UMACTA-30-M Financial Accounting: Cash Flow Analysis Report

VerifiedAdded on 2023/01/19

|13

|2233

|71

Report

AI Summary

This report analyzes the financial performance and investment potential of Working Computers PLC's Bernoulli division, focusing on cash flow analysis and investment appraisal techniques. The report begins with an introduction to fundamental accounting principles and the context of the investment project, including the declining market share of the Bernoulli device and the need for a new capital investment plan. It then delves into the proposed investment, free cash flow, terminal value, and sensitivity analysis to evaluate the financial impact of the investment. The report examines potential sources of finance, including long-term and short-term options, and recommends an optimal balance to minimize the Weighted Average Cost of Capital (WACC). It uses the Net Present Value (NPV) method and Internal Rate of Return (IRR) to assess the investment's feasibility, considering projected cash flows, cost of capital, and inflation. The report also discusses the gap between financial theory and practice, highlighting the relevance of NPV and other investment appraisal methods. Finally, the report concludes with a recommendation to adopt the proposed investment, based on the positive NPV and IRR results, and advises the board of managers to proceed with the investment. Appendices provide detailed financial data and calculations supporting the analysis.

FINANCIAL ACCOUNTING

CASH FLOWS

CASH FLOWS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

Key aspects Subject to the investment project.......................................................................1

Proposed Investment..............................................................................................................2

Free Cash flow and terminal value.........................................................................................2

Sensitivity analysis.................................................................................................................3

Source of finance....................................................................................................................4

Investment appraisal technique..............................................................................................5

Gap between theory and practise............................................................................................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIXES.................................................................................................................................8

INTRODUCTION...........................................................................................................................1

Key aspects Subject to the investment project.......................................................................1

Proposed Investment..............................................................................................................2

Free Cash flow and terminal value.........................................................................................2

Sensitivity analysis.................................................................................................................3

Source of finance....................................................................................................................4

Investment appraisal technique..............................................................................................5

Gap between theory and practise............................................................................................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIXES.................................................................................................................................8

INTRODUCTION

Fundamental accounting principles and techniques assist the entity’s management and

functional decisions to accelerate the profitability graph of business. The report is prepared to

assist the analyst Jennifer Sobieski in the headquarters of Working Computers PLC regarding a

capital investment project. The report will assist the board of directors whether the project should

be designated or not. Financial concepts as NPV and cash flow forecasts are used considering the

actual and anticipated facts.

Key aspects Subject to the investment project

The case study of Working Computers Plc contains some key subject to business problem,

declining market price, low profitability and challenges to new capital investment plan. Critical

thinking and evaluative skills are used in order to sort out the complexities and extract the

reasons of declining figures. Company is seeking to sell out the division which is losing market

share and requires a high deal of new investment to remain more competitive. This division has

aligned product of Personal Data Appliance (PDA) which was once a leading product of the

organisation. The main reason of declining growth is considering the Bernoulli devise.

The Bernoulli system was indeed a lightweight, portable notepad type tool with embedded

apps for documenting schedules, addresses, contact details, or free form text. It was intended to

replace conventional calendar notebooks for executives. The devise was easy to access and

helpful for manufacturing industries at initial stage. Its compact size and easy interface was the

Unique Selling Point (USP) of the product. After a relishing period the product came in

competition. Various companies developed PDAs with more advanced features and

compatibility. Competitors launched portable devices that could be connected to different

figuring platforms. Whereas, the Bernoulli have only downloading and uploading specification

form a working brand computer. It could not connect with any other device which become the

reason of low sales and decreasing market share pricing. Stewart Workman appointed as a CEO

of Working Plc. He presented following points on Bernoulli device that it has become out dated

product and huge loophole for the company and introducing internal funds will increase capital

loss for entity.

1

Fundamental accounting principles and techniques assist the entity’s management and

functional decisions to accelerate the profitability graph of business. The report is prepared to

assist the analyst Jennifer Sobieski in the headquarters of Working Computers PLC regarding a

capital investment project. The report will assist the board of directors whether the project should

be designated or not. Financial concepts as NPV and cash flow forecasts are used considering the

actual and anticipated facts.

Key aspects Subject to the investment project

The case study of Working Computers Plc contains some key subject to business problem,

declining market price, low profitability and challenges to new capital investment plan. Critical

thinking and evaluative skills are used in order to sort out the complexities and extract the

reasons of declining figures. Company is seeking to sell out the division which is losing market

share and requires a high deal of new investment to remain more competitive. This division has

aligned product of Personal Data Appliance (PDA) which was once a leading product of the

organisation. The main reason of declining growth is considering the Bernoulli devise.

The Bernoulli system was indeed a lightweight, portable notepad type tool with embedded

apps for documenting schedules, addresses, contact details, or free form text. It was intended to

replace conventional calendar notebooks for executives. The devise was easy to access and

helpful for manufacturing industries at initial stage. Its compact size and easy interface was the

Unique Selling Point (USP) of the product. After a relishing period the product came in

competition. Various companies developed PDAs with more advanced features and

compatibility. Competitors launched portable devices that could be connected to different

figuring platforms. Whereas, the Bernoulli have only downloading and uploading specification

form a working brand computer. It could not connect with any other device which become the

reason of low sales and decreasing market share pricing. Stewart Workman appointed as a CEO

of Working Plc. He presented following points on Bernoulli device that it has become out dated

product and huge loophole for the company and introducing internal funds will increase capital

loss for entity.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Proposed Investment

The team indulged in project research to find out best possible options in respect of low

market price, sales and profitability. Jennifer collected essential facts after conducting research

about competitors, surfing data form internet and many PDA market strengths and weakness of

Bernoulli. It was found that the sales unit of Bernoulli unit presented estimated 15% of the

market capture however, the competitors are capturing 42% of sale market. Due to this market

share of company is declining by 1% each quarter. The researchers are working on major

upgradation of device as well as the software. This upgrade will improve compatibility of the

product with any personal computer in the market. The estimated cost to carry out the research

further will no less than £18 million to complete the advancement of the specialized product

phase in upcoming month. It is estimated that the proposed capital investment would help the

company to capture 8% of market share in five years and profitability of 4% after it. For better

evaluation the forecasted sales results are presented below;

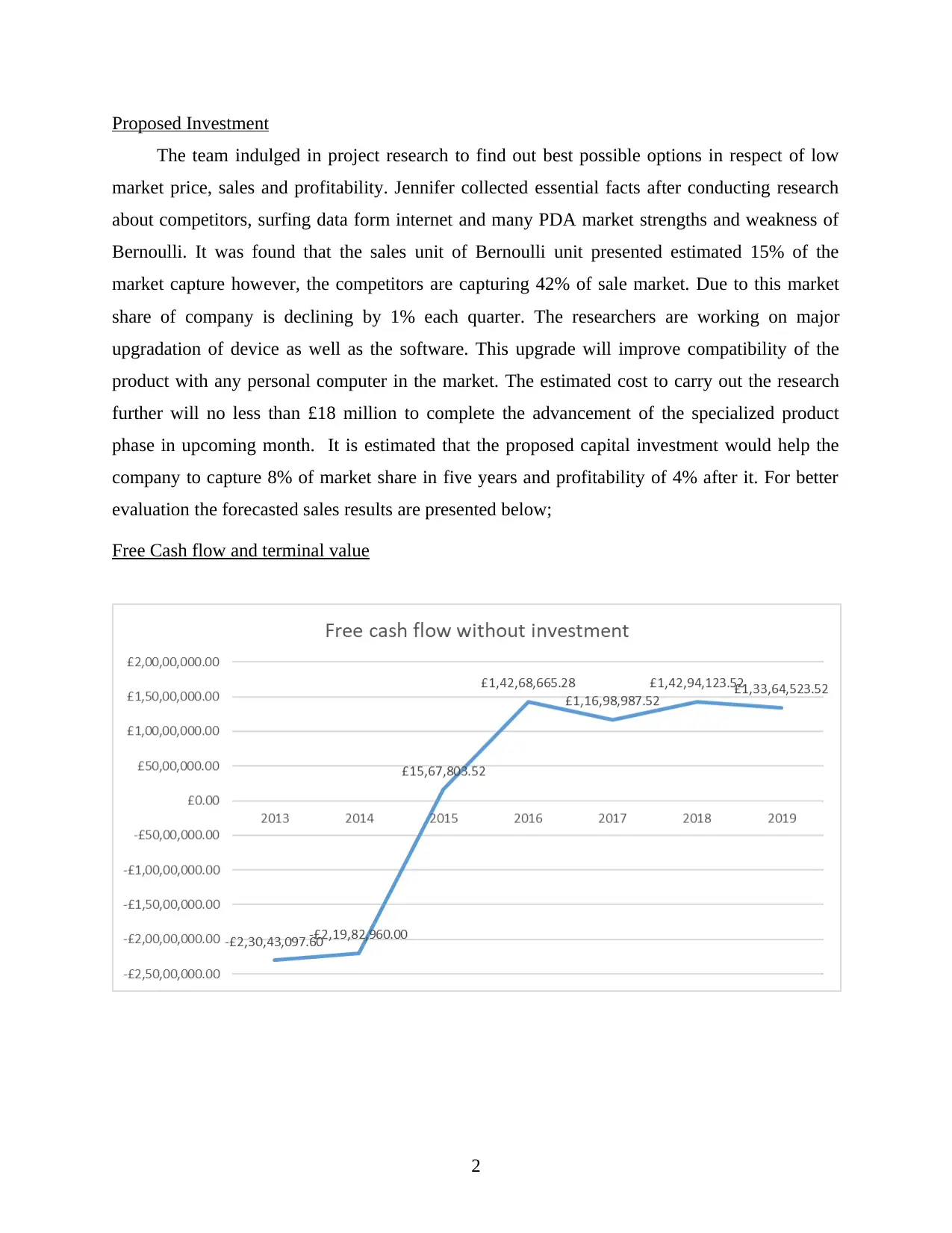

Free Cash flow and terminal value

2

The team indulged in project research to find out best possible options in respect of low

market price, sales and profitability. Jennifer collected essential facts after conducting research

about competitors, surfing data form internet and many PDA market strengths and weakness of

Bernoulli. It was found that the sales unit of Bernoulli unit presented estimated 15% of the

market capture however, the competitors are capturing 42% of sale market. Due to this market

share of company is declining by 1% each quarter. The researchers are working on major

upgradation of device as well as the software. This upgrade will improve compatibility of the

product with any personal computer in the market. The estimated cost to carry out the research

further will no less than £18 million to complete the advancement of the specialized product

phase in upcoming month. It is estimated that the proposed capital investment would help the

company to capture 8% of market share in five years and profitability of 4% after it. For better

evaluation the forecasted sales results are presented below;

Free Cash flow and terminal value

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

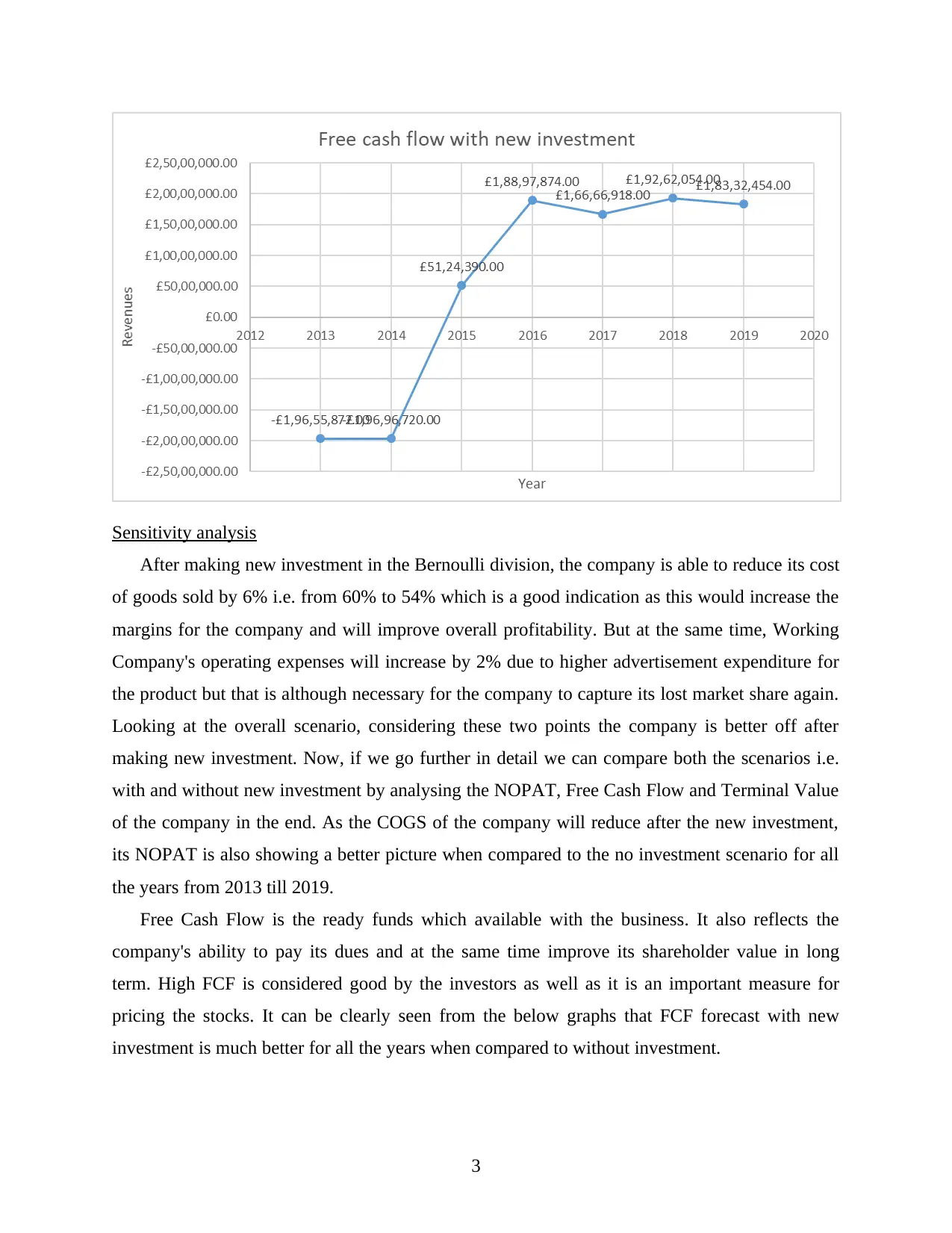

Sensitivity analysis

After making new investment in the Bernoulli division, the company is able to reduce its cost

of goods sold by 6% i.e. from 60% to 54% which is a good indication as this would increase the

margins for the company and will improve overall profitability. But at the same time, Working

Company's operating expenses will increase by 2% due to higher advertisement expenditure for

the product but that is although necessary for the company to capture its lost market share again.

Looking at the overall scenario, considering these two points the company is better off after

making new investment. Now, if we go further in detail we can compare both the scenarios i.e.

with and without new investment by analysing the NOPAT, Free Cash Flow and Terminal Value

of the company in the end. As the COGS of the company will reduce after the new investment,

its NOPAT is also showing a better picture when compared to the no investment scenario for all

the years from 2013 till 2019.

Free Cash Flow is the ready funds which available with the business. It also reflects the

company's ability to pay its dues and at the same time improve its shareholder value in long

term. High FCF is considered good by the investors as well as it is an important measure for

pricing the stocks. It can be clearly seen from the below graphs that FCF forecast with new

investment is much better for all the years when compared to without investment.

3

After making new investment in the Bernoulli division, the company is able to reduce its cost

of goods sold by 6% i.e. from 60% to 54% which is a good indication as this would increase the

margins for the company and will improve overall profitability. But at the same time, Working

Company's operating expenses will increase by 2% due to higher advertisement expenditure for

the product but that is although necessary for the company to capture its lost market share again.

Looking at the overall scenario, considering these two points the company is better off after

making new investment. Now, if we go further in detail we can compare both the scenarios i.e.

with and without new investment by analysing the NOPAT, Free Cash Flow and Terminal Value

of the company in the end. As the COGS of the company will reduce after the new investment,

its NOPAT is also showing a better picture when compared to the no investment scenario for all

the years from 2013 till 2019.

Free Cash Flow is the ready funds which available with the business. It also reflects the

company's ability to pay its dues and at the same time improve its shareholder value in long

term. High FCF is considered good by the investors as well as it is an important measure for

pricing the stocks. It can be clearly seen from the below graphs that FCF forecast with new

investment is much better for all the years when compared to without investment.

3

With new investment Without new investment

Terminal Value £59,22,79,296 £43,17,76,914

Total Present Value of

Company's operations

£4,32,52,210 £2,39,71,112

Terminal Value basically reflects the value of the organization after the forecast period. This

value shows 60-80% when we look at the total valuation of a company. So, by analysing both

the scenarios, we can say that company is getting better terminal value when new investment

is made.

Source of finance

When deciding upon the sources of finance which Working Computer PLC can use to

invest in its Bernoulli division, it can consider two options: as long term source of finance and

short term source of finance.

Long term source of finance: This type of source of finance mainly used to meet the huge

finance requirement. bank loans, bonds and debentures are some external source of finance that

help in generating the high amount of finance for business to meet long term business objective.

Short term source of finance: These sources mainly helps to fulfil the short term

financial requirements of entity shares. retaining earnings, reserves and surpluses are the sources

that helps the organisation to generate the financial requirement to meet the financial objective of

business.

Considering the Working Computers Plc finance requirement of £18 million, it is

suggested that organisation should generate funds through long term source of finance. So, to

reduce and reach the optimum level of WACC, Working Company has to consider proper

balance of both debt and equity to raise £18 million. Financing solely through equity share is not

at all a good option for the company because cost of equity is even higher than the cost of debt as

equity shareholders are taking more risk to invest in the company as compared to the bond

holders. Hence, equity shareholders will expect higher returns from the company for the risk they

have taken. On the other side, financing solely through debt will increase the risk of company

defaulting on the debt payments and with this the interest rates have also to be taken into

consideration because higher interest rates will again increase cost of debt. So, I would

4

Terminal Value £59,22,79,296 £43,17,76,914

Total Present Value of

Company's operations

£4,32,52,210 £2,39,71,112

Terminal Value basically reflects the value of the organization after the forecast period. This

value shows 60-80% when we look at the total valuation of a company. So, by analysing both

the scenarios, we can say that company is getting better terminal value when new investment

is made.

Source of finance

When deciding upon the sources of finance which Working Computer PLC can use to

invest in its Bernoulli division, it can consider two options: as long term source of finance and

short term source of finance.

Long term source of finance: This type of source of finance mainly used to meet the huge

finance requirement. bank loans, bonds and debentures are some external source of finance that

help in generating the high amount of finance for business to meet long term business objective.

Short term source of finance: These sources mainly helps to fulfil the short term

financial requirements of entity shares. retaining earnings, reserves and surpluses are the sources

that helps the organisation to generate the financial requirement to meet the financial objective of

business.

Considering the Working Computers Plc finance requirement of £18 million, it is

suggested that organisation should generate funds through long term source of finance. So, to

reduce and reach the optimum level of WACC, Working Company has to consider proper

balance of both debt and equity to raise £18 million. Financing solely through equity share is not

at all a good option for the company because cost of equity is even higher than the cost of debt as

equity shareholders are taking more risk to invest in the company as compared to the bond

holders. Hence, equity shareholders will expect higher returns from the company for the risk they

have taken. On the other side, financing solely through debt will increase the risk of company

defaulting on the debt payments and with this the interest rates have also to be taken into

consideration because higher interest rates will again increase cost of debt. So, I would

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

recommend that company should consider an optimum balance where they can minimize

WACC.

Investment appraisal technique

Net present value method of investment appraisal technique is used in order to determine

the identify the suitability of proposed investment. The feasibility of project the net present value

of investments is evaluated with projected cash flows. Cost of capital is considered as 16.5%. the

inflation rate is considered as 1.75% and the marginal rate of taxation is considered as 34%.

Without new investment

Cash flows

2013 -£5,60,00,000

2014 £1,57,19,781

2015 £40,19,392

2016 £1,45,67,891

2017 £1,26,27,129

2018 £1,43,42,257

2019 £1,34,15,322

NPV £26,57,317

IRR 9%

With new investment

Cash flows

2013 -£1,80,00,000

2014 £1,75,44,409

2015 £12,29,730

2016 £1,09,99,352

2017 £88,63,344

2018 £1,06,43,205

2019 £97,79,890

NPV £1,86,05,138

IRR 56%

5

WACC.

Investment appraisal technique

Net present value method of investment appraisal technique is used in order to determine

the identify the suitability of proposed investment. The feasibility of project the net present value

of investments is evaluated with projected cash flows. Cost of capital is considered as 16.5%. the

inflation rate is considered as 1.75% and the marginal rate of taxation is considered as 34%.

Without new investment

Cash flows

2013 -£5,60,00,000

2014 £1,57,19,781

2015 £40,19,392

2016 £1,45,67,891

2017 £1,26,27,129

2018 £1,43,42,257

2019 £1,34,15,322

NPV £26,57,317

IRR 9%

With new investment

Cash flows

2013 -£1,80,00,000

2014 £1,75,44,409

2015 £12,29,730

2016 £1,09,99,352

2017 £88,63,344

2018 £1,06,43,205

2019 £97,79,890

NPV £1,86,05,138

IRR 56%

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gap between theory and practise

The NPV law, always claiming it is equivalent to other strategies logically. Nevertheless,

given the move towards NPV, other approaches are used in action at only in tandem to IRR and

NPV-type approaches, most of which don't require disregarding. Because businesses are using

these other approaches, another of two assumptions could be taken: either companies are making

inadequate choices or in reality the expectations behind the NPV principle are not met. The

findings of this study were aligned with both the view that perhaps the claims outlined in

curriculum are generally understood and accepted. Technological advances, especially that

increase of computational power, have supported the broader use DCF, allowing measurements

simple and at reasonable cost. Readers continue to emphasize the NPV law, arguing frequently

that it is technically superior to others.

CONCLUSION

From the above evaluation of investment project, it is suggested that Working Computer Plc

must adopt the proposed investment proposal as the net present value of projected investment is

higher and IRR also present higher rate of returns. The board of managers are advised to go with

the proposed investment.

6

The NPV law, always claiming it is equivalent to other strategies logically. Nevertheless,

given the move towards NPV, other approaches are used in action at only in tandem to IRR and

NPV-type approaches, most of which don't require disregarding. Because businesses are using

these other approaches, another of two assumptions could be taken: either companies are making

inadequate choices or in reality the expectations behind the NPV principle are not met. The

findings of this study were aligned with both the view that perhaps the claims outlined in

curriculum are generally understood and accepted. Technological advances, especially that

increase of computational power, have supported the broader use DCF, allowing measurements

simple and at reasonable cost. Readers continue to emphasize the NPV law, arguing frequently

that it is technically superior to others.

CONCLUSION

From the above evaluation of investment project, it is suggested that Working Computer Plc

must adopt the proposed investment proposal as the net present value of projected investment is

higher and IRR also present higher rate of returns. The board of managers are advised to go with

the proposed investment.

6

REFERENCES

Books and Journals:

Izurieta, N. P. V., 2015. El Ecuador y el proceso de cambio de la matriz productiva:

consideraciones para el desarrollo y equilibrio de la balanza comercial. Observatorio de

la Economía Latinoamericana. (207).

Simon, R., 2015. Sensitivity, specificity, PPV, and NPV for predictive biomarkers. JNCI:

Journal of the National Cancer Institute. 107(8).

Park, K. and Jang, S. S., 2013. Capital structure, free cash flow, diversification and firm

performance: A holistic analysis. International Journal of Hospitality Management. 33.

pp.51-63.

Hou, K., Van Dijk, M. A. and Zhang, Y., 2012. The implied cost of capital: A new

approach. Journal of Accounting and Economics. 53(3). pp.504-526.

7

Books and Journals:

Izurieta, N. P. V., 2015. El Ecuador y el proceso de cambio de la matriz productiva:

consideraciones para el desarrollo y equilibrio de la balanza comercial. Observatorio de

la Economía Latinoamericana. (207).

Simon, R., 2015. Sensitivity, specificity, PPV, and NPV for predictive biomarkers. JNCI:

Journal of the National Cancer Institute. 107(8).

Park, K. and Jang, S. S., 2013. Capital structure, free cash flow, diversification and firm

performance: A holistic analysis. International Journal of Hospitality Management. 33.

pp.51-63.

Hou, K., Van Dijk, M. A. and Zhang, Y., 2012. The implied cost of capital: A new

approach. Journal of Accounting and Economics. 53(3). pp.504-526.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

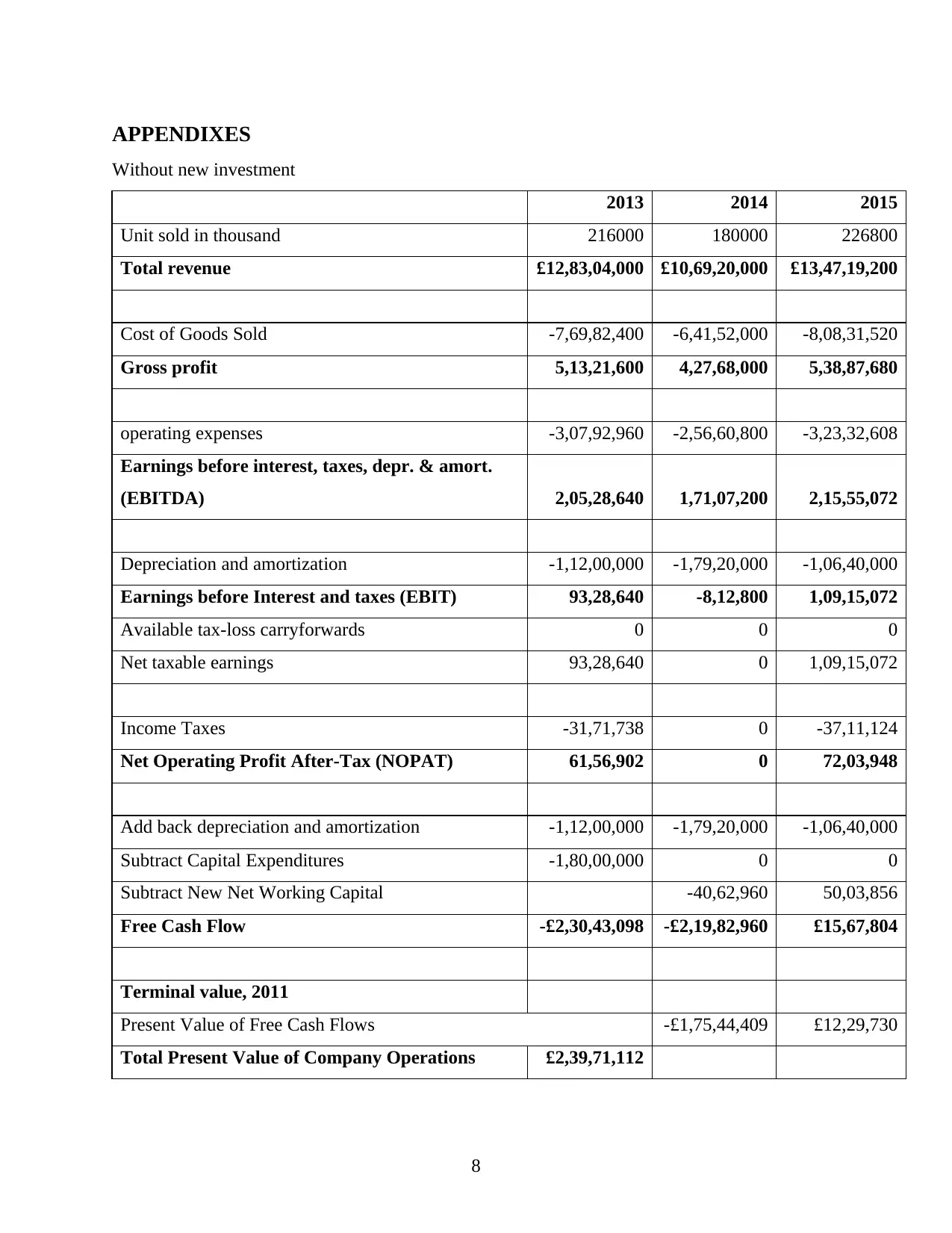

APPENDIXES

Without new investment

2013 2014 2015

Unit sold in thousand 216000 180000 226800

Total revenue £12,83,04,000 £10,69,20,000 £13,47,19,200

Cost of Goods Sold -7,69,82,400 -6,41,52,000 -8,08,31,520

Gross profit 5,13,21,600 4,27,68,000 5,38,87,680

operating expenses -3,07,92,960 -2,56,60,800 -3,23,32,608

Earnings before interest, taxes, depr. & amort.

(EBITDA) 2,05,28,640 1,71,07,200 2,15,55,072

Depreciation and amortization -1,12,00,000 -1,79,20,000 -1,06,40,000

Earnings before Interest and taxes (EBIT) 93,28,640 -8,12,800 1,09,15,072

Available tax-loss carryforwards 0 0 0

Net taxable earnings 93,28,640 0 1,09,15,072

Income Taxes -31,71,738 0 -37,11,124

Net Operating Profit After-Tax (NOPAT) 61,56,902 0 72,03,948

Add back depreciation and amortization -1,12,00,000 -1,79,20,000 -1,06,40,000

Subtract Capital Expenditures -1,80,00,000 0 0

Subtract New Net Working Capital -40,62,960 50,03,856

Free Cash Flow -£2,30,43,098 -£2,19,82,960 £15,67,804

Terminal value, 2011

Present Value of Free Cash Flows -£1,75,44,409 £12,29,730

Total Present Value of Company Operations £2,39,71,112

8

Without new investment

2013 2014 2015

Unit sold in thousand 216000 180000 226800

Total revenue £12,83,04,000 £10,69,20,000 £13,47,19,200

Cost of Goods Sold -7,69,82,400 -6,41,52,000 -8,08,31,520

Gross profit 5,13,21,600 4,27,68,000 5,38,87,680

operating expenses -3,07,92,960 -2,56,60,800 -3,23,32,608

Earnings before interest, taxes, depr. & amort.

(EBITDA) 2,05,28,640 1,71,07,200 2,15,55,072

Depreciation and amortization -1,12,00,000 -1,79,20,000 -1,06,40,000

Earnings before Interest and taxes (EBIT) 93,28,640 -8,12,800 1,09,15,072

Available tax-loss carryforwards 0 0 0

Net taxable earnings 93,28,640 0 1,09,15,072

Income Taxes -31,71,738 0 -37,11,124

Net Operating Profit After-Tax (NOPAT) 61,56,902 0 72,03,948

Add back depreciation and amortization -1,12,00,000 -1,79,20,000 -1,06,40,000

Subtract Capital Expenditures -1,80,00,000 0 0

Subtract New Net Working Capital -40,62,960 50,03,856

Free Cash Flow -£2,30,43,098 -£2,19,82,960 £15,67,804

Terminal value, 2011

Present Value of Free Cash Flows -£1,75,44,409 £12,29,730

Total Present Value of Company Operations £2,39,71,112

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

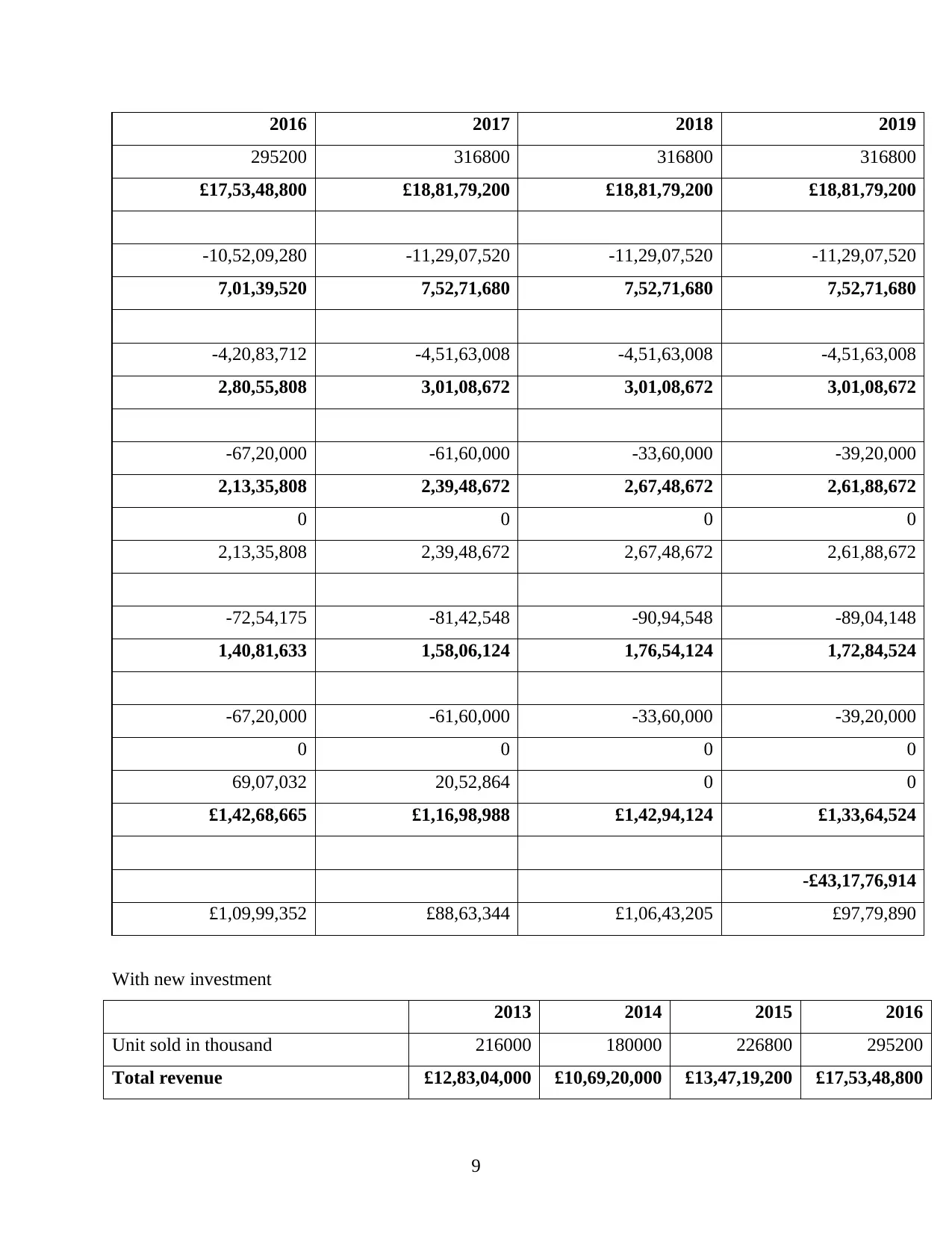

2016 2017 2018 2019

295200 316800 316800 316800

£17,53,48,800 £18,81,79,200 £18,81,79,200 £18,81,79,200

-10,52,09,280 -11,29,07,520 -11,29,07,520 -11,29,07,520

7,01,39,520 7,52,71,680 7,52,71,680 7,52,71,680

-4,20,83,712 -4,51,63,008 -4,51,63,008 -4,51,63,008

2,80,55,808 3,01,08,672 3,01,08,672 3,01,08,672

-67,20,000 -61,60,000 -33,60,000 -39,20,000

2,13,35,808 2,39,48,672 2,67,48,672 2,61,88,672

0 0 0 0

2,13,35,808 2,39,48,672 2,67,48,672 2,61,88,672

-72,54,175 -81,42,548 -90,94,548 -89,04,148

1,40,81,633 1,58,06,124 1,76,54,124 1,72,84,524

-67,20,000 -61,60,000 -33,60,000 -39,20,000

0 0 0 0

69,07,032 20,52,864 0 0

£1,42,68,665 £1,16,98,988 £1,42,94,124 £1,33,64,524

-£43,17,76,914

£1,09,99,352 £88,63,344 £1,06,43,205 £97,79,890

With new investment

2013 2014 2015 2016

Unit sold in thousand 216000 180000 226800 295200

Total revenue £12,83,04,000 £10,69,20,000 £13,47,19,200 £17,53,48,800

9

295200 316800 316800 316800

£17,53,48,800 £18,81,79,200 £18,81,79,200 £18,81,79,200

-10,52,09,280 -11,29,07,520 -11,29,07,520 -11,29,07,520

7,01,39,520 7,52,71,680 7,52,71,680 7,52,71,680

-4,20,83,712 -4,51,63,008 -4,51,63,008 -4,51,63,008

2,80,55,808 3,01,08,672 3,01,08,672 3,01,08,672

-67,20,000 -61,60,000 -33,60,000 -39,20,000

2,13,35,808 2,39,48,672 2,67,48,672 2,61,88,672

0 0 0 0

2,13,35,808 2,39,48,672 2,67,48,672 2,61,88,672

-72,54,175 -81,42,548 -90,94,548 -89,04,148

1,40,81,633 1,58,06,124 1,76,54,124 1,72,84,524

-67,20,000 -61,60,000 -33,60,000 -39,20,000

0 0 0 0

69,07,032 20,52,864 0 0

£1,42,68,665 £1,16,98,988 £1,42,94,124 £1,33,64,524

-£43,17,76,914

£1,09,99,352 £88,63,344 £1,06,43,205 £97,79,890

With new investment

2013 2014 2015 2016

Unit sold in thousand 216000 180000 226800 295200

Total revenue £12,83,04,000 £10,69,20,000 £13,47,19,200 £17,53,48,800

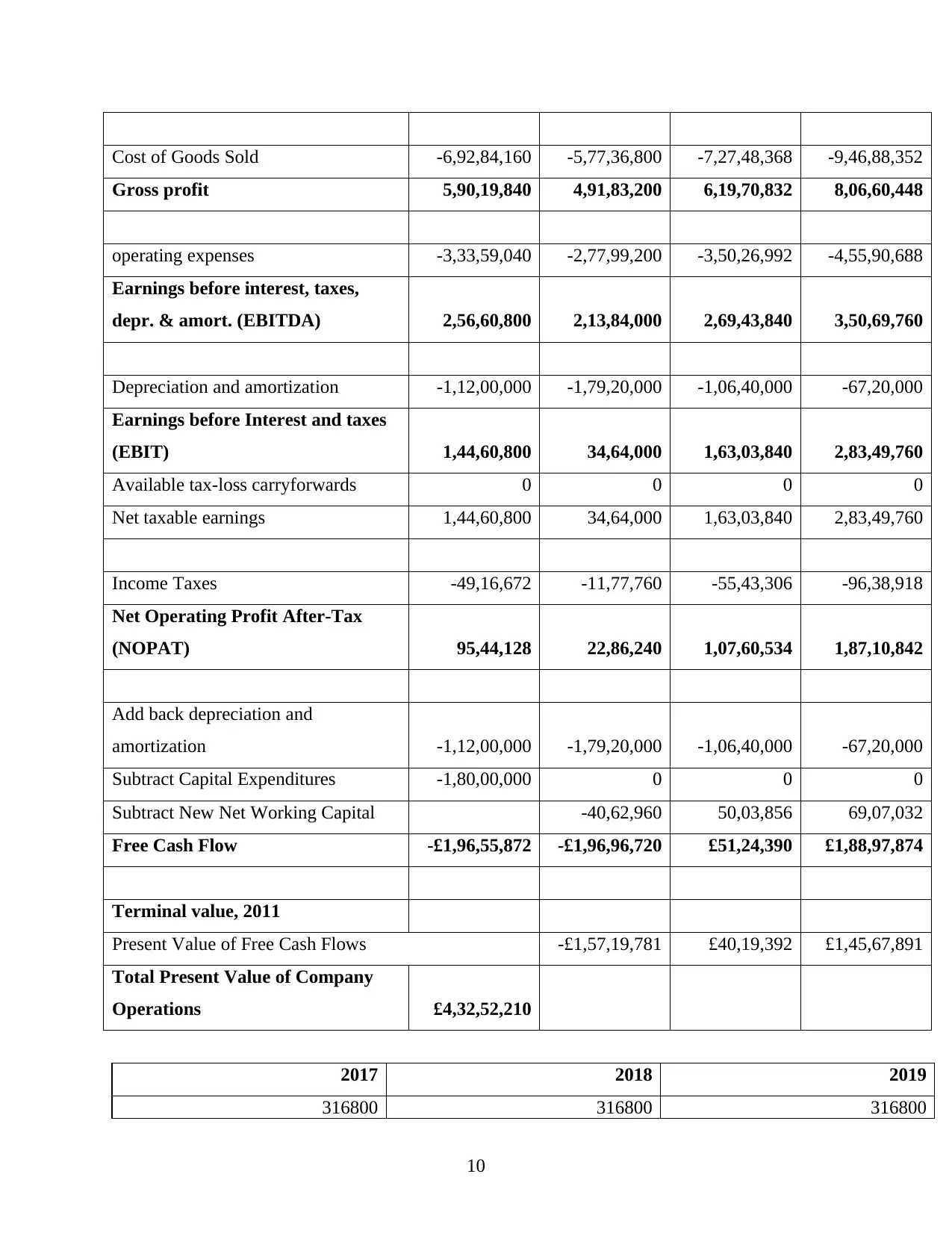

9

Cost of Goods Sold -6,92,84,160 -5,77,36,800 -7,27,48,368 -9,46,88,352

Gross profit 5,90,19,840 4,91,83,200 6,19,70,832 8,06,60,448

operating expenses -3,33,59,040 -2,77,99,200 -3,50,26,992 -4,55,90,688

Earnings before interest, taxes,

depr. & amort. (EBITDA) 2,56,60,800 2,13,84,000 2,69,43,840 3,50,69,760

Depreciation and amortization -1,12,00,000 -1,79,20,000 -1,06,40,000 -67,20,000

Earnings before Interest and taxes

(EBIT) 1,44,60,800 34,64,000 1,63,03,840 2,83,49,760

Available tax-loss carryforwards 0 0 0 0

Net taxable earnings 1,44,60,800 34,64,000 1,63,03,840 2,83,49,760

Income Taxes -49,16,672 -11,77,760 -55,43,306 -96,38,918

Net Operating Profit After-Tax

(NOPAT) 95,44,128 22,86,240 1,07,60,534 1,87,10,842

Add back depreciation and

amortization -1,12,00,000 -1,79,20,000 -1,06,40,000 -67,20,000

Subtract Capital Expenditures -1,80,00,000 0 0 0

Subtract New Net Working Capital -40,62,960 50,03,856 69,07,032

Free Cash Flow -£1,96,55,872 -£1,96,96,720 £51,24,390 £1,88,97,874

Terminal value, 2011

Present Value of Free Cash Flows -£1,57,19,781 £40,19,392 £1,45,67,891

Total Present Value of Company

Operations £4,32,52,210

2017 2018 2019

316800 316800 316800

10

Gross profit 5,90,19,840 4,91,83,200 6,19,70,832 8,06,60,448

operating expenses -3,33,59,040 -2,77,99,200 -3,50,26,992 -4,55,90,688

Earnings before interest, taxes,

depr. & amort. (EBITDA) 2,56,60,800 2,13,84,000 2,69,43,840 3,50,69,760

Depreciation and amortization -1,12,00,000 -1,79,20,000 -1,06,40,000 -67,20,000

Earnings before Interest and taxes

(EBIT) 1,44,60,800 34,64,000 1,63,03,840 2,83,49,760

Available tax-loss carryforwards 0 0 0 0

Net taxable earnings 1,44,60,800 34,64,000 1,63,03,840 2,83,49,760

Income Taxes -49,16,672 -11,77,760 -55,43,306 -96,38,918

Net Operating Profit After-Tax

(NOPAT) 95,44,128 22,86,240 1,07,60,534 1,87,10,842

Add back depreciation and

amortization -1,12,00,000 -1,79,20,000 -1,06,40,000 -67,20,000

Subtract Capital Expenditures -1,80,00,000 0 0 0

Subtract New Net Working Capital -40,62,960 50,03,856 69,07,032

Free Cash Flow -£1,96,55,872 -£1,96,96,720 £51,24,390 £1,88,97,874

Terminal value, 2011

Present Value of Free Cash Flows -£1,57,19,781 £40,19,392 £1,45,67,891

Total Present Value of Company

Operations £4,32,52,210

2017 2018 2019

316800 316800 316800

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.