Analysis of XERO Limited's Financial Reporting and GPFR Framework

VerifiedAdded on 2021/06/18

|17

|2244

|71

Report

AI Summary

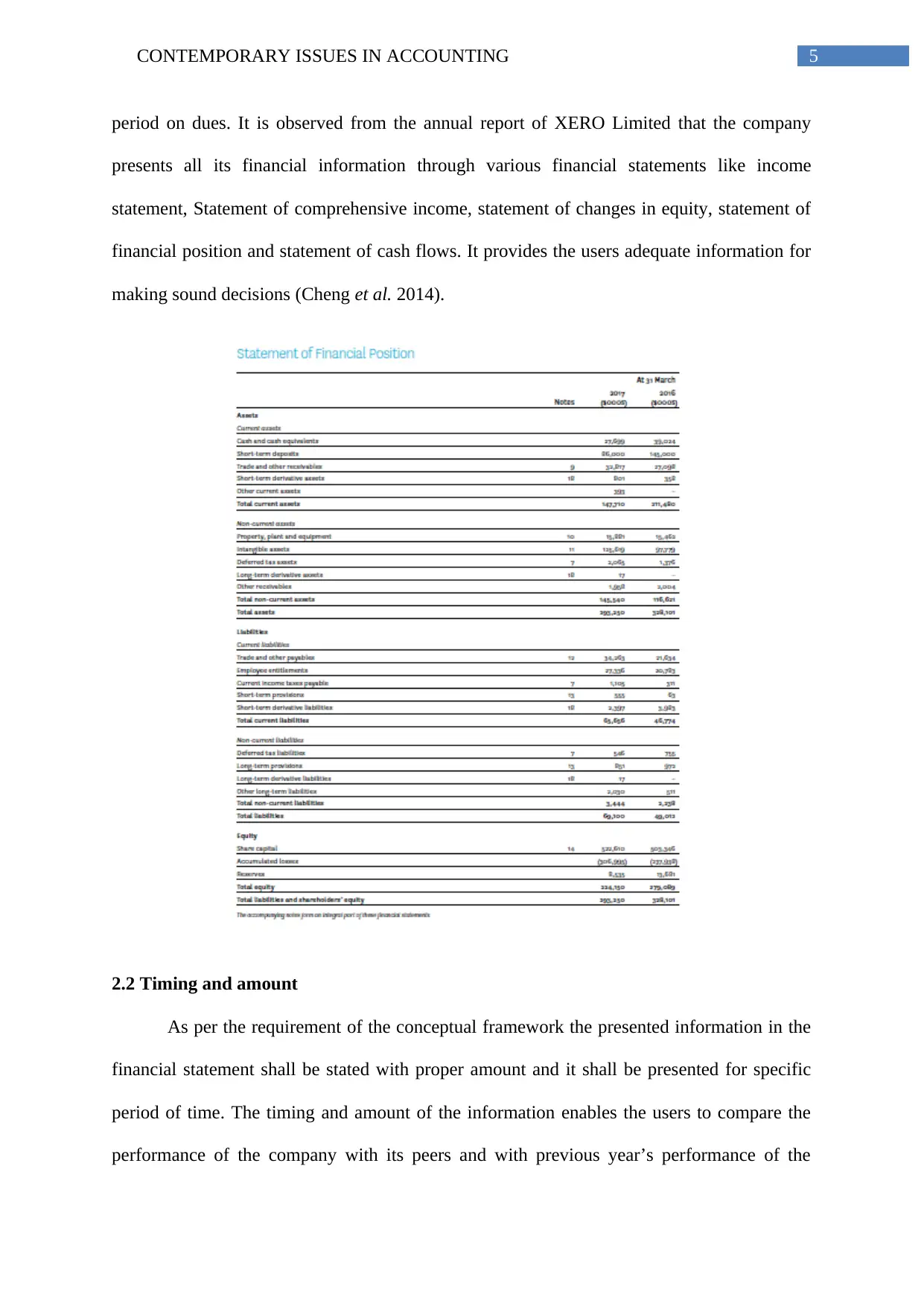

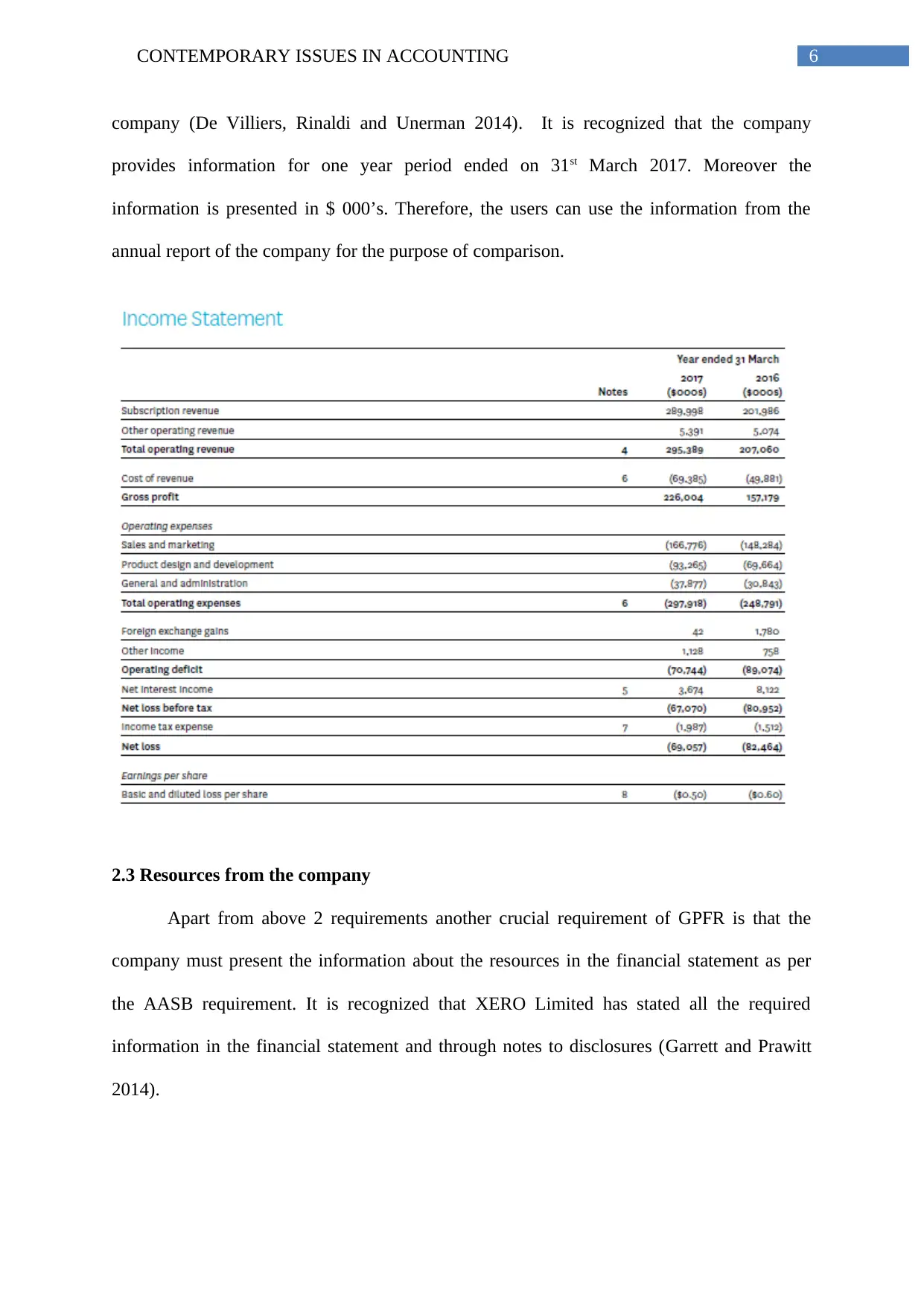

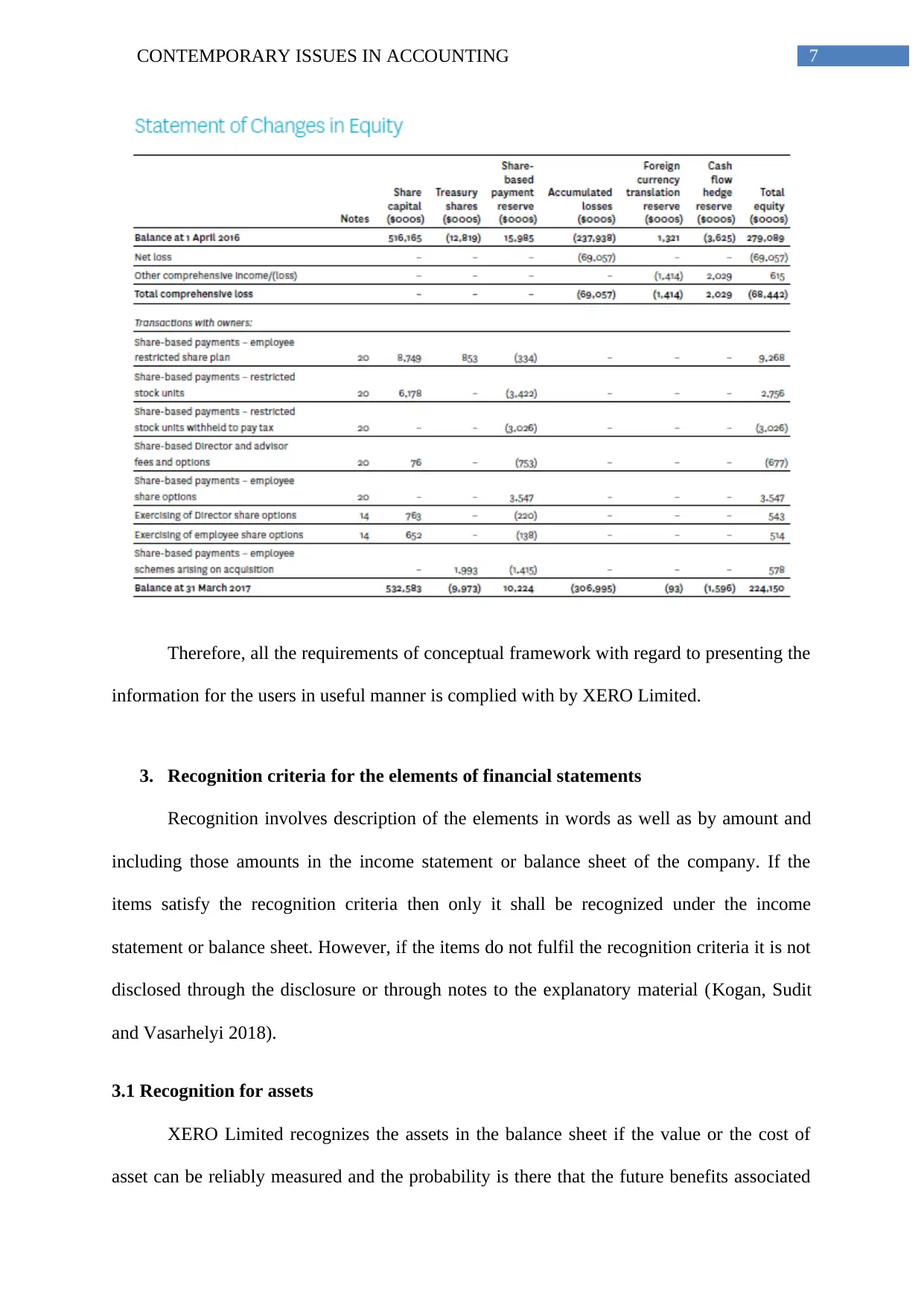

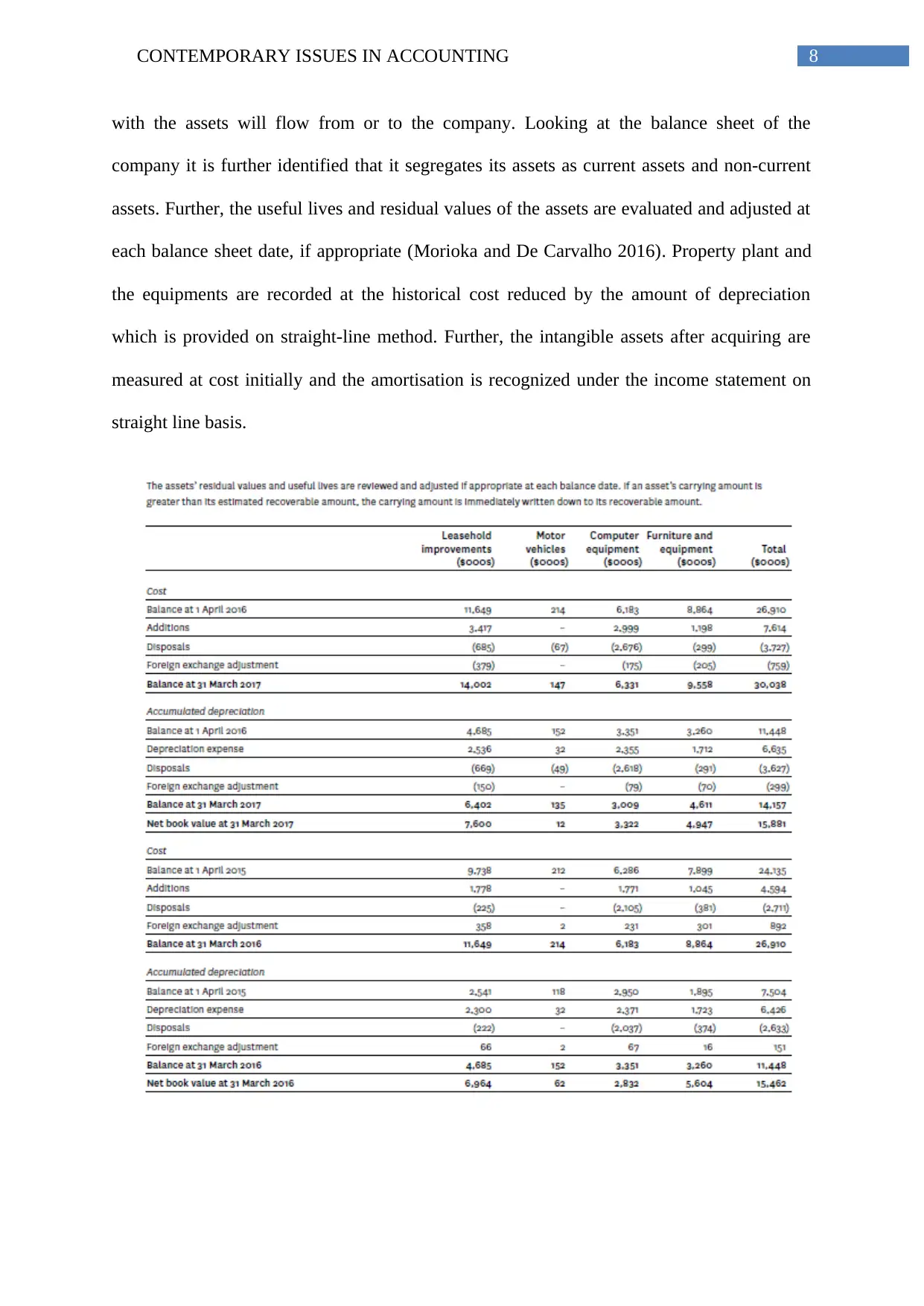

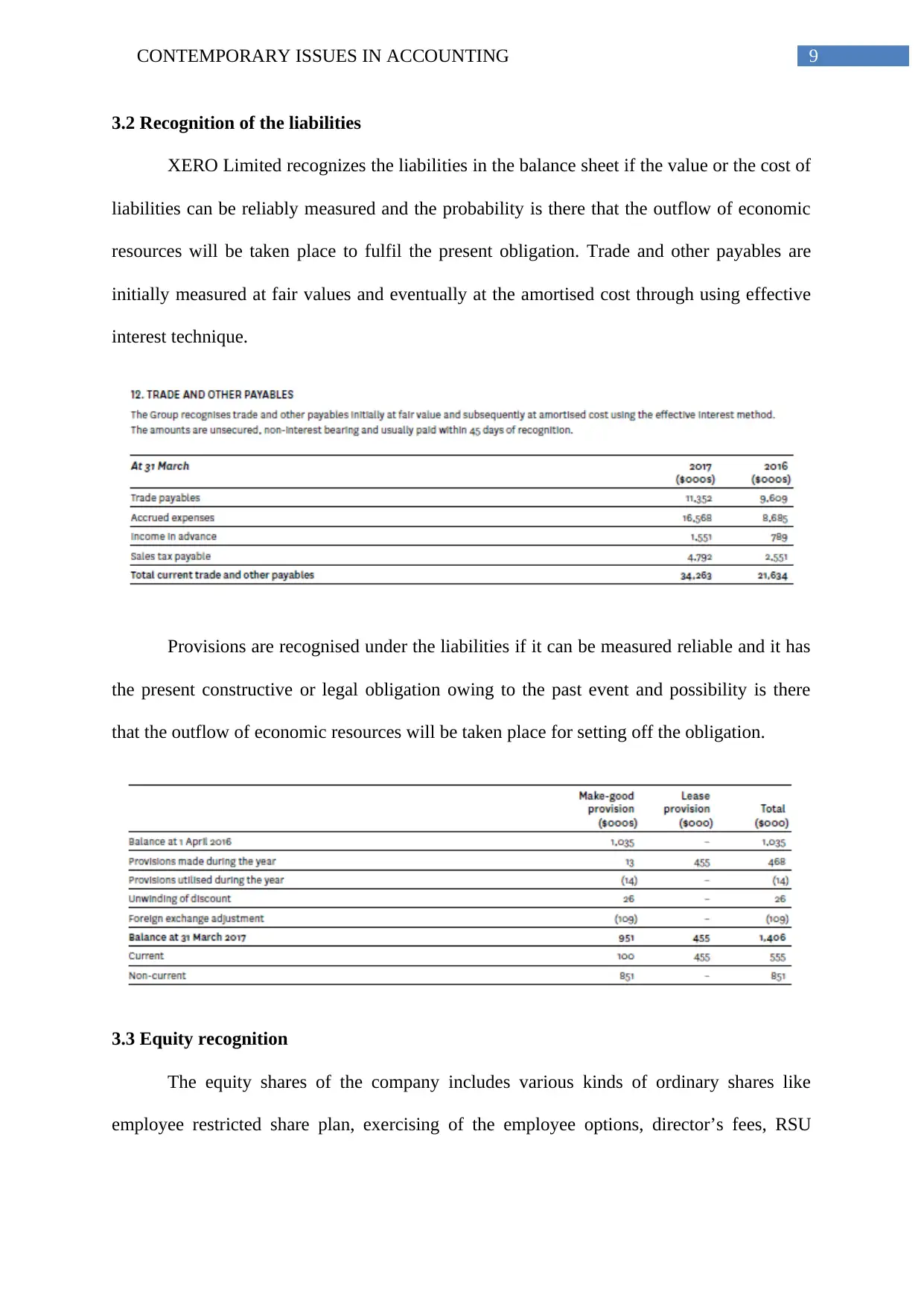

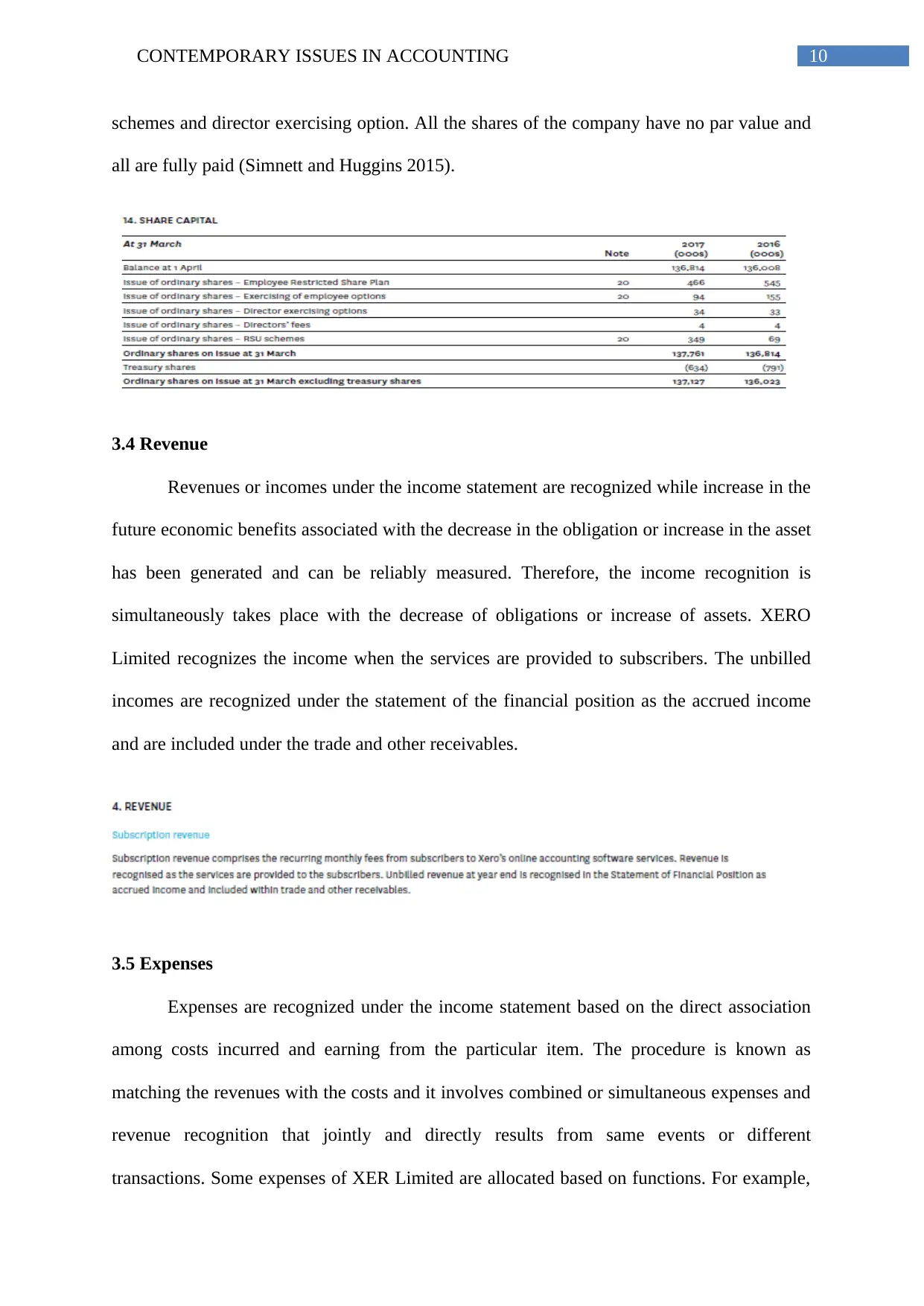

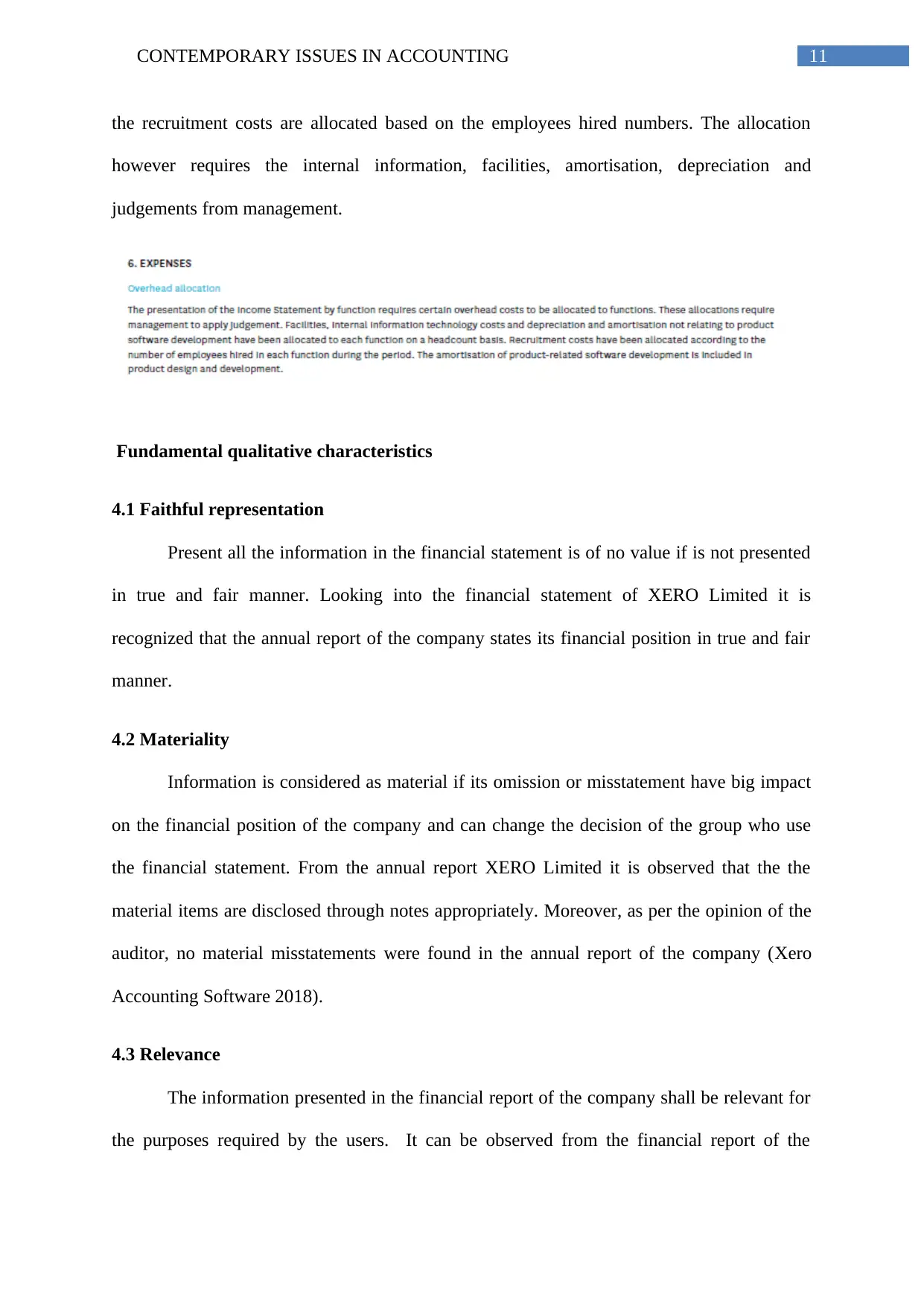

This report critically analyzes XERO Limited's financial reporting practices in relation to the General Purpose Financial Reporting (GPFR) framework. It begins with an introduction to the objectives of GPFR, emphasizing the importance of providing adequate and useful information to stakeholders such as investors, creditors, and lenders. The report then assesses whether XERO Limited's financial statements provide sufficient information regarding timing, amount, and company resources to facilitate sound decision-making. The analysis further explores the recognition criteria for various elements of financial statements, including assets, liabilities, equity, revenue, and expenses, examining how XERO Limited applies these criteria. The report also evaluates the company's compliance with fundamental qualitative characteristics such as faithful representation, materiality, and relevance, along with enhancing qualitative characteristics like timeliness, comparability, and understandability. The conclusion summarizes the company's adherence to the GPFR framework, highlighting its compliance with recognition criteria and qualitative characteristics. The report references various sources to support its findings and analysis.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.