Business Finance Report: Bright Lawns and BoatWorld Financial Analysis

VerifiedAdded on 2023/01/18

|11

|3709

|55

Report

AI Summary

This comprehensive finance report delves into the financial performance of two companies, Bright Lawns Ltd and BoatWorld Plc. Part 1 focuses on Bright Lawns Ltd, analyzing its profit, cash flow, and working capital management. It examines the impact of changes in working capital and recommends strategies to improve cash flow through better working capital management, including reducing credit periods, managing inventory levels, and automating accounts receivable. Part 2 shifts to BoatWorld Plc, exploring the purposes of budgeting, comparing traditional and alternative budgeting approaches, and analyzing their strengths and weaknesses. The report recommends alternative budgetary systems to effectively plan for future cost management. The report provides detailed financial analysis, practical recommendations, and a comparative study of financial management techniques, offering valuable insights for business decision-making and financial strategy development.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

PART 1............................................................................................................................................1

Executive Summary ........................................................................................................................1

MAIN BODY...................................................................................................................................1

a. Profit and cash flow.................................................................................................................1

b. Working capital........................................................................................................................2

c. Changes in the working capital................................................................................................2

ii) Concepts used to present the financial aspects to manage the impact of concepts upon

financial results............................................................................................................................3

Analyse and recommend what steps should now be taken to improve this company’s cashflow

through better Working Capital management..............................................................................3

PART 2............................................................................................................................................4

Executive summary......................................................................................................................4

1. Purposes of preparing a budget, explanation of traditional budgeting approaches and

alternative budget methods along with their strengths and weaknesses......................................4

2. Application of budgets to plan future cost management of business.......................................7

3. Analysis of appropriateness of traditional or alternative budgetary systems..........................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

PART 1............................................................................................................................................1

Executive Summary ........................................................................................................................1

MAIN BODY...................................................................................................................................1

a. Profit and cash flow.................................................................................................................1

b. Working capital........................................................................................................................2

c. Changes in the working capital................................................................................................2

ii) Concepts used to present the financial aspects to manage the impact of concepts upon

financial results............................................................................................................................3

Analyse and recommend what steps should now be taken to improve this company’s cashflow

through better Working Capital management..............................................................................3

PART 2............................................................................................................................................4

Executive summary......................................................................................................................4

1. Purposes of preparing a budget, explanation of traditional budgeting approaches and

alternative budget methods along with their strengths and weaknesses......................................4

2. Application of budgets to plan future cost management of business.......................................7

3. Analysis of appropriateness of traditional or alternative budgetary systems..........................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

PART 1

Executive Summary

The particular case study mainly based on the Bright Lawns Ltd that face many issues

and analysis the financial performance of the organisation where consist of profit, cash flow,

inventory and many others. Through these activities know the actual position and take decision

regrading to investment.

MAIN BODY

a. Profit and cash flow

Profit: It describes as the financial benefit that gain by the organisation when they have

extra income as compare of expenses. It is a amount of the income left over after all the

important and matched expenses and less for certain period of time. As per the matching

principle all the expenditure were consisted to generate the income and identified in the given

period of time. Many time company face net loss when expenses exceed to income. Businesses

use three types of profit to analysis various places of an organisation (Baldock and North, 2015). Gross profit: To calculate this profit required to less variable cost from the revenues from

the every product line. For this profit does not require fixed cost such as equipment, plant

& HR department. An organisation comparison in the product lines to see which is most

profitable. Net Profit: For this profit consist of all costs that present right position of the company in

present time and how much money the business is creating. While, many times it may

misleading to top directors.

Operating Profit: In this profit consisted of fixed and variable costs. For this includes

some financial costs which is called as EBITA. It is calculated by the mostly organisation

to know the amount of the deprecation, tax and amortization.

Cash flow: It is the net amount of cash and cash equivalents that move into and out of

business. In finance, the particular term utilise to define the net amount of cash which is earned

in particular accounting period of time. There are different kind of cash flow that is essential use

by the organisation to run and presenting financial analysis (Butler, 2016).

Difference between profit and cash flow:

1

Executive Summary

The particular case study mainly based on the Bright Lawns Ltd that face many issues

and analysis the financial performance of the organisation where consist of profit, cash flow,

inventory and many others. Through these activities know the actual position and take decision

regrading to investment.

MAIN BODY

a. Profit and cash flow

Profit: It describes as the financial benefit that gain by the organisation when they have

extra income as compare of expenses. It is a amount of the income left over after all the

important and matched expenses and less for certain period of time. As per the matching

principle all the expenditure were consisted to generate the income and identified in the given

period of time. Many time company face net loss when expenses exceed to income. Businesses

use three types of profit to analysis various places of an organisation (Baldock and North, 2015). Gross profit: To calculate this profit required to less variable cost from the revenues from

the every product line. For this profit does not require fixed cost such as equipment, plant

& HR department. An organisation comparison in the product lines to see which is most

profitable. Net Profit: For this profit consist of all costs that present right position of the company in

present time and how much money the business is creating. While, many times it may

misleading to top directors.

Operating Profit: In this profit consisted of fixed and variable costs. For this includes

some financial costs which is called as EBITA. It is calculated by the mostly organisation

to know the amount of the deprecation, tax and amortization.

Cash flow: It is the net amount of cash and cash equivalents that move into and out of

business. In finance, the particular term utilise to define the net amount of cash which is earned

in particular accounting period of time. There are different kind of cash flow that is essential use

by the organisation to run and presenting financial analysis (Butler, 2016).

Difference between profit and cash flow:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

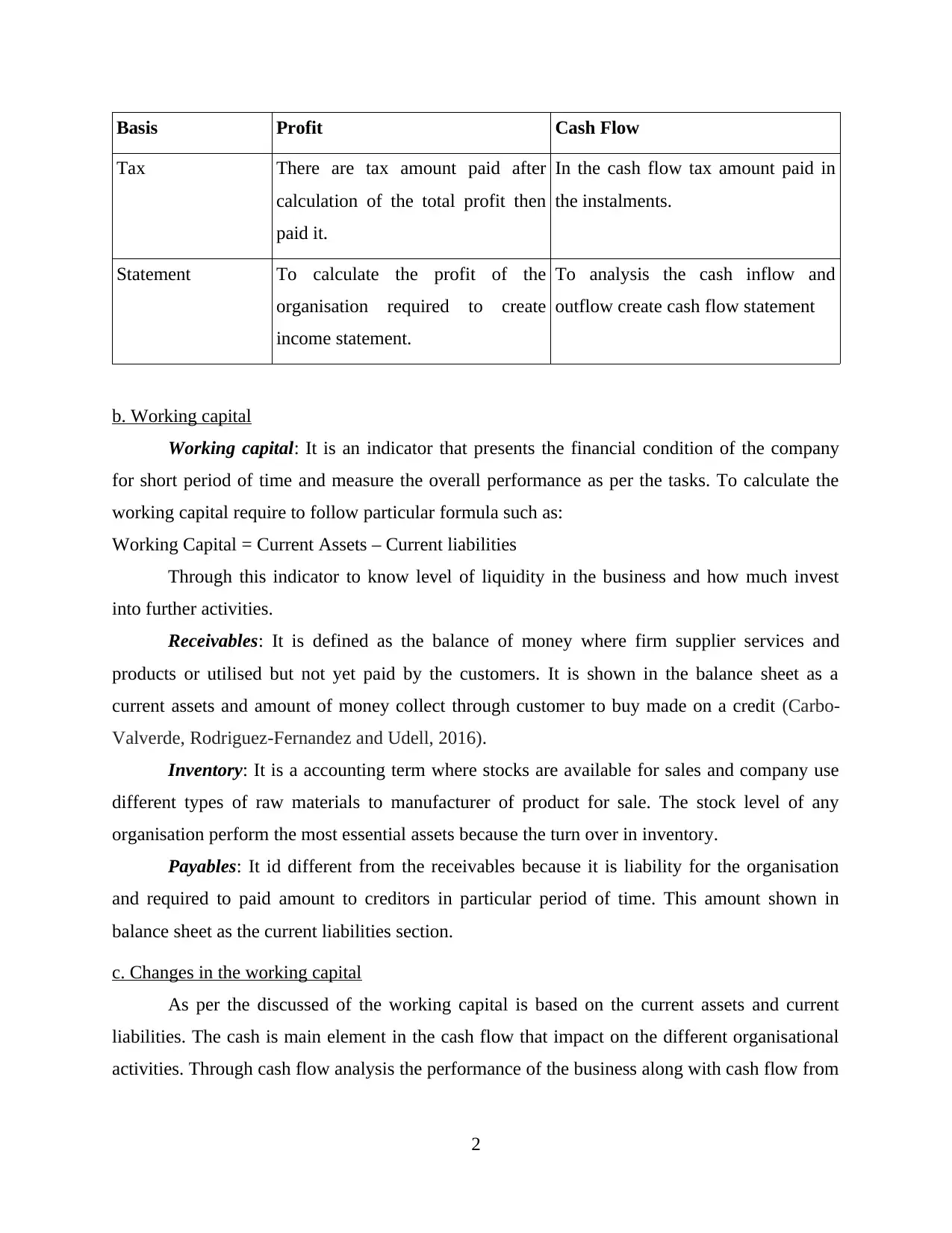

Basis Profit Cash Flow

Tax There are tax amount paid after

calculation of the total profit then

paid it.

In the cash flow tax amount paid in

the instalments.

Statement To calculate the profit of the

organisation required to create

income statement.

To analysis the cash inflow and

outflow create cash flow statement

b. Working capital

Working capital: It is an indicator that presents the financial condition of the company

for short period of time and measure the overall performance as per the tasks. To calculate the

working capital require to follow particular formula such as:

Working Capital = Current Assets – Current liabilities

Through this indicator to know level of liquidity in the business and how much invest

into further activities.

Receivables: It is defined as the balance of money where firm supplier services and

products or utilised but not yet paid by the customers. It is shown in the balance sheet as a

current assets and amount of money collect through customer to buy made on a credit (Carbo‐

Valverde, Rodriguez‐Fernandez and Udell, 2016).

Inventory: It is a accounting term where stocks are available for sales and company use

different types of raw materials to manufacturer of product for sale. The stock level of any

organisation perform the most essential assets because the turn over in inventory.

Payables: It id different from the receivables because it is liability for the organisation

and required to paid amount to creditors in particular period of time. This amount shown in

balance sheet as the current liabilities section.

c. Changes in the working capital

As per the discussed of the working capital is based on the current assets and current

liabilities. The cash is main element in the cash flow that impact on the different organisational

activities. Through cash flow analysis the performance of the business along with cash flow from

2

Tax There are tax amount paid after

calculation of the total profit then

paid it.

In the cash flow tax amount paid in

the instalments.

Statement To calculate the profit of the

organisation required to create

income statement.

To analysis the cash inflow and

outflow create cash flow statement

b. Working capital

Working capital: It is an indicator that presents the financial condition of the company

for short period of time and measure the overall performance as per the tasks. To calculate the

working capital require to follow particular formula such as:

Working Capital = Current Assets – Current liabilities

Through this indicator to know level of liquidity in the business and how much invest

into further activities.

Receivables: It is defined as the balance of money where firm supplier services and

products or utilised but not yet paid by the customers. It is shown in the balance sheet as a

current assets and amount of money collect through customer to buy made on a credit (Carbo‐

Valverde, Rodriguez‐Fernandez and Udell, 2016).

Inventory: It is a accounting term where stocks are available for sales and company use

different types of raw materials to manufacturer of product for sale. The stock level of any

organisation perform the most essential assets because the turn over in inventory.

Payables: It id different from the receivables because it is liability for the organisation

and required to paid amount to creditors in particular period of time. This amount shown in

balance sheet as the current liabilities section.

c. Changes in the working capital

As per the discussed of the working capital is based on the current assets and current

liabilities. The cash is main element in the cash flow that impact on the different organisational

activities. Through cash flow analysis the performance of the business along with cash flow from

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investing activities changes the value of the investments. So changes in the working capital

shows positive as well as negative way:

Positive Impact: As per the particular case the value of the current assets is increasing in

the working capital so it presents positive impact on the cash flow. It is because the value of

current assets helps to increase the value of cash flow in different activities like operation as well

as investing (Dang, Li and Yang, 2018).

Negative Impact: It is also affects in negative manner on the cash flow when current

liabilities increase so liquid level change of the company. It will become important for the

business entities to make payment through cash.

ii) Concepts used to present the financial aspects to manage the impact of concepts upon

financial results.

Profit: In the presented case study British Lawns limited get the amount of the had last

year turn over about £50 million. They have reasonable profit like operating profit was £5

million last year before interest and tax. It presents good position of the company.

Accounts Receivable: The company have mostly accounting receivables are stakeholders

that had taken in the fund and supplying goods in upcoming period of time. Such as they

have £1.5 million from C & P company with an assurance of delivering goods in

futuristic time (Soros, 2015)..

Accounts payable: The above bright lawns company's debt amount are of £18 that

increased by £2 as compare to last year because in previous year it was of £16.

Inventory: This company provides different types of products like valves, fittings and

many more. To produce these goods require to follow the procedure of raw material,

work in progress and finished goods.

Analyse and recommend what steps should now be taken to improve this company’s cashflow

through better Working Capital management

In order to improve cash flow by managing working capital in better manner, finance

department of BrightLawns Ltd are recommended to reduce credit period that managers offers

to their debtors. The CFOs of the entity should time to time review credit terms so to make sure

that credit levels provided to debtors are exact or accurate for managing cash flow requiremenst

of the business. By managing debtors effectively will ensure the entity that money is coming

inside the premise on time. With this, the company will be able to acquire the required funds and

3

shows positive as well as negative way:

Positive Impact: As per the particular case the value of the current assets is increasing in

the working capital so it presents positive impact on the cash flow. It is because the value of

current assets helps to increase the value of cash flow in different activities like operation as well

as investing (Dang, Li and Yang, 2018).

Negative Impact: It is also affects in negative manner on the cash flow when current

liabilities increase so liquid level change of the company. It will become important for the

business entities to make payment through cash.

ii) Concepts used to present the financial aspects to manage the impact of concepts upon

financial results.

Profit: In the presented case study British Lawns limited get the amount of the had last

year turn over about £50 million. They have reasonable profit like operating profit was £5

million last year before interest and tax. It presents good position of the company.

Accounts Receivable: The company have mostly accounting receivables are stakeholders

that had taken in the fund and supplying goods in upcoming period of time. Such as they

have £1.5 million from C & P company with an assurance of delivering goods in

futuristic time (Soros, 2015)..

Accounts payable: The above bright lawns company's debt amount are of £18 that

increased by £2 as compare to last year because in previous year it was of £16.

Inventory: This company provides different types of products like valves, fittings and

many more. To produce these goods require to follow the procedure of raw material,

work in progress and finished goods.

Analyse and recommend what steps should now be taken to improve this company’s cashflow

through better Working Capital management

In order to improve cash flow by managing working capital in better manner, finance

department of BrightLawns Ltd are recommended to reduce credit period that managers offers

to their debtors. The CFOs of the entity should time to time review credit terms so to make sure

that credit levels provided to debtors are exact or accurate for managing cash flow requiremenst

of the business. By managing debtors effectively will ensure the entity that money is coming

inside the premise on time. With this, the company will be able to acquire the required funds and

3

will maintain its cash flow in better manner. Similarly, by reducing expenses concerned with

debt services will help in dropping cash outflow at some extent which will further result in

improving cash flows with proper management of available cash. Reduction in expenses with

proper reviewing of fixed along with variable costs will ascertain the key areas that needs

improvements and hence managing working capital. Similarly, the essential factor that makes

working capital for the firm is prudent inventory management. It is also recommended to

manage desired stock level so that finished products are soon sold so to attain inflow of cash

and eliminating situations like overstocking. Excess stock puts heavy load on business cash

resources while insufficient stock shows lost sales addition to damaging customer relations.

With this, products and services at selected entity which are not performing or are unproductive

can be cut and working capital can be maintained in better ways. By automating accounts

receivable is also a strong option to manage working capital through better aspects. When

accounts receivable will be managed through computers then there will be less probabilities of

mistakes and will help in avoiding delays in account payments and streamlining entire working

capital procedure. Through this, customers will receive invoices digitally as well as can pay in

same manner prior or on due date that will improve inflow of cash that will further result in

managing working capital in proper manner.

PART 2

Executive summary

This part of the report is based upon analysis of BoatWorld Plc which is an international

leisure company that rents boats to holiday makers. This part summarises the purposes of

preparing a budget, explanation of traditional budgeting approaches and alternative methods of

budgets. With the help of them an organisation can plan for future cost management. The

organisation is recommended to use alternative budgetary system for the purpose of operating

business in planned form.

1. Purposes of preparing a budget, explanation of traditional budgeting approaches and

alternative budget methods along with their strengths and weaknesses

Budget: The financial plan which is formulated by the companies every year is known as

budget which helps managers to keep track record of funds which are spent upon different

operational activities of the company. It is beneficial for all the companies because with the help

4

debt services will help in dropping cash outflow at some extent which will further result in

improving cash flows with proper management of available cash. Reduction in expenses with

proper reviewing of fixed along with variable costs will ascertain the key areas that needs

improvements and hence managing working capital. Similarly, the essential factor that makes

working capital for the firm is prudent inventory management. It is also recommended to

manage desired stock level so that finished products are soon sold so to attain inflow of cash

and eliminating situations like overstocking. Excess stock puts heavy load on business cash

resources while insufficient stock shows lost sales addition to damaging customer relations.

With this, products and services at selected entity which are not performing or are unproductive

can be cut and working capital can be maintained in better ways. By automating accounts

receivable is also a strong option to manage working capital through better aspects. When

accounts receivable will be managed through computers then there will be less probabilities of

mistakes and will help in avoiding delays in account payments and streamlining entire working

capital procedure. Through this, customers will receive invoices digitally as well as can pay in

same manner prior or on due date that will improve inflow of cash that will further result in

managing working capital in proper manner.

PART 2

Executive summary

This part of the report is based upon analysis of BoatWorld Plc which is an international

leisure company that rents boats to holiday makers. This part summarises the purposes of

preparing a budget, explanation of traditional budgeting approaches and alternative methods of

budgets. With the help of them an organisation can plan for future cost management. The

organisation is recommended to use alternative budgetary system for the purpose of operating

business in planned form.

1. Purposes of preparing a budget, explanation of traditional budgeting approaches and

alternative budget methods along with their strengths and weaknesses

Budget: The financial plan which is formulated by the companies every year is known as

budget which helps managers to keep track record of funds which are spent upon different

operational activities of the company. It is beneficial for all the companies because with the help

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of it unnecessary spendings could be determined and decisions for resolution of them could be

formulated. In order to make sure that finance is allocated to all the operations appropriately it is

very important to formulate budgets. Most of the companies such as BoatWorld Plc generate

them for different purposes (Haas, 2014). All of them are as follows:

Management create budgets to communicate financial position of business with top

authority.

In order to coordinate with business process budget is prepared by companies.

For the purpose of reaching set business goals budget are prepared so that funds could be

allotted to all the activities according to their requirements. In business entities are formulated to evaluate financial position by comparing actual

figures with budgeted ones.

Traditional budgeting: It is a method of preparing budgets by focusing on the financial

information of previous year. Under this type of procedure management create budget by

adjusting current year's records. Expenses which are recorded with the help of this technique are

based upon changes in different elements such as market situations, inflation rate, customer

demand etc. There is a main approach of it which is as follows:

Incremental budgeting: In this approach of traditional budgeting last year's budget is

considered as the base for current year's records. With the help of it managers make sure that

they allocate appropriate and reasonable amount to different procedures of the organisation so

that overspending of them could be stopped. The process of formulating budget under this

approach is very simple which helps internal as well as external users to determine actual

position of business. There are various strengths and weaknesses of it which are as follows:

Strengths: With the help of it consistency and operational stability of it could be assured

because it takes previous year's data in to consideration. It guides managers to allocate

equal finance to all the departments sop that internal rivalry among them could be

reduced. Weaknesses: It is not possible to account changes in this approach of budgeting which

affects accuracy of it. It is based upon unreal assumptions therefore it results in negative

impacts of it on the potential growth of the company (Hull, 2014)

Alternative budgeting methods: In most of the companies different types of methods are

used for the purpose of formulating budgets. With the help of all of them position of organisation

5

formulated. In order to make sure that finance is allocated to all the operations appropriately it is

very important to formulate budgets. Most of the companies such as BoatWorld Plc generate

them for different purposes (Haas, 2014). All of them are as follows:

Management create budgets to communicate financial position of business with top

authority.

In order to coordinate with business process budget is prepared by companies.

For the purpose of reaching set business goals budget are prepared so that funds could be

allotted to all the activities according to their requirements. In business entities are formulated to evaluate financial position by comparing actual

figures with budgeted ones.

Traditional budgeting: It is a method of preparing budgets by focusing on the financial

information of previous year. Under this type of procedure management create budget by

adjusting current year's records. Expenses which are recorded with the help of this technique are

based upon changes in different elements such as market situations, inflation rate, customer

demand etc. There is a main approach of it which is as follows:

Incremental budgeting: In this approach of traditional budgeting last year's budget is

considered as the base for current year's records. With the help of it managers make sure that

they allocate appropriate and reasonable amount to different procedures of the organisation so

that overspending of them could be stopped. The process of formulating budget under this

approach is very simple which helps internal as well as external users to determine actual

position of business. There are various strengths and weaknesses of it which are as follows:

Strengths: With the help of it consistency and operational stability of it could be assured

because it takes previous year's data in to consideration. It guides managers to allocate

equal finance to all the departments sop that internal rivalry among them could be

reduced. Weaknesses: It is not possible to account changes in this approach of budgeting which

affects accuracy of it. It is based upon unreal assumptions therefore it results in negative

impacts of it on the potential growth of the company (Hull, 2014)

Alternative budgeting methods: In most of the companies different types of methods are

used for the purpose of formulating budgets. With the help of all of them position of organisation

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is determined on yearly, half-yearly, quarterly and monthly basis. There are three main examples

of these methods which are as follows:

Rolling budget: The financial plan in which continuous modifications are made on the

basis of changes in market situations is known as rolling budget. It keeps less details as compare

to the traditional methods in which detailed information was recorded to perform budgeting

related activities. With the help of it management gets aware of the steps which are required to

be taken by them for the betterment of organisation. The strengths and weaknesses of this budget

are as follows:

Strengths: Changes could be made in this budget easily as it allows management to

make timely upgradation according to alteration in business model. With the help of it

managers can spend the money wisely because it helps them to analyse the actual

situation and they take spending decision (Lindley and McIntosh, 2017)..

Weaknesses: For all the users of budgets it is very difficult to interpret the changes

which are made according to market situations. The process which is followed by

organisations to formulate it is time taking.

Zero based budget: It can be defined as a budget in which all the budgetary allocations

for all the divisions of the company starts from a zero and information of previous year is not

taken in to consideration to formulate current year's records. With the help of it top authority gets

aware of all the factors which may affect performance of business as for every new year a new

budget is prepared by ignoring records of prior year (Zero based budget, 2019). All the strengths

and weaknesses of it for the companies are as follows:

Strengths: It guides management to make sure that they allocate efficient funds to all the

divisions according to their needs so that possibility of unnecessary spendings could be

reduced. With the help of it services and utilisation of cost effective methods can be

improved because it ignores information of previous year.

Weaknesses: For the purpose of using it high manpower is required which may divert the

attention of managers from business to recruitment processes. This method is considered

as very expensive as compare to other budgets as high level of complexity is involved in

it (Minsky, 2016).

Activity based budget: Under this method of alternative budgeting an organisation can

record, analyse and evaluate all the activities which are resulting in costs to the company. Main

6

of these methods which are as follows:

Rolling budget: The financial plan in which continuous modifications are made on the

basis of changes in market situations is known as rolling budget. It keeps less details as compare

to the traditional methods in which detailed information was recorded to perform budgeting

related activities. With the help of it management gets aware of the steps which are required to

be taken by them for the betterment of organisation. The strengths and weaknesses of this budget

are as follows:

Strengths: Changes could be made in this budget easily as it allows management to

make timely upgradation according to alteration in business model. With the help of it

managers can spend the money wisely because it helps them to analyse the actual

situation and they take spending decision (Lindley and McIntosh, 2017)..

Weaknesses: For all the users of budgets it is very difficult to interpret the changes

which are made according to market situations. The process which is followed by

organisations to formulate it is time taking.

Zero based budget: It can be defined as a budget in which all the budgetary allocations

for all the divisions of the company starts from a zero and information of previous year is not

taken in to consideration to formulate current year's records. With the help of it top authority gets

aware of all the factors which may affect performance of business as for every new year a new

budget is prepared by ignoring records of prior year (Zero based budget, 2019). All the strengths

and weaknesses of it for the companies are as follows:

Strengths: It guides management to make sure that they allocate efficient funds to all the

divisions according to their needs so that possibility of unnecessary spendings could be

reduced. With the help of it services and utilisation of cost effective methods can be

improved because it ignores information of previous year.

Weaknesses: For the purpose of using it high manpower is required which may divert the

attention of managers from business to recruitment processes. This method is considered

as very expensive as compare to other budgets as high level of complexity is involved in

it (Minsky, 2016).

Activity based budget: Under this method of alternative budgeting an organisation can

record, analyse and evaluate all the activities which are resulting in costs to the company. Main

6

purpose of preparing this budget is to reduce expenses by providing meaningful data to the

decision makers of company. Various strengths and weaknesses of it are listed below:

Strengths: It is mainly based upon analysis of all the operational activities which helps

managers to make effective decisions for proper execution of them. It can help the

managers to formulate effective decisions according to the actual situation of company.

Weaknesses: As it covers information of all the activities so it create difficulties to figure

out detailed information of all of them (Pilbeam, 2018).

2. Application of budgets to plan future cost management of business

In traditional budgeting previous year's data is used for the purpose of formulating

records of upcoming years. Incremental budgeting is one of the main approach in this procedure.

With the help of it managers can plan for future cost management as it can guide them to

estimate it on the basis of available information. In this approach products and processes will be

budgeted according to prior year's details.

Alternative system have three main types of budgets which are rolling, zero and activity

based budgeting. All of them could also be used for the purpose of planning future cost and

budgeting the products and processes of business.

Managers in BoatWorld Plc can open new outlets in Netherlands and Germany with the

help of rolling budget because it can help them to make proper adjustments according to the

situations which are taking place in the market. With the help of it future cost could be managed

properly as it will guide the managers to deal with them by making adjustments in the books.

Zero based budgeting can also be used by managers in BoatWorld Plc to budget the

products and processes because it starts with a zero base therefore only details of new outlets in

Netherlands and Germany will be taken in to consideration by this method. By focusing on them

it will also help to manage future costs (Pimenta and Fama, 2014).

Activity based budget are also beneficial for BoatWorld Plc for the business expansion in

Netherlands in Germany because it will help them to keep detailed information of all the

activities which will be performed for this purpose. It will also facilitate in the budgeting of

products and process by planning future cost management because with the help of it

management will be able to analyse the activities which may result in higher expenses.

7

decision makers of company. Various strengths and weaknesses of it are listed below:

Strengths: It is mainly based upon analysis of all the operational activities which helps

managers to make effective decisions for proper execution of them. It can help the

managers to formulate effective decisions according to the actual situation of company.

Weaknesses: As it covers information of all the activities so it create difficulties to figure

out detailed information of all of them (Pilbeam, 2018).

2. Application of budgets to plan future cost management of business

In traditional budgeting previous year's data is used for the purpose of formulating

records of upcoming years. Incremental budgeting is one of the main approach in this procedure.

With the help of it managers can plan for future cost management as it can guide them to

estimate it on the basis of available information. In this approach products and processes will be

budgeted according to prior year's details.

Alternative system have three main types of budgets which are rolling, zero and activity

based budgeting. All of them could also be used for the purpose of planning future cost and

budgeting the products and processes of business.

Managers in BoatWorld Plc can open new outlets in Netherlands and Germany with the

help of rolling budget because it can help them to make proper adjustments according to the

situations which are taking place in the market. With the help of it future cost could be managed

properly as it will guide the managers to deal with them by making adjustments in the books.

Zero based budgeting can also be used by managers in BoatWorld Plc to budget the

products and processes because it starts with a zero base therefore only details of new outlets in

Netherlands and Germany will be taken in to consideration by this method. By focusing on them

it will also help to manage future costs (Pimenta and Fama, 2014).

Activity based budget are also beneficial for BoatWorld Plc for the business expansion in

Netherlands in Germany because it will help them to keep detailed information of all the

activities which will be performed for this purpose. It will also facilitate in the budgeting of

products and process by planning future cost management because with the help of it

management will be able to analyse the activities which may result in higher expenses.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Analysis of appropriateness of traditional or alternative budgetary systems

There are two different ways of budgeting one is traditional and another is alternative

budgets. Both of them are good on their places as with the help of them managers can reach to

the judgements which may provide benefits to the business.

Traditional budgeting is focused with analysis of previous year's information but the

alternative methods ignore the prior records. As BoatWorld Plc is planing to open new outlets in

Netherlands and Germany so it is very important for the company to use best method of

budgeting. The most appropriate mode for them will be alternative methods which are rolling,

activity and zero based budgets. By using all of them management of the company will be able to

keep detailed information of current year's transactions and execute the business in the planned

future form (Scholtens, 2017)

CONCLUSION

As per the discussion, it is concluded that finance is core for all business. Business

finance is characterised as money addition to capital which is employed within business. Finance

is required for acquiring assets, material as well as to carry out operations for achieving

revenues. For analysing places within entity, types of profits like gross profit, operating profit as

well as net profit are used. To satisfy stakeholders, managers of company are required to share

essential information based on all elements with distinct stakeholders. Budgets are prepared for

communicating financial position, reducing overspending situations, coordinating business

procedures and identifying deviations. Methods for budget preparations are incremental

budgeting, rolling budgeting, activity based budgeting and zero based budgeting. At the time

budgets are prepared, accounting professionals must be having knowledge about correctitude of

tradition addition to alternative budgetary system. When budgets are properly applied then

business administrators can effectively plan cost management for coming duration.

8

There are two different ways of budgeting one is traditional and another is alternative

budgets. Both of them are good on their places as with the help of them managers can reach to

the judgements which may provide benefits to the business.

Traditional budgeting is focused with analysis of previous year's information but the

alternative methods ignore the prior records. As BoatWorld Plc is planing to open new outlets in

Netherlands and Germany so it is very important for the company to use best method of

budgeting. The most appropriate mode for them will be alternative methods which are rolling,

activity and zero based budgets. By using all of them management of the company will be able to

keep detailed information of current year's transactions and execute the business in the planned

future form (Scholtens, 2017)

CONCLUSION

As per the discussion, it is concluded that finance is core for all business. Business

finance is characterised as money addition to capital which is employed within business. Finance

is required for acquiring assets, material as well as to carry out operations for achieving

revenues. For analysing places within entity, types of profits like gross profit, operating profit as

well as net profit are used. To satisfy stakeholders, managers of company are required to share

essential information based on all elements with distinct stakeholders. Budgets are prepared for

communicating financial position, reducing overspending situations, coordinating business

procedures and identifying deviations. Methods for budget preparations are incremental

budgeting, rolling budgeting, activity based budgeting and zero based budgeting. At the time

budgets are prepared, accounting professionals must be having knowledge about correctitude of

tradition addition to alternative budgetary system. When budgets are properly applied then

business administrators can effectively plan cost management for coming duration.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Baldock, R. and North, D., 2015. The role of UK government hybrid venture capital funds in

addressing the finance gap facing innovative SMEs in the post-2007 financial crisis

era. Handbook on entrepreneurial finance, pp.125-146.

Butler, K. C., 2016. Multinational Finance: Evaluating the Opportunities, Costs, and Risks of

Multinational Operations. John Wiley & Sons.

Carbo‐Valverde, S., Rodriguez‐Fernandez, F. and Udell, G. F., 2016. Trade credit, the financial

crisis, and SME access to finance. Journal of Money, Credit and Banking. 48(1).

pp.113-143.

Dang, C., Li, Z. F. and Yang, C., 2018. Measuring firm size in empirical corporate

finance. Journal of Banking & Finance. 86. pp.159-176.

Haas, J. J., 2014. Corporate finance. West Academic.

Hull, J. C., 2014. The evaluation of risk in business investment. Elsevier.

Lindley, J. and McIntosh, S., 2017. Finance sector wage growth and the role of human

capital. Oxford Bulletin of Economics and Statistics. 79(4). pp.570-591.

Minsky, H., 2016. Can it happen again?: Essays on instability and finance. Routledge.

Pilbeam, K., 2018. Finance & financial markets. Macmillan International Higher Education.

Pimenta, A. and Fama, R., 2014. Behavioral finance: a bibliometric mapping of academic

publications in USA since 1993. Available at SSRN 2406763.

Scholtens, B., 2017. Why finance should care about ecology. Trends in ecology & evolution.

32(7). pp.500-505.

Soros, G., 2015. The alchemy of finance. John Wiley & Sons.

Online

Zero based budget. 2019. [Online]. Available through:

<https://www.finweb.com/financial-planning/pros-and-cons-of-zero-based-

budgeting.html>

9

Books and Journals:

Baldock, R. and North, D., 2015. The role of UK government hybrid venture capital funds in

addressing the finance gap facing innovative SMEs in the post-2007 financial crisis

era. Handbook on entrepreneurial finance, pp.125-146.

Butler, K. C., 2016. Multinational Finance: Evaluating the Opportunities, Costs, and Risks of

Multinational Operations. John Wiley & Sons.

Carbo‐Valverde, S., Rodriguez‐Fernandez, F. and Udell, G. F., 2016. Trade credit, the financial

crisis, and SME access to finance. Journal of Money, Credit and Banking. 48(1).

pp.113-143.

Dang, C., Li, Z. F. and Yang, C., 2018. Measuring firm size in empirical corporate

finance. Journal of Banking & Finance. 86. pp.159-176.

Haas, J. J., 2014. Corporate finance. West Academic.

Hull, J. C., 2014. The evaluation of risk in business investment. Elsevier.

Lindley, J. and McIntosh, S., 2017. Finance sector wage growth and the role of human

capital. Oxford Bulletin of Economics and Statistics. 79(4). pp.570-591.

Minsky, H., 2016. Can it happen again?: Essays on instability and finance. Routledge.

Pilbeam, K., 2018. Finance & financial markets. Macmillan International Higher Education.

Pimenta, A. and Fama, R., 2014. Behavioral finance: a bibliometric mapping of academic

publications in USA since 1993. Available at SSRN 2406763.

Scholtens, B., 2017. Why finance should care about ecology. Trends in ecology & evolution.

32(7). pp.500-505.

Soros, G., 2015. The alchemy of finance. John Wiley & Sons.

Online

Zero based budget. 2019. [Online]. Available through:

<https://www.finweb.com/financial-planning/pros-and-cons-of-zero-based-

budgeting.html>

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.