Management Accounting Report: XLG Company's Performance Evaluation

VerifiedAdded on 2023/01/07

|11

|3281

|91

Report

AI Summary

This report provides a comprehensive analysis of XLG, a company manufacturing household cleaners in the UK, focusing on management accounting principles. Part A delves into variance analysis, calculating sales price variance, sales volume variance, and material cost variances for Chemical X and Y, providing detailed formulas and calculations. It then evaluates the advantages and disadvantages of using variances to assess managerial performance, emphasizing the importance of variance analysis in budgeting, control, and liability determination, while acknowledging its limitations regarding non-financial factors and potential manipulation. Part B explores a make-or-buy decision, considering the increased cost of an imported component (Fama Q) from Brazil. It examines the options of manufacturing Fama Q in the UK versus continuing to import, considering patent regulations, cost implications, and potential demand increases, providing a comparative analysis to aid in decision-making. The report highlights the importance of accurate financial data for effective variance analysis and managerial evaluation.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Financial statements of company have to be properly reported and more changes can be

taken. Management accounting (MA) performs a crucial role throughout this area because this is

related to consistently reviewing, assessing non - financial and financial information so decision-

making can be processed by management through collected evidence (Chorley, 2019). The report

is prepared on a company that is XLG, which manufactures various types of household cleaners

and sells throughout the UK.

Part A and B are included in the study, which comprises of distinct material, based on

business information received. In Part A, data has been included regarding the calculation of

various differences alongside benefits and drawbacks. While second Part is being analysed about

whether business must implement make item at residence or manufacture from another country.

TASK

PART A

(i) Deals price and capacity contribution difference.

Sales Price Variance: This variability could be described as the variation among real market

value selling and total budget cost revenue. According to the given data, this variability was

calculated in a really way shows below:

Method: (Actual Price-Standard price) x Actual number of units

Chemical X:

Given data:

Actual price= 45 Pounds

Standard price= 35 Pounds

Actual number of sales unit= 850 units

Sales price variance: (45-35) *850

= 8500 (F)

Chemical Y:

Given data:

Actual price= 37 Pounds

Standard price= 30 Pounds

Financial statements of company have to be properly reported and more changes can be

taken. Management accounting (MA) performs a crucial role throughout this area because this is

related to consistently reviewing, assessing non - financial and financial information so decision-

making can be processed by management through collected evidence (Chorley, 2019). The report

is prepared on a company that is XLG, which manufactures various types of household cleaners

and sells throughout the UK.

Part A and B are included in the study, which comprises of distinct material, based on

business information received. In Part A, data has been included regarding the calculation of

various differences alongside benefits and drawbacks. While second Part is being analysed about

whether business must implement make item at residence or manufacture from another country.

TASK

PART A

(i) Deals price and capacity contribution difference.

Sales Price Variance: This variability could be described as the variation among real market

value selling and total budget cost revenue. According to the given data, this variability was

calculated in a really way shows below:

Method: (Actual Price-Standard price) x Actual number of units

Chemical X:

Given data:

Actual price= 45 Pounds

Standard price= 35 Pounds

Actual number of sales unit= 850 units

Sales price variance: (45-35) *850

= 8500 (F)

Chemical Y:

Given data:

Actual price= 37 Pounds

Standard price= 30 Pounds

Actual number of sales unit= 750 units

Sales price variance: (37-30) * 750

= 5250 (F)

Variability in expenditure sales volume: This variability could be devoted to the analysis

of revenue transformation due to the variation among budgeted and actual selling quantities

(Zhang, 2020).

Formula: (Current units priced for each unit at a premium price) – (budged unit priced at a

budget price per unit).

Chemical X:

Specified data:

Real elements sold= 850 Units

Planned value for all unit= 35 Pounds

Planned unit wholesaled= 595 Units

Planned worth for all unit= 35 Pounds

Sales volume effect modification: (850*35) – (595*35)

= 8925 (F)

Chemical Y:

Assumed data:

Definite units traded= 750 Units

Accounted price for all unit = 30 Pounds

Planned unit sold= 595 Units

Planned price for each unit= 30 Pounds

Sales capacity influence variance: (750*30) – (595*30)

= 4650 (F)

The variability in material cost organising as well as the difference throughout the

organisational price of the material.

Variability in material price organising: this is indeed a type of variability calculated to

determine the difference between all the actual and planned rates of the material. It is determined

using the equation described below which is as follows:

Sales price variance: (37-30) * 750

= 5250 (F)

Variability in expenditure sales volume: This variability could be devoted to the analysis

of revenue transformation due to the variation among budgeted and actual selling quantities

(Zhang, 2020).

Formula: (Current units priced for each unit at a premium price) – (budged unit priced at a

budget price per unit).

Chemical X:

Specified data:

Real elements sold= 850 Units

Planned value for all unit= 35 Pounds

Planned unit wholesaled= 595 Units

Planned worth for all unit= 35 Pounds

Sales volume effect modification: (850*35) – (595*35)

= 8925 (F)

Chemical Y:

Assumed data:

Definite units traded= 750 Units

Accounted price for all unit = 30 Pounds

Planned unit sold= 595 Units

Planned price for each unit= 30 Pounds

Sales capacity influence variance: (750*30) – (595*30)

= 4650 (F)

The variability in material cost organising as well as the difference throughout the

organisational price of the material.

Variability in material price organising: this is indeed a type of variability calculated to

determine the difference between all the actual and planned rates of the material. It is determined

using the equation described below which is as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Equation: [(Revised Budget Sales x Standard Margin)- (Actual Standard Margin X Sales

Quantity)]

Chemical X:

Given numbers-

Reviewed budgeted deals= 595 units @ 4.5

Normal Margin= 25

Definite Sales Amount= 850 Units

Average Margin= 25

Substantial price preparation variance: [(595*4.5*25) -(850*25)]

45687.5

Chemical Y:

Specified records-

Revised budgeted sales= 595 units @ 4.5

Average Margin= 20

Definite Sales Extent= 750 Units

Standard Margin= 20

Physical price preparation variance: [(595*4.5*20) - (750*20)]

38550

Variation in the operation of commodity costs: This form of variation is measured to

assess disparity in material prices, labour, etc. This is assessed by multiplying the actual story

and the amended budgets with the actual results (Salles, Rocha and Gonçalves, 2020). In respect

of the financial information provided, this variance was computed in a really way as to be as

described in the following manner:

Chemical X:

Method: [(Original budgeted sales x Standard Margin) – (Revised budgeted sales x Standard

Margin)]

Particular data:

Unique accounted sales= 595 Units @ 2.5

Usual Margin= 25

Revised planned sales= 595 Units @ 4.5

Quantity)]

Chemical X:

Given numbers-

Reviewed budgeted deals= 595 units @ 4.5

Normal Margin= 25

Definite Sales Amount= 850 Units

Average Margin= 25

Substantial price preparation variance: [(595*4.5*25) -(850*25)]

45687.5

Chemical Y:

Specified records-

Revised budgeted sales= 595 units @ 4.5

Average Margin= 20

Definite Sales Extent= 750 Units

Standard Margin= 20

Physical price preparation variance: [(595*4.5*20) - (750*20)]

38550

Variation in the operation of commodity costs: This form of variation is measured to

assess disparity in material prices, labour, etc. This is assessed by multiplying the actual story

and the amended budgets with the actual results (Salles, Rocha and Gonçalves, 2020). In respect

of the financial information provided, this variance was computed in a really way as to be as

described in the following manner:

Chemical X:

Method: [(Original budgeted sales x Standard Margin) – (Revised budgeted sales x Standard

Margin)]

Particular data:

Unique accounted sales= 595 Units @ 2.5

Usual Margin= 25

Revised planned sales= 595 Units @ 4.5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ordinary Margin= 25

Material worth planning difference= [(595*2.5*25) -(595*4.5*25)]

= -29750

Chemical Y:

Given information:

New budgeted trades= 595 Units @ 2.5

Standard Margin= 20

Revised accounted sales= 595 Units @ 4.5

Standard margin= 20

Material price planning variance= [(595*2.5*20) -(595*4.5*20)]

= -23800

Despite the transition of procedures, the benefits and disadvantages of using variances when

determining the success of managers are objectively assessed.

Variance descriptive analysis is also an analysis of variances in actual practice toward

anticipated or planned actions in financial forecasting or financial accounting (Telesca, Helbig

and Kanevski, 2019). It mainly deals by how the difference between actual and expected

operations indicates the business performance is being influenced. In simple term, the

evaluation of variance is really the formal assessment of the difference between actual and

predicted behaviour. Using this review maintains control over the firm. For instance, because the

revenue estimate is $10,000 and the true income is $8,000, then the variability analysis results in

a disparity of $2,000. The variance analysis plays an important role in assessing managers'

efficiency because this it is continuous for everyone if it is supervisor or worker. Using this

method, a company's manager can try comparing real statistics to approximate actual

performance. When the result shows a bad effect, it will be viewed as an adverse consequence

because if outcome shows a favourable result, it will be interpreted as a good result. In the event

that management' success produces negative effects, it can be determined that executives are

unable to meet set targets. As regards evaluating supervisor's output, it is critical that certain

performance should be measured at the close of the budget year. Its efficiency cannot be

adequately measured within a calendar year (Choi, Sun and Chung, 2019).

Material worth planning difference= [(595*2.5*25) -(595*4.5*25)]

= -29750

Chemical Y:

Given information:

New budgeted trades= 595 Units @ 2.5

Standard Margin= 20

Revised accounted sales= 595 Units @ 4.5

Standard margin= 20

Material price planning variance= [(595*2.5*20) -(595*4.5*20)]

= -23800

Despite the transition of procedures, the benefits and disadvantages of using variances when

determining the success of managers are objectively assessed.

Variance descriptive analysis is also an analysis of variances in actual practice toward

anticipated or planned actions in financial forecasting or financial accounting (Telesca, Helbig

and Kanevski, 2019). It mainly deals by how the difference between actual and expected

operations indicates the business performance is being influenced. In simple term, the

evaluation of variance is really the formal assessment of the difference between actual and

predicted behaviour. Using this review maintains control over the firm. For instance, because the

revenue estimate is $10,000 and the true income is $8,000, then the variability analysis results in

a disparity of $2,000. The variance analysis plays an important role in assessing managers'

efficiency because this it is continuous for everyone if it is supervisor or worker. Using this

method, a company's manager can try comparing real statistics to approximate actual

performance. When the result shows a bad effect, it will be viewed as an adverse consequence

because if outcome shows a favourable result, it will be interpreted as a good result. In the event

that management' success produces negative effects, it can be determined that executives are

unable to meet set targets. As regards evaluating supervisor's output, it is critical that certain

performance should be measured at the close of the budget year. Its efficiency cannot be

adequately measured within a calendar year (Choi, Sun and Chung, 2019).

Failure to apply this approach performance measurement will make it impossible for

organizations to assess real success levels. In the context of above business, in order to figure out

the importance of actual results, they should implement variance analysis process. Beyond

measuring managers' results, this is often helpful in evaluating staff results and behaviours as

well. This is so since a company's management can measure the gap between real costs and

financial projections on the grounds of that as well. Through this method, as well as personal

performance levels of each staff member are also measured. Here are some of the main

advantages and demerits of using this method to assess the success of management as described

in the following way:

Advantages

Analysis of variances facilitates successful budgeting as management wants to see fewer

deviations from planned expenditures. Generally, having a smaller deviation helps

managers make detailed, forward-looking economic choices. In simple term, these

managers can use their assistance to concentrate on those operations for which the

variability is advantageous. Over this, a company has become feasible to take into

account positive actions rather than disadvantageous operations.

Analysing variances acts as a means of control as on simple necessities makes the

company appreciate the issue and lets management identify new ways to avoid a lot of

variance (Vaske, 2019). It outcomes as a stronger success of a firm because supervisors

are becoming able to determine about which unfavourable variance of operations is

appropriate about which that's not sustainable. As a result, a top business helps prepare

efficient and effective methods which can lead to success from every circumstance.

Analysis of variances motivates liability determination and activates organizational

monitoring systems when required. For instance, if variability in labour productivity is

deemed unfavourable or output over variation in raw material costs is unfavourable, the

manager should strengthen control of those divisions to optimize productivity. In other

words, it provides a summary of what sort of measures need to be introduced to boost the

company profit by attaining the desired results of different operations.

Disadvantages

Evaluation of deviation as an event relies on annual statements that are released even

later after the reporting period; there may be a time gap that will have an effect on the

organizations to assess real success levels. In the context of above business, in order to figure out

the importance of actual results, they should implement variance analysis process. Beyond

measuring managers' results, this is often helpful in evaluating staff results and behaviours as

well. This is so since a company's management can measure the gap between real costs and

financial projections on the grounds of that as well. Through this method, as well as personal

performance levels of each staff member are also measured. Here are some of the main

advantages and demerits of using this method to assess the success of management as described

in the following way:

Advantages

Analysis of variances facilitates successful budgeting as management wants to see fewer

deviations from planned expenditures. Generally, having a smaller deviation helps

managers make detailed, forward-looking economic choices. In simple term, these

managers can use their assistance to concentrate on those operations for which the

variability is advantageous. Over this, a company has become feasible to take into

account positive actions rather than disadvantageous operations.

Analysing variances acts as a means of control as on simple necessities makes the

company appreciate the issue and lets management identify new ways to avoid a lot of

variance (Vaske, 2019). It outcomes as a stronger success of a firm because supervisors

are becoming able to determine about which unfavourable variance of operations is

appropriate about which that's not sustainable. As a result, a top business helps prepare

efficient and effective methods which can lead to success from every circumstance.

Analysis of variances motivates liability determination and activates organizational

monitoring systems when required. For instance, if variability in labour productivity is

deemed unfavourable or output over variation in raw material costs is unfavourable, the

manager should strengthen control of those divisions to optimize productivity. In other

words, it provides a summary of what sort of measures need to be introduced to boost the

company profit by attaining the desired results of different operations.

Disadvantages

Evaluation of deviation as an event relies on annual statements that are released even

later after the reporting period; there may be a time gap that will have an effect on the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

corrective action getting the chance to some degree (Lei, Liu that Zhang, 2019). Not all

sources of difference should also be found in accounting reports, which makes it difficult

to rely on deviations.

A further disadvantage of the variance approach is it cannot be extended to non-financial

factors. It can only be applicable in the context of study of financial information like

evaluation of normal and real data relating to prices, profits etc.

Another issue regarding the technique of variance analysis would be that supervisors can

modify the information shown in this strategy. Unless the financial results reported was

inaccurate, so it will be impossible for businesses to figure out the accurate variation

between the various categories between practices and operations. For this problem, the

real performance appraisal of management will be inaccurate and companies may not

have been able to make accurate policies to achieve higher productivity.

Thus these a few other key advantages and disadvantages about using the aforementioned

described variance analytical method. This really is important for companies to evaluate the

quality of their management and workers just how well they implement that as well. The

effectiveness and consistency of the boost business under that same technique extremely refers to

the financial information supplied for comparing. When the statistics published is accurate the

differences would also be accurate (Ferdous, Adams and Boyce, 2019). Moreover, this section

does not apply to management teams as they have the obligation to deceive real statistics and

since from which their success could not be assessed effectively.

Part B:

As described according to the above portion, if XLG purchase the fama Q item from Brazil

so its charge of obtaining this product increases. Prior to actually lockdown, the cost of the

item for every unit was about 2.50 pounds but increased after lockdown cost increased as it

became 3.70 pounds for XLG per component. Over this corporation mark-up cost for each

component of fama Q increases to 4.50 pounds. This business already has a monopoly upon that

product to ensure that they alone are entitled to market this throughout the UK. In this crucial

situation, above-mentioned organization has two options to manufacture this commodity at

residence or to manufacture the item from Brazil they used to do previously. There have been

some problems with both options now client has to pick only one that is acceptable and less

expensive. Assessment of both options is conducted in the following part in just such a way:

sources of difference should also be found in accounting reports, which makes it difficult

to rely on deviations.

A further disadvantage of the variance approach is it cannot be extended to non-financial

factors. It can only be applicable in the context of study of financial information like

evaluation of normal and real data relating to prices, profits etc.

Another issue regarding the technique of variance analysis would be that supervisors can

modify the information shown in this strategy. Unless the financial results reported was

inaccurate, so it will be impossible for businesses to figure out the accurate variation

between the various categories between practices and operations. For this problem, the

real performance appraisal of management will be inaccurate and companies may not

have been able to make accurate policies to achieve higher productivity.

Thus these a few other key advantages and disadvantages about using the aforementioned

described variance analytical method. This really is important for companies to evaluate the

quality of their management and workers just how well they implement that as well. The

effectiveness and consistency of the boost business under that same technique extremely refers to

the financial information supplied for comparing. When the statistics published is accurate the

differences would also be accurate (Ferdous, Adams and Boyce, 2019). Moreover, this section

does not apply to management teams as they have the obligation to deceive real statistics and

since from which their success could not be assessed effectively.

Part B:

As described according to the above portion, if XLG purchase the fama Q item from Brazil

so its charge of obtaining this product increases. Prior to actually lockdown, the cost of the

item for every unit was about 2.50 pounds but increased after lockdown cost increased as it

became 3.70 pounds for XLG per component. Over this corporation mark-up cost for each

component of fama Q increases to 4.50 pounds. This business already has a monopoly upon that

product to ensure that they alone are entitled to market this throughout the UK. In this crucial

situation, above-mentioned organization has two options to manufacture this commodity at

residence or to manufacture the item from Brazil they used to do previously. There have been

some problems with both options now client has to pick only one that is acceptable and less

expensive. Assessment of both options is conducted in the following part in just such a way:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

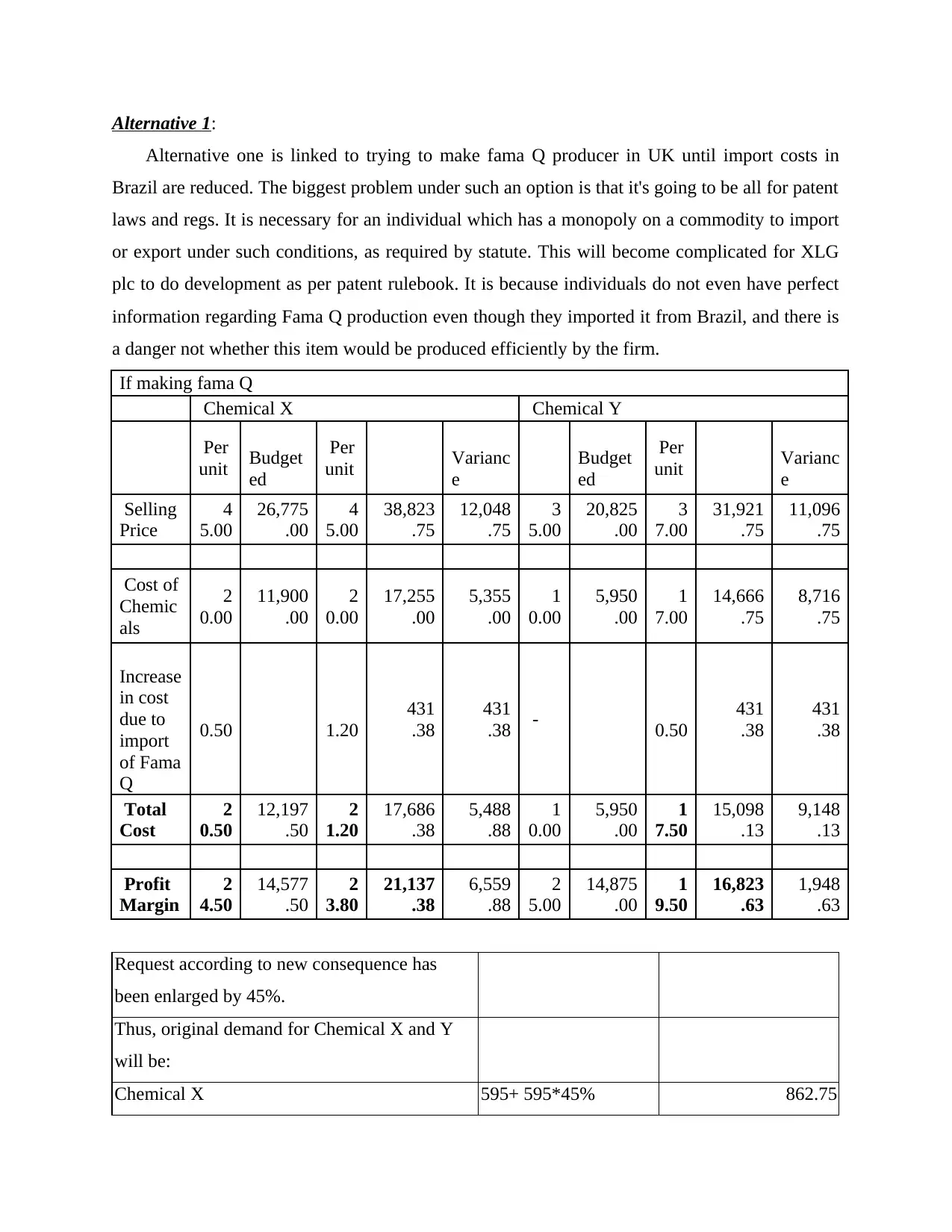

Alternative 1:

Alternative one is linked to trying to make fama Q producer in UK until import costs in

Brazil are reduced. The biggest problem under such an option is that it's going to be all for patent

laws and regs. It is necessary for an individual which has a monopoly on a commodity to import

or export under such conditions, as required by statute. This will become complicated for XLG

plc to do development as per patent rulebook. It is because individuals do not even have perfect

information regarding Fama Q production even though they imported it from Brazil, and there is

a danger not whether this item would be produced efficiently by the firm.

If making fama Q

Chemical X Chemical Y

Per

unit Budget

ed

Per

unit Varianc

e

Budget

ed

Per

unit Varianc

e

Selling

Price

4

5.00

26,775

.00

4

5.00

38,823

.75

12,048

.75

3

5.00

20,825

.00

3

7.00

31,921

.75

11,096

.75

Cost of

Chemic

als

2

0.00

11,900

.00

2

0.00

17,255

.00

5,355

.00

1

0.00

5,950

.00

1

7.00

14,666

.75

8,716

.75

Increase

in cost

due to

import

of Fama

Q

0.50 1.20

431

.38

431

.38 - 0.50

431

.38

431

.38

Total

Cost

2

0.50

12,197

.50

2

1.20

17,686

.38

5,488

.88

1

0.00

5,950

.00

1

7.50

15,098

.13

9,148

.13

Profit

Margin

2

4.50

14,577

.50

2

3.80

21,137

.38

6,559

.88

2

5.00

14,875

.00

1

9.50

16,823

.63

1,948

.63

Request according to new consequence has

been enlarged by 45%.

Thus, original demand for Chemical X and Y

will be:

Chemical X 595+ 595*45% 862.75

Alternative one is linked to trying to make fama Q producer in UK until import costs in

Brazil are reduced. The biggest problem under such an option is that it's going to be all for patent

laws and regs. It is necessary for an individual which has a monopoly on a commodity to import

or export under such conditions, as required by statute. This will become complicated for XLG

plc to do development as per patent rulebook. It is because individuals do not even have perfect

information regarding Fama Q production even though they imported it from Brazil, and there is

a danger not whether this item would be produced efficiently by the firm.

If making fama Q

Chemical X Chemical Y

Per

unit Budget

ed

Per

unit Varianc

e

Budget

ed

Per

unit Varianc

e

Selling

Price

4

5.00

26,775

.00

4

5.00

38,823

.75

12,048

.75

3

5.00

20,825

.00

3

7.00

31,921

.75

11,096

.75

Cost of

Chemic

als

2

0.00

11,900

.00

2

0.00

17,255

.00

5,355

.00

1

0.00

5,950

.00

1

7.00

14,666

.75

8,716

.75

Increase

in cost

due to

import

of Fama

Q

0.50 1.20

431

.38

431

.38 - 0.50

431

.38

431

.38

Total

Cost

2

0.50

12,197

.50

2

1.20

17,686

.38

5,488

.88

1

0.00

5,950

.00

1

7.50

15,098

.13

9,148

.13

Profit

Margin

2

4.50

14,577

.50

2

3.80

21,137

.38

6,559

.88

2

5.00

14,875

.00

1

9.50

16,823

.63

1,948

.63

Request according to new consequence has

been enlarged by 45%.

Thus, original demand for Chemical X and Y

will be:

Chemical X 595+ 595*45% 862.75

Chemical Y 595+ 595 * 45% 862.75

Interpretation: The above equation shows that if they make it in the United Kingdom, demand

for fama Q can grow effectively. In comparison, the expense of all goods like chemical X and Y

is also smaller compared with profit margin. Therefore, this would be possible in terms of the

financial context for the aforementioned business to manufacture this drug in the UK. However,

suggesting earlier without allowing assessment of the second option would be incorrect. The

findings can be distinguished in comparative study (Ji, Zhou and Liang, 2019).

Alternative 2:

This option has to do with sourcing the commodity through Brazil and company had been doing

previously according to the details given. Nonetheless, after lockout, the cost of this import was

increased and before it, such imports was profitable for the business because they were having

goods at lower expense. To test this option a comprehensive cost study that resulted in the course

of purchasing this drug was effectively carried out. This is essential here again to understand that

even under this every company complies with patent laws and regulations. Thus, it is important

to determine only certain financial viewpoint of this solution which is performed in such a way:

If

Imports

:

Chemical X Chemical Y

Budget

ed

Per

unit Actual Varianc

e

Budget

ed

Per

unit Varian

ce

Selling

Price 35.0

0

20,825

.00

4

5.00

38,250

.00

17,425

.00 35.0

0

20,825

.00

3

7.00

27,750

.00

6,925.

00

Cost of

Chemic

als

10.0

0

5,950

.00

2

0.00

17,000

.00

11,050

.00 10.0

0

5,950

.00

1

7.00

12,750

.00

6,800.

00

Increase

in cost

due to

import

of Fama

Q

- 1.20

1,020

.00

1,020

.00 - 1.20

900

.00

900.

00

Total

Cost 10.0

0

5,950

.00

2

1.20

18,020

.00

12,070

.00 10.0

0

5,950

.00

1

8.20

13,650

.00

7,700.

00

Interpretation: The above equation shows that if they make it in the United Kingdom, demand

for fama Q can grow effectively. In comparison, the expense of all goods like chemical X and Y

is also smaller compared with profit margin. Therefore, this would be possible in terms of the

financial context for the aforementioned business to manufacture this drug in the UK. However,

suggesting earlier without allowing assessment of the second option would be incorrect. The

findings can be distinguished in comparative study (Ji, Zhou and Liang, 2019).

Alternative 2:

This option has to do with sourcing the commodity through Brazil and company had been doing

previously according to the details given. Nonetheless, after lockout, the cost of this import was

increased and before it, such imports was profitable for the business because they were having

goods at lower expense. To test this option a comprehensive cost study that resulted in the course

of purchasing this drug was effectively carried out. This is essential here again to understand that

even under this every company complies with patent laws and regulations. Thus, it is important

to determine only certain financial viewpoint of this solution which is performed in such a way:

If

Imports

:

Chemical X Chemical Y

Budget

ed

Per

unit Actual Varianc

e

Budget

ed

Per

unit Varian

ce

Selling

Price 35.0

0

20,825

.00

4

5.00

38,250

.00

17,425

.00 35.0

0

20,825

.00

3

7.00

27,750

.00

6,925.

00

Cost of

Chemic

als

10.0

0

5,950

.00

2

0.00

17,000

.00

11,050

.00 10.0

0

5,950

.00

1

7.00

12,750

.00

6,800.

00

Increase

in cost

due to

import

of Fama

Q

- 1.20

1,020

.00

1,020

.00 - 1.20

900

.00

900.

00

Total

Cost 10.0

0

5,950

.00

2

1.20

18,020

.00

12,070

.00 10.0

0

5,950

.00

1

8.20

13,650

.00

7,700.

00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit

Margin 25.0

0

14,875

.00

2

3.80

20,230

.00

5,355

.00 25.0

0

14,875

.00

1

8.80

14,100

.00

-

775.00

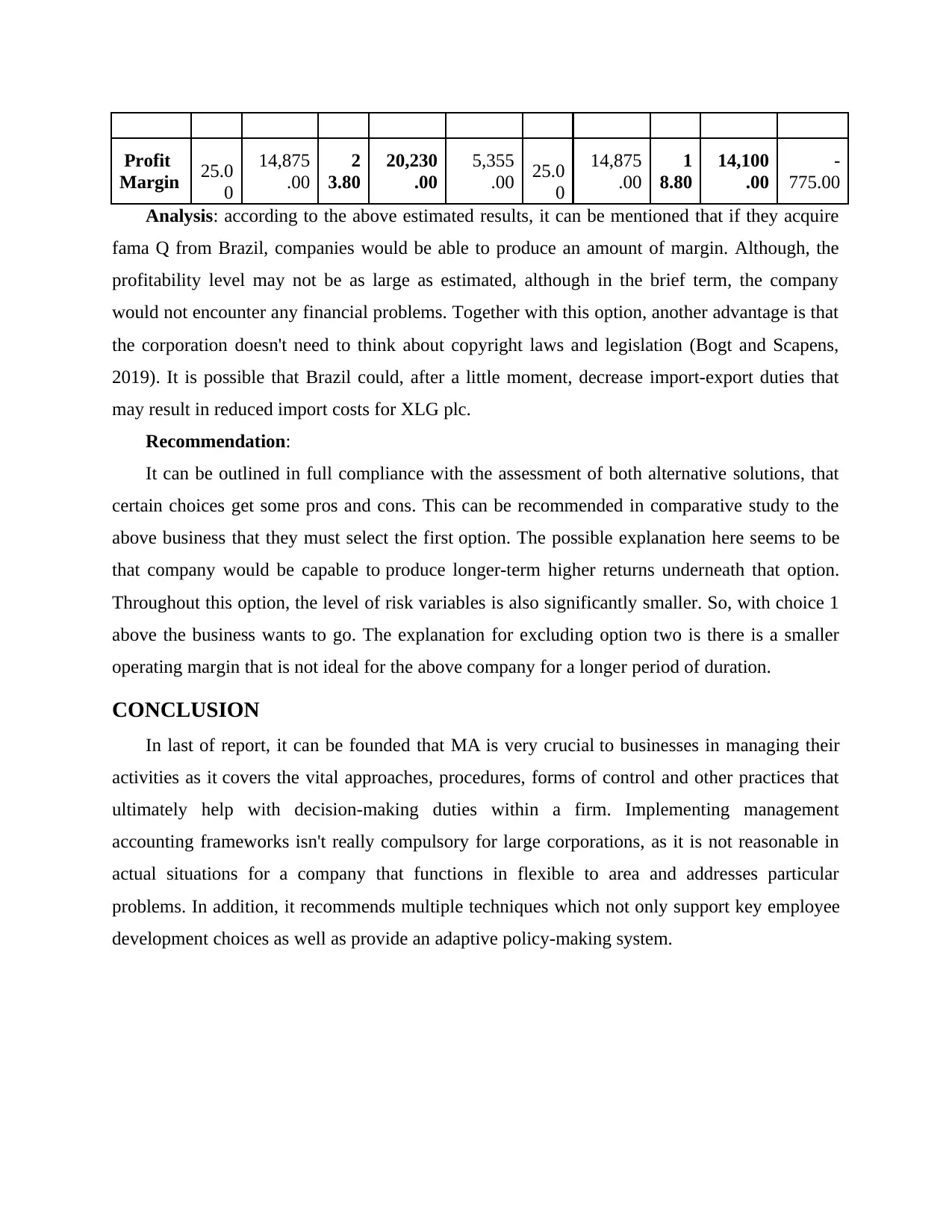

Analysis: according to the above estimated results, it can be mentioned that if they acquire

fama Q from Brazil, companies would be able to produce an amount of margin. Although, the

profitability level may not be as large as estimated, although in the brief term, the company

would not encounter any financial problems. Together with this option, another advantage is that

the corporation doesn't need to think about copyright laws and legislation (Bogt and Scapens,

2019). It is possible that Brazil could, after a little moment, decrease import-export duties that

may result in reduced import costs for XLG plc.

Recommendation:

It can be outlined in full compliance with the assessment of both alternative solutions, that

certain choices get some pros and cons. This can be recommended in comparative study to the

above business that they must select the first option. The possible explanation here seems to be

that company would be capable to produce longer-term higher returns underneath that option.

Throughout this option, the level of risk variables is also significantly smaller. So, with choice 1

above the business wants to go. The explanation for excluding option two is there is a smaller

operating margin that is not ideal for the above company for a longer period of duration.

CONCLUSION

In last of report, it can be founded that MA is very crucial to businesses in managing their

activities as it covers the vital approaches, procedures, forms of control and other practices that

ultimately help with decision-making duties within a firm. Implementing management

accounting frameworks isn't really compulsory for large corporations, as it is not reasonable in

actual situations for a company that functions in flexible to area and addresses particular

problems. In addition, it recommends multiple techniques which not only support key employee

development choices as well as provide an adaptive policy-making system.

Margin 25.0

0

14,875

.00

2

3.80

20,230

.00

5,355

.00 25.0

0

14,875

.00

1

8.80

14,100

.00

-

775.00

Analysis: according to the above estimated results, it can be mentioned that if they acquire

fama Q from Brazil, companies would be able to produce an amount of margin. Although, the

profitability level may not be as large as estimated, although in the brief term, the company

would not encounter any financial problems. Together with this option, another advantage is that

the corporation doesn't need to think about copyright laws and legislation (Bogt and Scapens,

2019). It is possible that Brazil could, after a little moment, decrease import-export duties that

may result in reduced import costs for XLG plc.

Recommendation:

It can be outlined in full compliance with the assessment of both alternative solutions, that

certain choices get some pros and cons. This can be recommended in comparative study to the

above business that they must select the first option. The possible explanation here seems to be

that company would be capable to produce longer-term higher returns underneath that option.

Throughout this option, the level of risk variables is also significantly smaller. So, with choice 1

above the business wants to go. The explanation for excluding option two is there is a smaller

operating margin that is not ideal for the above company for a longer period of duration.

CONCLUSION

In last of report, it can be founded that MA is very crucial to businesses in managing their

activities as it covers the vital approaches, procedures, forms of control and other practices that

ultimately help with decision-making duties within a firm. Implementing management

accounting frameworks isn't really compulsory for large corporations, as it is not reasonable in

actual situations for a company that functions in flexible to area and addresses particular

problems. In addition, it recommends multiple techniques which not only support key employee

development choices as well as provide an adaptive policy-making system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Choi, T.M., Wen, X., Sun, X. and Chung, S.H., 2019. The mean-variance approach for global

supply chain risk analysis with air logistics in the blockchain technology

era. Transportation Research Part E: Logistics and Transportation Review, 127, pp.178-

191.

Chorley, R.J. ed., 2019. Spatial analysis in geomorphology. Routledge.

Ferdous, M.I., Adams, C.A. and Boyce, G., 2019. Institutional drivers of environmental

management accounting adoption in public sector water organisations. Accounting,

Auditing & Accountability Journal.

Ji, K., Wang, Z., Zhou, Y. and Liang, Y., 2019. Improved zeroth-order variance reduced

algorithms and analysis for nonconvex optimization. arXiv preprint arXiv:1910.12166.

Lei, H., Liu, J. and Zhang, L., 2019, December. Tourism Image Endorsement Based on

Experiment and Variance Analysis. In IOP Conference Series: Earth and Environmental

Science (Vol. 371, No. 5, p. 052001). IOP Publishing.

Salles, T., Rocha, L. and Gonçalves, M., 2020. A bias-variance analysis of state-of-the-art

random forest text classifiers. Advances in Data Analysis and Classification, pp.1-27.

Telesca, L., Guignard, F., Helbig, N. and Kanevski, M., 2019. Wavelet Scale Variance Analysis

of Wind Extremes in Mountainous Terrains. Energies, 12(16), p.3048.

ter Bogt, H.J. and Scapens, R.W., 2019. Institutions, situated rationality and agency in

management accounting. Accounting, Auditing & Accountability Journal.

Vaske, J.J., 2019. Survey research and analysis. Sagamore-Venture. 1807 North Federal Drive,

Urbana, IL 61801.

Zhang, Z.C., 2020. Variance analysis of linear canonical Wigner distribution. Optik, p.164633.

Books and Journals

Choi, T.M., Wen, X., Sun, X. and Chung, S.H., 2019. The mean-variance approach for global

supply chain risk analysis with air logistics in the blockchain technology

era. Transportation Research Part E: Logistics and Transportation Review, 127, pp.178-

191.

Chorley, R.J. ed., 2019. Spatial analysis in geomorphology. Routledge.

Ferdous, M.I., Adams, C.A. and Boyce, G., 2019. Institutional drivers of environmental

management accounting adoption in public sector water organisations. Accounting,

Auditing & Accountability Journal.

Ji, K., Wang, Z., Zhou, Y. and Liang, Y., 2019. Improved zeroth-order variance reduced

algorithms and analysis for nonconvex optimization. arXiv preprint arXiv:1910.12166.

Lei, H., Liu, J. and Zhang, L., 2019, December. Tourism Image Endorsement Based on

Experiment and Variance Analysis. In IOP Conference Series: Earth and Environmental

Science (Vol. 371, No. 5, p. 052001). IOP Publishing.

Salles, T., Rocha, L. and Gonçalves, M., 2020. A bias-variance analysis of state-of-the-art

random forest text classifiers. Advances in Data Analysis and Classification, pp.1-27.

Telesca, L., Guignard, F., Helbig, N. and Kanevski, M., 2019. Wavelet Scale Variance Analysis

of Wind Extremes in Mountainous Terrains. Energies, 12(16), p.3048.

ter Bogt, H.J. and Scapens, R.W., 2019. Institutions, situated rationality and agency in

management accounting. Accounting, Auditing & Accountability Journal.

Vaske, J.J., 2019. Survey research and analysis. Sagamore-Venture. 1807 North Federal Drive,

Urbana, IL 61801.

Zhang, Z.C., 2020. Variance analysis of linear canonical Wigner distribution. Optik, p.164633.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.