, M.,2006).

For a business to survive in a long run, the business must be profitable. As the Australian

construction industry is the third largest industry to provide employment, its survival matters

a lot to the whole industry. No study has been done to know whether effective working

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

capital management will lead to increased profitability of ASX listed Construction

Companies.

1.2 Research Aim, Objectives and Research Questions

The aim of this research is to examine the relationship between working capital

management and profitability of ASX listed construction firms.

Some specific research objectives are as follows:

a) To know whether there is significant relationship between working capital

management and firm’s profitability

b) To know how working capital components such as cash conversion cycle

(CCC), average collection policy (ACP), average receivable period (ARP),

Inventory Turnover in Days (ITO) affects profitability.

The research questions to achieve the aim and objectives are:

(a) Is there any significant relationship between working capital management

and profitability in ASX listed Construction Companies?

(b) Does effective management of the working capital result in increased

profitability in ASX listed Construction Companies?

2. Conceptual Framework

2.1 Working Capital Management

Working Capital Management is one of the most important aspect of financial

management a business organization without which the company cannot operate

(Deloof, 2013). The company’s investment on short term assets such as cash,

account receivables, inventories and other short-term assets comprises the

working capital. In other words, it is the management of current assets and

current liabilities so as to maximize the return on assets efficiently and effectively

(Makori, 2013). Many researchers suggest Cash Conversion Cycle (CCC) as the

best measure for the measurement of working capital (Baños et al., 2012). As per

Nobanee et al. (2011), the total time it takes for a company to convert the cash it

has invested in its daily operations to cash received from final goods and services

is known as cash conversion cycle (CCC). CCC is calculated as:

CCC= Average collection period (ACP)+Inventory Turnover Days (ITD)-

Average Payable Period (APP)

4 | P a g e

Companies.

1.2 Research Aim, Objectives and Research Questions

The aim of this research is to examine the relationship between working capital

management and profitability of ASX listed construction firms.

Some specific research objectives are as follows:

a) To know whether there is significant relationship between working capital

management and firm’s profitability

b) To know how working capital components such as cash conversion cycle

(CCC), average collection policy (ACP), average receivable period (ARP),

Inventory Turnover in Days (ITO) affects profitability.

The research questions to achieve the aim and objectives are:

(a) Is there any significant relationship between working capital management

and profitability in ASX listed Construction Companies?

(b) Does effective management of the working capital result in increased

profitability in ASX listed Construction Companies?

2. Conceptual Framework

2.1 Working Capital Management

Working Capital Management is one of the most important aspect of financial

management a business organization without which the company cannot operate

(Deloof, 2013). The company’s investment on short term assets such as cash,

account receivables, inventories and other short-term assets comprises the

working capital. In other words, it is the management of current assets and

current liabilities so as to maximize the return on assets efficiently and effectively

(Makori, 2013). Many researchers suggest Cash Conversion Cycle (CCC) as the

best measure for the measurement of working capital (Baños et al., 2012). As per

Nobanee et al. (2011), the total time it takes for a company to convert the cash it

has invested in its daily operations to cash received from final goods and services

is known as cash conversion cycle (CCC). CCC is calculated as:

CCC= Average collection period (ACP)+Inventory Turnover Days (ITD)-

Average Payable Period (APP)

4 | P a g e

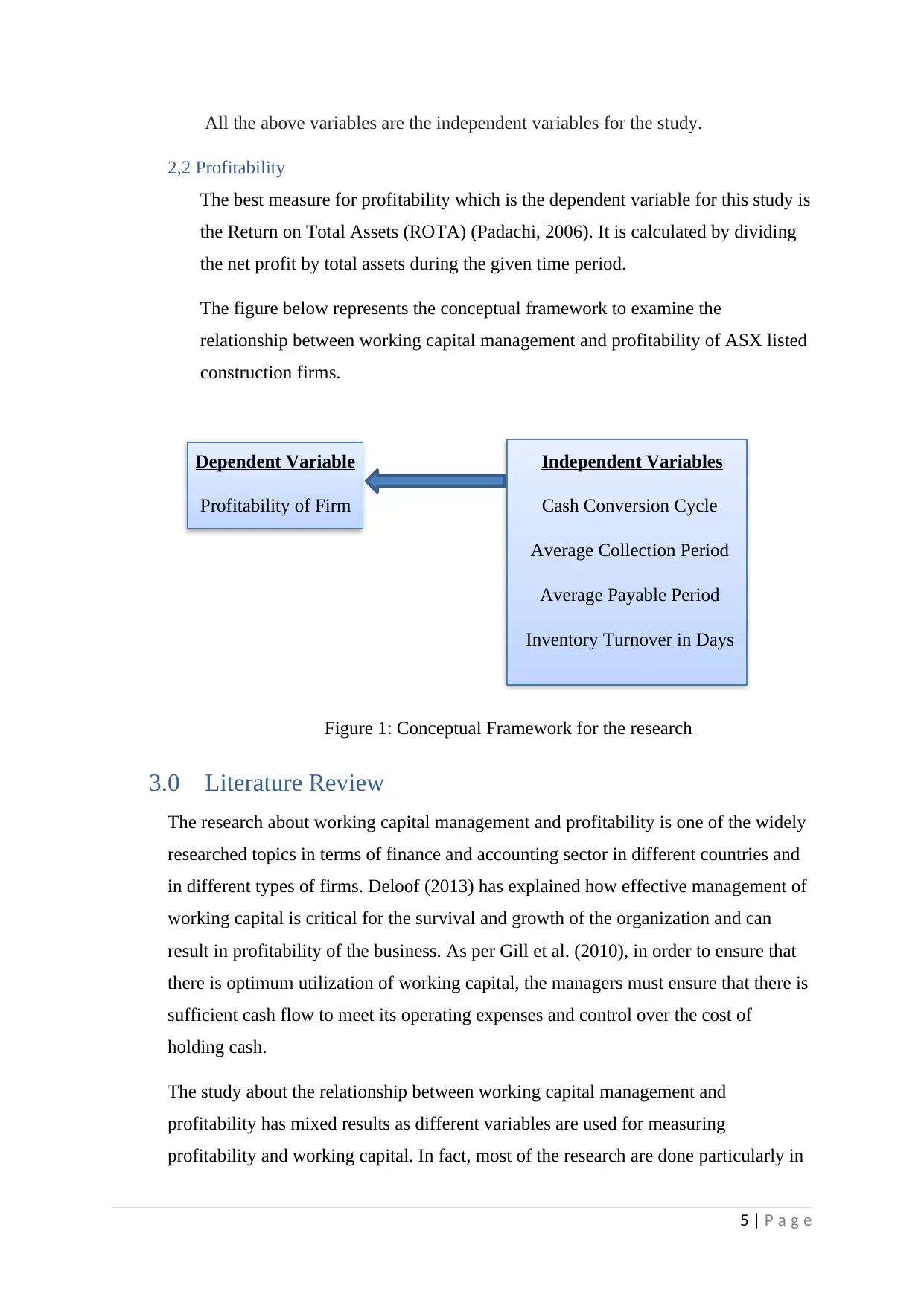

All the above variables are the independent variables for the study.

2,2 Profitability

The best measure for profitability which is the dependent variable for this study is

the Return on Total Assets (ROTA) (Padachi, 2006). It is calculated by dividing

the net profit by total assets during the given time period.

The figure below represents the conceptual framework to examine the

relationship between working capital management and profitability of ASX listed

construction firms.

Dependent Variable Independent Variables

Profitability of Firm Cash Conversion Cycle

Average Collection Period

Average Payable Period

Inventory Turnover in Days

Figure 1: Conceptual Framework for the research

3.0 Literature Review

The research about working capital management and profitability is one of the widely

researched topics in terms of finance and accounting sector in different countries and

in different types of firms. Deloof (2013) has explained how effective management of

working capital is critical for the survival and growth of the organization and can

result in profitability of the business. As per Gill et al. (2010), in order to ensure that

there is optimum utilization of working capital, the managers must ensure that there is

sufficient cash flow to meet its operating expenses and control over the cost of

holding cash.

The study about the relationship between working capital management and

profitability has mixed results as different variables are used for measuring

profitability and working capital. In fact, most of the research are done particularly in

5 | P a g e

2,2 Profitability

The best measure for profitability which is the dependent variable for this study is

the Return on Total Assets (ROTA) (Padachi, 2006). It is calculated by dividing

the net profit by total assets during the given time period.

The figure below represents the conceptual framework to examine the

relationship between working capital management and profitability of ASX listed

construction firms.

Dependent Variable Independent Variables

Profitability of Firm Cash Conversion Cycle

Average Collection Period

Average Payable Period

Inventory Turnover in Days

Figure 1: Conceptual Framework for the research

3.0 Literature Review

The research about working capital management and profitability is one of the widely

researched topics in terms of finance and accounting sector in different countries and

in different types of firms. Deloof (2013) has explained how effective management of

working capital is critical for the survival and growth of the organization and can

result in profitability of the business. As per Gill et al. (2010), in order to ensure that

there is optimum utilization of working capital, the managers must ensure that there is

sufficient cash flow to meet its operating expenses and control over the cost of

holding cash.

The study about the relationship between working capital management and

profitability has mixed results as different variables are used for measuring

profitability and working capital. In fact, most of the research are done particularly in

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

manufacturing firms only and the methodology for the research between those two

variables are also different. Therefore, major gaps have been identified in the section

below so as to be crystal clear about the main aims and objectives of this research.

The effective management of the working capital is possible by considering all the

components of working capital and they are accounts receivable, accounts payable

and inventory (Karaduman et al. 2011). Besides, efficient working capital can be

achieved if CCC is low such that the business can easily convert its investment to

cash received from selling goods and services (Raheman & Nasr, 2007).

According to Bauer (2007), the shorter Average Collection Period (ACP) meaning the

timely receipts from suppliers will improve the firm’s liquidity leading to increased

financial performance. On one hand, the increase in account receivable period through

credit sales will risk the business and on the other hand the decrease in ACP will

effect relationship with suppliers (Moran, 2011). In terms of Inventory turnover

period, holding inventory for a long time can lead to increased carrying costs and

holding up of cash (Kroes & Manikas, 2014). And lower inventory levels can reduce

the sales opportunity a business may have. So, optimal management of inventory is

vital for keeping up the sales. Furthermore, the lesser the average payable period, the

more cash will be available on hold resulting in increased liquidity. However, due to

this the firm can miss early discounts and suppliers may have negative impacts on the

business (Fawcett et al., 2010). Therefore, the management of all these working

capital components is very important for business success and will benefit the

business.

Lazaridis & Tryfonidis (2006) researched about relationship between the corporate

profitability and working capital management of Athens Stock Exchange (ASE) listed

131 firms and found out that there is statistically significant relationship between

them. Here, the profitability was measured through gross operating profit. In this

study, they proved that there exist negative relationship between profitability and cash

conversion cycle. In addition to that, it was concluded that the less profitable firms

will try to reduce their cash gap by decreasing their accounts receivable as both

accounts receivables and profitability had negative relationship.

In the research conducted in United States by Gill et al. (2010) among 88 firms listed

on New York Exchange (NYE) from 2005 to 2007, they found that there is negative

6 | P a g e

variables are also different. Therefore, major gaps have been identified in the section

below so as to be crystal clear about the main aims and objectives of this research.

The effective management of the working capital is possible by considering all the

components of working capital and they are accounts receivable, accounts payable

and inventory (Karaduman et al. 2011). Besides, efficient working capital can be

achieved if CCC is low such that the business can easily convert its investment to

cash received from selling goods and services (Raheman & Nasr, 2007).

According to Bauer (2007), the shorter Average Collection Period (ACP) meaning the

timely receipts from suppliers will improve the firm’s liquidity leading to increased

financial performance. On one hand, the increase in account receivable period through

credit sales will risk the business and on the other hand the decrease in ACP will

effect relationship with suppliers (Moran, 2011). In terms of Inventory turnover

period, holding inventory for a long time can lead to increased carrying costs and

holding up of cash (Kroes & Manikas, 2014). And lower inventory levels can reduce

the sales opportunity a business may have. So, optimal management of inventory is

vital for keeping up the sales. Furthermore, the lesser the average payable period, the

more cash will be available on hold resulting in increased liquidity. However, due to

this the firm can miss early discounts and suppliers may have negative impacts on the

business (Fawcett et al., 2010). Therefore, the management of all these working

capital components is very important for business success and will benefit the

business.

Lazaridis & Tryfonidis (2006) researched about relationship between the corporate

profitability and working capital management of Athens Stock Exchange (ASE) listed

131 firms and found out that there is statistically significant relationship between

them. Here, the profitability was measured through gross operating profit. In this

study, they proved that there exist negative relationship between profitability and cash

conversion cycle. In addition to that, it was concluded that the less profitable firms

will try to reduce their cash gap by decreasing their accounts receivable as both

accounts receivables and profitability had negative relationship.

In the research conducted in United States by Gill et al. (2010) among 88 firms listed

on New York Exchange (NYE) from 2005 to 2007, they found that there is negative

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

relationship between account receivable period and profitability. The profitability

which was measured through gross operating profit had a positive relationship

between cash conversion cycle.

There has been some contradicting findings in relation to the working capital

components and profitability. A study on 263 non-financial firms listed on Bombay

Stock Exchange for the period 2000 to 2008 exhibits the positive relationship between

working capital management and profitability like previous studies done by many

researchers revealed. However, average days in receivable had positive relationship

with the profitability unlike previous studies in working capital and profitability

(Sharma & Kumar, 2011). Padachi (2006) study of 58 small manufacturing firms in

Mauritius stated that there was positive relationship between the profitability and

CCC where profitability was measured by Return on Assets (ROA). Kroes & Manikas

(2014), revealed that in terms of large manufacturing US firms, there was

insignificant relationship between working capital measured through CCC and

profitability.

All the above reviews shows that different researchers has come up with different

results in relation to the working capital, its component and profitability. On top of

that, there is no study on the Australian Firms regarding working capital management

and profitability. In terms of Australia, assets structure, growth and profitability were

revealed as determinants of capital structure and financing of small and medium

enterprises (Cassar, 2003). But no research was conducted on ASX listed firms in

relation to working capital management and profitability. So, this research aims to

know the relationship between working capital and profitability of ASX listed

construction firms as the construction industry is now facing survival difficulty.

The hypothesis developed to conduct the research are:

H0: There is significant relationship between working capital management and

profitability

H1: There is non-significant relationship between working capital management and

profitability.

7 | P a g e

which was measured through gross operating profit had a positive relationship

between cash conversion cycle.

There has been some contradicting findings in relation to the working capital

components and profitability. A study on 263 non-financial firms listed on Bombay

Stock Exchange for the period 2000 to 2008 exhibits the positive relationship between

working capital management and profitability like previous studies done by many

researchers revealed. However, average days in receivable had positive relationship

with the profitability unlike previous studies in working capital and profitability

(Sharma & Kumar, 2011). Padachi (2006) study of 58 small manufacturing firms in

Mauritius stated that there was positive relationship between the profitability and

CCC where profitability was measured by Return on Assets (ROA). Kroes & Manikas

(2014), revealed that in terms of large manufacturing US firms, there was

insignificant relationship between working capital measured through CCC and

profitability.

All the above reviews shows that different researchers has come up with different

results in relation to the working capital, its component and profitability. On top of

that, there is no study on the Australian Firms regarding working capital management

and profitability. In terms of Australia, assets structure, growth and profitability were

revealed as determinants of capital structure and financing of small and medium

enterprises (Cassar, 2003). But no research was conducted on ASX listed firms in

relation to working capital management and profitability. So, this research aims to

know the relationship between working capital and profitability of ASX listed

construction firms as the construction industry is now facing survival difficulty.

The hypothesis developed to conduct the research are:

H0: There is significant relationship between working capital management and

profitability

H1: There is non-significant relationship between working capital management and

profitability.

7 | P a g e

4.0 Methodology

4.1 Data Collection

The data for this research was collected from all the secondary sources. The statistics

about the construction industry was collected from Australian Bureau of Statistics

website: http://www.abs.gov.au/AUSSTATS/abs@.nsf/DetailsPage/8165.0Jun

%202013%20to%20Jun%202017?OpenDocument

The website of ASX (https://www.asx.com.au) and Ibis World (accessed from CQU

university’s computer) (https://www.ibisworld.com.au/) was used to explore more

about the selected construction companies in Australia. The annual report of the

selected 4 construction firms available from the respective company’s website for 12

years period i.e. from 2005-2017 was used. At first all the detail about the net profit,

total assets, opening and ending inventory, opening and ending account receivable,

opening and ending account payable, costs of sale, sales revenue were derived from

their financial statements. Then, Return on Assets (ROA), Average Collection Period

(ACP), Inventory Turnover in days (ITO), Average Payable Period (APP) and Cash

conversion Cycle (CCC) is calculated using their respective formulas in an excel

sheet. A total of 48 observations was formed and analysed.

4.2 Data Analysis

To find the answer to the research questions, quantitative data analysis method

was used where all the data related to the dependent variable (ROTA) and

independent variables (CCC, ACP, ITO in days, APP) were analysed. At first

descriptive analysis was done to know about the relevant phenomena of cash

conversion cycle (CCC) and other variables in an SPSS software (Raheman,

2007). Then, analysis is done using Pearson’s Bivariate Correlation to know

degree of association between variables and then linear regression analysis is done

8 | P a g e

4.1 Data Collection

The data for this research was collected from all the secondary sources. The statistics

about the construction industry was collected from Australian Bureau of Statistics

website: http://www.abs.gov.au/AUSSTATS/abs@.nsf/DetailsPage/8165.0Jun

%202013%20to%20Jun%202017?OpenDocument

The website of ASX (https://www.asx.com.au) and Ibis World (accessed from CQU

university’s computer) (https://www.ibisworld.com.au/) was used to explore more

about the selected construction companies in Australia. The annual report of the

selected 4 construction firms available from the respective company’s website for 12

years period i.e. from 2005-2017 was used. At first all the detail about the net profit,

total assets, opening and ending inventory, opening and ending account receivable,

opening and ending account payable, costs of sale, sales revenue were derived from

their financial statements. Then, Return on Assets (ROA), Average Collection Period

(ACP), Inventory Turnover in days (ITO), Average Payable Period (APP) and Cash

conversion Cycle (CCC) is calculated using their respective formulas in an excel

sheet. A total of 48 observations was formed and analysed.

4.2 Data Analysis

To find the answer to the research questions, quantitative data analysis method

was used where all the data related to the dependent variable (ROTA) and

independent variables (CCC, ACP, ITO in days, APP) were analysed. At first

descriptive analysis was done to know about the relevant phenomena of cash

conversion cycle (CCC) and other variables in an SPSS software (Raheman,

2007). Then, analysis is done using Pearson’s Bivariate Correlation to know

degree of association between variables and then linear regression analysis is done

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

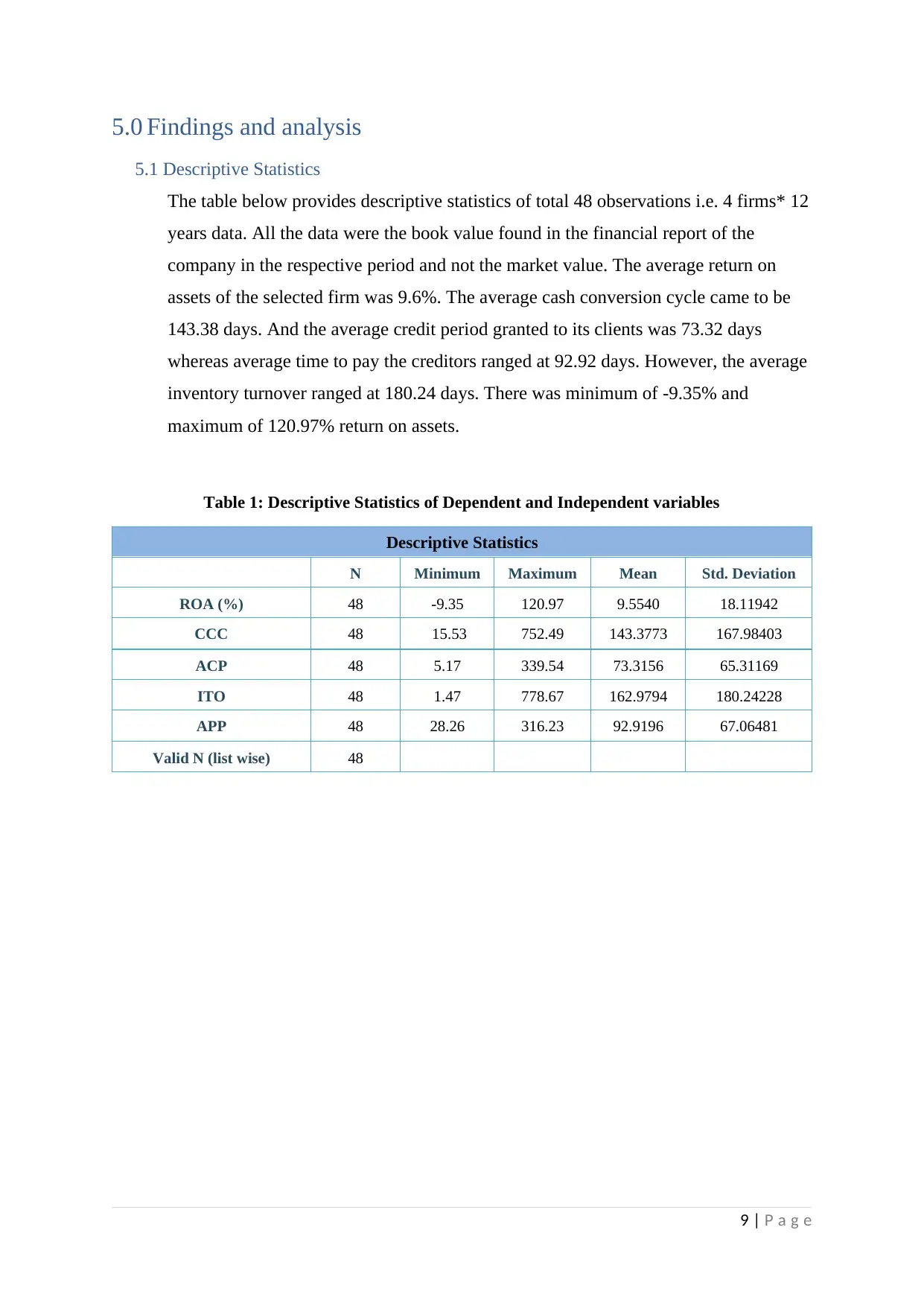

5.0 Findings and analysis

5.1 Descriptive Statistics

The table below provides descriptive statistics of total 48 observations i.e. 4 firms* 12

years data. All the data were the book value found in the financial report of the

company in the respective period and not the market value. The average return on

assets of the selected firm was 9.6%. The average cash conversion cycle came to be

143.38 days. And the average credit period granted to its clients was 73.32 days

whereas average time to pay the creditors ranged at 92.92 days. However, the average

inventory turnover ranged at 180.24 days. There was minimum of -9.35% and

maximum of 120.97% return on assets.

Table 1: Descriptive Statistics of Dependent and Independent variables

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

ROA (%) 48 -9.35 120.97 9.5540 18.11942

CCC 48 15.53 752.49 143.3773 167.98403

ACP 48 5.17 339.54 73.3156 65.31169

ITO 48 1.47 778.67 162.9794 180.24228

APP 48 28.26 316.23 92.9196 67.06481

Valid N (list wise) 48

9 | P a g e

5.1 Descriptive Statistics

The table below provides descriptive statistics of total 48 observations i.e. 4 firms* 12

years data. All the data were the book value found in the financial report of the

company in the respective period and not the market value. The average return on

assets of the selected firm was 9.6%. The average cash conversion cycle came to be

143.38 days. And the average credit period granted to its clients was 73.32 days

whereas average time to pay the creditors ranged at 92.92 days. However, the average

inventory turnover ranged at 180.24 days. There was minimum of -9.35% and

maximum of 120.97% return on assets.

Table 1: Descriptive Statistics of Dependent and Independent variables

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

ROA (%) 48 -9.35 120.97 9.5540 18.11942

CCC 48 15.53 752.49 143.3773 167.98403

ACP 48 5.17 339.54 73.3156 65.31169

ITO 48 1.47 778.67 162.9794 180.24228

APP 48 28.26 316.23 92.9196 67.06481

Valid N (list wise) 48

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

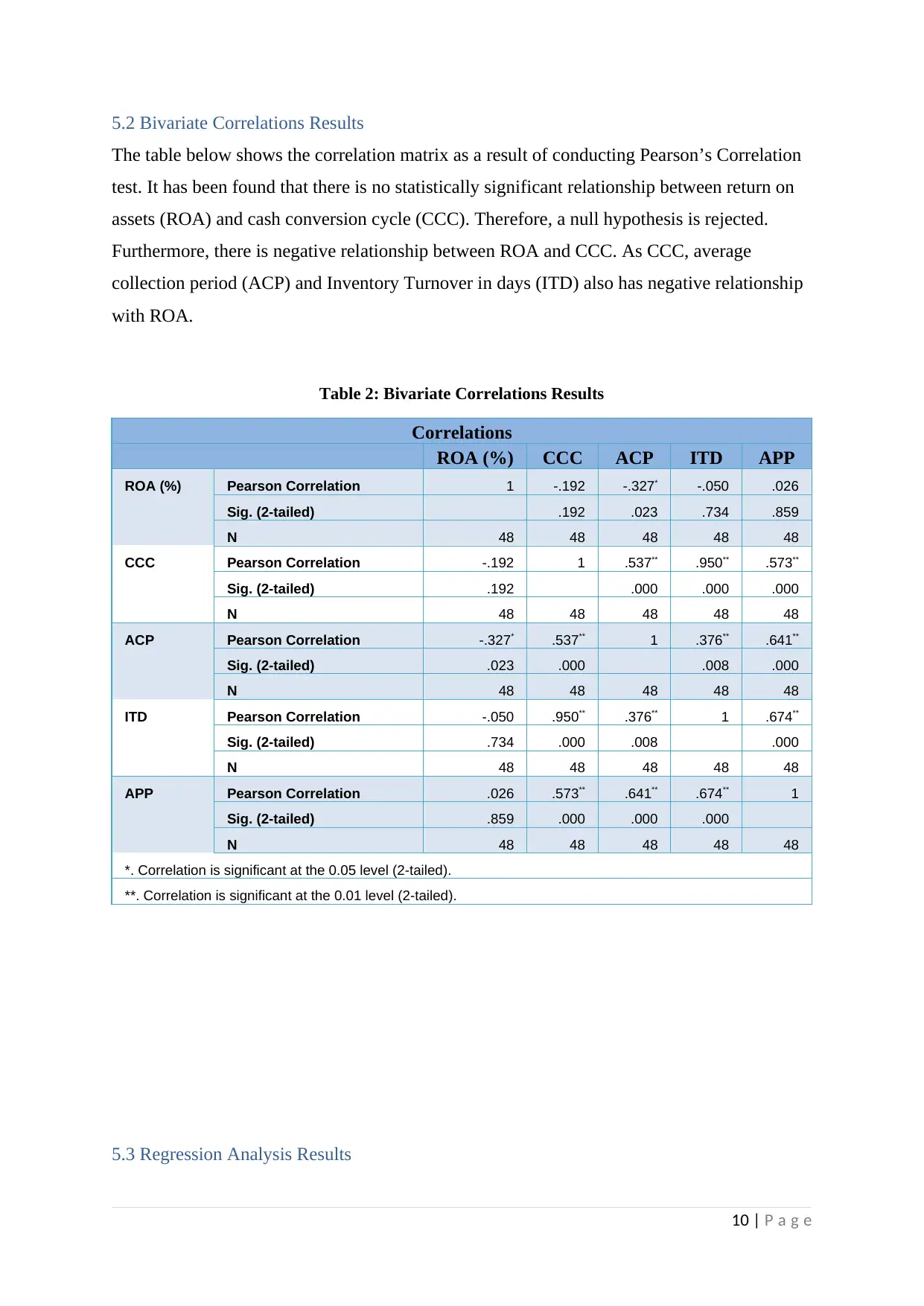

5.2 Bivariate Correlations Results

The table below shows the correlation matrix as a result of conducting Pearson’s Correlation

test. It has been found that there is no statistically significant relationship between return on

assets (ROA) and cash conversion cycle (CCC). Therefore, a null hypothesis is rejected.

Furthermore, there is negative relationship between ROA and CCC. As CCC, average

collection period (ACP) and Inventory Turnover in days (ITD) also has negative relationship

with ROA.

Table 2: Bivariate Correlations Results

Correlations

ROA (%) CCC ACP ITD APP

ROA (%) Pearson Correlation 1 -.192 -.327* -.050 .026

Sig. (2-tailed) .192 .023 .734 .859

N 48 48 48 48 48

CCC Pearson Correlation -.192 1 .537** .950** .573**

Sig. (2-tailed) .192 .000 .000 .000

N 48 48 48 48 48

ACP Pearson Correlation -.327* .537** 1 .376** .641**

Sig. (2-tailed) .023 .000 .008 .000

N 48 48 48 48 48

ITD Pearson Correlation -.050 .950** .376** 1 .674**

Sig. (2-tailed) .734 .000 .008 .000

N 48 48 48 48 48

APP Pearson Correlation .026 .573** .641** .674** 1

Sig. (2-tailed) .859 .000 .000 .000

N 48 48 48 48 48

*. Correlation is significant at the 0.05 level (2-tailed).

**. Correlation is significant at the 0.01 level (2-tailed).

5.3 Regression Analysis Results

10 | P a g e

The table below shows the correlation matrix as a result of conducting Pearson’s Correlation

test. It has been found that there is no statistically significant relationship between return on

assets (ROA) and cash conversion cycle (CCC). Therefore, a null hypothesis is rejected.

Furthermore, there is negative relationship between ROA and CCC. As CCC, average

collection period (ACP) and Inventory Turnover in days (ITD) also has negative relationship

with ROA.

Table 2: Bivariate Correlations Results

Correlations

ROA (%) CCC ACP ITD APP

ROA (%) Pearson Correlation 1 -.192 -.327* -.050 .026

Sig. (2-tailed) .192 .023 .734 .859

N 48 48 48 48 48

CCC Pearson Correlation -.192 1 .537** .950** .573**

Sig. (2-tailed) .192 .000 .000 .000

N 48 48 48 48 48

ACP Pearson Correlation -.327* .537** 1 .376** .641**

Sig. (2-tailed) .023 .000 .008 .000

N 48 48 48 48 48

ITD Pearson Correlation -.050 .950** .376** 1 .674**

Sig. (2-tailed) .734 .000 .008 .000

N 48 48 48 48 48

APP Pearson Correlation .026 .573** .641** .674** 1

Sig. (2-tailed) .859 .000 .000 .000

N 48 48 48 48 48

*. Correlation is significant at the 0.05 level (2-tailed).

**. Correlation is significant at the 0.01 level (2-tailed).

5.3 Regression Analysis Results

10 | P a g e

The multi regression analysis conducted show results below in Table 3, 4 and 5. From Table

3 we can know that R i.e. multiple correlation coefficient has value of 0.469 so it indicates a

good level of prediction of the dependent variable. The coefficient of determination i.e. R

Square with a value 0.220 indicates that the independent variables explain 22% if the

variability of dependent variable (ROTA).

Table 3: Model Summary

Model Summary

Model R R Square Adjusted R

Square

Std. Error of the

Estimate

1 .469a .220 .166 16.54235

a. Predictors: (Constant), Avg payable period, Cash Conversion

Cycle, Avg collection period

Table 4: Table for Coefficients

Coefficientsa

Model Unstandardized

Coefficients

Standardized

Coefficients

t Sig.

B Std.

Error

Beta

1 (Constant) 11.352 4.174 2.720 .009

CCC -.019 .018 -.172 -1.022 .312

ACP -.148 .050 -.533 -2.961 .005

APP .126 .050 .467 2.518 .016

a. Dependent Variable: Return on Assets (%)

In the table 4, the general equation to predict ROTA from different working capital

components is predicted as ROA= 11.352-(0.019*CCC-(0.148*ACP) + (0.126*APP). The

unstandardized coefficients (B) show the variability of dependent variable with independent

variables keeping all other independent variable constant. To know the statistical

significance of independent variables, t-value and p-value in t and Sig. section of the above

table is considered respectively. So, only ACP and APP were statistical significant to the

prediction (ROTA, F(3,44)= 4.130, p<0.0005, R2=0.220) as p-value<0.05 and CCC was not

considered statistically significant.

11 | P a g e

3 we can know that R i.e. multiple correlation coefficient has value of 0.469 so it indicates a

good level of prediction of the dependent variable. The coefficient of determination i.e. R

Square with a value 0.220 indicates that the independent variables explain 22% if the

variability of dependent variable (ROTA).

Table 3: Model Summary

Model Summary

Model R R Square Adjusted R

Square

Std. Error of the

Estimate

1 .469a .220 .166 16.54235

a. Predictors: (Constant), Avg payable period, Cash Conversion

Cycle, Avg collection period

Table 4: Table for Coefficients

Coefficientsa

Model Unstandardized

Coefficients

Standardized

Coefficients

t Sig.

B Std.

Error

Beta

1 (Constant) 11.352 4.174 2.720 .009

CCC -.019 .018 -.172 -1.022 .312

ACP -.148 .050 -.533 -2.961 .005

APP .126 .050 .467 2.518 .016

a. Dependent Variable: Return on Assets (%)

In the table 4, the general equation to predict ROTA from different working capital

components is predicted as ROA= 11.352-(0.019*CCC-(0.148*ACP) + (0.126*APP). The

unstandardized coefficients (B) show the variability of dependent variable with independent

variables keeping all other independent variable constant. To know the statistical

significance of independent variables, t-value and p-value in t and Sig. section of the above

table is considered respectively. So, only ACP and APP were statistical significant to the

prediction (ROTA, F(3,44)= 4.130, p<0.0005, R2=0.220) as p-value<0.05 and CCC was not

considered statistically significant.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.