Management Accounting Report: XLG Cleaning Products, Variance Analysis

VerifiedAdded on 2023/01/09

|12

|2950

|82

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, specifically focusing on variance analysis and its application within XLG, a cleaning product company. The report begins with an introduction to management accounting and its role in strategic decision-making, followed by a detailed examination of various variances, including sales price variance, sales volume contribution variance, material price planning variance, and material price operational variance. The merits and demerits of using variances are critically evaluated, considering their impact on cost management, performance evaluation, accountability, and organizational structure. The report then transitions to assessing the 'make or buy' decision, specifically focusing on XLG's choice to either import famaQ from Brazil or manufacture it in the UK, considering factors such as production costs, shipping times, and market demand. The analysis incorporates calculations of key variances and demonstrates decision-making abilities under risk, providing a well-rounded understanding of financial management in a competitive business environment. The report concludes with a summary of findings and recommendations for XLG.

Report Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

PART A...........................................................................................................................................1

1. Calculate price and sales volume variance..............................................................................1

2. Calculate the material price planning and operational variance..............................................3

3. Critically evaluate the merits or demerits of using variances..................................................5

PART B...........................................................................................................................................7

1. Assessing the report that FamaQ in house in UK keep importing from Brazil.......................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

MAIN BODY..................................................................................................................................1

PART A...........................................................................................................................................1

1. Calculate price and sales volume variance..............................................................................1

2. Calculate the material price planning and operational variance..............................................3

3. Critically evaluate the merits or demerits of using variances..................................................5

PART B...........................................................................................................................................7

1. Assessing the report that FamaQ in house in UK keep importing from Brazil.......................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting is a method that companies use to monitor company success and to

make strategic decisions (Adler, 2018). The supervisors should be free, with the support of it, to

determine whether or not it should make adjustments in organizational policies. There have been

multiple stakeholders including staff, administrators, senior executives, and owners etc. who use

performance reviews to determine if the company is operating well or not. This assessment is

based on the business XLG that is a consumer cleaning agency that is headquartered in the

eastern region of Britain. There will be two separate organisation-made cleaning services. There

are two separate chemicals that are called X and Y. The demand for business in the industry is

quite strong. The company decided to switch all of its sales digitally due to lockout due to

COVID pandemic. Various elements should be examined for this reason. This involves

estimating variances such as market price and quantity, commodity quality forecasting and

organizational variation, and assessing the advantages and disadvantages of including them in

managerial performance evaluation. In addition, a comparative summary is also provided in this

study which assesses the choice to make famaQ at home in the UK or continue to imports from

Brazil or not.

MAIN BODY

PART A

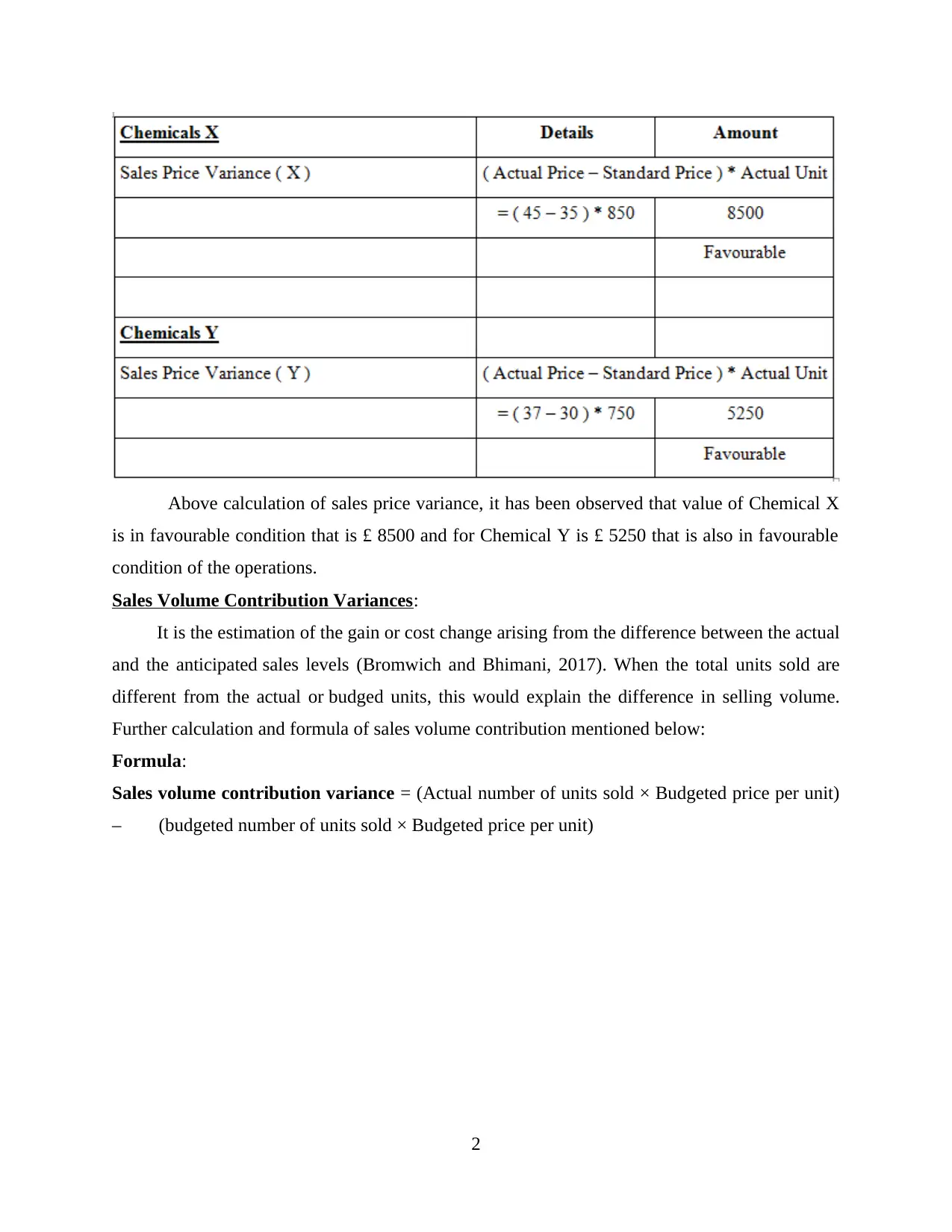

1. Calculate price and sales volume variance

Sales Price Variances:

The sales price variance is equal to the variation among actual market demand prices and

target price projections (Bastable and Bao, 2018). Net prices are both the amount of the products

that are actually available and the net unit price. Likewise, real sales at the total budget point suit

the overall sold units and the budgeted price for each unit. Below mention calculation are as

follow:

1

Management accounting is a method that companies use to monitor company success and to

make strategic decisions (Adler, 2018). The supervisors should be free, with the support of it, to

determine whether or not it should make adjustments in organizational policies. There have been

multiple stakeholders including staff, administrators, senior executives, and owners etc. who use

performance reviews to determine if the company is operating well or not. This assessment is

based on the business XLG that is a consumer cleaning agency that is headquartered in the

eastern region of Britain. There will be two separate organisation-made cleaning services. There

are two separate chemicals that are called X and Y. The demand for business in the industry is

quite strong. The company decided to switch all of its sales digitally due to lockout due to

COVID pandemic. Various elements should be examined for this reason. This involves

estimating variances such as market price and quantity, commodity quality forecasting and

organizational variation, and assessing the advantages and disadvantages of including them in

managerial performance evaluation. In addition, a comparative summary is also provided in this

study which assesses the choice to make famaQ at home in the UK or continue to imports from

Brazil or not.

MAIN BODY

PART A

1. Calculate price and sales volume variance

Sales Price Variances:

The sales price variance is equal to the variation among actual market demand prices and

target price projections (Bastable and Bao, 2018). Net prices are both the amount of the products

that are actually available and the net unit price. Likewise, real sales at the total budget point suit

the overall sold units and the budgeted price for each unit. Below mention calculation are as

follow:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Above calculation of sales price variance, it has been observed that value of Chemical X

is in favourable condition that is £ 8500 and for Chemical Y is £ 5250 that is also in favourable

condition of the operations.

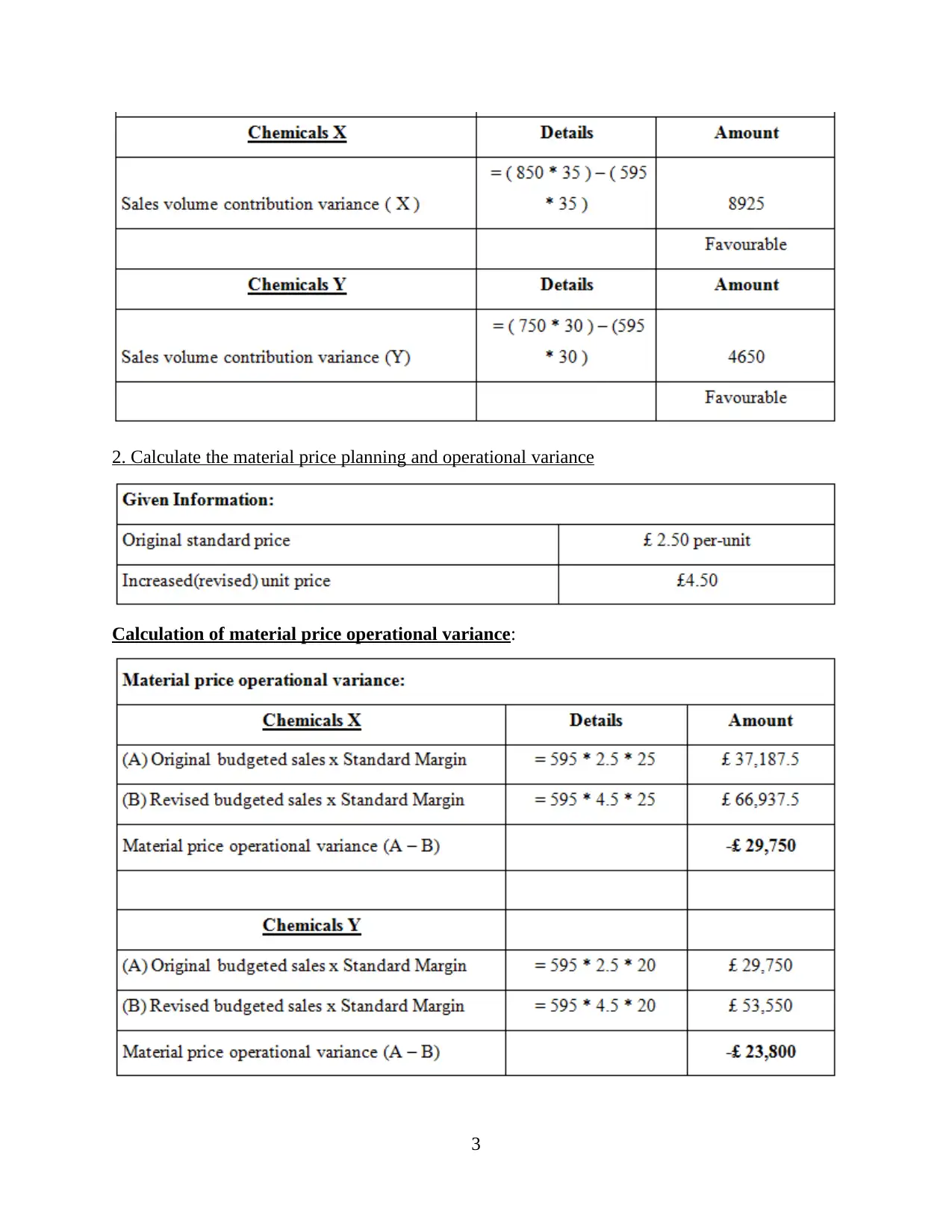

Sales Volume Contribution Variances:

It is the estimation of the gain or cost change arising from the difference between the actual

and the anticipated sales levels (Bromwich and Bhimani, 2017). When the total units sold are

different from the actual or budged units, this would explain the difference in selling volume.

Further calculation and formula of sales volume contribution mentioned below:

Formula:

Sales volume contribution variance = (Actual number of units sold × Budgeted price per unit)

– (budgeted number of units sold × Budgeted price per unit)

2

is in favourable condition that is £ 8500 and for Chemical Y is £ 5250 that is also in favourable

condition of the operations.

Sales Volume Contribution Variances:

It is the estimation of the gain or cost change arising from the difference between the actual

and the anticipated sales levels (Bromwich and Bhimani, 2017). When the total units sold are

different from the actual or budged units, this would explain the difference in selling volume.

Further calculation and formula of sales volume contribution mentioned below:

Formula:

Sales volume contribution variance = (Actual number of units sold × Budgeted price per unit)

– (budgeted number of units sold × Budgeted price per unit)

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Calculate the material price planning and operational variance

Calculation of material price operational variance:

3

Calculation of material price operational variance:

3

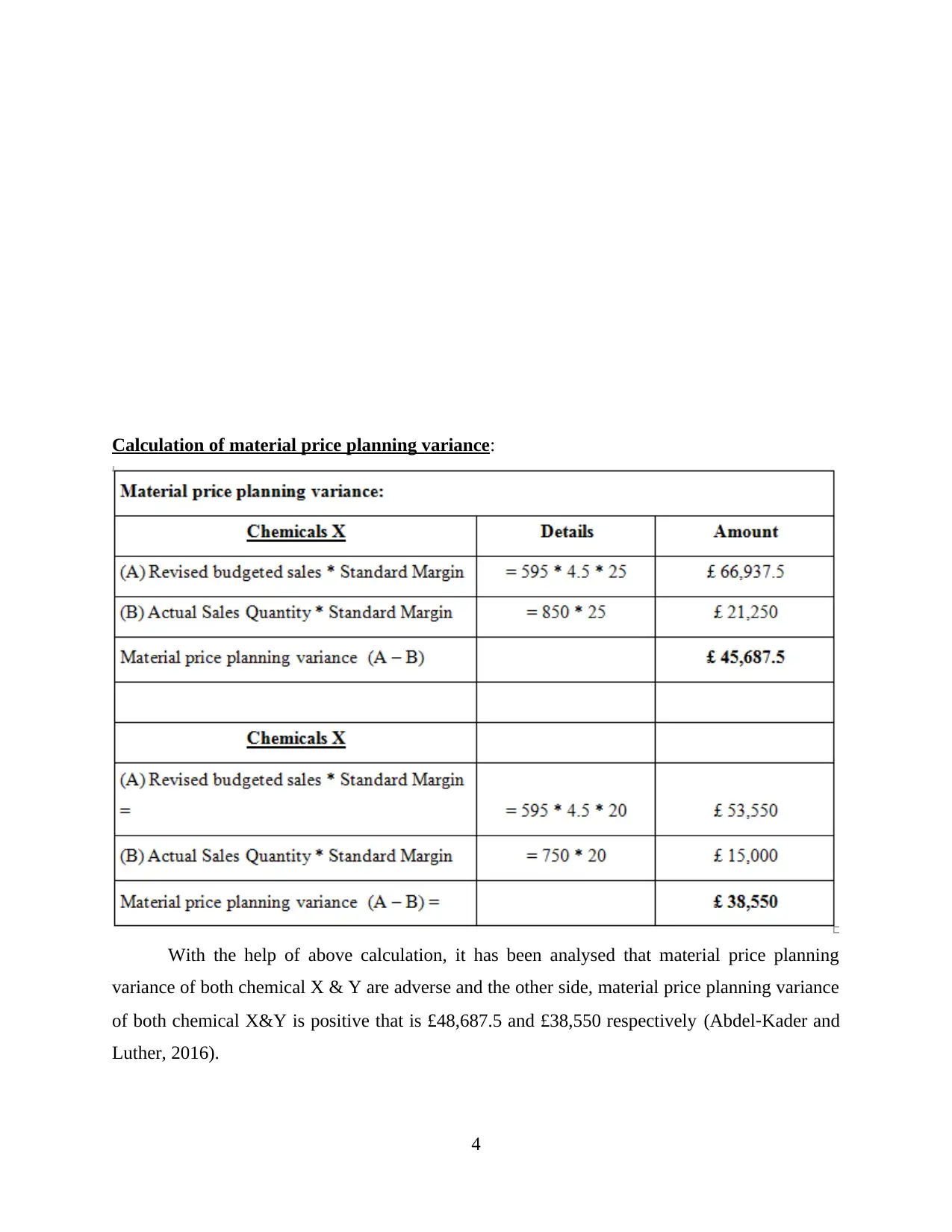

Calculation of material price planning variance:

With the help of above calculation, it has been analysed that material price planning

variance of both chemical X & Y are adverse and the other side, material price planning variance

of both chemical X&Y is positive that is £48,687.5 and £38,550 respectively (Abdel‐Kader and

Luther, 2016).

4

With the help of above calculation, it has been analysed that material price planning

variance of both chemical X & Y are adverse and the other side, material price planning variance

of both chemical X&Y is positive that is £48,687.5 and £38,550 respectively (Abdel‐Kader and

Luther, 2016).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Critically evaluate the merits or demerits of using variances

Variance analysis may be characterized as method of evaluating the differences among the

entities expectation and actual output, so that it can be evaluated whether or not the company

would meet its predictions (Cobb, Helliar and Innes, 2015). When the companies are unable to

forecast correctly otherwise the real expenses will be higher relative to the amounts budgeted.

Because of this a company could suffer losses. To ensure correct predictions are made, all

companies administrators are expected to evaluate the current market situation and instead make

potential decisions.

It is really essential for all organizations to ensure that they too are informed of both the

benefits and demerit points of it by using variances for different purpose of building decisions

for the coming future (Dolde and Tirtiroglu, 2017). Since different variances such as market

price and quantity allocation, commodity quality forecasting and operating differences will be

included in XLG to assess the efficiency of managers, so it would be important for the

organization to evaluate both the benefits and demerits of using them. Any of the important

aspects which can help explain both the advantages and disadvantages of using several variances

are addressed below. It also helps the managers to make effective strategic decisions which

maximise their operational performances and profitability.

Merits:

As variances are being used by organizations to determine the effectiveness of managers and

other uses, they may result in different benefits. These are all as follows:

Managing expenses: Evaluation of variances plays a key role in managing expenditures

since, if the outcomes of variances are unfavourable, administrators will take reasonable

measures to mitigate the adverse condition. Seek to explain the causes for adverse effects

to better function the management so they take care of associated behaviour so that they

might enhance the efficiency of the company. The actual selling is quite high in case of

XLG Business due to the increased demand that has been leads to adverse variance. The

administrators should have acquired more content than the regular one to cope with this

case, as it would have contributed to desirable variation.

Performance evaluation: Variance analysis is used to assess company's profitability by

assessing whether or not the real outcomes are consistent with the estimates budget

(Eldenburg, Krishnan and Krishnan, 2017). This also allows evaluating the success of

5

Variance analysis may be characterized as method of evaluating the differences among the

entities expectation and actual output, so that it can be evaluated whether or not the company

would meet its predictions (Cobb, Helliar and Innes, 2015). When the companies are unable to

forecast correctly otherwise the real expenses will be higher relative to the amounts budgeted.

Because of this a company could suffer losses. To ensure correct predictions are made, all

companies administrators are expected to evaluate the current market situation and instead make

potential decisions.

It is really essential for all organizations to ensure that they too are informed of both the

benefits and demerit points of it by using variances for different purpose of building decisions

for the coming future (Dolde and Tirtiroglu, 2017). Since different variances such as market

price and quantity allocation, commodity quality forecasting and operating differences will be

included in XLG to assess the efficiency of managers, so it would be important for the

organization to evaluate both the benefits and demerits of using them. Any of the important

aspects which can help explain both the advantages and disadvantages of using several variances

are addressed below. It also helps the managers to make effective strategic decisions which

maximise their operational performances and profitability.

Merits:

As variances are being used by organizations to determine the effectiveness of managers and

other uses, they may result in different benefits. These are all as follows:

Managing expenses: Evaluation of variances plays a key role in managing expenditures

since, if the outcomes of variances are unfavourable, administrators will take reasonable

measures to mitigate the adverse condition. Seek to explain the causes for adverse effects

to better function the management so they take care of associated behaviour so that they

might enhance the efficiency of the company. The actual selling is quite high in case of

XLG Business due to the increased demand that has been leads to adverse variance. The

administrators should have acquired more content than the regular one to cope with this

case, as it would have contributed to desirable variation.

Performance evaluation: Variance analysis is used to assess company's profitability by

assessing whether or not the real outcomes are consistent with the estimates budget

(Eldenburg, Krishnan and Krishnan, 2017). This also allows evaluating the success of

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

managing supervisors as it can represent positive results whenever the variances end

favourably. Unless the findings are negative then it would indicate that supervisors have

made no attempts to make reasonable choices or predictions.

Accountability measurement: A framework of transparency inside the company may be

developed using variance analysis or estimates. When an owner takes steps for

future possibility, the primary obligation should be to be responsible to do the same in

order to assess their results. If the findings are negative it'll also be very necessary to take

accountability. If the degree of transparency in XLG is poor therefore the bad

performance of company's managers can be shown.

Creating structure for roles and duties inside the company: Analysis of variance is

being used to establish a framework to correctly delegate all positions and obligations to

the team members. The top management will, with aid of it, assess the skill of managers

and then create structure that can best achieve the long-term targets and goals. Control

systems and performance inside the company may be strengthened and expanded with the

aid of it.

Modifying budgeted forecasts: Evaluating variances enables the revision of budget

projections (Gibson, 2018) (Harris, 2019). If in regular statistics the explanation for the

negative deviation is inaccurate calculation otherwise the results should be revised and

modified. When the executives are actively engaged in this phase so it would help to

effectively measure their effectiveness and enhance company's performance. This is one

of the key merits of variances to test executive performance in XLG.

Demerits:

Variance drawbacks for XLG Business are numerous. Below discussion provide better

understanding and these are as follow:

Time taking process: It is a time consuming procedure that takes too long to evaluate the

results of both the company and management. Regardless of this, the company's senior

managements are helpless to assess employee’s results on schedule and devise specific

strategies for market change. Aside from that, the measurement of variances moves the

emphasis from increased market efficiency to the evaluation of current practices of

company that may contribute to potential problems.

6

favourably. Unless the findings are negative then it would indicate that supervisors have

made no attempts to make reasonable choices or predictions.

Accountability measurement: A framework of transparency inside the company may be

developed using variance analysis or estimates. When an owner takes steps for

future possibility, the primary obligation should be to be responsible to do the same in

order to assess their results. If the findings are negative it'll also be very necessary to take

accountability. If the degree of transparency in XLG is poor therefore the bad

performance of company's managers can be shown.

Creating structure for roles and duties inside the company: Analysis of variance is

being used to establish a framework to correctly delegate all positions and obligations to

the team members. The top management will, with aid of it, assess the skill of managers

and then create structure that can best achieve the long-term targets and goals. Control

systems and performance inside the company may be strengthened and expanded with the

aid of it.

Modifying budgeted forecasts: Evaluating variances enables the revision of budget

projections (Gibson, 2018) (Harris, 2019). If in regular statistics the explanation for the

negative deviation is inaccurate calculation otherwise the results should be revised and

modified. When the executives are actively engaged in this phase so it would help to

effectively measure their effectiveness and enhance company's performance. This is one

of the key merits of variances to test executive performance in XLG.

Demerits:

Variance drawbacks for XLG Business are numerous. Below discussion provide better

understanding and these are as follow:

Time taking process: It is a time consuming procedure that takes too long to evaluate the

results of both the company and management. Regardless of this, the company's senior

managements are helpless to assess employee’s results on schedule and devise specific

strategies for market change. Aside from that, the measurement of variances moves the

emphasis from increased market efficiency to the evaluation of current practices of

company that may contribute to potential problems.

6

Postponed disciplinary actions: If the organization's top-level officials are unable to

evaluate if the employees or corporation performance well or not in a timely way that

would also impact the processes for taking some action. This will result in slower

remedial measures, because of high level managers; they will not be capable of taking the

appropriate decisions at right time (Ismail, Isa and Mia, 2018). As a result, the risk of

rising market success may be raised, causing detrimental impacts on meeting all the long

term targets and priorities.

Non-standardization production: Unless an organization exists throughout the service

industry, the implementation of variance analysis would be very challenging. Because

XLG is looking to just go online now it will be the part of retail sector and the operating

costs will rise which also cause problems for company. When monitoring internet

transactions, it would be very essential for business executives to ensure that they will

be able to accurately evaluate variances because it would show their abilities to better

carry out their tasks.

Psychological issues: Analysis of variance can lead to short term projects due to its

inherent propensity towards quantitative, short-term goals and outcomes. With the

exception of this, when there is adverse opinion about it so the inadequate activity among

the workers is encouraged. For example: it is trying to include budgetary slacks. This was

one of the key negative points of just using variance analysis to determine whether or not

the administrators are doing well.

Before making any decisions in context of the organizations, managers of XLG Company

need to evaluate the advantages or disadvantages of variances which can affect the decision

making process of managers (Malcom, 2019). After that managers should evaluate that, whether

they should implement variance analysis or not.

PART B

1. Assessing the report that FamaQ in house in UK keep importing from Brazil

XLG is a pharmaceutical corporation that works in the UK and a few other European areas.

The marketplace where it conducts operations has quite competition and one of key chemicals

that gives it competitive edge is the importing from famaQ, Brazil. The national shutdown

which took place in the 2nd quarter of March of 2020, and it has been imposed by UK state

7

evaluate if the employees or corporation performance well or not in a timely way that

would also impact the processes for taking some action. This will result in slower

remedial measures, because of high level managers; they will not be capable of taking the

appropriate decisions at right time (Ismail, Isa and Mia, 2018). As a result, the risk of

rising market success may be raised, causing detrimental impacts on meeting all the long

term targets and priorities.

Non-standardization production: Unless an organization exists throughout the service

industry, the implementation of variance analysis would be very challenging. Because

XLG is looking to just go online now it will be the part of retail sector and the operating

costs will rise which also cause problems for company. When monitoring internet

transactions, it would be very essential for business executives to ensure that they will

be able to accurately evaluate variances because it would show their abilities to better

carry out their tasks.

Psychological issues: Analysis of variance can lead to short term projects due to its

inherent propensity towards quantitative, short-term goals and outcomes. With the

exception of this, when there is adverse opinion about it so the inadequate activity among

the workers is encouraged. For example: it is trying to include budgetary slacks. This was

one of the key negative points of just using variance analysis to determine whether or not

the administrators are doing well.

Before making any decisions in context of the organizations, managers of XLG Company

need to evaluate the advantages or disadvantages of variances which can affect the decision

making process of managers (Malcom, 2019). After that managers should evaluate that, whether

they should implement variance analysis or not.

PART B

1. Assessing the report that FamaQ in house in UK keep importing from Brazil

XLG is a pharmaceutical corporation that works in the UK and a few other European areas.

The marketplace where it conducts operations has quite competition and one of key chemicals

that gives it competitive edge is the importing from famaQ, Brazil. The national shutdown

which took place in the 2nd quarter of March of 2020, and it has been imposed by UK state

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

authorities. Because of that, organizations are decided to move its revenues generating process

through digitally so it could address all of the lockout problems that are happening.

Being one of the key chemicals that the company uses to produce the end product, it is

supplied from Brazil so that it may respond to market issues in a systemic way (Matsuoka,

2020). That would be very necessary for organization to ensure it tackles all of the potential

consequences which might arise from this. Since of Lockdown, it would be unlikely for XLG to

import chemical famaQ from Brazil. However, if it is to be transported it will lead to different

threats. There are higher risks of transmitting the corona virus, high processing time, additional

cost etc.

After that, if company not imported then it will leads to reduce the overall profit

and comparative benefit which famaQ provided. Consequently, the demand for chemicals X and

Y has also been forecast to rise by 45 percent and will definitely grow as per market surveys.

Some of key options that company should work on manufacturing are the famaQ throughout the

UK so it can satisfy the demand of the consumer. When it is made in the UK, the distribution

time could be shortened by 15 days from the earlier date, which ensures that the company will

commence manufacturing soon.

Production cost per unit of famaQ throughout the UK would be 3 pounds that would be small

relative to manufactured cost of 3.7 pounds per product (Tekathen, 2019). This indicates

that company, instead of buying it from Brazil, would make famaQ in the UK, because it would

bring in multiple market benefits. Several of its main advantages include:

If famaQ is manufactured it would promote the market because the production costs are

quite low relative to the producer prices.

The shipping time should be shortened by 15 days, meaning that production will begin

faster and satisfy consumer demand earlier.

Unless the famaQ chemicals are produced instead of shipped from Brazil, the risk for

transmitting corona virus will be low.

It would be very challenging to import things at Lockdown and producing famaQ in the

UK is the best option for operations to be carried out regularly in future.

After considering all of the above factors, import costs and advantages of producing famaQ

in the UK, it was evaluated that XLG will produce the chemical in UK instead of importing

chemical from Brazil because it would be advantageous for business success.

8

through digitally so it could address all of the lockout problems that are happening.

Being one of the key chemicals that the company uses to produce the end product, it is

supplied from Brazil so that it may respond to market issues in a systemic way (Matsuoka,

2020). That would be very necessary for organization to ensure it tackles all of the potential

consequences which might arise from this. Since of Lockdown, it would be unlikely for XLG to

import chemical famaQ from Brazil. However, if it is to be transported it will lead to different

threats. There are higher risks of transmitting the corona virus, high processing time, additional

cost etc.

After that, if company not imported then it will leads to reduce the overall profit

and comparative benefit which famaQ provided. Consequently, the demand for chemicals X and

Y has also been forecast to rise by 45 percent and will definitely grow as per market surveys.

Some of key options that company should work on manufacturing are the famaQ throughout the

UK so it can satisfy the demand of the consumer. When it is made in the UK, the distribution

time could be shortened by 15 days from the earlier date, which ensures that the company will

commence manufacturing soon.

Production cost per unit of famaQ throughout the UK would be 3 pounds that would be small

relative to manufactured cost of 3.7 pounds per product (Tekathen, 2019). This indicates

that company, instead of buying it from Brazil, would make famaQ in the UK, because it would

bring in multiple market benefits. Several of its main advantages include:

If famaQ is manufactured it would promote the market because the production costs are

quite low relative to the producer prices.

The shipping time should be shortened by 15 days, meaning that production will begin

faster and satisfy consumer demand earlier.

Unless the famaQ chemicals are produced instead of shipped from Brazil, the risk for

transmitting corona virus will be low.

It would be very challenging to import things at Lockdown and producing famaQ in the

UK is the best option for operations to be carried out regularly in future.

After considering all of the above factors, import costs and advantages of producing famaQ

in the UK, it was evaluated that XLG will produce the chemical in UK instead of importing

chemical from Brazil because it would be advantageous for business success.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

On the basis of above discussion it has been concluded that management accounting is very

essential for the organizations as well as for managers to manage all the operational activities.

With the help of it, management is able to make strategic decisions to maximise it operational

performance or enhance the business growth. It is a method that used by internal as well as

external stakeholders to determine the current status of company in terms or profitability or

overall operational performance. It should be very necessary for both companies to be ensured

that they were using appropriate strategies when attempting to make tactical plans for business.

This is the measurement of variance which is essential to take certain decisions. The overall

success of both company and management may be estimated with the help of it. This would be

very essential to be conscious of both its benefits and demerits whilst using it, so that successful

strategies can be made for the future and use it to maximise the growth of business and

profitability. Management will select the most suitable options which help the organization to

maximise profit margin through reducing manufacturing cost as well as also ensure that spread

of COVID-19 should be low otherwise it will be dangerous for everyone and it expand the

lockdown period which will leads to suffer economy most.

9

On the basis of above discussion it has been concluded that management accounting is very

essential for the organizations as well as for managers to manage all the operational activities.

With the help of it, management is able to make strategic decisions to maximise it operational

performance or enhance the business growth. It is a method that used by internal as well as

external stakeholders to determine the current status of company in terms or profitability or

overall operational performance. It should be very necessary for both companies to be ensured

that they were using appropriate strategies when attempting to make tactical plans for business.

This is the measurement of variance which is essential to take certain decisions. The overall

success of both company and management may be estimated with the help of it. This would be

very essential to be conscious of both its benefits and demerits whilst using it, so that successful

strategies can be made for the future and use it to maximise the growth of business and

profitability. Management will select the most suitable options which help the organization to

maximise profit margin through reducing manufacturing cost as well as also ensure that spread

of COVID-19 should be low otherwise it will be dangerous for everyone and it expand the

lockdown period which will leads to suffer economy most.

9

REFERENCES

Books & Journals

Abdel‐Kader, M. and Luther, R., 2016. Management accounting practices in the British food and

drinks industry. British food journal.

Adler, R. W., 2018. Strategic performance management: Accounting for organizational control.

Taylor & Francis.

Bastable, C. W. and Bao, D. H., 2018. The fiction of sales-mix and sales-quantity

variances. Accounting Horizons, 2(2), p.10.

Bromwich, M. and Bhimani, A., 2017. Management accounting: Pathways to progress. Cima

publishing.

Cobb, I., Helliar, C. and Innes, J., 2015. Management accounting change in a bank. Management

accounting research, 6(2), pp.155-175.

Dolde, W. and Tirtiroglu, D., 2017. Temporal and spatial information diffusion in real estate

price changes and variances. Real Estate Economics. 25(4). pp.539-565.

Eldenburg, L. G., Krishnan, H. A. and Krishnan, R., 2017. Management accounting and control

in the hospital industry: A review. Journal of Governmental & Nonprofit Accounting.

6(1). pp.52-91.

Gibson, B., 2018. Determining Meaningful Sales Relational (Mix) Variances. Accounting and

Business Research. 21(81). pp.35-40.

Harris, L., 2019. Estimation of stock price variances and serial covariances from discrete

observations. Journal of Financial and Quantitative Analysis, pp.291-306.

Ismail, K., Isa, C. R. and Mia, L., 2018. Market competition, lean manufacturing practices and

the role of management accounting systems (MAS) information. Jurnal Pengurusan

(UKM Journal of Management). 52.

Malcom, R. E., 2019. The Effect of Product Aggregation in Determining Sales

Variances. Accounting Review, pp.162-169.

Matsuoka, K., 2020. Exploring the interface between management accounting and marketing: a

literature review of customer accounting. Journal of Management Control. pp.1-52.

Tekathen, M., 2019. Unpacking the Fluidity of Management Accounting Concepts: An

Ethnographic Social Site Analysis of Enterprise Risk Management. European Accounting

Review. 28(5). pp.977-1010.

10

Books & Journals

Abdel‐Kader, M. and Luther, R., 2016. Management accounting practices in the British food and

drinks industry. British food journal.

Adler, R. W., 2018. Strategic performance management: Accounting for organizational control.

Taylor & Francis.

Bastable, C. W. and Bao, D. H., 2018. The fiction of sales-mix and sales-quantity

variances. Accounting Horizons, 2(2), p.10.

Bromwich, M. and Bhimani, A., 2017. Management accounting: Pathways to progress. Cima

publishing.

Cobb, I., Helliar, C. and Innes, J., 2015. Management accounting change in a bank. Management

accounting research, 6(2), pp.155-175.

Dolde, W. and Tirtiroglu, D., 2017. Temporal and spatial information diffusion in real estate

price changes and variances. Real Estate Economics. 25(4). pp.539-565.

Eldenburg, L. G., Krishnan, H. A. and Krishnan, R., 2017. Management accounting and control

in the hospital industry: A review. Journal of Governmental & Nonprofit Accounting.

6(1). pp.52-91.

Gibson, B., 2018. Determining Meaningful Sales Relational (Mix) Variances. Accounting and

Business Research. 21(81). pp.35-40.

Harris, L., 2019. Estimation of stock price variances and serial covariances from discrete

observations. Journal of Financial and Quantitative Analysis, pp.291-306.

Ismail, K., Isa, C. R. and Mia, L., 2018. Market competition, lean manufacturing practices and

the role of management accounting systems (MAS) information. Jurnal Pengurusan

(UKM Journal of Management). 52.

Malcom, R. E., 2019. The Effect of Product Aggregation in Determining Sales

Variances. Accounting Review, pp.162-169.

Matsuoka, K., 2020. Exploring the interface between management accounting and marketing: a

literature review of customer accounting. Journal of Management Control. pp.1-52.

Tekathen, M., 2019. Unpacking the Fluidity of Management Accounting Concepts: An

Ethnographic Social Site Analysis of Enterprise Risk Management. European Accounting

Review. 28(5). pp.977-1010.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.