Financial Reporting Compliance of Xero Limited: An Analysis

VerifiedAdded on 2023/04/23

|13

|2085

|234

Report

AI Summary

This report provides a detailed analysis of Xero Limited's financial reporting practices, focusing on its compliance with the International Accounting Standards Board (IASB) conceptual framework. The analysis evaluates Xero's adherence to measurement criteria, fundamental and enhancing qualitative characteristics, and the overall requirements of general purpose financial reporting. The report examines how Xero's financial statements meet the needs of end-users, such as investors and lenders, in making informed decisions. It also explores the level of accounting knowledge required by these users. The study utilizes Xero's 2018 annual report and relevant academic research to support its arguments, providing a comprehensive assessment of Xero's financial reporting integrity and transparency.

Contemporary Issues in Accounting: Xero Limited

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report is developed for providing an examination of the annual report of an ASX

listed entity, that is, Xero Ltd, in accordance with the principles of conceptual accounting

framework of IASB. It has been identified from analyzing the compliance of the company that it

has effectively followed all the general purpose financial reporting requirements stated by the

CF. The fundamental and enhancing qualitative characteristics are adequately met and it has met

the general objective of developing the financial statements.

2

This report is developed for providing an examination of the annual report of an ASX

listed entity, that is, Xero Ltd, in accordance with the principles of conceptual accounting

framework of IASB. It has been identified from analyzing the compliance of the company that it

has effectively followed all the general purpose financial reporting requirements stated by the

CF. The fundamental and enhancing qualitative characteristics are adequately met and it has met

the general objective of developing the financial statements.

2

Contents

Introduction......................................................................................................................................4

Critical Analysis of General Purpose Financial Reporting by XERO Ltd......................................4

Measurement Criteria Adopted by the Company & its Compliance with Conceptual

Framework Requirements............................................................................................................4

Fundamental Qualitative Characteristics of Conceptual Framework Applied by Xero Limited.5

Enhancing Qualitative Characteristics of Conceptual Framework Applied by Company...........7

Decision Making Relevance of the Financial Report of the Company......................................10

Knowledge required by the end-users of Financial Reports as stated by CF to Assist in

Decision Making........................................................................................................................11

Evaluation whether Xero Ltd has met the requirement of general purpose financial report.....11

Conclusion.....................................................................................................................................11

Recommendation...........................................................................................................................12

References......................................................................................................................................13

3

Introduction......................................................................................................................................4

Critical Analysis of General Purpose Financial Reporting by XERO Ltd......................................4

Measurement Criteria Adopted by the Company & its Compliance with Conceptual

Framework Requirements............................................................................................................4

Fundamental Qualitative Characteristics of Conceptual Framework Applied by Xero Limited.5

Enhancing Qualitative Characteristics of Conceptual Framework Applied by Company...........7

Decision Making Relevance of the Financial Report of the Company......................................10

Knowledge required by the end-users of Financial Reports as stated by CF to Assist in

Decision Making........................................................................................................................11

Evaluation whether Xero Ltd has met the requirement of general purpose financial report.....11

Conclusion.....................................................................................................................................11

Recommendation...........................................................................................................................12

References......................................................................................................................................13

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The compliance with the conceptual framework of accounting is becoming essential for

business entities around the world developing their financial statements in accordance with IASB

(International Accounting Standard Board). The AASB (Australian Accounting Standards

Board) have also directed all the ASX listed entities to develop their financial reports as per the

IASB standards. In this context, this report is directed to a selected an ASX listed corporation by

providing an evaluation of its compliance with the essential requirements of the conceptual

framework of accounting. This is undertaken by evaluation of the annual report of the selected

company and examining its compliance with the qualitative and measurement criteria’s stated by

the CF. The Company selected for analysis purpose is Xero Limited, a public software company

involved in providing cloud based software platform for small and medium-sized business.

Critical Analysis of General Purpose Financial Reporting by XERO Ltd

Measurement Criteria Adopted by the Company & its Compliance with Conceptual

Framework Requirements

As per the Conceptual Framework, a listed reporting entity needs to provide information

about the measurement base it chooses to value its assets & Liabilities. A Business entity can

choose measurement approach either historical cost or current value as stated by CF. Current

value is divided into fair value, value in use ¤t cost. An Entity needs to select an

appropriate measurement approach which meets the requirement and objective of General

Purpose Financial Reporting (Complied Framework, 2015).On the evaluation on Annual Report

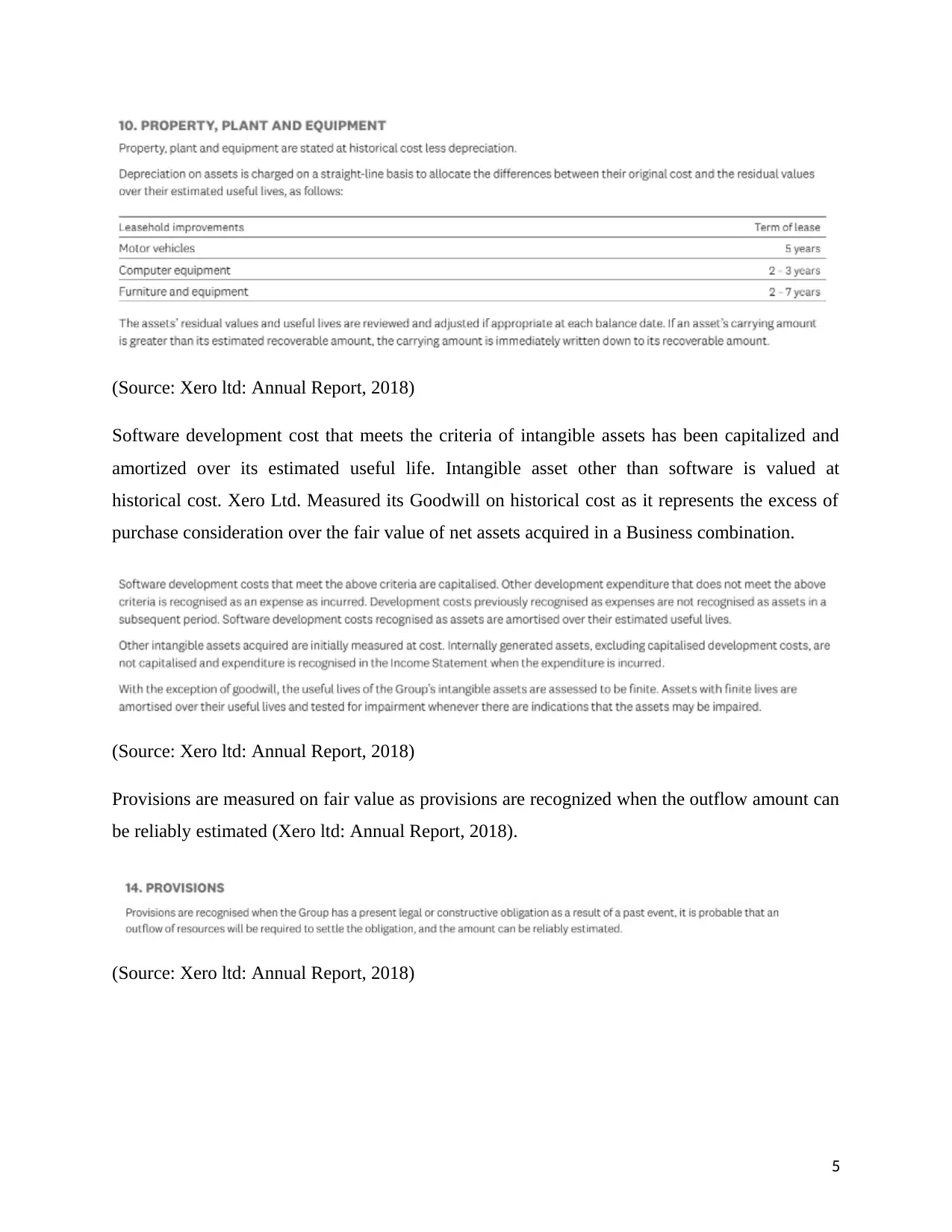

it can be said that Xero Ltd. has valued its fixed assets (Property, Plant & Equipment) on

historical cost less Depreciation which is charged on Straight Line basis. Fixed Assets are tested

for Impairment whenever there are indications of it.

4

The compliance with the conceptual framework of accounting is becoming essential for

business entities around the world developing their financial statements in accordance with IASB

(International Accounting Standard Board). The AASB (Australian Accounting Standards

Board) have also directed all the ASX listed entities to develop their financial reports as per the

IASB standards. In this context, this report is directed to a selected an ASX listed corporation by

providing an evaluation of its compliance with the essential requirements of the conceptual

framework of accounting. This is undertaken by evaluation of the annual report of the selected

company and examining its compliance with the qualitative and measurement criteria’s stated by

the CF. The Company selected for analysis purpose is Xero Limited, a public software company

involved in providing cloud based software platform for small and medium-sized business.

Critical Analysis of General Purpose Financial Reporting by XERO Ltd

Measurement Criteria Adopted by the Company & its Compliance with Conceptual

Framework Requirements

As per the Conceptual Framework, a listed reporting entity needs to provide information

about the measurement base it chooses to value its assets & Liabilities. A Business entity can

choose measurement approach either historical cost or current value as stated by CF. Current

value is divided into fair value, value in use ¤t cost. An Entity needs to select an

appropriate measurement approach which meets the requirement and objective of General

Purpose Financial Reporting (Complied Framework, 2015).On the evaluation on Annual Report

it can be said that Xero Ltd. has valued its fixed assets (Property, Plant & Equipment) on

historical cost less Depreciation which is charged on Straight Line basis. Fixed Assets are tested

for Impairment whenever there are indications of it.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Source: Xero ltd: Annual Report, 2018)

Software development cost that meets the criteria of intangible assets has been capitalized and

amortized over its estimated useful life. Intangible asset other than software is valued at

historical cost. Xero Ltd. Measured its Goodwill on historical cost as it represents the excess of

purchase consideration over the fair value of net assets acquired in a Business combination.

(Source: Xero ltd: Annual Report, 2018)

Provisions are measured on fair value as provisions are recognized when the outflow amount can

be reliably estimated (Xero ltd: Annual Report, 2018).

(Source: Xero ltd: Annual Report, 2018)

5

Software development cost that meets the criteria of intangible assets has been capitalized and

amortized over its estimated useful life. Intangible asset other than software is valued at

historical cost. Xero Ltd. Measured its Goodwill on historical cost as it represents the excess of

purchase consideration over the fair value of net assets acquired in a Business combination.

(Source: Xero ltd: Annual Report, 2018)

Provisions are measured on fair value as provisions are recognized when the outflow amount can

be reliably estimated (Xero ltd: Annual Report, 2018).

(Source: Xero ltd: Annual Report, 2018)

5

Fundamental Qualitative Characteristics of Conceptual Framework Applied by Xero

Limited

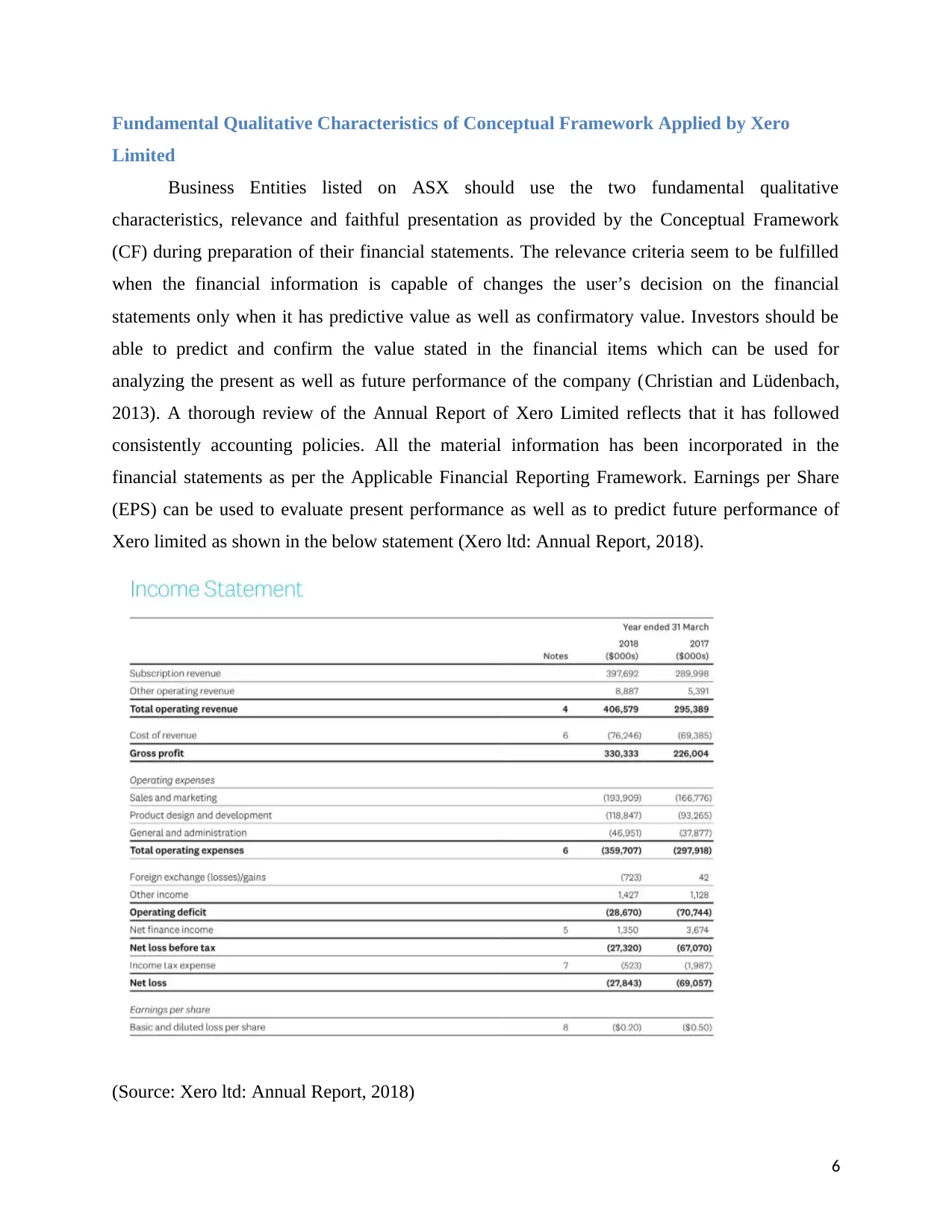

Business Entities listed on ASX should use the two fundamental qualitative

characteristics, relevance and faithful presentation as provided by the Conceptual Framework

(CF) during preparation of their financial statements. The relevance criteria seem to be fulfilled

when the financial information is capable of changes the user’s decision on the financial

statements only when it has predictive value as well as confirmatory value. Investors should be

able to predict and confirm the value stated in the financial items which can be used for

analyzing the present as well as future performance of the company (Christian and Lüdenbach,

2013). A thorough review of the Annual Report of Xero Limited reflects that it has followed

consistently accounting policies. All the material information has been incorporated in the

financial statements as per the Applicable Financial Reporting Framework. Earnings per Share

(EPS) can be used to evaluate present performance as well as to predict future performance of

Xero limited as shown in the below statement (Xero ltd: Annual Report, 2018).

(Source: Xero ltd: Annual Report, 2018)

6

Limited

Business Entities listed on ASX should use the two fundamental qualitative

characteristics, relevance and faithful presentation as provided by the Conceptual Framework

(CF) during preparation of their financial statements. The relevance criteria seem to be fulfilled

when the financial information is capable of changes the user’s decision on the financial

statements only when it has predictive value as well as confirmatory value. Investors should be

able to predict and confirm the value stated in the financial items which can be used for

analyzing the present as well as future performance of the company (Christian and Lüdenbach,

2013). A thorough review of the Annual Report of Xero Limited reflects that it has followed

consistently accounting policies. All the material information has been incorporated in the

financial statements as per the Applicable Financial Reporting Framework. Earnings per Share

(EPS) can be used to evaluate present performance as well as to predict future performance of

Xero limited as shown in the below statement (Xero ltd: Annual Report, 2018).

(Source: Xero ltd: Annual Report, 2018)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Faithful presentation of information is the second fundamental qualitative characteristics

in financial reporting provided by the Conceptual Framework. The financial information should

be free from material misstatement and errors. It should give a true and fair representation of

company’s financial position (Schroeder, Clark and Cathey, 2016). By analyzing the financial

report and audit report of Xero Limited prepared by E & Y, we can say that the financial

information provided in financial statements is complete and gives a faithful presentation as

stated in below report (Xero ltd: Annual Report, 2018).

(Source: Xero ltd: Annual Report, 2018)

Enhancing Qualitative Characteristics of Conceptual Framework Applied by Company

The Conceptual Framework has provided some enhancing qualitative principles in

addition to the above mentioned fundamental qualitative characteristics that need to be followed

7

in financial reporting provided by the Conceptual Framework. The financial information should

be free from material misstatement and errors. It should give a true and fair representation of

company’s financial position (Schroeder, Clark and Cathey, 2016). By analyzing the financial

report and audit report of Xero Limited prepared by E & Y, we can say that the financial

information provided in financial statements is complete and gives a faithful presentation as

stated in below report (Xero ltd: Annual Report, 2018).

(Source: Xero ltd: Annual Report, 2018)

Enhancing Qualitative Characteristics of Conceptual Framework Applied by Company

The Conceptual Framework has provided some enhancing qualitative principles in

addition to the above mentioned fundamental qualitative characteristics that need to be followed

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

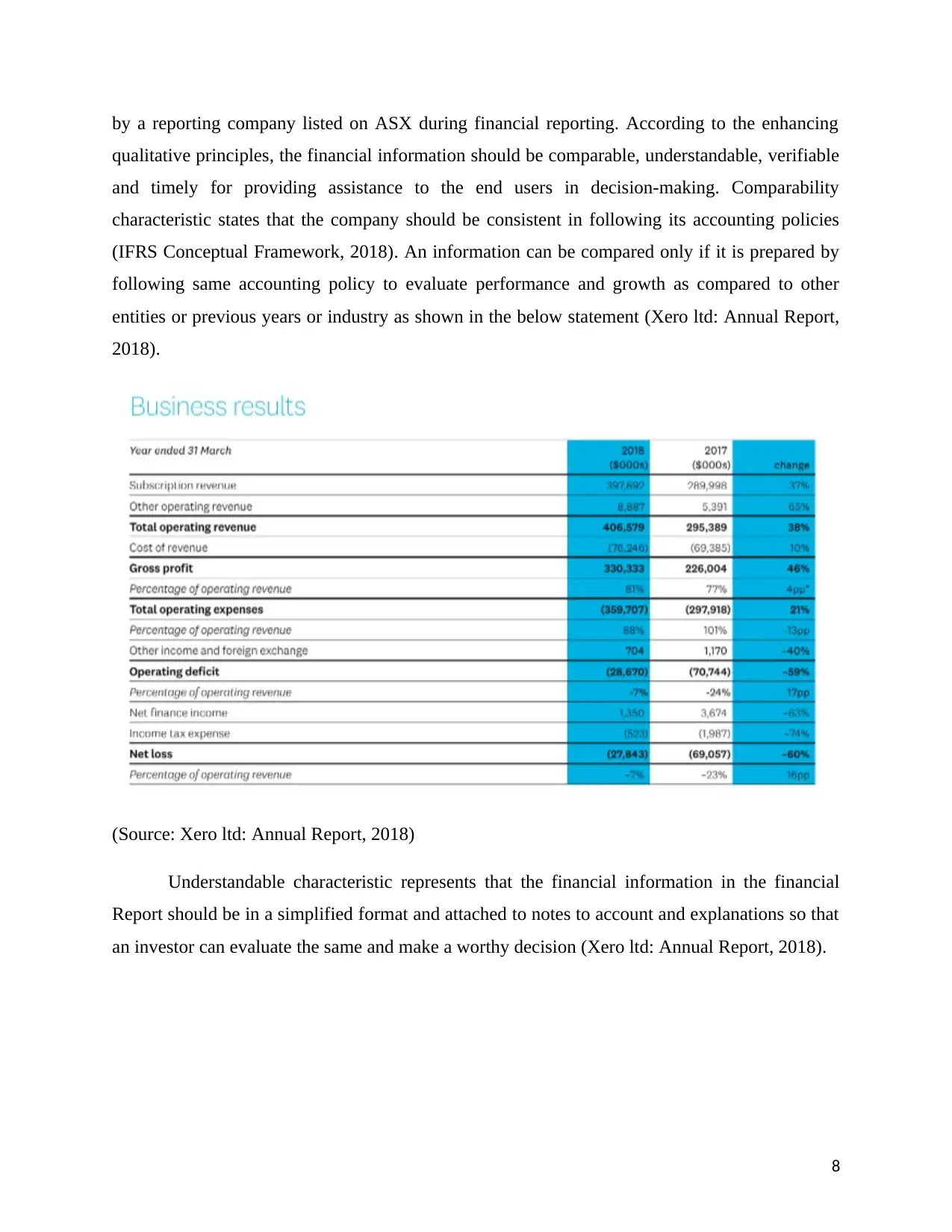

by a reporting company listed on ASX during financial reporting. According to the enhancing

qualitative principles, the financial information should be comparable, understandable, verifiable

and timely for providing assistance to the end users in decision-making. Comparability

characteristic states that the company should be consistent in following its accounting policies

(IFRS Conceptual Framework, 2018). An information can be compared only if it is prepared by

following same accounting policy to evaluate performance and growth as compared to other

entities or previous years or industry as shown in the below statement (Xero ltd: Annual Report,

2018).

(Source: Xero ltd: Annual Report, 2018)

Understandable characteristic represents that the financial information in the financial

Report should be in a simplified format and attached to notes to account and explanations so that

an investor can evaluate the same and make a worthy decision (Xero ltd: Annual Report, 2018).

8

qualitative principles, the financial information should be comparable, understandable, verifiable

and timely for providing assistance to the end users in decision-making. Comparability

characteristic states that the company should be consistent in following its accounting policies

(IFRS Conceptual Framework, 2018). An information can be compared only if it is prepared by

following same accounting policy to evaluate performance and growth as compared to other

entities or previous years or industry as shown in the below statement (Xero ltd: Annual Report,

2018).

(Source: Xero ltd: Annual Report, 2018)

Understandable characteristic represents that the financial information in the financial

Report should be in a simplified format and attached to notes to account and explanations so that

an investor can evaluate the same and make a worthy decision (Xero ltd: Annual Report, 2018).

8

(Source: Xero ltd: Annual Report, 2018)

Verifiability characteristic ensures that the information should be easily verifiable by the

decision makers. Timely information represents the updated information on the right time.

Xero Limited has given its financial information pursuant to relevant years in quantitative

format with all the explanations to it to make it comparable, understandable, verifiable and

timely. Xero Limited has properly fulfilled all the requirements of conceptual framework for

enhancing its qualitative characteristics of financial information as can be seen from the below

statements and reports (Xero ltd: Annual Report, 2018).

9

Verifiability characteristic ensures that the information should be easily verifiable by the

decision makers. Timely information represents the updated information on the right time.

Xero Limited has given its financial information pursuant to relevant years in quantitative

format with all the explanations to it to make it comparable, understandable, verifiable and

timely. Xero Limited has properly fulfilled all the requirements of conceptual framework for

enhancing its qualitative characteristics of financial information as can be seen from the below

statements and reports (Xero ltd: Annual Report, 2018).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Source: Xero ltd: Annual Report, 2018)

Decision Making Relevance of the Financial Report of the Company

The general purpose financial report is useful only if it provides the required financial

information at the right time to the right person in the right quantity. The end users of the

financial reports such as investors, potential investors, lenders, bankers are going to use this

financial report to grab the information from the report which is useful for them in decision

making. As such, the company has provided financial statements, business results, revenue

statement to be used by the present and potential investors for developing overview of the

company, and analyze its future growth prospects. The balance sheet has provided information

10

Decision Making Relevance of the Financial Report of the Company

The general purpose financial report is useful only if it provides the required financial

information at the right time to the right person in the right quantity. The end users of the

financial reports such as investors, potential investors, lenders, bankers are going to use this

financial report to grab the information from the report which is useful for them in decision

making. As such, the company has provided financial statements, business results, revenue

statement to be used by the present and potential investors for developing overview of the

company, and analyze its future growth prospects. The balance sheet has provided information

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

relating to its type of assets and liabilities that is largely useful for the creditors and lenders to

examine the liquidity and solvency position of the company (Xero ltd: Annual Report, 2018).

Knowledge required by the end-users of Financial Reports as stated by CF to Assist in

Decision Making

The CF has stated that end-users of financial report should have basic accounting

knowledge to understand the financial information presented by an entity. It helps the end users

to understand the information provided in the report and use it in their investment decision

making. Thus, end-users of financial reports must have sound knowledge of accounting and

finance to evaluate the present performance of the company and predict future performance.

However, in addition with the basic knowledge of accounting, the investors and financial

analysts need to have accounting expertise to predict the company growth trends by using

analytical techniques such as ratio analysis, horizontal analysis, vertical analysis (Macve, 2015).

Evaluation whether Xero Ltd has met the requirement of general purpose financial report

In general the requirement of general purpose financial report is provide all essential

information to the users of the financial report that helps them to make useful decision and

information provided must complies the legitimacy requirement define in various laws and

regulation. In this context, Xero Ltd has followed all the requirement of general purpose

financial report through providing information such as complete set of financial statements

(Income statement, statement of financial position, cash flow statement and statement of change

in equity) and annual report has also disclosed proper notes to accounts that explains how

accounting of financial statements have been performed and abide with required laws and

regulations. Financial statement of Xero Ltd has been prepared in accordance with generally

accepted accounting practice of New Zealand (NZ GAAP) and this company also complies with

the International Financial Reporting Standards (IFRS). Through looking at the annual report it

can be said that Xero Ltd. has successfully adopted new accounting standards in order to

promote the comparability of financial reports and also to improve the decision making process

of users (IFRS Conceptual Framework, 2018).

11

examine the liquidity and solvency position of the company (Xero ltd: Annual Report, 2018).

Knowledge required by the end-users of Financial Reports as stated by CF to Assist in

Decision Making

The CF has stated that end-users of financial report should have basic accounting

knowledge to understand the financial information presented by an entity. It helps the end users

to understand the information provided in the report and use it in their investment decision

making. Thus, end-users of financial reports must have sound knowledge of accounting and

finance to evaluate the present performance of the company and predict future performance.

However, in addition with the basic knowledge of accounting, the investors and financial

analysts need to have accounting expertise to predict the company growth trends by using

analytical techniques such as ratio analysis, horizontal analysis, vertical analysis (Macve, 2015).

Evaluation whether Xero Ltd has met the requirement of general purpose financial report

In general the requirement of general purpose financial report is provide all essential

information to the users of the financial report that helps them to make useful decision and

information provided must complies the legitimacy requirement define in various laws and

regulation. In this context, Xero Ltd has followed all the requirement of general purpose

financial report through providing information such as complete set of financial statements

(Income statement, statement of financial position, cash flow statement and statement of change

in equity) and annual report has also disclosed proper notes to accounts that explains how

accounting of financial statements have been performed and abide with required laws and

regulations. Financial statement of Xero Ltd has been prepared in accordance with generally

accepted accounting practice of New Zealand (NZ GAAP) and this company also complies with

the International Financial Reporting Standards (IFRS). Through looking at the annual report it

can be said that Xero Ltd. has successfully adopted new accounting standards in order to

promote the comparability of financial reports and also to improve the decision making process

of users (IFRS Conceptual Framework, 2018).

11

Conclusion

It has inferred from the overall evaluation of the annual report of the company that it has

followed all the qualitative characteristics provided by the conceptual accounting framework.

The company has met the general objective behind the development of financial reporting as

stated within the conceptual framework of accounting.

Recommendation

It can be recommended from the overall discussion held within the report that company

has adequately followed all the reporting requirements that the conceptual framework of

accounting requires to be adopted by the ASX listed entities. As such, the integrity and

transparency in its financial operations are ensured and therefore it presents less risk for the

investors in respect of occurrence of any error or fraud that can negatively impact the interests of

the investors.

12

It has inferred from the overall evaluation of the annual report of the company that it has

followed all the qualitative characteristics provided by the conceptual accounting framework.

The company has met the general objective behind the development of financial reporting as

stated within the conceptual framework of accounting.

Recommendation

It can be recommended from the overall discussion held within the report that company

has adequately followed all the reporting requirements that the conceptual framework of

accounting requires to be adopted by the ASX listed entities. As such, the integrity and

transparency in its financial operations are ensured and therefore it presents less risk for the

investors in respect of occurrence of any error or fraud that can negatively impact the interests of

the investors.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.