Management Accounting Report: XLG Company's Performance Analysis

VerifiedAdded on 2023/01/09

|13

|3284

|59

Report

AI Summary

This management accounting report provides a comprehensive analysis of XLG company's financial performance, focusing on variance analysis. The report begins with an introduction to management accounting and its role in decision-making, followed by a detailed examination of sales price variance, sales volume contribution variance, material price planning variance, and material price operational variance. The analysis includes calculations and formulas for each variance, providing insights into the company's performance. Furthermore, the report critically analyzes the merits and demerits of using variances in assessing managers' performance, offering a balanced perspective. Part B explores the decision of whether XLG should manufacture a product at home or import it, considering patent regulations and financial implications. The report concludes with a summary of findings and recommendations, offering valuable insights for financial decision-making.

Management

Accounting - Report

Accounting - Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Part A:..........................................................................................................................................3

Part B:..........................................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Part A:..........................................................................................................................................3

Part B:..........................................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

The financial transactions of a company need to be recorded in an effective manner so that

better decisions can be carried out. In this aspect management accounting (MA) plays a key role

as this is linked to analysing, interpreting financial and non-financial data in a systematic way so

that managers can get needed data at the time of decision making (Chorley, 2019). The project

report is based on a company which is XLG, this company produces different types of cleaning

products and sell all around the United Kingdom. On the basis of provided information about

company, part A and B are covered in report that consists distinct information. In part A,

information about calculation of different variances along with merits and demerits is included.

While part B analysis is done about whether company should apply make product at home or

import from other nation.

MAIN BODY

Part A:

(i) Sales price and volume contribution variance.

Sales Price Variance- This variance can be defined as difference between actual sales of

market price and actual sales at budgeted price. In accordance of given data, calculation of this

variance has been done in such manner:

Formula: (Actual Price-Standard price) x Actual number of units

Chemical X:

Given data:

Actual price= 45 Pounds

Standard price= 35 Pounds

Actual number of sales unit= 850 units

Sales price variance: (45-35) *850

= 8500 (F)

Chemical Y:

Given data:

The financial transactions of a company need to be recorded in an effective manner so that

better decisions can be carried out. In this aspect management accounting (MA) plays a key role

as this is linked to analysing, interpreting financial and non-financial data in a systematic way so

that managers can get needed data at the time of decision making (Chorley, 2019). The project

report is based on a company which is XLG, this company produces different types of cleaning

products and sell all around the United Kingdom. On the basis of provided information about

company, part A and B are covered in report that consists distinct information. In part A,

information about calculation of different variances along with merits and demerits is included.

While part B analysis is done about whether company should apply make product at home or

import from other nation.

MAIN BODY

Part A:

(i) Sales price and volume contribution variance.

Sales Price Variance- This variance can be defined as difference between actual sales of

market price and actual sales at budgeted price. In accordance of given data, calculation of this

variance has been done in such manner:

Formula: (Actual Price-Standard price) x Actual number of units

Chemical X:

Given data:

Actual price= 45 Pounds

Standard price= 35 Pounds

Actual number of sales unit= 850 units

Sales price variance: (45-35) *850

= 8500 (F)

Chemical Y:

Given data:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

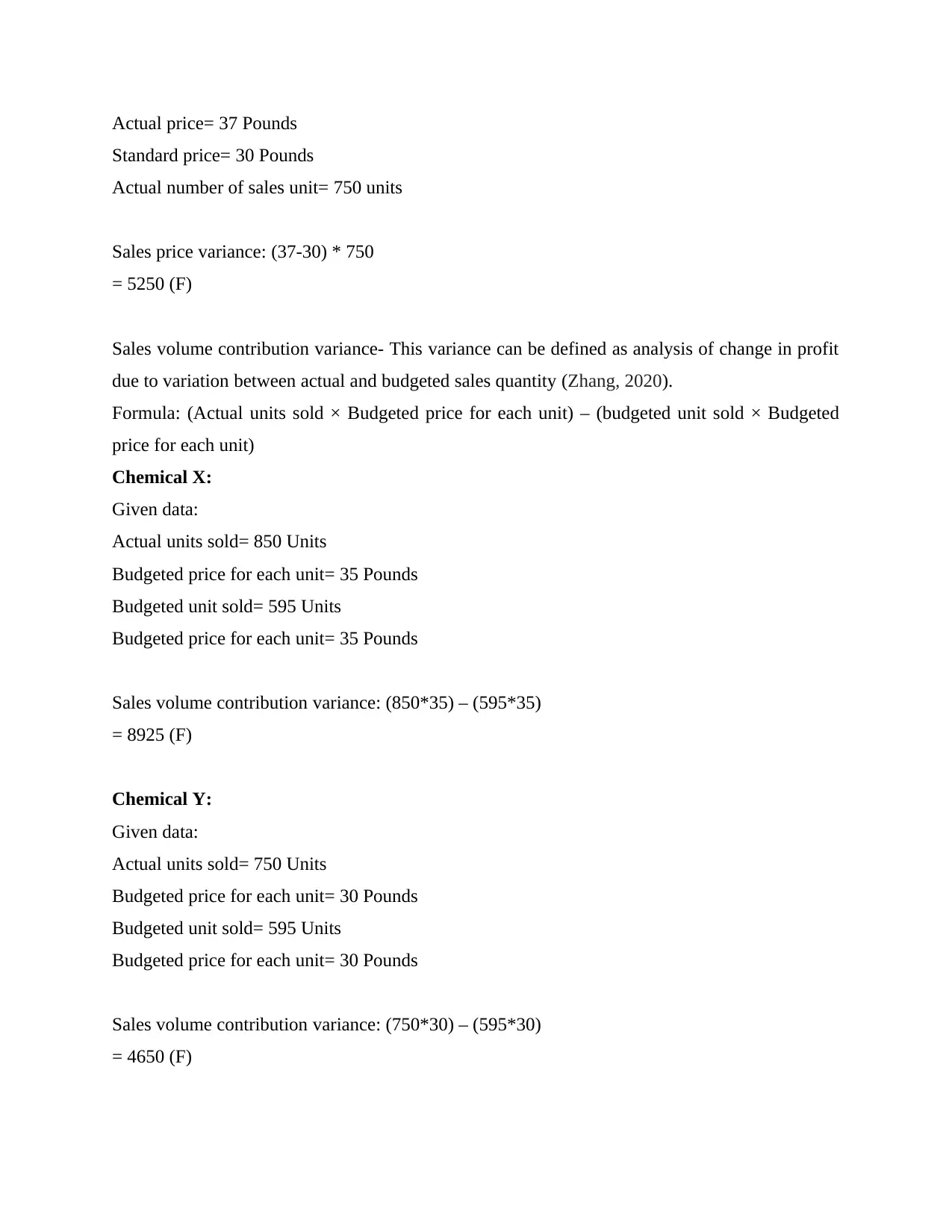

Actual price= 37 Pounds

Standard price= 30 Pounds

Actual number of sales unit= 750 units

Sales price variance: (37-30) * 750

= 5250 (F)

Sales volume contribution variance- This variance can be defined as analysis of change in profit

due to variation between actual and budgeted sales quantity (Zhang, 2020).

Formula: (Actual units sold × Budgeted price for each unit) – (budgeted unit sold × Budgeted

price for each unit)

Chemical X:

Given data:

Actual units sold= 850 Units

Budgeted price for each unit= 35 Pounds

Budgeted unit sold= 595 Units

Budgeted price for each unit= 35 Pounds

Sales volume contribution variance: (850*35) – (595*35)

= 8925 (F)

Chemical Y:

Given data:

Actual units sold= 750 Units

Budgeted price for each unit= 30 Pounds

Budgeted unit sold= 595 Units

Budgeted price for each unit= 30 Pounds

Sales volume contribution variance: (750*30) – (595*30)

= 4650 (F)

Standard price= 30 Pounds

Actual number of sales unit= 750 units

Sales price variance: (37-30) * 750

= 5250 (F)

Sales volume contribution variance- This variance can be defined as analysis of change in profit

due to variation between actual and budgeted sales quantity (Zhang, 2020).

Formula: (Actual units sold × Budgeted price for each unit) – (budgeted unit sold × Budgeted

price for each unit)

Chemical X:

Given data:

Actual units sold= 850 Units

Budgeted price for each unit= 35 Pounds

Budgeted unit sold= 595 Units

Budgeted price for each unit= 35 Pounds

Sales volume contribution variance: (850*35) – (595*35)

= 8925 (F)

Chemical Y:

Given data:

Actual units sold= 750 Units

Budgeted price for each unit= 30 Pounds

Budgeted unit sold= 595 Units

Budgeted price for each unit= 30 Pounds

Sales volume contribution variance: (750*30) – (595*30)

= 4650 (F)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(ii) The material price planning variance and material price operational variance.

Material price planning variance: This is a form of variance which is computed to find out

difference between planned and actual material prices. It is computed by below mentioned

formula that is as follows:

Formula: [(Revised budgeted sales x Standard Margin)- (Actual Sales Quantity X Standard

Margin)]

Chemical X:

Given data-

Revised budgeted sales= 595 units @ 4.5

Standard Margin= 25

Actual Sales Quantity= 850 Units

Standard Margin= 25

Material price planning variance: [(595*4.5*25) -(850*25)]

45687.5

Chemical Y:

Given data-

Revised budgeted sales= 595 units @ 4.5

Standard Margin= 20

Actual Sales Quantity= 750 Units

Standard Margin= 20

Material price planning variance: [(595*4.5*20) -(750*20)]

38550

Material price operation variance: This type of variance is calculated for finding difference in

prices of material, labour etc. This is being calculated by comparing original and revised budgets

and revised budgets with actual outcomes (Salles, Rocha and Gonçalves, 2020). In regards to

given financial data, this variance has been calculated in such manner that is as follows:

Chemical X:

Formula: [(Original budgeted sales x Standard Margin) – (Revised budgeted sales x Standard

Margin)]

Material price planning variance: This is a form of variance which is computed to find out

difference between planned and actual material prices. It is computed by below mentioned

formula that is as follows:

Formula: [(Revised budgeted sales x Standard Margin)- (Actual Sales Quantity X Standard

Margin)]

Chemical X:

Given data-

Revised budgeted sales= 595 units @ 4.5

Standard Margin= 25

Actual Sales Quantity= 850 Units

Standard Margin= 25

Material price planning variance: [(595*4.5*25) -(850*25)]

45687.5

Chemical Y:

Given data-

Revised budgeted sales= 595 units @ 4.5

Standard Margin= 20

Actual Sales Quantity= 750 Units

Standard Margin= 20

Material price planning variance: [(595*4.5*20) -(750*20)]

38550

Material price operation variance: This type of variance is calculated for finding difference in

prices of material, labour etc. This is being calculated by comparing original and revised budgets

and revised budgets with actual outcomes (Salles, Rocha and Gonçalves, 2020). In regards to

given financial data, this variance has been calculated in such manner that is as follows:

Chemical X:

Formula: [(Original budgeted sales x Standard Margin) – (Revised budgeted sales x Standard

Margin)]

Given data:

Original budgeted sales= 595 Units @ 2.5

Standard Margin= 25

Revised budgeted sales= 595 Units @ 4.5

Standard Margin= 25

Material price planning variance= [(595*2.5*25) -(595*4.5*25)]

= -29750

Chemical Y:

Given data:

Original budgeted sales= 595 Units @ 2.5

Standard Margin= 20

Revised budgeted sales= 595 Units @ 4.5

Standard Margin= 20

Material price planning variance= [(595*2.5*20) -(595*4.5*20)]

= -23800

(iii) Given the change in operations, critically analyse the merits and demerits of using variances

in assessing managers’ performance.

Variance analysis is the examination of variations in current activity against predicted or

expected behaviour in financial planning or management accounting (Telesca, Helbig and

Kanevski, 2019). It is primarily dealing with how the disparity between real and expected

activities shows that output of company is being affected.

In other words, variance analysis is the systematic study of the disparity between real and

expected actions. This analysis is used to retain influence over a company. For example, if the

estimation for revenue to be $10,000 and real revenues are $8,000, variance analysis produces a

discrepancy of $2,000. In order to assess performance of managers, the variance analysis play a

key role this is so because this is constant for all whether it is manager or employee. By help of

this tool, director of a company can compare actual data with estimated level of performance. If

outcome is showing negative result, then this will be presented as adverse and if outcome is

showing positive result then this will be presented as favourable. In the case, when performance

Original budgeted sales= 595 Units @ 2.5

Standard Margin= 25

Revised budgeted sales= 595 Units @ 4.5

Standard Margin= 25

Material price planning variance= [(595*2.5*25) -(595*4.5*25)]

= -29750

Chemical Y:

Given data:

Original budgeted sales= 595 Units @ 2.5

Standard Margin= 20

Revised budgeted sales= 595 Units @ 4.5

Standard Margin= 20

Material price planning variance= [(595*2.5*20) -(595*4.5*20)]

= -23800

(iii) Given the change in operations, critically analyse the merits and demerits of using variances

in assessing managers’ performance.

Variance analysis is the examination of variations in current activity against predicted or

expected behaviour in financial planning or management accounting (Telesca, Helbig and

Kanevski, 2019). It is primarily dealing with how the disparity between real and expected

activities shows that output of company is being affected.

In other words, variance analysis is the systematic study of the disparity between real and

expected actions. This analysis is used to retain influence over a company. For example, if the

estimation for revenue to be $10,000 and real revenues are $8,000, variance analysis produces a

discrepancy of $2,000. In order to assess performance of managers, the variance analysis play a

key role this is so because this is constant for all whether it is manager or employee. By help of

this tool, director of a company can compare actual data with estimated level of performance. If

outcome is showing negative result, then this will be presented as adverse and if outcome is

showing positive result then this will be presented as favourable. In the case, when performance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of managers is showing adverse outcome then this can be estimated that manager is not able to

deliver targeted goals. In respect to assess performance of manager, this is important that their

performance need to be assessed at the end of financial year. In between of a financial year, their

performance cannot be evaluated in a better way (Choi, Sun and Chung, 2019).

In the absence of applying this method performance analysis, this can become difficult for

companies to measure actual level of performance. Such as in regards to above mentioned

company, they can apply variance analysis method in order to find out value of actual

performance. Apart from the assessment of performance of managers, this is also useful for

analysing performance of employees and activities too. It is so because on the basis of this, a

manager of company can track variance between actual cost and estimated cost. As well as

individual level of performance of each employee is also computed by help of this tool. Herein,

below some key merits and demerits of using this technique for assessing managers’

performance is mentioned in such manner that is as follows:

Merits-

Variance analysis encourages effective budgeting operation because management aims to

see smaller variations from the expected budgets. Wanting a smaller variance typically

allows administrators to make comprehensive, forward-looking financial choices. In

other words, by help of this managers can focus on those activities whose variance is

favourable. Due to this it becomes viable for an organization to consider beneficial

activities instead of unfavourable activities.

Variance analysis serves as a control method. Assessment of deviations on basic

essentials assists the business in understanding the problem, and it help managers look

into potential ways of how much difference can be prevented (Vaske, 2019). It results as

better performance of a company because managers become able to know that on which

activities or operations adverse variance is acceptable on which this is not viable. As a

consequence, management of a company prepares effective and viable strategies which

may lead to better performance in each condition.

Variance analysis encourages determining liability and activates management systems on

organizations when it is necessary. For example, if labour performance variance is

considered to be unfavourable or production over raw material cost variance is

unfavourable, the management should improve regulation over certain divisions to

deliver targeted goals. In respect to assess performance of manager, this is important that their

performance need to be assessed at the end of financial year. In between of a financial year, their

performance cannot be evaluated in a better way (Choi, Sun and Chung, 2019).

In the absence of applying this method performance analysis, this can become difficult for

companies to measure actual level of performance. Such as in regards to above mentioned

company, they can apply variance analysis method in order to find out value of actual

performance. Apart from the assessment of performance of managers, this is also useful for

analysing performance of employees and activities too. It is so because on the basis of this, a

manager of company can track variance between actual cost and estimated cost. As well as

individual level of performance of each employee is also computed by help of this tool. Herein,

below some key merits and demerits of using this technique for assessing managers’

performance is mentioned in such manner that is as follows:

Merits-

Variance analysis encourages effective budgeting operation because management aims to

see smaller variations from the expected budgets. Wanting a smaller variance typically

allows administrators to make comprehensive, forward-looking financial choices. In

other words, by help of this managers can focus on those activities whose variance is

favourable. Due to this it becomes viable for an organization to consider beneficial

activities instead of unfavourable activities.

Variance analysis serves as a control method. Assessment of deviations on basic

essentials assists the business in understanding the problem, and it help managers look

into potential ways of how much difference can be prevented (Vaske, 2019). It results as

better performance of a company because managers become able to know that on which

activities or operations adverse variance is acceptable on which this is not viable. As a

consequence, management of a company prepares effective and viable strategies which

may lead to better performance in each condition.

Variance analysis encourages determining liability and activates management systems on

organizations when it is necessary. For example, if labour performance variance is

considered to be unfavourable or production over raw material cost variance is

unfavourable, the management should improve regulation over certain divisions to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maximize output. In other words, it gives an overview about what kinds of policies are

need to be carried out in order to enhance performance of various kinds of activities and

operations for a particular time period.

Demerits:

Variance analysis as an operation is focused on financial statements, which are published

far longer after period closing; there will be a time delay and can impact the corrective

measures taking the opportunity to a certain degree (Lei, Liu and Zhang, 2019). Also, not

all causes of variation can be included in accounting records, which renders acting upon

variances challenging.

In addition to this, the another drawback of variance analysis is that it cannot be applied

on non-financial aspects. This can be applied only in the case of financial data analysis

such as making comparison of standard and actual data related to cost, income etc.

Another issue of variance analysis method is that managers can manipulate the data

which are used in this approach. If presented financial data are wrong, then this may

become difficult for companies to find out correct variance of different kinds of activities

and operations. Due to this issue, the actual evaluation of performance of managers can

be wrong and organization will not be able to make effective policies to gain higher

profitability.

So these some key benefits and drawbacks of using above mentioned technique of variance

analysis. This is essential for companies that how well they are applying it for assessing

performance of their managers and employees. The efficiency and accuracy of produced

outcome under this method highly depends on provided financial data for comparison. If

provided data are correct then variances will also be right (Ferdous, Adams and Boyce, 2019). In

addition, this method cannot be applied for managers because they have right to manipulate

actual data and due to which actual evaluation of their performance cannot be done.

Part B:

As in the above part, this has been explained that if XLG company imports the fama Q product

from Brazil then their cost of acquiring this product is increasing. Before lockdown the price of

this product was around 2.50 pounds for each unit but after lockdown price raised and it became

need to be carried out in order to enhance performance of various kinds of activities and

operations for a particular time period.

Demerits:

Variance analysis as an operation is focused on financial statements, which are published

far longer after period closing; there will be a time delay and can impact the corrective

measures taking the opportunity to a certain degree (Lei, Liu and Zhang, 2019). Also, not

all causes of variation can be included in accounting records, which renders acting upon

variances challenging.

In addition to this, the another drawback of variance analysis is that it cannot be applied

on non-financial aspects. This can be applied only in the case of financial data analysis

such as making comparison of standard and actual data related to cost, income etc.

Another issue of variance analysis method is that managers can manipulate the data

which are used in this approach. If presented financial data are wrong, then this may

become difficult for companies to find out correct variance of different kinds of activities

and operations. Due to this issue, the actual evaluation of performance of managers can

be wrong and organization will not be able to make effective policies to gain higher

profitability.

So these some key benefits and drawbacks of using above mentioned technique of variance

analysis. This is essential for companies that how well they are applying it for assessing

performance of their managers and employees. The efficiency and accuracy of produced

outcome under this method highly depends on provided financial data for comparison. If

provided data are correct then variances will also be right (Ferdous, Adams and Boyce, 2019). In

addition, this method cannot be applied for managers because they have right to manipulate

actual data and due to which actual evaluation of their performance cannot be done.

Part B:

As in the above part, this has been explained that if XLG company imports the fama Q product

from Brazil then their cost of acquiring this product is increasing. Before lockdown the price of

this product was around 2.50 pounds for each unit but after lockdown price raised and it became

of 3.70 pounds per unit for XLG. Due to this company increase their mark-up price till 4.50

pounds for each unit of fama Q. Along with, this company has patent of this product which

indicates that only they have right to sell this in all around the United Kingdom. In this critical

condition, above company has two alternatives which is to produce this product at home or

import product from Brazil which they were doing earlier. In both alternatives, there are some

issues now company has to choose only one which is suitable and less costly. In the below part,

analysis of both alternatives is done in such manner:

Alternative one:

The option one is related to making production of fama Q in United Kingdom till cost of

import reduces in Brazil. The main issue under this alternative is that it will be against rules and

regulation of patent. As per the law, this is essential for an entity who has patent on a product to

import or make production under certain guidelines. For XLG plc, this can become difficult to do

production as per the rulebook of patent. This is so because they do not have enough knowledge

about manufacturing of Fama Q because they were importing it from Brazil so there is a risk that

whether company will produce this product effectively or not. From the perspective of finance, a

detailed analysis of this option of producing Fama Q has been done below in such manner that is

as follows:

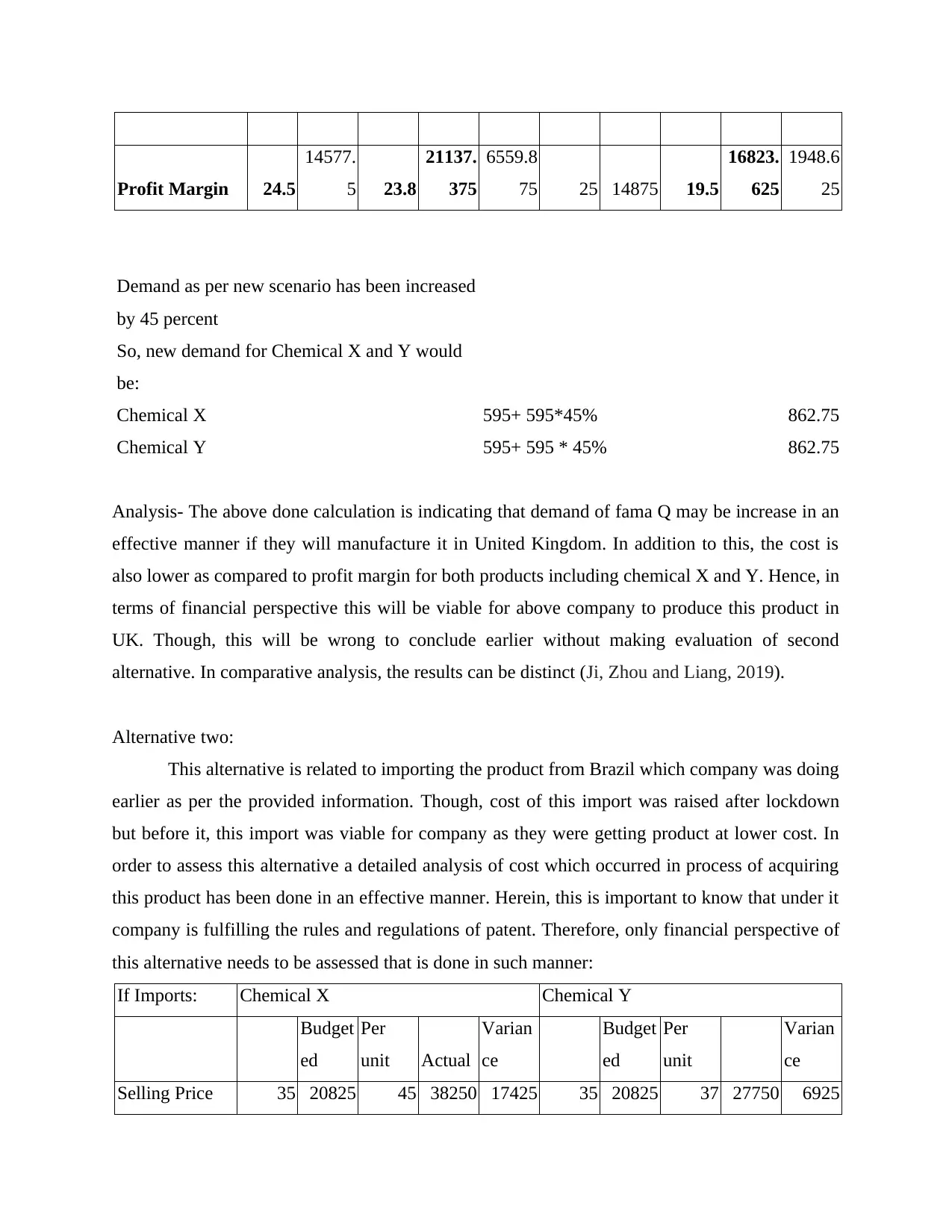

If making fama Q

Chemical X Chemical Y

Per

unit

Budget

ed

Per

unit

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in cost

due to import of

Fama Q 0.5 1.2

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

pounds for each unit of fama Q. Along with, this company has patent of this product which

indicates that only they have right to sell this in all around the United Kingdom. In this critical

condition, above company has two alternatives which is to produce this product at home or

import product from Brazil which they were doing earlier. In both alternatives, there are some

issues now company has to choose only one which is suitable and less costly. In the below part,

analysis of both alternatives is done in such manner:

Alternative one:

The option one is related to making production of fama Q in United Kingdom till cost of

import reduces in Brazil. The main issue under this alternative is that it will be against rules and

regulation of patent. As per the law, this is essential for an entity who has patent on a product to

import or make production under certain guidelines. For XLG plc, this can become difficult to do

production as per the rulebook of patent. This is so because they do not have enough knowledge

about manufacturing of Fama Q because they were importing it from Brazil so there is a risk that

whether company will produce this product effectively or not. From the perspective of finance, a

detailed analysis of this option of producing Fama Q has been done below in such manner that is

as follows:

If making fama Q

Chemical X Chemical Y

Per

unit

Budget

ed

Per

unit

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in cost

due to import of

Fama Q 0.5 1.2

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit Margin 24.5

14577.

5 23.8

21137.

375

6559.8

75 25 14875 19.5

16823.

625

1948.6

25

Demand as per new scenario has been increased

by 45 percent

So, new demand for Chemical X and Y would

be:

Chemical X 595+ 595*45% 862.75

Chemical Y 595+ 595 * 45% 862.75

Analysis- The above done calculation is indicating that demand of fama Q may be increase in an

effective manner if they will manufacture it in United Kingdom. In addition to this, the cost is

also lower as compared to profit margin for both products including chemical X and Y. Hence, in

terms of financial perspective this will be viable for above company to produce this product in

UK. Though, this will be wrong to conclude earlier without making evaluation of second

alternative. In comparative analysis, the results can be distinct (Ji, Zhou and Liang, 2019).

Alternative two:

This alternative is related to importing the product from Brazil which company was doing

earlier as per the provided information. Though, cost of this import was raised after lockdown

but before it, this import was viable for company as they were getting product at lower cost. In

order to assess this alternative a detailed analysis of cost which occurred in process of acquiring

this product has been done in an effective manner. Herein, this is important to know that under it

company is fulfilling the rules and regulations of patent. Therefore, only financial perspective of

this alternative needs to be assessed that is done in such manner:

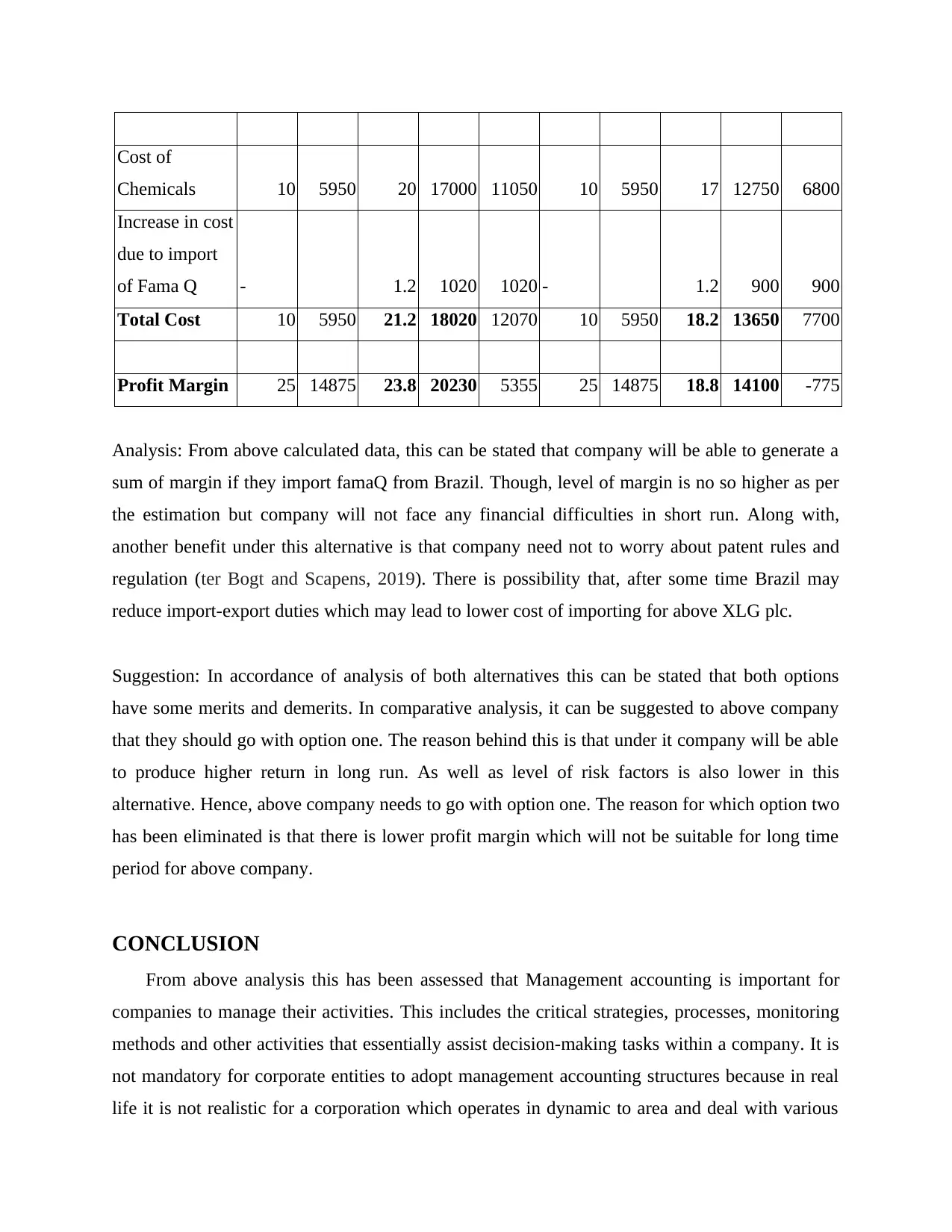

If Imports: Chemical X Chemical Y

Budget

ed

Per

unit Actual

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

14577.

5 23.8

21137.

375

6559.8

75 25 14875 19.5

16823.

625

1948.6

25

Demand as per new scenario has been increased

by 45 percent

So, new demand for Chemical X and Y would

be:

Chemical X 595+ 595*45% 862.75

Chemical Y 595+ 595 * 45% 862.75

Analysis- The above done calculation is indicating that demand of fama Q may be increase in an

effective manner if they will manufacture it in United Kingdom. In addition to this, the cost is

also lower as compared to profit margin for both products including chemical X and Y. Hence, in

terms of financial perspective this will be viable for above company to produce this product in

UK. Though, this will be wrong to conclude earlier without making evaluation of second

alternative. In comparative analysis, the results can be distinct (Ji, Zhou and Liang, 2019).

Alternative two:

This alternative is related to importing the product from Brazil which company was doing

earlier as per the provided information. Though, cost of this import was raised after lockdown

but before it, this import was viable for company as they were getting product at lower cost. In

order to assess this alternative a detailed analysis of cost which occurred in process of acquiring

this product has been done in an effective manner. Herein, this is important to know that under it

company is fulfilling the rules and regulations of patent. Therefore, only financial perspective of

this alternative needs to be assessed that is done in such manner:

If Imports: Chemical X Chemical Y

Budget

ed

Per

unit Actual

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Increase in cost

due to import

of Fama Q - 1.2 1020 1020 - 1.2 900 900

Total Cost 10 5950 21.2 18020 12070 10 5950 18.2 13650 7700

Profit Margin 25 14875 23.8 20230 5355 25 14875 18.8 14100 -775

Analysis: From above calculated data, this can be stated that company will be able to generate a

sum of margin if they import famaQ from Brazil. Though, level of margin is no so higher as per

the estimation but company will not face any financial difficulties in short run. Along with,

another benefit under this alternative is that company need not to worry about patent rules and

regulation (ter Bogt and Scapens, 2019). There is possibility that, after some time Brazil may

reduce import-export duties which may lead to lower cost of importing for above XLG plc.

Suggestion: In accordance of analysis of both alternatives this can be stated that both options

have some merits and demerits. In comparative analysis, it can be suggested to above company

that they should go with option one. The reason behind this is that under it company will be able

to produce higher return in long run. As well as level of risk factors is also lower in this

alternative. Hence, above company needs to go with option one. The reason for which option two

has been eliminated is that there is lower profit margin which will not be suitable for long time

period for above company.

CONCLUSION

From above analysis this has been assessed that Management accounting is important for

companies to manage their activities. This includes the critical strategies, processes, monitoring

methods and other activities that essentially assist decision-making tasks within a company. It is

not mandatory for corporate entities to adopt management accounting structures because in real

life it is not realistic for a corporation which operates in dynamic to area and deal with various

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Increase in cost

due to import

of Fama Q - 1.2 1020 1020 - 1.2 900 900

Total Cost 10 5950 21.2 18020 12070 10 5950 18.2 13650 7700

Profit Margin 25 14875 23.8 20230 5355 25 14875 18.8 14100 -775

Analysis: From above calculated data, this can be stated that company will be able to generate a

sum of margin if they import famaQ from Brazil. Though, level of margin is no so higher as per

the estimation but company will not face any financial difficulties in short run. Along with,

another benefit under this alternative is that company need not to worry about patent rules and

regulation (ter Bogt and Scapens, 2019). There is possibility that, after some time Brazil may

reduce import-export duties which may lead to lower cost of importing for above XLG plc.

Suggestion: In accordance of analysis of both alternatives this can be stated that both options

have some merits and demerits. In comparative analysis, it can be suggested to above company

that they should go with option one. The reason behind this is that under it company will be able

to produce higher return in long run. As well as level of risk factors is also lower in this

alternative. Hence, above company needs to go with option one. The reason for which option two

has been eliminated is that there is lower profit margin which will not be suitable for long time

period for above company.

CONCLUSION

From above analysis this has been assessed that Management accounting is important for

companies to manage their activities. This includes the critical strategies, processes, monitoring

methods and other activities that essentially assist decision-making tasks within a company. It is

not mandatory for corporate entities to adopt management accounting structures because in real

life it is not realistic for a corporation which operates in dynamic to area and deal with various

issues. Furthermore, it recommends many strategies that not only help key decisions of

developing employees but also provide an assistive system for creation of policies.

developing employees but also provide an assistive system for creation of policies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.