XLG Company: Financial Variance Analysis and Decision Report

VerifiedAdded on 2023/01/07

|12

|3086

|40

Report

AI Summary

This report analyzes the financial performance of XLG Company, a drug distribution firm, focusing on variance analysis. It calculates sales price and volume contribution variances for chemicals X and Y, and material price variances. The report critically evaluates the merits and demerits of using variance analysis to assess managerial performance, highlighting its role in tracking performance, facilitating responsibility, and identifying deviations from standards. The report also includes an assessment of the decision to manufacture famaQ in-house in the UK versus importing it from Brazil, considering the risks and benefits of each option during a shutdown. The analysis provides insights into how variance analysis can be used to make more informed financial decisions and improve overall company performance.

Businesses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

PART A...........................................................................................................................................1

1. Calculate the price and sales volume contribution variance....................................................1

2. Calculation of material price planning variance and material price operational variance.......3

3. Critically evaluate merits and demerits of variance to evaluate manager’s performances......4

PART B...........................................................................................................................................7

1. Report assessing the decision to make famaQ in house in the UK to keep importing it from

Brazil............................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

MAIN BODY..................................................................................................................................1

PART A...........................................................................................................................................1

1. Calculate the price and sales volume contribution variance....................................................1

2. Calculation of material price planning variance and material price operational variance.......3

3. Critically evaluate merits and demerits of variance to evaluate manager’s performances......4

PART B...........................................................................................................................................7

1. Report assessing the decision to make famaQ in house in the UK to keep importing it from

Brazil............................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

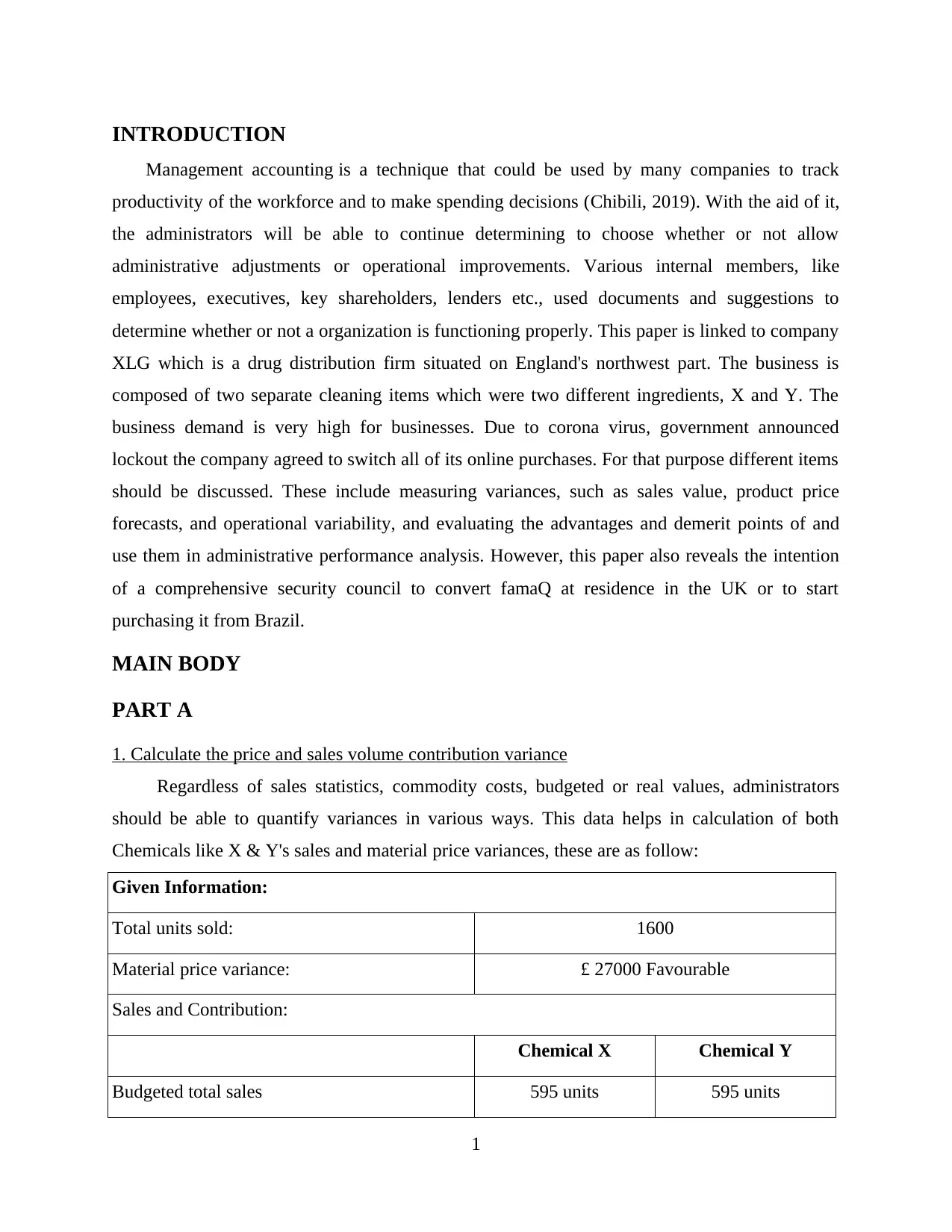

INTRODUCTION

Management accounting is a technique that could be used by many companies to track

productivity of the workforce and to make spending decisions (Chibili, 2019). With the aid of it,

the administrators will be able to continue determining to choose whether or not allow

administrative adjustments or operational improvements. Various internal members, like

employees, executives, key shareholders, lenders etc., used documents and suggestions to

determine whether or not a organization is functioning properly. This paper is linked to company

XLG which is a drug distribution firm situated on England's northwest part. The business is

composed of two separate cleaning items which were two different ingredients, X and Y. The

business demand is very high for businesses. Due to corona virus, government announced

lockout the company agreed to switch all of its online purchases. For that purpose different items

should be discussed. These include measuring variances, such as sales value, product price

forecasts, and operational variability, and evaluating the advantages and demerit points of and

use them in administrative performance analysis. However, this paper also reveals the intention

of a comprehensive security council to convert famaQ at residence in the UK or to start

purchasing it from Brazil.

MAIN BODY

PART A

1. Calculate the price and sales volume contribution variance

Regardless of sales statistics, commodity costs, budgeted or real values, administrators

should be able to quantify variances in various ways. This data helps in calculation of both

Chemicals like X & Y's sales and material price variances, these are as follow:

Given Information:

Total units sold: 1600

Material price variance: £ 27000 Favourable

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

1

Management accounting is a technique that could be used by many companies to track

productivity of the workforce and to make spending decisions (Chibili, 2019). With the aid of it,

the administrators will be able to continue determining to choose whether or not allow

administrative adjustments or operational improvements. Various internal members, like

employees, executives, key shareholders, lenders etc., used documents and suggestions to

determine whether or not a organization is functioning properly. This paper is linked to company

XLG which is a drug distribution firm situated on England's northwest part. The business is

composed of two separate cleaning items which were two different ingredients, X and Y. The

business demand is very high for businesses. Due to corona virus, government announced

lockout the company agreed to switch all of its online purchases. For that purpose different items

should be discussed. These include measuring variances, such as sales value, product price

forecasts, and operational variability, and evaluating the advantages and demerit points of and

use them in administrative performance analysis. However, this paper also reveals the intention

of a comprehensive security council to convert famaQ at residence in the UK or to start

purchasing it from Brazil.

MAIN BODY

PART A

1. Calculate the price and sales volume contribution variance

Regardless of sales statistics, commodity costs, budgeted or real values, administrators

should be able to quantify variances in various ways. This data helps in calculation of both

Chemicals like X & Y's sales and material price variances, these are as follow:

Given Information:

Total units sold: 1600

Material price variance: £ 27000 Favourable

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

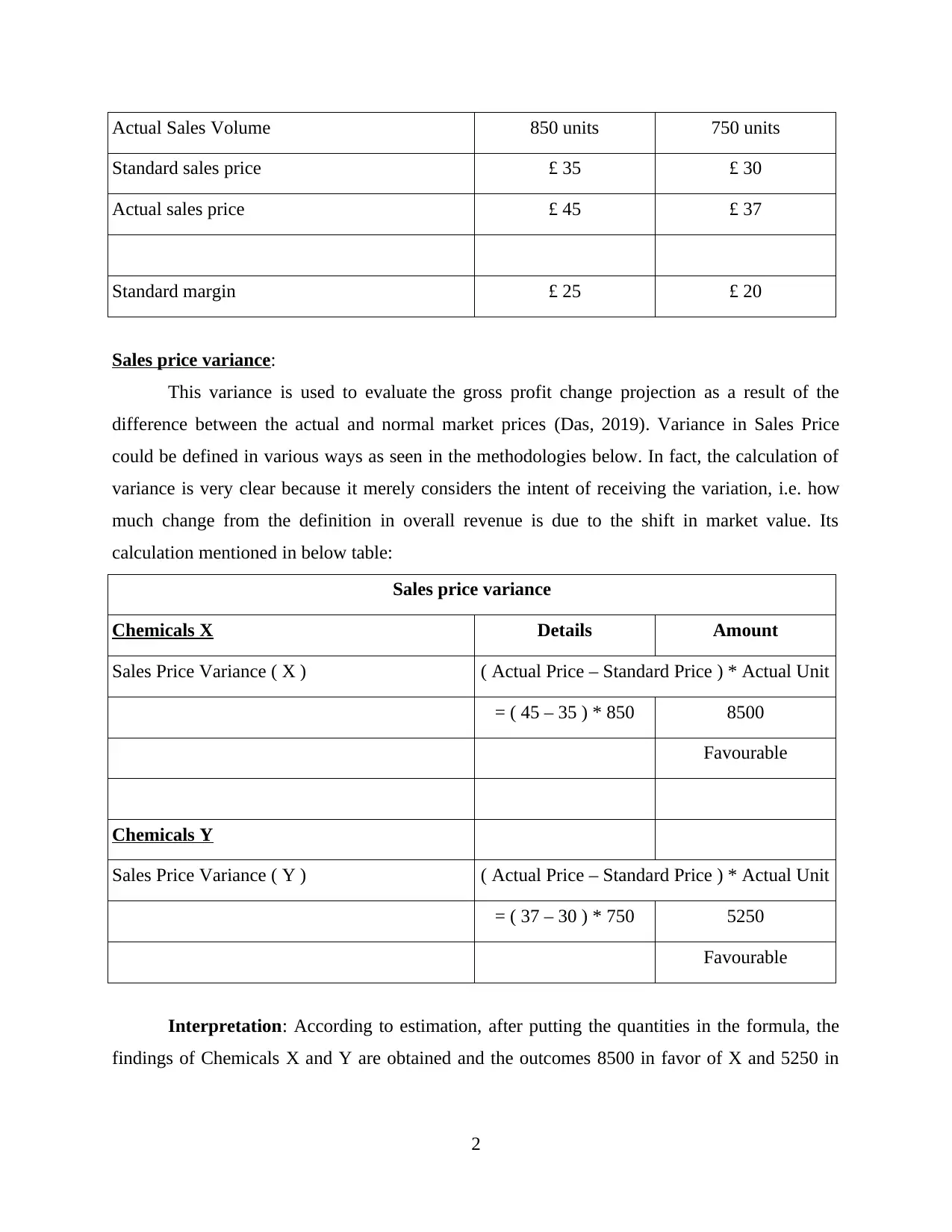

Actual Sales Volume 850 units 750 units

Standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

Standard margin £ 25 £ 20

Sales price variance:

This variance is used to evaluate the gross profit change projection as a result of the

difference between the actual and normal market prices (Das, 2019). Variance in Sales Price

could be defined in various ways as seen in the methodologies below. In fact, the calculation of

variance is very clear because it merely considers the intent of receiving the variation, i.e. how

much change from the definition in overall revenue is due to the shift in market value. Its

calculation mentioned in below table:

Sales price variance

Chemicals X Details Amount

Sales Price Variance ( X ) ( Actual Price – Standard Price ) * Actual Unit

= ( 45 – 35 ) * 850 8500

Favourable

Chemicals Y

Sales Price Variance ( Y ) ( Actual Price – Standard Price ) * Actual Unit

= ( 37 – 30 ) * 750 5250

Favourable

Interpretation: According to estimation, after putting the quantities in the formula, the

findings of Chemicals X and Y are obtained and the outcomes 8500 in favor of X and 5250 in

2

Standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

Standard margin £ 25 £ 20

Sales price variance:

This variance is used to evaluate the gross profit change projection as a result of the

difference between the actual and normal market prices (Das, 2019). Variance in Sales Price

could be defined in various ways as seen in the methodologies below. In fact, the calculation of

variance is very clear because it merely considers the intent of receiving the variation, i.e. how

much change from the definition in overall revenue is due to the shift in market value. Its

calculation mentioned in below table:

Sales price variance

Chemicals X Details Amount

Sales Price Variance ( X ) ( Actual Price – Standard Price ) * Actual Unit

= ( 45 – 35 ) * 850 8500

Favourable

Chemicals Y

Sales Price Variance ( Y ) ( Actual Price – Standard Price ) * Actual Unit

= ( 37 – 30 ) * 750 5250

Favourable

Interpretation: According to estimation, after putting the quantities in the formula, the

findings of Chemicals X and Y are obtained and the outcomes 8500 in favor of X and 5250 in

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

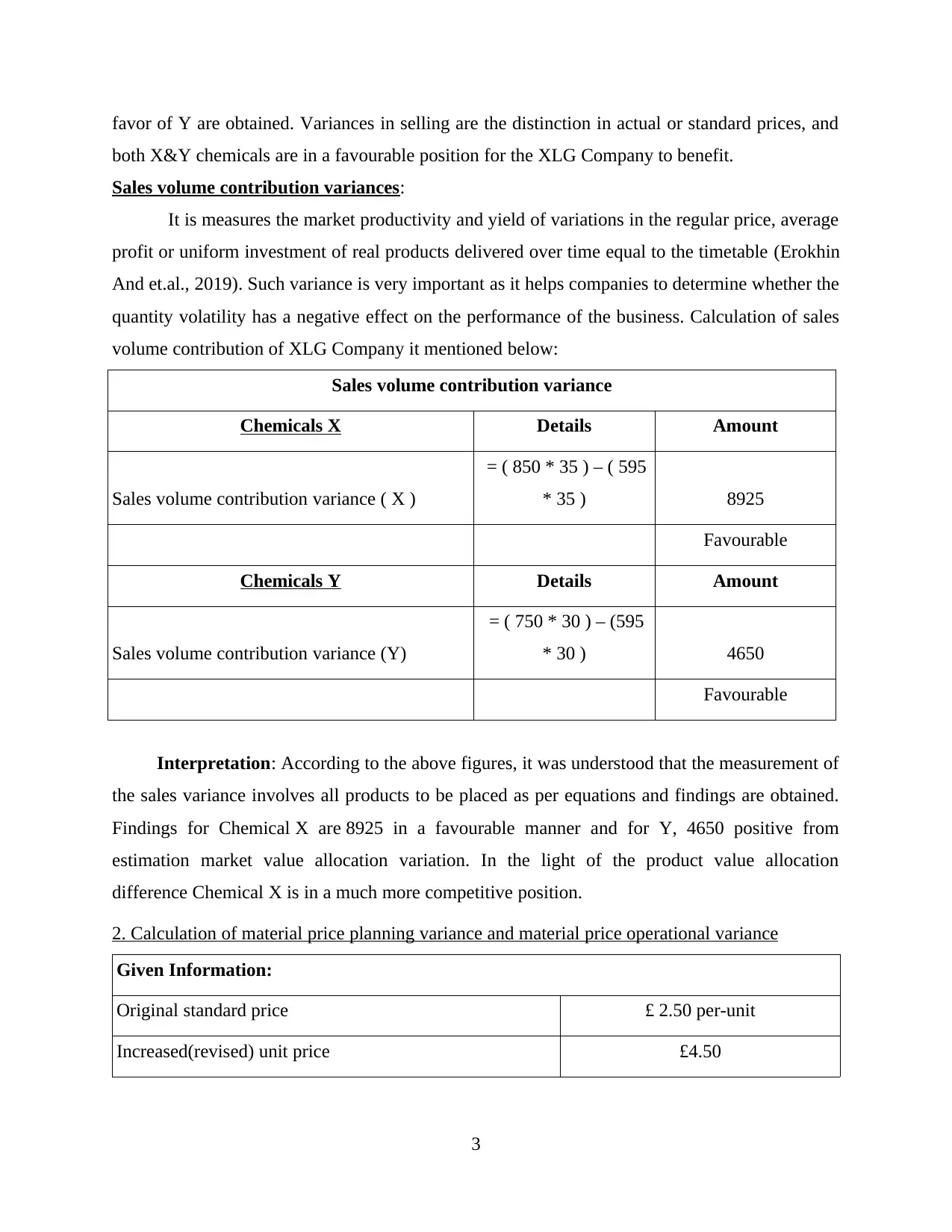

favor of Y are obtained. Variances in selling are the distinction in actual or standard prices, and

both X&Y chemicals are in a favourable position for the XLG Company to benefit.

Sales volume contribution variances:

It is measures the market productivity and yield of variations in the regular price, average

profit or uniform investment of real products delivered over time equal to the timetable (Erokhin

And et.al., 2019). Such variance is very important as it helps companies to determine whether the

quantity volatility has a negative effect on the performance of the business. Calculation of sales

volume contribution of XLG Company it mentioned below:

Sales volume contribution variance

Chemicals X Details Amount

Sales volume contribution variance ( X )

= ( 850 * 35 ) – ( 595

* 35 ) 8925

Favourable

Chemicals Y Details Amount

Sales volume contribution variance (Y)

= ( 750 * 30 ) – (595

* 30 ) 4650

Favourable

Interpretation: According to the above figures, it was understood that the measurement of

the sales variance involves all products to be placed as per equations and findings are obtained.

Findings for Chemical X are 8925 in a favourable manner and for Y, 4650 positive from

estimation market value allocation variation. In the light of the product value allocation

difference Chemical X is in a much more competitive position.

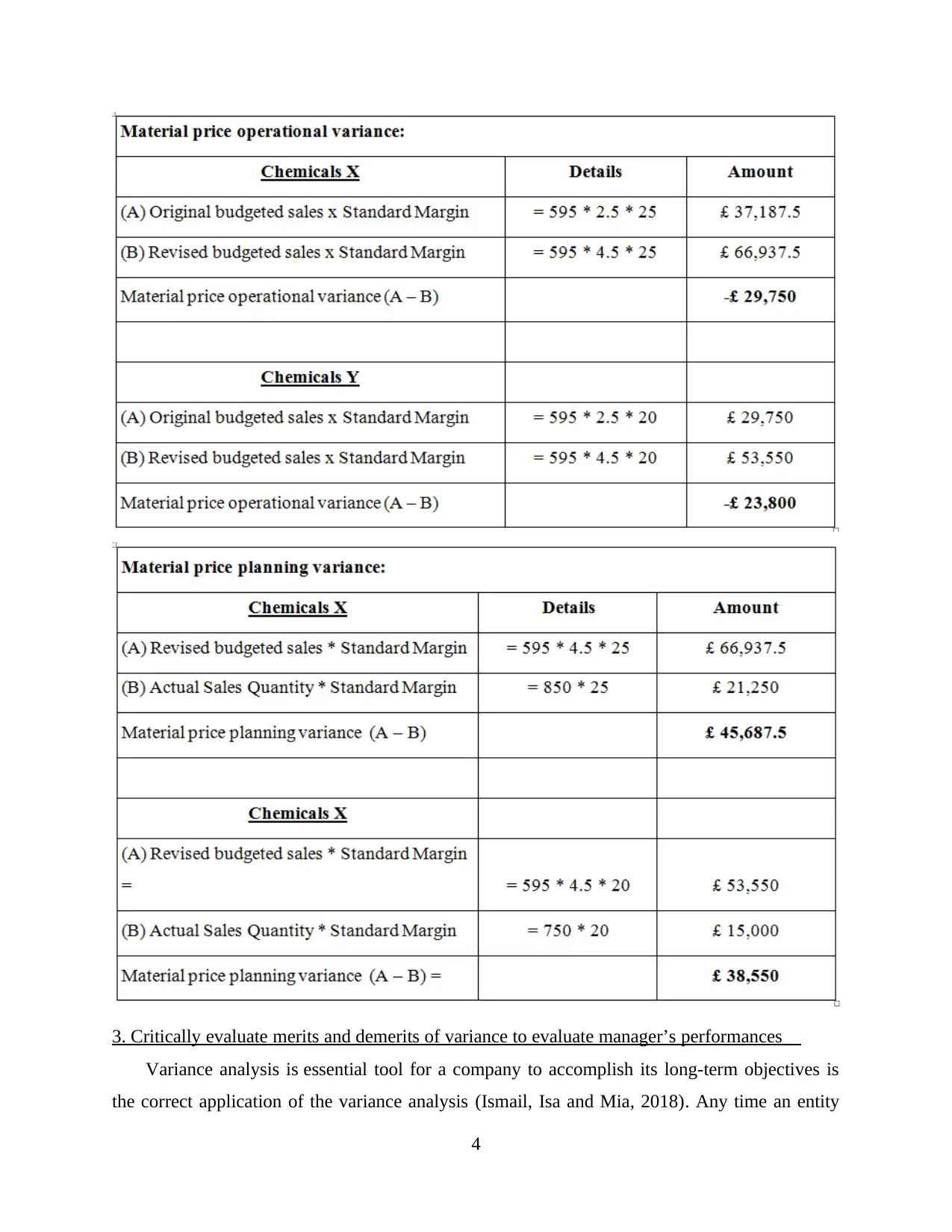

2. Calculation of material price planning variance and material price operational variance

Given Information:

Original standard price £ 2.50 per-unit

Increased(revised) unit price £4.50

3

both X&Y chemicals are in a favourable position for the XLG Company to benefit.

Sales volume contribution variances:

It is measures the market productivity and yield of variations in the regular price, average

profit or uniform investment of real products delivered over time equal to the timetable (Erokhin

And et.al., 2019). Such variance is very important as it helps companies to determine whether the

quantity volatility has a negative effect on the performance of the business. Calculation of sales

volume contribution of XLG Company it mentioned below:

Sales volume contribution variance

Chemicals X Details Amount

Sales volume contribution variance ( X )

= ( 850 * 35 ) – ( 595

* 35 ) 8925

Favourable

Chemicals Y Details Amount

Sales volume contribution variance (Y)

= ( 750 * 30 ) – (595

* 30 ) 4650

Favourable

Interpretation: According to the above figures, it was understood that the measurement of

the sales variance involves all products to be placed as per equations and findings are obtained.

Findings for Chemical X are 8925 in a favourable manner and for Y, 4650 positive from

estimation market value allocation variation. In the light of the product value allocation

difference Chemical X is in a much more competitive position.

2. Calculation of material price planning variance and material price operational variance

Given Information:

Original standard price £ 2.50 per-unit

Increased(revised) unit price £4.50

3

3. Critically evaluate merits and demerits of variance to evaluate manager’s performances

Variance analysis is essential tool for a company to accomplish its long-term objectives is

the correct application of the variance analysis (Ismail, Isa and Mia, 2018). Any time an entity

4

Variance analysis is essential tool for a company to accomplish its long-term objectives is

the correct application of the variance analysis (Ismail, Isa and Mia, 2018). Any time an entity

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

detects a difference in an item such as material, labour, etc. It needs awareness of the

considerable impact of disclosing the quarterly statements, as well as relating to such a variance,

which may influence managers' activities against such operational objectives attained.

Examination of variances is a mathematical analysis of the difference between current and

predicted behaviour. Using this analysis is to establish control of corporations. It could allow

managers to earn a bunch of improvements and main decisions which could help the company

more competitive in the long term. Understanding that evaluating variances does not really lead

to market impact issues is important. This also offers qualified accountants and administrators

with an example of how they will behave in case of potential knowledge issues.

A variance reflects both the difference between the standard ability and the true capability

restrictions for the operating activities. Fluctuations can have to do with variations in demand or

price differences. Unless the actual cost increases the normal expenditure or the expected cost,

then the variance is an adverse discrepancy. If another actual cost is greater than standard cost or

the projected value, if the amount is positive, the distinction is a beneficial one. While positive

differences are favourable variance and unfavourable variance will be the negative disparity.

Variance interlinks with many other variations, as it’s important in strategic planning whether

favourable or unfavourable (Pavlatos and Kostakis, 2018). Variance analysis has many merits as

well as demerits factors that influence the company's ultimate result. In effort to expand

their efficiency as well as usefulness, management teams need to analyze their pros and cons that

help actually spend their business. Within this sense, a thorough debate on the key benefits and

demerits of using variations in the calculation of organizational performance continues:

Merits:

Variance analysis enables an efficient reward operation, as managers have to see

narrower variances from the projected cost. Generally having a lower variance helps

management to make more effective financial decisions which are detailed or forward

planning.

This acts as a tracking tool to detect variances. Reviewing significant variation on

important goods encourages XLG Company's managers to understand the causes, which

lets managers check for new ways to avoid too much volatility.

Variation analysis facilitates responsibility transition and triggers oversight mechanisms

on units in which they are required. If labour efficiency variation is treated as undesirable

5

considerable impact of disclosing the quarterly statements, as well as relating to such a variance,

which may influence managers' activities against such operational objectives attained.

Examination of variances is a mathematical analysis of the difference between current and

predicted behaviour. Using this analysis is to establish control of corporations. It could allow

managers to earn a bunch of improvements and main decisions which could help the company

more competitive in the long term. Understanding that evaluating variances does not really lead

to market impact issues is important. This also offers qualified accountants and administrators

with an example of how they will behave in case of potential knowledge issues.

A variance reflects both the difference between the standard ability and the true capability

restrictions for the operating activities. Fluctuations can have to do with variations in demand or

price differences. Unless the actual cost increases the normal expenditure or the expected cost,

then the variance is an adverse discrepancy. If another actual cost is greater than standard cost or

the projected value, if the amount is positive, the distinction is a beneficial one. While positive

differences are favourable variance and unfavourable variance will be the negative disparity.

Variance interlinks with many other variations, as it’s important in strategic planning whether

favourable or unfavourable (Pavlatos and Kostakis, 2018). Variance analysis has many merits as

well as demerits factors that influence the company's ultimate result. In effort to expand

their efficiency as well as usefulness, management teams need to analyze their pros and cons that

help actually spend their business. Within this sense, a thorough debate on the key benefits and

demerits of using variations in the calculation of organizational performance continues:

Merits:

Variance analysis enables an efficient reward operation, as managers have to see

narrower variances from the projected cost. Generally having a lower variance helps

management to make more effective financial decisions which are detailed or forward

planning.

This acts as a tracking tool to detect variances. Reviewing significant variation on

important goods encourages XLG Company's managers to understand the causes, which

lets managers check for new ways to avoid too much volatility.

Variation analysis facilitates responsibility transition and triggers oversight mechanisms

on units in which they are required. If labour efficiency variation is treated as undesirable

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

or cost variation procurement of raw materials is unfavourable, managers may retain

these departments' control to enhance performance.

Verification of divergence from standard or expected tends to be the main feature of

study of variations. This deviation will focus the management analysis. The managers

should be given the requisite details such a withdrawal, in general for unfavourable

variation where expense is more than anticipated figures.

Another advantage of the variance will be the limited budget value. In case of

unfavourable variation managers take action to track equally. Where another advantage

of the variance will be the expenditure limited interest. In case of unfavourable variation

managers take action to track equally. Where there are inadequate grounds for doing this

and appropriate mitigation measures are taken, proof of an adverse difference is tested

first.

The potential adjustment of the quantities budgeted is ambiguity or volatility (Quinn and

Hiebl, 2018). If there is no reasonable reason for confusion in relation to an inaccurate

expenditure calculation, the viewpoints for incentive will be revised or revamped.

Further benefits of variances analysis is the assessment of the productivity of the

managers and the management team control system in general. Favourable

value indicates higher effectiveness for mangers, whilst also adverse variance means

underperformance.

The benefit of the volatility is the small amount of spending. In case of adverse variance

administrators take appropriate measures to keep track of the same. In which reasons for

using it are inadequate and reasonable preventative measures are taken, data of an

unfavourable variation is analyzed initially.

Inconsistency or fluctuations is the prospective modification of the amounts budged.

When there is no fair cause for uncertainty about an incorrect estimate of consumption,

the bonus requirements will be updated or changed.

Demerits:

Variance analysis is indeed an operation focused on financial statements released much

further after the end of the accounting year. There could be a time gap that may somehow

affect the capacity-taking corrective action. Additionally, it is not easy to obtain all

6

these departments' control to enhance performance.

Verification of divergence from standard or expected tends to be the main feature of

study of variations. This deviation will focus the management analysis. The managers

should be given the requisite details such a withdrawal, in general for unfavourable

variation where expense is more than anticipated figures.

Another advantage of the variance will be the limited budget value. In case of

unfavourable variation managers take action to track equally. Where another advantage

of the variance will be the expenditure limited interest. In case of unfavourable variation

managers take action to track equally. Where there are inadequate grounds for doing this

and appropriate mitigation measures are taken, proof of an adverse difference is tested

first.

The potential adjustment of the quantities budgeted is ambiguity or volatility (Quinn and

Hiebl, 2018). If there is no reasonable reason for confusion in relation to an inaccurate

expenditure calculation, the viewpoints for incentive will be revised or revamped.

Further benefits of variances analysis is the assessment of the productivity of the

managers and the management team control system in general. Favourable

value indicates higher effectiveness for mangers, whilst also adverse variance means

underperformance.

The benefit of the volatility is the small amount of spending. In case of adverse variance

administrators take appropriate measures to keep track of the same. In which reasons for

using it are inadequate and reasonable preventative measures are taken, data of an

unfavourable variation is analyzed initially.

Inconsistency or fluctuations is the prospective modification of the amounts budged.

When there is no fair cause for uncertainty about an incorrect estimate of consumption,

the bonus requirements will be updated or changed.

Demerits:

Variance analysis is indeed an operation focused on financial statements released much

further after the end of the accounting year. There could be a time gap that may somehow

affect the capacity-taking corrective action. Additionally, it is not easy to obtain all

6

options to variation in financial information which often makes it incredibly difficult to

operate on variances.

If the financial planning has still not been done properly, bearing in mind the detailed

analysis of each factor, the budget preparation process shall be carried out unilaterally

and shall be allowed to separate itself from the actual estimates (Rikhardsson and

Yigitbasioglu, 2018). Afterwards, variance analysis may not be a useful tool.

Some variation factors are not included in financial reporting, so to determine the reasons

of these variances, accounting teams have to research and analyze facts such as labour

allocation, production costs or payroll statistics. The bring-on method is cost-effective

because the administrators were able to successfully solve the issues on the basis of the

information given.

An investigation of the variance appears to have a significant downside in that it requires

far longer determining the impact of the variance which will thus delay the corrective

measures. The tracking process leads to a large time frame contraction which would

greatly hinder the application of protective strategies.

Variance analysis has a major drawback, in that it takes some time to determine the

relationship of variance and, therefore, it suspends effective behavior. The monitoring

method results in a substantial amount of time that will therefore delay the execution of

control measures considerably.

Another performance measure is uncertainty that may be attributed to system instability.

Answer interpretation determines the final outcome, since it differs from the planned

practices.

PART B

1. Report assessing the decision to make famaQ in house in the UK to keep importing it from

Brazil

XLG is a pharmaceutical company based in the UK and in a few parts of Europe. The

market where it conducts activities has a high degree of rivalry and another key benefit of core

chemicals is sourcing from Brazil's famaQ (Samuel, 2018). The shutdown happened in March

2020, which was enforced by the British government. Despite of this, company is preferred to

transfer the money generating mechanism forward remotely so that it can resolve all of the

7

operate on variances.

If the financial planning has still not been done properly, bearing in mind the detailed

analysis of each factor, the budget preparation process shall be carried out unilaterally

and shall be allowed to separate itself from the actual estimates (Rikhardsson and

Yigitbasioglu, 2018). Afterwards, variance analysis may not be a useful tool.

Some variation factors are not included in financial reporting, so to determine the reasons

of these variances, accounting teams have to research and analyze facts such as labour

allocation, production costs or payroll statistics. The bring-on method is cost-effective

because the administrators were able to successfully solve the issues on the basis of the

information given.

An investigation of the variance appears to have a significant downside in that it requires

far longer determining the impact of the variance which will thus delay the corrective

measures. The tracking process leads to a large time frame contraction which would

greatly hinder the application of protective strategies.

Variance analysis has a major drawback, in that it takes some time to determine the

relationship of variance and, therefore, it suspends effective behavior. The monitoring

method results in a substantial amount of time that will therefore delay the execution of

control measures considerably.

Another performance measure is uncertainty that may be attributed to system instability.

Answer interpretation determines the final outcome, since it differs from the planned

practices.

PART B

1. Report assessing the decision to make famaQ in house in the UK to keep importing it from

Brazil

XLG is a pharmaceutical company based in the UK and in a few parts of Europe. The

market where it conducts activities has a high degree of rivalry and another key benefit of core

chemicals is sourcing from Brazil's famaQ (Samuel, 2018). The shutdown happened in March

2020, which was enforced by the British government. Despite of this, company is preferred to

transfer the money generating mechanism forward remotely so that it can resolve all of the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

shutdown problems that arise. This is imported from Brazil as one of the company's key

chemicals used to produce the finished product, in required to be allowed to respond structurally

to business issues.

Ensuring that a organization addresses all the potential risks they might bring should be very

important. Import and export of chemical famaQ via Brazil by XLG would be impossible after

shutdown. Nonetheless, that would lead to several risks if it is to be delivered. There tends to be

a high risk of dissemination of COVID-19, a higher computing time, additional expenditures etc.

If the commodity is not imported so it would be the net profit and the marginal gain given by

famaQ.

As a result, there is also projected to be a 45 percent rise in demand for chemicals X and Y

and it will definitely grow as per market statistics (Uyar, 2019). Those wherein the business also

will concentrate on exporting are now the UK-wide famaQ, so it can satisfy customer demand.

When it is made in the UK, the delivery time will be shortened by 15 days from either previous

date, which means that the company will commence development early.

The production cost per famaQ device in the UK could be 3 pounds that would have been

small in comparison to the output cost of 3.7 pounds per service. It means the company must

manufacture famaQ in the UK instead of sourcing it from Brazil. This would bring substantial

advantages for the market. Numerous of the core advantages include:

This would stimulate the business if famaQ were manufactured as the cost of

production is very low compared to the value of customer.

The shipping time should be shortened by 15 days, which ensures production will begin

earlier and satisfy customer requirements quicker.

Unless the famaQ chemicals are produced rather than transported from Brazil can the

transmission rate of corona virus be minimal.

It would be quite expensive to produce products at Lockdown and the production of

famaQ in the UK may well have been better option for potential activities to be

undertaken by the company.

Considering several other factors, development costs and advantages of producing famaQ in

the United Kingdom, it was decided that XLG will also produce chemicals in United Kingdom

instead of import chemicals from Brazil even though it would be useful for business success

(Wales And et.al., 2020). It is strongly recommended that XLG business produces the chemicals

8

chemicals used to produce the finished product, in required to be allowed to respond structurally

to business issues.

Ensuring that a organization addresses all the potential risks they might bring should be very

important. Import and export of chemical famaQ via Brazil by XLG would be impossible after

shutdown. Nonetheless, that would lead to several risks if it is to be delivered. There tends to be

a high risk of dissemination of COVID-19, a higher computing time, additional expenditures etc.

If the commodity is not imported so it would be the net profit and the marginal gain given by

famaQ.

As a result, there is also projected to be a 45 percent rise in demand for chemicals X and Y

and it will definitely grow as per market statistics (Uyar, 2019). Those wherein the business also

will concentrate on exporting are now the UK-wide famaQ, so it can satisfy customer demand.

When it is made in the UK, the delivery time will be shortened by 15 days from either previous

date, which means that the company will commence development early.

The production cost per famaQ device in the UK could be 3 pounds that would have been

small in comparison to the output cost of 3.7 pounds per service. It means the company must

manufacture famaQ in the UK instead of sourcing it from Brazil. This would bring substantial

advantages for the market. Numerous of the core advantages include:

This would stimulate the business if famaQ were manufactured as the cost of

production is very low compared to the value of customer.

The shipping time should be shortened by 15 days, which ensures production will begin

earlier and satisfy customer requirements quicker.

Unless the famaQ chemicals are produced rather than transported from Brazil can the

transmission rate of corona virus be minimal.

It would be quite expensive to produce products at Lockdown and the production of

famaQ in the UK may well have been better option for potential activities to be

undertaken by the company.

Considering several other factors, development costs and advantages of producing famaQ in

the United Kingdom, it was decided that XLG will also produce chemicals in United Kingdom

instead of import chemicals from Brazil even though it would be useful for business success

(Wales And et.al., 2020). It is strongly recommended that XLG business produces the chemicals

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

rather than importing from Brazil. This would boost shipping prices; reduce total additives

expenses, reducing XLG Company’s profitability. Therefore, importing content from Brazil

would also be very dangerous, as it will contribute to the spread of Corona Virus through one

location to another; this will also produce more problems for UK nation.

CONCLUSION

From the above discussion it has been observed that management accounting techniques are

very essential for the organizations. Financial management plays a crucial role in optimizing the

financial efficiency of transactions. With the assistance of technology, managers may create

strategic strategies to boost the corporate performance or accelerate business development. That's

an instrument being used by various stakeholders to evaluate the organizational status of the

company in terms of financial performance, or total operating efficiencies. It will be very

essential for both firms to be vigilant when seeking to make practical business strategies whether

they have used techniques that are correct. Measurement of the difference based on the real or

expected value of the amount of revenue which is important for making certain decisions.

9

expenses, reducing XLG Company’s profitability. Therefore, importing content from Brazil

would also be very dangerous, as it will contribute to the spread of Corona Virus through one

location to another; this will also produce more problems for UK nation.

CONCLUSION

From the above discussion it has been observed that management accounting techniques are

very essential for the organizations. Financial management plays a crucial role in optimizing the

financial efficiency of transactions. With the assistance of technology, managers may create

strategic strategies to boost the corporate performance or accelerate business development. That's

an instrument being used by various stakeholders to evaluate the organizational status of the

company in terms of financial performance, or total operating efficiencies. It will be very

essential for both firms to be vigilant when seeking to make practical business strategies whether

they have used techniques that are correct. Measurement of the difference based on the real or

expected value of the amount of revenue which is important for making certain decisions.

9

REFERENCES

Books & Journals

Chibili, M., 2019. Basic management accounting for the hospitality industry. Routledge.

Das, S. C., 2019. Management control systems: Principles and practices. PHI Learning Pvt. Ltd..

Erokhin, V. And et.al., 2019. Management accounting change as a sustainable economic

development strategy during pre-recession and recession periods: evidence from

Russia. Sustainability. 11(11). p.3139.

Ismail, K., Isa, C. R. and Mia, L., 2018. Market competition, lean manufacturing practices and

the role of management accounting systems (MAS) information. Jurnal Pengurusan

(UKM Journal of Management), 52.

Pavlatos, O. and Kostakis, H., 2018. Management accounting innovations in a time of economic

crisis. The Journal of Economic Asymmetries. 18. p.e00106.

Quinn, M. and Hiebl, M. R., 2018. Management accounting routines: a framework on their

foundations. Qualitative Research in Accounting & Management.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Samuel, S., 2018. A conceptual framework for teaching management accounting. Journal of

Accounting Education. 44. pp.25-34.

Uyar, M., 2019. The management accounting and the business strategy development at

SMEs. Problems and perspectives in management, (17, Iss. 1), pp.1-10.

Wales, W. And et.al., 2020. Orienting toward sales growth? Decomposing the variance attributed

to three fundamental organizational strategic orientations. Journal of Business

Research. 109. pp.498-510.

10

Books & Journals

Chibili, M., 2019. Basic management accounting for the hospitality industry. Routledge.

Das, S. C., 2019. Management control systems: Principles and practices. PHI Learning Pvt. Ltd..

Erokhin, V. And et.al., 2019. Management accounting change as a sustainable economic

development strategy during pre-recession and recession periods: evidence from

Russia. Sustainability. 11(11). p.3139.

Ismail, K., Isa, C. R. and Mia, L., 2018. Market competition, lean manufacturing practices and

the role of management accounting systems (MAS) information. Jurnal Pengurusan

(UKM Journal of Management), 52.

Pavlatos, O. and Kostakis, H., 2018. Management accounting innovations in a time of economic

crisis. The Journal of Economic Asymmetries. 18. p.e00106.

Quinn, M. and Hiebl, M. R., 2018. Management accounting routines: a framework on their

foundations. Qualitative Research in Accounting & Management.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Samuel, S., 2018. A conceptual framework for teaching management accounting. Journal of

Accounting Education. 44. pp.25-34.

Uyar, M., 2019. The management accounting and the business strategy development at

SMEs. Problems and perspectives in management, (17, Iss. 1), pp.1-10.

Wales, W. And et.al., 2020. Orienting toward sales growth? Decomposing the variance attributed

to three fundamental organizational strategic orientations. Journal of Business

Research. 109. pp.498-510.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.